Animal Wound Care Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.55 Billion |

| Market Size (2031) | USD 2.25 Billion |

| Growth Rate (2026 - 2031) | 7.74% CAGR |

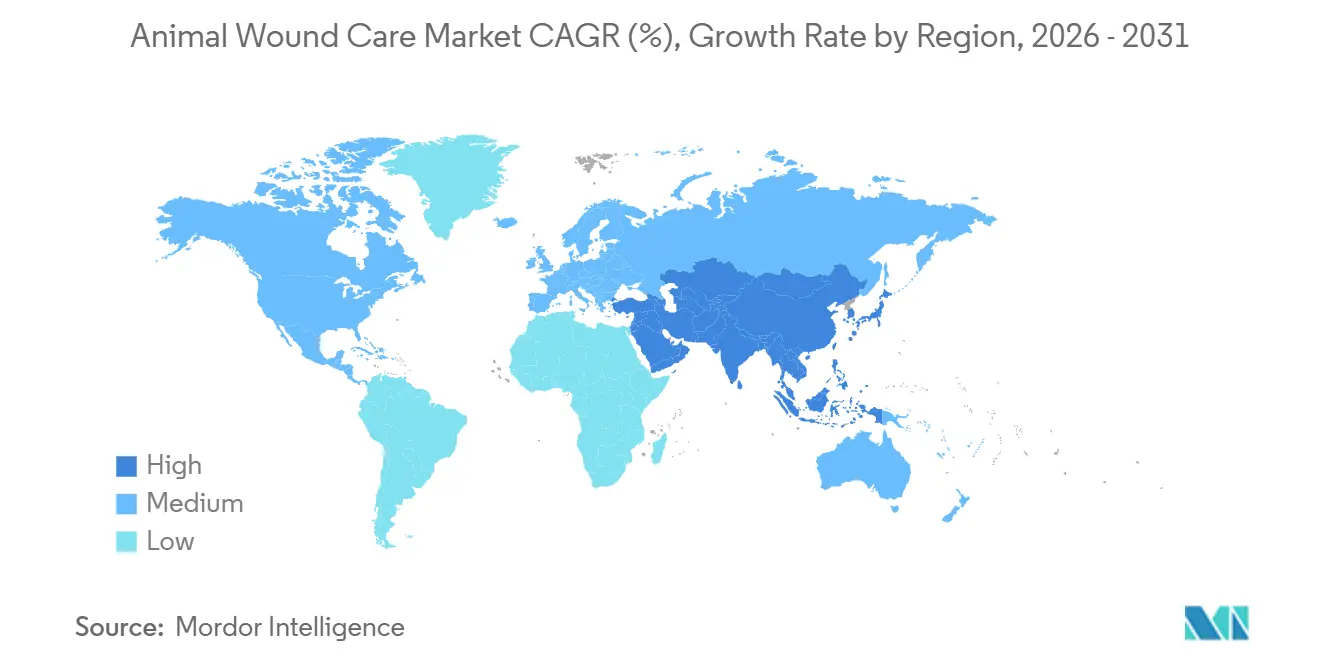

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

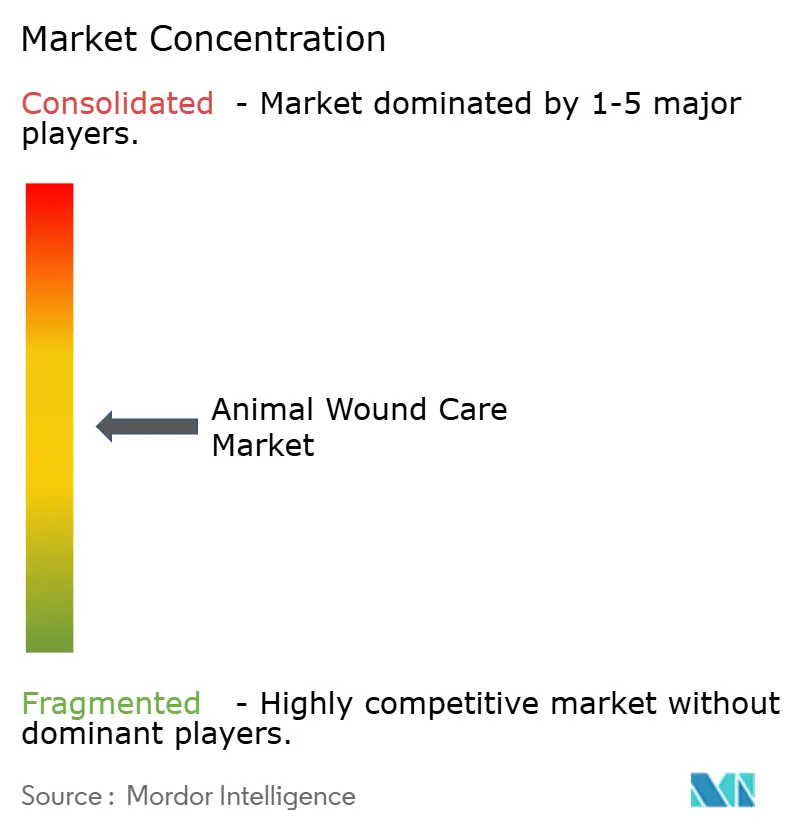

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Animal Wound Care Market Analysis by Mordor Intelligence

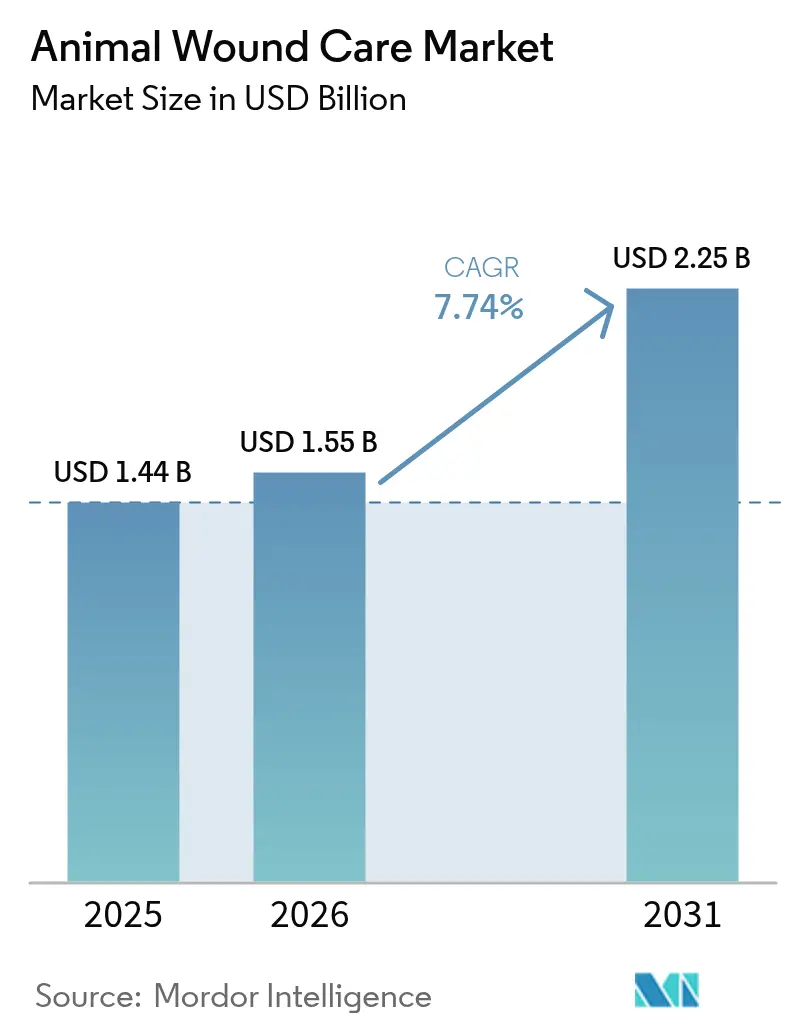

The Animal Wound Care Market size is expected to grow from USD 1.44 billion in 2025 to USD 1.55 billion in 2026 and is forecast to reach USD 2.25 billion by 2031 at 7.74% CAGR over 2026-2031.

Rising pet ownership, larger commercial-livestock populations, and the migration of human-grade dressings into veterinary practice underpin this steady expansion. A wider embrace of antimicrobial stewardship has heightened demand for topical therapies that limit systemic antibiotic use, while tele-veterinary platforms are broadening product access beyond brick-and-mortar hospitals. At the same time, regulatory agencies are tightening welfare and efficacy standards, prompting clinics to stock evidence-backed dressings despite cost pressures. Competitive dynamics are evolving as regenerative startups challenge incumbent pharmaceutical companies with keratin hydrogels, platelet-rich plasma kits, and miniaturized negative-pressure devices.

Key Report Takeaways

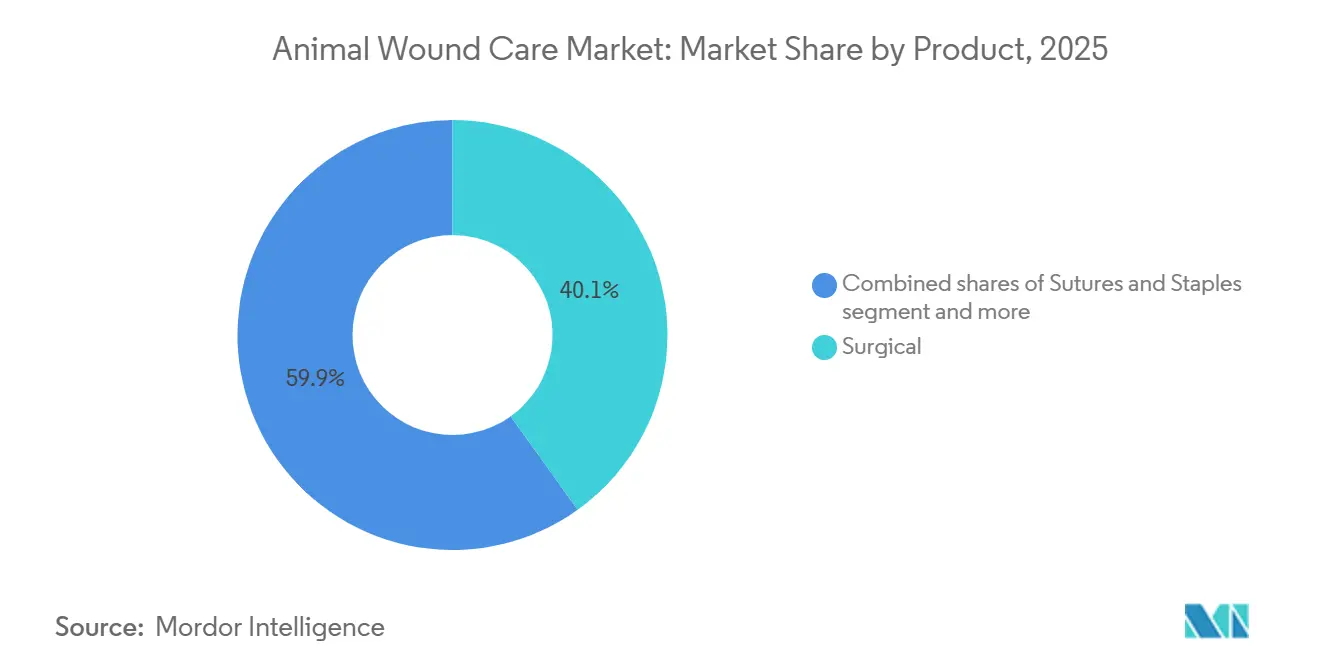

- By product category, surgical items led with 40.1% revenue share in 2025; advanced dressings are projected to expand at an 8.32% CAGR through 2031.

- By animal type, companion animals generated 64.12% of revenue in 2025, while livestock animals are poised to grow at a 7.75% CAGR over 2026-2031.

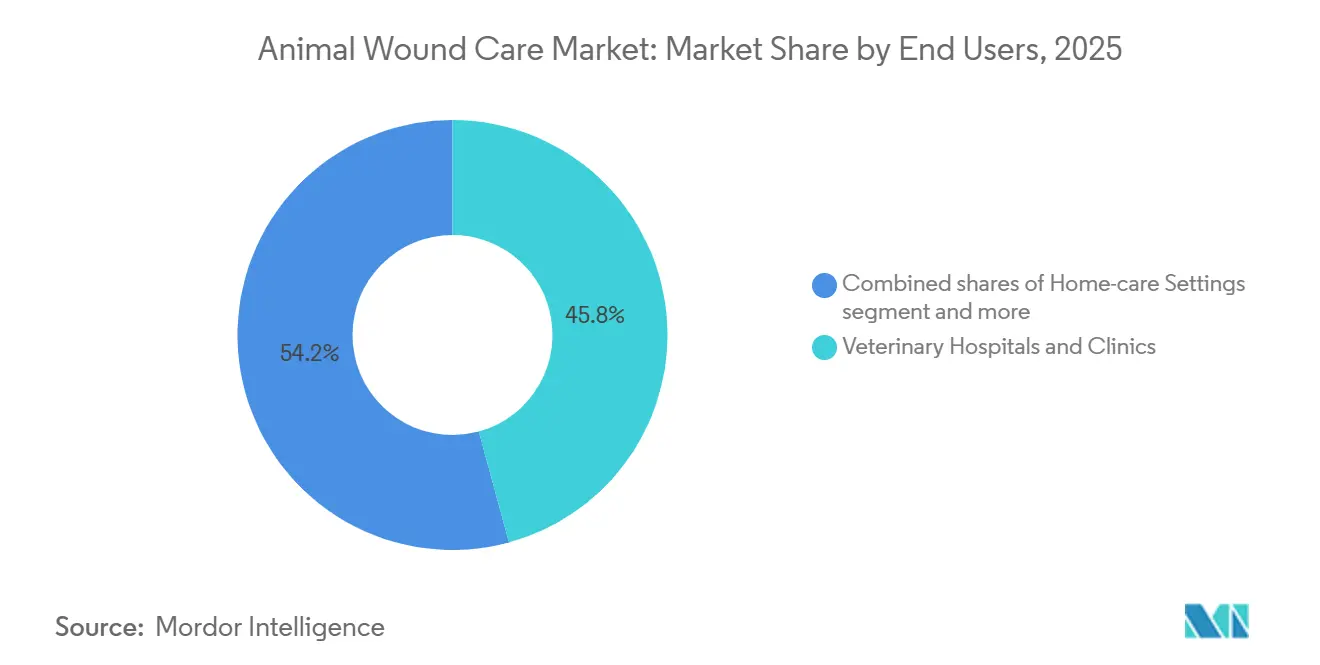

- By end user, veterinary hospitals and clinics commanded 45.76% share in 2025; home-care settings are advancing at an 8.12% CAGR to 2031.

- By geography, North America held 39.76% share in 2025, yet Asia-Pacific is forecast to post a 7.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Animal Wound Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government & Welfare Initiatives | +1.2% | Global, stronger in EU, North America, Australia | Medium term (2-4 years) |

| Pet Adoption & Healthcare Spending | +1.8% | North America, Europe, urban China, Japan, India | Short term (≤ 2 years) |

| Advanced Wound-Dressing Adoption | +1.5% | North America, EU core, spill-over to APAC and Latin America | Medium term (2-4 years) |

| Intensive Livestock-Farming Injuries | +0.9% | Global, concentrated in Brazil, US, China, EU poultry and swine belts | Long term (≥ 4 years) |

| Tele-Veterinary Wound Management | +1.0% | North America, Australia, urban APAC | Short term (≤ 2 years) |

| Regenerative Therapies Adoption | +1.4% | North America, Western Europe, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government & Welfare Initiatives

National welfare reforms are translating into mandatory protocols that elevate demand for evidence-based dressings. The 2024 USDA Animal Welfare Act amendments require analgesic hydrogel use during research procedures, pushing institutes to upgrade inventory [1]“Animal and Plant Health Inspection Service,” USDA, aphis.usda.gov. The European Union now restricts off-label use of human products on food-producing animals, channeling purchases toward veterinary-specific lines that meet residue standards. Australia’s 2025 farm-animal welfare plan ties export eligibility to documented wound treatment records, nudging producers toward antimicrobial-impregnated foam. These measures create a compliance-driven floor for the animal wound care market while penalizing suppliers that lack comparative-efficacy dossiers. Over the medium term, enforcement intensity in developed regions will ripple into export-oriented emerging markets, widening the addressable user base for premium therapies.

Pet Adoption & Healthcare Spending

Companion-animal ownership that surged during the pandemic remains elevated, and owners are spending more per visit on wound management. U.S. households averaged USD 1,201 in annual veterinary outlays per dog in 2025, compared with USD 1,060 in 2022, with post-surgical care a key line item [2]“American Veterinary Medical Association,” AVMA, avma.org. Single-person households in Japan are adopting cats at twice the rate of multi-person homes and choose collagen or antimicrobial foams for even minor lacerations. In India, pet-insurance penetration doubled to 1.6% in 2025, reducing out-of-pocket resistance to advanced therapies. Higher discretionary spending offsets volume saturation in mature markets and fuels the adoption of premium dressings in emerging urban centers.

Advanced Wound-Dressing Adoption

Clinics are transitioning from dry gauze to moisture-retentive and antimicrobial platforms as data accumulate on faster closure times. A 2024 Journal of Veterinary Surgery study showed foam dressings shortened canine incision healing by 3.2 days relative to gauze. Equine practitioners are adopting hydrocolloid dressings for limb wounds that require conformability and extended wear. Sales of honey-impregnated Activon Tulle rose 41% year over year in 2025, underscoring clinician confidence in non-antibiotic antimicrobials.

Draft FDA guidance issued in 2025 clarifies that antimicrobial dressings intended to prevent surgical infections fall under veterinary-device premarket notification, raising entry barriers yet signaling quality to cautious buyers.

Regenerative Therapies Adoption

Platelet-rich plasma, stem-cell sheets, and keratin hydrogels are moving from experimental protocols to commercial shelves. KeraVet Bio’s keratin hydrogel achieved a 68% complete-closure rate in diabetic dog wounds within 28 days, nearly doubling standard care outcomes. Vetlen Biosciences launched a centrifuge that prepares autologous plasma in 15 minutes, cutting turnaround time and lowering per-treatment cost to roughly USD 80. Zoetis partnered with a Japanese firm in 2026 to co-develop allogeneic stem-cell sheets for equine tendon injuries, targeting a 2027 rollout. These therapies carry premium price tags but resonate with owners of performance animals and geriatric pets for whom quality-of-life gains justify expenditure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of Comparative Studies | −0.8% | Global, more pronounced in emerging markets | Medium term (2-4 years) |

| High Veterinary-Care Costs | −1.1% | North America, Western Europe, Australia | Short term (≤ 2 years) |

| Regulatory Complexity (EU) | −0.6% | European Union | Medium term (2-4 years) |

| Limited Awareness (Developing Markets) | −0.5% | Sub-Saharan Africa, rural South Asia, parts of Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Veterinary-Care Costs

Consultation fees climbed 18% between 2022 and 2025 in the United States, reaching USD 61 per routine visit and over USD 400 for emergency debridement [3]“Australian Veterinary Association,” AVA, ava.com.au. Australia, 34% of pet owners deferred recommended wound care in 2025 because of affordability concerns, with rates rising to 48% in low-income households. Budget pressure steers owners toward over-the-counter gauze that lacks antimicrobial or moisture-retention features, limiting penetration of premium products. Livestock producers weigh dressing costs against slim profit margins, often opting for minimal intervention unless compliance or export mandates intervene. In regions where pet insurance remains scarce, cost sensitivity threatens uptake of collagen dressings and negative-pressure devices despite their clinical advantages.

Regulatory Complexity (EU)

The 2025 Veterinary Medicinal Products Regulation subjects certain antimicrobial dressings to full market authorization, including comparative-efficacy studies that can cost more than EUR 500,000. Animalcare Group delayed its silver-alginate launch by 14 months to meet requests for biofilm-reduction data, illustrating the barriers facing mid-sized firms. New labeling rules require withdrawal-period information even for topical use in food-producing animals, adding further compliance costs. The burden is consolidating the advanced-dressing segment around multinational companies with in-house regulatory teams, slowing innovation cycles in Europe, and driving clinicians to rely on a narrower range of products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Surgical Dominance Meets Advanced Innovation

Surgical items accounted for 40.1% of revenue in 2025, reflecting high volumes of spay-neuter procedures and fracture repairs conducted across clinics worldwide. Cyanoacrylate adhesives are popular for avian and exotic cases because delicate skin tears under traditional sutures; Jorgensen Laboratories recorded a 29% sales uplift for Vetbond in 2025. Advanced dressings are projected to outpace the broader animal wound care market at 8.32% CAGR through 2031, buoyed by clinical evidence of shorter healing times and fewer dressing changes. Antimicrobial foams, hydrocolloids, and silver alginates also align with antibiotic-stewardship goals, positioning them as frontline choices against biofilm. Traditional cotton gauze continues to serve budget-constrained settings but is yielding share as veterinary curricula emphasize moisture management and infection control.

Advanced dressings’ momentum underscores a shift in purchasing criteria from unit cost toward total cost of care. Clinics report fewer clinic visits and reduced anesthesia demand when moisture-retentive dressings are employed. Collagen dressings derived from bovine or porcine tissue are finding niches in equine limb wounds where granulation tissue forms slowly. The animal wound care market size for advanced dressings is expected to grow briskly as draft FDA guidance tightens antimicrobial classification, narrowing competitive sets and improving clinician confidence. Smaller manufacturers lacking regulatory resources may exit, further consolidating sales toward global suppliers with validated portfolios.

By Animal Type: Companion Loyalty Versus Livestock Scale

Companion animals generated 64.12% of revenue in 2025 as owners invested heavily in premium care for dogs and cats. Canine wounds often stem from outdoor activity and postoperative incision care, while feline injuries benefit from minimally invasive dressings due to grooming behavior. Exotic-pet veterinarians are adopting specialized chitosan hemostatic pads launched in 2025 to manage bleeding in small mammals and birds.

Livestock animals, despite lower per-case spending, are forecast to grow faster at 7.75% CAGR, driven by intensive poultry, swine, and cattle operations. Cattle producers use antimicrobial foams to prevent systemic antibiotic residues, and swine integrators reported 22% reductions in systemic antibiotic use after adopting silver-impregnated tail-wound dressings.

The animal wound care market share of livestock products is set to expand as export-oriented producers in Brazil and China respond to welfare audits from premium retail chains. Foam dressings are in pilot trials for keel-bone fractures in cage-free hens, demonstrating the growing application breadth. Companion-animal growth will remain steady but slightly slower than livestock, given the higher baseline adoption of advanced therapies. Nevertheless, regenerative options such as platelet-rich plasma and stem-cell sheets are almost exclusively companion animal-focused, adding high-value layers atop a wide installed base of surgical and advanced dressings.

By End User: Clinic Volumes Meet Home-Care Convenience

Veterinary hospitals and clinics captured 45.76% of revenue in 2025, reflecting their role in complex surgeries and trauma. These facilities adopt new technologies early, including keratin hydrogels and negative-pressure devices. The animal wound care market size generated by clinics will expand steadily, yet growth momentum is shifting toward home-care settings, which are advancing at 8.12% CAGR. Tele-veterinary platforms allow owners to send wound images for remote consultations, and clinicians ship dressings directly to households, cutting visit frequency. Wound-related tele-consultations accounted for 18% of Vetster’s traffic in 2025, highlighting digital channels’ contribution to sales.

Research institutes remain smaller revenue contributors but drive protocol adoption by publishing comparative studies, such as UC Davis findings on hydrocolloids reducing surgical-site infections by 37%. Animal shelters and NGOs handle high wound volumes and rely on donated antimicrobial hydrogels from manufacturers like Innovacyn, creating visibility for products among newly adopted pets. The animal wound care market is therefore broadening beyond traditional channels, with end-user diversity supporting resilient demand even when clinic volumes fluctuate.

Geography Analysis

North America retained a 39.76% share in 2025, supported by high pet ownership, robust insurance coverage, and rapid regulatory approvals. The FDA cleared 14 new wound-care devices between 2024 and 2025, enabling early adopter clinics to refresh formularies quickly. Canada benefits from regulatory alignment with the United States, although provincial variations introduce minor fragmentation. Mexico is emerging as a growth pole; a new Virbac distribution hub established in 2025 improves access across Central America and the southern United States.

Asia-Pacific is the fastest-growing region and is projected to post a 7.11% CAGR through 2031. Japan’s per-household veterinary spend reached JPY 89,000 (USD 610) in 2025, with wound-care products comprising 9% of the total. China’s dog and cat population surpassed 120 million in 2025, and Elanco’s Shanghai training center is equipping clinicians with advanced dressing protocols. India shows double-digit growth in pet populations, and veterinary colleges have begun teaching modern wound-management modules. Australia and New Zealand feature mature, high-spend markets where insurers already reimburse advanced therapies, making them useful test beds for product launches.

Europe’s stricter regulatory framework dampens short-term growth. Germany, the United Kingdom, and France remain sizable markets, but EMA compliance costs delay new product introductions. Spain and Italy are benefiting from rising ownership among younger demographics, while Poland and Hungary attract manufacturing investment. South America is anchored by Brazil, where livestock producers adopt antimicrobial foams to satisfy welfare-driven export requirements; Argentina’s market rebounded in 2025 as currency stabilization improved import capacity. The Middle East and Africa remain underpenetrated, with meaningful demand concentrated in Gulf Cooperation Council countries and South Africa.

Competitive Landscape

The top five companies, Zoetis, Elanco, Boehringer Ingelheim, Dechra Pharmaceuticals, and Virbac, held the majority of 2025 revenue, underscoring moderate concentration. Their integrated portfolios enable bundled supply contracts covering vaccines, diagnostics, and wound dressings, creating switching costs for veterinary chains. Nonetheless, niche innovators are capturing share with differentiated technologies. KeraVet Bio’s keratin hydrogel was adopted by 112 U.S. clinics within six months of its 2025 FDA approval, despite premium pricing.

Technology integration is a strategic differentiator. Elanco launched a computer-vision wound-assessment app in January 2026 that recommends dressing protocols, positioning the company to embed its products within digital workflows. Negative-pressure devices adapted by Solventum for veterinary use are gaining traction, and Dechra’s honey-impregnated Activon Tulle illustrates how natural antimicrobials can counter resistance concerns.

White-space opportunities revolve around cost-optimized advanced dressings for emerging markets, sub-USD 1,000 negative-pressure units for general practice, and antimicrobials targeting biofilm without fostering resistance. Sentrx and Innovacyn exemplify disruptors leveraging chitosan and hypochlorous gel technology. M&A is intensifying: Zoetis’ minority stake in a Japanese regenerative firm and Dechra’s reported interest in small-animal NPWT companies signal consolidation as incumbents seek growth beyond core segments.

Animal Wound Care Industry Leaders

Zoetis

Elanco Animal Health Incorporated

Boehringer Ingelheim

Dechra Pharmaceuticals

Virbac Animal Health India Pvt. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The Sree Chitra Tirunal Institute for Medical Sciences and Technology introduced CholeDerm, a novel wound-care dressing made from the gall bladders of farm animals and engineered to speed up healing

- August 2025: After logging a record USD 5.6 million revenue quarter in late 2025, Sonoma Pharmaceuticals disclosed plans to roll out its MicrocynAH animal-health range across major U.S. retail chains, including Menards and Walmart, throughout 2026.

Global Animal Wound Care Market Report Scope

As per the scope of the report, animal wound care encompasses a diverse range of products designed to manage injuries in both pets and livestock, ranging from basic antiseptic sprays to advanced bioactive dressings.

The animal wound care market is segmented by product, animal, end-user, and geography. By product, it is segmented into surgical (dressings, sutures & staples, tissue adhesives, and others), advanced (foam dressings, hydrocolloid dressings, hydrogel dressings, alginate dressings, collagen dressings, antimicrobial dressings), traditional (gauze, adhesive bandages, and cotton swabs & wraps), and other products (cell & gene therapies, platelet concentrates, and NPWT devices). By animal type, the market is segmented into companion animals (dogs, cats, and other companion animals) and livestock animals (cattle, swine, poultry, and sheep & goats). By End users, the market is segmented into veterinary hospitals & clinics, home-care settings, research & academic institutes, and animal shelters & NGOs. Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Surgical | Dressings |

| Sutures & Staples | |

| Tissue Adhesives | |

| Others | |

| Advanced | Foam Dressings |

| Hydrocolloid Dressings | |

| Hydrogel Dressings | |

| Alginate Dressings | |

| Collagen Dressings | |

| Antimicrobial Dressings | |

| Traditional | Gauze |

| Adhesive Bandages | |

| Cotton Swabs & Wraps | |

| Other Products | Cell & Gene Therapies |

| Platelet Concentrates | |

| NPWT Devices |

| Companion Animals | Dogs |

| Cats | |

| Other Companion | |

| Livestock Animals | Cattle |

| Swine | |

| Poultry | |

| Sheep & Goats |

| Veterinary Hospitals & Clinics |

| Home-care Settings |

| Research & Academic Institutes |

| Animal Shelters & NGOs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Surgical | Dressings |

| Sutures & Staples | ||

| Tissue Adhesives | ||

| Others | ||

| Advanced | Foam Dressings | |

| Hydrocolloid Dressings | ||

| Hydrogel Dressings | ||

| Alginate Dressings | ||

| Collagen Dressings | ||

| Antimicrobial Dressings | ||

| Traditional | Gauze | |

| Adhesive Bandages | ||

| Cotton Swabs & Wraps | ||

| Other Products | Cell & Gene Therapies | |

| Platelet Concentrates | ||

| NPWT Devices | ||

| By Animal Type | Companion Animals | Dogs |

| Cats | ||

| Other Companion | ||

| Livestock Animals | Cattle | |

| Swine | ||

| Poultry | ||

| Sheep & Goats | ||

| By End User | Veterinary Hospitals & Clinics | |

| Home-care Settings | ||

| Research & Academic Institutes | ||

| Animal Shelters & NGOs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the animal wound care market?

The market is expected to reach USD 1.55 billion in 2026 and is projected to reach USD 2.25 billion by 2031.

Which region is the fastest growing for animal wound treatments?

Asia-Pacific is forecast to expand at a 7.11% CAGR through 2031 due to rising pet ownership and upgraded veterinary infrastructure.

Which product category is expected to post the highest growth?

Advanced dressings such as foam, hydrocolloid, and antimicrobial platforms are projected to grow at 8.32% CAGR between 2026 and 2031.

How are tele-veterinary services influencing wound care sales?

Remote consultations increase home-care adoption, and wound-related tele-visits represented 18% of Vetster’s 2025 appointments, supporting demand for mail-order dressings

What role do regenerative therapies play in animal wound healing?

Platelet-rich plasma, keratin hydrogels, and stem-cell sheets are gaining commercial traction for chronic wounds, offering faster closure but at premium prices.

Page last updated on: