Thailand Tire Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

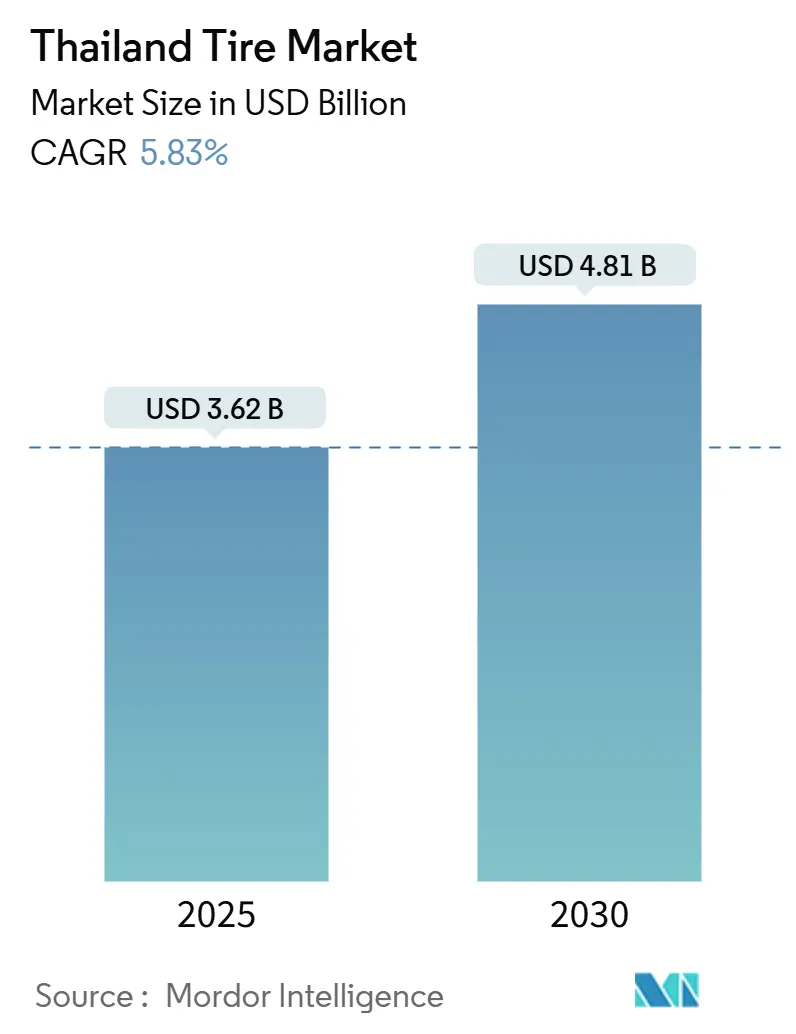

| Market Size (2025) | USD 3.62 Billion |

| Market Size (2030) | USD 4.81 Billion |

| Growth Rate (2025 - 2030) | 5.83% CAGR |

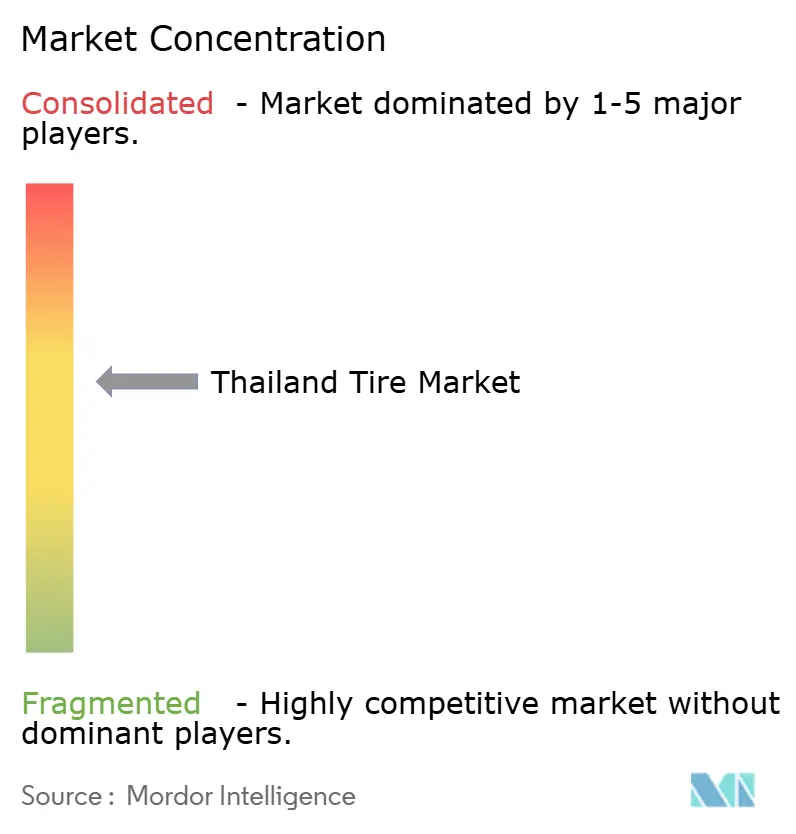

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Tire Market Analysis by Mordor Intelligence

The Thailand Tire Market size is estimated at USD 3.62 billion in 2025, and is expected to reach USD 4.81 billion by 2030, at a CAGR of 5.83% during the forecast period (2025-2030). Positive momentum stems from Thailand’s status as Southeast Asia’s largest vehicle producer, the world’s second-largest tire production center, and the leading natural-rubber supplier. Government EV incentives, robust export linkages into Europe and the United States, and a resilient aftermarket anchored in an aging vehicle parc all reinforce demand. At the same time, elevated natural rubber prices, new EU deforestation rules, and counterfeit imports apply cost and margin pressure. Market opportunities concentrate around EV-specific tires, larger rim sizes for pickups and SUVs, and premium radial technology targeted at mandatory tire-labeling rules. Manufacturers leverage the Eastern Economic Corridor for scale economies, deep-water port access, and preferential investment terms while rapidly aligning portfolios toward battery-electric vehicles.

Key Report Takeaways

- By season, all-season tires captured 53.24% of the Thailand tire market share in 2024, while winter tires are projected to record the fastest growth at a 5.85% CAGR through 2030.

- By tire design, radial technology led with 87.65% of the Thailand tire market share in 2024, whereas Non-pneumatic / Airless is forecasted to grow at a CAGR of 5.87% through 2030.

- By vehicle type, passenger cars accounted for 45.54% of the Thailand tire market size in 2024 and are forecast to advance at a 5.91% CAGR through 2030.

- By application, on-road products held 83.21% of the Thailand tire market share in 2024; off-road tires are forecast to expand at a 5.93% CAGR by 2030.

- By end user, the aftermarket commanded 63.47% of the Thailand tire market share in 2024, and OEM is forecasted to grow at a 5.94% CAGR till 2030.

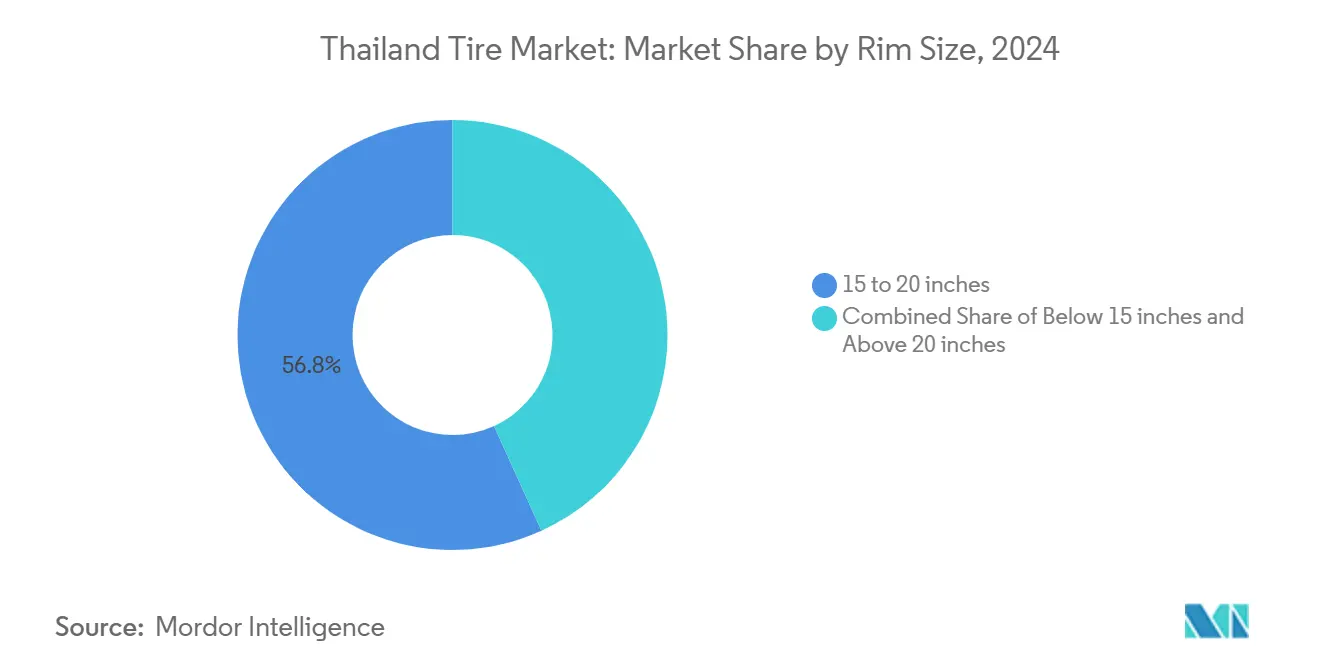

- By rim size, 15–20-inch products captured a 56.82% share of the Thailand tire market in 2024. The market for tires above 20 inches is forecasted to grow at a 5.89% CAGR through 2030.

- By propulsion, internal combustion vehicles led with 86.71% share of the Thailand tire market in 2024, whereas battery-electric cars are set to post the fastest segment CAGR at 5.88% through 2030.

Thailand Tire Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government EV-Subsidy Program | +1.2% | National, concentrated in Bangkok and EEC provinces | Medium term (2-4 years) |

| Rapid E-Commerce Growth | +0.9% | Urban centers, expanding to provincial areas | Short term (≤ 2 years) |

| Tourism Rebound | +0.7% | Tourism hubs including Bangkok, Phuket, Chiang Mai | Short term (≤ 2 years) |

| OEM Shift To Larger Rim Sizes | +0.6% | National, aligned with production centers | Medium term (2-4 years) |

| Rise Of Ride-Hailing Two-Wheeler Fleets | +0.5% | Urban areas with expanding service coverage | Short term (≤ 2 years) |

| Mandatory Tire-Labeling Regulations Favoring Premium Radials | +0.4% | National implementation | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government EV-Subsidy Program Boosting BEV Tire Demand

Thailand’s EV 3.5 policy grants purchase THB 50,000–100,000 subsidies and cuts excise tax to a minimum, translating into a projected two-fifths jump in EV registrations during 2025[1]“EV 3.5 Policy Summary,” Thailand Board of Investment, boi.go.th. Heavier battery packs force automakers to specify tires with two-fifths higher load ratings and ultra-low rolling resistance compounds. A local-assembly rule multiple vehicles built domestically for every imported unit by December 2026—has attracted BYD and GAC Aion, whose combined Thai capacity tops almost 2 lakh units. Concentrated production in Chonburi and Rayong funnels predictable demand toward nearby tire plants. The continued rollout of public fast chargers will determine how far EV penetration will spread beyond Bangkok.

Rapid E-Commerce Growth Driving Last-Mile LCV Tire Volumes

Thailand’s e-commerce turnover is rising at double-digit rates, pushing platforms such as Grab and Skootar to deploy motorcycles and small vans that operate 8–12 hours daily and average 43 kilometers in Bangkok traffic. High utilization compresses replacement cycles, lifting light commercial and two-wheeler tire volumes. Fleet operators increasingly request high-durability compounds and extended mileage warranties, although price sensitivity keeps ultra-premium adoption in check. Urban logistics thus offers scale to medium-tier radial makers while allowing premium brands to pilot fleet-service contracts that prove total cost-of-ownership savings.

Tourism Rebound Accelerating Rental-Car Fleet Renewals

International arrivals surpassed pre-pandemic levels in 2025, swelling rental-car revenue exponentially. Enterprise Mobility’s partnership with Thai Rent-A-Car demonstrates foreign confidence, with the operator managing over 8,000 vehicles. Cars in rental duty typically retire tires every 40,000–60,000 kilometers, guaranteeing predictable aftermarket pull. All-season tread patterns with strong wet-grip ratings suit coastal and mountainous routes frequented by tourists. The seasonal tourism peaks in Phuket and Chiang Mai compel distributors to maintain buffer inventories that avoid stock-outs during high-demand months.

OEM Shifts to Larger Rim Sizes for SUVs & Pickups

Manufacturers building for export - Toyota, Isuzu, and Ford now fit 15–20-inch rims on mainstream pickup and SUV lines, giving this bracket more than half of Thailand's tire market share in 2024. Lower-profile sidewalls call for stronger bead packages and advanced carcass reinforcements that limit deformation on uneven roads. Average selling prices rise accordingly, enhancing revenue per unit even as longer-lasting compounds marginally stretch replacement intervals. Road-damage risk does increase on poorer rural surfaces, which may lift demand for tire-insurance products and spur OEMs to co-develop more rigid constructions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated Natural-Rubber Price Volatility | -0.8% | Global supply chain impact, concentrated in manufacturing regions | Short term (≤ 2 years) |

| Counterfeit & Grey-Market Tires Eroding Branded Sales | -0.6% | National, particularly in price-sensitive segments | Medium term (2-4 years) |

| High Import Duty | -0.4% | National, affecting mining and agricultural sectors | Medium term (2-4 years) |

| Slow Deployment Of Public Fast-Charging | -0.3% | Urban centers with gradual expansion to provinces | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Elevated Natural-Rubber Price Volatility

Benchmark RSS-3 rubber touched 12-year highs in early 2025 as growers raced to comply with EU deforestation rules restricting imports from newly cleared land. Thai tire plants enjoy proximity to plantations, yet still absorb higher feedstock costs because synthetic substitutes cannot fully replace natural rubber in heavy-duty truck and aviation applications. Premium brands manage risk via long-term supply deals and digital traceability tools, but margin erosion persists in price-sensitive domestic segments where pass-through is limited. Currency swings compound volatility by inflating dollar-denominated raw-material invoices when the baht weakens.

Counterfeit & Grey-Market Tires Eroding Branded Sales

Customs seizures of relabeled imports underscore Thailand’s struggle with counterfeit tires that undercut authorized dealers by up to two-fifths[2]“Counterfeit Tire Seizure Report 2025,” Royal Thai Customs, customs.go.th . Such products carry unverifiable safety credentials, tarnish brand reputation, and distort competition. Enforcement stepped up in 2024, yet porous borders and flourishing informal channels keep illicit flows alive. Premium manufacturers push QR-code verification on sidewalls and collaborate with e-commerce platforms to delist suspect sellers. Nevertheless, the grey market’s presence constrains pricing power and forces legitimate manufacturers to extend promotions in rural zones where price overrides safety.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Season: All-Season Dominance Reflects Climate Consistency

All-season patterns captured 53.24% of the Thailand tire market in 2024, benefiting from the country’s year-round tropical climate that removes the need for seasonal swaps. Winter tire shipments, however, are rising at a 5.85% CAGR through 2030, driven by export contracts servicing Europe and North America. This incremental production supports the Thailand tire market size by broadening factory load factors and justifying new specialized curing presses. Continental’s Rayong expansion dedicates multiple curing lines to studdable winter designs meeting the EU mandate.

Export-oriented winter output illustrates how Thai plants leverage economies of scale while domestic motorists remain firmly committed to all-season treads. Summer performance tires cater to a niche of enthusiasts and luxury import owners who account for a small but profitable channel. Meanwhile, monsoon-grade compounds with high silica content differentiate Thai all-season offerings, delivering superior wet grip on oil-slick roads. This blend of domestic stability and export diversification underpins resilient utilization across seasonal categories.

By Tire Design: Radial Technology Maintains Manufacturing Leadership

Radial casings delivered 87.65% of the Thailand tire market in 2024, underscoring the country’s world-class steel belt, cord fabric, and precision molding infrastructure. Non-pneumatic airless designs are advancing at a 5.87% CAGR through 2030, as Bridgestone pilots airless bus tires on Bangkok BRT routes and Michelin tests Tweel platforms for agricultural implements. Bias-ply formats persist in niche agriculture and mining, where price and repairability still trump high-speed performance.

Investment in high-strength aramid and eco-friendly resin matrices positions Thai plants to mass-produce next-generation airless tires once commercialization hurdles fall. In parallel, radial producers push for lighter, “green” composites that lower rolling resistance by up to 15%, aligning with OEM carbon-reduction targets. Domestic R&D alliances between universities and suppliers focus on bio-based elastomers derived from Thai latex exports, reinforcing supply independence and lowering lifecycle emissions.

By Vehicle Type: Passenger Cars Lead Amid Production Rebound

Passenger-car fitments controlled 45.54% of the Thailand tire market in 2024 and will grow at a 5.91% CAGR through 2030, making them the prime contributor to the market's size growth. The segment demonstrates resilience despite a one-fifth drop in auto assemblies in 2024 after banks tightened credit. E-commerce fueled light commercial vehicle demand, while heavy trucks benefited from cross-border trade recovery with Malaysia and Cambodia.

Motorcycle tires remain vital given Thailand’s two-wheeler output, projected to grow exponentially in 2025. Off-the-road tire demand tracks commodity cycles; mining rebound in Phichit and agricultural mechanization in Nakhon Sawan sustain specialty segments. Manufacturers fine-tune product mixes, balancing high-volume passenger lines with higher-margin specialty runs that stabilize earnings through downturns.

By Application: On-Road Dominance Mirrors Urban Mobility Needs

On-road applications represented 83.21% of the Thailand tire market in 2024, reflecting intensive passenger and freight flows across Thailand’s expressway network. Off-road demand is expected to grow at a 5.93% CAGR due to mining concessions in Loei and continued sugarcane farm mechanization. Urban road congestion promotes low-rolling-resistance compounds that reduce fuel and electricity consumption, while rural transport operators value robust casings resisting pothole impact.

Government road-upgrade programs under Thailand 4.0 funnel investment into secondary highways, which should gradually raise speed limits and accelerate tread wear. Meanwhile, off-road buyers seek cut-resistant sidewalls and deep lugs adaptable to wet soil, extending product lifecycles in harsh conditions. This dual demand guides plant scheduling, ensuring mold inventories cover touring radials and aggressive lug patterns.

By End User: Aftermarket Replacement Drives Volume Growth

Replacement channels captured 63.47% of the Thailand tire market in 2024, propelled by an average passenger-car age of 11.2 years and challenging road conditions that trim service life. The OEM pathway rebounds at 5.94% CAGR as automakers step up EV assembly to meet subsidy conditions. Replacement volumes anchor cash flow because sales are spread across more than 8,000 independent retailers nationwide, limiting exposure to any single customer.

Retread operators offer cost-effective truck solutions, yet face competition from imported low-cost new tires that narrow price gaps. Digital fitment platforms now link fleets with service centers, enabling predictive replacement scheduling and boosting premium-tier uptake. On the OEM side, tire makers secure vehicle-launch nominations years in advance, locking in baseline volumes and technology-transfer agreements that enrich domestic technical skill sets.

By Rim Size: Mid-Range Sizes Reflect Market Preferences

Rims of 15–20 inches contributed 56.82% to Thailand's tire market share in 2024, capturing the sweet spot for pickups, SUVs, and mid-size passenger cars. Above-20-inch products will expand 5.89% CAGR, following premium-vehicle import growth and export-oriented luxury assembly. Below-15-inch sizes remain essential for budget sedans and the sizable used-car fleet, where owners prioritize affordability.

Increasing rim diameters necessitate ultrahigh-tensile bead wires and aramid-reinforced sidewalls to maintain ride comfort on uneven routes. Manufacturers invest in multi-stage bead-forming lines and advanced pressure-monitoring systems integral to larger wheels. Upsizing also aligns with automakers’ aesthetic push, elevating curb appeal and therefore tire ASPs, supporting revenue expansion even if aggregate unit volume plateaus.

By Propulsion: ICE Vehicles Retain Scale as EV Tires Surge

Internal combustion platforms accounted for 86.71% of 2024 sales. Still, the EV segment posts the highest 5.88% CAGR, paving the way for differentiated products such as foam-lined acoustic tires that suppress electric drivetrain noise. Plug-in hybrids keep a foothold as range-anxiety mitigators, while fuel-cell trials remain nascent. EV tire production relies on high-load index constructions and silica-rich treads that cut rolling resistance by roughly one-fifths.

Thai plants now integrate automated visual-inspection stations to detect the slightest uniformity issues that could amplify torque ripple in EVs. Battery-friendly tires also enhance regenerative-braking efficiency, a selling point carmakers emphasize in showroom brochures. The parallel coexistence of ICE and EV tires compels factories to run flexible curing schedules capable of flipping molds within hours to satisfy varied carcass widths and bead diameters.

Geography Analysis

Eastern Economic Corridor provinces, Chachoengsao, Chonburi, and Rayong contribute significant national output, hosting Bridgestone, Continental, Sumitomo Rubber, and Prinx Chengshan plants clustered near Laem Chabang Port[3]“EEC Investment Incentives,” Thailand Board of Investment, boi.go.th . This agglomeration leverages SEZ tax holidays, shared logistics, and a vocational talent pool specializing in polymer science and precision engineering. Proximity to Bangkok’s metropolitan region ensures steady replacement demand while global exports flow efficiently through deep-water berths.

Bangkok delivers the most significant slice of Thailand's tire market demand due to the country’s highest vehicle density and ride-hailing saturation. Stop-start traffic and elevated ambient temperatures accelerate tread wear, pushing motorists toward value-oriented radials offering extended mileage warranties. Fleet operators centralize procurement through digital platforms that aggregate orders for taxis, delivery vans, and corporate sedans, creating predictable uptake for tire makers with urban warehouse presence.

Northern provinces, Chiang Mai, Lampang, and Chiang Rai, generate mixed demand from tourism vans, agricultural pickups, and all-terrain motorcycles serving hillside farming areas. Tourism seasonality forces distributors to anticipate peak holiday surges by staging inventory months ahead. Southern coastal hubs, Phuket, Surat Thani, and Songkhla, require salt-resistant compounds for resort shuttle buses and fishing-industry trucks exposed to corrosive sea spray. Cross-border haulage into Malaysia adds traffic that further lifts replacement cycles in these provinces.

Competitive Landscape

Global majors Bridgestone, Continental, and Michelin anchor technology leadership through integrated latex plantations, in-house synthetic rubber, and dedicated R&D centers that adapt compounds to Thailand’s tropical climate. Their combined share exceeds two-fifths of the total. However, emerging Chinese entrants such as Prinx Chengshan and Zhongce Rubber chip away by pitching cost-competitive radials with export-grade certifications. Moderate regulatory barriers on foreign capital encourage joint ventures that import turnkey production lines and leverage Thailand’s skilled labor.

Differentiation increasingly revolves around EV-specific tires and airless technology pilots. Bridgestone showcases Enliten lightweight compounds, while Continental deploys ContiSilent acoustic foams to cut cabin noise in premium EVs. Local players invest in digital traceability systems, aligning with EU anti-deforestation statutes, using blockchain to document latex provenance, giving them an advantage over low-cost grey-market competitors.

Distribution networks remain fragmented. Tier-one brands operate branded retail chains such as Cockpit (Bridgestone) and BestDrive (Continental) that guarantee service quality, while multibrand independents dominate provincial markets where price competition is fiercest. Online marketplaces capture younger consumers, prompting tire makers to roll out click-and-install platforms that link e-sales with partner garages. Competitive intensity thus balances technology races with channel innovation and supply-chain compliance.

Thailand Tire Industry Leaders

Bridgestone Corporation

Michelin SCA

Goodyear Tire & Rubber Co.

Yokohama Rubber Co.

Continental AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Yanggu Huatai broke ground on a new manufacturing plant in the Eastern Economic Corridor, adding annual capacity of 6 million passenger-car tires.

- October 2024: Continental completed phase one of its THB 13 billion Rayong expansion, unlocking 3 million tires annually and 600 skilled jobs.

Thailand Tire Market Report Scope

| Summer |

| Winter |

| All-Season |

| Radial |

| Bias |

| Non-pneumatic / Airless |

| Two-Wheelers |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Trucks & Buses |

| Off-the-Road & Specialty (OTR, Agriculture, Mining, Racing) |

| On-Road |

| Off-Road |

| OEM |

| Aftermarket |

| Below 15 inches |

| 15 – 20 inches |

| Above 20 inches |

| Internal-Combustion Vehicles |

| Battery-Electric Vehicles |

| Hybrid & Fuel-Cell Vehicles |

| By Season | Summer |

| Winter | |

| All-Season | |

| By Tire Design | Radial |

| Bias | |

| Non-pneumatic / Airless | |

| By Vehicle Type | Two-Wheelers |

| Passenger Cars | |

| Light Commercial Vehicles | |

| Heavy Commercial Trucks & Buses | |

| Off-the-Road & Specialty (OTR, Agriculture, Mining, Racing) | |

| By Application | On-Road |

| Off-Road | |

| By End User | OEM |

| Aftermarket | |

| By Rim Size | Below 15 inches |

| 15 – 20 inches | |

| Above 20 inches | |

| By Propulsion | Internal-Combustion Vehicles |

| Battery-Electric Vehicles | |

| Hybrid & Fuel-Cell Vehicles |

Key Questions Answered in the Report

How significant is Thailand’s tire segment in 2025?

The segment is valued at USD 3.62 billion in 2025.

What annual growth rate is forecast for Thai tire sales to 2030?

Sales are projected to rise at a 5.83% CAGR through 2030.

Which tire type leads by design in Thailand?

Radial constructions dominate with 87.65% share of 2024 volumes.

What share do all-season tires hold in Thai demand?

All-season patterns accounted for 53.24% of 2024 shipments.

Which propulsion category is expanding fastest for Thai tire suppliers?

Battery-electric vehicle fitments are set to post a 5.88% CAGR to 2030.

Why is the Eastern Economic Corridor significant to tire producers?

The corridor hosts most major plants, offers port access, and supplies over two-thirds of national output.

Page last updated on: