Healthcare Video Conferencing Solutions Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

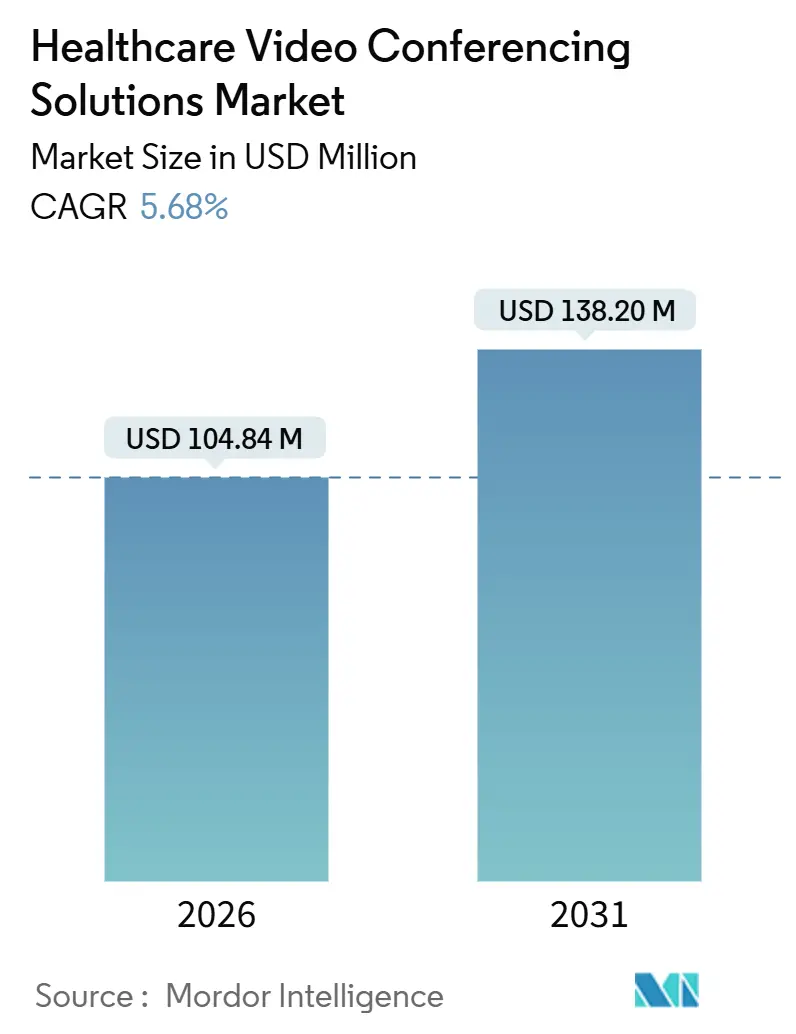

| Market Size (2026) | USD 104.84 Million |

| Market Size (2031) | USD 138.20 Million |

| Growth Rate (2026 - 2031) | 5.68% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Video Conferencing Solutions Market Analysis by Mordor Intelligence

The Healthcare Video Conferencing Solutions Market size is estimated at USD 104.84 million in 2026, and is expected to reach USD 138.20 million by 2031, at a CAGR of 5.68% during the forecast period (2026-2031).

This advance signals the transition from emergency pandemic deployment to deliberate, workflow-oriented adoption. Demand is sustained by telehealth flexibilities that extend audio-only reimbursement and site-of-service waivers through January 2026, by the rising need for Fast Healthcare Interoperability Resources (FHIR) compliance, and by hospital investments in low-latency 5G backbones that improve time-critical care. Competitive focus has shifted to deep electronic-health-record (EHR) linkage, ambient documentation, and hybrid-cloud data governance as health systems weigh capital efficiency against regional privacy rules. Vendors that embed artificial-intelligence (AI) scribes, remote-patient-monitoring dashboards, and single sign-on APIs are winning share while generic meeting platforms compress prices for undifferentiated services. Simultaneously, broadband grants and private 5G rollouts widen addressable reach, although rural fiber gaps, physician video fatigue, and unsettled reimbursement rules moderate the growth cadence of the Healthcare Video Conferencing Solutions market.

Key Report Takeaways

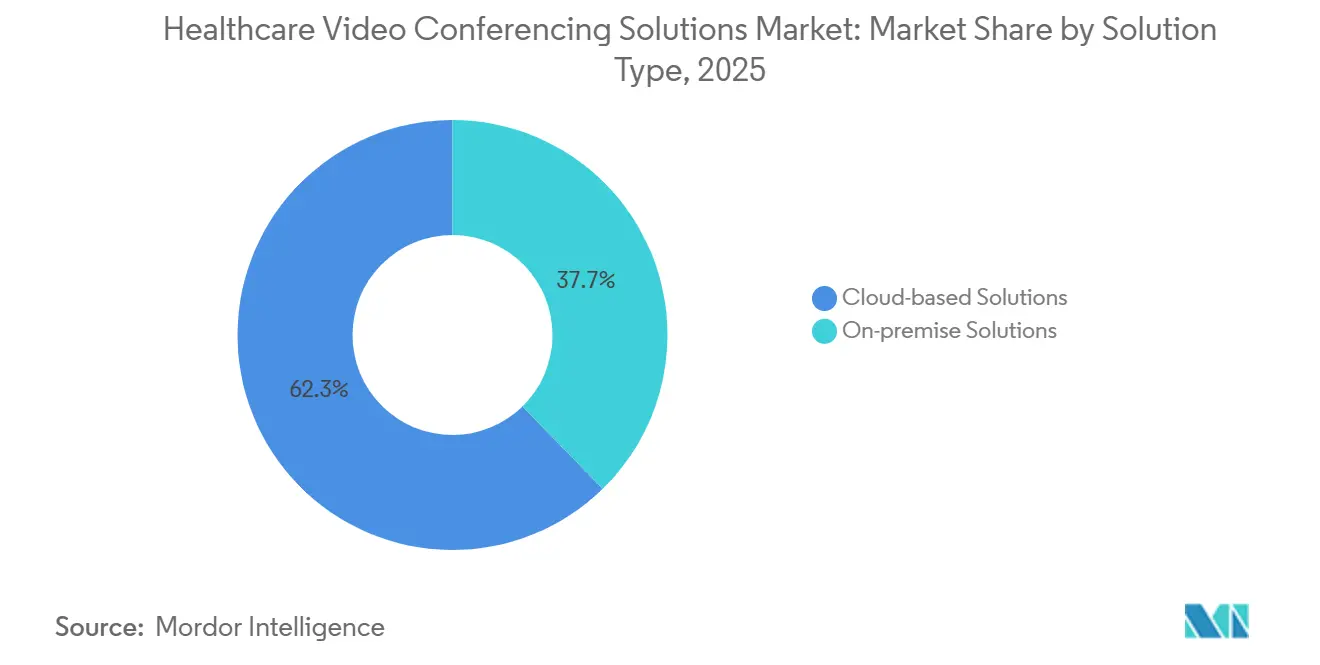

- By solution type, cloud-based offerings held 62.32% revenue share in 2025, while hybrid cloud is projected to grow at a 9.76% CAGR through 2031.

- By deployment model, public cloud accounted for 54.13% share in 2025, whereas hybrid configurations are forecast to expand at a 9.76% CAGR to 2031.

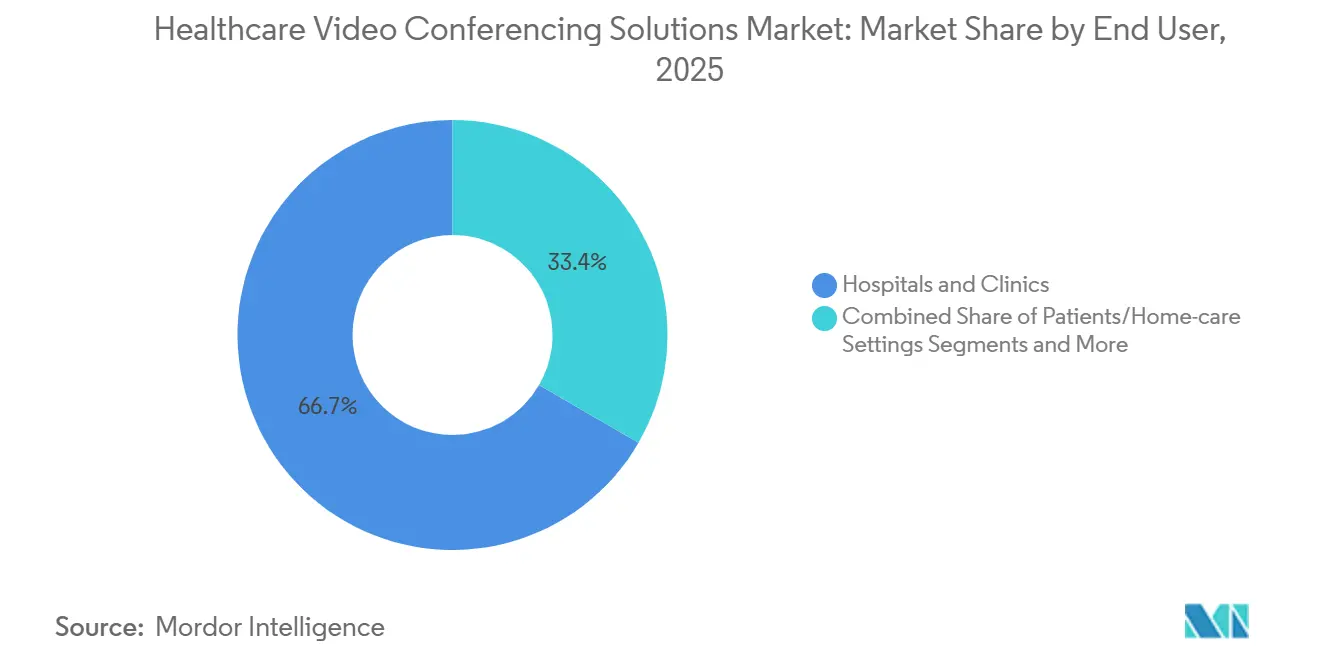

- By end user, hospitals and clinics led with 66.65% revenue share in 2025, and patient-facing platforms are advancing at an 8.42% CAGR to 2031.

- By application, tele-consultation commanded 44.43% share in 2025, while remote patient monitoring is rising at a 9.43% CAGR through 2031.

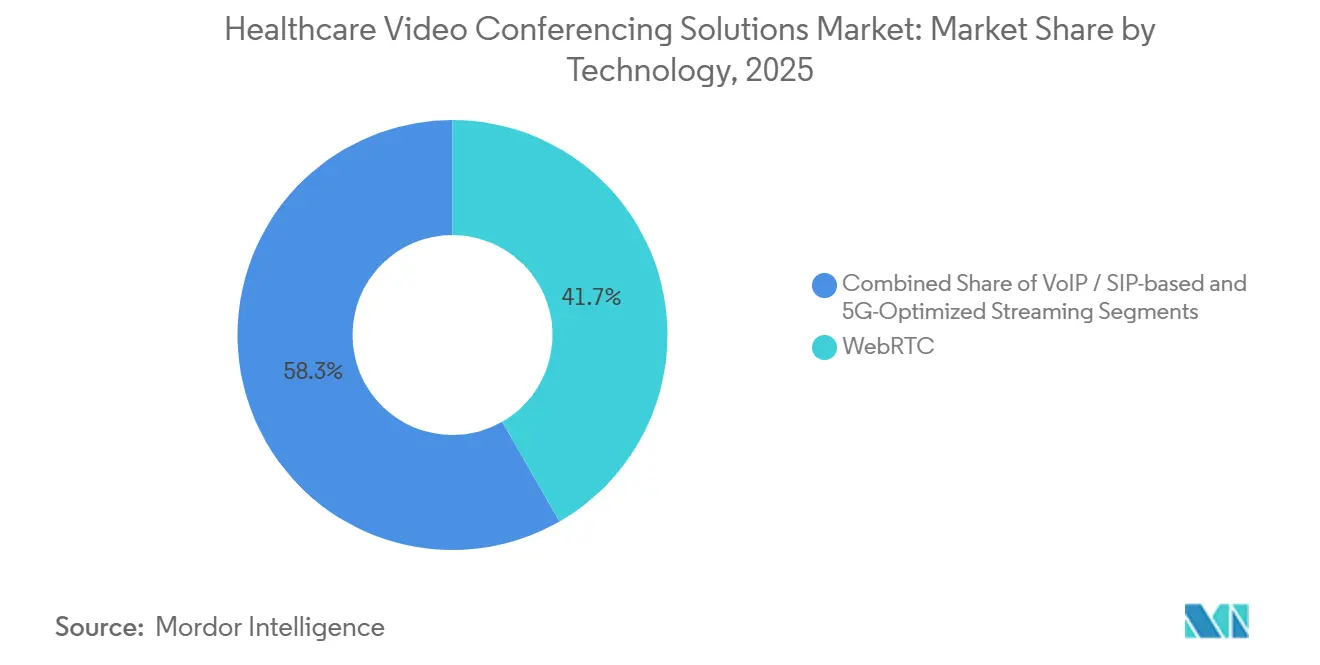

- By technology stack, WebRTC captured 41.72% share in 2025, whereas 5G-optimized streaming is slated for a 7.36% CAGR to 2031.

- By geography, North America led with 33.23% revenue share in 2025, and Asia-Pacific is expected to expand at a 7.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Healthcare Video Conferencing Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-COVID Normalization & Supportive Regulation | +1.2% | North America, Europe | Medium term (2-4 years) |

| Integration with EHR & Clinical Workflows | +1.4% | Global urban centers | Long term (≥ 4 years) |

| Cloud Scalability & Cost Advantages | +0.9% | Global, strongest in emerging Asia-Pacific | Short term (≤ 2 years) |

| AI-Driven Quality & Documentation Analytics | +1.1% | North America, Europe | Medium term (2-4 years) |

| 5G-Enabled Mobile Tele-Consults | +0.7% | United States, China, Japan, South Korea | Long term (≥ 4 years) |

| Enterprise Platform Standardization | +0.8% | North America, Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Post-COVID Normalization & Supportive Regulation

Temporary Medicare policies that maintain payment parity for virtual visits and waive geographic restrictions keep adoption levels steady yet inject budgeting risk because the rules expire in January 2026.[1]Centers for Medicare & Medicaid Services, “Calendar Year 2024 Physician Fee Schedule Final Rule,” cms.gov Health-system leaders therefore proceed with modular investments that can scale up or wind down. Enforcement actions, such as the USD 3.7 million Cerebral settlement for tracking-pixel violations, elevate compliance scrutiny and push vendors toward privacy-first architectures.[2]U.S. Department of Health and Human Services, “Settlement with Cerebral Over HIPAA Breaches,” hhs.gov Outside the United States, China now allows cross-provincial consultations, broadening specialist reach, while India links Ayushman Bharat accounts to kiosk networks that channel video visits into primary-care routines. These policy moves collectively lift baseline usage across the Healthcare Video Conferencing Solutions market.

Integration with EHR & Clinical Workflows

The 2024 Cures Act Final Rule obliges video platforms to surface FHIR APIs for patient context, medications, and billing codes, or risk exclusion from Epic and Cerner environments that cover 70% of U.S. hospital beds.[3]Office of the National Coordinator for Health Information Technology, “FHIR Fact Sheets,” healthit.gov Civil penalties of up to USD 1 million per information-blocking violation encourage rapid compliance. A 2024 KLAS survey showed 42% of health systems now prefer single-vendor ecosystems tied to collaboration suites, compressing the shelf life of stand-alone video tools. The Veterans Health Administration reports that embedded video reduced no-show rates by 18%, demonstrating the clinical gain from unified workflows. These shifts intensify platform stickiness and support long-term expansion of the Healthcare Video Conferencing Solutions market.

Cloud Scalability & Cost Advantages

Subscription pricing below USD 50 per clinician per month democratizes access for small practices while HIPAA-ready public clouds remove capital hurdles. Health systems in Latin America and Southeast Asia adopt web-based portals that run on commodity laptops, cutting deployment time to days. Hybrid designs store recordings on-premises to satisfy provincial data residence rules yet stream live sessions through cloud edge nodes, balancing compliance and latency. Planned Health Data Space rules in the European Union will further encourage localized storage, fuelling hybrid-cloud uptake and underpinning near-term growth of the Healthcare Video Conferencing Solutions market.

AI-Driven Quality & Documentation Analytics

Ambient AI scribes deployed by Kaiser Permanente trimmed documentation time by 22%, which freed 1.2 additional appointment slots per day per physician. Mass General Brigham reports near-complete note accuracy, although United Kingdom guidance mandates human review before entries reach the legal record, slowing throughput. Real-time sentiment analysis flags patient distress, yet Stanford researchers warn of racial bias in emotion detection, compelling vendors to retrain models on diverse datasets. Absence of formal FDA classification leaves liability lines blurry, but early productivity gains bolster the Healthcare Video Conferencing Solutions market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Security & HIPAA-Compliance Complexity | −0.6% | North America, European Union | Short term (≤ 2 years) |

| Broadband & Digital-Literacy Gaps | −0.5% | Rural North America, rural Asia-Pacific, Africa | Long term (≥ 4 years) |

| Clinician Video-Fatigue & Burnout | −0.4% | North America, Western Europe | Medium term (2-4 years) |

| Commoditization by Generic Platforms | −0.3% | Worldwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data-Security & HIPAA-Compliance Complexity

The U.S. Office for Civil Rights recorded 14 telehealth breaches in 2024 and fined BetterHelp USD 7.8 million for sharing metadata with advertising partners, underlining the cost of non-compliance. The European General Data Protection Regulation threatens penalties of up to 4% of global turnover for cross-border mishandling, pushing vendors to add regional data centers. An Inspector General audit found 23% of Medicare Advantage plans employed non-compliant tools during the pandemic, exposing 1.2 million beneficiaries. These incidents elevate procurement caution and soften near-term gains in the Healthcare Video Conferencing Solutions market.

Broadband & Digital-Literacy Gaps in Rural Areas

Although the FCC’s Healthcare Connect Fund granted USD 657 million in 2024, 19% of U.S. rural hospitals still lack fiber lines that sustain 1080p streams. Service interruptions, mobile-data caps, and limited device fluency among seniors constrain video usage among those who might benefit most. Pew researchers note that 24% of rural adults are without home broadband, while NIH studies show 31% of Medicare beneficiaries older than 75 require caregiver help to complete a video visit. Similar bandwidth gaps persist in rural India and sub-Saharan Africa, braking adoption across the Healthcare Video Conferencing Solutions market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Hybrid Design Marries Compliance and Scale

Cloud offerings held 62.32% of Healthcare Video Conferencing Solutions market share in 2025, propelled by subscription economics that shed capital expenditure. The hybrid cohort, however, is predicted to expand at a 9.25% CAGR as hospitals split storage and live traffic to align with state data-residency laws and meet sub-200-millisecond latency targets for tele-stroke protocols. Cisco’s decision to retire on-premise Webex appliances by 2027 adds urgency for migration planning.

Hybrid configurations cache imaging files locally and process AI analytics in the cloud, lowering round-trip time by 34% versus public-cloud-only setups, according to a 2024 Journal of Telemedicine and Telecare study. As European Health Data Space rules emerge, hybrid frameworks will underpin regional sovereignty while underpinning the broader Healthcare Video Conferencing Solutions market.

By Deployment Model: Private Cloud Protects Sensitive Missions

Public cloud represented 54.13% of 2025 revenue, yet hybrid implementations are on track for a 9.76% CAGR because Veterans Affairs, defense clinics, and academic centers retain on-premise storage for classified information. The Healthcare Video Conferencing Solutions market size for private cloud remains modest but stable in these regulated enclaves. Cost curves shift in favor of public hyperscalers as Amazon Web Services cut sector prices by 18% in 2024, yet FedRAMP High restrictions preserve a niche for private hosts.

CommonSpirit’s 2024 rollout proved that hybrid architecture can satisfy California privacy statutes while exploiting Azure load balancing. HIMSS guidelines now recommend hybrid patterns for multi-state networks, further distributing uptake across the Healthcare Video Conferencing Solutions market.

By End User: Home-Care Growth Outpaces Facility Use

Hospitals and clinics generated 66.65% of 2025 revenue, but patient-facing channels are forecast to grow 8.42% annually to 2031, encouraged by CMS codes that reimburse USD 51.14 for remote-monitoring setup and USD 62.06 per monthly review. Kaiser Permanente reports 18% lower no-show rates for video visits compared with in-person appointments, highlighting convenience gains.

Veterans Affairs logged 2.3 million home-originated appointments in 2024, confirming that consumer endpoints are shifting volumes. Physician practices lean on freemium video portals to manage cost, while payers pilot video prior-authorization flows that shrink approval cycles by 68%. These factors collectively reinforce sustained expansion of the Healthcare Video Conferencing Solutions market.

By Application: Monitoring Converges with Video Visits

Tele-consultation dominated with 44.43% share in 2025, yet remote patient monitoring is growing at 9.43% CAGR as platforms merge live video and biometric dashboards. The Healthcare Video Conferencing Solutions market size for RPM is widening because new CPT code 99458 reimburses an extra USD 50.64 for prolonged review, making video-supported data checks financially attractive.

Kaiser Permanente’s hypertension program enrolled 180,000 members in 2024, reducing emergency visits by 14% and saving USD 42 million, evidence that integrated video and device data yield tangible returns. Education use cases soften as academic programs return to campus, and administrative collaboration continues to split between healthcare-specific portals and generic suites.

By Technology Stack: 5G Adds Ultralow Latency

WebRTC delivered 41.72% of 2025 revenue thanks to browser-based simplicity. Hospital investment in 5G aims at latency-sensitive ambulance handoffs, growing that segment at 7.36% CAGR. The Healthcare Video Conferencing Solutions market size for 5G streaming is supported by Verizon’s private networks that cut stroke door-to-needle times by 8 minutes.

China Mobile’s rural 5G ultrasound pilots and the FCC’s 100 MHz spectrum allocation encourage similar use cases, although USD 1.5 million deployment costs restrict adoption to well-funded centers. VoIP and SIP hardware faces retirement as software-defined WebRTC continues to undercut hardware gateways.

Geography Analysis

North America produced 33.23% of 2025 revenue and is expected to track a 5.68% CAGR to 2031. Medicare’s temporary parity rules, HIPAA enforcement, and RPM billing codes keep demand steady, yet uncertainty over post-2026 reimbursement caps longer contracts. Canada maintains patchwork parity rules by province, and Mexico’s national platform reaches 60 million citizens but remains urban-centric.

Asia-Pacific will post a 7.11% CAGR as China enables cross-province consultation and India scales 680 million Ayushman Bharat accounts linked to kiosk networks. Japan okayed online prescription fulfillment, and South Korea subsidized island 5G, both moves that spur regional volumes. Australia added 11 Medicare telehealth items in 2024, supporting uptake across remote territories.

In Europe, Germany benefits from statutory reimbursement, and the United Kingdom completed 18 million virtual GP visits in 2024. Data-residency clauses, however, force vendors to operate fragmented clouds, inflating compliance cost. Anticipated Health Data Space rules could harmonize infrastructure but require rebuilds.

Competitive Landscape

The Healthcare Video Conferencing Solutions market displays moderate concentration. Zoom and Microsoft capture hospital information-technology budgets through enterprise bundles, driving down per-seat prices by nearly 40%. Cisco pursues low-latency encoding patents, while Teladoc integrates chronic-disease analytics after acquiring Livongo. Doxy.me and Caregility thrive in specialist niches—small practice freemium models and intensive-care-unit carts, respectively.

Interoperability remains an adoption filter; only 28% of suppliers met HIMSS-recommended API standards in 2024. Investors direct capital toward ambient AI scribes and hybrid-cloud compliance modules, areas where new entrants can still differentiate. Current dynamics suggest steady vendor consolidation as health systems standardize on unified collaboration environments.

Healthcare Video Conferencing Solutions Industry Leaders

Zoom Video Communications Inc.

Teladoc Health Inc.

Doxy.me

Amwell (American Well)

Cisco Systems Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Tencent and Bupa Hong Kong introduced palm-verification check-in for clinical visits, improving hygiene and throughput.

- December 2025: AONMeetings announced a HIPAA-ready browser-first platform for the Indian market with localized pricing.

- November 2025: Teladoc and Amazon Web Services deployed hybrid-cloud Outposts that store video locally while running AI transcripts in the cloud.

Global Healthcare Video Conferencing Solutions Market Report Scope

Healthcare video conferencing solutions are secure, HIPAA-compliant platforms that enable real-time audio-visual communication for remote diagnosis, treatment, consultation, and monitoring via devices like smartphones, tablets, and computers.

The Healthcare Video Conferencing Solutions Market Report is segmented by Solution Type, Deployment Model, End User, Application, Technology Stack, and Geography. By Solution Type, the market is segmented into Cloud-based and On-premise. By Deployment Model, the market is segmented into Public Cloud, Private Cloud, and Hybrid Cloud. By End User, the market is segmented into Hospitals & Clinics, Physician Practices, Patients/Home-care, and Payers. By Application, the market is segmented into Tele-consultation, Remote Patient Monitoring, Medical Education, and Administrative Collaboration. By Technology Stack, the market is segmented into WebRTC, VoIP/SIP, and 5G-Optimized. By Geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Cloud-based Solutions |

| On-premise Solutions |

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Hospitals & Clinics |

| Physician Practices |

| Patients / Home-care Settings |

| Payers & Other Stakeholders |

| Tele-consultation |

| Remote Patient Monitoring |

| Medical Education & Training |

| Administrative Collaboration |

| WebRTC |

| VoIP / SIP-based |

| 5G-Optimized Streaming |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Solution Type | Cloud-based Solutions | |

| On-premise Solutions | ||

| By Deployment Model | Public Cloud | |

| Private Cloud | ||

| Hybrid Cloud | ||

| By End User | Hospitals & Clinics | |

| Physician Practices | ||

| Patients / Home-care Settings | ||

| Payers & Other Stakeholders | ||

| By Application | Tele-consultation | |

| Remote Patient Monitoring | ||

| Medical Education & Training | ||

| Administrative Collaboration | ||

| By Technology Stack | WebRTC | |

| VoIP / SIP-based | ||

| 5G-Optimized Streaming | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the Healthcare Video Conferencing Solutions market in 2026?

The Healthcare Video Conferencing Solutions market size is USD 104.84 million in 2026 with a 5.68% CAGR outlook to 2031.

Which segment is expanding the fastest?

Hybrid cloud solutions lead growth, forecast at a 9.76% CAGR as hospitals balance compliance and cost.

What is driving adoption in Asia-Pacific?

China’s cross-province consultation rules and India’s Ayushman Bharat video kiosks push regional demand at a 7.11% CAGR.

How are AI scribes influencing clinician workload?

Ambient documentation cut note-taking time by 22% in a Kaiser Permanente pilot, freeing extra patient slots per clinician.

What connectivity challenges affect rural rollout?

Nineteen percent of U.S. rural hospitals still lack fiber, and one-quarter of rural adults are without home broadband, limiting HD-video consultations.

Page last updated on: