Eye Glasses Market Size and Share

Market Overview

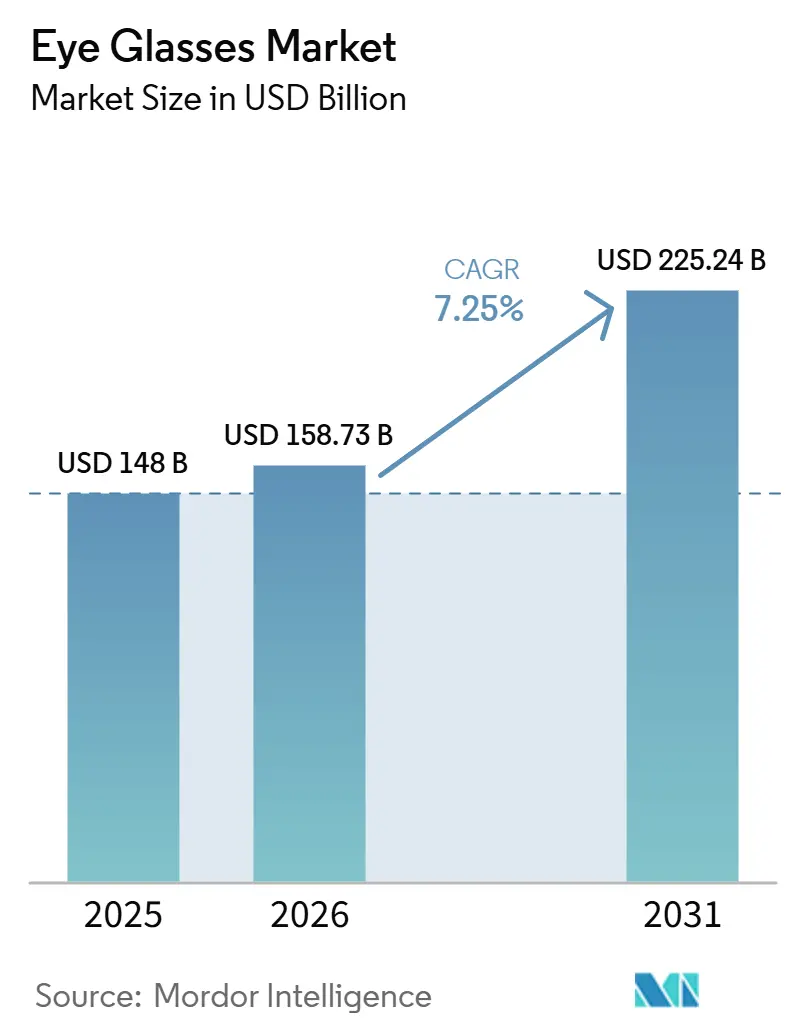

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 158.73 Billion |

| Market Size (2031) | USD 225.24 Billion |

| Growth Rate (2026 - 2031) | 7.25% CAGR |

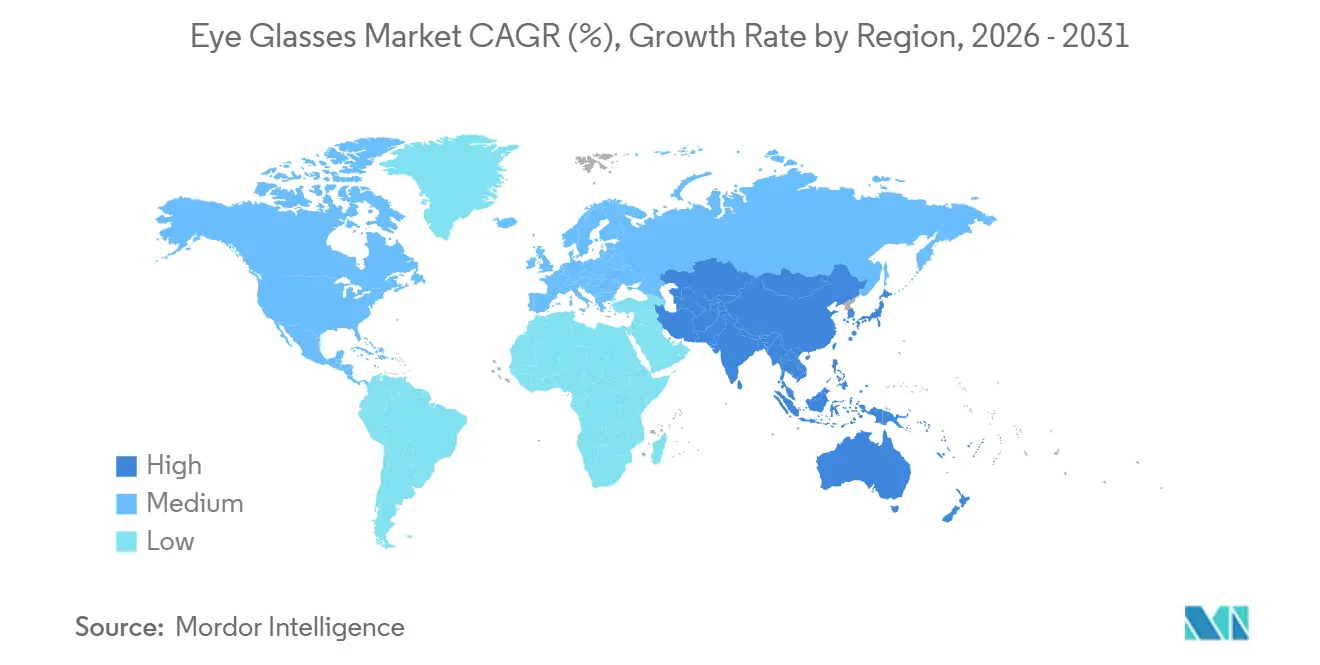

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

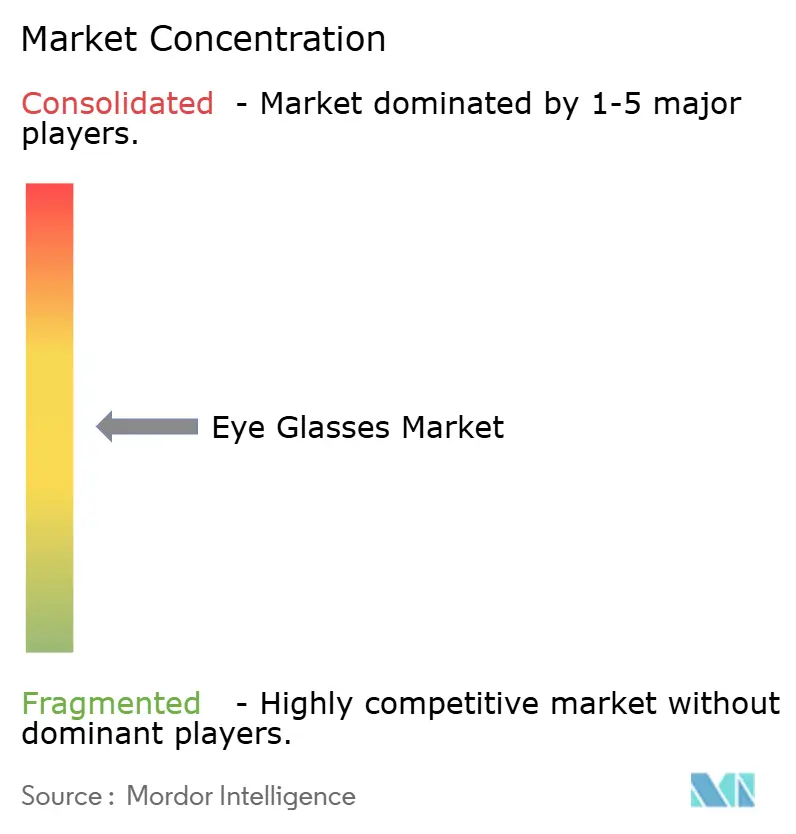

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Eye Glasses Market Analysis by Mordor Intelligence

The Eye Glasses Market size is projected to expand from USD 148 billion in 2025 and USD 158.73 billion in 2026 to USD 225.24 billion by 2031, registering a CAGR of 7.25% between 2026 to 2031.

The growth trajectory remains supported by the steady rise in refractive disorders, particularly myopia, driven by higher digital screen exposure and earlier onset among children and adolescents. The eye glasses market also benefits from shifting consumer behavior, as eyewear increasingly meets both medical needs and personal style preferences, supporting repeat purchases and higher average selling prices. Technology continues to expand the category, with Artificial Intelligence (AI)-enabled glasses moving closer to mainstream optical retail through major launches and rising unit sales. Regional demand remains strongest in North America and is growing fastest in Asia-Pacific, where premiumization in mature markets and the significant myopia burden in East Asia continue to shape the market’s long-term outlook.

Key Report Takeaways

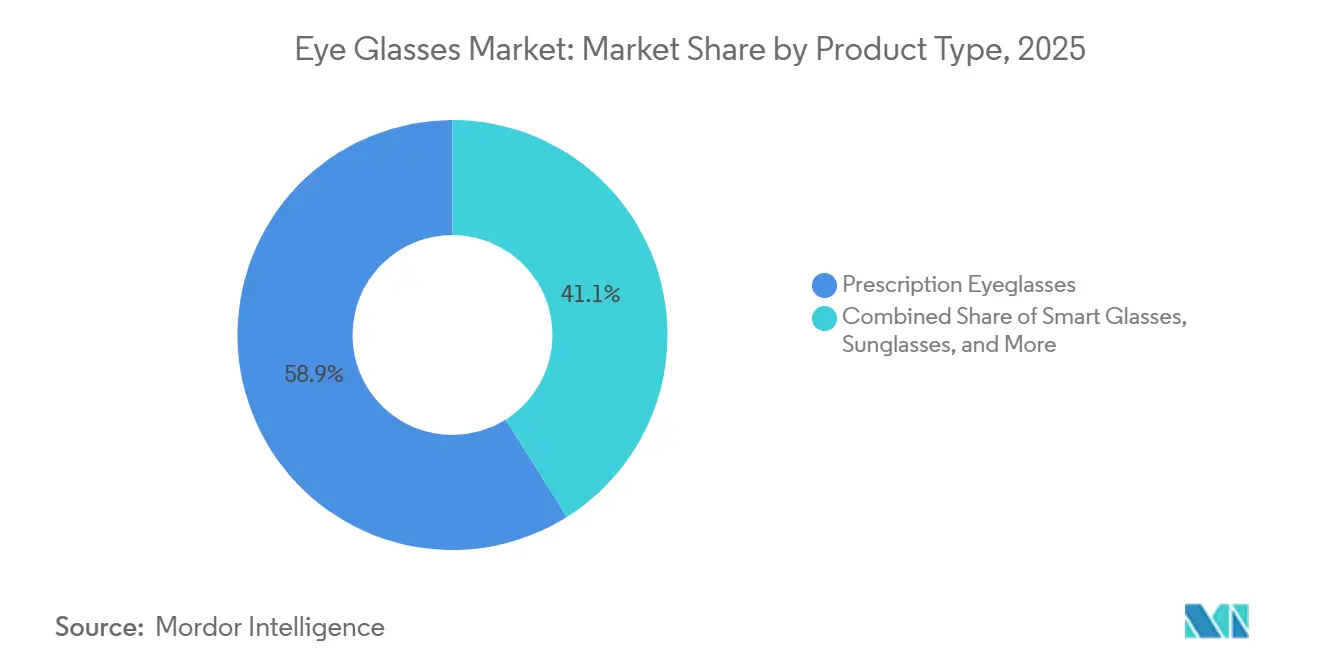

- By product type, prescription eyeglasses held 58.94% of the eye glasses market size in 2025, while smart glasses are forecast to expand at a 10.20% CAGR through 2031.

- By frame material, plastic frames accounted for 39.45% of the market in 2025, while titanium is projected to grow at a 9.67% CAGR through 2031.

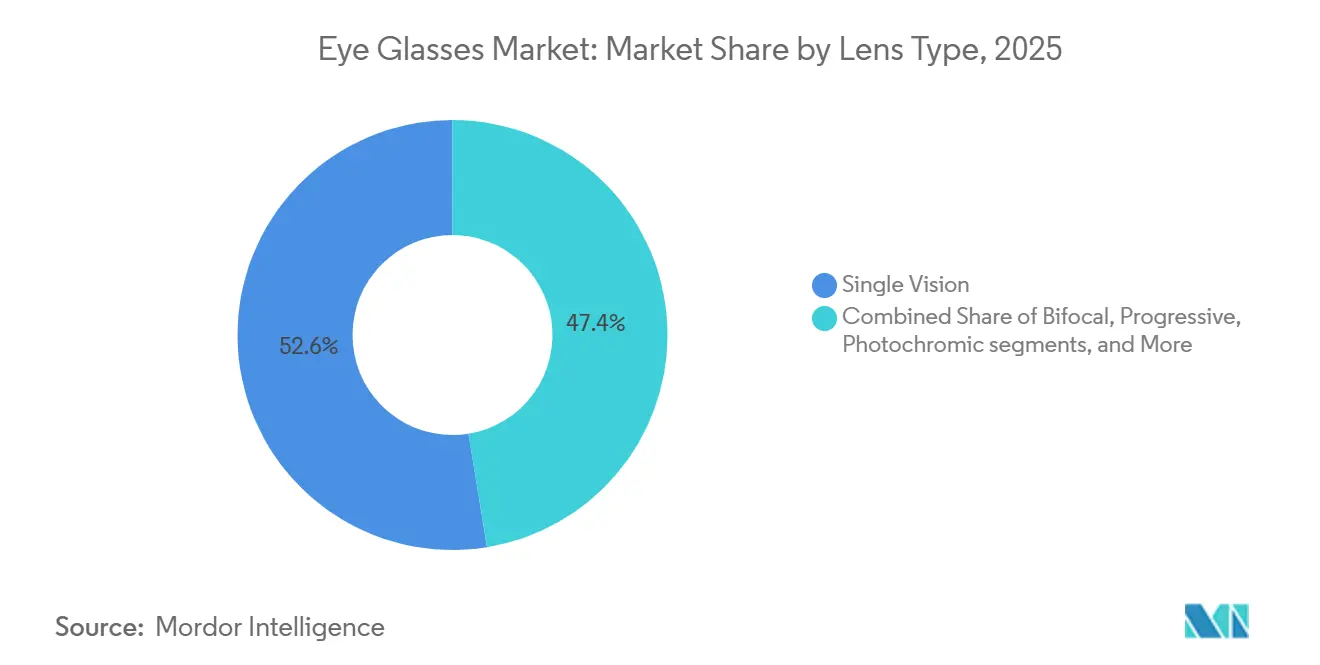

- By lens type, single vision lenses represented 52.56% of the eye glasses market size in 2025, while photochromic lenses are expected to advance at an 8.45% CAGR through 2031.

- By distribution channel, optical stores held 44.35% of the eye glasses market share in 2025, while e-commerce is forecast to grow at a 10.35% CAGR through 2031.

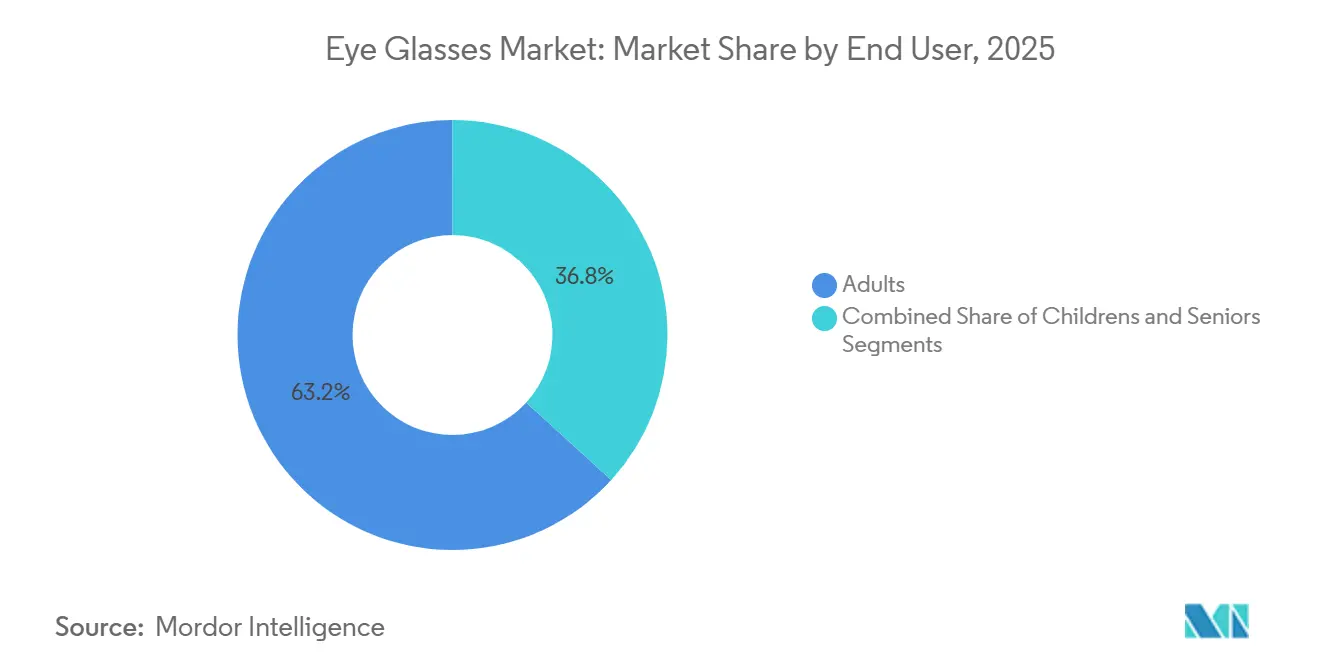

- By end user, adults captured 63.22% of the market in 2025, while children are projected to grow at a 9.65% CAGR through 2031.

- By geography, North America held 41.30% of the eye glasses market share in 2025, while Asia-Pacific is expected to expand at an 11.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Eye Glasses Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising myopia, presbyopia, and digital eye strain burden | +3.2% | Global | Short term (≤ 2 years) |

| Growth in premiumization and fashion-led frame replacement cycles | +1.5% | North America and Europe | Medium term (2-4 years) |

| Expansion of omnichannel optical retail and online try-on | +1.2% | Global, with stronger momentum in Asia-Pacific | Medium term (2-4 years) |

| Smart eyewear convergence with ar, audio, and health functions | +0.9% | North America, Europe, and select Asia-Pacific markets | Long term (≥ 4 years) |

| Rising myopia management adoption in children and young adults | +0.8% | Asia-Pacific, with spillover into North America and Europe | Medium term (2-4 years) |

| Increased employer and insurer-funded vision benefits in mature markets | +0.6% | North America and Western Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Myopia, Presbyopia, and Digital Eye Strain Burden

The clinical base of the eyeglasses market continues to strengthen as visual strain increases across younger and older age groups. A 2025 study in BMC Pediatrics reported global myopia prevalence of 31.4% among children using smartphones and 35.4% among children using television and computer games.[1]A. Ha et al., “Digital Screen Time and Myopia: A Systematic Review and Dose-Response Meta-Analysis,” JAMA Network Open, jamanetwork.com A separate 2025 meta-analysis found that smart device screen time was associated with a 26% increase in the odds of myopia, reinforcing the link between digital habits and prescription demand.[2]B. Holden et al., “Global Prevalence, Trend and Projection of Myopia in Children and Adolescents from 1990 to 2050,” British Journal of Ophthalmology, bmj.com The International Myopia Institute noted in its 2025 digest that screen-time reduction alone and outdoor activity alone do not adequately control axial elongation, supporting specialty spectacle lenses as a longer-term management tool.[3]The Vision Council, “U.S. Optical Industry Reaches $69.5 Billion Despite Declines in Product Volume and Eye Exams,” The Vision Council, thevisioncouncil.org EssilorLuxottica’s myopia management portfolio grew 22% worldwide in 2025, indicating stronger premium lens demand within the eyeglasses market.

Growth in Premiumization and Fashion-Led Frame Replacement Cycles

The eyeglasses market is moving beyond vision correction, as purchases increasingly reflect style preferences, brand affinity, and a willingness to own more than one pair. Safilo reported resilient prescription frame demand across geographies in 2025, while sport, contemporary, and lifestyle frames delivered 2.6% organic growth, excluding the Lenti deconsolidation effect. Premiumization increases replacement frequency and average selling price, particularly in North America and Europe, where branded frames carry stronger lifestyle value. Prescription buyers in mature markets increasingly treat frames as wearable accessories, supporting second-pair and third-pair purchases within the same year. This behavior helps stabilize revenue even when unit growth slows, as consumers trade up in materials, brand labels, coatings, and design features.

Expansion of Omnichannel Optical Retail and Online Try-On

Retail structure is reshaping demand capture in the eyeglasses market, although store-based service remains central for eye exams, fitting, and prescription validation. Warby Parker added 47 net new stores in 2025, reached USD 876 million in revenue, and launched an artificial intelligence-powered shopping advisor that works with its virtual try-on tools. KITS Eyecare crossed CAD 200 million, equivalent to USD 148 million, in 2025 revenue and exceeded 1 million two-year active customers, supported by its OpticianAI-based digital fit experience and vertically integrated lens production. These digital tools reduce friction in browsing and repurchasing while keeping professional fitting relevant for more complex prescriptions. Stronger omnichannel models also improve data capture around fit, style selection, and repeat behavior, supporting targeted retention efforts.

Smart Eyewear Convergence With AR, Audio, and Health Functions

Smart functionality is expanding the role of eyewear and creating a new growth layer within the eyeglasses market rather than replacing traditional prescription demand. EssilorLuxottica reported that it sold more than 7 million artificial intelligence-glass units in 2025, while the Ray-Ban Meta line generated revenue that more than tripled year over year. In June 2026, EssilorLuxottica and Meta launched the Meta Glasses collection from USD 299, with three prescription-compatible styles aimed at a wider consumer base. The category remains at an early stage, but the price point and optical-first design approach indicate a broader addressable audience than earlier smart-glass launches. Privacy compliance remains important for devices with cameras, sensors, or health monitoring functions and will shape how the eyeglasses market develops in regulated consumer environments.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High prevalence of substitution from contact lenses and refractive surgery | -1.4% | Global | Short term (≤ 2 years) |

| Counterfeit and grey-market frames eroding premium pricing | -0.8% | Asia-Pacific, Middle East and Africa, and South America | Short term (≤ 2 years) |

| Dependence on skilled optician distribution and fitting infrastructure | -0.5% | Sub-Saharan Africa, South Asia, and South America | Medium term (2-4 years) |

| Consumer trade-down during discretionary spending slowdowns | -0.7% | North America and Western Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Prevalence of Substitution From Contact Lenses and Refractive Surgery

The eyeglasses market continues to face direct competition from contact lenses and laser-based corrective procedures across the same adult patient base. LASIK, SMILE, and related surgical options can limit frame demand among working-age consumers who prefer a one-time intervention over continued spectacle use. This pressure remains more visible in mature markets, where higher income levels and better access to elective procedures support a shift away from routine spectacle wear. However, this restraint does not affect the eyeglasses market uniformly, as surgery does not suit every patient and cannot address all use cases requiring ongoing visual support. Children provide a meaningful buffer because myopia management still relies heavily on spectacle-based treatment, and minors generally do not qualify for refractive surgery. This trend maintains a durable prescription pipeline for the eyeglasses market, from early diagnosis into adulthood.

Counterfeit and Grey-Market Frames Eroding Premium Pricing

Counterfeit products and unauthorized distribution continue to weaken pricing discipline in parts of the eyeglasses market, especially where online enforcement remains inconsistent. A June 2025 investigation cited by the Association of Optometrists reported that sunglasses purchased through major online platforms failed UV safety tests and lacked required conformity markings, such as CE or UKCA labels. The issue extends beyond safety concerns, as gray-market sales also reset consumer price expectations and reduce the perceived value of authorized retail channels. As a result, premium brands in the eyeglasses market face pressure to defend price points while protecting brand trust and product legitimacy. The problem remains most acute in price-sensitive markets, where cross-border digital commerce makes unauthorized inventory easier to move. Until platform oversight becomes more consistent, counterfeit and gray-market distribution will remain a recurring drag on premium realization in the eyeglasses market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Prescription Eyeglasses Anchor Revenue, Smart Glasses Lift the Growth Ceiling

Prescription eyeglasses are expected to lead the eye glasses market with a 58.94% share in 2025, reflecting the scale and persistence of global refractive errors. The segment remains the revenue anchor as corrective use is medically necessary, while repeat purchases are driven by updated prescriptions, frame wear, and evolving visual needs. Reading glasses continue to benefit from rising presbyopia across aging populations in North America, Europe, and East Asia. Sunglasses and safety or sports eyewear add demand across lifestyle and occupational applications, while prescription wear supports follow-on purchases in sun, protective, and performance frames.

Smart glasses are projected to grow at a 10.20% compound annual growth rate (CAGR) from 2026 to 2031, making them the fastest-growing product category in the eye glasses market. The category is shifting eyewear from a corrective product to a connected platform, especially as prescription compatibility removes a key adoption barrier. The June 2026 Meta Glasses launch at USD 299 in three Rx-able styles signals a move toward everyday use rather than niche technology positioning. EssilorLuxottica’s sale of more than 7 million AI-glass units in 2025 shows that smart eyewear demand is expanding across regions, while safety and sports eyewear remain relevant through workplace and outdoor use cases.

By Frame Material: Plastic Holds the Base, Titanium Gains on Value

Plastic frames are expected to account for 39.45% of the eye glasses market in 2025, supported by affordability, broad styling options, and strong availability across mass and mid-tier retail formats. Acetate continues to appeal to fashion-focused consumers in mature markets, while lighter plastic formats remain popular in price-sensitive and family-oriented purchases. The segment benefits from flexibility across age groups, prescription strengths, and design preferences. Plastic remains important as it balances manufacturing efficiency with a wide product assortment across clinical and lifestyle needs.

Titanium is expected to expand at a 9.67% CAGR through 2031, making it the fastest-growing material segment in the eye glasses market. Demand is rising as premium-category buyers prioritize low weight, durability, corrosion resistance, and hypoallergenic properties. Titanium also supports higher realized prices, helping premium optical brands improve revenue per frame rather than relying only on unit turnover. Metal frames remain relevant for precise fitting and structural rigidity, while bio-acetate is gaining traction in premium collections as sustainability becomes more visible in purchase decisions.

By Lens Type: Single Vision Dominates the Base, Photochromics Drive Upgrade Demand

Single vision lenses are expected to hold 52.56% of the market in 2025, keeping them central to the eye glasses market because they align with the dominant global pattern of myopia correction. Their scale is supported by the early onset of myopia in children and adolescents, which creates a large and recurring prescription pool. A 2025 study in the British Journal of Ophthalmology projected that childhood and adolescent myopia prevalence will exceed 39.80% by 2050, representing more than 740 million cases globally. Progressive lenses remain important for older users with presbyopia, while bifocals continue to lose ground in markets that favor seamless optics and cleaner aesthetics.

Photochromic lenses are projected to grow at an 8.45% CAGR from 2026 to 2031, making them the fastest-growing lens category in the eye glasses market. Their practical value lies in enabling users to move between indoor and outdoor conditions without carrying a separate pair of prescription sunglasses. In April 2026, HOYA launched its third-generation Sensity 3 lenses with 25% faster fade-back speed and improved color stability, addressing a long-standing user concern. ZEISS PhotoFusion X also emphasized faster clearing and integrated BlueGuard material that blocks up to 50% of potentially harmful blue light indoors, supporting premium lens adoption.

By Distribution Channel: Optical Stores Lead the Present, E-Commerce Reshapes Access

Optical stores are expected to hold 44.35% of the eye glasses market in 2025, supported by the continued importance of professional exams, frame fitting, and prescription validation. The Vision Council reported that the United States (US) optical industry reached USD 69.5 billion in 2025, with in-store exams remaining the preferred route for most prescription frame and lens purchases. This keeps the store channel central, especially for multifocal needs, premium coatings, and higher-value consultations. Retail chains and hospital-linked eye care channels also benefit from trust, bundled services, and repeat customer relationships built around annual exams.

E-commerce is projected to advance at a 10.35% CAGR through 2031, making it the fastest-growing channel in the eye glasses market. Growth is being driven by digital fit tools, prescription handling, and simplified repeat purchase journeys rather than price alone. Warby Parker’s use of artificial intelligence (AI)-based shopping support and KITS Eyecare’s OpticianAI platform show how digital systems are addressing fit and selection issues that previously limited online eyewear adoption. The market is moving toward an omnichannel model, where digital tools improve discovery and repeat conversion while physical sites manage exams, fittings, and complex prescriptions.

By End User: Adults Hold the Largest Base, Children Show the Strongest Momentum

Adults are expected to account for 63.22% of the eye glasses market in 2025, supported by ongoing correction needs across working-age and older populations. Myopia, astigmatism, and presbyopia create a stable demand pool that supports regular replacement cycles and layered lens upgrades. In mature markets, employer- and insurer-backed vision benefits increase purchase frequency by reducing out-of-pocket costs and keeping annual exams part of routine care. The US Federal Employees Dental and Vision Insurance Program and other private vision plans support this structure through frame and lens allowances tied to routine care.

Children are projected to record a 9.65% CAGR from 2026 to 2031, making them the fastest-growing end-user group in the eye glasses market. Growth is driven by the shift from basic correction to structured myopia management in pediatric eyewear. A 2025 randomized clinical trial in JAMA Ophthalmology found that 0.04% atropine was more effective than orthokeratology alone for myopia control in children aged 8 to 15, supporting broader co-management strategies in pediatric care. HOYA’s MiYOSMART line and EssilorLuxottica’s Stellest lens gained momentum in 2025, indicating stronger commercial acceptance of specialized spectacle-based pediatric solutions.

Geography Analysis

North America is expected to hold 41.30% of the eyeglasses market in 2025, making it the largest regional contributor by value. High per-capita spending, established reimbursement structures, and strong adoption of premium lenses, coatings, and branded frames support the region’s leadership. The Vision Council projects that the US optical industry will reach USD 69.5 billion in 2025, even as product volumes and eye exams decline, indicating stronger pricing and a richer product mix. Warby Parker plans to add 47 stores in 2025 and 50 more in 2026, reflecting continued confidence in integrated retail and clinical models. These factors strengthen North America’s role in premium product adoption and early commercialization of connected eyewear.

Europe remains the second-largest regional bloc in the eyeglasses market, supported by independent optician networks, a strong premium frame culture, and ongoing retail consolidation. Fielmann expects record results for fiscal year 2025 and has guided for EUR 2.55 billion to EUR 2.60 billion in fiscal year 2026 sales, supported by the planned rollout of AI-enabled automated refraction across 300 European stores and 70 new store openings in 2026. Italy continues to hold strategic importance through the Belluno manufacturing base, which supports much of the premium frame supply chain for major eyewear groups. Europe also plays a major role in smart eyewear launches, as the June 2026 Meta Glasses rollout is expected to include the United Kingdom, France, Italy, Germany, and Spain. These factors keep the region central to premium design, manufacturing quality, and branded value capture in the eyeglasses market.

Asia-Pacific is forecast to register an 11.56% compound annual growth rate through 2031, making it the fastest-growing region in the eyeglasses market. The region has the world’s highest myopia burden, and the World Health Organization Western Pacific office has described myopia as reaching epidemic levels, with prevalence near 50% among adolescents in China and Singapore and up to 80% among young adults in parts of East Asia. This trend creates a structurally strong correction base, especially among school-age and young adult populations entering long-term prescription cycles earlier than those in many other regions. India remains an important growth pocket, as organized optical retail continues to expand while disposable income and unmet correction needs rise.

Competitive Landscape

The eyeglasses market is moderately consolidated at the top, with EssilorLuxottica holding the clearest leadership position across lenses, frames, and retail reach. Brands such as Ray-Ban and Oakley, along with direct-to-consumer channels such as LensCrafters and Sunglass Hut, strengthen the company’s scale. The company’s reported sale of more than 7 million artificial intelligence (AI) glass units in 2025 also shows how it is using connected eyewear to expand beyond traditional optical categories. This gives EssilorLuxottica a broader strategic position in the eyeglasses market than companies focused only on licensed frames or regional retail.

Competition remains diverse because companies control different parts of the eyeglasses market. Safilo and Marcolin compete strongly in branded and licensed frame portfolios, while Fielmann and Specsavers maintain strong positions in European retail execution and customer access. Digital-first challengers such as Warby Parker, Zenni Optical, and Lenskart continue to pressure legacy operating models by simplifying standard prescription purchases and reducing some traditional markup layers. Safilo’s acquisition of SPY+ and Serengeti for USD 24.6 million in July 2026 is expected to strengthen its home-brand portfolio and add USD 39 million in combined 2025 revenue.

Technology and optics are becoming more closely linked, increasing the strategic value of companies that combine clinical credibility with product innovation. HOYA and ZEISS continue to advance premium lens upgrades through improved photochromic performance, faster adaptation, and better blue-light management. Warby Parker is investing in AI-enabled shopping and a larger store base, while established leaders are using smart-glass partnerships to strengthen their relevance among younger and more digitally engaged consumers. Barriers to entry in the eyeglasses market remain significant where prescription quality, lens performance, optical compliance, and physical fitting are critical.

Eye Glasses Industry Leaders

EssilorLuxottica

Carl Zeiss AG

Fielmann Group AG

Hoya Corporation

NIDEK CO., LTD.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Safilo Group acquired SPY+ and Serengeti from Bollé Brands for USD 24.6 million, adding USD 39 million in combined 2025 revenue and strengthening its sport and outdoor eyewear portfolio.

- June 2026: EssilorLuxottica and Meta launched the Meta Glasses collection, priced from USD 299, with three prescription-ready styles across seven key markets.

- June 2026: Carl Zeiss AG announced the planned acquisition of EDY OPTIC, a major optical lens and medical device distributor in Romania, with completion scheduled for Q3 2026.

- March 2026: EssilorLuxottica and Meta expanded their AI glasses portfolio with Ray-Ban Meta Optics and planned launches in Japan, South Korea, Singapore, Chile, Peru, and Colombia.

Global Eye Glasses Market Report Scope

As per the scope of the report, eye glasses, also known as spectacles or specs, are vision-correction and protection tools. They consist of a frame holding two pieces of specially shaped glass or plastic lenses. They sit on the nose bridge and hook over the ears, bending light rays to help the eyes focus properly.

The eye glasses market is segmented by product type, frame material, lens type, distribution channel, end user, and geography. By product type, the market includes prescription eyeglasses, reading glasses, sunglasses, smart glasses, and safety and sports eyewear. By frame material, the market is segmented into plastic, metal, acetate, titanium, and other frame materials. By lens type, the market is categorized into single vision, bifocal, progressive, photochromic, polarized, and other lens types. By distribution channel, the market is segmented into optical stores, retail chains, e-commerce, hospitals and eye care clinics, and other distribution channels. By end user, the market is segmented into adults, children, and seniors. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Prescription Eyeglasses |

| Reading Glasses |

| Sunglasses |

| Smart Glasses |

| Safety and Sports Eyewear |

| Plastic |

| Metal |

| Acetate |

| Titanium |

| Other Frame Materials |

| Single Vision |

| Bifocal |

| Progressive |

| Photochromic |

| Polarized |

| Others |

| Optical Stores |

| Retail Chains |

| E-Commerce |

| Hospitals and Eye Care Clinics |

| Others |

| Adults |

| Children |

| Seniors |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Prescription Eyeglasses | |

| Reading Glasses | ||

| Sunglasses | ||

| Smart Glasses | ||

| Safety and Sports Eyewear | ||

| By Frame Material | Plastic | |

| Metal | ||

| Acetate | ||

| Titanium | ||

| Other Frame Materials | ||

| By Lens Type | Single Vision | |

| Bifocal | ||

| Progressive | ||

| Photochromic | ||

| Polarized | ||

| Others | ||

| By Distribution Channel | Optical Stores | |

| Retail Chains | ||

| E-Commerce | ||

| Hospitals and Eye Care Clinics | ||

| Others | ||

| By End User | Adults | |

| Children | ||

| Seniors | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the Eye Glasses Market?

The eye glasses market size stands at USD 158.73 billion in 2026 and is projected to reach USD 225.24 billion by 2031 at a 7.20% CAGR.

Which product segment leads eyewear demand?

Prescription eyeglasses lead the category with 58.94% share in 2025 because corrective use remains medically necessary and recurring.

Which part of eyewear is growing the fastest?

Smart glasses are the fastest-growing product type, with a projected 10.20% CAGR from 2026 to 2031 as AI and prescription compatibility improve adoption.

Why is childrens eyewear becoming more important?

Children are the fastest-growing end-user group at a 9.65% CAGR, mainly because myopia management now involves longer-term and more specialized spectacle use.

Which sales channel is changing the fastest?

E-commerce is forecast to grow at a 10.35% CAGR, supported by AI-assisted fit tools, virtual try-on, and easier repeat purchases.

Which region matters most for future growth?

North America remains the largest region with 41.30% share in 2025, but Asia-Pacific is the fastest-growing region at an 11.56% CAGR due to its heavy myopia burden.

Page last updated on: