Veterinary Oncology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

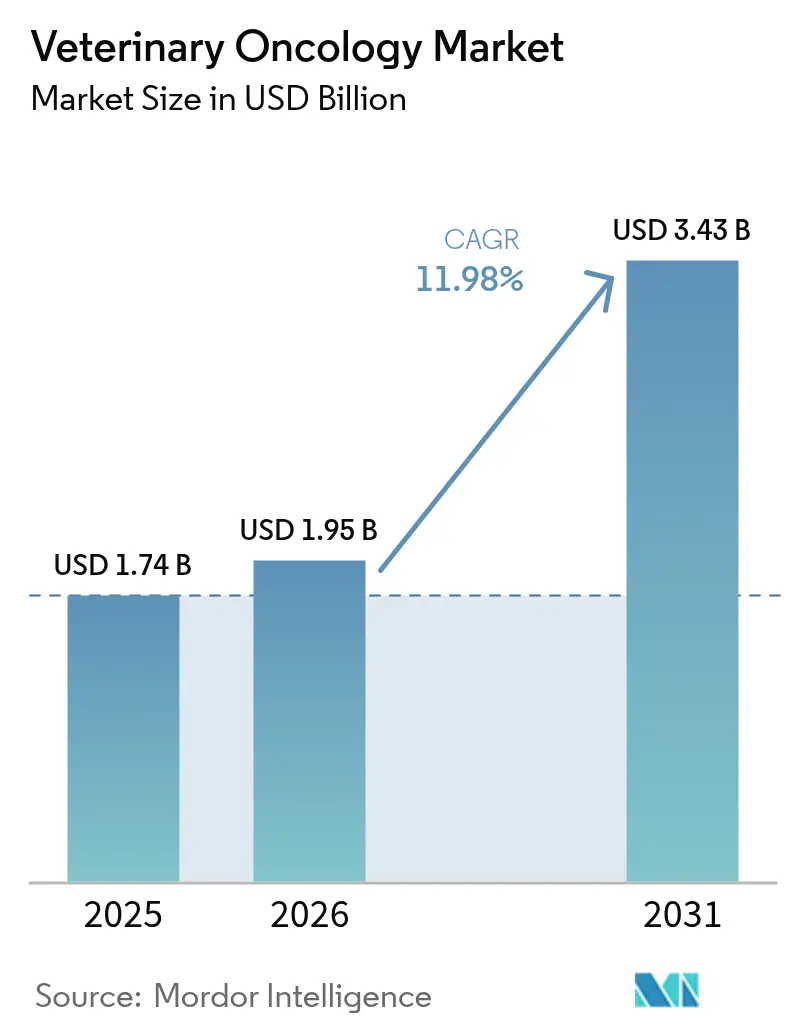

| Market Size (2026) | USD 1.95 Billion |

| Market Size (2031) | USD 3.43 Billion |

| Growth Rate (2026 - 2031) | 11.98% CAGR |

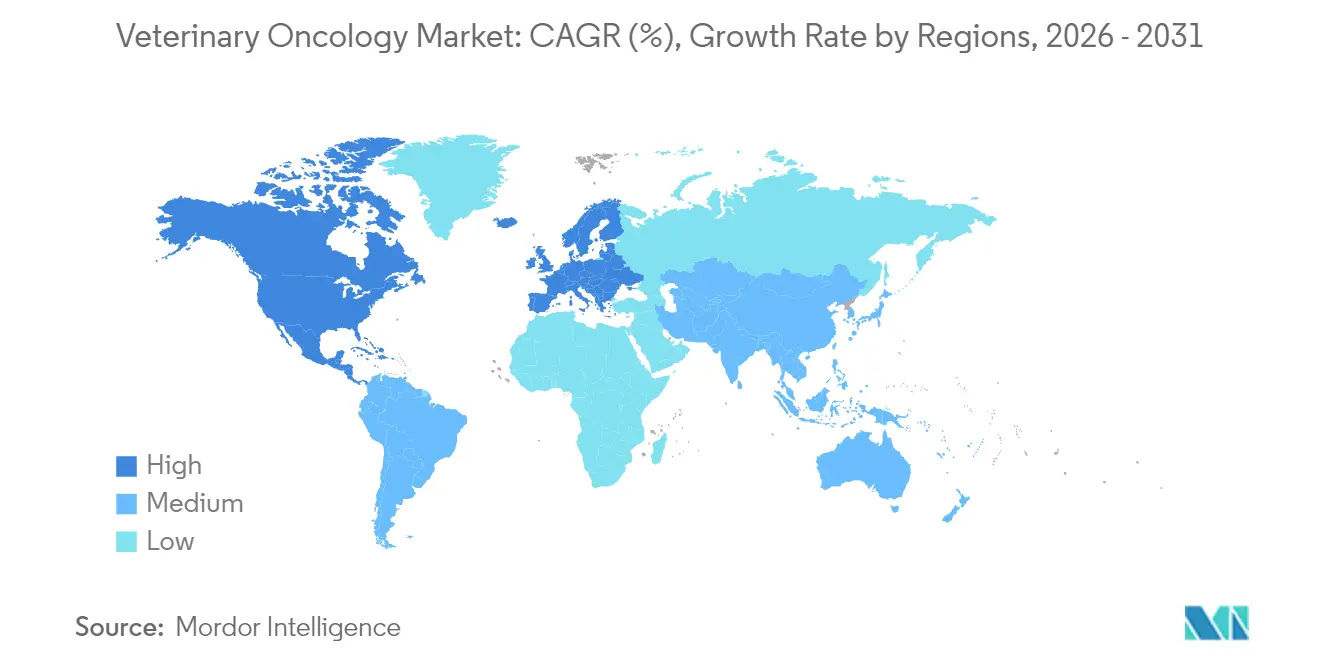

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veterinary Oncology Market Analysis by Mordor Intelligence

Veterinary oncology market size in 2026 is estimated at USD 1.95 billion, growing from 2025 value of USD 1.74 billion with 2031 projections showing USD 3.43 billion, growing at 11.98% CAGR over 2026-2031. Momentum builds as aging pets experience higher cancer incidence, owners embrace “pet-as-family” mind-sets, and insurers broaden coverage for sophisticated procedures. Earlier diagnosis through liquid biopsies and AI-assisted imaging shifts care from palliative to curative, lifting demand for precision medicine. Regulatory fast-track pathways shorten launch cycles, while multimodal protocols that combine surgery, radiation, and immunotherapy deliver measurable survival gains. Against this backdrop, competition intensifies as multinational drugmakers and specialty clinics race to embed data analytics and digital health tools across the care continuum.

Key Report Takeaways

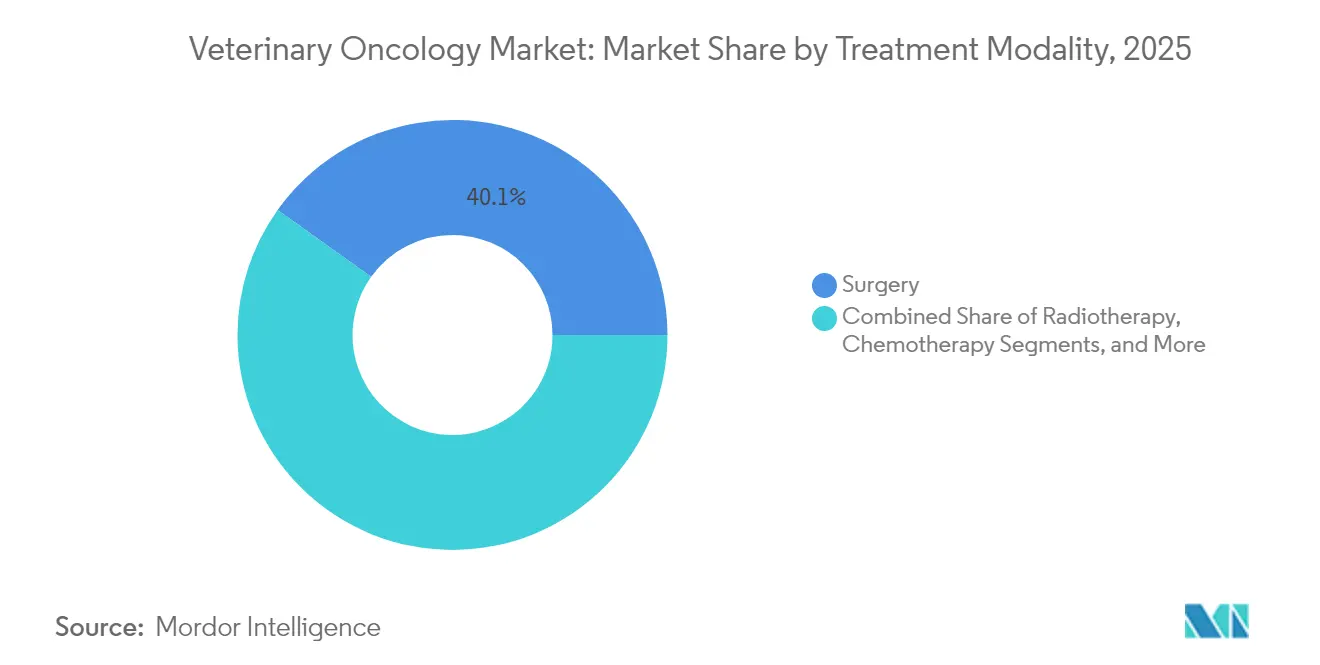

- By treatment modality, surgery led with 40.12% revenue share in 2025; immunotherapy is projected to expand at a 13.04% CAGR through 2031.

- By animal type, canine patients held 85.88% of the veterinary oncology market share in 2025, while feline cases are advancing at a 12.74% CAGR to 2031.

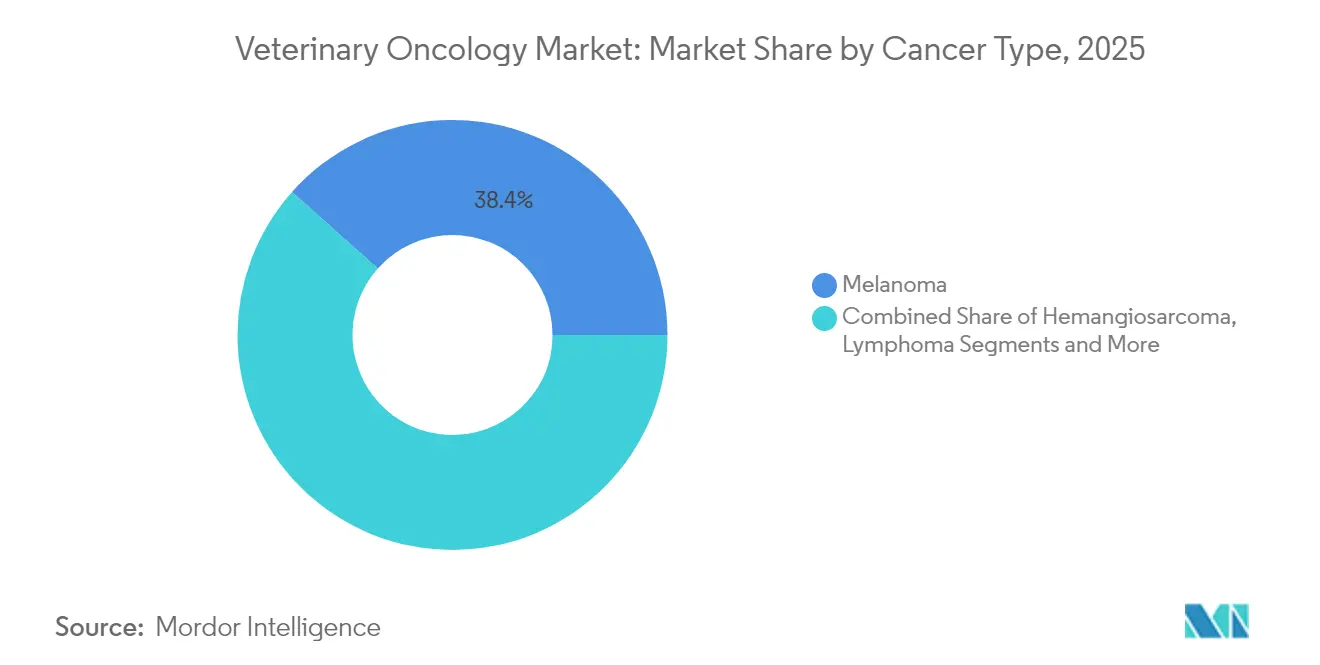

- By cancer type, melanoma accounted for 38.41% of the veterinary oncology market size in 2025; lymphoma treatments are forecast to grow at a 12.81% CAGR.

- By geography, North America captured 53.76% of 2025 revenues; Asia-Pacific is set to post the fastest 13.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Veterinary Oncology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of companion-animal cancers | +3.2% | Global, with highest impact in North America and Europe | Long term (≥ 4 years) |

| Increasing corporate & academic R&D funding in veterinary oncology | +2.8% | North America & EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Rapid adoption of advanced imaging & liquid-biopsy diagnostics | +2.1% | Global, led by developed markets | Short term (≤ 2 years) |

| Growth of pet-insurance policies covering oncology care | +1.9% | North America & EU core, emerging in Asia-Pacific | Medium term (2-4 years) |

| AI-assisted early-screening platforms entering clinical use | +1.5% | Global, with early adoption in North America | Short term (≤ 2 years) |

| Focused-ultrasound & photodynamic therapies expanding treatment toolbox | +0.5% | North America & EU, limited Asia-Pacific penetration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Companion-Animal Cancers

Nearly half of dogs over 10 years develop a neoplasm, a rate that keeps demand elevated for oncology services as preventive medicine lengthens life expectancy. Breed predispositions sharpen this need, with Golden Retrievers and Boxers exhibiting above-average lymphoma incidence. Earlier diagnosis now directs more cases into curative pathways, fuelling uptake of surgery, radiation, and emerging immunotherapies. Owners’ growing willingness to pursue aggressive protocols reinforces long-run service intensity, especially in markets with mature insurance penetration.

Increasing Corporate & Academic R&D Funding in Veterinary Oncology

Pharmaceutical firms cite translational value between companion-animal tumors and human oncology, prompting expansion of dedicated biologics capacity. Elanco’s USD 130 million Kansas facility emphasizes monoclonal antibody output for canine cancers. Universities add momentum; Virginia Tech’s histotripsy studies seek non-invasive osteosarcoma solutions. Non-profits such as Morris Animal Foundation channel grants toward limb-sparing immunotherapies, accelerating clinical timelines and broadening protocol sophistication.

Rapid Adoption of Advanced Imaging & Liquid-Biopsy Diagnostics

IDEXX introduced a USD 15 liquid-biopsy screen that flags canine lymphoma at the point of care, lowering barriers to annual testing [1]Zoetis Inc., “Vetscan Imagyst Expands AI Menu,” zoetis.com. Zoetis’ AI cytology platform shortens slide-to-answer times to minutes, allowing general practitioners to identify neoplastic cells without referral delays [2]IDEXX Laboratories Inc., “IDEXX Cancer Dx Launch Announcement,” idexx.com. Dedicated veterinary PET scanners now track metabolic tumor activity, enabling more tailored radiation dosing. Earlier intervention improves survival odds and shifts spending toward curative stages of the care journey.

AI-Assisted Early-Screening Platforms Entering Clinical Use

Machine-learning models trained on millions of pathology images now exceed pathologist sensitivity for select cancers. Zoetis’ Vetscan Imagyst integrates blood-smear and urine-sediment analytics, providing a near-real-time triage tool that expands specialty-grade diagnostics into general clinics. The technology’s accessibility is especially beneficial in rural settings where boarded oncologists are scarce, supporting more equitable access to advanced care.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High out-of-pocket costs for owners despite insurance gaps | -2.1% | Global, most severe in developing markets | Medium term (2-4 years) |

| Low disease awareness in developing pet-owner populations | -1.8% | Asia-Pacific, Latin America, Middle East & Africa | Long term (≥ 4 years) |

| Geographic scarcity of radiotherapy & advanced care centers | -1.3% | Rural areas globally, severe in developing regions | Long term (≥ 4 years) |

| Absence of harmonised clinical-trial endpoints delaying approvals | -0.9% | Global, particularly affecting EU-US regulatory alignment | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Out-of-Pocket Costs for Owners Despite Insurance Gaps

Comprehensive protocols can range from USD 10,000 to USD 30,000, often exceeding insurance caps and forcing difficult affordability decisions. Coverage exclusions for pre-existing conditions leave policyholders responsible for a large share of expenses. As immunotherapies and precision treatments enter the market at premium price points, the cost disparity between basic and advanced care widens, tempering uptake among middle-income households.

Geographic Scarcity of Radiotherapy & Advanced Care Centers

The Veterinary Cancer Society counts fewer than 100 veterinary radiotherapy units across the United States, leaving vast rural corridors underserved [3]Veterinary Cancer Society, “Radiation Facility Directory,” vetcancersociety.org. Travel distance inflates indirect costs and reduces treatment adherence. Emerging economies contend with even narrower infrastructure, limiting advanced modality penetration. Tele-oncology consults, mobile linear accelerators, and focused ultrasound platforms are beginning to ease these structural bottlenecks, but the build-out remains a multi-year endeavor.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Modality: Surgery Anchors Market While Immunotherapy Surges

Surgery secured 40.12% of global 2025 revenues, underscoring its role as a frontline curative option for solid tumors within the veterinary oncology market. Advances in intraoperative imaging and minimally invasive techniques enhance margin control while reducing recovery times. Concurrently, immunotherapy’s 13.04% CAGR reflects successful commercial launches of autologous cellular vaccines and small-molecule immune modulators that complement existing standards of care. Radiotherapy continues to grow as stereotactic protocols cut total fractions from 18 to three, shrinking owner travel commitments. Chemotherapy retains value for systemic malignancies, though genetic profiling refines dosing to minimize toxicity.

The therapeutic toolbox is moving toward truly multimodal regimens that marry surgical debulking with adjuvant radiation and checkpoint inhibitor courses. Focused ultrasound and photodynamic approaches add minimally invasive options for deep-seated or anatomically delicate lesions and are gaining traction as costs fall. AI-guided treatment planning leverages tumor genomics and imaging data to match patients with high-response regimens, improving outcomes and supporting evidence-based reimbursement.

By Animal Type: Canine Dominance Persists as Feline Protocols Mature

Dogs accounted for 85.88% of 2025 revenue, cementing their dominant role in the veterinary oncology market. Higher disease prevalence and more robust clinical evidence accelerate canine protocol adoption. Targeted therapies now segment recommendations by breed genetics, addressing elevated lymphoma risk in Boxers and osteosarcoma in Rottweilers. Cats, while historically underserved, are on a 12.74% CAGR as formulators develop feline-optimized chemotherapies that account for unique metabolic pathways. Equine oncology remains niche yet lucrative, driven by melanoma and sarcoid therapies for performance animals where career extension underpins owner willingness to pay.

Owner attitudes shift toward parity of care across species, pushing innovators to tailor pharmacokinetics, tablets, and dosing devices for smaller patients. Companion exotics such as ferrets and rabbits prompt exploratory trials into mini-dose immunotherapies, indicating longer-term addressable upside beyond core canine and feline cohorts. As species-specific evidence bases expand, clinicians gain confidence to recommend aggressive interventions, propelling further segment diversification.

By Cancer Type: Melanoma Leads While Lymphoma Innovation Accelerates

Melanoma retained the biggest slice at 38.41% in 2025, supported by established vaccines and predictable surgical outcomes. The segment benefits from relatively clear staging and localized disease progression, supporting early surgical resolution complemented by therapeutic vaccination when needed. Lymphoma now represents the fastest riser, advancing at a 12.81% CAGR on the back of oral therapies such as verdinexor and conditional approvals for canine-specific small molecules. Mast-cell tumors remain significant as injectable tigilanol tiglate allows non-surgical ablation of select lesions, broadening options for patients unsuited to anesthesia.

Precision oncology lifts hemangiosarcoma care, with genomic profiling guiding VEGF inhibitors that extend progression-free intervals. Osteosarcoma research prioritizes limb-sparing immunotherapy that combines autologous dendritic cells with intra-tumoral cytokine injections, reflecting owner priorities around mobility and quality of life. The upshot is deeper molecular stratification that aligns treatment choice with tumor biology, a hallmark of human oncology now migrating into companion-animal practice.

Geography Analysis

North America commanded 53.76% of 2025 sales, underpinned by high companion-animal spend, dense specialist networks, and a regulatory framework that allows conditional product approvals to reach clinics quickly. The United States hosts the largest pool of boarded veterinary oncologists, and its insurers increasingly reimburse advanced modalities, shortening payback periods for clinic investments in linear accelerators and CT scanners. University-industry collaborations funnel breakthrough science into commercial pipelines, further entrenching regional leadership.

Asia-Pacific stands out as the fastest-growing territory, charting a 13.62% CAGR to 2031 as pet humanization scales across China’s urban centers. Disposable income growth intersects with expanding private-clinic networks and rising awareness of pet insurance, narrowing care-access gaps. Japan’s mature small-animal market drives early adoption of precision biologics, while Australia’s research community pilots AI decision-support tools that gain regional traction. Hao-Animal, a Chinese start-up, recently opened Shanghai’s first integrated oncology-imaging hub, signaling domestic capacity build-up.

Europe holds the second-largest share, buoyed by stringent animal welfare statutes that encourage proactive oncology care. Harmonized EMA procedures streamline continental drug launches, though divergent reimbursement policies create pricing complexity. Germany’s robust veterinary R&D ecosystem pioneers isotope-guided surgery, and the UK accelerates clinical trials under dedicated veterinary-specific regulatory guidance. France and the Nordics prioritize minimally invasive therapies, reflecting cultural emphasis on quality-of-life metrics.

Competitive Landscape

The veterinary oncology market features moderate consolidation. Zoetis maintains scale advantages through an end-to-end platform that bundles diagnostics, pharmaceuticals, and AI analytics. Elanco doubles down on biologics manufacturing, leveraging recent acquisitions to fill pipeline gaps in monoclonal antibodies. Specialist chains such as PetCure Oncology deploy proprietary radiation centers in referral-dense corridors, creating regional treatment hubs. ELIAS Animal Health differentiates with autologous cell-based immunotherapies and leverages academic study networks for evidence generation.

Technological differentiation has overtaken molecule count as the critical battleground. Patent filings increase in micro-RNA diagnostics, nanoparticle drug delivery, and autologous vaccine processes. Mobile treatment units and tele-oncology portals address rural access voids, allowing disruptors to penetrate markets previously resistant to high-end services. Strategic alliances arise as large firms seek AI partners to accelerate workflow automation. M&A potential remains high as top players strive to integrate vertical capabilities and capture white-space geographies.

Veterinary Oncology Industry Leaders

Elanco

Zoetis

Siemens Healthineers (Varian Medical Systems)

Accuray Incorporated

OHC (One Health Company)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Privo Technologies formed BeneVet Oncology to apply its proprietary delivery platforms in companion-animal cancers.

- January 2025: IDEXX launched IDEXX Cancer Dx, the first residual diagnostic panel for early canine lymphoma detection.

- January 2024: ELIAS Animal Health secured a USDA determination that its ECI-OSA-04 pivotal study shows reasonable efficacy, advancing licensure for canine osteosarcoma immunotherapy.

- October 2023: Merck Animal Health released gilvetmab, a canine-directed monoclonal antibody now available to U.S. veterinary oncologists.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the veterinary oncology market as all 2025 revenue earned from surgery, chemotherapy, radiotherapy, and immunotherapy delivered to companion animals, mainly dogs and cats, and the related drugs and disposables billed on the same ticket.

Scope Exclusions: stand-alone diagnostic visits, livestock cancer care, and investigational-trial reimbursements fall outside scope.

Segmentation Overview

- By Treatment Modality

- Radiotherapy

- Surgery

- Chemotherapy

- Immunotherapy

- Other Treatments (Laser, Photodynamic, Focused Ultrasound)

- By Animal Type

- Canine

- Feline

- Equine

- Other Companion Animals (exotics, small mammals)

- By Cancer Type

- Lymphoma

- Mast-Cell Tumour

- Mammary & Squamous-Cell Carcinoma

- Osteosarcoma

- Hemangiosarcoma

- Melanoma

- Other Cancers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed referral-center heads, oncology nurses, senior clinicians, and distributors across North America, Europe, Asia-Pacific, and Latin America. Their insights aligned price bands, capacity use, and modality mixes that rarely appear in public datasets.

Desk Research

Mordor analysts gathered population, incidence, and spend indicators from open sources such as the American Veterinary Medical Association, European Pet Food Industry Federation, national pet-insurance yearbooks, customs logs tracking antineoplastic imports, and peer-reviewed journals like the Journal of Veterinary Internal Medicine. Annual reports and respected press articles clarified price corridors and modality uptake trends.

Subscription access to our D&B Hoovers and Dow Jones Factiva vaults verified company revenue splits and flagged material news. The sources named are illustrative; many other references informed screening, cross-checks, and clarification.

Market-Sizing & Forecasting

A top-down prevalence-to-treated-cohort build sets the 2025 baseline, while a sampled clinic roll-up cross-checks totals. Drivers modeled include companion-animal population growth, reported cancer incidence, average course cost, insurance penetration, oncology clinic density, and modality adoption curves. Multivariate regression projects each input to 2030, and scenario analysis frames upside and downside. Regional gaps are filled with weighted averages confirmed during follow-up calls.

Data Validation & Update Cycle

Outputs move through variance tests, peer review, and senior sign-off. Reports refresh every twelve months, with interim updates triggered by major regulatory or clinical events, so clients always receive an up-to-date view.

Why Mordor's Veterinary Oncology Market Baseline Commands Reliability

Published figures often diverge because firms vary service scope, base year, currency treatment, and refresh speed.

By holding a therapy-only scope, locking 2025 exchange rates, and updating annually, we provide a dependable anchor. Key gap drivers include whether diagnostics and equine spend are bundled and how fast immunotherapy prices erode, while several publishers still rely on 2019 utilization surveys that our latest interviews have already superseded.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.74 B (2025) | Mordor Intelligence | - |

| USD 1.57 B (2024) | Global Consultancy A | Excludes radiotherapy add-ons, assumes slower insurance uptake |

| USD 1.62 B (2024) | Industry Association B | Bundles diagnostics with disposables, uses older prevalence data |

| USD 0.91 B (2024) | Regional Consultancy C | Counts only canine cases, limits therapies to chemotherapy |

These contrasts show that Mordor's disciplined scope, carefully chosen drivers, and regular refresh rhythm give decision-makers a balanced baseline traceable to clear inputs.

Key Questions Answered in the Report

What is the current Veterinary Oncology Market size?

The market stands at USD 1.95 billion in 2026 and is projected to reach USD 3.43 billion by 2031.

Who are the key players in Veterinary Oncology Market?

Elanco, Zoetis, Siemens Healthineers (Varian Medical Systems), Accuray Incorporated and OHC (One Health Company) are the major companies operating in the Veterinary Oncology Market.

Which is the fastest growing region in Veterinary Oncology Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which treatment modality generates the highest revenue?

Surgery leads with 40.12% of 2025 global revenue, reflecting its central role for solid tumors.

Why is immunotherapy growing so quickly?

Breakthrough cellular vaccines and targeted immune modulators deliver higher response rates, driving a 13.04% forecast CAGR for immunotherapy through 2031.

Page last updated on: