Virtual Customer Premises Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 6.86 Billion |

| Market Size (2030) | USD 38.12 Billion |

| Growth Rate (2025 - 2030) | 40.91% CAGR |

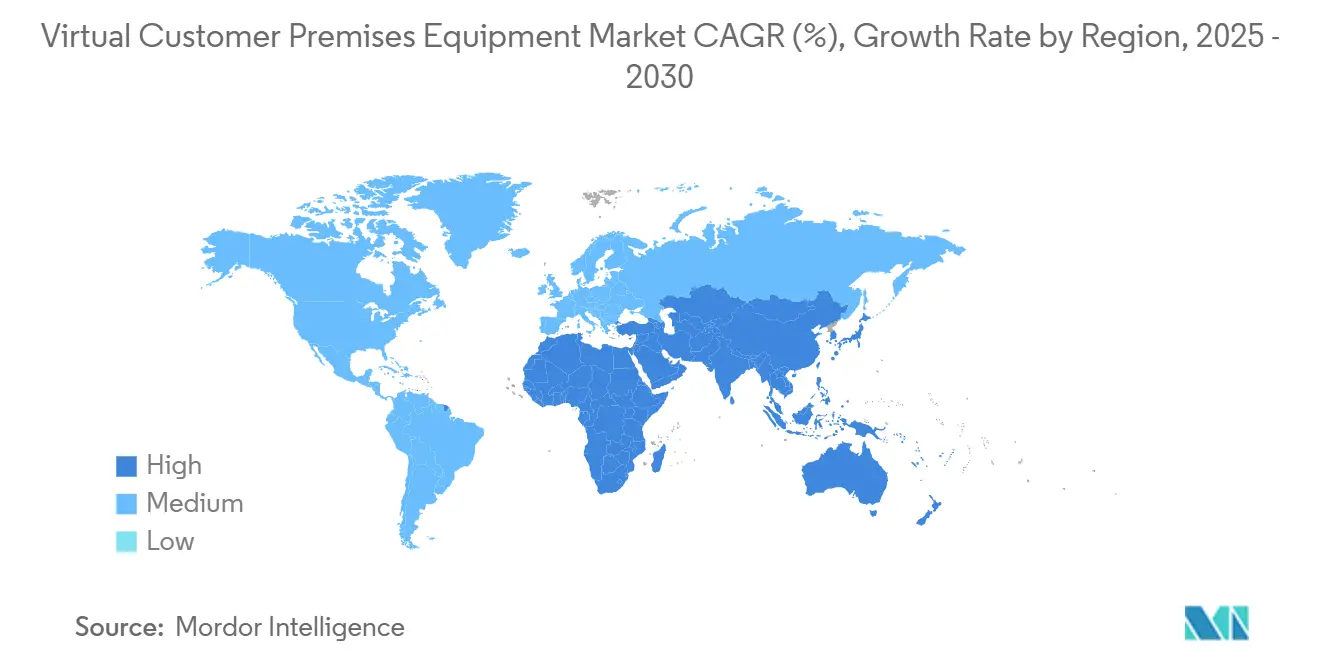

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Virtual Customer Premises Equipment Market Analysis by Mordor Intelligence

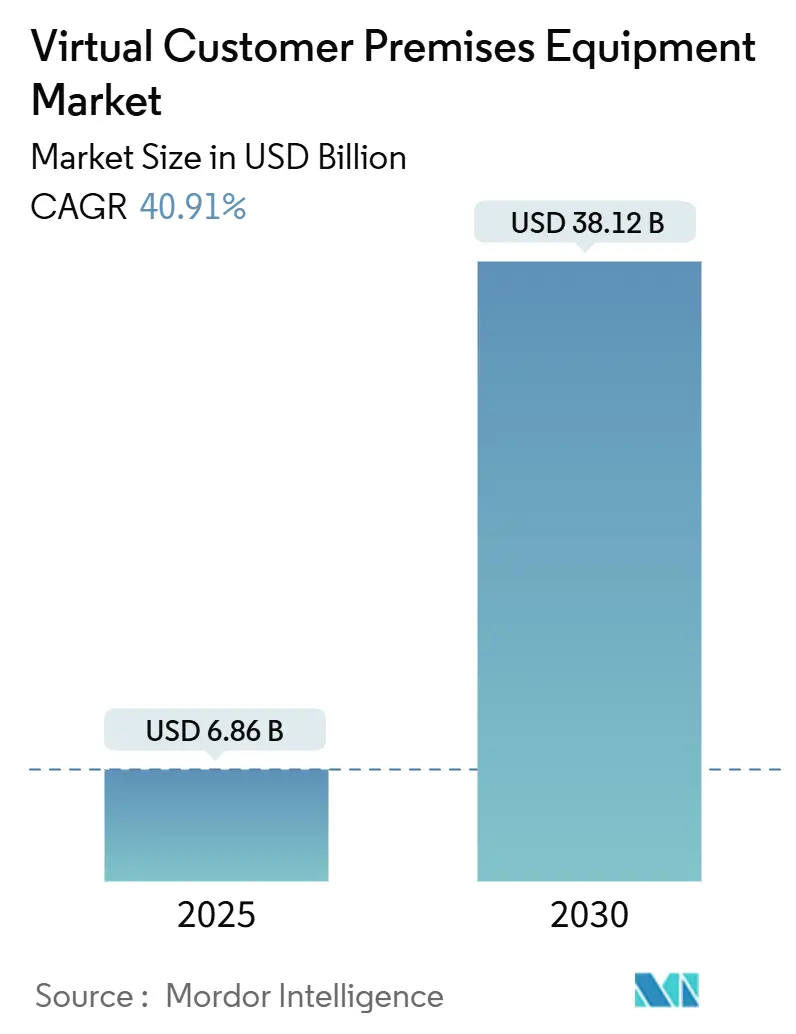

The virtual customer premises equipment market size reached USD 6.86 billion in 2025 and is projected to climb to USD 38.12 billion by 2030, advancing at a 40.91% CAGR. Capital spending shifts from proprietary routers to software-defined platforms that shorten service roll-out cycles and cut truck-roll costs, widening adoption among enterprises with dispersed branch footprints. Operators accelerate proofs of concept because the same uCPE hardware can host secure SD-WAN, firewall, and voice workloads, allowing quick bundling of revenue-generating services on one device. 5G standalone launches underscore the need for network-slice-ready edge platforms, positioning vCPE as the first commercial touchpoint for slicing. Carbon-reduction mandates bolster demand because replacing multiple power-hungry boxes with a single x86 appliance shrinks energy consumption and rack space. Competitive intensity remains moderate; incumbents rely on installed bases while white-box specialists enter through open-source orchestration.

Key Report Takeaways

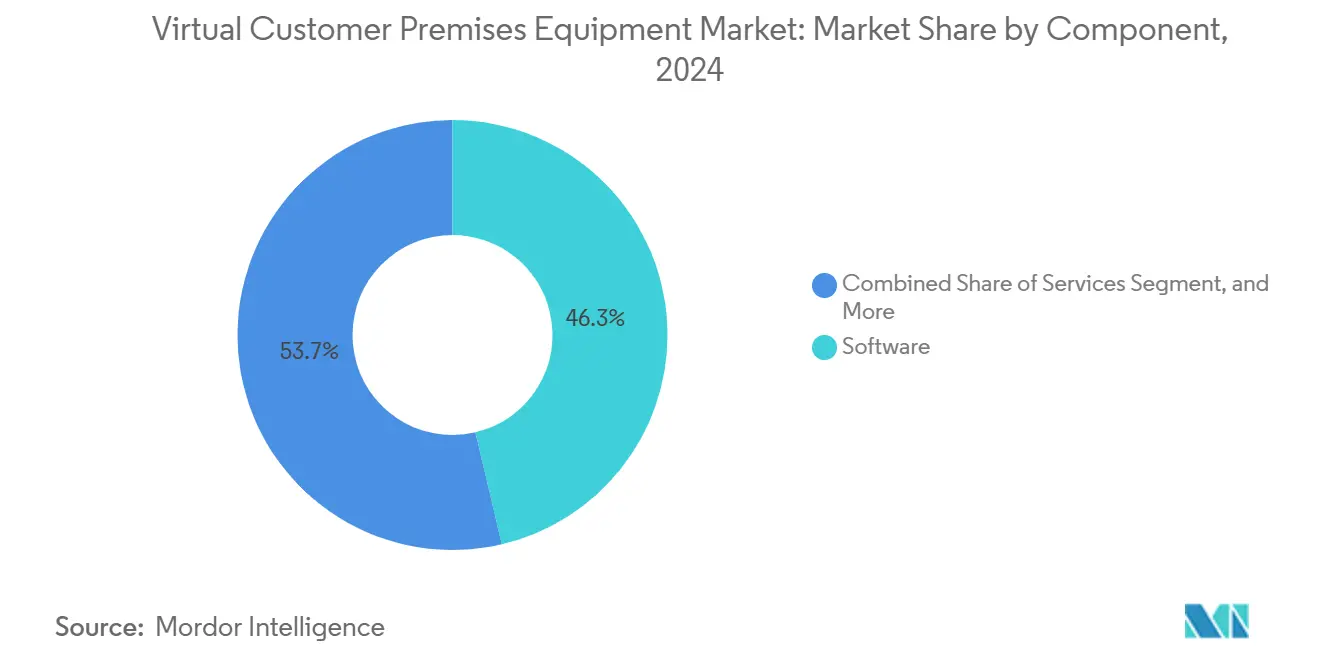

- By component, software led with a 46.32% virtual customer premises equipment market share in 2024. The services segment is forecast to expand at a 41.24% CAGR through 2030.

- By deployment mode, on-premises vCPE accounted for 57.33% of the virtual customer premises equipment market size in 2024. The cloud/hosted vCPE is projected to grow at a 41.32% CAGR between 2025 and 2030.

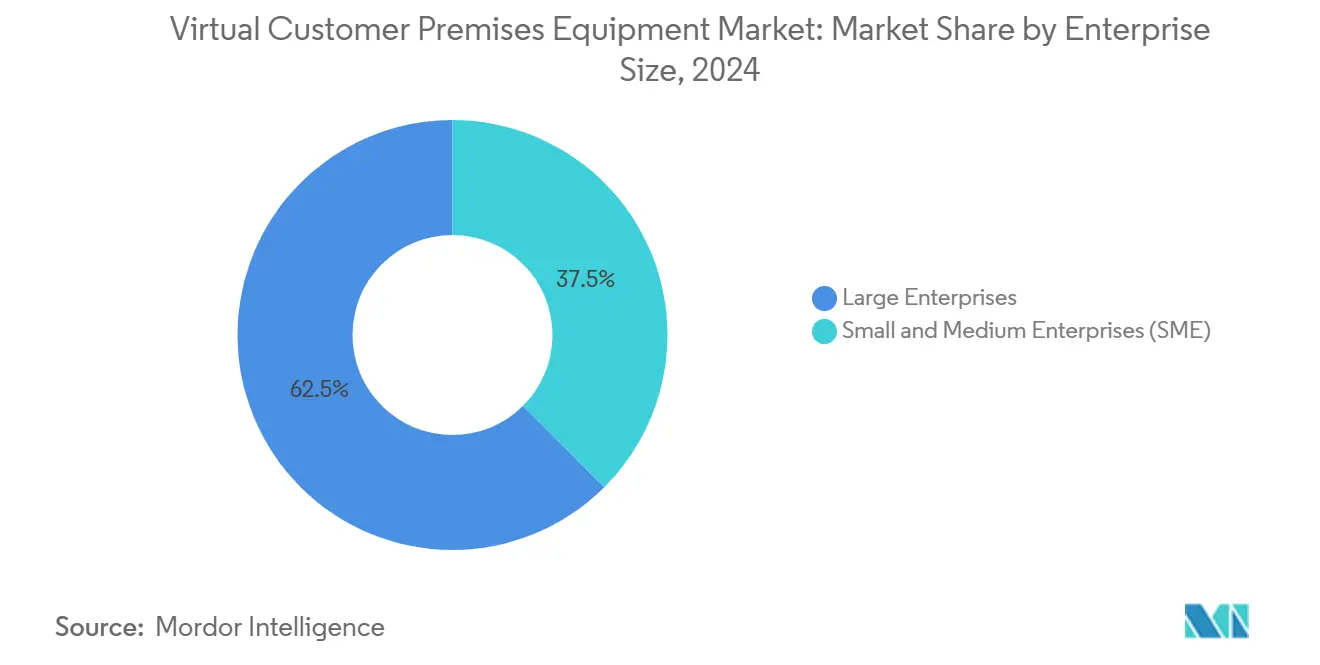

- By enterprise size, large enterprises captured 62.47% revenue share of the virtual customer premises equipment market in 2024. The SMEs are set to record a 41.19% CAGR through 2030.

- By end-user, telecom and Internet service providers commanded 39.87% of demand in 2024.The healthcare is advancing at a 40.11% CAGR to 2030.

- By geography, North America held 33.41% of the virtual customer premises equipment market in 2024 and Asia-Pacific is forecast to surge at a 40.97% CAGR through 2030.

Market Trends and Insights

Drivers Impact Analysis of Virtual Customer Premises Equipment Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid operator shift to software-defined networking (SDN/NFV) architectures | +12.3% | Global, with early gains in North America, Europe, Asia-Pacific core | Medium term (2-4 years) |

| Rising bandwidth demand from 5G and FTTH roll-outs | +10.8% | Asia-Pacific core, spill-over to North America and EU | Short term (≤ 2 years) |

| Cost-savings vs. physical CPE for multi-site enterprises | +8.7% | Global, particularly North America and EU enterprise markets | Short term (≤ 2 years) |

| Emerging 5G network slicing–ready vCPE designs | +6.2% | Asia-Pacific core, selective North America deployments | Long term (≥ 4 years) |

| Carbon-reduction targets favouring virtualisation | +2.1% | Europe, North America, with regulatory influence from EU Green Deal | Long term (≥ 4 years) |

| Open-source white-box hardware ecosystems | +1.8% | Global, with concentration in cost-sensitive emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid operator shift to software-defined networking architectures

Tier-1 carriers use enterprise vCPE roll-outs to validate NFV before core transport upgrades. NTT DOCOMO’s multi-vendor trial proved six suppliers could interoperate, de-risking subsequent national deployments. [1]NTT DOCOMO, “DOCOMO Successfully Trials NFV Using Multi-vendors' Virtualization Systems,” docomo.ne.jp Rakuten Mobile manages 48 network fabrics with only 15 engineers on a cloud-native stack that includes uCPE at branch sites, cutting operating costs while sustaining service agility. Similar pilots by Huawei and China Telecom demonstrate commercial readiness across thousands of Chinese business locations. These cases convince decision makers to migrate from fixed-function routers to flexible x86 nodes.

Rising bandwidth demand from 5G and FTTH roll-outs

Gigabit fiber backhaul and 5G radios push branch throughput requirements beyond legacy appliance headroom. VMware-powered network slicing lets operators carve SLA-graded logical pipes on the same link, an approach that mandates vCPE with real-time policy awareness. [2]Broadcom, “5G Network Slicing Concepts,” broadcom.com NEC reports its cloud-native vRAN lowers power draw 50% and total cost 30%, freeing budgets for edge roll-outs. Converging fixed and mobile access obliges a single device at the customer edge capable of wire-speed encryption for both media types.

Cost savings versus physical CPE for multi-site enterprises

Replacing purpose-built routers with software on commodity servers cuts hardware refresh cycles and truck rolls. Logistics firm Fliway halved network spend after swapping MPLS for vCPE-enabled secure SD-WAN across 24 depots. [3]Fortinet, “Fliway | Fortinet Case Study,” fortinet.com Retailer New Wave boosted bandwidth fivefold at flat cost by migrating to a cloud-delivered vCPE stack, driving a 90% drop in service tickets. Predictable subscription fees help finance teams shift capex to opex, smoothing cash flow and shortening payback periods.

Emerging 5G network-slice-ready vCPE designs

vCPE platforms now expose slice lifecycle APIs aligned with 3GPP management planes. Ciena shows operators how to price gold-, silver-, and bronze-grade slices on one transport network while assuring deterministic latency. Academic work confirms sharable virtual functions uphold isolation and utilization targets when orchestrated through micro-service meshes. Early adopters in healthcare test dedicated slices for real-time telemetry without buying private spectrum.

Restraints Impact Analysis of Virtual Customer Premises Equipment Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persisting security/performance concerns vs. dedicated hardware | -7.4% | Global, particularly regulated industries in North America and EU | Short term (≤ 2 years) |

| Interoperability gaps among multivendor VNFs | -5.2% | Global, with acute challenges in Asia-Pacific emerging markets | Medium term (2-4 years) |

| Telecom procurement inertia and legacy OSS/BSS lock-ins | -3.8% | North America and EU established markets | Medium term (2-4 years) |

| Shortage of NFV-literate operational talent | -2.6% | Global, particularly acute in emerging Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persisting security and performance concerns versus dedicated hardware

Financial institutions question shared-infrastructure isolation, delaying vCPE adoption for card-processing flows. Certification schemes often lag behind NFV innovation, so auditors prefer appliances with FIPS-validated chips. NEC and Fortinet respond by pairing hardware crypto accelerators with virtual firewalls that achieve near-native throughput, narrowing confidence gaps.

Interoperability gaps among multivendor VNFs

Operators target vendor diversity yet find lifecycle scripts differ across suppliers, raising integration costs. ADVA’s Ensemble framework introduces standardized hand-offs and zero-touch provisioning, but real-world uptake stays low because test matrices explode as VNF counts rise. Without common descriptors, brownfield operators risk tool sprawl that offsets NFV savings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Virtual Customer Premises Equipment Market Segment Analysis

By Component:

Software adoption standardizes the edgeSoftware held 46.32% of the virtual customer premises equipment market in 2024, underscoring the shift from ASIC-laden routers to license-based function stacks. Platform updates now ride live upgrade pipelines, so feature velocity surpasses hardware life spans. Users favor vendor-agnostic hypervisors that bolt SD-WAN, router, and voice VNFs onto Advantech or Lanner white boxes without soldering new boards. The services line’s 41.24% CAGR shows many buyers outsource day-2 operations rather than train staff in NFV toolchains. Consulting partners wrap design and security audits around subscription bundles, monetizing orchestration complexity.

Hardware revenue remains steady because each deployment still needs an x86 or ARM box. Component suppliers advance multi-core offload silicon that hits deterministic latency for 10 Gbps links, letting one appliance replace three legacy devices in a branch rack. Intel’s uCPE reference blueprint improves SR-IOV channelization so security VNFs process packets at line rate, holding back skepticism about software throughput. Interoperability labs certify driver stacks that allow drop-in fanless models for harsh retail or plant environments.

By Deployment Mode:

Hybrid emerges as the new defaultOn-premises nodes represented 57.33% of the virtual customer premises equipment market size in 2024. Data residency laws and ultra-low-latency workloads keep compute local, especially for point-of-sale encryption and video analytics. Yet a 41.32% CAGR for cloud/hosted options through 2030 shows enterprises lean on provider PoPs when branches lack skilled hands. Managed clouds host control VNFs and push lightweight data planes to the edge, balancing sovereignty with instant scaling.

ADTRAN’s Ensemble Connector lets operators spin identical images in a metro data center or on a branch-mounted box, shifting workloads as policy dictates. Edge computing complements the model: AI inference containers run on the same uCPE that backhauls traffic, avoiding separate gateways. Hybrid control portals give IT managers one pane to steer service chains, an advantage over siloed appliance dashboards.

By Enterprise Size:

SME uptake accelerates with SaaS-like offersLarge enterprises consumed 62.47% of 2024 demand. These firms run global MPLS-migration projects and need multi-tenant orchestration for hundreds of sites. They negotiate custom SLAs and often co-create service chains with carriers. SMEs, however, will be the growth engine as simplified portals hide NFV jargon behind wizard-driven templates. A 41.19% CAGR for the SME slice to 2030 highlights the democratization trend.

Network Computing notes branch managers can tweak QoS per user group without CLI expertise once SDN abstractions replace router configs. Container-native VNFs let providers strip bundles down to one or two features, pricing them within small-business budgets. Subscription models with zero-touch delivery appeal to firms that lack full-time network teams, flattening adoption barriers.

By End-user Industry:

Healthcare leads future demand curvesTelecom and ISP buyers accounted for 39.87% revenue in 2024, primarily as wholesale customers reselling managed SD-Branch services. They deploy vCPE both in their own POPs and at enterprise premises, capturing incremental ARPU. Healthcare is on track for a 40.11% CAGR, the fastest among end users. Smart-hospital blueprints place nurse-call, imaging, and telemetry traffic on isolated slices maintained by a single uCPE instead of disparate gateways.

Regulations such as HIPAA compel encryption at rest and in transit, pushing providers to integrate firewall and DLP VNFs with audit trails. Spectrum Business finds 88% of North-American providers rank network modernization a top-three digital health priority. BFSI and retail sustain steady uptake, focusing on fraud-prevention firewalls and omni-channel checkout latency, respectively.

Geography Analysis

North America Virtual Customer Premises Equipment Market

North America commanded 33.41% of 2024 revenue thanks to early SD-WAN roll-outs by Verizon, AT&T, and large banks that standardized on white-box edge routers. Verizon’s SD-Branch service with Versa shows how carriers package routing, security, and analytics into a one-click portal for Fortune 500 clients. Regulatory clarity on data localization favors on-premises vCPE, but hybrid adoption gains as hyperscalers open more regional PoPs.

APAC Virtual Customer Premises Equipment Market

Asia-Pacific is the fastest climber with a 40.97% CAGR to 2030, catalyzed by 5G standalone launches across Japan, China, and India. NTT DOCOMO’s Open RAN lab validated multi-vendor stacks that span radio to enterprise edge, setting a blueprint other operators follow. Vietnam’s IX expansions by CMC Telecom and BBIX illustrate local carriers investing in neutral hubs to back cross-border SaaS traffic. Governments fund broadband corridors that include uCPE in universal-service programs, jump-starting SME demand.

Europe Virtual Customer Premises Equipment Market

Europe posts steady growth as the EU Green Deal incentivizes carbon-efficient virtualization. Energy-aware scheduling in vCPE orchestrators aligns with utility rebates for data-center power capping. Region-wide data-sovereignty rules steer multinationals to hybrid topologies that keep PII within member states, so vendors emphasize encryption and geo-fencing policy engines.

MEA and South America Virtual Customer Premises Equipment Market

Middle East and Africa are nascent but promising. Gulf operators bundle managed uCPE with private 5G campus networks for oil-field telemetry, while South-African retailers adopt pay-as-you-go SD-WAN for rural outlets. South America sees Brazil’s Telefónica piloting vCPE in residential gateways to upsell parental-control firewalls, signaling cross-segment versatility.

Competitive Landscape

The arena is moderately concentrated. Cisco leverages the Meraki and Catalyst lines to cross-sell vCPE within installed wireless estates, giving it first call when branches refresh routers. VMware’s integration into Broadcom brings financial heft but raises road-map questions for telco-grade orchestrators despite Broadcom’s new VeloSky convergence appliance. Nokia and Ericsson court carriers that demand 5G-slice co-ordination, though slower revenue growth squeezes R&D budgets.

Start-ups such as Versa Networks and ADVA emphasize stateless micro-service VNFs and open APIs that ease multi-vendor mixes. Ekinops runs a validation program certifying all major firewall and SD-WAN VNFs on its white-box line, helping operators avoid lock-in. Patent filings around multi-interface policy enforcement suggest next-wave differentiation will center on automated packet steering rather than raw throughput.

Healthcare and SME bundles remain white-space segments where few incumbents offer compliance-ready, wizard-driven packages. Vendors that bake clinical workflow templates or one-click PCI-DSS configurations into portals can tap under-served verticals without head-to-head price wars against Tier-1 router brands.

Virtual Customer Premises Equipment Industry Leaders

Cisco Systems, Inc.

Juniper Networks, Inc.

VMware, Inc.

Nokia Corporation

Huawei Technologies Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Virtual Customer Premises Equipment Market Companies Covered in this Report

- Cisco Systems, Inc.

- Juniper Networks, Inc.

- VMware, Inc.

- Nokia Corporation

- Huawei Technologies Co., Ltd.

- NEC Corporation

- Orange Business Services S.A.

- Telefonaktiebolaget LM Ericsson

- Hewlett Packard Enterprise Company

- Versa Networks, Inc.

- ADVA Optical Networking SE

- Arista Networks, Inc.

- Ciena Corporation

- Dell Technologies Inc.

- Fortinet, Inc.

- Radisys Corporation

- Broadcom Inc.

- CommScope Holding Company, Inc. (Arris)

- Lanner Electronics Inc.

- Radware Ltd.

Recent Industry Developments in Virtual Customer Premises Equipment Market

- August 2025: Arista Networks acquired VeloCloud SD-WAN from Broadcom, reporting USD 2.205 billion Q2 2025 revenue and 30.4% annual growth.

- June 2025: Broadcom posted USD 15 billion Q2 2025 revenue with USD 4.4 billion from AI networking silicon, while VMware software climbed 25% to USD 6.6 billion.

- January 2025: Broadcom launched VeloSky, a converged fiber-cellular-satellite appliance that embeds dynamic application-based slicing for service providers.

- September 2024: NTT DOCOMO and StarHub completed an Open RAN lab trial that achieved high throughput and low latency across Fujitsu, NVIDIA, and Dell components.

Global Virtual Customer Premises Equipment Market Report Scope

Segmentation Overview

| Software |

| Services |

| Hardware |

| On-premises vCPE |

| Cloud/Hosted vCPE |

| Small and Medium Enterprises (SME) |

| Large Enterprises |

| Telecom and Internet Service Providers |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare |

| Retail and e-Commerce |

| Information Technology and Data Centres |

| Other End-user Industry |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Component | Software | ||

| Services | |||

| Hardware | |||

| By Deployment Mode | On-premises vCPE | ||

| Cloud/Hosted vCPE | |||

| By Enterprise Size | Small and Medium Enterprises (SME) | ||

| Large Enterprises | |||

| By End-user Industry | Telecom and Internet Service Providers | ||

| Banking, Financial Services and Insurance (BFSI) | |||

| Healthcare | |||

| Retail and e-Commerce | |||

| Information Technology and Data Centres | |||

| Other End-user Industry | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large is the virtual customer premises equipment market in 2025?

It stands at USD 6.86 billion and is on track for USD 38.12 billion by 2030.

What CAGR is forecast for virtual customer premises equipment through 2030?

The market is expected to grow at 40.91% annually over the 2025-2030 period.

Which component segment leads revenue today?

Software accounts for 46.32% of 2024 revenue, reflecting enterprises’ preference for flexible updates.

Which region is expanding fastest?

Asia-Pacific carries the highest growth outlook with a 40.97% CAGR to 2030 as 5G roll-outs accelerate.

Why are SMEs adopting vCPE solutions rapidly?

Wizard-driven portals and subscription pricing remove the need for deep in-house network skills, driving a 41.19% CAGR in the SME segment.

What is the key restraint slowing adoption in regulated industries?

Concerns about security isolation and performance predictability on shared hardware remain the primary barrier, especially for financial services.

Page last updated on: