Veterinary Laser Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

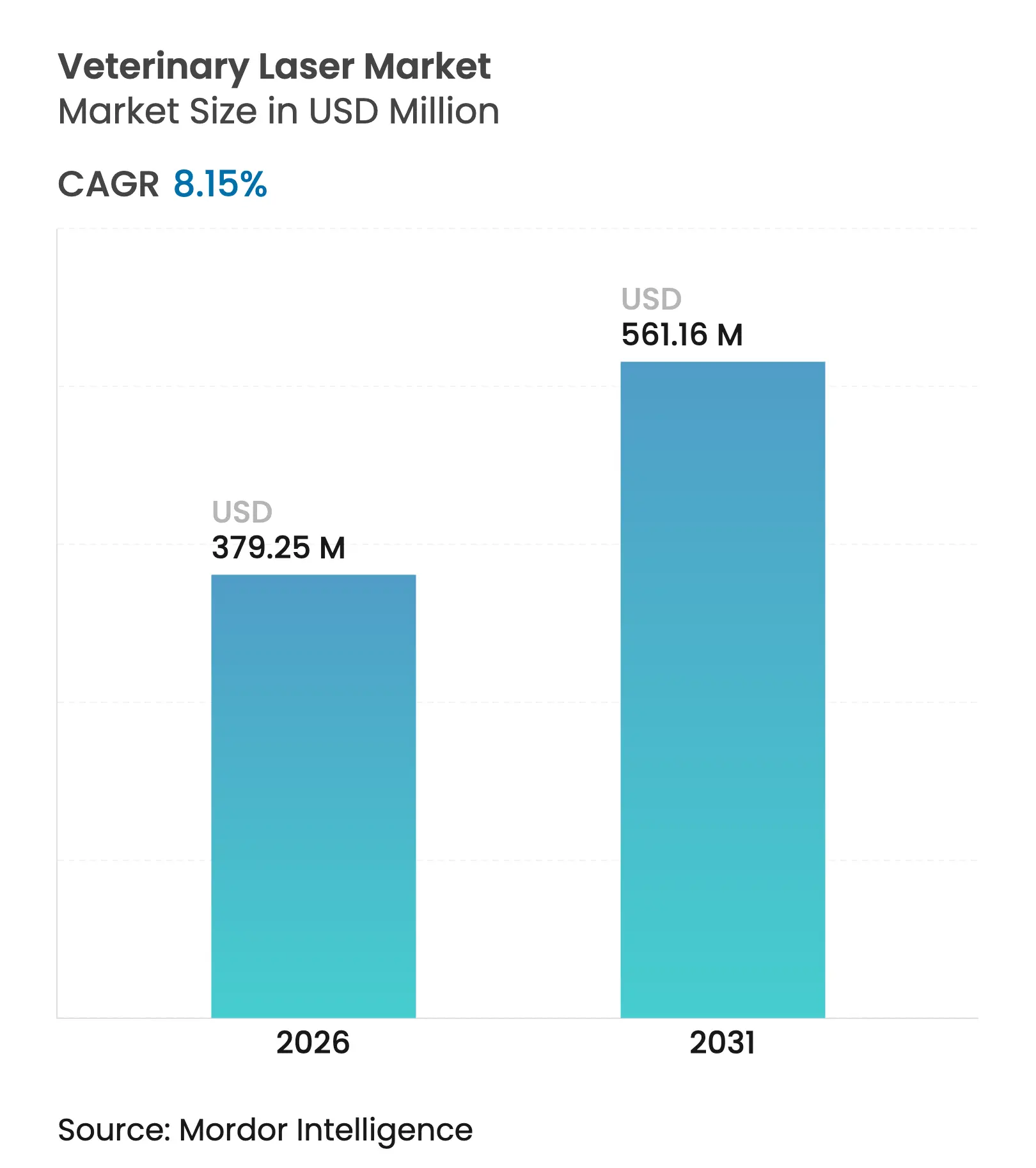

| Market Size (2026) | USD 379.25 Million |

| Market Size (2031) | USD 561.16 Million |

| Growth Rate (2026 - 2031) | 8.15 % CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Veterinary Laser Market Analysis by Mordor Intelligence

The veterinary laser market size is expected to grow from USD 350.67 million in 2025 to USD 379.25 million in 2026 and is forecast to reach USD 561.16 million by 2031 at 8.15% CAGR over 2026-2031. Growth continues to accelerate as companion-animal practices adopt photobiomodulation and surgical platforms to shorten recovery times, reduce post-operative pain, and limit pharmaceutical use. Demand also rises because newer high-power multi-wavelength diode systems are portable, battery-operated, and pre-programmed with species-specific protocols, making in-clinic integration simpler than earlier generations. Practices increasingly see faster payback—often within 18 months—when they bundle laser equipment, training, and follow-up services, a model that lowers upfront capital strain. In parallel, U.S. FDA 510(k) clearances for AI-guided real-time dosimetry reinforce clinical confidence and set global regulatory benchmarks [1]Center for Devices and Radiological Health, “510(k) Summary: Medical Diode Laser Systems,” fda.gov .

Key Report Takeaways

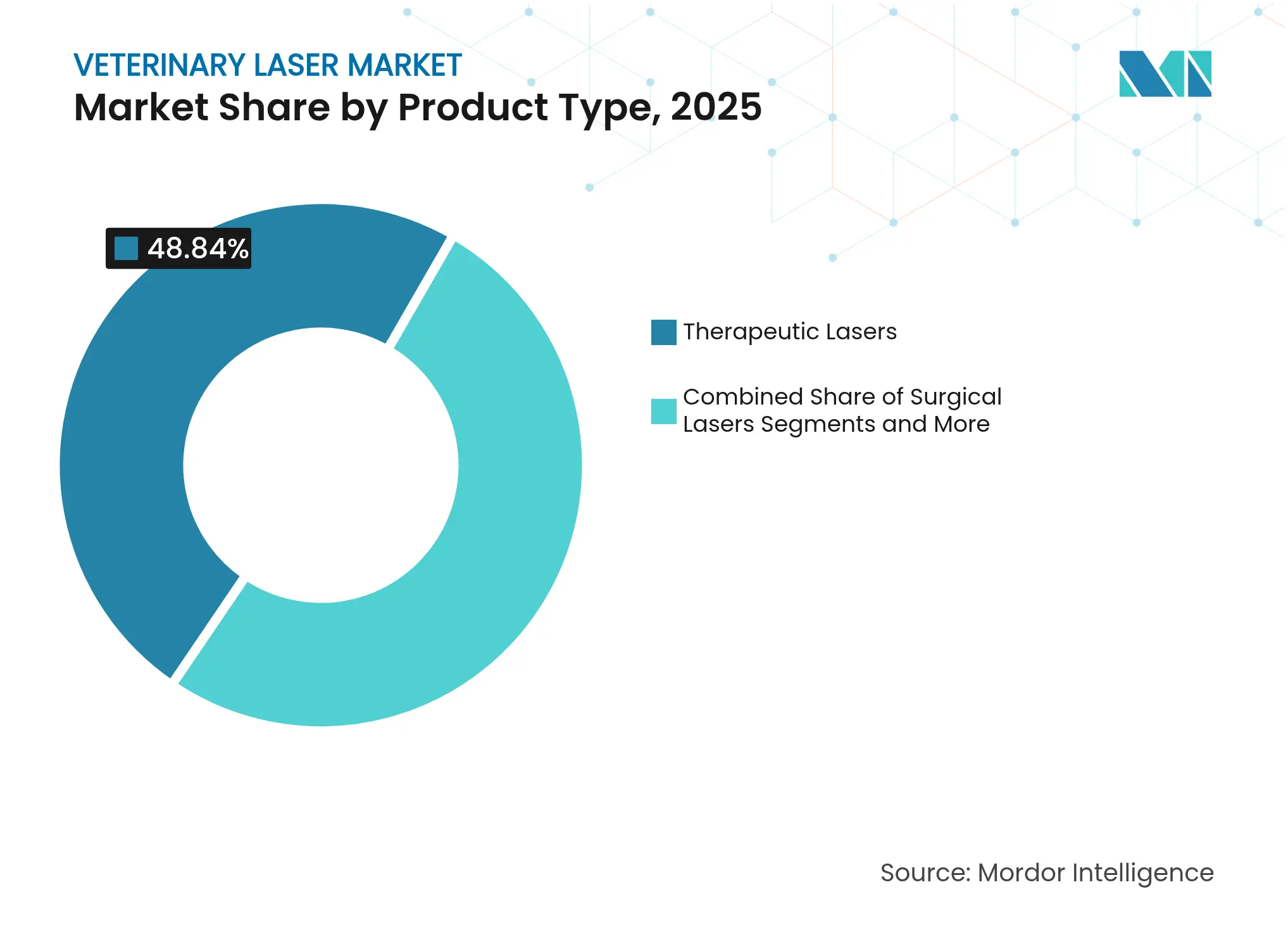

- By product type, therapeutic lasers led with 48.84% of veterinary laser market share in 2025, while surgical lasers are forecast to expand at a 8.95% CAGR through 2031.

- By animal type, dogs accounted for 41.96% share of the veterinary laser market size in 2025; cats are advancing at a 8.86% CAGR between 2026-2031.

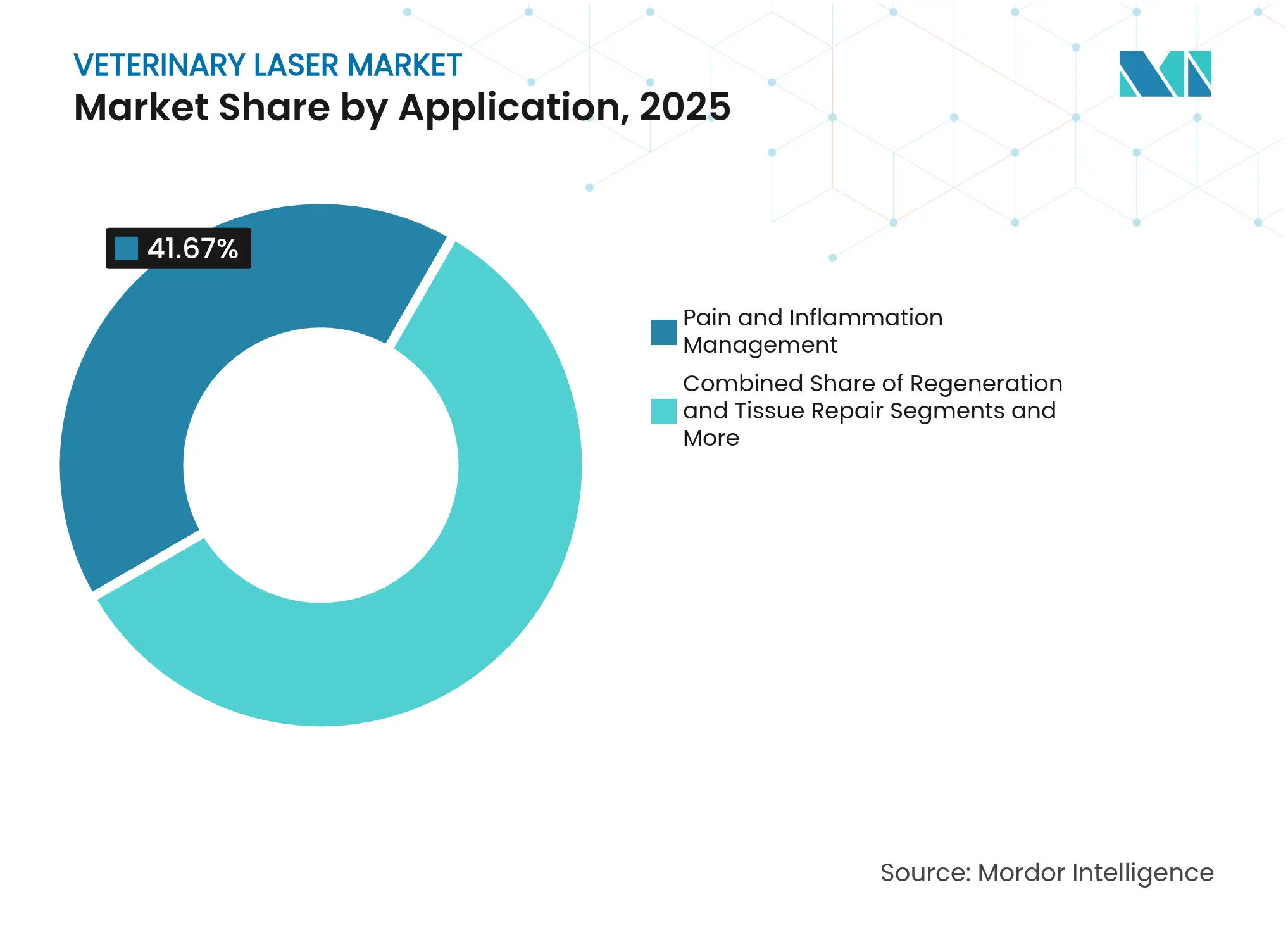

- By application, pain and inflammation management commanded 41.67% share of the veterinary laser market size in 2025, whereas regeneration and tissue repair is projected to grow at 8.91% CAGR to 2031.

- By end user, veterinary hospitals held 52.92% of the veterinary laser market share in 2025; independent clinics are set to grow fastest at 8.96% CAGR through 2031.

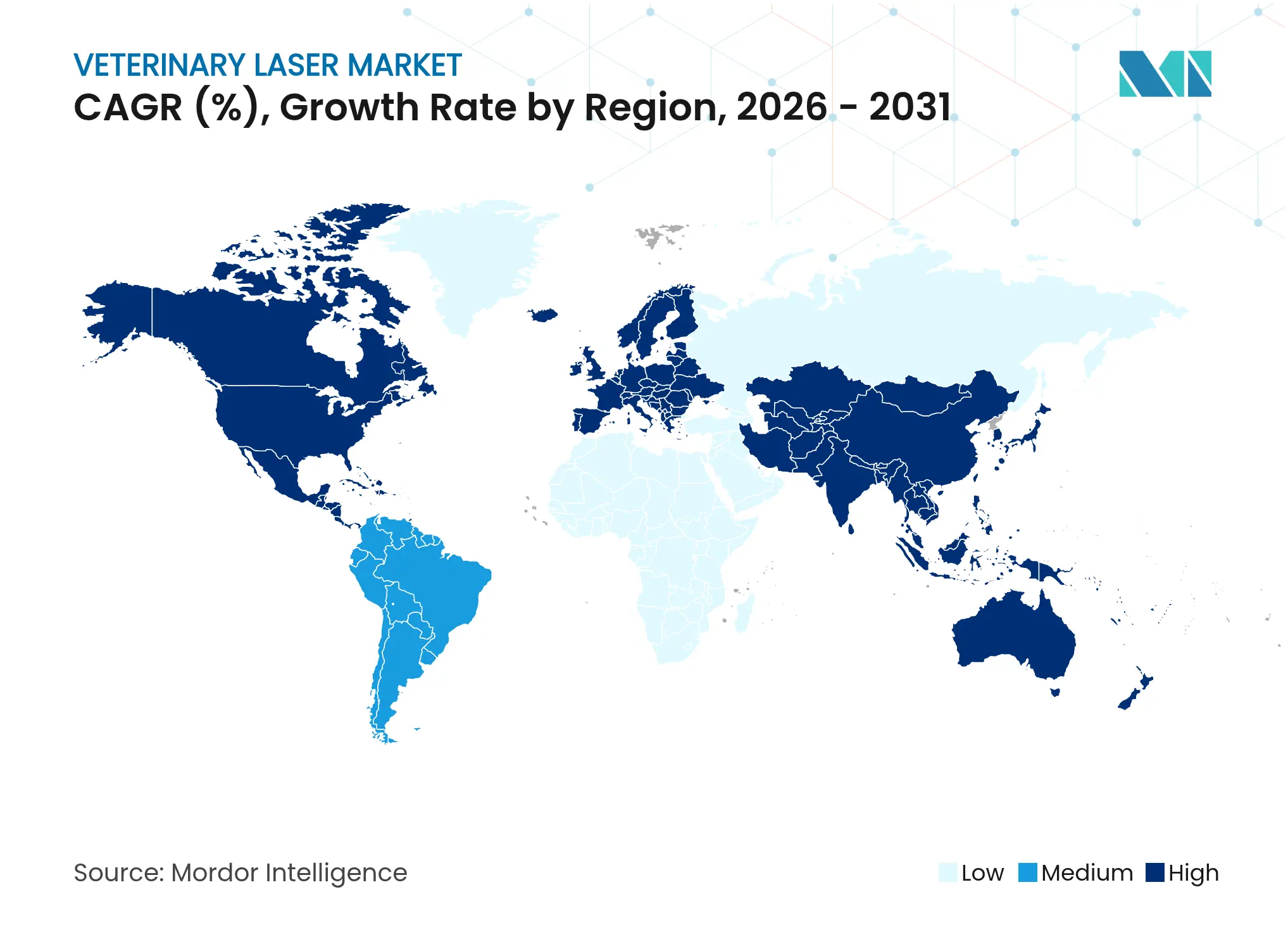

- By Geography, North America dominated with a 42.02% revenue contribution in 2025, while Asia-Pacific is on track to post the highest regional CAGR of 9.01% during the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Veterinary Laser Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rapid adoption of therapeutic lasers in companion-animal

practices

Rapid adoption of therapeutic lasers in companion-animal

practices

| +2.1% | Global, with early gains in North America, Europe | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

+2.1%

|

Geographic Relevance

:

Global, with early gains in North America, Europe

|

Impact Timeline

:

Medium term (2-4 years)

|

Surge in minimally-invasive surgical procedures across

referral centers

Surge in minimally-invasive surgical procedures across

referral centers

| +1.8% | North America & EU, spill-over to APAC core | Short term (≤ 2 years) | |||

Technological leap to portable, high-power

multi-wavelength diode systems

Technological leap to portable, high-power

multi-wavelength diode systems

| +1.5% | Global, with manufacturing concentration in Asia-Pacific | Medium term (2-4 years) | |||

Faster ROI for clinics through bundled laser and service

revenues

Faster ROI for clinics through bundled laser and service

revenues

| +1.3% | North America, expanding to developed APAC markets | Short term (≤ 2 years) | |||

AI-guided dosing & real-time dosimetry modules gaining

FDA-510(k) clearances

AI-guided dosing & real-time dosimetry modules gaining

FDA-510(k) clearances

| +0.9% | US-led, with regulatory influence spreading globally | Long term (≥ 4 years) | |||

Growth of home-use maintenance laser devices with

tele-veterinary oversight

Growth of home-use maintenance laser devices with

tele-veterinary oversight

| +0.8% | North America pilot markets, early APAC adoption | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rapid Adoption of Therapeutic Lasers in Companion-Animal Practices

Therapeutic laser systems now form a standard pain-management modality across a widening base of small-animal clinics. A national survey shows 53% of U.S. veterinarians have purchased therapy lasers and half of those owners deploy the devices in more than 10 weekly cases. The FDA classifies most veterinary therapy lasers under Product Code RGB, exempting them from Good Manufacturing Practice and shortening the commercialization pathway [2]Center for Devices and Radiological Health, “Laser Notices 34 and 35,” fda.gov . Average treatment fees between USD 15 and USD 90 per session, coupled with equipment costs commonly ranging USD 30,000-40,000, put the payback window at approximately 18 months for clinics with moderate caseloads. Class IV diode models, favored for deeper penetration and shorter session times, underpin the therapeutic laser segment’s 48.49% lead in the veterinary laser market.

Surge in Minimally-Invasive Surgical Procedures Across Referral Centers

Specialty and referral hospitals are turning to surgical lasers for controlled tissue ablation, hemostasis, and vaporization that produce less collateral damage than electrocautery. FDA 510(k) clearances in 2024 and 2025 approved dual-wavelength platforms operating at 980 nm and 1470 nm with outputs up to 30 W, expanding the indications list to dermatology, urology, and soft-tissue oncology. Intra-operative reports cite reduced bleeding, sharper margins, and shorter anesthesia times, all of which translate into quicker discharge and higher client satisfaction. As referral networks proliferate, the surgical segment’s 9.12% CAGR is expected to outpace overall veterinary laser market growth.

Technological Leap to Portable, High-Power Multi-Wavelength Diode Systems

Advances in semiconductor engineering have produced handheld devices that combine 660 nm, 800 nm, 905 nm, and 970 nm emitters in units weighing under 5 kg. The MR5 ACTIVet PRO 2.0, for example, delivers 50 W peak power yet relies on rechargeable batteries for field deployment. Integrated surface-emitting laser diodes extend mean time between failures beyond 30,000 hours, cutting lifecycle costs. Context-aware software auto-selects pulse patterns by species and pathology, while Bluetooth logs every joule delivered for cloud-based recordkeeping. Mobility is especially relevant to equine and farm-animal therapy, where treating a 570 kg sport horse in the stable rather than a clinic shortens downtime.

Faster ROI for Clinics Through Bundled Laser and Service Revenues

Vendors increasingly lease laser platforms together with clinical training, marketing collateral, and 24-hour technical support. In the United States, more than 750 clinics participate in such programs offered by equipment distributors who guarantee utilization targets and refresher courses. The bundled approach mitigates the capital hurdle while raising throughput, because technicians quickly master standardized settings and can counsel clients on package pricing. With ancillary revenue from consumables and follow-up assessments, solo practices match hospital-network performance, helping the independent segment capture the forecast-leading 9.14% CAGR.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Capital cost & lack of reimbursement for elective

laser treatments

Capital cost & lack of reimbursement for elective

laser treatments

| -1.4% | Global, particularly acute in emerging markets | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

-1.4%

|

Geographic Relevance

:

Global, particularly acute in emerging markets

|

Impact Timeline

:

Medium term (2-4 years)

|

Shortage of certified laser-therapy technicians in rural

areas

Shortage of certified laser-therapy technicians in rural

areas

| -0.8% | Rural regions globally, especially North America and Australia | Long term (≥ 4 years) | |||

Patchwork laser-class regulations causing import delays

and added testing

Patchwork laser-class regulations causing import delays

and added testing

| -0.6% | Global, with particular impact on Asia-Pacific imports | Short term (≤ 2 years) | |||

Skepticism among insurers on long-term photobiomodulation

efficacy data

Skepticism among insurers on long-term photobiomodulation

efficacy data

| -0.4% | North America & EU, expanding to developed APAC markets | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Capital Cost and Lack of Reimbursement for Elective Laser Treatments

Class IV therapy units priced from USD 12,500 to USD 34,999 and surgical systems above USD 40,000 remain a budget hurdle for many small practices. Whereas human orthopedics insurers reimburse laser sessions in some states, pet insurance policies seldom cover elective photobiomodulation. Owners therefore shoulder the costs of multi-session plans, limiting volume in price-sensitive regions. Financing options, including operating leases and revenue-share agreements, partly offset the capex barrier, yet penetration in emerging markets still lags the veterinary laser market uptake seen in North America.

Shortage of Certified Laser-Therapy Technicians in Rural Areas

Proper dosing calls for formal coursework in laser physics, optics safety, and species-specific parameters, but technician availability remains thin outside metro areas. Rural mixed-animal practices in North America struggle to recruit certified staff amid broader veterinary labor shortages. FDA Laser Notices 34 and 35 emphasize user training and labeling, leaving practices vulnerable to regulatory scrutiny when competency gaps exist [3]Center for Devices and Radiological Health, “CDRH Proposed Guidances for FY2025,” fda.gov . Cloud-based training modules and simplified graphical interfaces reduce the learning curve, but long-term talent pipeline constraints still cap expansion into underserved locales.

Segment Analysis

By Product Type: Surgical Precision Drives Innovation

Therapeutic devices dominated 48.84% of the veterinary laser market in 2025, anchored by Class IV systems operating around 980 nm at up to 40 W. Clinics rely on these platforms for arthritis pain, cruciate repair recovery, and chronic dermatitis. In contrast, surgical lasers will post the segment-leading 8.95% CAGR through 2031, fueled by dual-wavelength systems that incise, coagulate, and vaporize with millimeter-level accuracy. Recent clearances for 1470 nm-enabled units empower soft-tissue oncology and ENT procedures where water absorption is critical. Because combined therapy-and-surgery workstations streamline floor space and cross-train staff, integrated platforms are expected to gain share in multi-doctor hospitals.

A surge in portable high-power units further tilts adoption toward surgery. Where older CO₂ cabinets required dedicated suites, new diode rigs wheel between exam rooms or accompany mobile equine vets. These designs employ active cooling, redundant interlocks, and touch-screen presets that comply with IEC 60825-1, easing credentialing. With disposables limited to sterile fiber tips, procedural cost per case falls, nudging more specialists to adopt laser incision over electrocautery or scalpel.

Note: Segment shares of all individual segments available upon report purchase

By Animal Type: Feline Segment Accelerates

Dogs represented a 41.96% slice of the veterinary laser market size in 2025, reflecting mature protocols for hip dysplasia, IVDD, and post-operative care. Breed-specific presets—5 W continuous-wave for Chihuahua cruciate rehab, 15 W pulsed for Labrador spondylosis—let clinicians optimize outcomes without manual recalculation. Cats, however, will deliver a 8.86% CAGR as owner willingness to invest rises with the growing indoor-only feline population. New dosing tables account for differences in skin thickness and melanin content, reducing the overheating risk once blamed for variable results in cats.

Exotics and avian species form the “Others” bracket and present steady single-digit growth. Therapists increasingly use 660 nm, 100 mW settings to stimulate keratin recovery in feather-plucking parrots, or 905 nm, 0.5 W pulses on rabbit pododermatitis. Multi-wavelength devices let practitioners switch on the fly, broadening the case mix without purchasing niche hardware.

By Application: Regenerative Medicine Expansion

Pain and inflammation management owned 41.67% of revenue in 2025 because every orthopedic and dental case generates a candidate protocol. The anti-nociceptive and anti-inflammatory pathways triggered at 800-960 nm, from reduced prostaglandin synthesis to modulated bradykinin reception, enjoy robust literature support. Regeneration and tissue repair is forecast to outpace at 8.91% CAGR, propelled by studies showing enhanced collagen cross-linking and angiogenesis at fluences near 10 J/cm². Clinicians now couple laser therapy with platelet-rich plasma or stem-cell injections to bridge tendon ruptures in sport horses, creating a premium bundled service.

Dermatology, ophthalmology, and acupuncture form an emerging triad inside the “Others” bucket. Shallow-penetrating 660 nm beams target superficial mast-cell tumors, while 970 nm penetrates joint capsules for osteochondrosis in foals. As peer-reviewed evidence mounts, these sub-segments are likely to make incremental contributions to the broader veterinary laser market.

Note: Segment shares of all individual segments available upon report purchase

By End User: Independent Clinic Growth

Veterinary hospitals held 52.92% of the veterinary laser market share in 2025, buoyed by capital budgets and training departments that scale multi-unit deployment. Networks establish laser centers of excellence that standardize protocols from neuter pain blocks to oncologic resections, lifting utilization and revenue. Independent clinics, many with one or two full-time doctors, are forecast to grow 8.96% annually because distributors now bundle financing, onboarding, and marketing. Tablet-based user interfaces walk staff through anatomy-guided dosing, letting general practitioners achieve outcomes once limited to specialty centers.

Specialty and referral facilities lead surgical adoption for oncology, ophthalmology, and minimally invasive ENT. Therapists capture imaging data pre- and post-laser to quantify functional gains, which helps win client buy-in and differentiate services. Mobile units—veterinary trucks or equine ambulatory practices—complete the end-user landscape, using 18 V battery packs to deliver barn-side care and broaden geographic reach.

Geography Analysis

North America commanded 42.02% of global revenue in 2025 thanks to mature companion-animal health spending patterns and clear regulatory pathways. In the United States, 53% of surveyed veterinarians had installed therapy lasers, with an average weekly usage exceeding 10 sessions. Canada complements with robust equine demand, while Mexico’s urban centers show rising adoption as small-animal ownership climbs. The regional environment benefits from FDA 510(k) transparency and professional continuing-education requirements that encourage evidence-based practice.

Asia-Pacific is on track for the fastest 9.01% CAGR, propelled by surging pet ownership in China, expanding veterinary university programs, and local manufacturing. China’s pet medical market grew to ¥42.81 billion in 2022, and laser imports benefit from that momentum. Domestic players such as Hebei Zhemai secured U.S. clearances, validating export ambitions. Japan’s aging pet population and high insurance penetration foster premium care adoption, while South Korea and India present emerging urban niches where portable units offset clinic space constraints.

Europe posts moderate growth anchored by Germany, France, and the United Kingdom, all of which enforce CE Mark safety standards that align with IEC 60825-1. Scandinavian countries excel in equine sports medicine, using trailer-mounted lasers at competition grounds, whereas Mediterranean markets focus on small-animal dermatology under warm-weather parasite pressures. Eastern Europe represents white-space opportunity; as GDP per capita rises, clinics move from basic modalities toward laser-assisted surgery.

Competitive Landscape

Market Concentration

The veterinary laser market remains moderately concentrated. LiteCure, absorbed into Enovis in 2020, leverages its Companion and Pegasus lines, clinical research library, and global distribution to hold the leading share. K-Laser’s CUBE family differentiates with 20 W, multi-wavelength diode stacks and built-in fluoroscopic targeting, pushing deeper tissue power while maintaining Class IV safety margins. Multi Radiance Medical emphasizes portability with the MR5 ACTIVet PRO 2.0, which packs 50 W peak output into a 1.5 kg handheld.

Asian entrants—including Hebei Zhemai and Wuhan Dimed—use cost-efficient manufacturing to undersell incumbents by up to 20% while still meeting U.S. regulatory criteria. Competitive dynamics now hinge less on wattage alone and more on AI-enabled dosing, cloud-connected treatment logs, and subscription-based training portals. Distributors such as Patterson Animal Health widen their portfolios through acquisitions, creating purchasing groups that negotiate volume pricing and standardize clinic protocols. As a result, software ecosystems, service contracts, and data analytics increasingly determine brand loyalty.

Veterinary Laser Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Patterson Companies’ Animal Health division acquired Infusion Concepts Ltd. in the U.K. and Mountain Vet Supply assets in four U.S. states, giving its dealer network broader reach into practices likely to adopt laser technology

- September 2024: Wuhan Dimed Laser Technology earned FDA 510(k) clearance K252063 for dual-wavelength surgical diode systems up to 30 W, broadening the modality’s regulatory foothold in the United States

- May 2024: Leonard Green & Partners finalized its purchase of MedVet Associates, a referral-hospital chain that standardizes capital equipment across locations, including high-end laser suites

Table of Contents for Veterinary Laser Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rapid adoption of therapeutic lasers in companion-animal practices

- 4.2.2Surge in minimally-invasive surgical procedures across referral centers

- 4.2.3Technological leap to portable, high-power multi-wavelength diode systems

- 4.2.4Faster ROI for clinics through bundled laser and service revenues

- 4.2.5AI-guided dosing & real-time dosimetry modules gaining FDA-510(k) clearances

- 4.2.6Growth of home-use maintenance laser devices with tele-veterinary oversight

- 4.3Market Restraints

- 4.3.1Capital cost & lack of reimbursement for elective laser treatments

- 4.3.2Shortage of certified laser-therapy technicians in rural areas

- 4.3.3Patchwork laser-class regulations causing import delays and added testing

- 4.3.4Skepticism among insurers on long-term photobiomodulation efficacy data

- 4.4Regulatory Landscape

- 4.5Technological Outlook

- 4.6Porter’s Five Forces Analysis

- 4.6.1Threat of New Entrants

- 4.6.2Bargaining Power of Buyers

- 4.6.3Bargaining Power of Suppliers

- 4.6.4Threat of Substitutes

- 4.6.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Product Type

- 5.1.1Therapeutic Lasers

- 5.1.2Surgical Lasers

- 5.1.3Combined Therapy and Surgery Platforms

- 5.2By Animal Type

- 5.2.1Dogs

- 5.2.2Cats

- 5.2.3Others

- 5.3By Application

- 5.3.1Pain and Inflammation Management

- 5.3.2Regeneration and Tissue Repair

- 5.3.3Others

- 5.4By End User

- 5.4.1Veterinary Hospitals

- 5.4.2Specialty & Referral Centers

- 5.4.3Independent Clinics

- 5.4.4Others

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4Australia

- 5.5.3.5South Korea

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East and Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Cutting Edge Laser Technologies

- 6.3.2Companion Animal Health (LiteCure)

- 6.3.3Aesculight

- 6.3.4Biolase Inc.

- 6.3.5K-Laser LLC

- 6.3.6SpectraVET Inc.

- 6.3.7Aspen Laser Systems

- 6.3.8Erchonia Corporation

- 6.3.9Respond Systems

- 6.3.10Excel Lasers Ltd.

- 6.3.11Multi Radiance Medical

- 6.3.12THOR Photomedicine

- 6.3.13Diowave Laser Systems

- 6.3.14Dimed Laser

- 6.3.15GIGAALASER

- 6.3.16ServiceVet (J-Ray)

- 6.3.17IMV Imaging (BCF Technology)

- 6.3.18Changchun New Industries (CNI) Laser

- 6.3.19Laserex Technologies

- 6.3.20Omniray Medical

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Veterinary Laser Market Report Scope

As per the scope of the report, veterinary laser therapy is the process of treating an animal with the use of focused light. Unlike most light sources, the light from a laser is tuned to specific wavelengths. The veterinary laser market is segmented by product type (therapeutic lasers and surgery lasers), animal type (dogs, cats, and others), application (pain and inflammation management, regeneration or tissue repair, and others), laser type (class 2, class 3, and class 4), and geography (North America, Europe, Asia-Pacific, the Middle East and Africa, and South America). The report offers the value (in USD million) for the above segments.