Virtual Private Server Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

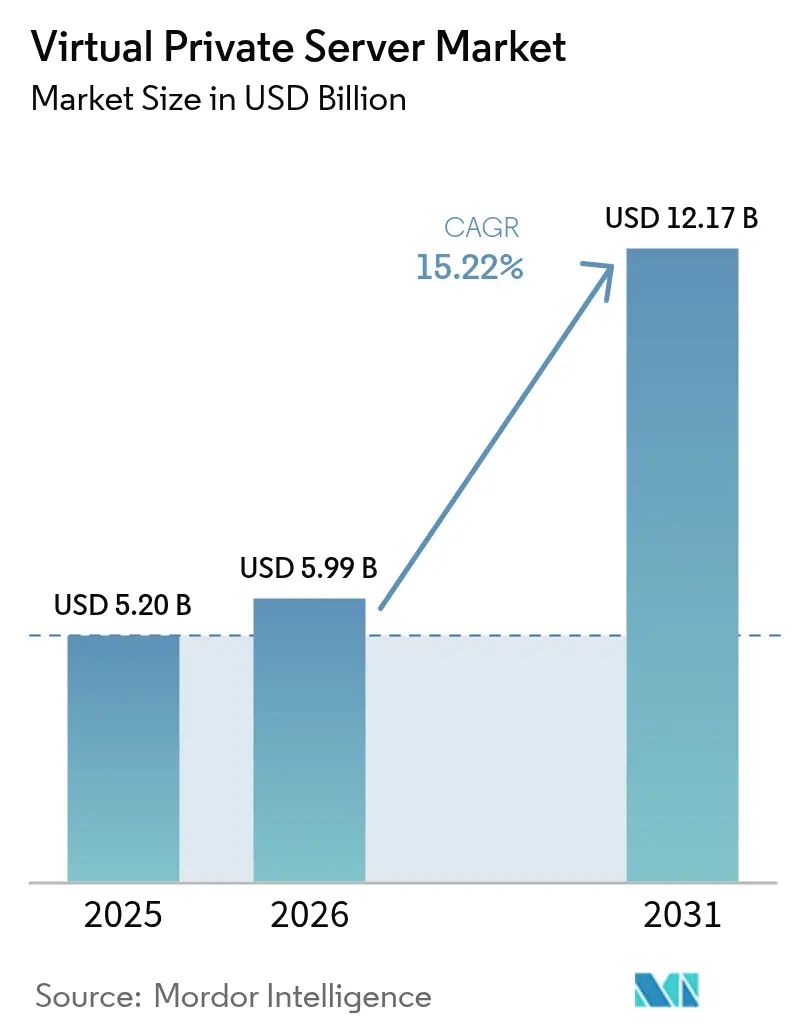

| Market Size (2026) | USD 5.99 Billion |

| Market Size (2031) | USD 12.17 Billion |

| Growth Rate (2026 - 2031) | 15.22% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Virtual Private Server Market Analysis by Mordor Intelligence

The virtual private server market size is expected to grow from USD 5.20 billion in 2025 to USD 5.99 billion in 2026 and is forecast to reach USD 12.17 billion by 2031 at 15.22% CAGR over 2026-2031. This sustained expansion illustrates how the virtual private server market acts as a midpoint between low-cost shared hosting and high-capex dedicated servers for organizations modernizing their digital estates[1]IBM Security, “Cost of a Data Breach Report 2024,” ibm.com. Demand accelerates because VPS instances provide the isolation, customizable security, and predictable performance now required for AI inference, edge-computing, and sovereign-cloud deployments that must meet local data-residency rules. The average data-breach cost climbed to USD 4.45 million in 2024, prompting security-conscious buyers to abandon shared hosting in favor of VPS environments with configurable firewalls and zero-trust architectures. At the same time, containerization and GPU-enabled instances are redefining price-performance expectations, forcing providers to innovate on billing transparency, network-egress waivers, and automated uptime guarantees.

Key Report Takeaways

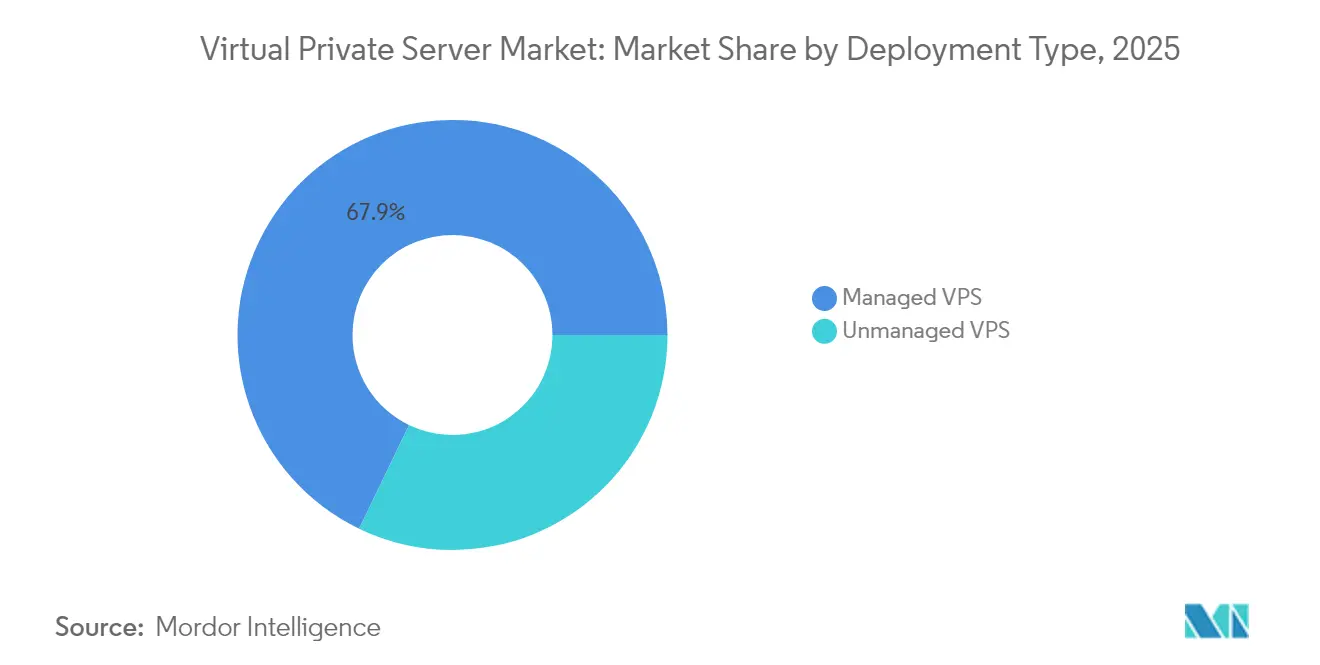

- By deployment type, managed services captured 67.85% of virtual private server market share in 2025, whereas unmanaged services are poised to register a 16.62% CAGR through 2031.

- By operating system, Linux held 55.60% of virtual private server market share in 2025, while Windows VPS is projected to expand at 14.07% CAGR by 2031.

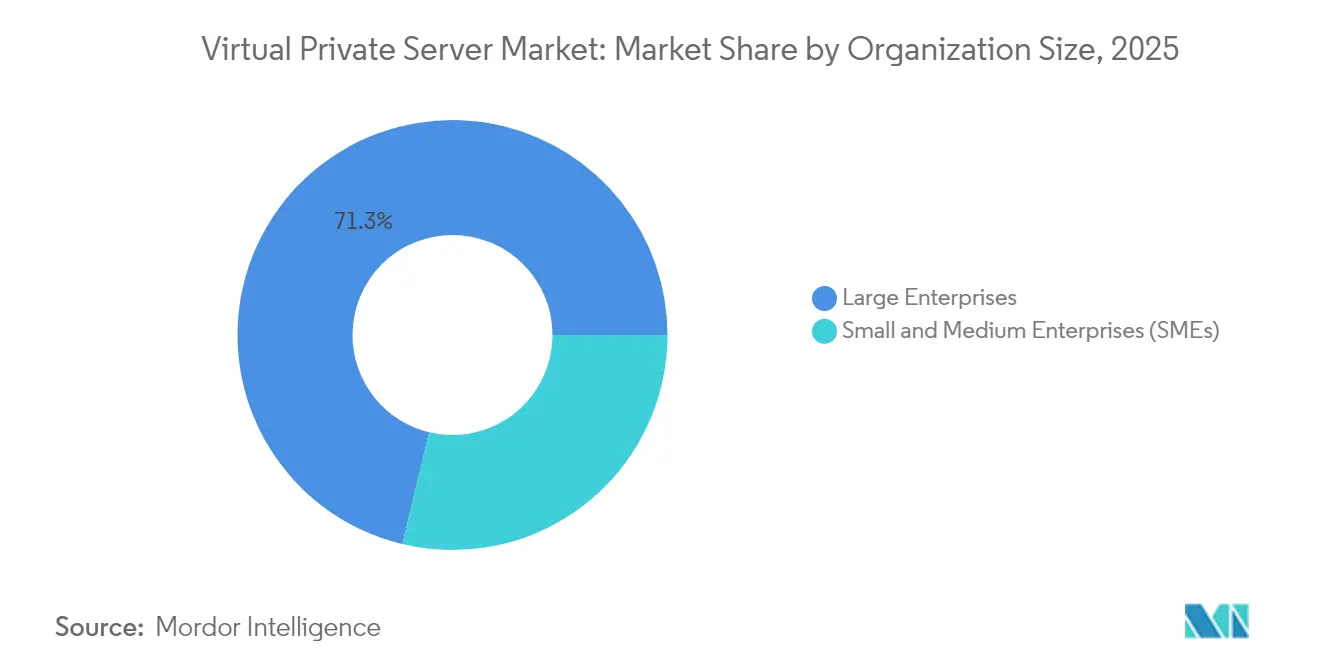

- By organization size, large enterprises controlled 71.25% of virtual private server market size in 2025; small and medium enterprises are advancing at a 16.74% CAGR through 2031.

- By end-user vertical, the IT and telecommunication segment led with 34.85% revenue share in 2025, while BFSI is growing fastest at 15.36% CAGR to 2031.

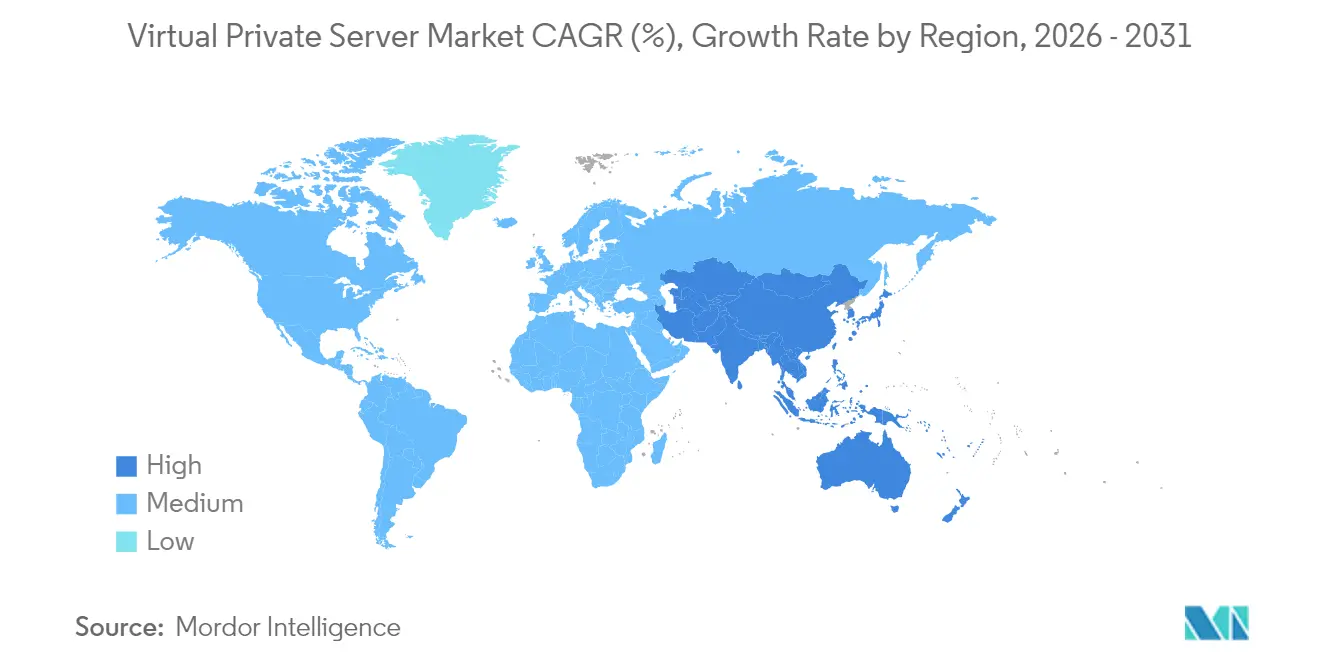

- By geography, North America commanded 37.10% of virtual private server market share in 2025; Asia-Pacific is on track for a 15.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Virtual Private Server Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising enterprise security concerns | +3.2% | North America and EU | Medium term (2-4 years) |

| Demand for cost-effective scalability and uptime | +2.8% | APAC and Latin America | Short term (≤ 2 years) |

| SMEs’ digital-commerce expansion | +2.1% | APAC, MEA spill-over | Medium term (2-4 years) |

| VPS as bridge in multi-cloud migration | +1.9% | North America, EU | Long term (≥ 4 years) |

| GPU-ready VPS for AI/ML workloads | +2.3% | North America and China | Medium term (2-4 years) |

| Sovereign-cloud and data-residency mandates | +1.8% | EU, APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Enterprise Security Concerns

Security remains the most influential adoption trigger because organizations need granular network controls unavailable in shared hosting. More than 56% of companies reported VPN-related cyberattacks during 2024, a statistic pushing buyers toward isolated virtual servers with programmable access rules. European businesses intensify this move to satisfy GDPR while maintaining full audit trails for regulators. Providers showcasing ISO 27001 certifications, hardware-root-of-trust, and real-time threat monitoring are translating these assurances into premium subscription tiers.

Demand for Cost-Effective Scalability and Uptime

Budget discipline fuels interest in VPS plans that mimic dedicated-server performance but at fractional cost. SMEs adopting cloud services report 2.1 times aggregate cost savings when VPS underpins their digital-commerce stack. Containerization strengthens this trend, with 92% of surveyed organizations running containers in production and 91% relying on Kubernetes orchestration. Vendors therefore emphasize auto-healing clusters and hourly billing models that scale linearly with actual resource draw.

SME Digital-Commerce Boom Driving VPS Uptake

Half of global SMEs increased digital-transformation budgets in 2025, cementing VPS as a foundational layer for customer-facing web applications. German SMEs showed an average ROI of 13.44 on new technology investments, where VPS enabled deeper analytics and improved customer experience. Managed VPS providers seize this momentum by bundling codeless deployment wizards that offset chronic DevOps skill shortages.

VPS as Bridge Solution in Multi-Cloud Migration

Roughly two-thirds of enterprises now operate across multiple public clouds, and many regard neutral VPS nodes as staging grounds before locking workloads into hyperscalers. The European Data Act entering force in September 2025 further boosts portability requirements, positioning VPS suppliers with robust API interoperability as preferred partners[2]European Union, “Regulation (EU) 2023/2854 – European Data Act,” europa.eu .

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intense price competition | −2.1% | North America and EU | Short term (≤ 2 years) |

| Limited DevOps skills within SMEs | −1.3% | Global, heavier in emerging markets | Medium term (2-4 years) |

| Server-hardware supply-chain volatility | −1.8% | Global | Medium term (2-4 years) |

| Sustainability regulations lifting OPEX | −1.1% | EU, North America, APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intense Price Competition

Hyperscalers like AWS, Azure, and Google exploit economies of scale to launch micro-instances that undercut specialist hosts, while shared-hosting providers blur the line with VPS-grade resource guarantees. Spot and pre-emptible VMs can be 75% cheaper for interruptible workloads, challenging mid-tier vendors to differentiate beyond raw price.

Limited DevOps Skills in SME Customer Base

A projected shortfall of 67,000 U.S. semiconductor-related engineers by 2030 signals broader talent constraints in cloud operations and automation. VPS vendors offering UI-driven configuration, auto-patching, and 24×7 chat support help mitigate this barrier, yet uptake in underserved regions still lags overall demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Managed Services Sustain Leadership

Managed services dominated with 67.85% revenue share in 2025 because enterprises offload patching, monitoring, and compliance to specialists. Tier-one providers now embed Kubernetes operators, real-time DDoS scrubbing, and Infrastructure-as-Code templates to sustain this lead. Unmanaged VPS still posts a compelling 16.62% CAGR through 2031, with hobbyists, game-server admins, and blockchain validators drawn to root-level freedom. The virtual private server market size for unmanaged plans is projected to reach USD 4.16 billion by 2031, demonstrating the dual-track nature of demand.

Managed portfolios increasingly include AI-ready clusters with pooled GPUs and shared model libraries that shorten development sprints. Zero-cost egress offers—first rolled out by UpCloud in April 2025—are spreading through the provider landscape as a differentiator against hyperscalers that still charge for outbound bandwidth. Over time, transparency on data-transfer pricing could become a decisive conversion lever, especially for SMEs hosting high-traffic e-commerce stores.

By Operating System: Linux Dominance Reinforced by Container Adoption

Linux retained 55.60% share in 2025 and is expected to advance at 16.21% CAGR through 2031. Cloud-native tooling such as Docker and Kubernetes natively targets Linux namespaces, elevating the platform as default for microservices deployment. Windows VPS fills a critical niche for .NET and Active Directory workloads in sectors like legal, finance, and manufacturing, but rising license costs keep its share below the Linux trajectory. Lightweight Linux distributions—some less than 200 MB—boot in seconds on edge devices, satisfying emerging low-latency use cases in smart retail and industrial IoT.

The AI surge prompts vendors to ship pre-configured Ubuntu or Rocky Linux images containing CUDA, cuDNN, and PyTorch, cutting model-deployment times from days to hours for data-science teams. Security advantages also matter: live-kernel patching reduces downtime, and SELinux or AppArmor provide mandatory-access controls without third-party agents.

By Organization Size: Enterprise Dominance with SME Acceleration

Large enterprises commanded 71.25% of virtual private server market size in 2025 because they require large-node fleets for ERP, disaster-recovery, and hybrid-cloud links. However, SMEs are growing fastest at 16.74% CAGR, propelled by rising digital-commerce adoption and easy-to-use managed stacks. One provider reported that average onboarding time for SMEs dropped below 48 hours after launching guided DNS and SSL setup wizards—a clear productivity gain that accelerates market penetration.

Higher adoption among SMEs also stems from per-second billing, prepaid credit options, and localized language support portals that lower psychological switching costs. While SME workloads remain smaller, volume gains can materially lift provider utilization, especially across under-tapped emerging markets in Southeast Asia and Latin America.

By End-User Vertical: IT and Telecom Lead, BFSI Gains Momentum

IT and telecommunication firms absorbed 34.85% of virtual private server market share in 2025 due to their role in delivering SaaS, managed network services, and white-label cloud offerings. Banking, financial services, and insurance is the fastest mover at 15.36% CAGR because regulators now permit safe-cloud models for sensitive data once real-time encryption, geofencing, and audit logging are in place.

Healthcare uses VPS to host electronic health records, telemedicine portals, and diagnostic-image archives, meeting HIPAA or local equivalents. Manufacturers deploy edge-positioned VPS instances to process factory-floor sensor data in near real time, reducing latency and bandwidth overhead compared with centralized cloud pushes. Public-sector agencies adopt sovereign VPS nodes so citizen data stays inside national borders, addressing transparency mandates under freedom-of-information laws.

Geography Analysis

North America controlled 37.10% of virtual private server market share in 2025, powered by dense carrier-neutral data-center ecosystems and well-funded enterprise IT budgets. Secondary markets like Phoenix and Montréal post double-digit capacity growth because land availability and renewable-energy mix outperform saturated coastal hubs. Providers here leverage mature power-purchase agreements to secure carbon-neutral energy, anticipating stricter state-level climate statutes.

Asia-Pacific is projected to record the fastest CAGR at 15.82% through 2031, supported by government digital-economy blueprints and rapid fiber backhaul deployment. Colocation power is expected to rise from 10,233 MW in 2023 to 19,069 MW by 2028, reflecting a 13.3% compound rate that underpins VPS node expansion. Major players such as Alibaba Cloud and AWS open new availability zones in Jakarta, Hyderabad, and Osaka, scaling regional supply and spurring competitive price benchmarking among local hosts.

Europe’s focus on data-sovereignty and sustainability shapes a distinct adoption profile. The impending European Data Act forces providers to guarantee portability and fair exit clauses, encouraging buyers to consider open-API VPS suppliers. Power-grid constraints in Amsterdam and Frankfurt push operators toward emerging hubs in Madrid, Warsaw, and Milan where municipalities offer favorable tax incentives for green facilities. Strict energy-reporting obligations foster adoption of immersion cooling and waste-heat reuse, translating sustainability goals into concrete capital-expenditure lines.

Competitive Landscape

The virtual private server market remains moderately fragmented. Hyperscalers—AWS, Microsoft Azure, and Google Cloud—dominate high-value enterprise contracts, but specialized providers like DigitalOcean, Vultr, and Linode carve developer and SME niches via simplified UX and transparent pricing. Regional hosts such as OVHcloud, Hetzner, and Leaseweb focus on local compliance, customizable hardware, and multilingual support.

Strategic moves illustrate divergent paths. Vultr raised USD 333 million in fresh equity, led by AMD Ventures, to finance GPU-dense zones and edge locations across five continents. DigitalOcean posted Q1 2025 revenue of USD 211 million, a 14% year-on-year uptick, attributing triple-digit AI revenue growth to its new GenAI platform. UpCloud’s zero-cost egress policy places pressure on competitors still charging per-GB transfer fees. Meanwhile, consolidation continues as World Host Group acquires stalwarts like A2 Hosting to scale east-west traffic coverage.

Technology roadmaps converge around automation, security, and carbon transparency. Providers integrate Terraform modules, Kubernetes CRDs, and SAML-based single sign-on into base plans. Hardware refreshes feature AMD EPYC 9004 “Genoa” CPUs or Intel Sapphire Rapids chips to achieve higher performance per watt. Confidential-computing enclaves powered by AMD SEV-SNP or Intel TDX enter general availability in mid-tier SKUs, attracting regulated industries seeking extra data-in-use protection.

Virtual Private Server Industry Leaders

Amazon Web Services, Inc.

GoDaddy Inc.

Rackspace Inc.

DigitalOcean, Inc.

Liquid Web, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Cloudzy completed the acquisition of BuyVM, expanding budget VPS offerings in the low-end market.

- January 2025: Leaseweb Global launched new VPS infrastructure priced at EUR 3.99 per month with NVMe storage and integrated DDoS protection.

- January 2025: World Host Group acquired A2 Hosting in its largest acquisition to date, continuing consolidation in the hosting sector.

- December 2024: Vultr secured USD 333 million in equity financing led by LuminArx Capital Management and AMD Ventures at a USD 3.5 billion valuation.

Global Virtual Private Server Market Report Scope

A VPS-or virtual private server-is a virtual machine that provides virtualized server resources on a physical server that is shared with other users. With VPS hosting, you get dedicated server space with a reserved amount of resources, offering greater control and customization than shared hosting.

The virtual private server market is segmented by operating system (Windows, Linux, and other operating systems), organization size (small and medium-sized enterprises (SMEs) and large enterprises), end-user vertical (iIT& communication, BFSI, retail, healthcare, and other end-user verticals), and geography (North America, Europe, Asia Pacific, Latin America, and Middle East and Africa).

The market sizes and forecasts are provided in terms of value (USD billion) for all the above segments.

| Managed VPS |

| Unmanaged VPS |

| Linux |

| Windows |

| Other Operating System |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| IT and Telecommunication |

| BFSI |

| Retail and E-commerce |

| Healthcare and Life Sciences |

| Manufacturing |

| Government and Public Sector |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| By Deployment Type | Managed VPS | ||

| Unmanaged VPS | |||

| By Operating System | Linux | ||

| Windows | |||

| Other Operating System | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By End-user Vertical | IT and Telecommunication | ||

| BFSI | |||

| Retail and E-commerce | |||

| Healthcare and Life Sciences | |||

| Manufacturing | |||

| Government and Public Sector | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the virtual private server market?

The virtual private server market size reached USD 5.99 billion in 2026 and is projected to rise to USD 12.17 billion by 2031 at a 15.22% CAGR over 2026-2031.

Which deployment model dominates the virtual private server market?

Managed services lead with 67.85% market share because enterprises outsource patching, monitoring, and compliance to specialist providers.

Why is Linux preferred for VPS hosting?

Linux commands 55.60% market share thanks to its alignment with Docker, Kubernetes, and other cloud-native tools, plus lower licensing costs versus proprietary operating systems.

Which region is projected to grow fastest?

Asia-Pacific is expected to post a 15.82% CAGR through 2031, buoyed by government digital-economy initiatives and large-scale data-center investment.

How do data-sovereignty laws influence VPS adoption?

Regulations such as the European Data Act require providers to ensure data portability and residency, prompting organizations to select VPS hosts with in-country infrastructure and open APIs.

What differentiates specialized VPS providers from hyperscalers?

Specialized hosts compete on transparent pricing, developer-friendly UX, and region-specific compliance, while hyperscalers leverage extensive service portfolios and global private networks.

Page last updated on: