Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

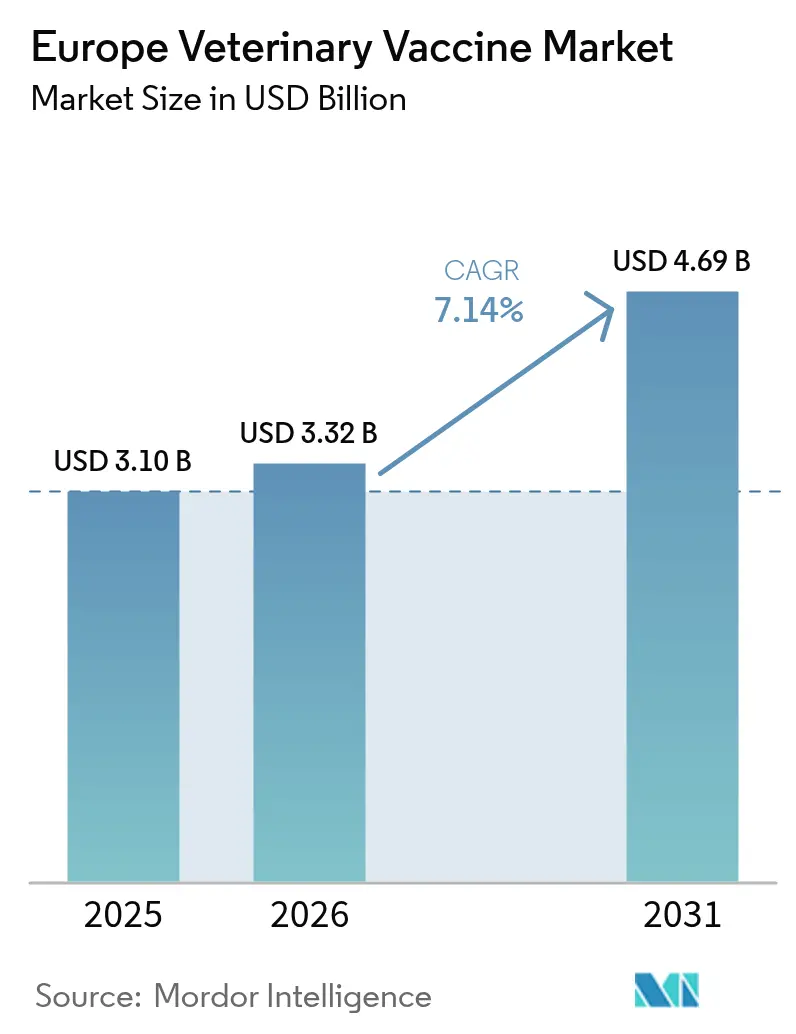

| Base Year Market Size (2025) | USD 3.10 Billion |

| Market Size (2026) | USD 3.32 Billion |

| Market Size (2031) | USD 4.69 Billion |

| Growth Rate (2026 - 2031) | 7.14% CAGR |

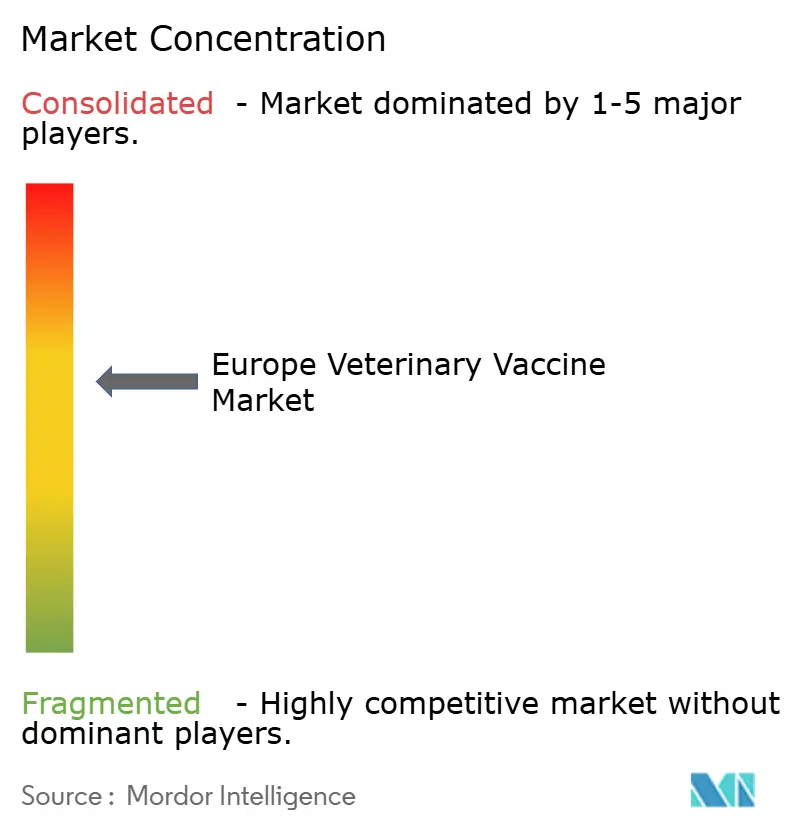

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Veterinary Vaccine Market Analysis by Mordor Intelligence

The Europe Veterinary Vaccine Market size was valued at USD 3.10 billion in 2025 and estimated to grow from USD 3.32 billion in 2026 to reach USD 4.69 billion by 2031, at a CAGR of 7.14% during the forecast period (2026-2031).

Strong veterinary‐health infrastructure, mandatory immunization policies and fast‐tracking of next-generation biologics underpin steady expansion. The region’s stringent surveillance programs following recent foot-and-mouth and Bluetongue outbreaks compel livestock producers to vaccinate in line with Single Market trade requirements, ensuring the veterinary vaccines market retains a resilient demand base. Growth momentum is further reinforced by rising pet insurance uptake, which makes preventive care affordable for urban pet owners and lifts premium vaccine sales. Investment in mRNA, DNA and recombinant platforms accelerates as regulators adopt adaptive-pathway reviews that shorten time-to-market for antigen updates. Meanwhile, e-commerce channels capitalize on pandemic-era digital adoption to widen access, especially in underserved rural areas.

Key Report Takeaways

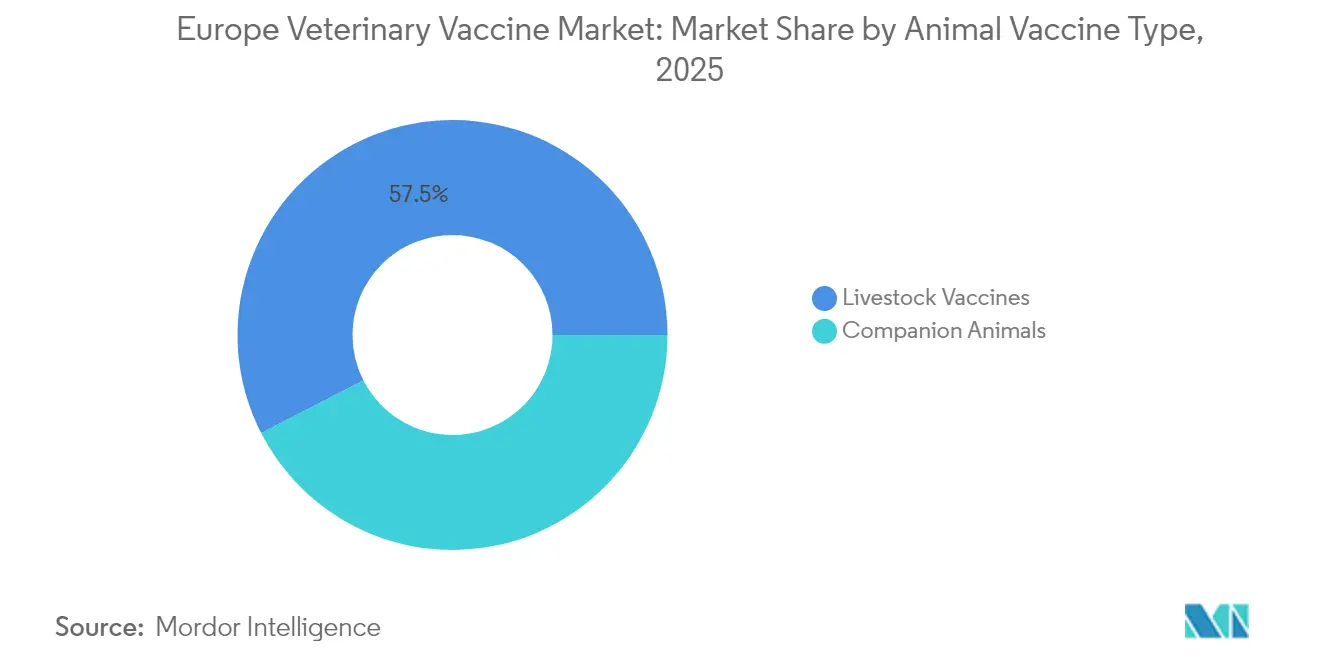

- By animal vaccine type, livestock applications led with 57.54% of European veterinary vaccines market share in 2025, while companion-animal products are projected to expand at a 8.95% CAGR to 2031.

- By vaccine technology, inactivated/killed formulations accounted for 41.92% of the veterinary vaccines market size in 2025, whereas mRNA and DNA platforms are set to advance at a 9.21% CAGR over 2026-2031.

- By disease indication, foot-and-mouth disease vaccines captured 19.62% share of the veterinary vaccines market size in 2025, and avian influenza vaccines show the fastest 9.64% CAGR through 2031.

- By distribution channel, veterinary hospitals and clinics held 53.21% revenue share in 2025; retail and e-commerce are growing at a 10.18% CAGR to 2031.

- By geography, Germany commanded 23.88% of European veterinary vaccines market share in 2025, while Rest of Europe is forecast to log a 10.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Veterinary Vaccine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying EU surveillance & mandatory livestock immunization campaigns | +2.1% | EU-wide, strongest in Germany, France, Netherlands | Medium term (2-4 years) |

| Growing companion-animal vaccine uptake via pet-insurance penetration | +1.8% | Western Europe core, expanding to Eastern markets | Long term (≥ 4 years) |

| Expansion of poultry & aquaculture exports inside the Single Market | +1.5% | France, Netherlands, Denmark with spillover effects | Short term (≤ 2 years) |

| Technological shift toward recombinant & vector platforms | +1.3% | Germany, UK, France leading innovation clusters | Long term (≥ 4 years) |

| mRNA pipeline for rabies & emerging zoonoses (under-the-radar) | +0.9% | EU research hubs, early adoption in Nordic countries | Long term (≥ 4 years) |

| Surge readiness rules for emergency GMO vaccines (under-the-radar) | +0.7% | EU-wide regulatory framework implementation | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intensifying EU Surveillance & Mandatory Livestock Immunization Campaigns

Heightened post-outbreak vigilance has transformed voluntary immunization into compulsory programs across most member states. France budgeted EUR 22 million (USD 24 million) to vaccinate 1 million sheep and 700,000 cattle against Bluetongue in 2024, covering 85% of producer costs. Real-time coverage reporting to the European Food Safety Authority now links public funding to compliance, ensuring uniform uptake across borders. Emergency-preparedness directives mandate pre-positioned stockpiles, creating recurring contracts that anchor the veterinary vaccines market. Lessons from the 2019-2022 African swine fever crisis also pushed regulators to favor recombinant platforms that can be rapidly re-tooled for new serotypes. Overall, compulsory programs institutionalize demand and strategically benefit manufacturers with scalable production lines.

Growing Companion-Animal Vaccine Uptake Via Pet-Insurance Penetration

Vaccination reimbursement mandates embedded in pet-insurance policies raise compliance levels and boost premium adoption. French clinics charge EUR 50-90 (USD 54-97) for canine combination shots and EUR 192 (USD 207) for feline primo-series, up to 80% of which insurers refund. Consolidated veterinary chains introduce standardized care protocols that prioritize annual boosters, while digital health records allow insurers to audit claims and incentivize owners through lower premiums. Nordic markets illustrate the upside: pet insurance exceeds 40% penetration, enabling uptake of combination vaccines that target emerging pathogens. As Eastern European incomes rise, insurers are extending low-tier plans that include core vaccinations, establishing a long runway for the veterinary vaccines market.

Expansion of Poultry & Aquaculture Exports Inside the Single Market

To meet intra-EU trade standards, exporters align with the strictest member-state requirements, effectively harmonizing vaccination protocols upward. France’s 2024 mandate to immunize 32.5 million ducks against highly pathogenic avian influenza at a public cost of EUR 100 million (USD 108 million) set a new compliance benchmark. The European Commission’s emergency-measures framework fast-tracks vaccine rollouts, supporting aquaculture exporters that must demonstrate freedom from marine pathogens. These actions lift baseline demand and create predictable order cycles that manufacturers can forecast, further consolidating the European veterinary vaccines market.

Technological Shift Toward Recombinant & Vector Platforms

Merck Animal Health’s SEQUIVITY platform exemplifies the pivot to RNA particle technologies that allow herd-specific formulations within months. The European Medicines Agency now supports platform-designation filings, letting firms submit streamlined variations instead of full dossiers when swapping antigens. Thermostable vectors also counteract cold-chain gaps in rural clinics, particularly in Eastern Europe. Collectively, these advances shorten release times, bolster supply security and strengthen the innovation reputation of the animal vaccines industry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy EMA batch-release timelines for biologics | -1.2% | EU-wide, particularly affecting smaller manufacturers | Medium term (2-4 years) |

| Cold-chain gaps in Eastern & Rest of Europe veterinary clinics | -0.9% | Eastern Europe, rural areas of Southern Europe | Short term (≤ 2 years) |

| Vaccine hesitancy among small ruminant farmers (under-the-radar) | -0.6% | Mediterranean regions, traditional farming areas | Medium term (2-4 years) |

| Limited DIVA test availability delaying bTB vaccine roll-out (under-the-radar) | -0.4% | UK, Ireland, with EU monitoring implications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lengthy EMA Batch-Release Timelines for Biologics

Official Medicines Control Laboratory testing can delay commercial release by 4-6 weeks, elevating carrying costs and exposing manufacturers to seasonal demand risk. Large multinationals manage by staggering overlapping batches, but smaller firms often cannot finance parallel production, dampening competitive diversity in the veterinary vaccines market. While the centralized system guarantees product safety, stakeholders continue to lobby for risk-based sampling that could shorten release cycles without compromising quality.

Cold-Chain Gaps in Eastern & Rest of Europe Veterinary Clinics

Field audits show 59% of farm refrigerators surpass 8 °C and 53% fall below 2 °C, with extremes hitting 24 °C and -12 °C that destroy potency. Rural practices lack backup power and digital monitoring, eroding farmer confidence when vaccines fail to protect herds. Manufacturers answer with thermostable formulations and education campaigns, but infrastructure investments remain essential. Until then, cold-chain lapses continue to cap uptake potential, especially for high-value biologics that dominate the veterinary vaccines market size.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Animal Vaccine Type: Livestock Dominance Drives Market Foundation

Livestock formulations delivered 57.54% of European veterinary vaccines market share in 2025 as mandatory programs underpinned broad adoption across cattle, swine and poultry sectors. Companion-animal vaccines, however, are forecast to post a 8.95% CAGR on the back of rising pet humanization and insurance penetration, signaling a gradual broadening of the veterinary vaccines market size toward discretionary segments.

Bovine biologics lead livestock demand because of extensive dairy and beef herds in Germany, France and the Netherlands. Poultry vaccines are scaling quickly as integration of value chains and export ambitions call for stringent health certificates. Among pets, canine shots remain the backbone of preventive care, yet feline uptake is accelerating given urban owner preference for cats. Equine products cater to a high-value audience that absorbs premium pricing, adding a profitable niche within the broader veterinary vaccines market.

By Vaccine Technology: Innovation Accelerates Platform Adoption

Inactivated products retained a 41.92% revenue share in 2025 thanks to well-known safety and efficacy profiles, but mRNA and DNA candidates carry a compelling 9.21% CAGR outlook, reflecting regulatory confidence built during the COVID-19 era. This trend deepens the technological diversification of the veterinary vaccines market.

Live-attenuated and sub-unit formulations remain relevant for pathogens requiring robust cellular responses or exceptional safety. Recombinant and vector platforms offer middle-ground advantages in scalability and thermostability, making them attractive where cold-chain gaps persist. EMA platform designations now reduce review times for antigen swaps, prompting firms to invest in modular manufacturing. As a result, platform agility is becoming a decisive competitive lever, influencing long-term growth trajectories in the animal vaccines industry.

By Disease Indication: Emergency Preparedness Reshapes Priorities

Foot-and-mouth disease vaccines commanded 19.62% of veterinary vaccines market share in 2025 because of the pathogen’s severe trade implications; member states stockpile doses as an insurance policy against economic disruption. Avian influenza biologics, driven by France’s landmark duck campaign, exhibit the fastest 9.64% CAGR, mirroring heightened poultry export risk management.

Bovine respiratory vaccines persistently sell into high-density feedlots, while porcine circovirus inputs rise alongside professionalization of swine farms. Rabies shots bridge companion-animal and wildlife programs, and DIVA-compatible tuberculosis vaccines for cattle advance through late-stage trials. Climate change introduces novel vector-borne challenges, pushing R&D pipelines toward multiplexed antigens that can address shifting pathogen landscapes and secure the veterinary vaccines market against future shocks.

By Distribution Channel: Digital Transformation Accelerates Access

Veterinary hospitals and clinics anchored 53.21% of 2025 sales, leveraging professional oversight and prescription control to maintain primacy within the veterinary vaccines market. E-commerce and retail outlets, however, are growing at 10.18% CAGR as logistics providers master temperature-controlled last-mile delivery.

Government procurement dominates during emergency livestock campaigns, creating bulk purchase spikes that concentrate demand in short windows. Clinics benefit from bundled service offerings that include diagnostics and record-keeping, securing repeat visits. Online platforms appeal to smallholders and pet owners in remote areas who seek convenience, but regulatory safeguards around prescription biologics still funnel high-value transactions through professionals. This multi-channel evolution ultimately broadens reach without diluting quality standards across the veterinary vaccines market size.

Geography Analysis

Germany’s 23.88% share underscores its role as Europe’s livestock powerhouse and an innovation hub that incubates platform technologies under EMA supervision. Federal surveillance and export certification standards mandate vaccination for economically significant diseases, embedding recurring demand across species. France follows closely, with state-funded campaigns like the EUR 100 million avian influenza drive influencing neighbor markets to elevate their own immunization thresholds.

The United Kingdom, despite post-Brexit regulatory divergence, positions itself as a research frontrunner in DIVA testing and bovine tuberculosis vaccines, cementing its relevance inside the wider veterinary vaccines market. Italy and Spain add weight through large dairy, swine and poultry sectors, yet uneven rural cold-chain capacity tempers uptake. Mediterranean climates catalyze unique seasonal disease pressures, pushing local producers toward tailored vaccination calendars that differ from Northern Europe’s.

Rest of Europe posts the strongest 10.55% CAGR as Eastern accession states upgrade veterinary services to meet EU accession criteria. Nordic nations, boasting pet insurance penetration above 40%, nurture a premium segment for combination biologics that require stringent cold-chain integrity. Meanwhile, Eastern Europe’s rapid livestock intensification presents high-volume prospects, albeit constrained by education and infrastructure gaps that manufacturers must address to fully unlock the region’s veterinary vaccines market potential.

Regulatory Landscape

Veterinary vaccines in Europe are regulated as veterinary medicinal products under Regulation (EU) 2019/6, with harmonized rules for authorization, manufacturing, distribution, and pharmacovigilance across the Single Market. The European Medicines Agency (EMA) and its Committee for Medicinal Products for Veterinary Use (CVMP) run the centralized scientific evaluation pathway, while the Union Product Database (UPD) supports authorization visibility and lifecycle compliance obligations.

Regulatory priorities continue to balance availability and innovation with safety and surveillance, reflected in the CVMP work plan for 2026 (adopted in December 2025), which highlights support for new technologies and streamlined development interactions, including scientific advice and platform approaches. Authorization activity under this framework includes products granted EU marketing authorization in 2025 such as Ceva Sante Animale's Vectormune HVT-AIV (28 March 2025, exceptional circumstances under Article 25), alongside additional EU authorization decisions published in the Official Journal (for example, February 2026 summaries), reinforcing an active, centrally coordinated approvals environment.

Value Chain Analysis

The European veterinary vaccine value chain begins with biologics inputs (antigens, adjuvants, cell lines, excipients), followed by specialized R&D and clinical development, then GMP manufacturing and quality control that culminate in regulatory batch release and pharmacovigilance. EMA-led centralized authorization under Regulation (EU) 2019/6, together with animal-health requirements under the EU Animal Health Law (Regulation (EU) 2016/429), influences product availability and enables supply across multiple countries from single manufacturing hubs.

Downstream, validated cold-chain logistics and wholesaler networks distribute temperature-sensitive vaccines to veterinary hospitals and clinics, support government procurement channels for outbreak programs, and increasingly feed into retail and e-commerce layers where national dispensing controls apply. Manufacturing footprint and capacity draw on established European producers, including Zendal (CZ Vaccines) with GMP-certified facilities in Spain (Pontevedra, Leon, and Barcelona), while industry bodies such as AnimalhealthEurope help coordinate stakeholders on supply availability, harmonization needs, and preparedness planning.

Competitive Landscape

The European veterinary vaccines market remains moderately fragmented. Global leaders such as Zoetis, Boehringer Ingelheim and Merck leverage broad portfolios and R&D depth, while regional specialists like HIPRA, Ceva Santé Animale and IDT Biologika exploit therapeutic niches and local relationships. High regulatory hurdles and batch-release delays favor incumbents with seasoned compliance teams.

Platform technology investment shapes strategic agendas. Merck’s SEQUIVITY RNA particle system enables herd-specific vaccines within weeks, positioning the firm to win time-sensitive contracts. Ceva’s upcoming IPO, valuing the company at USD 10 billion, signals investor confidence in the animal vaccines industry’s growth runway. Refrigeration-resilient formulations also draw capital, as they could open underserved rural markets across Eastern Europe.

Consolidation pressure mounts as development costs rise; acquisitions that add platform expertise or fill portfolio gaps accelerate. Yet antitrust vigilance and national security concerns around biological products prevent excessive concentration, ensuring competition and innovation continue to thrive in the veterinary vaccines market.

Europe Veterinary Vaccine Industry Leaders

Zoetis Inc.

Merck & Co. Inc.

Virbac SA

Boehringer Ingelheim International GmbH

Elanco

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Outbreak-driven vaccination programs create a visible opportunity for antigen updates and multi-serotype coverage, particularly for transboundary diseases such as bluetongue and avian influenza. Recent authorization activity reflects product renewal and portfolio expansion in this area, including Verovaccines receiving EU-wide market authorization for a bluetongue vaccine (VeroBlue-3) and Zendal (Vetia) obtaining authorization for a trivalent bluetongue vaccine in Spain and Portugal (serotypes 1, 4, and 8), which fit with the region's surveillance-led procurement cycles.

A second opportunity is next-generation platforms and combination immunological products that reduce administration burden and improve compliance in companion animals and intensive livestock systems. The CVMP positive opinion in April 2026 for Nobivac NXT HCPChFeLV, positioned as the first self-amplifying RNA (saRNA) veterinary vaccine in the EU for cats, indicates regulatory throughput for novel modalities, while the January 2026 guideline update on combined vaccines and associations of immunological products provides a clearer development path for manufacturers. Consolidation and portfolio specialization also create space for differentiated niche vaccines, supported by Ceva Animal Health's June 2026 acquisition of Aquilón CyL S.L., bringing in what was described as Europe's only commercial vaccine against swine dysentery.

Recent Industry Developments

- July 2026: Zoetis received European Commission marketing authorization for Poulvac Procerta HVT-ND, a recombinant vector vaccine for Newcastle disease and Marek's disease in chickens. The approval strengthens Zoetis presence in poultry biologics where multi-disease protection supports integrated production systems and tighter health certification requirements.

- November 2025: Boehringer Ingelheim reported two EU CVMP positive opinions for avian influenza vaccines, VAXXITEK HVT+IBD+H5 and VAXXINACT H5. The opinions advance outbreak-response toolkits for highly pathogenic avian influenza and support procurement planning for vaccination strategies used to protect poultry supply chains and trade continuity.

- March 2024: Merck Animal Health announced European approval of NOBILIS MULTRIVA REOm for use in chickens. The approval broadened MSD Animal Health's poultry vaccine portfolio in Europe and reinforced competitive intensity around respiratory and production-impacting diseases in commercial flocks.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues earned from veterinary vaccines sold for use in animals across Europe, including companion animals and livestock, across common technologies and disease indications, as captured at manufacturer and channel selling prices.

Scope exclusions: It does not include veterinary pharmaceuticals other than vaccines, diagnostics, feed additives, or in-clinic service fees that are not part of vaccine product revenue.

Segmentation Overview

- By Animal Vaccine Type

- Livestock

- Bovine Vaccines

- Poultry Vaccines

- Porcine Vaccines

- Other Livestock Vaccines

- Companion Animals

- Canine Vaccines

- Feline Vaccines

- Livestock

- By Vaccine Technology

- Equine Vaccines

- Live Attenuated

- Inactivated / Killed

- Sub-unit & Toxoid

- Recombinant / Vector

- mRNA & DNA

- By Disease Indication

- Foot-and-Mouth Disease

- Bovine Respiratory Disease Complex

- Avian Influenza

- Porcine Circovirus

- Rabies

- Others

- By Distribution Channel

- Veterinary Hospitals & Clinics

- Government Procurement Programs

- Retail & E-commerce

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by mapping the demand pool and the regulatory setting for animal immunization in Europe, then translating that into a data backbone for sizing. We rely on public and official sources such as the European Medicines Agency (veterinary product authorizations and safety updates), Eurostat (livestock numbers and farm structure series), WOAH disease notifications, and national agriculture and animal health agencies across major European countries.

Alongside these, we review company filings, investor presentations, and reputable press to understand product launches, manufacturing footprint changes, and supply constraints that can shift pricing or availability. Patent databases are also referenced to sanity check innovation intensity by technology type. When needed, paid subscriptions focused on company financials and a separate news and financials product are used to cross-check revenue disclosures and timing of key events. The desk sources mentioned above are illustrative rather than exhaustive, and we also refer to many other public documents for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to turn desk signals into practical assumptions, mainly around country mix, animal species mix, and how vaccine demand behaves during outbreaks versus routine cycles. We speak with manufacturers, distributors, veterinarians, and large farm operators across Western, Northern, and Southern Europe, and we also include respondents linked to smaller markets in the Rest of Europe to avoid over-weighting the largest countries.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 20% | |

| Mid tier: 50% | Functional/Unit leaders: 27% | |

| Smaller Players: 21% | Managers: 53% |

Market-Sizing & Forecasting

Sizing is built using a top-down demand pool approach, where animal population by species is combined with vaccination intensity assumptions, then adjusted for disease-driven boosters and country-level adoption patterns. To keep this grounded, the model is cross-checked with selective bottom-up approximations, including sampled product ASP ranges by technology, distributor margin checks, and manufacturer revenue splits discussed in interviews. If the two views disagree, totals are adjusted to reconcile the difference.

Key inputs used in the model include livestock headcount and farm structure, companion animal ownership and clinic visit trends, vaccine schedule frequency for core diseases, outbreak signals that temporarily lift volumes, and observed pricing progression by technology type (for example, recombinant versus inactivated). When interview feedback points to missing coverage, gaps are handled by building proxy multipliers from similar countries and then testing sensitivity to avoid overstating smaller markets.

Forecasting uses scenario analysis built around three demand paths, routine prevention growth, stable conditions, and a higher-incidence scenario for specific disease indications. The final forecast is chosen after reconciling it with expert expectations on policy enforcement and farm economics.

Data Validation & Update Cycle

Validation is done through triangulation across independent signals, so the final market number has to make sense against animal population trends, authorization activity, and country-level demand narratives from interviews. Outliers are flagged through variance checks at the country and technology levels, then reviewed by a second analyst before sign-off, especially when a single country drives a large share change.

The report is refreshed annually, and interim updates are triggered when there are material events such as major outbreaks, large portfolio approvals, or meaningful pricing changes. Before delivery, we run a final review pass to ensure the latest public releases and key interview learnings are reflected in the model.

Mordor Intelligence's Europe Veterinary Vaccines Market Size Compared With Other Published Estimates

Published market sizes for Europe veterinary vaccines often differ because the scope and the math behind volumes and pricing are not aligned across sources. Differences can come from whether revenue is counted at manufacturer level or at later channel levels, how countries are grouped into Europe, and whether routine vaccination and outbreak-driven demand are treated as one pool or modeled separately.

The main gap comes from how outbreak-related vaccination waves and the resulting short-term price shifts are treated, where Mordor Intelligence models these as episodic lifts that sit on top of routine schedules rather than being spread evenly across the full year. Other estimates may also blend adjacent animal health products into the total, or they may use one average price across technologies, which can reduce market value when higher-priced platforms grow faster.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.10 B (2025) | |

| Industry Publisher A | USD 2.71 B (2025) | May smooth outbreak-driven demand into a steady annual run-rate and apply a more blended ASP, which can reduce the value captured when technology mix shifts toward higher-priced platforms. |

| Consulting Firm B | USD 3.21 B (2022) | Uses an earlier base year and a different normalization for post-2020 recovery, and it can miss later authorization-led mix shifts that change the price and volume trajectory. |

Taken together, the spread is mainly explained by what is counted as vaccine-only revenue, how short-term outbreak demand is handled, and how pricing is carried forward by technology. By keeping inputs tied to observable animal population series and interview-checked usage and price patterns, the final estimate stays traceable and can be repeated when new country or disease signals appear.

Key Questions Answered in the Report

How large is the Europe Veterinary Vaccine Market in 2026?

The Europe Veterinary Vaccine Market size in Europe reaches USD 3.32 billion in 2026.

What CAGR is forecast for European veterinary biologics through 2031?

The market is projected to grow at a 7.14% CAGR between 2026 and 2031.

Which segment shows the fastest growth inside Europe?

Companion-animal vaccines post the highest 8.95% CAGR because of pet insurance expansion.

Why are mRNA and DNA platforms gaining traction?

EMAs adaptive pathways cut approval times, enabling 9.21% CAGR for nucleic-acid platforms.

Which country leads European demand?

Germany holds 23.88% of regional revenue owing to its large livestock base and strict surveillance.

What is the main barrier for new entrants?

Lengthy EMA batch-release testing adds 4-6 weeks to product launch timelines, favoring incumbents.

Page last updated on: