U.S. Eye Care Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

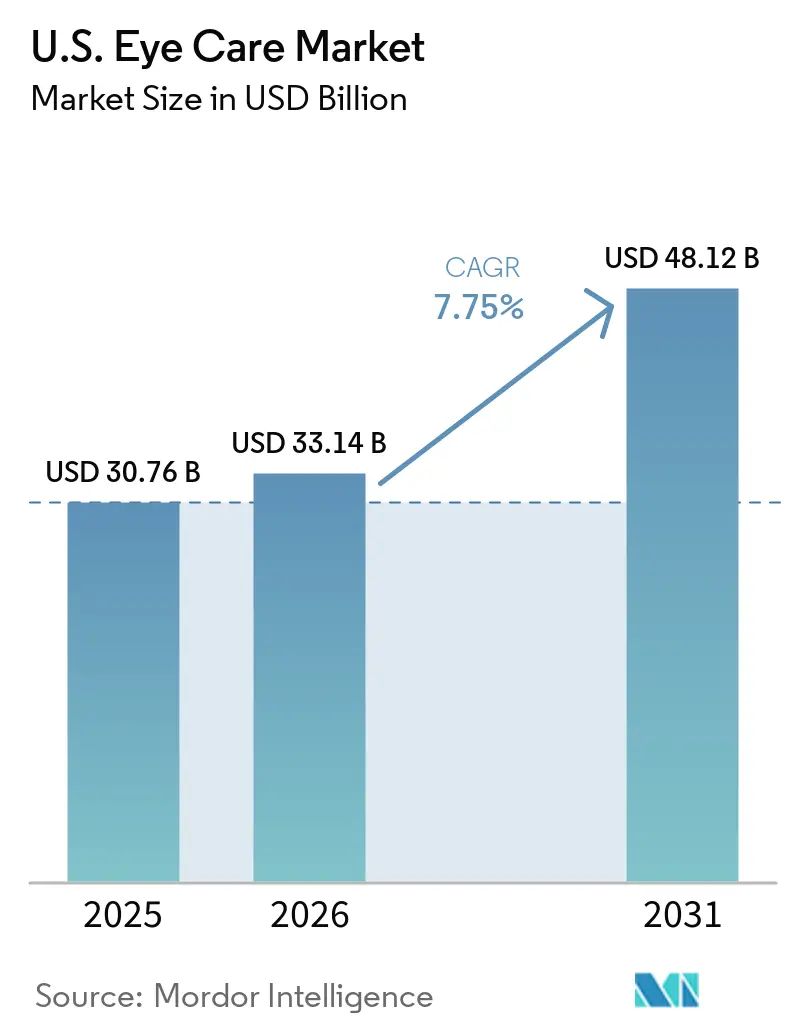

| Base Year Market Size (2025) | USD 30.76 Billion |

| Market Size (2026) | USD 33.14 Billion |

| Market Size (2031) | USD 48.12 Billion |

| Growth Rate (2026 - 2031) | 7.75% CAGR |

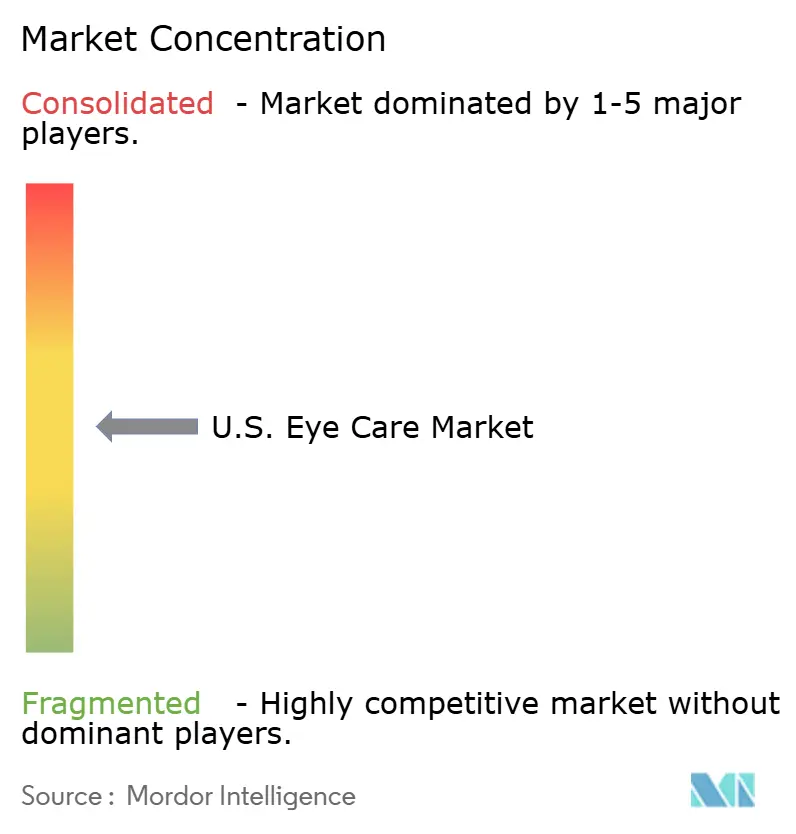

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

U.S. Eye Care Market Analysis by Mordor Intelligence

The U.S. Eye Care Market size is expected to increase from USD 30.76 billion in 2025 to USD 33.14 billion in 2026 and reach USD 48.12 billion by 2031, growing at a CAGR of 7.75% over 2026-2031.

The United States eye care market faces a significant care gap. While 93 million adults are at high risk for serious vision loss, only about half visited an eye doctor in the past year, indicating unmet needs rather than a demand ceiling. Digital exposure is driving demand further. By 2025, employees are expected to average 97 hours of screen time weekly, with 68% reporting digital eye strain symptoms and 63% experiencing at least one eye issue.[1]Workplace Intelligence, “2025 Workplace Vision Health Report,” Workplace Intelligence, workplaceintelligence.com The aging population adds to the long-term treatment burden from conditions like glaucoma, cataracts, age-related macular degeneration, and diabetic retinopathy, ensuring consistent utilization across clinical and consumer channels.

Key Report Takeaways

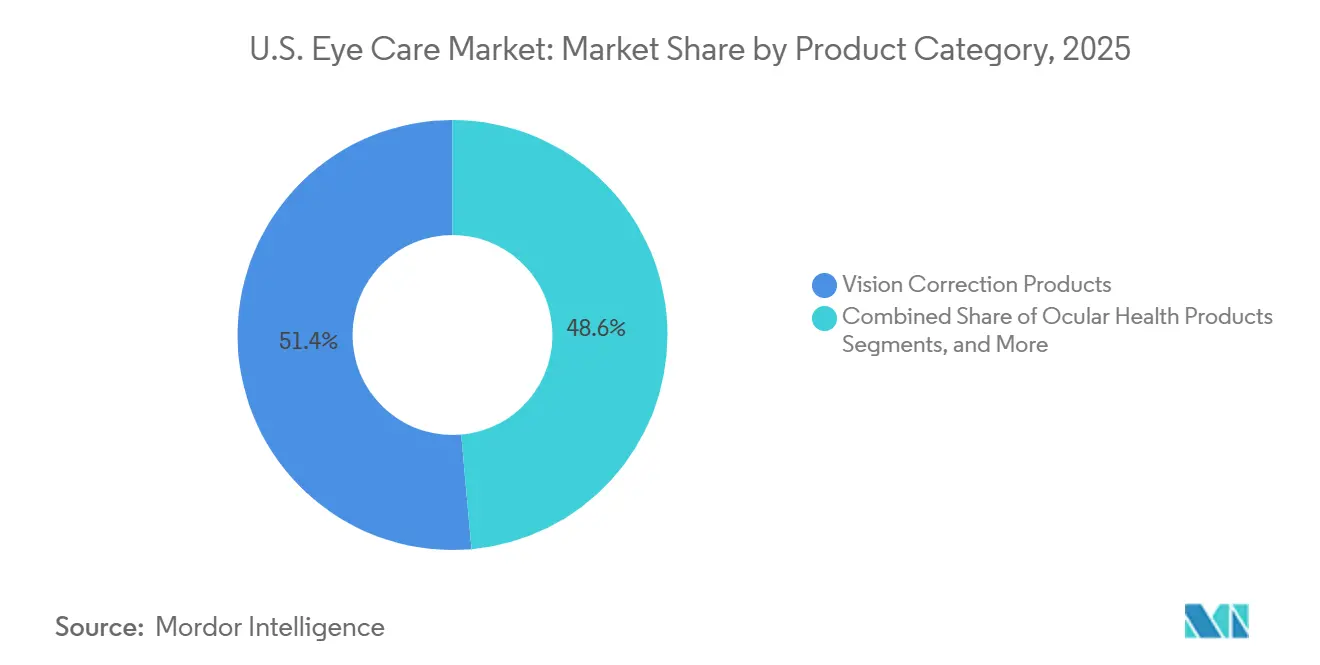

- By product category, vision correction products held 51.44% of revenue in 2025, while ocular health products are projected to grow at an 8.10% CAGR through 2031.

- By mode of purchase, prescribed (Rx) products accounted for 73.22% of purchases in 2025, while over-the-counter products are forecast to expand at an 8.40% CAGR through 2031.

- By distribution channel, ophthalmology clinics and optometry stores represented 38.67% of the US eye care market share in 2025, while the online channel is projected to grow at a 10.45% CAGR through 2031.

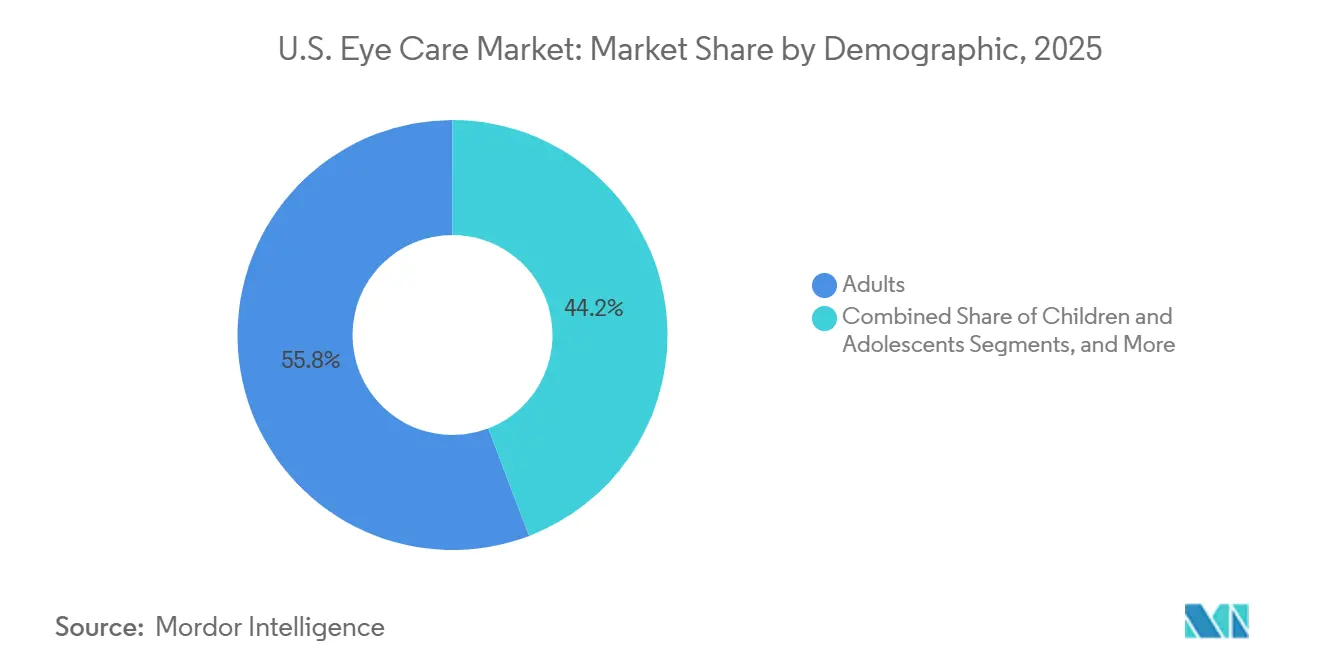

- By demographic, adults aged 18-64 accounted for 55.78% of revenue in 2025, while the geriatric segment is expected to advance at an 8.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

U.S. Eye Care Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Aging-linked ocular disease burden | +2.1% | National, with stronger intensity in the South and Sun Belt states such as Florida and Texas | Long term (≥ 4 years) |

| Screen-time-driven vision correction and dry-eye demand | +1.6% | National, with stronger effect in metro areas and technology-heavy workforce hubs on the West Coast and in the Northeast | Short term (≤ 2 years) |

| Omnichannel access and managed vision care utilization | +1.0% | National, with stronger relevance in markets with high managed-care penetration in the Northeast and Midwest | Medium term (2-4 years) |

| Primary-care AI retinal screening expansion | +0.9% | National, with early gains in California, Ohio, and North Carolina health systems using integrated EMR platforms | Medium term (2-4 years) |

| Durable myopia-management outcomes improve clinical adoption | +0.7% | National, with concentration in urban markets and pediatric ophthalmology centers in large metro areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging-Linked Ocular Disease Burden Sustains Multi-Category Demand

The aging population continues to drive the United States eye care market. In 2024, 4.22 million adults were affected by glaucoma, with the older population exceeding 54 million.[2]Centers for Disease Control and Prevention, “Glaucoma Prevalence, United States, 2022,” CDC, cdc.gov Conditions like cataracts, diabetic retinopathy, and age-related macular degeneration also rise with age, requiring ongoing treatment. Companies with diverse portfolios across multiple disease areas are better positioned to mitigate risks from reimbursement changes compared to single-category players.

Screen Time Expands the Dry-Eye and Vision Correction Addressable Market

Screen exposure has become a significant driver for the United States eye care market. Full-time employees averaged 97 hours of weekly screen time in 2025, with 68% reporting digital eye strain and 63% experiencing eye issues, up from 50% the previous year. This trend sustains demand for blue-light-filtering lenses, prescription eyewear, contact lenses, and dry-eye products, while expanding the market to include pediatric care through myopia management and related treatments.

Omnichannel Access and Managed Vision Care Deepen Market Penetration

Distribution convenience is reshaping the United States eye care market. Managed vision care covered 48% of households in 2025, encouraging routine exams, eyewear purchases, and replenishment cycles. Seamless transitions between clinic-based exams, digital prescriptions, and online fulfillment enhance continuity and reorder behavior. Provider-connected omnichannel models outperform purely offline or digital approaches, maintaining the role of eye care professionals.

Primary-Care AI Retinal Screening Expands the Diagnostic Funnel

AI-based retinal screening is expanding the diagnostic reach of the United States eye care market. By January 2025, Sutter Health deployed AI retinal cameras in 28 primary care practices, improving diabetic eye exam compliance from 62% to 68%. Autonomous AI-assisted screenings increase specialist referrals, streamline workflows, and convert silent disease burdens into active treatment demand, enhancing the overall diagnostic funnel.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Coverage gaps and cash-pay affordability pressure | -1.4% | National, with the strongest pressure in Medicaid non-expansion states across the South and Southeast and in rural markets with limited managed-care access | Medium term (2-4 years) |

| Ophthalmology and subspecialty workforce bottleneck | -1.2% | National, with the greatest pressure in rural regions and across the Mountain West and Plains states | Long term (≥ 4 years) |

| Tariff-led cost inflation across frames, lenses, and equipment | -0.9% | National, with stronger impact on practices and retailers that depend on Chinese-made optical products | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Coverage Gaps and Cash-Pay Affordability Constrain Utilization

Coverage design remains a significant challenge for the United States eye care market. In 2024, 6.5 million Medicaid enrollees (12%) lived in states without routine adult eye exam coverage, while 14.6 million (27%) lacked coverage for glasses. Vision benefits are often treated as supplemental, making them narrower and prone to network gaps. This limits access for lower-income patients and older adults, delaying exams, eyewear purchases, and follow-ups, leaving a substantial portion of demand unmet.

Ophthalmology and Subspecialty Workforce Bottleneck Caps Service Throughput

Workforce shortages continue to constrain the United States eye care market. By early 2026, 16,290 ophthalmologists were practicing, falling short by 2,310, with a projected shortfall of 7,290 by 2038. Access is uneven, with 55.7% of counties lacking ophthalmologists, impacting rural areas and regions like the Mountain West. Limited specialist availability leads to longer wait times, reduced procedure volumes, and lower utilization of drugs and devices, despite rising disease prevalence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Ocular Health Therapeutics Gain Share in a Multi-Segment Market

In 2025, Vision Correction Products accounted for 51.44% of revenue, making it the largest product category in the United States eye care market. This reflects the widespread use of spectacles, contact lenses, and refractive corrections, supported by routine replacements, screen-related vision issues, and broad clinical and retail access. Ocular Health Products, the fastest-growing segment, is projected to expand at an 8.10% CAGR through 2031, driven by demand for dry-eye therapeutics, anti-VEGF treatments, and premium ocular supplements.

The market is shifting from episodic corrections to recurring disease management. Surgical and Implantable Products are gaining traction, with RxSight achieving 300,000 Light Adjustable Lens implants by April 2026 and Glaukos advancing Epioxa commercialization in Q1 2026. Diagnostics and Monitoring Systems are also growing as AI tools enhance screening access, favoring companies with strong regulatory capabilities and comprehensive portfolios.

By Mode of Purchase: Rx Dominance Holds, While OTC Demand Builds Steadily

Prescribed products represented 73.22% of purchases in 2025, highlighting the dominance of clinically directed categories in the United States eye care market. Prescription eyewear, specialty contact lenses, surgical implants, and retinal therapies rely on licensed practitioners, keeping the Rx channel central. Over-the-Counter products are forecast to grow at an 8.40% CAGR through 2031, driven by consumer spending on dry-eye drops, ocular vitamins, and allergy-related eye care, supported by aging demographics and preventive self-care trends.

The FTC Eyeglass Rule update in September 2024 improved prescription portability, enabling easier transitions across fulfillment channels. Tele-optometry platforms are further enhancing digital prescription workflows. While the Rx channel remains critical for high-value categories, digital prescription mobility supports both OTC and online Rx fulfillment, blurring the lines between prescribed and consumer-directed purchases.

By Distribution Channel: Physical Clinics Lead, While Online Formats Expand the Fastest

Ophthalmology Clinics and Optometry Stores accounted for 38.67% of revenue in 2025, reflecting their role as key distribution channels in the United States eye care market. Patients rely on physical visits for exams, fittings, and high-value product decisions, ensuring the durability of this channel. The Online Channel, however, is the fastest-growing format, with a projected 10.45% CAGR through 2031, driven by the convenience of digital ordering for contact lenses and other products.

While over 80% of prescription frame and ophthalmic lens transactions occurred in person in 2026, hybrid models like those of Warby Parker and National Vision are scaling by combining physical stores with e-commerce. Tele-optometry collaborations, such as 20/20NOW's 2025 partnership with Walmart Vision Centers, are expanding access in underserved areas. Retail pharmacies are also strengthening their role in OTC eye care sales, creating a dual distribution model where convenience categories shift online, while clinical and fit-sensitive categories remain in person.

By Demographic: Adults Lead Revenue, While Geriatric Demand Advances the Fastest

Adults aged 18-64 contributed 55.78% of revenue in 2025, making them the largest demographic in the United States eye care market. This is driven by workplace vision benefits, routine eyewear demand, and screen-induced eye strain, supported by managed vision care coverage. The Geriatric segment is projected to grow at an 8.95% CAGR through 2031, driven by cataract procedures, anti-VEGF therapy, and glaucoma management, which generate sustained demand.

The younger demographic, though smaller in revenue, is gaining strategic importance. Rising screen-related myopia and dry-eye issues are increasing interest in orthokeratology lenses, low-dose atropine therapy, and defocus-based spectacles. The STAR myopia clinical trial, with results published in 2026, is expected to boost pediatric referrals and treatment adoption. The market thus has two growth poles: older adults with higher disease intensity and children with early prevention-led product needs, broadening the long-term patient pipeline.

Geography Analysis

Across the United States, the eye care market operates on a national scale, yet regional demand varies significantly. The South and Southeast face the highest burden, with states like Texas, Georgia, and the Carolinas experiencing elevated diabetes rates. This drives strong demand for diabetic retinopathy screenings and treatments. Florida's aging population further increases the need for cataract surgeries, anti-VEGF injections, and glaucoma management.

In Texas, high clinical demand is offset by affordability challenges. This reflects a broader issue of uneven insurance coverage and underinsurance, which limits access to routine exams and eyewear despite high disease prevalence. Value-driven retail chains play a critical role in converting unmet needs into actual visits and purchases.

The Northeast and West Coast are key regions for premium care adoption and technological advancements. Northeastern states like New York, Massachusetts, New Jersey, and Pennsylvania leverage strong academic and subspecialty networks to drive the use of advanced diagnostics, branded ophthalmic drugs, and premium surgical devices. On the West Coast, California leads in adopting AI-supported screenings through large integrated systems such as Sutter Health.

Competitive Landscape

In the United States eye care market, a few key players dominate the premium product categories. Alcon, Allergan Eye Care (a unit of AbbVie), Johnson & Johnson Vision Care, Bausch & Lomb, and EssilorLuxottica leverage extensive portfolios, strong clinician relationships, and large-scale manufacturing or retail platforms. These companies maintain significant influence across surgical devices, ophthalmic pharmaceuticals, lenses, and optical retail.

Recent strategic developments reflect evolving competition in the United States eye care market. In April 2026, Alcon expanded its premium intraocular lens portfolio with the launch of Clareon TruPlus, strengthening its position in cataract procedures. Similarly, Johnson & Johnson Medtech received FDA approval in March 2026 for the TECNIS PureSee EDOF intraocular lens, with a planned United States launch later in 2026, directly challenging Alcon in the premium IOL segment.

Outside the major multinational players, competition is diverse. Warby Parker integrates physical stores, e-commerce, and insurance partnerships, while National Vision focuses on affordable pricing and managed-care alignment. VSP Vision remains influential due to its benefits network, which drives recurring demand and patient retention. AI-driven companies like AEYE Health and Optain Health target early detection and remote access, particularly in primary care and underserved regions.

U.S. Eye Care Industry Leaders

Alcon Inc.

Bausch + Lomb Corporation

CooperVision, Inc.

EssilorLuxottica SA

HOYA Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Alcon introduced Clareon TruPlus, an advanced monofocal and toric intraocular lens, enhancing its Clareon platform with improved depth-of-focus and expanding its presence in the premium IOL market.

- April 2026: RxSight achieved the milestone of 300,000 Light Adjustable Lens implants, reflecting strong clinical adoption and reinforcing its premium position in the cataract surgery market.

- April 2026: Johnson and Johnson Medtech received US FDA approval for the TECNIS Puresee EDOF intraocular lens, intensifying competition in the premium IOL segment and impacting pricing dynamics.

- March 2026: Glaukos launched Epioxa HD and Epioxa, the first FDA-approved epithelium-on corneal cross-linking treatments for keratoconus, supported by co-pay assistance and awareness programs.

- January 2026: AEYE Health expanded its integration with Epic EMR, enabling rapid, autonomous AI diabetic retinopathy screenings within clinical workflows across US healthcare systems.

U.S. Eye Care Market Report Scope

As per the scope of the report, eye care encompasses the prevention, diagnosis, and treatment of visual and ocular health conditions. It involves a broad spectrum of interventions, ranging from routine vision correction (eyeglasses and contact lenses) to over-the-counter (OTC) eye drops, advanced diagnostics, and surgical procedures (e.g., LASIK and cataract removal).

The U.S. eye care market is segmented by product category, mode of purchase, distribution channel, and demographic. By product category, the market includes vision correction products, ocular health products, surgical & implantable products, diagnostics & monitoring systems, and others. By mode of purchase, the market is segmented into prescription (Rx) products and over-the-counter products. By distribution channel, the market is categorized into optical retail chains & independent optical stores, ophthalmology clinics & optometry stores, ambulatory surgery centers, hospitals, retail pharmacies, and online platforms. By demographics, the market is segmented into children & adolescents, adults, and the geriatric. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Vision Correction Products |

| Ocular Health Products |

| Surgical & Implantable Products |

| Diagnostics & Monitoring Systems |

| Others |

| Prescribed (Rx) Products |

| Over-the-Counter Products |

| Optical Retail Chains & Independent Optical Stores |

| Ophthalmology Clinics & Optometry Stores |

| Ambulatory Surgery Centers |

| Hospitals |

| Retail Pharmacies |

| Online Channel |

| Children & Adolescents |

| Adults |

| Geriatric |

| By Product Category | Vision Correction Products |

| Ocular Health Products | |

| Surgical & Implantable Products | |

| Diagnostics & Monitoring Systems | |

| Others | |

| By Mode of Purchase | Prescribed (Rx) Products |

| Over-the-Counter Products | |

| By Distribution Channel | Optical Retail Chains & Independent Optical Stores |

| Ophthalmology Clinics & Optometry Stores | |

| Ambulatory Surgery Centers | |

| Hospitals | |

| Retail Pharmacies | |

| Online Channel | |

| By Demographic | Children & Adolescents |

| Adults | |

| Geriatric |

Key Questions Answered in the Report

How large is the US eye care market in 2026 and what is the outlook through 2031?

The US eye care market stands at USD 33.16 billion in 2026 and is projected to reach USD 48.14 billion by 2031, growing at a CAGR of 7.75% over 2026-2031.

What is driving growth in eye care demand across the United States?

The strongest demand drivers are aging-related eye disease, high screen exposure, wider omnichannel access, and AI-supported retinal screening that brings more at-risk patients into treatment pathways.

Which product category leads revenue in US eye care?

Vision Correction Products led revenue with a 51.44% share in 2025, supported by strong demand for spectacles, contact lenses, and refractive correction services.

Which distribution channel is growing the fastest for eye care products and services?

The Online Channel is the fastest-growing format, with a 10.45% CAGR through 2031, helped by contact lens replenishment, prescription eyewear e-commerce, and tele-optometry expansion.

Which age group offers the strongest long-term opportunity?

The Geriatric segment is expanding the fastest at an 8.95% CAGR through 2031 because older adults require more cataract procedures, retinal therapies, glaucoma care, and monitoring.

What is the main challenge holding back broader utilization of eye care services?

Coverage gaps, out-of-pocket costs, and specialist shortages remain the main constraints, especially in rural areas and in states with weaker routine vision coverage.

Page last updated on: