Veterinary Anti-infectives Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 9.19 Billion |

| Market Size (2031) | USD 11.87 Billion |

| Growth Rate (2026 - 2031) | 5.24% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

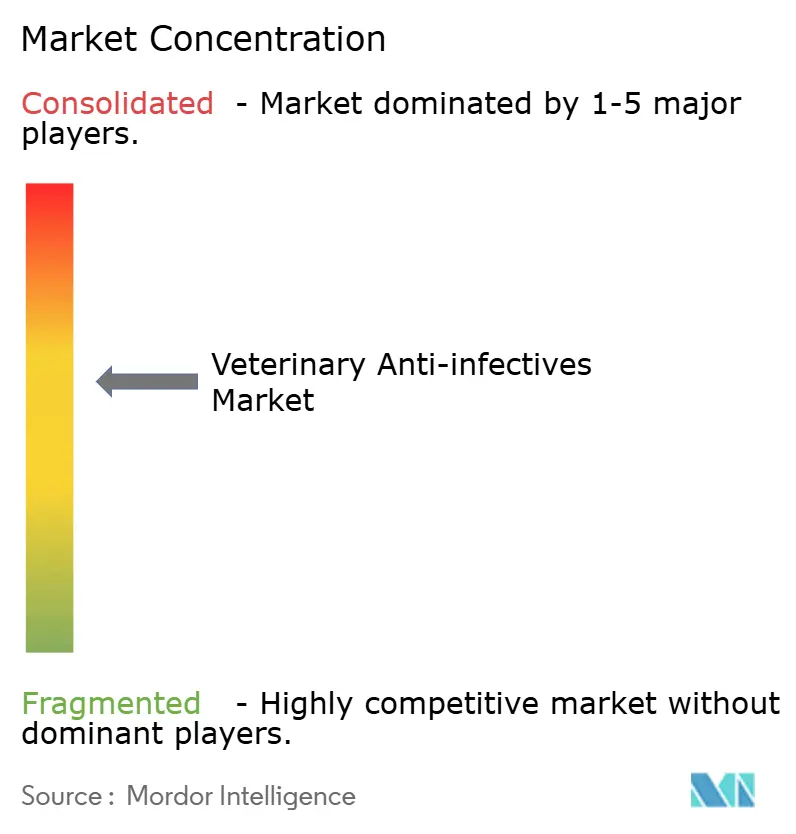

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veterinary Anti-infectives Market Analysis by Mordor Intelligence

The veterinary anti-infectives market size was valued at USD 8.74 billion in 2025 and estimated to grow from USD 9.19 billion in 2026 to reach USD 11.87 billion by 2031, at a CAGR of 5.24% during the forecast period (2026-2031). Robust demand spans both food-producing and companion animals as antimicrobial agents remain essential for managing respiratory, enteric, and dermatological infections. Livestock intensification, especially in Asia Pacific, is lifting volume needs, while rising pet ownership and “humanization” trends are expanding premium product sales in developed economies. Governments are simultaneously tightening antimicrobial stewardship rules, stimulating investment in precision-dosing technologies, targeted formulations, and alternatives that mitigate resistance. Consolidation among manufacturers and a pivot toward digital pharmacy channels further shape competitive strategies as companies seek scale, regulatory expertise, and direct-to-consumer reach within the veterinary anti-infectives market.

Key Report Takeaways

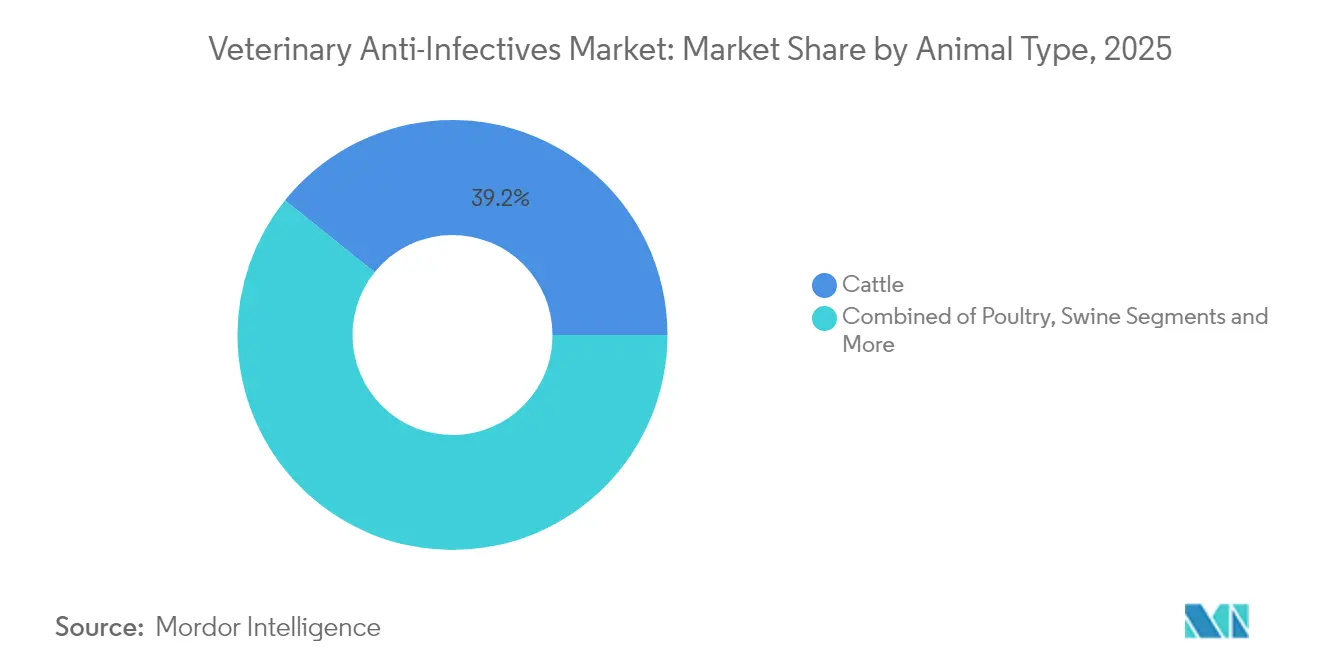

- By animal type, cattle led with 39.22% veterinary anti-infectives market share in 2025; poultry is projected to advance at a 6.22% CAGR through 2031.

- By product type, antibacterials commanded 28.95% of the veterinary anti-infectives market size in 2025, while antivirals are expected to grow at an 8.05% CAGR to 2031.

- By mode of administration, oral solutions accounted for 50.05% of the veterinary anti-infectives market size in 2025; injectables are set to expand at a 6.31% CAGR between 2026 and 2031.

- By distribution channel, veterinary hospitals held 45.55% of the veterinary anti-infectives market share in 2025, while online platforms are forecast to post a 11.74% CAGR through 2031.

- By geography, North America commanded a 31.95% share in 2025, whereas Asia-Pacific is advancing at a 7.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Veterinary Anti-infectives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of zoonotic & food-borne diseases | +1.20% | Global, acute in APAC & Sub-Saharan Africa | Medium term (2-4 years) |

| Growing companion-animal ownership & spend | +0.90% | North America & EU core; urban APAC expanding | Long term (≥ 4 years) |

| Expansion of intensive livestock systems | +0.80% | APAC core; Latin America & MEA spill-over | Medium term (2-4 years) |

| Pipeline of novel antimicrobial classes | +0.60% | North America & EU led | Long term (≥ 4 years) |

| Precision-livestock tools enabling dosing | +0.40% | North America & EU; early Australia adoption | Medium term (2-4 years) |

| Aquaculture regulations spurring innovation | +0.30% | Norway, Chile & APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Zoonotic & Food-Borne Diseases

Frequent H5N1 outbreaks in poultry and recent detections in US dairy herds have heightened awareness of cross-species transmission risks, prompting emergency vaccine collaborations between Elanco and Medgene. Surveillance reports show 75% of emerging infectious diseases are zoonotic, leading veterinary authorities to boost monitoring budgets and fast-track rapid diagnostic approvals. Zoetis introduced an AI-enabled in-clinic hematology analyser that delivers reference-lab quality results, accelerating therapy decisions and supporting data-driven antimicrobial stewardship. Demand for broad-spectrum and long-acting drugs consequently increases across the veterinary anti-infectives market. Governments are also funding One-Health initiatives that merge human and animal epidemiological data, creating sustained procurement pipelines for anti-infective stockpiles. As biosecurity investments rise, suppliers with scalable manufacturing and regulatory fluency gain competitive leverage.

Growing Companion-Animal Ownership & Spending

Pet ownership rates climbed again in 2025, yet more than half of US pet owners deferred at least one medical service primarily due to cost concerns. This affordability gap fuels interest in long-acting injectables such as cefovecin, which provide two-week coverage from a single dose and reduce repeat clinic visits. Corporate practice groups and insurers are piloting wellness-plan models that bundle diagnostics and prescriptions, supporting predictable uptake of premium therapeutics in the veterinary anti-infectives market. Boehringer Ingelheim’s 2024 acquisition of Saiba Animal Health added a virus-like-particle platform that aims to produce therapeutic vaccines for chronic canine diseases, reflecting broader demand for novel modalities. Tele-triage and e-prescribing services are scaling rapidly, bringing previously underserved owners into the formal care pathway and expanding the prescription base for anti-infectives. Digital pharmacies integrate seamlessly with these services, offering overnight delivery and automated refill reminders that enhance compliance.

Expansion of Intensive Livestock Production Systems

FAO modelling indicates global antibiotic use in food animals could jump 30% by 2040 without intervention, underscoring the tension between productivity goals and antimicrobial conservation. Large dairies and feedlots post the highest treatment intensities, pushing the veterinary anti-infectives market toward precision dosing and targeted formulations. Merck Animal Health’s SenseHub Feedlot platform harnesses biometric sensors to detect bovine respiratory disease earlier, cutting therapeutic courses and mortality. Producers adopting similar systems report up to 57% reductions in drug volumes, illustrating the commercial incentive to link performance analytics with antibiotic stewardship. Asia Pacific mega-farms, especially in China and India, invest heavily in automated drinker and feeder medicators that ensure accurate drug delivery, mitigating under- or over-dosing risks. These trends spur demand for high-concentration soluble powders and water-stable premixes engineered for modern production environments.

Pipeline of Novel Antimicrobial Classes & Formulations

Artificial-intelligence screening has rapidly expanded the discovery universe, unveiling nearly 900,000 antimicrobial peptide candidates from microbial genomic data. Halicin, an AI-identified small molecule, demonstrates bactericidal activity against 13 prominent veterinary pathogens with low resistance development profiles. University of Saskatchewan scientists isolated porcine β-defensin-5 that shows promise against swine dysentery, hinting at species-specific biologics. Nanotechnology carriers, such as microbubble-encapsulated oxytetracycline, improve tissue penetration and reduce drug quantities, aligning with stewardship aims. Phage therapy advances are particularly relevant for poultry and aquaculture sectors grappling with multi-drug-resistant E. coli, and early trials demonstrate protective benefits in broiler models. These discoveries ensure a vibrant research pipeline that will diversify the veterinary anti-infectives market beyond conventional small molecules.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of counterfeit veterinary medicines | -0.80% | Sub-Saharan Africa, Asia & Latin America | Short term (≤ 2 years) |

| Escalating cost of veterinary care services | -0.60% | Global, acute in developed markets | Medium term (2-4 years) |

| AMR-driven usage caps reducing prophylaxis | -0.90% | EU & North America, expanding globally | Long term (≥ 4 years) |

| API supply shocks from environmental rules | -0.40% | India & China manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Proliferation of Counterfeit Veterinary Medicines

The WHO estimates that antimicrobial and antimalarial agents dominate global counterfeit seizures, with veterinary channels particularly vulnerable in regions lacking robust regulatory oversight.[3]World Organization for Animal Health, “Global Antimicrobial Resistance Strategy,” woah.orgStudies indicate one-fifth of medicines in sub-Saharan Africa fail quality specifications, threatening treatment outcomes and accelerating resistance. Fragmented supply chains that rely on informal agro-vet stores invite infiltration by falsified products bearing popular brand names. Serialization and blockchain track-and-trace pilots launched by multinational producers demonstrate technical feasibility but remain costly for low-margin rural markets. Regional economic blocs, including ECOWAS, have begun harmonizing registration processes to block unlicensed imports, yet enforcement capacity lags. This proliferation depresses brand equity and complicates stewardship, restraining value growth within the veterinary anti-infectives market.

Escalating Cost of Veterinary Care Services

Veterinary fees in North America and Western Europe rose faster than consumer inflation between 2020 and 2024, resulting in delayed consultations and prescription abandonment. Surveys reveal 71% of US pet owners cite cost as the top barrier to recommended treatments. Higher practice overhead, wage pressures, and investment in diagnostic equipment contribute to rising invoices. Consequently, budget-constrained owners may demand lower-priced generics or forego therapy, limiting premium product uptake in the veterinary anti-infectives market. Insurers respond with expanded accident-and-illness policies that reimburse medications, but adoption remains below 5% of the dog and cat population. Subsidized community clinics and tele-health triage alleviate some access gaps, yet macroeconomic uncertainty keeps price sensitivity high.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Animal Type: Cattle Scale Meets Poultry Momentum

Cattle generated the most significant revenue within the veterinary anti-infectives market in 2025, with a 39.22% share, as dairy and beef operations relied on antimicrobials for mastitis and respiratory disease control. The veterinary anti-infectives market size for bovine therapeutics is forecast to grow steadily as large herd operations adopt precision-dosing tools that increase value per dose while containing volumes. Poultry, however, is projected to outpace all other species at a 6.22% CAGR through 2031, propelled by expanding broiler capacity in China, India, and Brazil. Avian-specific formulations with short withdrawal times gain uptake as exporters comply with tighter residue limits. Swine producers continue to grapple with post-weaning diarrhea and African swine fever threats, supporting demand for both antibiotics and immune-modulating feed additives. Companion animals remain a premium niche as owners prioritize convenience formulations, though cost sensitivity shapes purchasing decisions in lower-income brackets.

The segmental outlook is increasingly shaped by digital surveillance, with cattle feedlots integrating RFID ear tags connected to cloud dashboards that alert veterinarians to subclinical illnesses. These systems shift purchases toward high-potency injectables used earlier in disease cycles, enhancing therapeutic outcomes while reducing course length. Poultry integrators invest in waterline medication controllers that adjust dosing based on real-time flock metrics, raising demand for soluble powders designed for variable pH environments. Aquaculture, though still modest in revenue, emerges as a strategic frontier as Atlantic salmon producers trial phage biocontrol and nano-encapsulated antibiotics to combat sea lice and vibrio infections. The diversified species mix ensures resilience in the veterinary anti-infectives market even as stewardship pressure alters individual usage patterns.

By Product Type: Antibacterials Dominate, Antivirals Accelerate

Antibacterials retained a 28.95% share of the veterinary anti-infectives market size in 2025, supported by a broad catalogue of β-lactams, tetracyclines, and macrolides cleared across multiple species. Stewardship initiatives now favor narrow-spectrum and combination products aimed at specific pathogens, prompting reformulation activity among leading brands. Antivirals are forecast to register the fastest 8.05% CAGR as H5N1, porcine reproductive and respiratory syndrome, and koi herpesvirus outbreaks expose gaps in preventive measures. R&D pipelines feature nucleoside analogues and virus-like particle vaccines that promise shorter treatment courses and lower resistance development potential. Antifungals, while representing a smaller revenue pool, address rising incidences of Malassezia and Aspergillus infections in pets, with single-dose otic gels such as Otiserene and Mometamax Single gaining adoption due to simplified compliance. Antiprotozoals maintain relevance in endemic regions battling coccidiosis and babesiosis, and ongoing trials of toltrazuril combinations highlight a shift toward multi-target therapies.

The innovation pipeline concentrates on delivery enhancements. Long-acting injectable suspensions deliver steady plasma levels for up to two weeks, boosting adherence while limiting clinic revisits. Water-stable micropellets allow uniform dispersion in poultry and shrimp ponds, reducing sediment wastage. Companies also explore biodegradable implant matrices for slow-release antiviral peptides in swine, bridging prophylaxis and treatment. Collectively, these advances ensure the veterinary anti-infectives market retains a balanced mix of established classes and breakthrough modalities that respond to species-specific disease burdens.

By Mode of Administration: Oral Convenience, Injectable Precision

Oral solutions dominated with a 50.05% share of the veterinary anti-infectives market size in 2025, as mass-medication via drinking systems or feed remains economical for herd and flock settings. Soluble antibiotics such as oxytetracycline succeed because they integrate seamlessly with automated waterlines and permit rapid flock-wide exposure following pathogen detection. Yet bioavailability variability and palatability issues drive interest in micro-encapsulated powders that bypass upper-gut degradation. Injectable formulations are predicted to post the highest 6.31% CAGR, driven by long-acting cephalosporins and macrolides that deliver therapeutic coverage from a single shot. Veterinarians value such precision for valuable breeding stock, where treatment timing directly affects reproductive and performance metrics.

Topical applications fill niche roles in dermatology and ontology, with once-a-week ear gels eliminating owner errors and boosting cure rates. Intramammary infusions have seen formulation revisions that marry anti-inflammatory agents with antibiotics, cutting mastitis downtime in high-yield dairy cows. Looking forward, transdermal patches under exploration for feline viral infections could expand options for cats that resist oral dosing. These advances maintain clinician flexibility and reinforce stewardship goals by matching drug exposure to infection site and severity across the veterinary anti-infectives market.

By Distribution Channel: Hospitals Hold, E-commerce Scales

Veterinary hospitals captured 45.55% of prescription sales in 2025, leveraging trust relationships and regulatory requirements mandating veterinary oversight. Their embedded diagnostic assets enable same-visit prescriptions, a convenience particularly valued by pet owners facing acute conditions. However, e-commerce is the fastest mover at a 11.74% CAGR as platforms such as Amazon Pharmacy integrate with vet-validation partners to meet prescription rules while offering doorstep delivery. The shift benefits chronic therapy categories where refill frequency is predictable.

Rural mixed-practice clinics remain vital for livestock segments, especially in regions where mobile-vet services cover expansive geographies. Their competitive posture now hinges on stocking broad portfolios and offering telemedicine follow-ups that limit producer travel. Brick-and-mortar drug stores lose share because over-the-counter access to medically important antimicrobials has vanished under FDA Guidance #263.Distributors increasingly bundle software portals that automate veterinary script approvals and compliance logs, smoothing the path for online retailers while ensuring stewardship data capture within the veterinary anti-infectives market.

Geography Analysis

North America retained the largest revenue in 2024, anchored by advanced veterinary infrastructure and high per-animal spending. FDA prescription-only reforms curtailed hobby-farmer antibiotic purchases, but stimulated demand for diagnostics and refined dosing tools that help practitioners justify therapies in stewardship-scrutinized environments. Canada’s Veterinary Drugs Directorate aligns closely with US regulations, easing cross-border trade and encouraging harmonized label expansions for new molecules. Mexico benefits from integrated supply chains, though varied enforcement capacity leads multinational firms to emphasize training and quality-assurance initiatives to safeguard brand integrity.

Europe showcases the world’s strictest antimicrobial-usage controls, achieving a 50% reduction in veterinary antibiotic sales over 12 years through the ESVAC surveillance network. Distributors now report usage volumes into a centralized EU database, a transparency measure that influences purchasing and supplier negotiations. Category-B caps reorient sales toward first-line products, prompting companies to divulge robust stewardship arguments when submitting new dossiers. Post-Brexit, the UK introduced fast-track procedures for innovative veterinary medicines, accelerating launches but maintaining follow-up pharmacovigilance to guard against resistance.

Asia Pacific is the fastest-growing arena at 7.05% CAGR, propelled by China and India’s expanding protein appetites and maturing companion-animal markets. Government programs to modernize dairy and broiler sectors prioritize biosecurity, elevating orders for high-quality injectable ceftiofur and florfenicol. Simultaneously, environmental crackdowns on pharmaceutical-plant effluent in China periodically tighten API exports, adding volatility to regional supply of tetracyclines and macrolides. Japan’s Ministry of Agriculture requires annual farm-level antibiotic reporting from 2026, a precedent that could inspire similar mandates across ASEAN and further evolve the veterinary anti-infectives market.

Competitive Landscape

The veterinary anti-infectives market is moderately concentrated. Zoetis, Boehringer Ingelheim, and Merck Animal Health anchor global revenues with broad species portfolios and strong regulatory affairs capacity. These leaders exploit comprehensive pharmacovigilance datasets to expedite label extensions and satisfy stewardship reporting.

Strategic M&A continues as incumbents fill portfolio gaps in aquaculture and companion-animal niches. Merck Animal Health’s 2025 acquisition of Elanco’s aqua unit added vaccines and antibiotics, positioning it for Chilean and Norwegian regulations. Boehringer Ingelheim’s purchase of Saiba Animal Health underscores a shift toward therapeutic vaccines that could offset declining prophylactic antibiotic volumes. AI-focused biotechs partner with majors for peptide and phage candidates, exchanging discovery algorithms for clinical and manufacturing muscle.

Technology integration is now pivotal. Diagnostics firms align with drug makers to create closed-loop ecosystems where early detection prompts targeted prescription of branded therapeutics, strengthening customer stickiness. Cloud-connected dosing guns automatically log treatment data, easing compliance audits and feeding population-level analytics that inform R&D priorities. Generics manufacturers remain competitive on unit cost, but stewardship reporting requirements and compliance audits raise fixed costs, potentially squeezing smaller players. Consequently, the competitive arena favors firms that marry novel science, regulatory proficiency, and digital services within the veterinary anti-infectives market.

Veterinary Anti-infectives Industry Leaders

Boehringer Ingelheim GmbH

Ceva Santé Animale

Zoetis Inc.

Merck & Co., Inc.

Elanco Animal Health Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Dechra received FDA approval for Otiserene, a single-dose, long-acting otic suspension combining marbofloxacin, terbinafine, and dexamethasone to treat canine otitis externa. Clinical trials showed 71.3% improvement rates compared to 26.3% in control groups.

- May 2025: MSD Animal Health obtained FDA clearance for Mometamax Single, the first one-dose Pseudomonas otic solution for dogs.

- April 2025: Zoetis secured an expanded Simparica Trio indication covering flea and tapeworm prevention by killing vector fleas.

- February 2025: Merck Animal Health completed the acquisition of Elanco’s aqua business to broaden its fish-health portfolio.

Research Methodology Framework and Report Scope

Market Definition and Key Coverage

Our study defines the veterinary anti-infectives market as finished prescription and over-the-counter drugs, antibiotics, antivirals, antifungals, and antiparasitics, administered to companion and food-producing animals for therapeutic or metaphylactic control of infectious pathogens. According to Mordor Intelligence, valuation starts at the finished-dosage level and covers all global sales through clinical, retail, and digital channels.

Exclusions: growth-promoting feed additives, farm disinfectants, and biologic vaccines fall outside this scope.

Segmentation Overview

- By Animal Type

- Cattle

- Poultry

- Swine

- Cats

- Dogs

- Other Animals

- By Product Type

- Antibacterials

- Antivirals

- Antifungals

- Antiprotozoals & Others

- By Mode of Administration

- Oral

- Parenteral

- Topical

- Others

- By Distribution Channel

- Veterinary Hospitals

- Veterinary Clinics

- Pharmacies & Drug Stores

- Online Channels

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed practicing veterinarians, livestock integrators, pharmacy buyers, and regulators across North America, Europe, Asia, and Latin America. These conversations validated dosing patterns, price corridors, and regulation-driven usage caps, and they informed final adjustments in regional demand assumptions.

Desk Research

We began with government datasets such as OIE animal-disease notifications, USDA livestock inventories, Eurostat veterinary expenditure series, and FAO meat production dashboards, which framed the demand pool. Industry associations, for example, the World Veterinary Association and HealthforAnimals, provided drug usage codes and stewardship guidelines that guided spectrum splits. Company 10-Ks, investor decks, and patent abstracts retrieved through D&B Hoovers, Dow Jones Factiva, and Questel helped our team benchmark average selling prices and pipeline flow. A variety of peer-reviewed journals on antimicrobial resistance trends rounded out the literature. This list is illustrative, and many other public and paid sources were reviewed for validation.

Market-Sizing & Forecasting

A top-down demand pool was first built from species population, disease prevalence indices, and treatment penetration rates, which are then cross-checked with sampled supplier roll-ups for antibacterials and broader anti-infectives. Where channel data were thin, we filled gaps with import shipment values flagged in Volza and with average treatment-cost insights from clinic surveys. Key model drivers include livestock headcount growth, companion animal spend, antimicrobial resistance policy milestones, average therapy length, and currency movement. Multivariate regression, complemented by scenario analysis around AMR legislation timing, guides projections through 2030.

Data Validation & Update Cycle

Outputs pass variance checks against independent trade statistics, analyst peer review, and supervisor sign-off. Reports refresh each year, and interim updates trigger when a material event, such as a major drug class ban, occurs. Before any client release, an analyst reruns the latest data sweep to keep the baseline current.

Why Our Veterinary Anti-infectives Baseline Commands Reliability

Published figures often diverge because firms count different drug classes, apply distinct usage-rate assumptions, or freeze exchange rates at older benchmarks. We anchor our totals to clearly stated scope boundaries and refresh currency and livestock data every twelve months, which keeps our baseline aligned with market reality.

Key gap drivers include competitors limiting their scope to antimicrobials only, folding vaccines into totals, or using a fixed 2024 livestock census without mid-year revisions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| Mordor Intelligence | USD 8.74 B (2025) | - |

| Regional Consultancy A | USD 8.69 B (2025) | Excludes antivirals and antifungals, uses static 2023 exchange rates |

| Global Consultancy B | USD 9.09 B (2025) | Adds in-feed additives and preventive biologics, applies aggressive ASP uplift |

These comparisons show that Mordor's disciplined scope choices and annual refresh cadence deliver a balanced, transparent baseline that decision-makers can trace back to verifiable variables.

Key Questions Answered in the Report

What is the current Veterinary Anti-infectives Market size?

The Veterinary Anti-infectives Market size is estimated at USD 9.19 billion in 2026 and is projected to register a CAGR of 5.24% during the forecast period (2026-2031)

Who are the key players in Veterinary Anti-infectives Market?

Bayer AG, Boehringer Ingelheim GmbH, Ceva Santé Animale, Elanco and Zoetis Inc. are the major companies operating in the Veterinary Anti-infectives Market.

Which is the fastest growing region in Veterinary Anti-infectives Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Veterinary Anti-infectives Market?

In 2025, the North America accounts for the largest market share in Veterinary Anti-infectives Market.

What years does this Veterinary Anti-infectives Market cover?

The report covers the Veterinary Anti-infectives Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Veterinary Anti-infectives Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: