Ophthalmology Diagnostics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

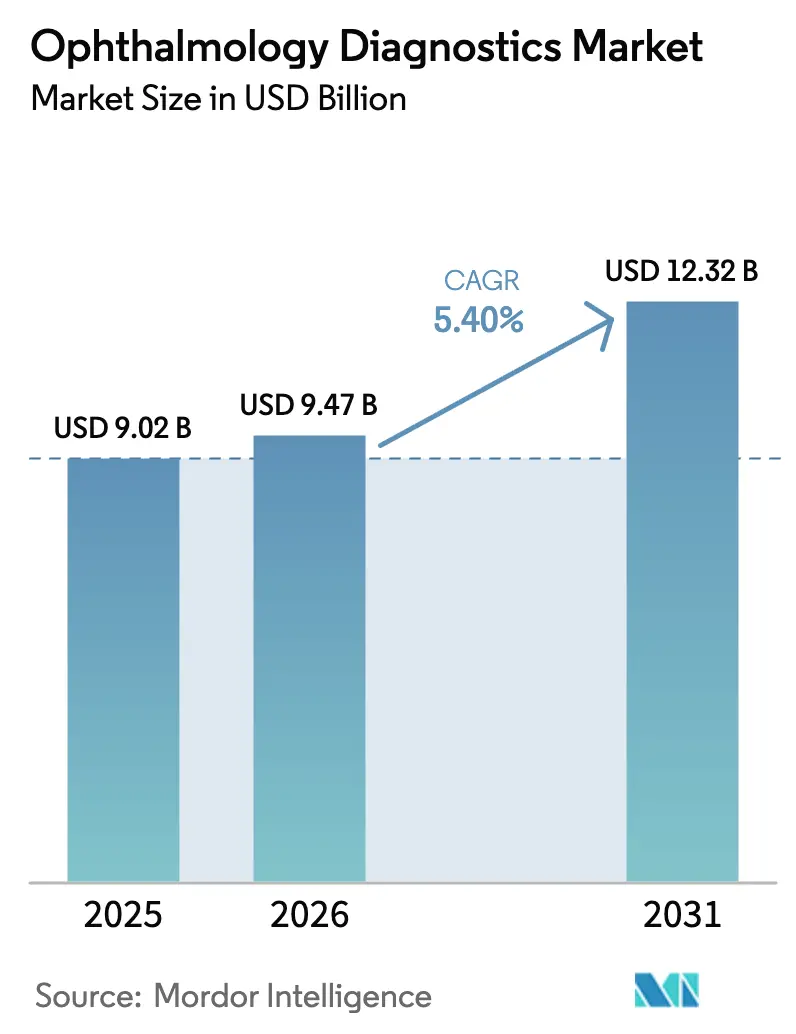

| Market Size (2026) | USD 9.47 Billion |

| Market Size (2031) | USD 12.32 Billion |

| Growth Rate (2026 - 2031) | 5.40% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ophthalmology Diagnostics Market Analysis by Mordor Intelligence

The Ophthalmology Diagnostics Market size is expected to grow from USD 9.02 billion in 2025 to USD 9.47 billion in 2026 and is forecast to reach USD 12.32 billion by 2031 at 5.40% CAGR over 2026-2031.

The adoption of autonomous artificial-intelligence screening in primary care, rising diabetes prevalence, and the private-equity-backed migration of diagnostic capital from hospitals to specialty clinics collectively push unit volumes upward. Momentum is amplified when payers reimburse AI screening for glaucoma, age-related macular degeneration, and diabetic retinopathy, a coverage inflection estimated to lift annual procedure growth by 1.2 percentage points. Near-term demand is strongest for ultra-widefield fundus cameras that embed algorithmic triage, reducing specialist review time by 70%. At the same time, swept-source optical coherence tomography (OCT) platforms defend the premium end of the product mix. Competitive behaviour is shifting toward subscription software models that reduce upfront capital outlay to one-tenth of that of traditional devices, eroding incumbents’ margin headroom. Reimbursement timelines, data-privacy mandates, and technician shortages remain structural frictions, yet are partially offset by handheld imaging tools and tele-ophthalmology networks that redistribute workload.

Key Report Takeaways

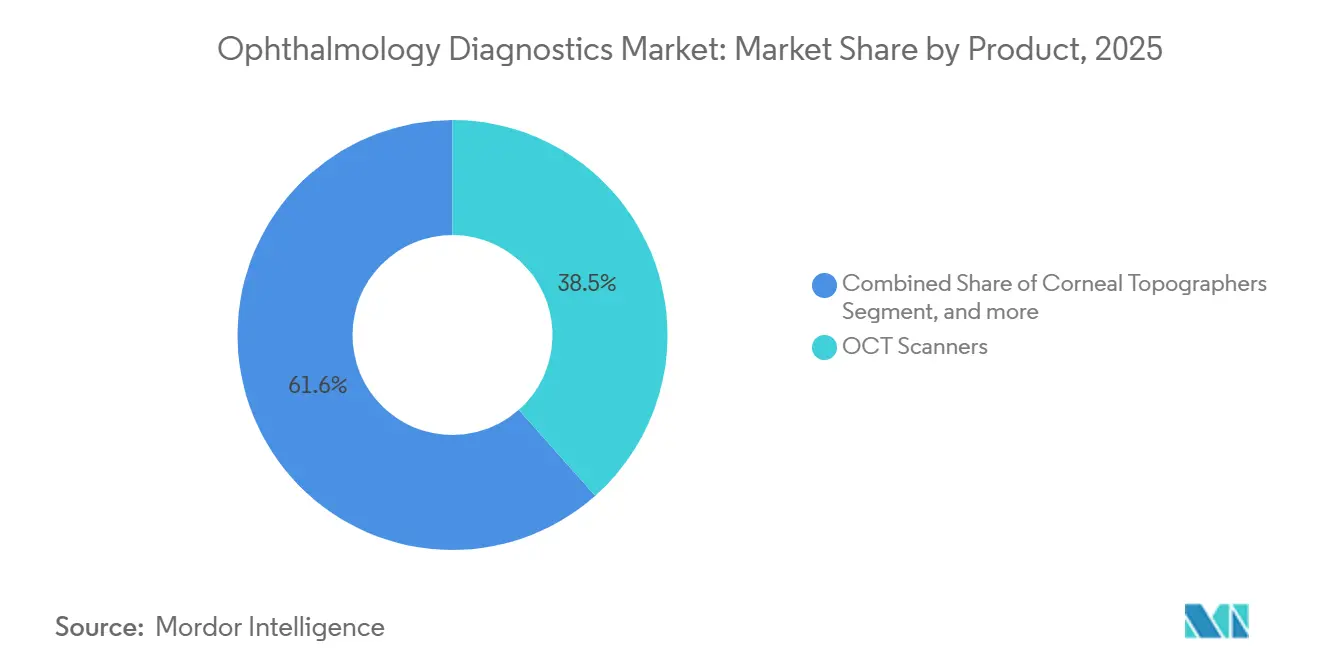

- By product, OCT scanners accounted for 38.45% of the revenue in 2025. In contrast, fundus cameras are projected to grow at the fastest rate, with a 7.58% CAGR through 2031, reflecting divergent price points and primary care adoption dynamics.

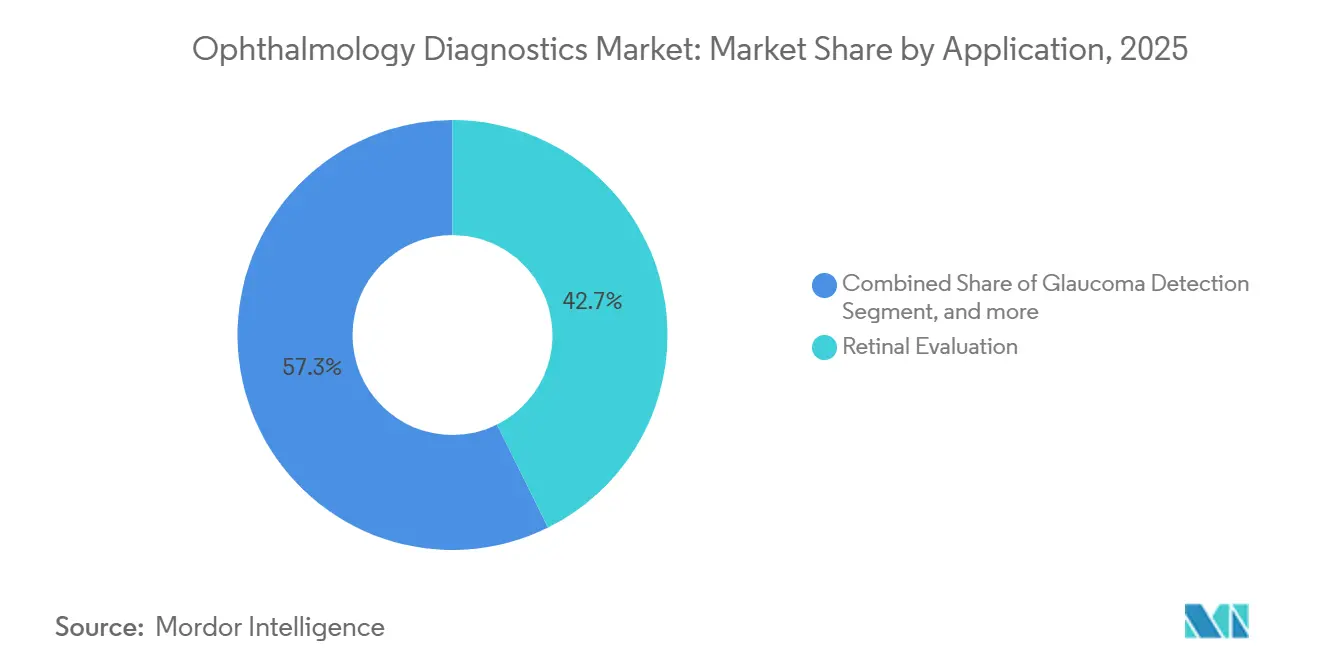

- By application, retinal evaluation led with a 42.67% revenue share in 2025, while surgical evaluation is advancing at a 7.34% CAGR, driven by the rebound in cataract surgery and gains in swept-source biometry accuracy.

- By end-user, hospitals retained a 57.54% share in 2025; however, specialty clinics showed the highest growth rate at an 8.43% CAGR, as group-practice consolidators negotiated discounts of 15–25% on equipment.

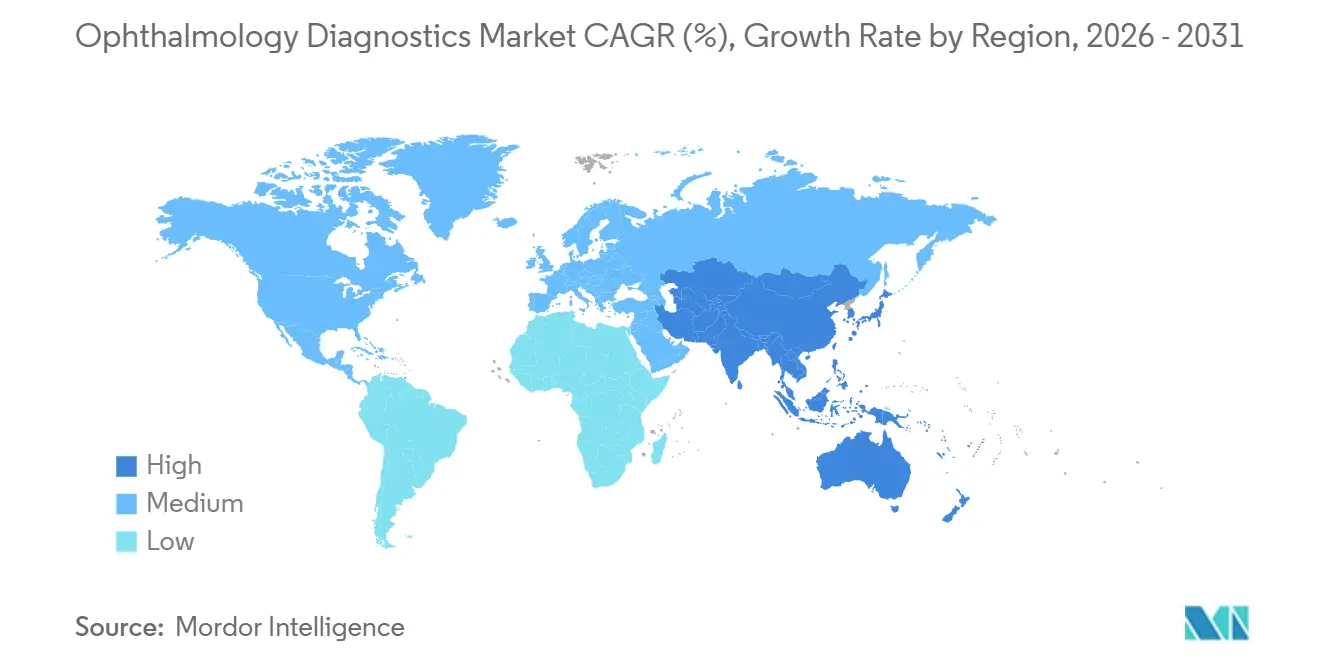

- By geography, North America commanded 41.87% of the 2025 revenue, and the Asia-Pacific region is forecast to post the fastest 6.43% CAGR through 2031, driven by the establishment of nationwide tele-ophthalmology hubs in India and the implementation of mandatory annual eye exams in China.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ophthalmology Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of eye diseases due to aging population and diabetes | 1.80% | Global, with highest impact in Asia-Pacific and North America | Long term (≥ 4 years) |

| Growing adoption of OCT and AI-integrated imaging modalities | 1.50% | North America & Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Favorable government programs for vision care | 0.90% | North America, Europe, Asia-Pacific (India, China) | Medium term (2-4 years) |

| Embedding ophthalmic diagnostics into point-of-care primary clinics via compact handheld devices | 0.70% | Global, with early gains in North America and urban Asia | Short term (≤ 2 years) |

| Integration of teleophthalmology platforms with cloud-based diagnostic analytics | 0.60% | North America, Europe, select Asia-Pacific markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Eye Diseases Due to Aging Population and Diabetes

Diabetic retinopathy now affects 103 million adults worldwide, a 24% rise since 2021, while age-related macular degeneration cases are projected to reach 288 million by 2040: both trends multiply diagnostic workloads. American Diabetes Association guideline revisions in 2025 shortened screening intervals from 24 to 12 months, effectively doubling test frequency[1]American Diabetes Association, “Standards of Care 2025,” diabetes.org. Cataract procedures rebounded to 28 million in 2025, increasing demand for biometry and corneal topography equipment. India budgeted INR 12 billion (USD 144 million) to equip 3,000 primary centers with fundus cameras and autorefractors, illustrating government pull-through. The ophthalmology workforce deficit of 1 specialist per 17,000 population amplifies the imperative for automated diagnostics.

Growing Adoption of OCT and AI-Integrated Imaging Modalities

Swept-source OCT shipments expanded 18% year-over-year in 2025, fueled by deeper penetration and faster scan speeds that improve visualization of choroidal layers. Seven AI diagnostic algorithms earned U.S. FDA De Novo or 510(k) clearances between 2024 and 2025, including Notal Vision’s home-use OCT system, evidencing regulatory momentum. Cloud services, such as EyePACS, processed 1.2 million images in 2025, returning 92% of expected results within 24 hours and reducing unnecessary referrals. Reimbursement gaps outside the United States persist, with only four EU nations covering autonomous diabetic retinopathy screening as of 2025. IT integration costs per hospital run USD 50,000–150,000, tempering implementation velocity.

Favorable Government Programs for Vision Care

CPT 92229, introduced by Medicare in 2024 at USD 60 per bilateral AI screen, boosted U.S. primary-care test volume by 40% within 12 months. India’s Ayushman Bharat Digital Mission aims to embed tele-ophthalmology into 150,000 health and wellness centers by the end of 2025, reducing rural travel costs by INR 800 per visit. China’s Healthy China 2030 blueprint mandates annual eye exams for citizens over 60, expected to add 140 million diagnostic encounters per year after 2027. The European Union Medical Device Regulation harmonized CE-marking, but increased compliance spending for manufacturers, ultimately accelerating pan-EU AI launches. Saudi Arabia’s Vision 2030 funded 47 new vision centers outfitted with OCT and fundus cameras, widening access in underserved provinces.

Embedding Ophthalmic Diagnostics into Point-of-Care Primary Clinics via Handheld Devices

Handheld fundus cameras under 500 grams and priced below USD 10,000 enable on-site retinal imaging within routine primary-care visits. Optomed’s Aurora AEYE achieved 1,200 U.S. deployments by December 2025, winning 8% of diabetic-retinopathy screens formerly managed by tabletop devices. Smartphone-based Fundus-on-Phone scanned 2.3 million patients across India, Kenya, and Brazil in 2025, showing 94% concordance with standard fundus photography. Medicare reimburses handheld photography at 85% of tabletop rates, leaving a USD 12 per-exam gap that slows adoption in fee-for-service sites. Home OCT systems reduce clinic visits by 60% for macular degeneration monitoring, underscoring the potential for decentralization. AI Optics’ Sentinel camera runs for 8 hours on battery and meets the American Academy of Ophthalmology's imaging standards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of advanced imaging systems | -0.8% | Global, most acute in emerging markets and small practices | Medium term (2-4 years) |

| Shortage of skilled ophthalmologists and technicians | -0.6% | Global, severe in rural areas and low-income countries | Long term (≥ 4 years) |

| Data privacy concerns hindering cloud deployment of diagnostic images | -0.3% | Europe, North America, select Asia-Pacific markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Advanced Imaging Systems

Swept-source OCT units list at USD 120,000–180,000, which exceeds the capital expenditure (cap-ex) envelope of many stand-alone practices whose annual equipment budgets typically sit below USD 200,000. Ultra-widefield cameras cost USD 80,000–150,000 and require 800–1,200 studies per year for a three-year payback at Medicare tariff levels. Leasing carries an interest rate of 6–8%, adding USD 15,000–25,000 to the cost of five-year ownership. Import tariffs of 15–30% inflate device prices in India, Brazil, and South Africa, while interest rates exceed 12%. National tenders move slowly; India delivered only 2,100 of 5,000 ordered cameras by December 2025 due to procurement delays.

Shortage of Skilled Ophthalmologists and Technicians

The global ratio is 1 ophthalmologist per 17,000 population, well below the WHO target of 1 per 10,000. U.S. practices reported a 25% vacancy rate for ophthalmic technicians in 2025, which elevated labor costs and led to throughput constraints. Residency slots have not expanded since 2020, resulting in the graduation of 475 physicians annually, despite a 12% rise in demand for cataract and retina services. Technician programs require 18–24 months and tuition ranging from USD 5,000 to USD 8,000, deterring entrants compared to faster medical-assistant tracks. Autonomous AI removes grader workload from 85% of regular retinopathy exams, but scope-of-practice laws still limit optometrists to 22 U.S. states.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: OCT Leadership Meets Fundus-Camera Acceleration

OCT scanners generated 38.45% of the revenue in 2025, underscoring their dominance in retina and glaucoma imaging, while fundus cameras posted the fastest 7.58% CAGR from 2026 to 2031. The Ophthalmology Diagnostics market size for fundus cameras is projected to expand as primary care practices deploy ultra-widefield devices under CPT code 92229 reimbursement. Ultra-widefield platforms capture 200-degree views in a single shot, easing exams in pediatric and cognitively challenged cohorts. Corneal-topography systems priced at USD 40,000–60,000 are gaining ground in refractive planning, although adoption tends to skew toward high-volume laser centers. Digital replacements are outpacing handheld ophthalmoscopes priced below USD 1,000; Welch Allyn reported a 12%-unit decline in 2025. Swept-source OCT, led by Topcon Triton and Zeiss PLEX Elite, captured 60% of 2025 installations by offering 100,000 A-scans per second, compared to 70,000 for spectral-domain peers, thereby trimming scan times and enhancing choroidal visualization. Regulatory hurdles are moderate; most systems can be cleared under FDA 510(k) pathways, allowing for 12–18-month development cycles.

Fundus-camera growth outpaces other categories because unit prices (USD 15,000–80,000) align with primary-care budgets. Ultra-widefield imaging enables referral-quality screening without dilation, and AI integration facilitates automated triage, reducing specialist workload by 70%. Camera makers now bundle software-as-a-service, shifting costs from capital expenditure to operating expenditure. Competitive gaps persist: smartphone attachments match 94% diagnostic concordance yet still face partial reimbursement. The product mix is expanding to include multimodal devices that combine OCT, OCT-A, and fundus photography, as evident in Heidelberg Engineering’s Spectralis platform, which captured 35% of European tertiary-center spend in 2025.

By Application: Retinal Dominance, Surgical Momentum

Retinal evaluation accounted for 42.67% of the 2025 revenue from mandatory screening for diabetic retinopathy and age-related macular degeneration. The Ophthalmology Diagnostics market share linked to surgical assessment is increasing the fastest, growing at a 7.34% CAGR as cataract procedures surpass 28 million annually and surgeons rely on swept-source biometry with accuracy of 10 microns[2]European Society of Cataract and Refractive Surgeons, “Clinical Survey 2025,” escrs.org. Barrett Universal II and other fourth-generation formulas, embedded in modern biometers, have improved IOL prediction in post-LASIK eyes, now accounting for 18% of developed-market cataract cases. OCT-angiography straddles application lines, helping detect early glaucoma via optic-nerve perfusion mapping, thus broadening its TAM. Glaucoma detection expanded by 6.1% in 2025, as guidelines encouraged earlier intervention for intraocular pressures above 21 mmHg. Autorefractor-based refraction assessment grows in parallel with a 4.2% uptick in eye-exam volumes as telehealth retailers scale. Corneal topography and pachymetry remain niche, but they rose 5.8% in the Asia-Pacific region as LASIK volumes climbed 14% during 2025.

By End-User: Hospital Core, Specialty-Clinic Acceleration

Hospitals held 57.54% of the revenue in 2025, reflecting the entrenched presence of tertiary imaging for complex cases. However, specialty clinics are expected to grow at an 8.43% CAGR to 2031, as private-equity platforms assemble groups with 200-plus locations and command double-digit vendor discounts. EyeCare Partners deployed 120 OCTs and 200 fundus cameras in 2025, leveraging its network scale. Ambulatory surgery centers performed 40% of U.S. cataract surgeries in 2025, facilitating the migration of biometry and corneal topography outside hospital walls. Medicare site-neutral payment cuts reduced hospital reimbursement by 15% for diagnostic imaging, accelerating the shift toward outpatient care. Optical retail chains and mobile vans expanded 6.2% after Walmart and Costco installed digital phoropters to ease throughput. Tele-ophthalmology extended reach: Federally qualified centers deployed 1,200 handheld cameras, capturing 8% of the diabetic retinopathy screening volume.

Geography Analysis

North America generated 41.87% of the revenue in 2025, anchored by CPT 92229 reimbursement, which spiked primary-care screens by 40% in the first year. Ophthalmologist saturation in urban areas, combined with negotiated rate cuts of 8–12% by Medicare Advantage plans, tempers growth. Private-equity consolidation now covers 60% of U.S. practices with five or more physicians, aggregating purchasing leverage and reducing equipment prices by 15–25%. Canada lags in advanced imaging; only four provinces reimburse OCT-angiography for diabetic macular edema.

Asia-Pacific is poised for a 6.43% CAGR, the swiftest regional climb, with India scaling tele-ophthalmology to 500 districts by 2027 and China mandating annual exams for seniors under Healthy China 2030[3]National Health Commission of China, “Healthy China 2030 Vision Care Roadmap,” nhc.gov.cn. India added 2,100 fundus cameras in 2025, yet still reaches only 15% of its primary-care targets. Japan’s myopia prevalence (40% of adults) drives swept-source OCT adoption, now 55% of new installations. Domestic Chinese vendors priced 40% below multinationals, winning a 22% share of the fundus-camera market, although false-negative rates are 8% higher in validation studies.

Europe contributed 28% of 2025 revenue but faces GDPR-driven cloud hesitancy, which is pushing 40% of practices toward on-premise data stores and increasing IT spend. Germany and France reimburse OCT-angiography nationally; however, southern markets struggle with budget limits. The United Kingdom’s NHS placed 180 OCTs in community optometry sites, cutting glaucoma referral wait times from 12 to 3 weeks.

The Middle East & Africa posted 5.8% growth, driven by Saudi Vision 2030 funding for 47 vision centers in 2025. Sub-Saharan Africa still supports only 1 ophthalmologist per 250,000 people; smartphone-based screening by Peek Vision covered 400,000 patients in 2025. South America advanced 5.2%; Brazil tendered 1,200 cameras, but import tariffs and delivery delays curbed deployment.

Competitive Landscape

The ophthalmology diagnostics industry exhibits moderate concentration, with the five largest manufacturers—Zeiss Meditec, Topcon, Heidelberg Engineering, Canon, and Nidek—collectively accounting for 55% of the revenue in 2025. Patent thickets surrounding swept-source OCT and OCT angiography keep barriers high; Zeiss filed 47 imaging patents between 2024 and 2025. Heidelberg’s multimodal Spectralis platform won 35% European tertiary-center OCT bids in 2025 by combining OCT, OCT-A, and fundus photography. Alcon’s partnership with Visionix bundles autorefractors into surgical ecosystems, illustrating vertical bundling. Notal Vision commercialized home OCT at USD 4,800, disrupting in-clinic models by undercutting capital expenditures by 70%. Eyenuk processed 800,000 AI diabetic-retinopathy exams for USD 15 per test, one-quarter the cost of manual review, and won four Medicare Advantage contracts. Smartphone attachments, such as Fundus-on-Phone and Sentinel, achieve 94% diagnostic concordance yet face reimbursement ceilings. Traditional ophthalmoscope suppliers lost traction; Welch Allyn reported a 12%-unit decline in 2025. Standards bodies stiffen interoperability demands; DICOM’s 2024 OCT-A specification is now a gating factor in hospital IT tenders.

Ophthalmology Diagnostics Industry Leaders

Topcon Corporation

Ziemer Ophthalmic Systems AG

Alcon Inc.

NIDEK CO., LTD

Canon Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: OpZira, Inc., a forward-thinking ophthalmic medical device company founded on a legacy of research excellence announced its official formation. OpZira is dedicated to delivering innovative technologies that enhance the detection and monitoring of ocular disease, empowering clinicians with advanced diagnostic tools.

- July 2025: Topcon Healthcare, Inc., a global leader in digital health and ocular data solutions acquired Intelligent Retinal Imaging Systems (IRIS), the U.S.-based pioneer in cloud-based retinal screening technology. This strategic acquisition marks a significant step in enhancing Topcon Healthcare’s presence in primary care, reinforcing its commitment to early disease detection through connected, data-driven care.

- April 2024: Optomed Aurora AEYE handheld fundus camera earned FDA clearance and reached 1,200 U.S. primary-care clinics by year-end.

Global Ophthalmology Diagnostics Market Report Scope

According to the report's scope, ophthalmology diagnostics refer to the equipment used to diagnose and monitor various ophthalmic diseases, including cataracts, glaucoma, color blindness, and refractive errors. Ophthalmic diagnostic and monitoring devices encompass a wide range of equipment, including fundus cameras, ophthalmoscopes, refractors, and corneal topography systems, among others. These help ophthalmologists to identify the power of Intraocular Lenses (IOLs) and examine the visual field, which has a considerable demand to prevent visual impairment and loss of vision.

The Ophthalmology Diagnostics Market Report is Segmented by Product (Corneal Topographers, Fundus Cameras, Ophthalmoscopes, OCT Scanners, Retinoscopes, Refractors, and Other Products), Application (Retinal Evaluation, Glaucoma Detection, Surgical Evaluation, Refraction Assessment, and Other Applications), End-User (Hospitals, Specialty Clinics, and Other End-Users), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Corneal Topographers |

| Fundus Cameras |

| Ophthalmoscopes |

| OCT Scanners |

| Retinoscopes |

| Refractors |

| Other Products |

| Retinal Evaluation |

| Glaucoma Detection |

| Surgical Evaluation |

| Refraction Assessment |

| Other Applications |

| Hospitals |

| Specialty Clinics |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Corneal Topographers | |

| Fundus Cameras | ||

| Ophthalmoscopes | ||

| OCT Scanners | ||

| Retinoscopes | ||

| Refractors | ||

| Other Products | ||

| By Application | Retinal Evaluation | |

| Glaucoma Detection | ||

| Surgical Evaluation | ||

| Refraction Assessment | ||

| Other Applications | ||

| By End-User | Hospitals | |

| Specialty Clinics | ||

| Other End-Users | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the forecast value of the Ophthalmology Diagnostics market by 2031?

The ophthalmology diagnostics market is projected to reach USD 12.32 billion by 2031.

Which product category is expected to grow the fastest through 2031?

Fundus cameras, especially ultra-widefield models with integrated AI, are poised for the fastest 7.58% CAGR.

Which region shows the highest growth outlook?

Asia-Pacific is forecast to expand at a 6.43% CAGR driven by India's tele-ophthalmology hubs and China's mandatory senior eye exams.

How do handheld fundus cameras impact primary-care screening?

Handheld cameras allow in-office imaging, trimming diabetic-retinopathy referral time from weeks to minutes and capturing 8% of U.S. screening volume in 2025.

What is the major restraint limiting emerging-market adoption?

High capital cost of advanced OCT and fundus systems, compounded by 15-30% import tariffs and scarce low-interest financing options, slows uptake.

Which companies dominate swept-source OCT?

Zeiss, Topcon, and Heidelberg Engineering maintain leadership via patent portfolios and integrated multimodal platforms.

Page last updated on: