China Tyre Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

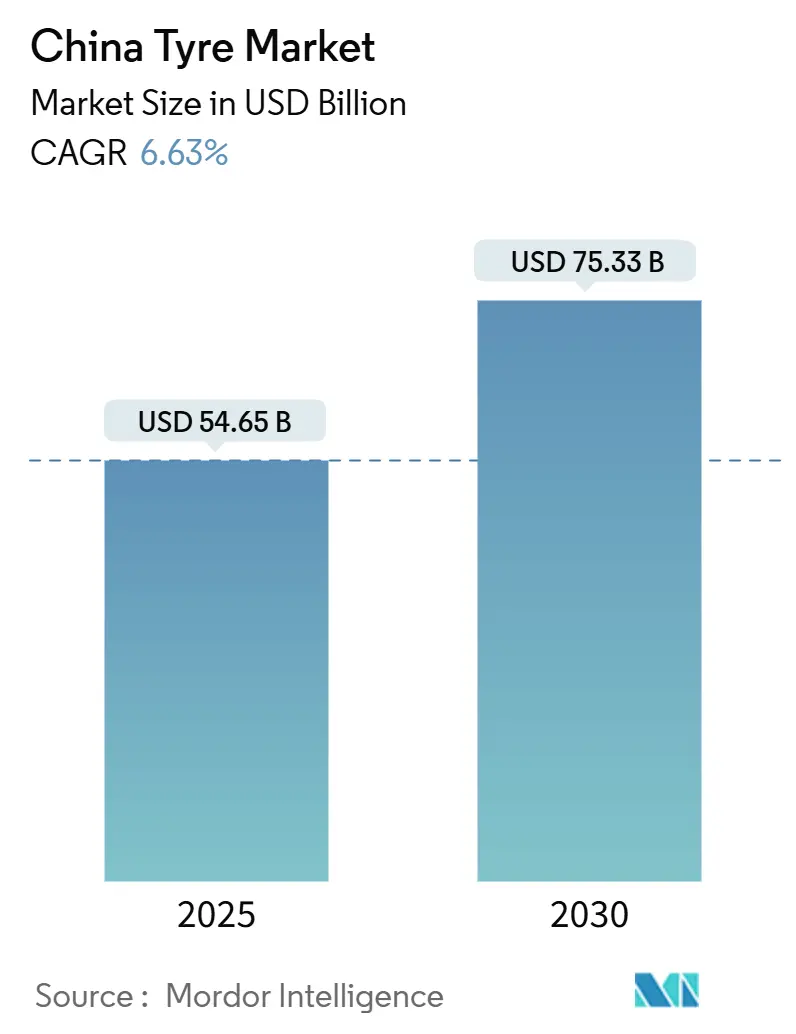

| Market Size (2025) | USD 54.65 Billion |

| Market Size (2030) | USD 75.33 Billion |

| Growth Rate (2025 - 2030) | 6.63% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Tyre Market Analysis by Mordor Intelligence

The Chinese tyre market size stood at USD 54.65 billion in 2025 and is forecast to reach USD 75.33 billion by 2030, advancing at a 6.63% CAGR in that period. Consistent demand stems from an expanding vehicle parc, rapid electric-vehicle (EV) penetration, and continuing infrastructure investments that lift commercial and specialty volumes. Competitive intensity remains high because domestic producers command scale advantages yet contend with raw-material volatility, synthetic-rubber shortfalls, and anti-dumping actions in several export destinations. Policy-driven premiumization also shapes product roadmaps as tougher GB-9743/9744 rules drive compound upgrades, while digital B2B platforms streamline distribution and reinforce pricing transparency. Notably, the Chinese tyre market has moved beyond pure volume metrics; the primary value opportunity now sits in ultra-high-performance, EV-specific, and smart-sensor-enabled products that combine durability with energy efficiency.

Key Report Takeaways

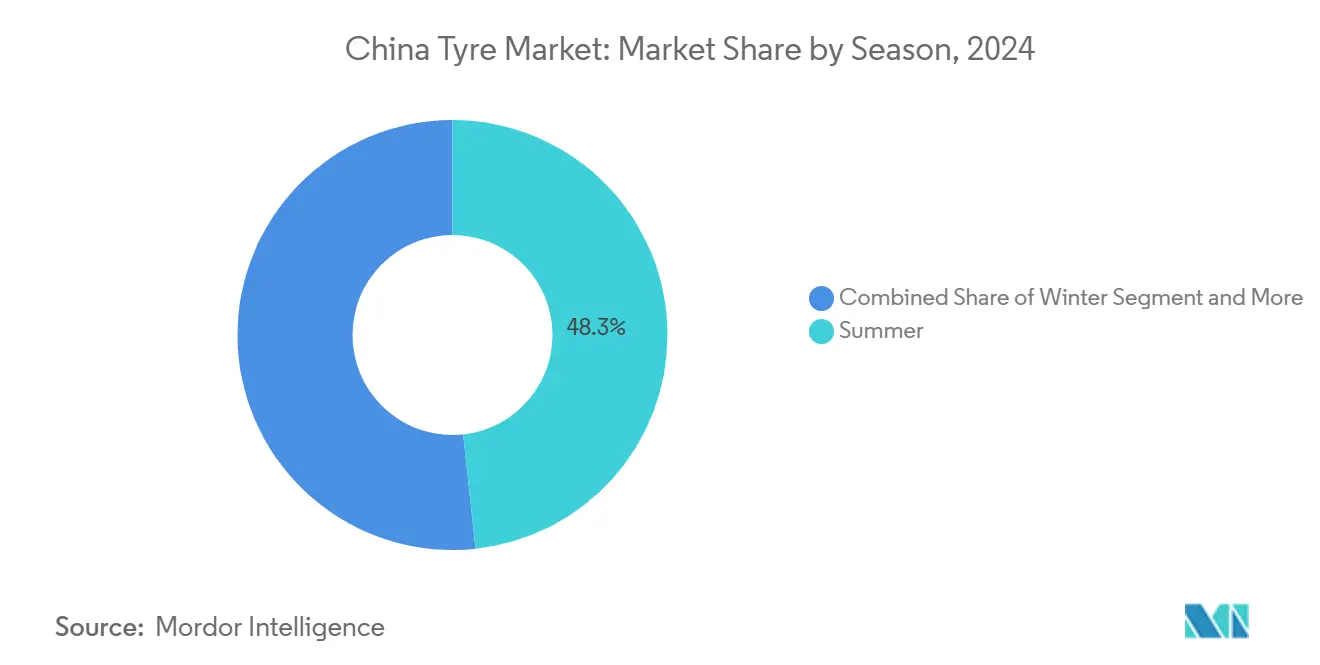

- By season, summer tyres led with 48.33% of the Chinese tyre market share in 2024, while all-season designs are projected to grow at a 7.94% CAGR to 2030.

- By tire design, radial formats held 91.26% of the Chinese tyre market share in 2024 and are expected to post a 6.96% CAGR through 2030.

- By vehicle type, passenger-car fitments captured 62.55% of the China tyre market share in 2024; the off-the-road segment is forecast to expand at a 7.16% CAGR through 2030.

- By application, on-road tyres accounted for 77.41% of the Chinese tyre market size in 2024, whereas off-road applications are advancing at a 7.54% CAGR to 2030.

- By end user, the aftermarket held a 69.24% of the China tyre market share in 2024 and is growing at an 8.05% CAGR through 2030.

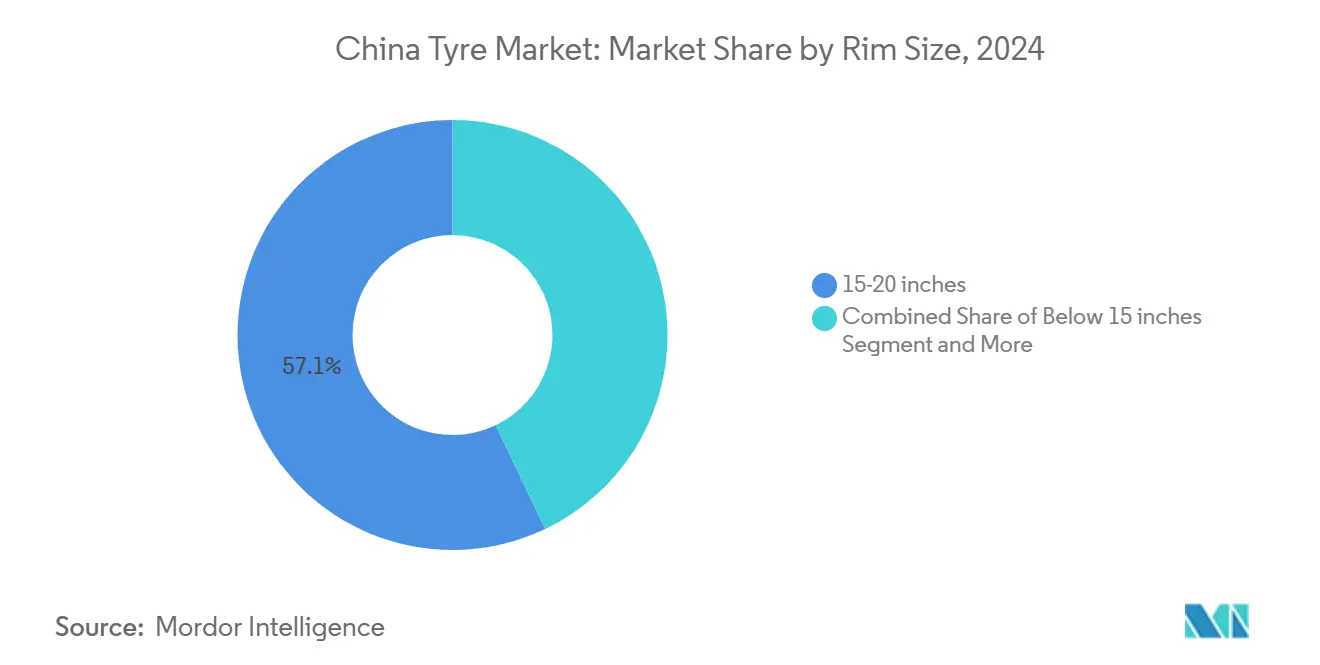

- By rim size, 15–20-inch tyres represented 57.11% of the China tyre market share in 2024; diameters above 20 in. are set to register an 8.66% CAGR by 2030.

- By propulsion, internal-combustion vehicles retained 83.12% of the Chinese tyre market share in 2024, while battery-electric vehicles led growth at a 9.13% CAGR through 2030.

China Tyre Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Fleet Increases Replacement Demand | +1.8% | National; Tier 1–3 cities | Medium term (2–4 years) |

| EV Incentives Drive Low-Resistance Tyres | +1.5% | National; early gains in Beijing, Shanghai, Shenzhen | Short term (≤ 2 years) |

| Infrastructure Boom Fuels OTR, Commercial | +1.2% | Western provinces; Belt and Road corridors | Long term (≥ 4 years) |

| Radial Shift Boosts Fuel Efficiency | +0.9% | National; commercial hubs | Medium term (2–4 years) |

| Digitalization Transforms Tyre Distribution | +0.7% | National; eastern coastal regions | Short term (≤ 2 years) |

| Tougher Rules Accelerate Premium Shift | +0.5% | National; uniform implementation | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Replacement Demand from Expanding Vehicle Parc

The installed base of passenger cars and commercial vehicles keeps rising in lower-tier cities, shifting purchasing patterns from first-time buyers to repeat purchasers seeking higher-quality replacements. Semi-steel capacity utilization stayed healthy in 2024 because passenger-car replacements required shorter lead times, whereas all-steel truck lines ran below optimal rates. Predictive-maintenance solutions that embed sensors in premium tyres allow fleet managers to monitor tread depth and pressure remotely, supporting longer service intervals but pulling demand toward higher-margin SKUs. As these technology-enabled products proliferate, the Chinese tyre market benefits from improved pricing power and brand loyalty. Growth in ride-hailing and car-sharing fleets compounds replacement cycles because intensive urban mileage accelerates wear. Replacement demand offers a stable, counter-cyclical revenue stream that helps mitigate OEM production swings.

Government Incentives for NEVs Spur Low-Rolling-Resistance Tyre Uptake

China’s dual-credit scheme and purchase subsidies catalyze EV sales, making tyre rolling resistance a battery-range determinant and a regulatory compliance metric. Domestic producers responded quickly: ZC Rubber launched its EV PRO line, while Sailun’s liquid-gold compound targets energy-efficiency gains in the 8-10% range [1]“Liquid-Gold Compound Press Release,” Sailun Group, en.sailungroup.com. Battery-electric vehicles create a parallel ecosystem for specialized silica compounds, lightweight carcass designs, and foam-based noise dampening. Provincial incentives in Shanghai, Beijing, and Shenzhen further accelerate urban adoption, prompting distributors to create EV-specific product zones that educate retailers on fitment nuances. In parallel, global OEMs localize EV tyre sourcing to qualify for domestic content credits, locking in long-term supply contracts that strengthen capacity utilization at technology-focused plants. These dynamics collectively lift the top line of the China tyre market while widening the performance gap between premium and commodity suppliers.

Infrastructure Boom Sustaining OTR and Commercial Tyre Volumes

The Belt-and-Road Initiative and domestic megaprojects keep construction equipment fleets active, generating robust demand for off-the-road (OTR) tyres with wide-base profiles and cut-resistant compounds[2]“Infrastructure Outlook 2025,” Asian Infrastructure Investment Bank, aiib.org. Engineering-tyre exports rose during the first ten months of 2024 as Chinese contractors shipped equipment to Central Asia and Africa. Triangle Tyre and Guizhou Tyre expanded mining-specific lines, and OEM supply agreements with leading excavator makers further anchor volumes. Larger rim diameters and higher ply ratings dominate procurement lists because heavier haul-truck loads require enhanced heat dissipation. As a result, the Chinese tyre market secures a dependable growth pillar that balances cyclical passenger-car swings.

Shift to Radial Technology in Trucks and Buses for Fuel Efficiency

Radial tyres continue to displace bias construction in heavy-duty fleets because their lower rolling resistance cuts fuel consumption and extends casing life. Operating data from express-freight carriers show that switching an all-steel truck fleet from bias to radial formats lowers diesel use, a saving large enough to offset the higher purchase price within the first year of service. Government mandates that link freight-operator tax rebates to documented fuel-efficiency gains add further momentum, making radial adoption an industry standard in commercial hubs along the eastern seaboard. Domestic manufacturers upgraded bead-wire quality and belt-tension uniformity, enabling radial casings to survive multiple retread cycles and thus boosting lifecycle economics for long-haul bus operators.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rubber Volatility Squeezing Margins | –1.4% | Eastern processing hubs | Short term (≤ 2 years) |

| Overcapacity Driving Domestic Price Wars | –1.1% | National manufacturing clusters | Medium term (2–4 years) |

| Anti-Dumping Duties Curb Exports | –0.8% | Export-oriented coastal regions | Long term (≥ 4 years) |

| Shortage of High-Grade Synthetic Rubber | –0.6% | National; premium segments | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Natural-Rubber Price Volatility Squeezing Margins

Raw material costs account for as much as 70% of a tyre’s ex-factory price, making the Chinese tyre industry highly sensitive to latex price swings. Larger manufacturers such as Linglong employ futures hedging and long-term contracts, but tier-two suppliers face squeezed gross margins, restricting capital expenditure. Synthetic rubber offered partial relief, yet premium SBR grades used in EV tyres remained tight, forcing allocation decisions that delayed some OE programs. If the volatility persists, near-term profitability across the Chinese tyre market could slip, slowing capex into advanced compounding lines.

Intense Domestic Over-Capacity Driving Price Wars

China’s boom-era capacity build-out created a structural oversupply, especially in all-steel truck-and-bus lines where utilization dipped during 2024’s weak freight cycle. Price wars ensued, eroding average selling prices in lower-tier markets and undermining brand equity. Larger players reacted by shuttering obsolete bias lines, shifting to high-margin EV SKUs, and opening overseas plants to diversify demand. Smaller factories lacking export certifications or technology depth struggled to keep operations afloat, accelerating consolidation. Overcapacity also discourages rapid adoption of sustainability upgrades because payback periods stretch when unit prices fall. Until capacity rationalization settles, the Chinese tyre market remains vulnerable to periodic margin dips.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Season: All-Season Gains Traction

All-season products, once a niche, now ride urbanization and convenience narratives. Summer tyres still held the bulk at 48.33% of the China tyre market in 2024, securing the largest slice of the China tyre market share. All-season uptake climbs with a 7.94% CAGR through 2030 as consumers seek a single set that performs year-round, eliminating semi-annual changeovers. Digital channels amplify the trend by promoting simplified SKU assortments that lower dealer inventory risk and quicken fulfillment cycles. In colder northeast provinces, winter tyres retain relevance, yet penetration inches forward only where mandatory fitment laws apply. As regulatory focus tilts toward rolling resistance, all-season compounds optimized for a wider temperature band align well with GB-9743 requirements, reinforcing their growth premium.

The convenience factor intersects with the proliferation of express-service chains offering value bundles of tyres, plus balancing, TPMS, and alignment in one stop. Manufacturers of all-season tyres must balance snow traction with wet handling, prompting investment in multi-functional tread designs. Consequently, the Chinese tyre market witnesses a technology race centered on adaptive siping and polymer blends that retain elasticity in both summer heat and winter chill. Embedded RFID tags that track mileage make warranty programs more transparent, further swaying buyers toward established brands.

By Tire Design: Radial Dominance Continues

Radial construction remained the undisputed norm in 2024, capturing 91.26% of the Chinese tyre market size and logging a 6.96% CAGR by 2030. The technology’s lower rolling resistance and superior heat management translate into fuel savings for passenger and freight fleets. Government carbon-reduction targets act as an additional lever, nudging biases and cross-plies toward niche applications such as specialty agriculture or severe-service mining. Airless prototypes from global brands receive media buzz yet await scaling because manufacturing economics and ride-comfort hurdles persist.

Domestic factories upgrade curing-press automation and high-precision molds to close quality gaps with premium imports. These steps reposition Chinese radials for higher-speed ratings and longer tread-wear warranties, supporting OEM acceptance. Moreover, fleets value radials’ retreadability—another cost lever as road freight margins trend thinner. Operating conditions favor radials even in mixed-surface provinces where trucks shuttle between highways and construction sites, indicating the design’s resilience across duty cycles within the China tyre market.

By Vehicle Type: Passenger Cars Lead, OTR Accelerates

Passenger-car tyres retained a 62.55% of the China tyre market share in 2024, buoyed by post-pandemic mobility recovery and greater car ownership in Tier 2 and 3 cities. Ride-hailing fleets also add mileage faster, shortening replacement intervals. The fastest expansion, however, emerges in off-the-road lines that post a 7.16% CAGR on infrastructure megaproject momentum. Heavy-duty mining dumpers and construction cranes generate high ASPs because their tyres contain specialty reinforcement layers and cut-resistant compounds.

Light commercial vehicles (LCVs) benefiting from e-commerce demand represent a middle ground, displaying steady unit growth and premiumization toward larger rim sizes and reinforced sidewalls. Two-wheeler electrification in urban zones spawns a micro-segment for high-torque scooter tyres, where torque loads necessitate upgraded bead and belt packages to prevent slippage. Collectively, these dynamics sustain a diversified demand mix that buffers the Chinese tyre market against shocks in a single vehicle category.

By Application: Off-Road Gains Momentum

On-road fitments dominated with 77.41% of the China tyre market share in 2024 because passenger cars and urban logistics still make up the majority of rolling stock. Off-road tyres, encompassing mining, construction, and agricultural equipment, expand at a 7.54% CAGR to 2030 as Belt-and-Road project pipelines mature. The segment’s revenue density is high, given that each 57-inch OTR tyre retails at a price equivalent to dozens of passenger-car units. That pricing power anchors factory profitability even when raw-material costs swell.

Smart OTR tyres with internal sensors track temperature, pressure, and load cycles in real time, enabling predictive maintenance that minimizes costly equipment downtime. High silica and cut-resistant tread compounds are standard because mine haul roads and construction debris pose severe abrasion threats. Such technical requirements create entry barriers that fortify margins for seasoned suppliers, amplifying the value captured in the China tyre market.

By End User: Aftermarket Dominance Persists

The aftermarket’s 69.24% of the China tyre market share in 2024 underscores the shift from OEM dependence to replacement-centric business models, and the segment’s 8.05% CAGR cements its role as the primary growth engine. Consumers purchase online and install at nationwide service centers that promise a 45-minute turnaround, tightening the logistics chain between factories and end users. The trend favors brands integrating with digital platforms and delivering small-lot shipments quickly.

Retreading gains renewed interest because sustainability metrics and cost considerations converge. Large logistics fleets contract retread service providers under mileage-based billing, reducing capex and waste. Yet EV fleets complicate retread adoption because specialized bead designs and ultra-low rolling resistance targets make carcass reuse harder. For suppliers, balancing retread programs with next-generation EV lines becomes a strategic juggling act in the Chinese tyre market.

By Rim Size: Larger Sizes Drive Growth

Mainstream 15- to 20-inch sizes held 57.11% of the China tyre market share in 2024, aligned with China’s robust C-segment sedan and compact SUV sales. Upsizing trends lift rim diameters above 20 inches, delivering the fastest 8.66% CAGR through 2030 as luxury SUVs and premium sports sedans proliferate. Larger wheel wells host wider tyre profiles, enhancing cornering stability but increasing unsprung mass, so compound engineers counter with lightweight aramid belts and optimized bead apex geometry.

The aspirational lifestyle push influences cosmetic choices; consumers pay premiums for staggered setups or performance-oriented tread aesthetics. Consequently, profit per tyre rises, supporting ROI for advanced curing presses capable of handling low-profile sizes. Commodity producers focusing on sub-15-inch SKUs face declining volumes, prompting tooling upgrades or strategic exits, thereby reshaping capacity allocation across the China tyre market.

By Propulsion: Electric Vehicles Accelerate

Internal-combustion vehicles still accounted for 83.12% of the Chinese tyre market share in 2024, but their share erodes as battery-electric volumes record a 9.13% CAGR to 2030. EVs demand low-rolling-resistance, high-load-index, and noise-damping features. Foam-insert technology and pattern-sequencing reduce cabin decibels, a crucial factor when drivetrain noise is absent. Sailun and ZC Rubber introduced dedicated EV programs with graphene-enhanced treads, touting 6% longer range in OEM certification tests.

Hybrid powertrains present unique torque profiles that accelerate irregular tread wear, so multi-compound treads that vary in hardness across shoulders and center belts gain traction. Fuel-cell prototypes, although nascent, require similar low-resistance characteristics, positioning suppliers to leverage shared R&D. As propulsion diversity widens, the Chinese tyre market increases its demand for portfolio agility and material science breakthroughs.

Geography Analysis

China’s eastern seaboard, particularly Shandong, Jiangsu, and Zhejiang, hosted a significant share of installed capacity in 2024, giving these provinces unmatched supplier ecosystems and efficient export port access [3]“Regional Vehicle Parc 2025,” China Association of Automobile Manufacturers, caam.org.cn. Shandong counts Linglong, Triangle, and Sailun among its incumbents, combining polymer feedstock pipelines, skilled labor pools, and mature logistics. Production specialization deepens as factories within industrial parks cluster around specific technologies such as semi-steel radials or large OTR moulds, leveraging shared utilities to trim unit costs.

Western provinces, including Xinjiang, Inner Mongolia, and Shanxi, register the highest demand growth because mining and energy projects consume heavy-duty tyres at a rapid clip. Provincial governments approve rail spurs and integrated warehouse hubs that shorten supply lines from eastern factories, but rising logistics costs still justify capacity migration. Triangle Tyre’s proposed OTR site in Inner Mongolia exemplifies a decentralization wave designed to place output nearer end users and temper freight overhead.

Southern economic zones, Guangdong, Guangxi, and Fujian, enjoy strong replacement momentum as vehicle ownership rates climb alongside household incomes. Their proximity to rubber-producing Southeast Asian nations offers freight savings on natural-rubber imports. EV penetration accelerates in Shenzhen and Guangzhou, where municipal policies prioritize zero-emission fleets, prompting retailers to stock EV-specific tyres prominently. Regional variance in vehicle mix, income profiles, and policy incentives collectively enriches opportunity diversity within th,e China tyre market.

Competitive Landscape

Domestic players controlled a significant volume of unit shipments in 2024, with Hangzhou Zhongce (ZC Rubber), Shandong Linglong, and Sailun Group anchoring the leaderboard. These producers exploit economies of scale, vertically integrate synthetic rubber supply, and move quickly on product localization for EV platforms. International majors Michelin, Bridgestone, and Continental defend premium niches through brand equity and advanced R&D, often partnering with domestic OEMs to secure mid-premium fitments.

Strategically, leading Chinese firms pursue overseas manufacturing as a hedge against anti-dumping tariffs. Product premiumization parallels geographic diversification; both initiatives aim to lift gross margins that price wars depress domestically. Digital transformation has become a third competitive pillar. ZC Rubber’s cloud-linked manufacturing lines deploy machine-vision inspection to cut defect rates, while Continental retrofitted its Hefei site with AI-based predictive maintenance that increases press uptime.

Circular-economy ventures also gain prominence: Guizhou Tyre piloted a pyrolysis facility converting end-of-life tyres into recovered carbon black, targeting OEM sustainability scorecards. Such initiatives reinforce corporate reputations and satisfy evolving customer KPIs, enhancing competitive positioning in the Chinese tyre market.

China Tyre Industry Leaders

Hangzhou Zhongce Rubber Co., Ltd.

Shandong Linglong Tyre Co., Ltd.

Sailun Group Co. Ltd.

Triangle Tyre Co., Ltd

Guizhou Tyre Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Sailun Group, via Sailun (Shenyang) Tire, agreed to acquire 100% equity of Bridgestone (Shenyang) Tire for RMB 265 million (USD 37 million).

- July 2024: Yokohama announced a new passenger-car tyre plant in Hangzhou, Zhejiang, starting with 9 million-unit capacity.

- June 2024: Continental completed phase-four expansion of its Hefei plant, targeting 18 million passenger and light-truck tires by 2027.

- April 2024: Double Coin rolled out its expanded Anhui factory, debuting 205/60 R16 92V tires tailored for new-energy vehicles.

China Tyre Market Report Scope

| Summer |

| Winter |

| All-Season |

| Radial |

| Bias |

| Non-pneumatic / Airless |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Trucks and Buses |

| Two-Wheelers |

| Off-the-Road and Specialty (OTR, Agriculture, Mining, Racing) |

| On-Road |

| Off-Road (Construction, Mining, Agriculture) |

| OEM |

| Aftermarket (Replacement and Retread) |

| Below 15 inches |

| 15 – 20 inches |

| Above 20 inches |

| Internal-Combustion Vehicles |

| Battery-Electric Vehicles |

| Hybrid and Fuel-Cell Vehicles |

| By Season | Summer |

| Winter | |

| All-Season | |

| By Tire Design | Radial |

| Bias | |

| Non-pneumatic / Airless | |

| By Vehicle Type | Passenger Cars |

| Light Commercial Vehicles | |

| Heavy Commercial Trucks and Buses | |

| Two-Wheelers | |

| Off-the-Road and Specialty (OTR, Agriculture, Mining, Racing) | |

| By Application | On-Road |

| Off-Road (Construction, Mining, Agriculture) | |

| By End User | OEM |

| Aftermarket (Replacement and Retread) | |

| By Rim Size | Below 15 inches |

| 15 – 20 inches | |

| Above 20 inches | |

| By Propulsion | Internal-Combustion Vehicles |

| Battery-Electric Vehicles | |

| Hybrid and Fuel-Cell Vehicles |

Key Questions Answered in the Report

How large is the China tyre market in 2025 and what is its forecast growth?

The China tyre market size is USD 54.65 billion in 2025 and is forecast to grow at a 6.63% CAGR to reach USD 75.33 billion by 2030.

Which vehicle segment drives the highest tyre demand in China?

Passenger-car fitments lead, holding 62.55% share in 2024, though off-the-road tyres show the fastest growth on infrastructure needs.

What is the dominant tyre design in China?

Radial construction dominates with 91.26% share and continues to expand because of fuel-efficiency and durability advantages.

Which rim sizes are gaining popularity in China?

Diameters above 20 inch exhibit the fastest growth, driven by premium SUV and luxury-sedan sales favoring larger wheels for performance and aesthetics.

Page last updated on: