Gluten Intolerance Treatment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

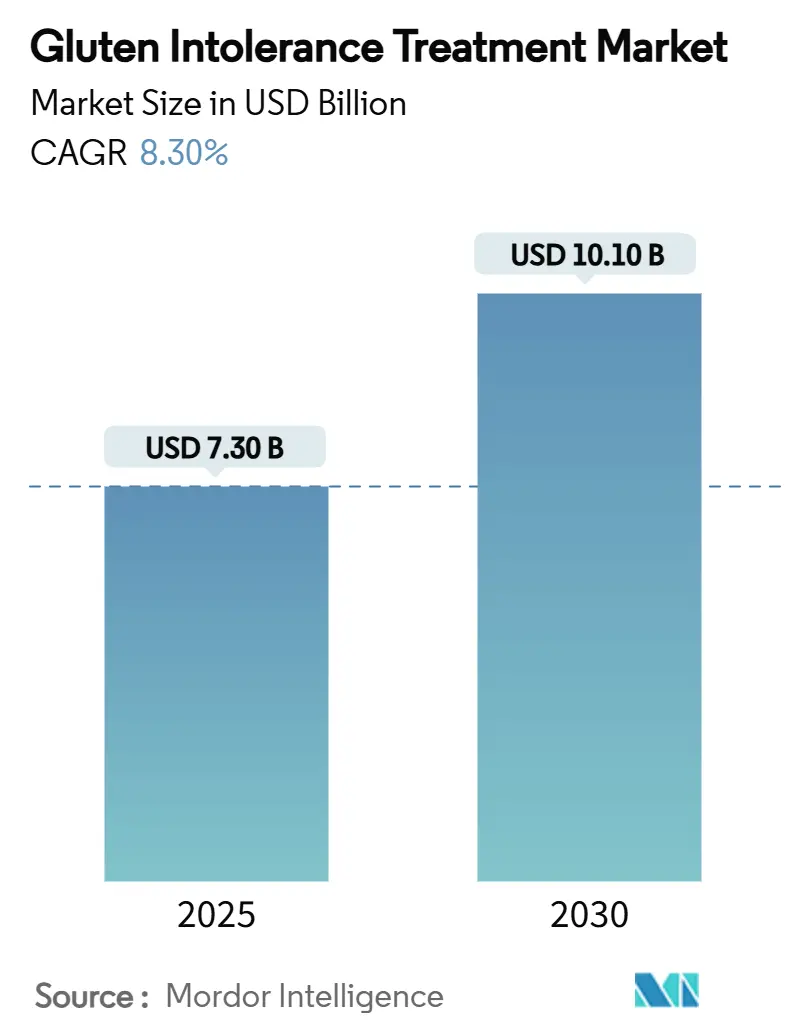

| Market Size (2025) | USD 7.30 Billion |

| Market Size (2030) | USD 10.10 Billion |

| Growth Rate (2025 - 2030) | 8.30% CAGR |

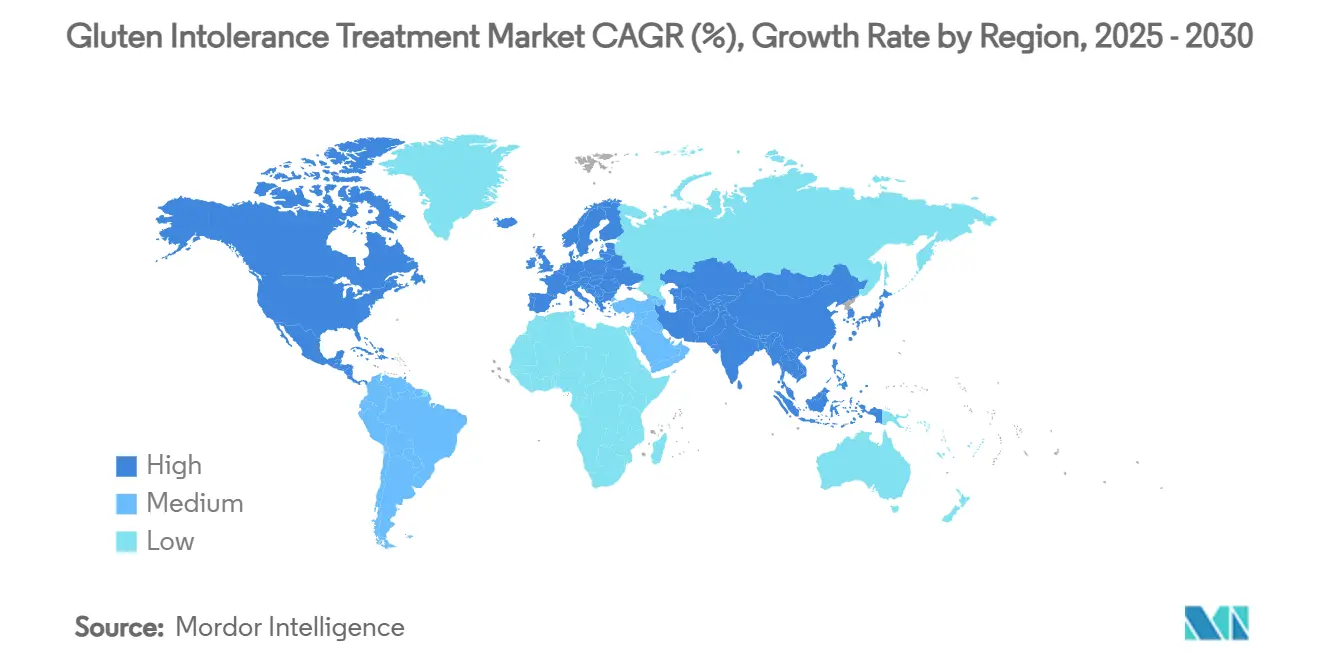

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gluten Intolerance Treatment Market Analysis by Mordor Intelligence

The gluten intolerance treatment market size stood at USD 7.3 billion in 2025 and is forecast to reach USD 10.1 billion by 2030, advancing at an 8.3% CAGR over the period. The expansion reflects widening diagnostic reach, rapid therapeutic innovation, and supportive orphan-drug policies that collectively elevate pharmaceutical intervention beyond dietary management. Improved case-finding tools—such as HLA-DQ–gluten tetramer assays—are uncovering large pools of previously unrecognized patients, while fast-track designations for novel enzyme and biologic assets have compressed development timelines. Multinational manufacturers are pairing prescription launches with digital adherence programs that capture real-world evidence, and venture-backed start-ups are crowding early pipelines with gut-health platforms that could feed future licensing deals. Together, these forces underpin sustained demand momentum, growing competitive rivalry, and rising capital flows into the gluten intolerance treatment market.

Key Report Takeaways

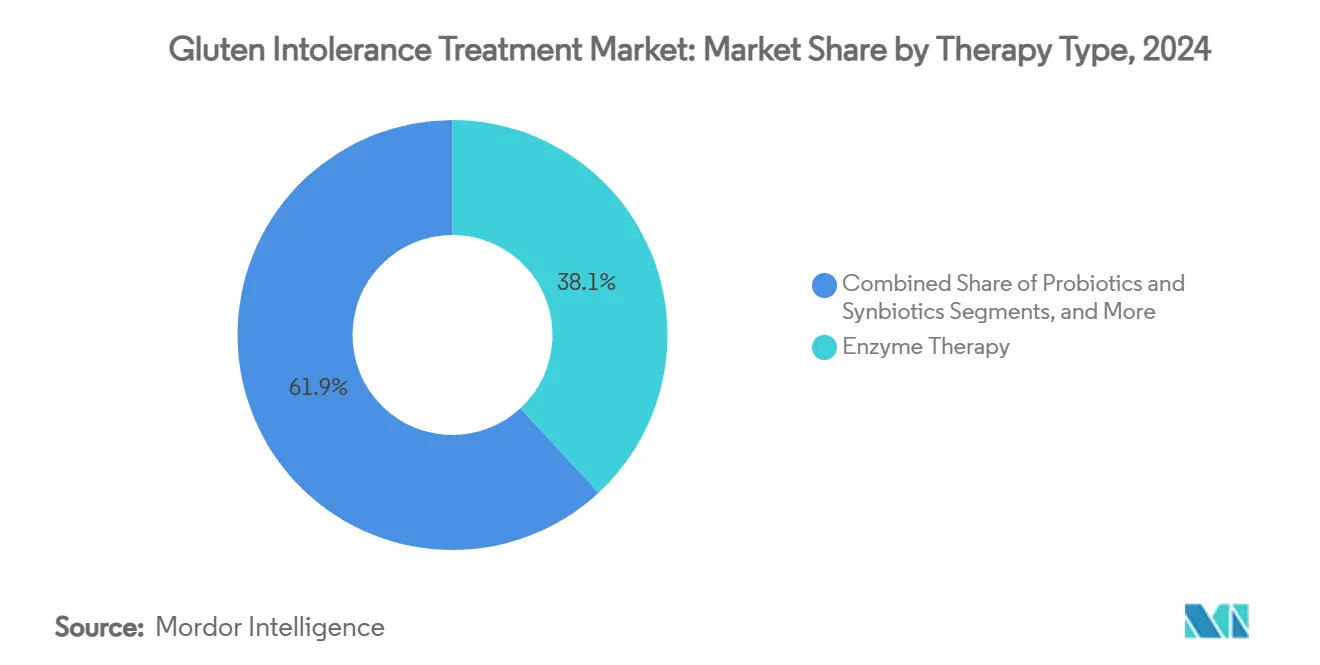

- By therapy type, Enzyme therapy held 38.1% revenue share of the gluten intolerance treatment market in 2024, while biologic therapy is set to grow at 13.8% CAGR through 2030.

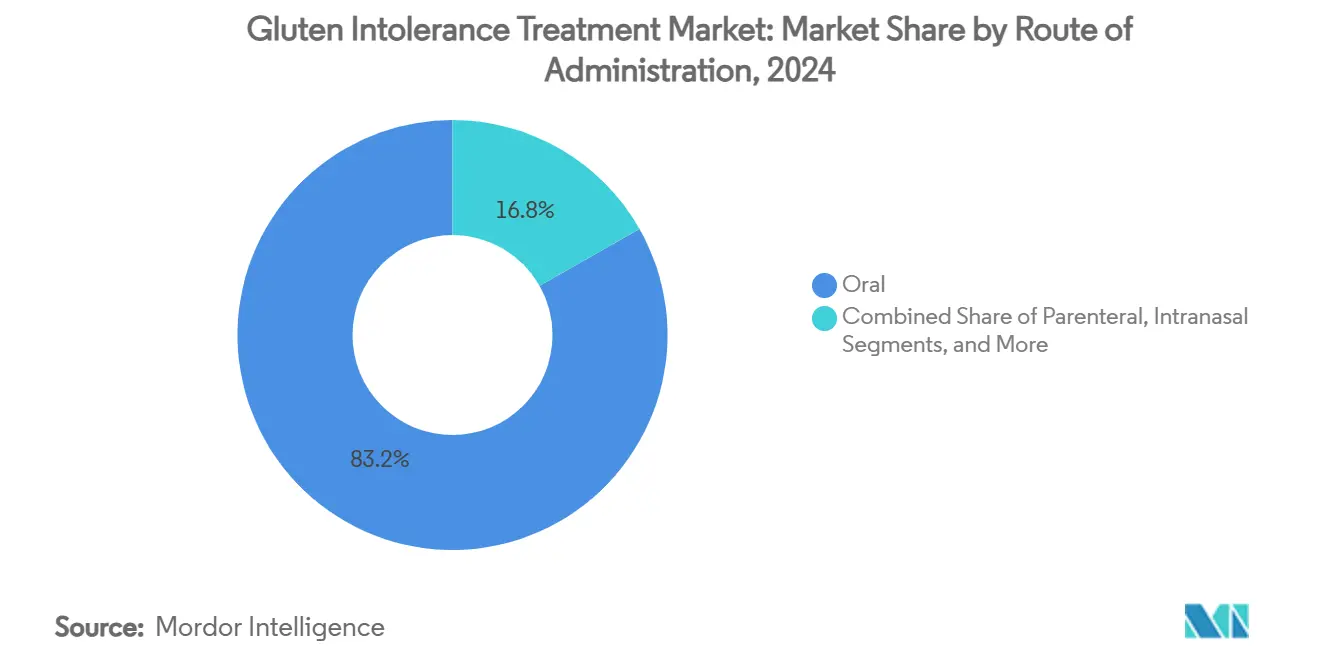

- By route of administration, the oral route of administration captured 83.2% of the gluten intolerance treatment market share in 2024, whereas parenteral delivery is advancing at a 9.4% CAGR due to monoclonal antibody uptake.

- Geographically, North America led the gluten intolerance treatment market with 3.3 million diagnosed patients in 2024; Asia-Pacific is projected to register the highest regional CAGR over the forecast window.

Global Gluten Intolerance Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ )% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising diagnosed celiac disease prevalence | +2.10% | North America & Europe; accelerating in APAC | Medium term (2-4 years) |

| Increasing R&D funding for enzyme & biologic therapies | +1.80% | North America & EU core; expansion in APAC | Long term (≥ 4 years) |

| Consumer shift toward gluten-free nutraceuticals | +1.40% | Global, led by high-income economies | Short term (≤ 2 years) |

| Regulatory incentives for orphan drugs | +1.20% | North America & EU | Long term (≥ 4 years) |

| Venture-capital inflow into gut-health start-ups | +0.90% | North America, Europe, early Asia | Medium term (2-4 years) |

| Digital gut-monitoring apps steering prescriptions | +0.70% | North America & Europe, urban APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Diagnosed Celiac Disease Prevalence

Diagnostic practices are shifting from symptom-based suspicion to systematic antibody and genetic screening, revealing that 1% of the world’s population harbors the autoimmune condition. Advanced assays capable of detecting disease activity even in adherent gluten-free dieters are moving from specialty centers into routine laboratories, compressing the historic 4-year diagnostic lag to fewer than 18 months. Expanding insurance coverage for serology panels in the United States and Europe is accelerating test volumes, while professional-society campaigns in India, China, and South Korea are prompting primary-care physicians to include celiac panels when evaluating unexplained anemia or growth failure. This escalating case-finding pipeline enlarges the treated population base and anchors long-run revenue visibility for the gluten intolerance treatment market.[1]Celiac Disease Foundation, “Undiagnosed Celiac Disease Remains a Significant Public-Health Issue,” celiac.org

Increasing R&D Funding for Enzyme & Biologic Therapies

Global pharmaceutical and venture investors poured record capital into celiac pipelines across 2024-2025, encouraged by clearer regulatory guidance on adjunctive drug pathways and by early-phase readouts that validate multiple mechanisms. Takeda’s USD 330 million full buy-out of PvP Biologics for an orally active glutenase typifies the premium placed on enzyme assets, while anti-IL-15 antibodies from Teva and Sanofi have secured successive fast-track milestones that shorten review clocks. National Institutes of Health co-funding for immunomodulatory trials lowers scientific risk, and public-private partnerships in the European Union extend non-dilutive grants to mid-stage programs. These financial catalysts accelerate candidate progression, diversify modality options, and reinforce investor confidence in the gluten intolerance treatment market.

Consumer Shift Toward Gluten-Free Nutraceuticals

A decade of double-digit expansion in gluten-free packaged foods has familiarized consumers with celiac pathophysiology and normalized the concept of disease-specific dietary solutions. App-based nutrition platforms now link barcode scanning with symptom diaries, producing high-resolution exposure datasets that document unintentional gluten ingestion rates hovering near 73% despite vigilant diet adherence. Such evidence has reframed gluten tolerance as a medical rather than lifestyle issue, creating fertile demand for pharmacologic safeguards that complement diet. Pharmaceutical marketers leverage these digital ecosystems to educate prospective patients, embed adherence reminders, and funnel real-world outcome metrics into post-launch surveillance, thereby closing the loop between consumer wellness trends and prescription uptake in the gluten intolerance treatment market.

Regulatory Incentives for Orphan Drugs

Celiac disease qualified for orphan designation in both the United States and European Union in 2024, conferring seven-year exclusivity, user-fee waivers, and tax credits that materially improve risk-adjusted project net present value. The U.S. FDA’s disease-specific draft guidance further clarified acceptable endpoints—histologic mucosal healing coupled with symptom scales—reducing protocol ambiguity and facilitating accelerated approval pathways. European regulators echoed this stance through PRIME advisory support, enabling rolling data submissions. The alignment of regulatory carrots across major markets lowers the barrier to entry for mid-cap innovators. It encourages big pharma re-engagement, thereby cementing a pro-development policy backdrop for the gluten intolerance treatment market.[2]Food and Drug Administration, “Celiac Disease: Developing Drugs for Adjunctive Treatment,” FDA, fda.gov

Restraints Impact Analysis*

| Restraint | ( ~ )% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High attrition rates in late-stage trials | –1.9% | Global, particularly North America & EU programs | Medium term (2-4 years) |

| Limited physician awareness outside NA & EU | –1.3% | Asia-Pacific, Latin America, Middle East & Africa | Long term (≥ 4 years) |

| Price sensitivity in emerging markets | –0.8% | Asia-Pacific, Latin America, Middle East & Africa | Medium term (2-4 years) |

| Cross-contamination risk undermining drug efficacy | –0.6% | Regions with weaker manufacturing oversight | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Attrition Rates in Late-Stage Clinical Trials

Multiple Phase 3 setbacks—most prominently larazotide acetate’s failure to achieve co-primary endpoints—underscore the difficulty of translating mid-stage symptom improvement into histologic remission. Heterogeneous patient adherence to controlled gluten challenges, regional variations in baseline inflammation, and the need for invasive biopsy verification increase statistical noise and elevate development costs. Sponsors now deploy adaptive enrichment designs and digital pill-tracking to sharpen signal detection, yet attrition risk remains the chief drag on investor sentiment. Despite these hurdles, pipeline—wide mechanistic diversity reduces correlation of failure across assets, preserving the long-term growth story for the gluten intolerance treatment market.

Limited Physician Awareness Outside North America & EU

Underdiagnosis in emerging economies stems from low clinical suspicion, limited access to gastroenterology services, and scarce reimbursement for antibody panels. Surveys in Brazil, Turkey, and mainland China reveal that fewer than 35% of pediatricians routinely test for celiac markers when confronted with nonspecific growth faltering. International medical societies are deploying multilingual algorithms and tele-mentoring programs, yet uptake is gradual. Until provider competence rises, potential prescription volumes remain capped in high-population countries, tempering upside for the gluten intolerance treatment market.[3]National Library of Medicine, “Knowledge of Celiac Disease Among Physicians in Turkey,” pubmed.ncbi.nlm.nih.gov

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapy Type: Enzyme Leadership Meets Biologic Momentum

Enzyme formulations commanded the highest share of the gluten intolerance treatment market at 38.1% in 2024, benefiting from straightforward oral delivery and an intuitive mechanism of degrading immunogenic peptides before immune activation. The segment comprises broad-spectrum proteases co-formulated with acid-stable peptidases, promising rapid symptom relief during inadvertent dietary lapses. Investment in enteric-coated capsules and delayed-release micro-granules now targets activity in the proximal small intestine, the primary absorptive zone for gluten fragments. Commercial opportunity is amplified by consumer familiarity with over-the-counter digestive aids, easing physician-patient discussions and accelerating early adoption. However, sustained market leadership is not guaranteed. Biologic therapies, buoyed by a 13.8% CAGR, are closing the gap through pipeline depth and mechanism diversity. Anti-IL-15 monoclonal antibodies deliver systemic immunomodulation capable of addressing both acute mucosal injury and chronic inflammatory sequelae. They additionally offer therapeutic appeal for serology-positive patients who remain symptomatic despite strict diets, a cohort estimated at 10-15% of the diagnosed population. Several biologics now carry fast-track or orphan designations that shorten regulatory review and may trigger a tipping point for prescriber preference once pivotal data mature..

Biologics also attract cross-specialty familiarity among gastroenterologists accustomed to administering anti-TNF and JAK inhibitors for inflammatory bowel disease, fostering readiness to adopt injectable regimens. Nonetheless, enzyme developers counter by exploring adjunctive use with biologics, positioning enzymes as front-line guards that reduce dietary gluten load while biologics tackle residual immune activity. This potential combination sets the stage for a complementary rather than zero-sum competitive narrative inside the gluten intolerance treatment market. Venture funds are additionally underwriting next-generation synbiotic cocktails that pair enzymes with microbiome modulators, aiming to lengthen mucosal remission intervals. Investors view the enzyme category’s immediate revenue visibility as a bridge to the longer-term biologic opportunity, sustaining parallel capital flows into both modalities.

By Route of Administration: Oral Platform Dominates as Injectables Scale

The oral route captured 83.2% gluten intolerance treatment market share in 2024, fueled by patient convenience, low administration cost, and direct intestinal exposure that maximizes enzyme efficiency. Advances in polymer science now allow pH-responsive coatings that open precisely at the jejunal pH transition, preserving enzyme activity during gastric transit. Sublingual immunotherapy tablets testing tolerogenic gluten peptides are proceeding through early trials and could further broaden the oral portfolio.

Against this backdrop, parenteral products, including subcutaneous antibodies and lipid-nanoparticle tolerance inducers, are widening acceptance: unit sales are projected to climb at 9.4% CAGR to 2030. Device innovation mitigates injection burden; prefilled pens with hidden needles mirror insulin-pen ergonomics and support home administration. Intranasal nanoparticles remain pre-clinical but entice investors by offering mucosal immunity re-programming without first-pass degradation. Diversification across oral and injectable modalities positions the gluten intolerance treatment market to address heterogeneous patient preferences and disease phenotypes.

Geography Analysis

North America generated the highest revenue in 2024, benefiting from 3.3 million diagnosed patients, broad insurance coverage for antibody panels, and accelerated approval programs that encourage early commercial launches. The United States alone contributed more than half of regional turnover, reinforced by direct-to-consumer disease-awareness campaigns and active patient-advocacy lobbying for gluten labeling mandates. Canada, featuring universal healthcare reimbursement for serological screening, drives high testing penetration and exhibits prescription fill rates comparable with leading U.S. states. Europe ranks second in absolute value, underpinned by coordinated Horizon research consortia that subsidize multicenter trials and by parliamentary motions that endorse pharmacy-level gluten testing kits. Germany, France, and the United Kingdom form the triad of high-spend countries, each hosting government-funded celiac registries that streamline patient recruitment into pivotal studies. Collective purchasing frameworks through national health services may, however, pressure launch prices, influencing profit pools inside the gluten intolerance treatment market.

Asia-Pacific represents the fastest-growing arena, spurred by urban dietary westernization and emerging epidemiologic recognition that local prevalence mirrors Western baselines. China’s school-age screening initiatives revealed celiac autoimmunity in 2.19% of adolescents, galvanizing provincial governments to invest in laboratory infrastructure and gastroenterology fellowships. India’s responsive private-health sector is opening specialty celiac clinics across Tier-1 cities, and South Korea’s adoption of real-time PCR HLA typing within national screening pilots promises early detection scaling. Australia, with mature diagnostic networks, functions as the region’s bellwether for novel therapy adoption, a status accentuated by its strong patient-advocacy ecosystem. Nevertheless, wide inter-country disparities in physician education and insurance reimbursement continue to temper near-term uptake, moderating overall contribution to the gluten intolerance treatment market size until sustained awareness campaigns take hold.

Latin America, the Middle East, and Africa collectively deliver smaller revenue slices at present, constrained by fragmented healthcare financing and modest diagnostic throughput. Brazil and Argentina spearhead Latin American growth but confront knowledge gaps that limit referral volumes; targeted continuous-medical-education webinars are starting to close these deficits. In the Gulf Cooperation Council, high household purchasing power offsets smaller patient bases, enabling premium biologic uptake through private clinics. South Africa represents Africa’s chief opportunity due to its specialist gastroenterology clusters, albeit hindered by unequal rural-urban access. Over the forecast horizon, multilateral partnerships—combining non-profit awareness grants with industry-funded diagnostic subsidies—should progressively unlock these latent markets, widening geographic dispersion of the gluten intolerance treatment market.

Competitive Landscape

The gluten intolerance treatment market retains a fragmented structure with no incumbent holding more than 10% global revenue, leaving significant whitespace for first-to-approval contenders. Takeda exemplifies the diversified strategy, advancing TAK-101 nanoparticles, TAK-062 enzymes, and TAK-227 tissue-TG inhibitors in tandem while leveraging digital-therapeutic alliances for adherence monitoring. Johnson & Johnson’s Janssen unit has licensed an early anti-IL-21 candidate, bolstering its autoimmune franchise with potential celiac crossover. Sanofi pushes amlitelimab, an anti-OX40L biologic, in parallel with companion diagnostic co-development to pre-select non-responsive celiac cohorts. Among pure-play innovators, Anokion’s immune-tolerance platform recently produced Phase 2 symptom improvement, positioning the Swiss-U.S. biotech as a potential acquisition target. Entero Therapeutics pushes latiglutenase toward Phase 3, underpinned by remote-monitoring partnerships that cut site-visit frequency by 30%, an operational edge well regarded by investors.

Platform technologies matter as much as single molecules. Digital companion apps collect meal-time photos and real-time symptom stamps that feed machine-learning algorithms, allowing dynamic dosing recommendations and forming data moats around early movers. Manufacturing know-how further differentiates entrants: enzyme producers must achieve high specific-activity yields under GMP, while biologic players navigate complex cell-culture scale-up. Strategic collaborations proliferate; Takeda signed material-supply pacts with Zedira GmbH for transglutaminase inhibitor APIs, and Teva partnered with data-analytics start-ups to model responder profiles from biopsy genomics. Such alliances accelerate knowledge transfer across the value chain and lift barriers to latecomers eyeing the gluten intolerance treatment market share.

Funding flows illustrate the shifting power map. Venture rounds above USD 50 million became commonplace in 2025 as gut-health investors rotated out of probiotic fast-followers into clinically validated drug assets. IPO windows reopened when Anokion floated on Nasdaq, raising USD 200 million to bankroll registrational trials. Larger groups pursue bolt-on acquisitions to access specialty know-how without organic build-out delays; Takeda’s earlier PvP buy-out set a pricing benchmark for phase-1 assets at 10-times projected peak-sales multiples. Collectively, these dynamics signal an imminent tipping point when the first FDA approval will likely trigger cascading commercialization and consolidation waves inside the gluten intolerance treatment market.

Gluten Intolerance Treatment Industry Leaders

Takeda Pharmaceutical

9 Meters Biopharma

ImmunogenX

Provention Bio

Nestlé Health Science

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Teva Pharmaceutical received FDA Fast Track designation for TEV-53408, an investigational anti-IL-15 antibody for treating celiac disease, accelerating its review timeline.

- January 2025: Anokion announced positive symptom data from its Phase 2 ACeD-it trial evaluating KAN-101, demonstrating significant reductions in gluten-induced symptoms and celiac-specific biomarkers via immune-tolerance induction.

- December 2024: Anokion completed early enrollment in two concurrent Phase 2 studies of KAN-101, underscoring strong investigator and patient interest in tolerance-induction approaches.

Global Gluten Intolerance Treatment Market Report Scope

| Enzyme Therapy |

| Biologic Therapy |

| Small-Molecule Inhibitors |

| Probiotics & Synbiotics |

| Others (Vaccines, Desensitization, Gene-Editing) |

| Oral |

| Parenteral |

| Intranasal |

| Sublingual |

| Transdermal |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Therapy Type | Enzyme Therapy | |

| Biologic Therapy | ||

| Small-Molecule Inhibitors | ||

| Probiotics & Synbiotics | ||

| Others (Vaccines, Desensitization, Gene-Editing) | ||

| By Route of Administration | Oral | |

| Parenteral | ||

| Intranasal | ||

| Sublingual | ||

| Transdermal | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the gluten intolerance treatment market by 2030?

The gluten intolerance treatment market is forecast to reach USD 10.1 billion by 2030, growing at an 8.3% CAGR.

Which therapy type currently generates the highest revenue?

Enzyme therapy leads with 38.1% market share, supported by patient-friendly oral capsules that degrade gluten peptides.

Why are anti-IL-15 biologics attracting fast-track designations?

They directly block a key cytokine driving mucosal damage, and early data show promising histologic improvement, prompting regulators to expedite review.

How fast are online pharmacies expanding in this space?

Online channels are advancing at a 12.5% CAGR through 2030, reflecting demand for discrete delivery and integrated digital support tools.

Which region is expected to post the fastest growth?

Asia-Pacific is projected to record the highest regional CAGR as diagnostic capacity widens and wheat consumption rises.

What remains the biggest development hurdle for late-stage candidates?

High Phase 3 attrition, linked to stringent histological endpoints and variable gluten-challenge protocols, continues to delay approvals and elevate costs.

Page last updated on: