Veterinary Dermatology Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

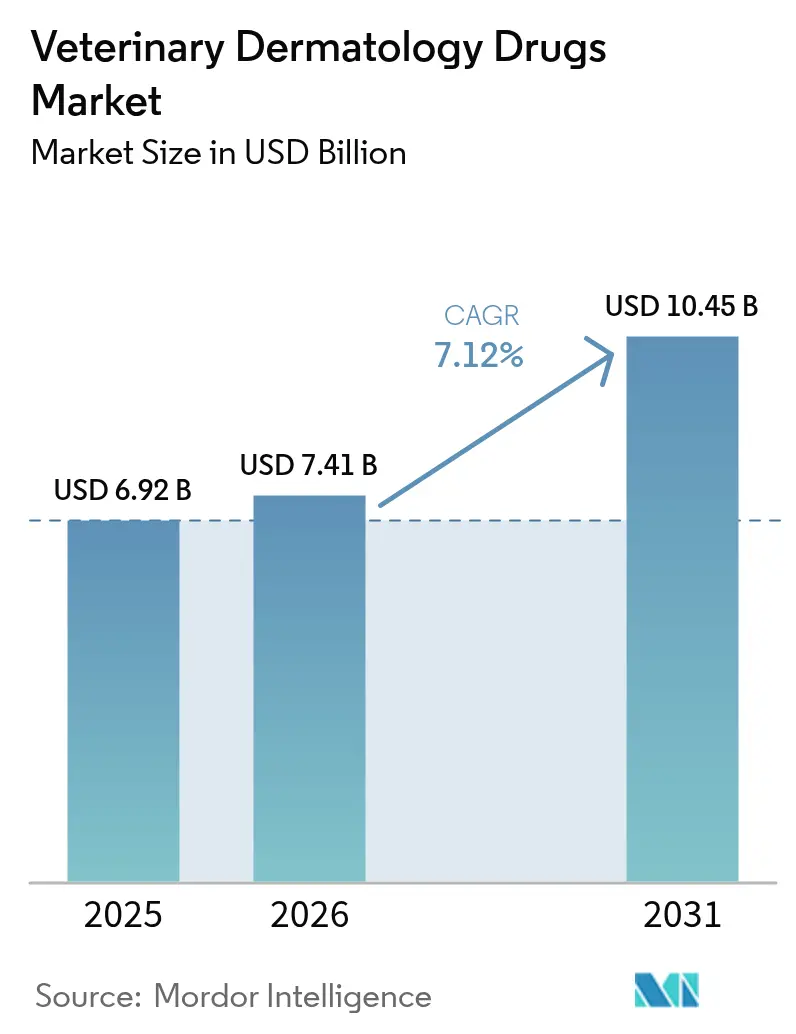

| Market Size (2026) | USD 7.41 Billion |

| Market Size (2031) | USD 10.45 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

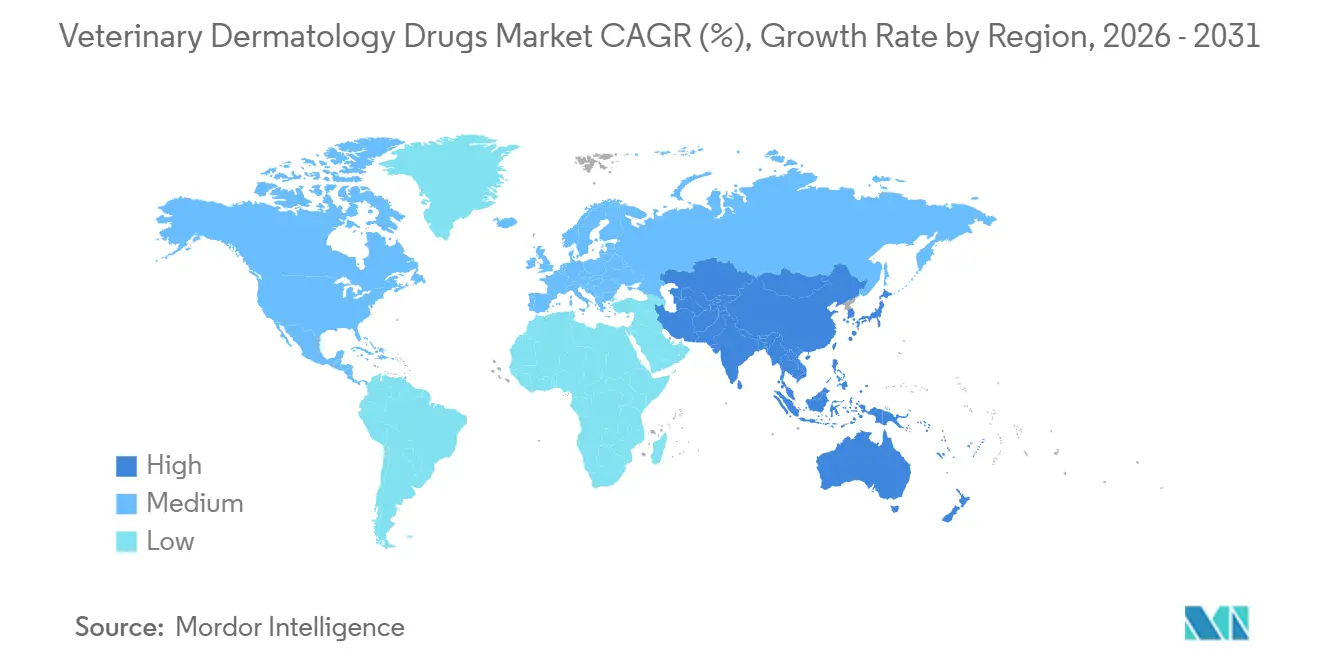

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veterinary Dermatology Drugs Market Analysis by Mordor Intelligence

The veterinary dermatology drugs market size was valued at USD 6.92 billion in 2025 and estimated to grow from USD 7.41 billion in 2026 to reach USD 10.45 billion by 2031, at a CAGR of 7.12% during the forecast period (2026-2031). Mounting pet-owner willingness to treat skin disorders with the same urgency shown in human care, together with year-round parasite pressure, is lifting prescription volumes in both preventive and chronic segments. Anti-bacterial agents still anchor revenue, yet double-digit expansion in monoclonal antibodies signals a pivot toward targeted immunomodulation. E-commerce is widening access and price transparency, while large retailers integrate pharmacy fulfillment with clinic rollouts, shifting share away from traditional veterinary practices. Competitive intensity is rising as incumbents defend oral isoxazoline franchises and challengers launch new JAK inhibitors, all under closer post-marketing surveillance from regulators.

Key Report Takeaways

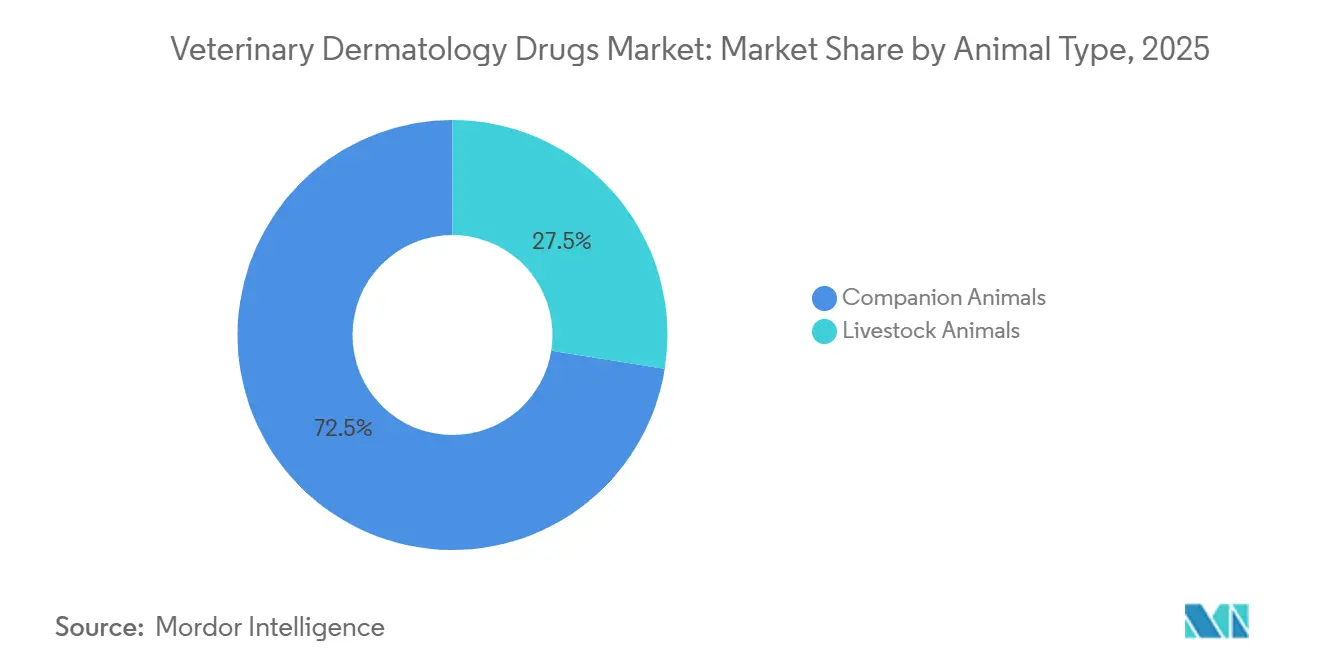

- By animal type, companion animals captured 72.53% of 2025 revenue and are projected to expand at a 9.75% CAGR between 2026-2031.

- By route, topical formulations accounted for 46.15% of 2025 sales, yet injectables are growing at 10.82% annually through 2031.

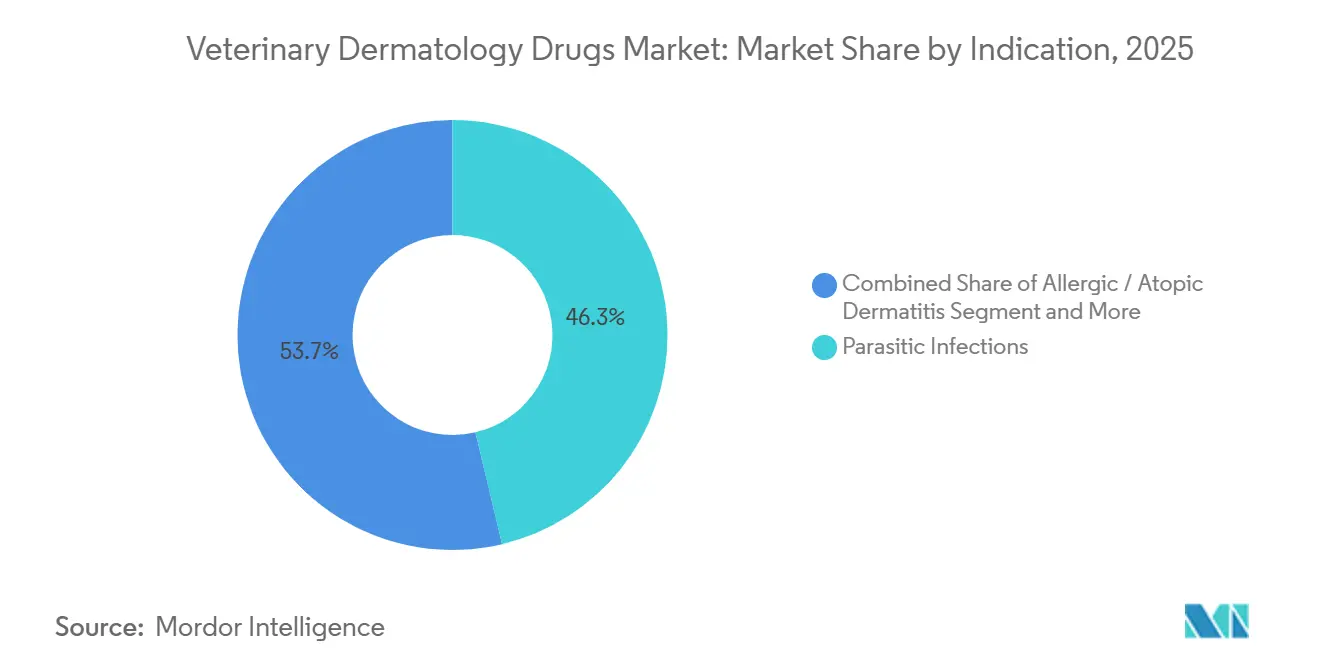

- By indication, allergic and atopic dermatitis is forecast to rise at 11.19% annually, outpacing the 46.32% share held by parasitic infections in 2025.

- By distribution channel, e-commerce platforms are climbing at 12.56% CAGR, while veterinary hospitals & clinics controlled 38.21% revenue share in 2025.

- By geography, North America contributed 38.52% of 2025 revenue, whereas Asia-Pacific is advancing at a 11.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Veterinary Dermatology Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of allergic & atopic dermatitis in companion animals | +1.8% | Global, concentrated in North America & Europe | Medium term (2–4 years) |

| Surge in global pet ownership & humanization expenditure | +2.1% | Asia-Pacific core, spill-over to Latin America | Long term (≥4 years) |

| Rapid uptake of monoclonal-antibody & JAK-inhibitor therapies | +1.5% | North America & EU, expanding to APAC | Short term (≤2 years) |

| Climate-driven expansion of ectoparasite ranges elevating skin infections | +1.3% | Global, acute in temperate & subtropical zones | Medium term (2–4 years) |

| AI-enabled tele-dermatology platforms widening early-diagnosis reach | +0.7% | North America, pilot adoption in Asia-Pacific | Long term (≥4 years) |

| Subscription pet-wellness plans bundling dermatology preventives | +0.9% | North America & Europe, emerging in urban Asia | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Surge in Global Pet Ownership & Humanization Expenditure

Pet humanization is turning dermatology from episodic intervention to planned care. Urban households allocate budgets once reserved for pediatric health, driving adherence to multi-month atopic regimens. Rapid growth in cat ownership in East-Asia and expanding telemedicine use broaden access to early diagnosis, raising the treated population. Higher disposable incomes in Latin America are also moving owners toward branded parasiticides rather than homemade remedies. Together, these trends enlarge the paying base for the veterinary dermatology drugs market.

Rapid Uptake of Monoclonal-Antibody & JAK-Inhibitor Therapies

Biologics that block specific cytokines are replacing broad anti-inflammatories. Cytopoint has treated more than 10 million dogs worldwide since launch. Apoquel delivers fast relief through oral dosing yet carries label cautions on live-vaccine overlap, prompting veterinarians to stagger immunizations. Elanco’s Zenrelia faced a 2024 FDA safety communication about vaccine-induced disease, proving that post-market vigilance can slow adoption[2]U.S. Food and Drug Administration, “Safety Communication on Zenrelia,” fda.gov . Despite such headwinds, the segment grows fastest because owners accept higher prices for drugs that avoid steroid-linked adverse events.

Climate-Driven Expansion of Ectoparasite Ranges Elevating Skin Infections

Warmer winters extend tick activity into new latitudes, converting seasonal prevention into year-round protocols. The Asian longhorned tick has settled in 19 U.S. states as of 2024, pushing veterinarians to recommend uninterrupted isoxazoline coverage. European guidelines now advise continuous protection in endemic zones[1]European Scientific Counsel Companion Animal Parasites, “Guideline on Ectoparasite Control,” esccap.org. Longer exposure seasons raise sales of long-acting chewables and injectables, boosting the veterinary dermatology drugs market.

AI-Enabled Tele-Dermatology Platforms Widening Early-Diagnosis Reach

Platforms such as Vetscan Imagyst analyze lesion images in minutes, guiding general practitioners toward faster intervention. Remote access is vital in countries where board-certified dermatologists are scarce. Retailers bundle virtual consults into loyalty programs, as Walmart added Pawp tele-vet services to Walmart+ in 2025. Early detection expands the addressable patient pool, supporting sustained revenue growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of biologics & chronic therapies | -1.2% | Global, acute in price-sensitive emerging markets | Short term (≤2 years) |

| Limited awareness & veterinary access in low-income regions | -0.9% | Sub-Saharan Africa, rural Asia, Latin America | Long term (≥4 years) |

| Emerging resistance to isoxazoline ectoparasiticides | -0.8% | Brazil, Southeast Asia, sporadic in North America | Medium term (2–4 years) |

| Vaccine–drug interaction warnings curbing new JAK-inhibitor uptake | -0.6% | North America & EU (strict pharmacovigilance) | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High Cost of Biologics & Chronic Therapies

A single monoclonal-antibody dose for a medium-sized dog can cost USD 50-100, straining budgets in emerging economies without robust pet-insurance coverage. Rural owners often default to generic corticosteroids, leaving chronic dermatitis unmanaged. Production-animal use is even rarer because herd economics favor culling over expensive individual treatment. Subscription wellness plans partly offset costs but remain concentrated in wealthier regions, keeping adoption uneven.

Emerging Resistance to Isoxazoline Ectoparasiticides

Studies in 2024 confirmed fluralaner resistance in Brazilian cattle ticks and afoxolaner resistance in certain flea strains. Mutations in chloride channels and metabolic detoxification reduce efficacy, forcing clinicians to rotate classes and combine topicals, which complicates compliance. Regulatory agencies have not yet finalized stewardship guidelines, raising the risk of wider resistance and a drag on the veterinary dermatology drugs market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Animal Type: Companion Dominance, Livestock Underserved

Companion animals captured 72.53% of 2025 sales and will expand at 9.75% annually through 2031, driven by urbanization and higher spend per pet. Livestock accounts for the remaining 27.47%, constrained by price sensitivity and strict antibiotic policies. The veterinary dermatology drugs market size for companion animals is forecast to cross USD 8 billion by 2031. Dairy farmers often weigh drug cost against herd replacement, limiting biologic use in cattle.

Urban millennials in East-Asia prefer cats due to apartment living, further lifting feline dermatology prescriptions. In contrast, poultry operations focus on biosecurity rather than post-infection drugs, keeping that niche small. These dynamics ensure investment remains skewed toward companion-animal breakthroughs.

By Route of Administration: Injectables Gain on Compliance Advantage

Topicals led with 46.15% share in 2025, yet injectables are growing at 10.82% annually. Cytopoint’s 4-to-8-week dosing schedule eliminates owner forgetfulness and secures veterinarian oversight. Long-acting depot steroids for flare management are in trials, aiming to replicate this benefit. Oral chewables remain popular for parasites due to palatability improvements.

A 2024 AVMA survey found 32.9% of owners buying from online pharmacies, but adherence to multi-week orals lagged, underscoring the appeal of clinic-administered injectables. The veterinary dermatology drugs market share for injectables could reach 32% by 2031 if current growth holds.

By Indication: Allergic Dermatitis Outpaces Parasitic Infections

Parasitic infections held 46.32% of indication share in 2025, yet allergic and atopic dermatitis is climbing at 11.19% annually. Genetic predispositions in popular breeds and rising environmental allergens make chronic itch a recurring revenue driver. Year-round parasite prevalence further blurs traditional seasonality, expanding prophylactic demand.

Continuous tick presence since the establishment of Haemaphysalis longicornis in the Eastern U.S. amplified demand for dual-action products that address both parasites and inflammatory sequelae. Owners increasingly prefer therapies that control pruritus without systemic steroids, reinforcing the appeal of monoclonals.

By Distribution Channel: E-Commerce Disrupts Traditional Clinics

Veterinary clinics retained 38.21% of sales in 2025, but e-commerce is growing at 12.56% annually. Amazon’s collaboration with Vetsource delivers verified prescriptions via Prime two-day shipping[3]Amazon Inc., “Amazon-Vetsource Partnership,” aboutamazon.com . WalmartPetRx.com couples online purchases with in-store clinic pick-up, while Tractor Supply targets rural customers through Tractor Supply Rx.

The veterinary dermatology drugs market now sees online marketplaces capturing a growing slice as owners seek convenience and competitive pricing. Regulatory guidance issued in 2024 mandates prescription validation, favoring larger platforms capable of compliance.

Geography Analysis

North America generated 38.52% of 2025 revenue, supported by high spend per pet and early biologic adoption. Growth is plateauing as preventive parasiticide penetration nears saturation and price competition intensifies. Canada posts steady gains, while Mexico lags due to income disparities and fewer specialty clinics.

Asia-Pacific is the fastest-growing region at an 11.32% CAGR through 2031. Rising disposable income, urban apartment living that favors small pets, and expanding telemedicine adoption support demand. Regional regulatory reliance on Japanese PMDA reviews accelerates product availability, shortening launch timelines.

Europe remains sizeable but slower-moving, constrained by stricter pricing rules and upcoming generic bioequivalence guidelines that may squeeze branded margins. The United Kingdom’s online retailer registration regime, launched in 2024, standardizes e-pharmacy practices and could curb grey-market imports. Latin America and the Middle East & Africa together represent a smaller share but show pockets of rapid growth in major urban centers, offset by limited cold-chain infrastructure for biologics.

Regulatory Landscape

In the United States, veterinary dermatology drugs are regulated by the FDA Center for Veterinary Medicine (CVM) and generally require approval via a New Animal Drug Application (NADA) or Abbreviated NADA (ANADA) before marketing. The conditional approval pathway (CNADA) permits time-limited commercialization while effectiveness data is completed, and FDA activity in this area continued through 2018-2026. FDA also issued a technical amendment effective February 2026 updating administrative actions for NADAs, ANADAs, and CNADAs recorded during Q3 2025.

In Europe, Regulation (EU) 2019/6 governs veterinary medicinal product authorization and reinforces pharmacovigilance and harmonized requirements across member states. The United Kingdom updated its post-Brexit framework via the Veterinary Medicines (Amendment etc.) Regulations 2024 (effective May 2024), including transitional supply provisions for certain products until January 29, 2027. International alignment continues through VICH guidance and the FDA-EMA parallel scientific advice procedure, which adopted revised operating timelines and feedback processes in June 2024, supporting more consistent global development packages for dermatology therapies (including biologics) across major markets.

Competitive Landscape

The market is moderately concentrated. The top manufacturers—Zoetis, Elanco, Ceva Sante Animale, and Virbac—hold a majority of global sales. Zoetis leverages its direct sales force and diagnostics integration to defend Cytopoint and Apoquel leadership positions. Boehringer Ingelheim’s NexGard franchise keeps pressure on oral parasiticides, while Elanco’s Credelio complements its dermatology lineup.

Private equity interest surfaced when EQT and Abu Dhabi Investment Authority acquired Dechra in 2024, signaling confidence in recurring-revenue niches. Technology partnerships add differentiation: Zoetis’ launch of Vetscan Imagyst embeds AI into clinic workflows, driving loyalty. Niche firms such as Nextmune grow via allergen-specific immunotherapy, offering personalized solutions for refractory atopy.

Retail giants are reshaping channel economics rather than inventing drugs. Amazon, Walmart, and Tractor Supply invest in logistics and subscription auto-refill models that lock in customers. Recent FDA online-pharmacy guidance raises compliance costs, advantaging these capital-rich entrants over smaller web retailers.

Veterinary Dermatology Drugs Industry Leaders

Bimeda, Inc.

Zoetis, Inc.

Virbac SA

Ceva Sante Animale

Elanco Animal Health

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Steroid-sparing immunomodulators are expanding the treated population in allergic and atopic dermatitis, and 2026 regulatory actions point to active innovation in this segment. In February 2026, FDA approved MSD Animal Healths Numelvi (atinvicitinib) tablets for canine pruritus control, broadening oral JAK inhibitor options for clinics managing chronic dermatitis cases.

Longer-acting biologics and differentiated dosing intervals also offer a whitespace for owner compliance and clinic workflow, supported by new products and late-stage data. Elanco began a phased US commercial rollout of Befrena (tirnovetmab) in May 2026 following its December 2025 USDA approval as an anti-IL-31 monoclonal antibody for canine allergic and atopic dermatitis. Akston Biosciences presented 2026 data for AKS-699 showing sustained pruritus control in canine models with fewer treatments in a head-to-head IL-31 challenge study. On the supply side, interest in faster-deploying biologics manufacturing approaches, including plant-based expression platforms discussed in recent academic and industry materials, aligns with the market push toward injectable, long-acting therapies that require reliable cold-chain and batch-to-batch consistency at scale.

Recent Industry Developments

- July 2026: Zoetis announced the launch of Lenivia (izenivetmab injection) in Canada and European Union member states. The rollout expands Zoetis footprint in long-acting monoclonal antibody injections, reinforcing clinic-administered biologics as a core modality alongside oral and topical dermatology regimens.

- May 2026: Elanco initiated a phased US launch of Befrena (tirnovetmab), an anti-IL-31 monoclonal antibody injection for canine allergic and atopic dermatitis, following its December 2025 USDA approval. This strengthens competitive intensity in targeted itch control and adds another branded biologic option that can shift prescribing away from steroids and some chronic oral anti-inflammatories.

- December 2025: Elanco received USDA approval for Befrena (tirnovetmab), an anti-IL-31 monoclonal antibody for canine allergic and atopic dermatitis. The approval expanded the pool of regulated biologic therapies available for chronic pruritus management, increasing the importance of pharmacovigilance and product differentiation on dosing interval and clinical response.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers prescription and OTC drugs used to diagnose, treat, and manage skin-related conditions in animals, including therapies for allergy-driven dermatitis, parasitic infestations, and infectious skin issues, across common routes of administration.

Scope exclusions: Devices and hygiene products such as shampoos, wipes, and grooming tools are excluded unless they are regulated as drug therapies.

Segmentation Overview

- By Animal Type

- Companion Animals

- Livestock Animals

- By Route of Administration

- Topical

- Oral

- Injectable

- Other Routes

- By Indication

- Parasitic Infections

- Allergic / Atopic Dermatitis

- Bacterial & Fungal Skin Infections

- Other Indications

- By Distribution Channel

- Veterinary Hospitals & Clinics

- Retail Pharmacies

- E-commerce

- Other Channels

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research helped us lock the market boundary and build a clean demand map by indication, animal type, route, channel, and region. Public sources were used to understand the animal health system, disease context, and policy signals that influence dermatology prescriptions.

We referenced non-paywalled sources such as FDA Center for Veterinary Medicine releases, USDA animal health and census outputs, the European Medicines Agency public assessment reports, and WOAH disease and animal population context, along with peer-reviewed veterinary dermatology journals for condition prevalence ranges and treatment approaches. Company annual reports, investor presentations, reputable press, and selected paid subscriptions for company financials and patent databases were also used to translate product activity into practical market inputs. These examples are not exhaustive, and many other sources were checked to collect data, validate assumptions, and clarify gaps.

Primary Interviews and Surveys

Primary work focused on veterinarians, dermatology specialists, distributor and pharmacy stakeholders, and industry experts who track animal health product demand across regions. We used their input to test what we saw in secondary sources.

For a global view, conversations were spread across key demand centers in APAC, EMEA, and the Americas, so pricing, channel mix, and switching between drug classes could be confirmed before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 13% | APAC: 45% |

| Mid tier: 61% | Functional/Unit leaders: 28% | EMEA: 36% |

| Smaller Players: 14% | Managers: 59% | Americas: 19% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where treated-case demand is reconstructed by region using companion versus livestock population context, expected dermatology case incidence, and the share that reaches a vet and receives drug therapy. That case demand is then translated into value through typical therapy mix and price bands. Once that structure is in place, we corroborate totals using selective bottom-up checks, such as sampling key drug classes and using channel feedback as volume proxies, before adjustments are applied.

Inputs used in the model include (illustratively) growth in companion animal ownership, the mix of allergic dermatitis versus parasitic and infectious cases, average treatment duration for chronic flare management, the split of topical versus oral versus injectable use, and shifts in distribution between hospital pharmacies, retail, and e-commerce. Where a segment did not have clean visibility in every country, gaps were handled through nearby market proxies and expert-validated ratios, then re-checked so the final country roll-ups stayed realistic.

Forecasts were produced using scenario analysis supported by expert views on pricing progression, adoption of newer immunomodulating therapies, and expected changes in parasite pressure and vet visit behavior. When the outlook was sensitive to one driver, we tested the model under conservative and aggressive ranges before locking the final base case.

Data Validation & Update Cycle

Validation is done through triangulation across independent signals, and then the numbers are stress-tested for odd jumps by class, route, channel, and region. If a region-level outcome looks out of line with known demand indicators, we re-check underlying assumptions, re-run the arithmetic, and re-contact sources when the variance cannot be explained cleanly.

Before sign-off, outputs go through multi-step internal reviews so that unit logic, pricing logic, and conversion choices are consistent across countries. Reports are refreshed annually, with interim updates triggered when material events occur, and a fresh final pass is completed close to delivery so clients receive an up-to-date view.

Mordor Intelligence's Veterinary Dermatology Drugs Market Size Compared With Other Published Estimates

Published market sizes for veterinary dermatology drugs often vary because each publisher draws the market boundary differently and then uses different mixes of treatment, pricing, and channel assumptions. Differences also come from which year is treated as the current size, how fast prices are assumed to change, and how strictly estimates are checked against real-world demand signals.

The main gap comes from scope choices around what counts as a dermatology drug and how broad the condition set is. Mordor Intelligence counts only drug therapies tied to veterinary dermatology indications and keeps non-drug skin care items out of the revenue pool. The spread also reflects how some estimates lean on aggressive adoption curves for newer therapies, or apply a single global ASP uplift, while others do not separate companion versus livestock demand patterns and channel mix shifts that change realized pricing.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.41 B (2026) | |

| Trade Journal A | USD 8.67 B (2024) | Uses an earlier base year and tends to apply a higher growth profile from broad pet health spending trends, with limited clarity on therapy mix by route and distribution channel. |

| Regional Consultancy B | USD 17.98 B (2025) | Appears to bundle wider veterinary dermatology spending beyond drug therapies, and the scope likely captures adjacent products or services, which expands the value pool versus a drugs-only definition. |

The table shows that most of the variation is explained by what is included in the revenue pool and how prices and adoption are carried forward by year. By keeping inputs tied to treated demand, therapy mix, and channel reality, the final number stays traceable to repeatable steps that can be reviewed and updated as new signals emerge.

Key Questions Answered in the Report

What is the forecast size of the veterinary dermatology drugs market by 2031?

It is projected to reach USD 10.45 billion by 2031.

How quickly is e-commerce expanding in pet dermatology drug sales?

Online channels are expected to grow at 12.56% annually through 2031, the highest rate among all distribution modes.

Which region shows the highest growth potential?

Asia-Pacific is forecast to post an 11.32% CAGR between 2026-2031, outpacing all other regions.

Why are injectables gaining share over topicals?

Clinic-administered injectables remove owner compliance risk and deliver long-acting relief, driving a 10.82% yearly growth rate for the format.

What is driving demand for allergy therapies in pets?

Rising incidence of atopic dermatitis and owner preference for steroid-sparing options propel double-digit growth in targeted biologics.

Page last updated on: