Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.84 Billion |

| Market Size (2026) | USD 3.11 Billion |

| Market Size (2031) | USD 4.92 Billion |

| Growth Rate (2026 - 2031) | 9.61% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Paper Packaging Market Analysis by Mordor Intelligence

The Vietnam paper packaging market size was valued at USD 2.84 billion in 2025 and estimated to grow from USD 3.11 billion in 2026 to reach USD 4.92 billion by 2031, at a CAGR of 9.61% during the forecast period (2026-2031). This expansion significantly outpaces the global average, underscoring Vietnam’s strategic role in Southeast Asia’s evolving supply chain framework. Rising middle-class consumption, robust foreign direct investment, and regulatory incentives such as extended producer responsibility requirements are accelerating demand for paper-based formats. The surge in e-commerce parcel volumes, the relocation of fast-moving consumer goods and electronics production, and brand-owner carbon-cut commitments all converge to bolster the Vietnam paper packaging market.[1]SD Link, “The Growth Potential of Smart Logistics in Vietnam 2025,” sdlink.vn Meanwhile, virgin-fiber shortages and volatile recovered-paper import rules create supply-side friction that keeps prices and capacity expansion in sharp focus.

Key Report Takeaways

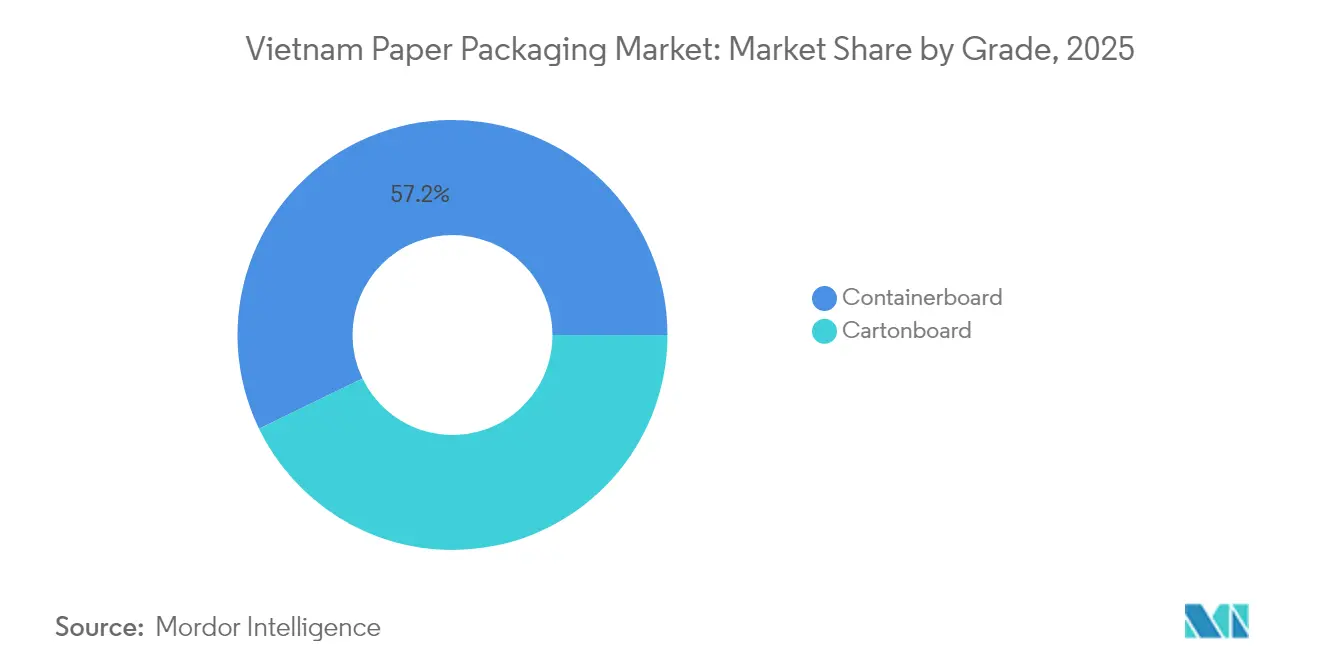

- By grade, containerboard captured 57.18% of the Vietnam paper packaging market share in 2025.

- By product, the Vietnam paper packaging market size for folding cartons is projected to grow at a 10.96% CAGR between 2026-2031.

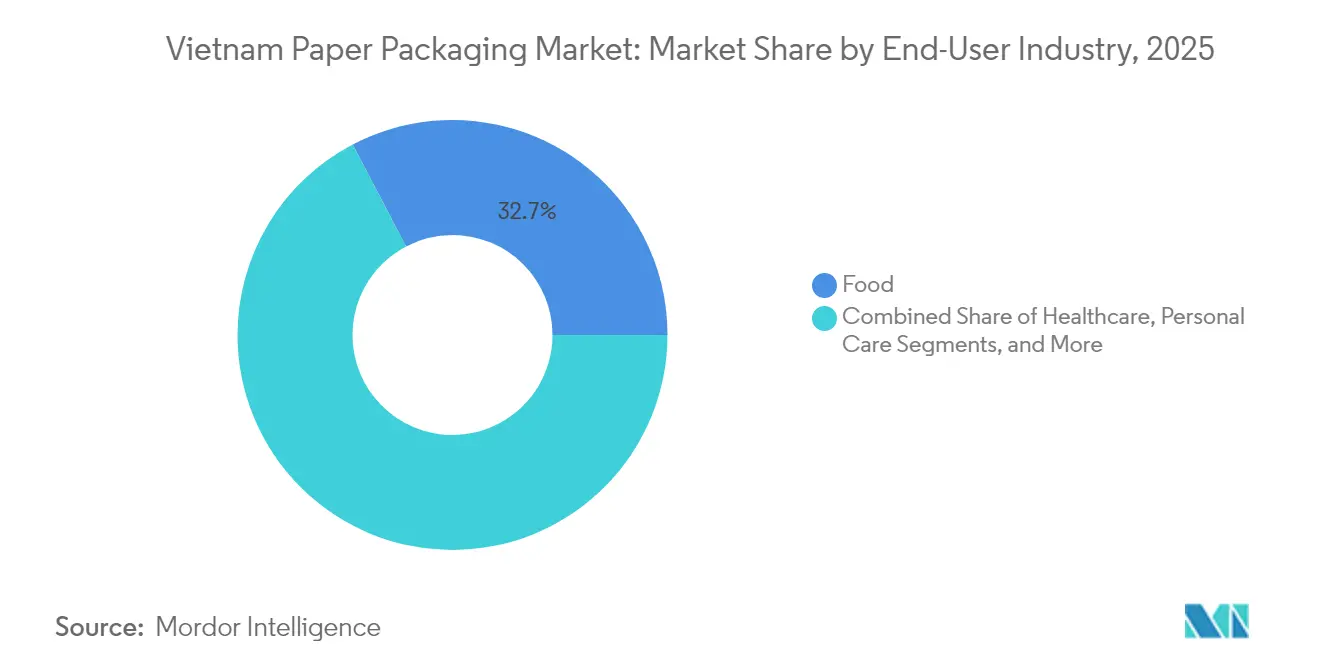

- By end-user industry, food applications captured 32.68% of the Vietnam paper packaging market share in 2025.

- By packaging format, the Vietnam paper packaging market size for molded fiber and pulp is projected to grow at a 11.78% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Paper Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Booming e-commerce parcel volumes | +2.1% | National, with concentration in Ho Chi Minh City, Hanoi, Da Nang | Short term (≤ 2 years) |

| Rapid FMCG and electronics off-shoring into Vietnam | +1.8% | Northern and Southern industrial zones, spillover to Central Vietnam | Medium term (2-4 years) |

| Plastic phase-out regulations (EPR and DRS) | +1.4% | National, early adoption in major cities | Medium term (2-4 years) |

| Foreign brand owners' Scope-3 carbon cuts push lightweight recycled board | +1.2% | Export-oriented hubs, multinational supplier networks | Long term (≥ 4 years) |

| Rise of social-commerce micro-fulfillment in tier-2 cities | +0.9% | Secondary urban centers, emerging e-commerce corridors | Medium term (2-4 years) |

| Tax-incentivized investments in high-speed digital printing lines | +0.7% | Industrial development zones, technology parks | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Booming e-commerce parcel volumes

National e-commerce turnover rose at a double-digit pace in 2024, driving aggregate parcel flows across Ho Chi Minh City, Hanoi, and Da Nang. The uptick amplifies demand for corrugated shipping containers engineered to survive multimodal logistics chains. Micro-fulfillment centers in tier-2 cities are shifting order profiles toward smaller-format boxes that fit parcel lockers and two-wheeler delivery racks. Vietnam’s Decision 221/QD-TTg targets a 9%–11% logistics GDP contribution, prompting automation upgrades that require standardized packaging dimensions for high-speed sortation. Capital spending of USD 5 billion earmarked for smart-logistics infrastructure through 2030 cements near-term volume visibility. The Vietnam paper packaging market gains immediate tailwinds from this parcel boom.

Rapid FMCG and electronics off-shoring into Vietnam

Over 66% of 2025’s fresh FDI pledges flowed into processing and manufacturing, catalyzing plant-level demand for transport-worthy cartons in Northern and Southern industrial belts. Snack-food producers, exemplified by the USD 90 million Ha Nam facility, anchor steady containerboard pull-through while prioritizing 100% sustainable sourcing goals. Electronics assemblers relocating from China specify anti-static liners, moisture barriers, and white-top kraftliners that meet global quality codes. Localization mandates by multinational corporations promote in-country board production to cut import reliance and Scope-3 emissions. As a result, the Vietnam paper packaging market secures long-run orders tied to foreign plant commissioning schedules.

Plastic phase-out regulations (EPR and DRS)

Decree 05/2025/ND-CP escalated carton-paper recycling quotas to 20% and lifted small-business exemptions, expanding producer compliance obligations nationwide. Twenty-four accredited recyclers now underpin a formal take-back network that feeds recovered fiber to domestic mills. The proposed Deposit-Return System could divert 77,000 tons of packaging waste annually, creating 6,400 formal jobs. Although compliance costs weigh on smaller converters, early adopters that integrate recycled content gain regulatory goodwill and preferred-supplier status with eco-conscious brand owners. Consequently, paper emerges as a functional substitute for banned plastic formats in the Vietnamese paper packaging market.

Foreign brand owners' Scope-3 carbon cuts push lightweight recycled board

Global companies impose emissions scorecards on suppliers, spurring demand for boards that use less fiber yet retain stacking strength. A EUR 217 million expansion lifts domestic output of advanced aseptic cartons to 30 billion units per year. Tetra Recart lines turn out 6,000 boxes per hour, achieving shelf-stable performance without preservatives. Lightweight recycled fluting and coated recycled board now qualify for high-graphics print, allowing exporters to hit carbon targets without sacrificing brand aesthetics. The Vietnam paper packaging market benefits as more multinationals specify these grades for regional sourcing.

Restraints Impact Analysis*

| Restraint | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Structural shortfall of domestic virgin fiber; import dependence | -1.6% | National, acute in Northern industrial zones | Long term (≥ 4 years) |

| Volatile recovered-paper import policy and quality controls | -1.1% | Port cities, recycling facility locations | Medium term (2-4 years) |

| US/EU trade actions on wood products tighten pulpwood feedstock | -0.8% | Export-oriented manufacturers, international supply chains | Medium term (2-4 years) |

| Industrial power-tariff hikes squeeze SME corrugators | -0.7% | SME manufacturing clusters, energy-intensive operations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Structural shortfall of domestic virgin fiber; import dependence

Vietnam’s mills cannot meet surging kraftliner demand because the country lacks large-scale, sustainable forestry plantations. In early 2023, total packaging-paper consumption hit 284,530 tons even as imports rose 9.2% month-on-month, underscoring the gap.[2]Vietnam Pulp and Paper Association, “Monthly Bulletin March 2023,” rippi.com.vn Currency swings and freight costs translate quickly into linerboard prices, affecting converter margins. Premium grades that rely on long fiber face periodic shortages, forcing users to down-spec or pay surcharges. The fiber deficit, therefore, acts as a structural drag on the Vietnam paper packaging market.

Volatile recovered-paper import policy and quality controls

Customs inspections targeting contaminant thresholds lengthen dwell times at seaports, complicating mill scheduling. Periodic quota freezes on certain recovered-paper categories trigger spot-price spikes that ripple through the supply chain. Converters lacking vertical integration pass costs to end users, eroding competitiveness against plastic substitutes. Until stable guidelines emerge, the Vietnam paper packaging market remains exposed to input-price volatility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Containerboard Dominance Amid Cartonboard Acceleration

Containerboard held 57.18% of the Vietnam paper packaging market share in 2025, a reflection of Vietnam’s export-oriented profile that relies on robust corrugating medium for global shipping. White-top kraftliner commands premium pricing in electronics clusters, whereas recycled fluting satisfies domestic food-and-beverage logistics. Semi-chemical fluting attracts buyers, balancing cost and strength. Cartonboard, although smaller, records an 11.13% CAGR to 2031, propelled by rising pharmaceutical labeling needs and retail-ready displays. Solid bleached sulfate and folding boxboard deliver high-graphics surfaces essential for brand differentiation among multinational FMCG firms. Coated recycled board and uncoated recycled board gain traction as eco-labels become purchasing criteria. Tetra Pak’s capacity boost dedicates 55% output to local buyers, signaling confidence in premium carton uptake.

The Vietnam paper packaging market size for containerboard is projected to rise steadily alongside warehouse construction in industrial parks. Meanwhile, the Vietnam paper packaging market size for cartonboard stands to benefit from regulatory pressure favoring lightweight formats with higher recycled content. Market positioning is thus shifting from commodity liner toward value-added board engineered for specific end uses and shorter print runs.

By Product: Corrugated Boxes and Containers Lead While Folding Cartons Accelerate

Corrugated Boxes and Containers accounted for 50.12% of the Vietnam paper packaging market size in 2025, as e-commerce and export shipping dominated volume patterns. Large shippers require B- and C-flute cases that strike a balance between crush resistance and stacking efficiency for sea freight. The rollout of USD 5 billion in smart-logistics infrastructure through 2030 ensures continued corrugated throughput. Folding cartons, however, are expanding at an 10.96% CAGR as healthcare and personal-care brands seek tamper-evident, shelf-ready solutions. Digital print subsidies accelerate carton customization, which supports premium pricing.

Down-gauge opportunities in corrugated remain limited until fiber supply stabilizes. In contrast, cartons utilize lightweight coated substrates to minimize material usage and align with Scope 3 emission targets. Molded pulp inserts integrated into folding-carton formats further differentiate offerings. The Vietnam paper packaging market is continuing to evolve from bulk shippers toward hybrid SKUs that combine structural protection with point-of-sale appeal.

By End-User Industry: Food Sector Stability Contrasts Healthcare Dynamism

Food applications accounted for 32.68% of the Vietnam paper packaging market share in 2025, driven by strong agricultural exports and rising domestic consumption of processed food. Shelf-stable beverage cartons benefit from the expansion of aseptic technology, which extends product reach into rural areas without cold-chain constraints. In contrast, healthcare packaging is expected to grow at a 10.05% CAGR as Vietnam localizes pharmaceutical production under industrial policy incentives. Tamper-evident folding cartons with braille embossing and moisture-barrier liners become standard.

Electronics account for a rising slice of demand after semiconductor investment surges, necessitating anti-static corrugated partitions. The personal-care and household-care segments follow urbanization trends, adopting high-graphics cartons that convey a premium positioning. The Vietnam paper packaging market thus pivots toward specialized end uses where compliance standards and branding drive incremental tonnage and higher margins.

By Packaging Format: Rigid Dominance Amid Molded Fiber Innovation

Rigid formats, including corrugated and solid board, commanded a 50.55% share of the Vietnam paper packaging market in 2025, reflecting Vietnam’s export container flows. Semi-rigid folding cartons anchor retail shelves, while flexible paper laminates serve niche food-service wrappers. Molded fiber, although accounting for less than 10% of the volume, is projected to post a 11.78% CAGR, driven by plastic-reduction mandates and the growing demand for electronics cushioning. Lightweight, form-fit pulp trays substitute for EPS foams, providing curb-side recyclability.

EPR quotas that require 20% recycled content favor molded-fiber solutions designed from post-consumer waste streams. Flexible formats are gaining momentum in single-serve beverage pouches lined with aqueous dispersions, which enable monomaterial recycling. The Vietnam paper packaging market, therefore, exhibits a format transition that rewards converters who invest in specialized tooling and barrier-coating expertise.

Geography Analysis

Northern industrial parks surrounding Hanoi draw electronics and automotive suppliers that require high-strength corrugated and specialty anti-static liners. Proximity to the China border ensures rapid component inflows, making the region the primary consumption hub for premium kraft grades. Southern economic zones anchored by Ho Chi Minh City handle high-volume FMCG export traffic, driving steady containerboard demand and supporting vertically integrated mills. Coastal ports such as Cai Mep reduce shipping lead times, further cementing the south’s share in the Vietnam paper packaging market size.

Central Vietnam, led by Da Nang, emerges as a growth corridor as infrastructure programs connect north and south logistics arteries. Government incentives lure foreign investors seeking diversification, creating green-field opportunities for mid-scale corrugators to supply new manufacturing clusters. Tier-2 cities in the Mekong Delta and Red River Delta adopt micro-fulfillment nodes for social commerce, boosting demand for right-sized cartons and digitally printed sleeves.

Border provinces benefit from ASEAN trade-corridor integration, necessitating multilingual labeling and compliance with varied regional standards. Here, folding-carton converters gain advantage by offering regulatory advisory and quick-turn artwork services. Overall, regional specialization enables the Vietnam paper packaging market to match localized needs, ensuring balanced national growth.

Competitive Landscape

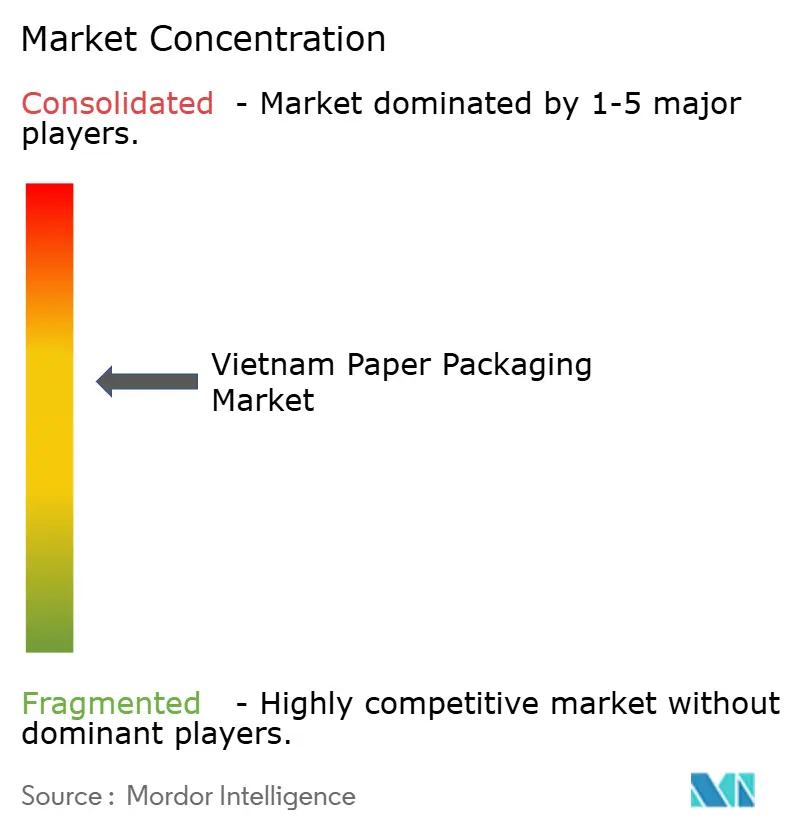

The market features moderate concentration. SCG Packaging leverages regional scale and recently reported VND 7.77 trillion (USD 301 million) in Vietnamese revenue with EBITDA expansion supported by eco-efficient board grades.[3]Vietnam Investment Review, “SCG Achieves Strong EBITDA and Profit Growth,” vir.com.vnTetra Pak’s capacity additions strengthen the premium aseptic-carton niche and introduce high-throughput Recart® lines targeting shelf-ready food exports. Domestic mid-tier players focus on cost-competitive corrugated supply, while new entrants invest in digital presses to capture short-run carton work boosted by tax incentives.

Competitive intensity rises as foreign mills study joint ventures to secure fiber and tap Vietnam’s ASEAN-wide trade access. Sustainability remains the key differentiation lever: converters tout recycled-content certifications and carbon-footprint dashboards to appeal to international buyers. Companies that integrate upstream pulping or downstream logistics stand to widen margins. Nonetheless, SMEs retain a foothold by serving regional customers with flexible lead times.

Integration moves continue. SCG’s acquisition of Starprint augments downstream folding-carton capacity and flexible-packaging know-how, enabling cross-selling into electronics and healthcare accounts. Meanwhile, molded-fiber startups deploy proprietary tooling to penetrate premium electronics cushioning. These dynamics illustrate an evolving Vietnam paper packaging market where technology adoption and sustainability positioning shape competitive outcomes.

Vietnam Paper Packaging Industry Leaders

Starprint Vietnam Joint Stock Company

Tetra Pak International S.A.

SCG Paper Public Company Limited

Lee & Man Paper Manufacturing Ltd.

Oji Interpack Vietnam Co., Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Tetra Pak inaugurated a EUR 97 million second-phase expansion of its Ho Chi Minh City aseptic-carton plant, raising capacity above 30 billion packs per year and introducing AI-enabled quality control.

- July 2025: Tetra Pak and Doveco commissioned a Tetra Recart line capable of 6,000 boxes per hour for preservative-free food.

- June 2025: SCG posted VND 834 billion (USD 32 million) profit in Q1 2025 as Vietnam operations generated VND 7.77 trillion (USD 301 million) sales.

- May 2025: Processed-goods exports reached USD 153 billion in the first five months, lifting packaging demand across manufacturing hubs.

Vietnam Paper Packaging Market Report Scope

Paper is frequently used to package products in several end-user industries. There are numerous grades of paperboard packaging. Paperboard, like folding cartons, is the most commonly used material in the manufacturing of containers. In the manufacturing process, the paperboard requires pulping, bleaching (optional), refining, sheet forming, drying, calendaring, and winding. Paper packaging materials can be efficiently reused and recycled compared to other materials, such as metals and plastics. This is why paper packaging is considered an eco-friendly and economical form of packaging. The Vietnamese paper packaging market tracks the revenue generated from various paper packaging types used across end-user industries in the country. The study provides qualitative coverage of the most widely adopted strategies and an analysis of key base indicators in emerging markets.

The Vietnamese paper packaging market is segmented by type (carton board and containerboard), product type (folding cartons, corrugated boxes and containers, and other product types), and end-user industry (food, beverage, healthcare, personal care, household care, electrical and electronics, and other end-user industries). The report provides market forecasts and sizes in value (USD) for all the aforementioned segments

By Grade

| Cartonboard | Solid Bleached Sulphate (SBS) |

| Solid Unbleached Sulphate (SUS) | |

| Folding Boxboard (FBB) | |

| Coated Recycled Board (CRB) | |

| Uncoated Recycled Board (URB) | |

| Other Cartonboard Grades | |

| Containerboard | White-top Kraftliner |

| Other Kraftliners | |

| White-top Testliner | |

| Other Testliners | |

| Semi-chemical Fluting | |

| Recycled Fluting | |

| Other Grades |

By Product

| Folding Cartons |

| Corrugated Boxes and Containers |

| Other Products |

By End-User Industry

| Food |

| Beverage |

| Healthcare |

| Personal Care |

| Household Care |

| Electrical and Electronics |

| Other End-User Industries |

By Packaging Format

| Rigid (Corrugated, Solid Board) |

| Semi-rigid (Folding Cartons excluding Solid Board Boxes) |

| Flexible Paper (Sachets, Wraps) |

| Molded Fiber and Pulp Packaging Products |

| By Grade | Cartonboard | Solid Bleached Sulphate (SBS) |

| Solid Unbleached Sulphate (SUS) | ||

| Folding Boxboard (FBB) | ||

| Coated Recycled Board (CRB) | ||

| Uncoated Recycled Board (URB) | ||

| Other Cartonboard Grades | ||

| Containerboard | White-top Kraftliner | |

| Other Kraftliners | ||

| White-top Testliner | ||

| Other Testliners | ||

| Semi-chemical Fluting | ||

| Recycled Fluting | ||

| Other Grades | ||

| By Product | Folding Cartons | |

| Corrugated Boxes and Containers | ||

| Other Products | ||

| By End-User Industry | Food | |

| Beverage | ||

| Healthcare | ||

| Personal Care | ||

| Household Care | ||

| Electrical and Electronics | ||

| Other End-User Industries | ||

| By Packaging Format | Rigid (Corrugated, Solid Board) | |

| Semi-rigid (Folding Cartons excluding Solid Board Boxes) | ||

| Flexible Paper (Sachets, Wraps) | ||

| Molded Fiber and Pulp Packaging Products | ||

Key Questions Answered in the Report

What is the current value of the Vietnam paper packaging market size in 2026?

It stands at USD 3.11 billion.

How fast is the sector projected to grow between 2026 and 2031?

It is forecast to expand at a 9.61% CAGR, reaching USD 4.92 billion by 2031.

Which product category contributes the highest revenue?

Corrugated Boxes and Containers lead with 50.12% share of Vietnam paper packaging market size in 2025.

What is the primary catalyst behind rising corrugated-box demand?

Rapid growth in e-commerce parcel volumes across Ho Chi Minh City, Hanoi, and Da Nang is boosting consumption of sturdy shipping cartons.

How are Extended Producer Responsibility rules shaping material choices?

EPR mandates a 20% recycling rate for carton paper, encouraging brands to switch from plastic to lightweight recycled board and molded-fiber solutions.

Page last updated on: