Customer Relationship Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

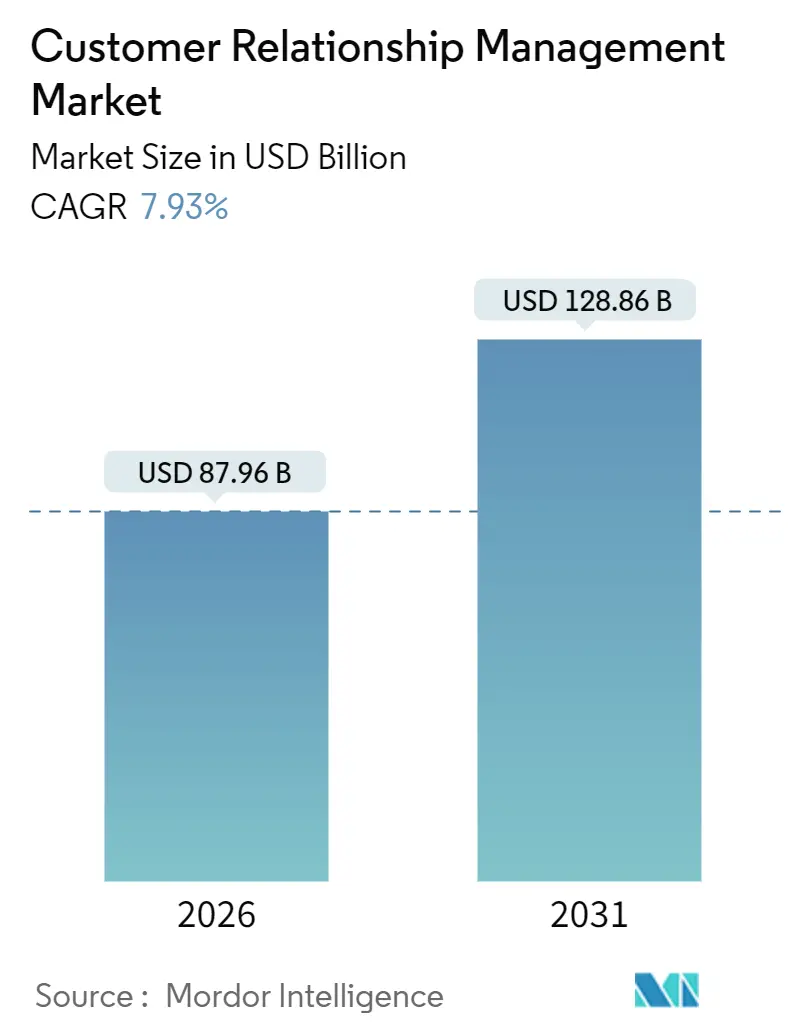

| Market Size (2026) | USD 87.96 Billion |

| Market Size (2031) | USD 128.86 Billion |

| Growth Rate (2026 - 2031) | 7.93% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

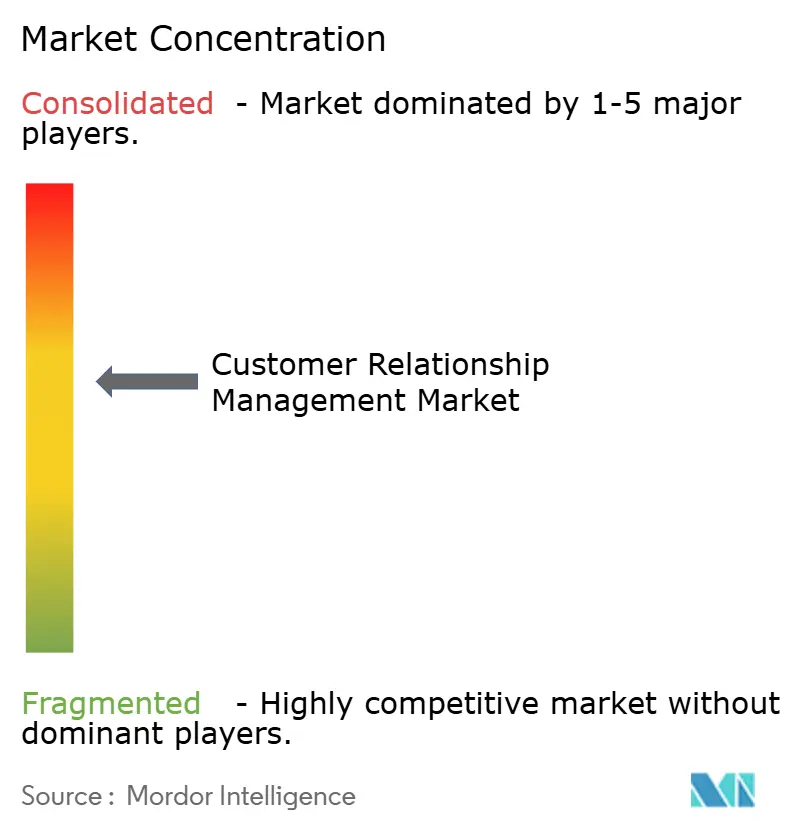

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Customer Relationship Management Market Analysis by Mordor Intelligence

The Customer Relationship Management market size is USD 87.96 billion in 2026 and is projected to rise to USD 128.86 billion by 2031, reflecting a 7.93% CAGR. Enterprises are moving from transactional systems toward orchestration platforms that merge sales, marketing, and service workflows under AI-driven agents. Continuous cloud migration, vertical-specific SaaS, and autonomous copilots are compressing sales cycles and elevating user expectations. Vendor investment confirms the growth trajectory, exemplified by Salesforce’s USD 4 billion expansion of data-center capacity and Microsoft’s decision to embed Copilot natively into Dynamics 365 modules. Demand for low-code configuration, data-residency assurances, and revenue-operations visibility is expanding total addressable opportunities across regions.

Key Report Takeaways

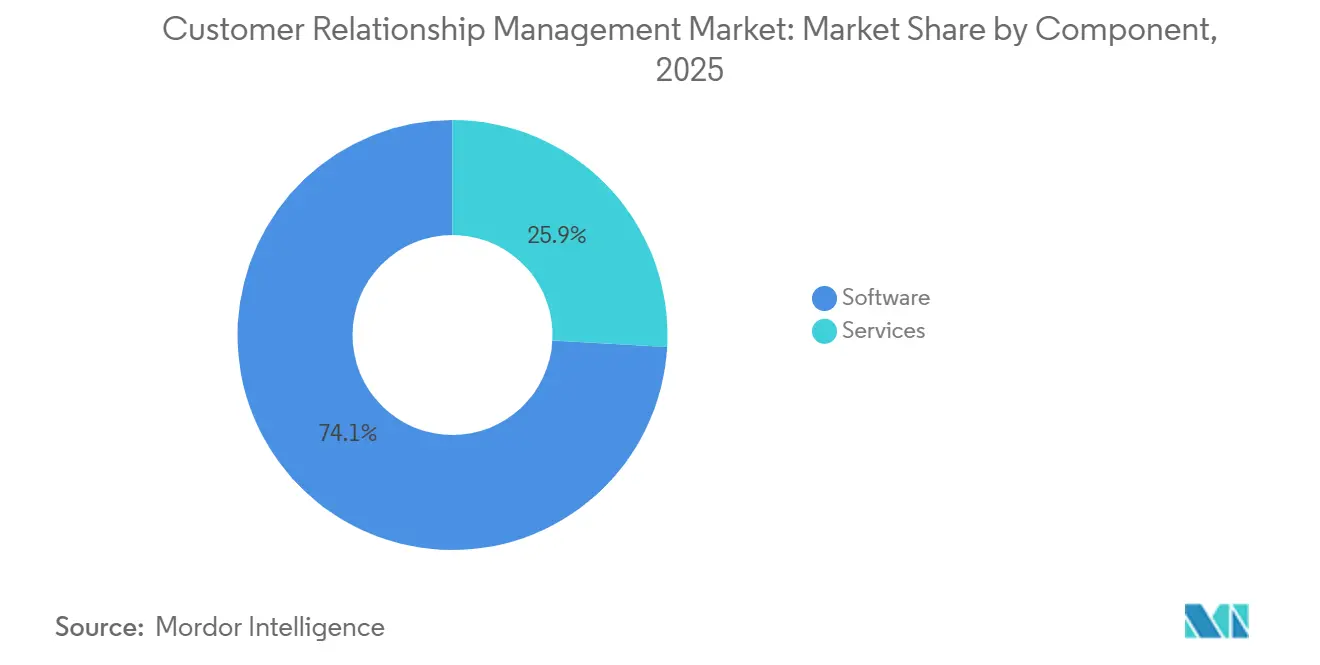

- By component, software led with 74.12% of value in 2025, while services are advancing at 9.52% CAGR through 2031.

- By deployment mode, cloud captured 80.16% revenue share in 2025 and hybrid architectures are growing at 9.04% CAGR through 2031.

- By organization size, large enterprises accounted for 62.66% spending in 2025, whereas SMEs are scaling at a 9.54% CAGR through 2031.

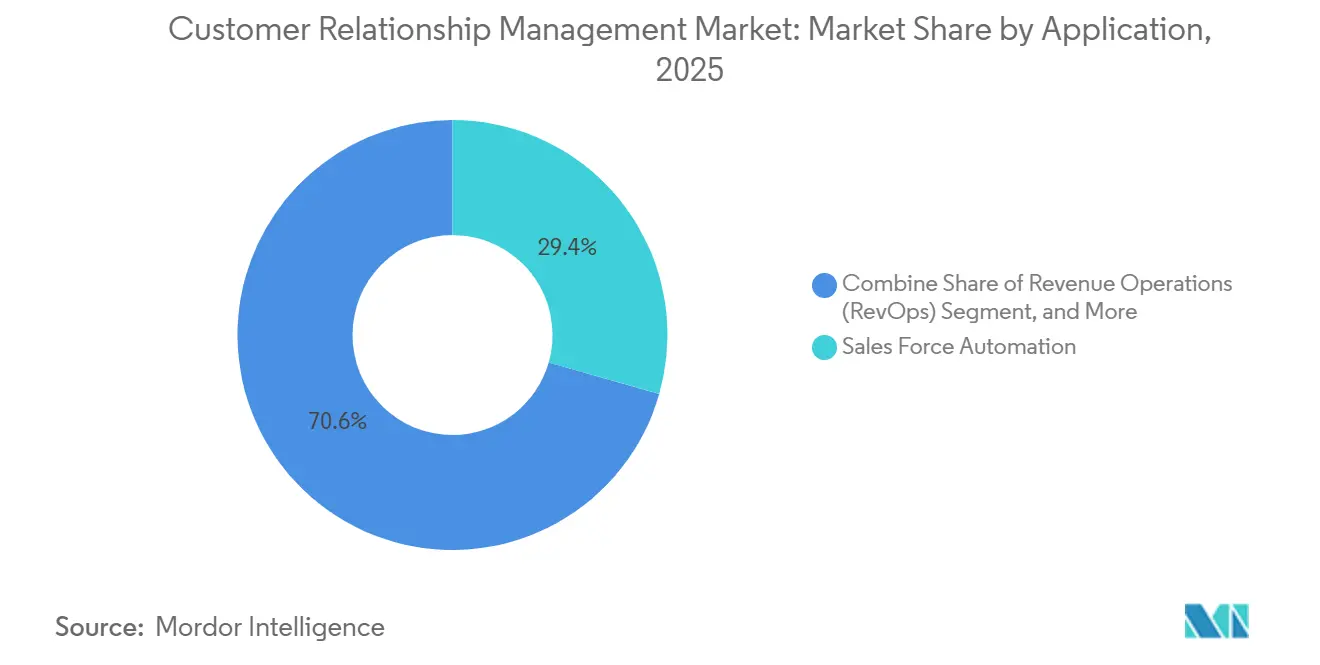

- By application, sales force automation held 29.42% share in 2025 and revenue-operations platforms are rising at an 8.03% CAGR through 2031.

- By end-user industry, BFSI led with 24.48% spending in 2025 and healthcare and life sciences are accelerating at an 8.63% CAGR through 2031.

- By geography, North America generated 44.18% revenue in 2025 and Asia Pacific is set to expand at 8.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Customer Relationship Management Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Integration of AI and Machine Learning for Predictive Insights | +1.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Accelerated Shift Toward Cloud-based Deployment | +1.5% | Global, particularly Asia Pacific and Latin America | Short term (≤ 2 years) |

| Digital Transformation Programs Among SMEs | +1.2% | Asia Pacific, Europe, Latin America | Medium term (2-4 years) |

| Omnichannel Engagement and Hyper-personalization | +1.0% | North America, Europe, Asia Pacific urban centers | Short term (≤ 2 years) |

| Vertical-specific SaaS CRM Ecosystems | +0.9% | Global, with early traction in BFSI and Healthcare | Long term (≥ 4 years) |

| Generative AI Copilots and Autonomous CRM Capabilities | +1.4% | North America, Europe, select Asia Pacific markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Integration of AI Machine Learning for Predictive Insights

Predictive models inside the Customer Relationship Management (CRM) market forecast churn, next-best actions, and deal closure probability at accuracy levels topping 80%, letting teams focus on high-value prospects. Salesforce Einstein generated more than 1 trillion predictions weekly by mid-2025, demonstrating how inference workloads have become core infrastructure rather than add-ons.[1]Salesforce Press Room, “Salesforce to Invest USD 4 Billion in Global Infrastructure,” salesforce.com Microsoft Copilot parses emails, transcripts, and CRM activity logs to suggest personalized outreach timing, lifting pilot win rates by 12%.[2]Adobe Experience Cloud Blog, “Implementation Best Practices,” adobe.com SAP’s Joule copilot allows natural-language pipeline queries, giving users instant dashboards without writing SQL. AI-generated call scripts shorten onboarding for new hires, while EU firms must document model logic under the AI Act.

Accelerated Shift Toward Cloud-based Deployment

Cloud architectures dominate the Customer Relationship Management market, removing capital expenditure and enabling pay-as-you-grow consumption. Salesforce said 87% of new implementations in 2024 were cloud-based. Oracle’s multi-cloud option lets Fusion CX run on Azure or Google Cloud, cutting lock-in risk. Hybrid remains vital for regulated sectors that keep core data on-premise while using cloud analytics engines. Low-tier SaaS plans below USD 15 per user per month spur SME uptake, and ISO 27001 or SOC 2 compliance is now baseline.

Digital Transformation Programs Among SMEs

SMEs adopt CRM at 9.54% CAGR, faster than large enterprises, because digital-first models demand single sources of customer truth from day one. Salesforce reported 78% of small firms running at least one cloud engagement tool in 2024. HubSpot’s freemium tier attracted over 200,000 new SME users the same year. India’s Digital India scheme issued subsidized cloud credits to more than 50,000 SMEs, accelerating adoption in retail and logistics. No-code workflow builders compress implementation timelines, and OECD data show integrated CRM boosts SME retention by 23%.

Generative AI Copilots and Autonomous CRM Capabilities

Generative copilots write emails, summarize conversations, and recommend products in real time, transforming CRM from a record system into a proactive advisor. Salesforce Agentforce resolves over 70% of routine inquiries without human handoff. Microsoft Copilot generates meeting recaps and updates opportunity records, saving 30% administrative effort. Adobe GenStudio produces campaign assets in hours rather than weeks. HubSpot Breeze AI blends content generation with predictive lead scoring for mid-market teams. Enterprises enforce human-in-the-loop reviews to curb hallucination risks and maintain brand tone.

Restraints Impact Analysis of Customer Relationship Management Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Total Cost of Ownership and Customization | -1.1% | Global, particularly acute in mid-market enterprises | Medium term (2-4 years) |

| Data-privacy and Compliance Complexities | -0.9% | Europe, North America, Asia Pacific (data-sovereignty markets) | Long term (≥ 4 years) |

| Vendor Lock-in Limiting Interoperability | -0.6% | Global, with concentration in multi-vendor IT environments | Long term (≥ 4 years) |

| Ethical Risks and Hallucination in AI-generated Customer Interactions | -0.5% | North America, Europe, regulated industries globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Ownership and Customization

License fees cover only 20% to 30% of overall spend as integration, data migration, and change management dominate budgets. Salesforce’s transition from Classic to Lightning in 2024 forced many customers to refactor custom components, inflating consulting bills and delaying rollouts. Proprietary code in debt collection software often becomes technical debt when vendors deprecate APIs. Ongoing costs include user training and premium tiers that unlock higher API limits. Simplified alternatives from Pipedrive or Copper lower entry prices, yet limited extensibility constrains complex sales models. Procurement cycles lengthen as buyers scrutinize total cost over multiyear horizons.

Data-Privacy and Compliance Complexities

A patchwork of laws raises overhead for firms in the Customer Relationship Management market. GDPR mandates deletion requests within 30 days and strict processing logs. California’s Privacy Rights Act grants consumers the right to correct data and opt out of automated decisions. China’s Personal Information Protection Law keeps customer data local unless explicit consent is obtained. Healthcare deployments must obey HIPAA encryption and audit requirements. Vendors chase ISO 27701 certifications and embed consent-management modules, yet regulatory change often outpaces product roadmaps, exposing firms to fines and reputational risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Customer Relationship Management Market Segment Analysis

By Component:

Services Surge as Complexity Outpaces Plug-and-Play PromisesServices are expanding at 9.52% CAGR, outperforming software despite software’s 74.12% revenue share in 2025 within the customer relationship management (CRM) market. Implementation contracts dominate as enterprises wire CRM to ERP, e-commerce, and data warehouses. Consulting teams map customer journeys and configure dashboards that match hierarchies. Training and support attract SMEs lacking in-house admins, while managed services grow fastest among firms preferring outsourced platform upkeep.

Software continues to innovate through no-code builders and industry templates, yet diverse use cases keep bespoke work common. Salesforce’s professional-services arm generated more than USD 1.5 billion in fiscal 2025. Adobe Experience Cloud rollouts often require integrators for 6-12 months.[3]Microsoft Official Blog, “Dynamics 365 Copilot General Availability,” microsoft.com Regulatory friction is limited, though managed-service providers in healthcare or finance need ISO 27001 and SOC 2 clearance.

By Deployment Mode:

Hybrid Architectures Reconcile Cloud Agility With Data SovereigntyCloud commanded 80.16% share in 2025, led by public-cloud uptake across North America and Western Europe in the CRM market. Private-cloud persists where data-residency rules dominate, and on-premise remains mainly within government entities. Hybrid architectures are rising at 9.04% CAGR, pairing on-premise storage with cloud analytics to access GPUs for AI-driven insight.

IBM offers hybrid CRM on Red Hat OpenShift, syncing local data with Watson AI services. The Digital Markets Act forces gatekeepers to open APIs, smoothing hybrid integration. FedRAMP and C5 certifications elevate vendor costs but deter smaller rivals. Multi-cloud distribution mitigates outage risk and pricing leverage, with Oracle and SAP each supporting rival clouds.

By Organization Size:

SMEs Accelerate Adoption Through No-Code Tools and Freemium TiersLarge enterprises held 62.66% spending in 2025 in the customer relationship management market, thanks to complex hierarchies and global footprints. They deploy broad suites that span sales, service, and marketing and invest heavily in customization.

SMEs are moving faster, however, with a 9.54% CAGR through 2031. HubSpot’s free tier drew over 200,000 SME sign-ups in 2024. Zoho Canvas lets non-technical staff create workflows by dragging and dropping components. India’s Digital India incentives further fuel SME adoption. OECD research links integrated CRM to 23% higher retention among small firms. The shift signals that centralized customer data is now foundational even for startups.

By Application:

Revenue Operations Unifies Pipeline Visibility Across FunctionsSales force automation remained the largest application at 29.42% of deployments in 2025. Marketing automation, customer service suites, and commerce engines round out core modules, each leveraging shared customer data to personalize journeys.

Revenue-operations platforms are growing at 8.03% CAGR as finance leaders seek unified pipeline insight in the customer relationship management market. Clari raised USD 150 million in 2024 to expand RevOps analytics. Salesforce embedded revenue intelligence into Sales Cloud in 2025. HubSpot’s RevOps Hub synchronizes leads, opportunities, and renewals for single-source reporting. Convergence reflects buyer fatigue with tool sprawl and desire for consolidated vendor contracts.

By End-user Industry:

Healthcare Surges on Patient Engagement and Telehealth IntegrationBFSI spent 24.48% of total in 2025, leveraging CRM to manage wealth customers and insurance renewals. Retail, telecom, manufacturing, media, and professional services follow with varied use cases.

Healthcare and life sciences are the fastest growers at 8.63% CAGR. Salesforce Health Cloud connects to Epic and Cerner records, giving coordinators unified patient views. Veeva CRM tracks pharmaceutical rep interactions under compliance codes. The U.S. Department of Health and Human Services linked integrated CRM-EHR deployments to an 18% drop in no-show rates. Strict HIPAA safeguards deter new entrants, benefiting established vendors.

Geography Analysis

North America Customer Relationship Management Market

North America generated 44.18% of Customer Relationship Management market revenue in 2025. U.S. enterprises adopt full-suite platforms that merge sales, service, and commerce, supported by dense SaaS ecosystems. Salesforce earned more than USD 34 billion in fiscal 2025 with roughly 60% bookings from the region. The California Privacy Rights Act imposes consent-management and data-correction duties, yet legal clarity and mature data centers sustain leadership.

APAC Customer Relationship Management Market

Asia Pacific will expand at 8.86% CAGR to 2031, the fastest regional pace. India’s cloud-credit vouchers and training support more than 50,000 SMEs, catalyzing adoption. China’s Personal Information Protection Law obliges local data storage, creating openings for domestic vendors like Kingdee and UFIDA. Japan migrates from on-premise to cloud CRM, while Singapore positions itself as a SaaS hub for Southeast Asia. Diverse languages and regulations complicate rollouts, yet e-commerce expansion keeps demand strong.

EMEA and LATAM Customer Relationship Management Market

Europe contributes a mid-tier share anchored by Germany, the United Kingdom, and France. GDPR enforces deletion rights and stringent consent, raising compliance budgets but leveling the playing field. The Digital Markets Act requires gatekeepers to provide data portability and API access, lowering switching costs and encouraging challenger platforms. Russia’s segment contracted after vendor exits, whereas the Middle East and Africa show pockets of growth as governments digitize citizen services. Latin America gains momentum through Brazilian and Mexican omnichannel retail investment in the CRM market.

Competitive Landscape

Global revenue is moderately concentrated for the customer relationship management market. Salesforce, Microsoft, SAP, Oracle, and Adobe together held roughly 55-60% of the Customer Relationship Management market in 2025. Salesforce sustains lead via continuous platform extension, integrating Slack collaboration and unveiling Agentforce autonomous agents. Microsoft exploits its Office and Azure estates, embedding Copilot across Dynamics 365. Oracle pursues vertical depth, integrating Cerner’s assets into healthcare CRM. Adobe combines Real-Time CDP with GenStudio to streamline creative workflows. SAP appeals to manufacturers seeking single-vendor ERP-CRM stacks.

Challengers focus on niches. HubSpot, Zoho, Freshworks, and Zendesk court SMEs with freemium entry and simple pricing. Clari specializes in revenue intelligence, aggregating pipeline data to forecast cash flow. Interoperability battles intensify after the Digital Markets Act forced gatekeepers to publish APIs. Patent filings reveal competition in AI-driven lead scoring, sentiment analysis, and autonomous agents; Salesforce alone filed more than 200 AI patents in 2024.[4]U.S. Patent and Trademark Office, “Salesforce AI Patent Filings 2024,” uspto.gov Market concentration is stable yet open to disruption through vertical specialization and AI-native design.

Customer Relationship Management Industry Leaders

Salesforce, Inc.

Microsoft Corporation

SAP SE

Oracle Corporation

Adobe Inc.

- *Disclaimer: Major Players sorted in no particular order

Customer Relationship Management Market Companies Covered in this Report

- Salesforce, Inc.

- Microsoft Corporation

- SAP SE

- Oracle Corporation

- Adobe Inc.

- HubSpot, Inc.

- Zoho Corporation Pvt. Ltd.

- Zendesk, Inc.

- Freshworks Inc.

- SugarCRM Inc.

- Pipedrive Inc.

- Insightly, Inc.

- Copper CRM, Inc.

- monday.com Ltd.

- Keap Inc. (Infusionsoft)

- The Sage Group plc

- Infor, Inc.

- International Business Machines Corporation

- ServiceNow, Inc.

- Pegasystems Inc.

- NICE Ltd.

- Genesys Telecommunications Laboratories, Inc.

- Creatio EMEA Ltd.

- Bitrix24 Ltd.

- VTiger CRM, Inc.

- Epicor Software Corporation

- Aptean, Inc.

- Intercom, Inc.

- Gainsight, Inc.

Recent Industry Developments in Customer Relationship Management Market

- January 2026: Salesforce committed USD 4 billion to expand data-center capacity across Europe, Japan, and Australia to support Agentforce and Einstein workload demand.

- November 2025: Microsoft embedded Copilot into Dynamics 365 Sales, Customer Service, and Marketing, with early adopters citing 15-20% administrative savings.

- May 2025: Microsoft reported USD 70.1 billion Q3 2025 revenue, with Dynamics 365 up 16% year-over-year.

- April 2025: SAP recorded 27% cloud revenue expansion to EUR 4.99 billion in Q1 2025.

Customer Relationship Management Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the global Customer Relationship Management (CRM) market as all licensed or subscription-based software, cloud, on-premise, or hybrid, designed to record, manage, and analyze customer interactions across marketing, sales, service, and digital commerce. According to Mordor Intelligence, revenues counted include core suites and add-on analytics modules sold as discrete CRM products and exclude generic databases and telephony hardware marketed without CRM functionality.

Scope Exclusions: Spend on custom integration projects, standalone email service providers, and contact-center hardware lies outside our coverage.

Segments Covered in This Report

- By Component

- Software

- Sales Force Automation Platforms

- Marketing Automation Platforms

- Customer Service and Support Suites

- Customer Data Platforms

- Digital Commerce Engines

- Analytics and Insights Tools

- Services

- Implementation and Integration

- Consulting

- Training and Support

- Managed Services

- Software

- By Deployment Mode

- Cloud

- Public Cloud

- Private Cloud

- Multi-cloud

- On-premise

- Hybrid

- Cloud

- By Organization Size

- Small and Medium Enterprises

- Large Enterprises

- By Application

- Sales Force Automation

- Marketing Automation

- Customer Service and Support

- Digital Commerce

- Analytics and Insights

- Revenue Operations (RevOps)

- Partner Relationship Management

- By End-user Industry

- BFSI

- Retail and E-Commerce

- Healthcare and Life Sciences

- IT and Telecom

- Manufacturing

- Media and Entertainment

- Professional Services

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Malaysia

- Singapore

- Australia

- Rest of Asia Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interviewed software vendors, implementation partners, CIOs of large enterprises, and SMB owners across North America, Europe, Asia-Pacific, and Latin America. These conversations refined average selling prices, typical seat counts, and emerging purchase triggers, closing gaps flagged during desk work.

Desk Research

We start with public datasets such as UN Comtrade software trade codes, World Bank Enterprise Surveys for firm density, and OECD ICT indicators that reveal cloud adoption by industry. Additional insight comes from bodies such as the Software & Information Industry Association, U.S. Bureau of Labor Statistics, and the European Telecommunications Network Operators Association, giving payroll and digitalization ratios that anchor the user pool. Paid repositories like D&B Hoovers and Dow Jones Factiva supply fresh vendor revenues and funding rounds, which we cross-check against SEC 10-Ks and investor decks. The sources cited are illustrative; many other references support data collection, validation, and clarification.

Market-Sizing & Forecasting

A single top-down build, enterprise counts × CRM penetration × weighted ASP creates the core model, which is then sense-checked through selective bottom-up supplier roll-ups. Key inputs include cloud-migration share, median license price per user, regional GDP per employee, digital-transformation spend ratios, and churn-to-replacement cycles. Forecasts rely on multivariate regression blended with scenario analysis so we can test outcomes against IT spend or currency shocks; missing granular data is bridged with elasticity factors discussed in expert calls.

Data Validation & Update Cycle

Outputs run through variance dashboards that flag deviations above five percent versus trendlines and external benchmarks. Senior reviewers challenge anomalies before sign-off. Reports refresh annually, with interim updates triggered by material M&A, regulation, or macro shocks, ensuring clients receive our most current view.

How Mordor Intelligence's Customer Relationship Management Market Size Compares to Other Published Estimates

Published estimates often diverge because firms mix services with software, adopt region-specific samples, or freeze exchange rates at different points. Our disciplined scope, yearly refresh, and dual validation steps keep the 2025 baseline dependable.

Key gap drivers include whether professional-services revenue is bundled, the aggressiveness of cloud-only growth assumptions, and the currency conversion month selected.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 81.20 B | Mordor Intelligence | - |

| USD 112.91 B | Global Consultancy A | Bundles implementation services; 18-month refresh cadence |

| USD 82.43 B | Industry Association B | Scales five-country data to global without weighting emerging markets |

Ultimately, clients gain a balanced, transparent baseline because every Mordor figure traces back to reproducible public statistics or clearly documented interview inputs, giving decision-makers dependable numbers they can defend.

Key Questions Answered in the Report

What is the current value of the Customer Relationship Management (CRM) market?

The CRM market stands at USD 87.96 billion in 2026 and is forecast to reach USD 128.86 billion by 2031.

Which region is growing fastest for CRM adoption?

Asia Pacific is projected to expand at an 8.86% CAGR through 2031, driven by India’s cloud incentives and China’s local-data mandates.

Why are services outpacing software in growth?

Integration, consulting, and managed-service demand is rising, pushing services to a 9.52% CAGR as firms grapple with complex deployments.

How are SMEs benefiting from modern CRM tools?

Freemium tiers, no-code builders, and government cloud credits enable SMEs to adopt CRM quickly, fueling a 9.54% CAGR within that segment.

What role does generative AI play in CRM today?

Copilots such as Salesforce Agentforce and Microsoft Copilot draft emails, resolve tickets, and forecast pipeline health, cutting administrative work and accelerating decisions.

Which end-user industry is growing fastest?

Healthcare and life sciences lead with an 8.63% CAGR by integrating CRM with electronic health records for proactive patient engagement.

Page last updated on: