Veterinary Infectious Disease Diagnostics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

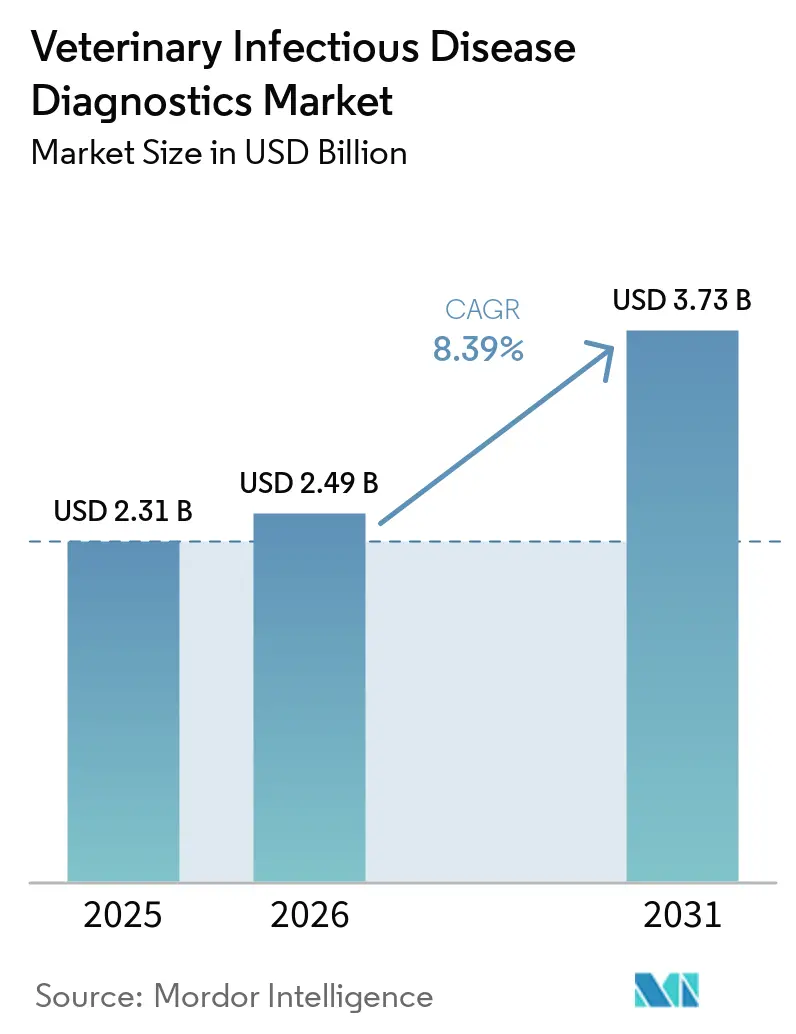

| Market Size (2026) | USD 2.49 Billion |

| Market Size (2031) | USD 3.73 Billion |

| Growth Rate (2026 - 2031) | 8.39% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veterinary Infectious Disease Diagnostics Market Analysis by Mordor Intelligence

The Veterinary Infectious Disease Diagnostics Market size is projected to expand from USD 2.31 billion in 2025 and USD 2.49 billion in 2026 to USD 3.73 billion by 2031, registering a CAGR of 8.39% between 2026 to 2031.

Growth stems from rapid adoption of AI-enabled diagnostic platforms, expanding companion-animal populations, and stricter One Health regulations that compel antimicrobial-resistance (AMR) surveillance. Molecular techniques such as PCR and next-generation sequencing are steadily replacing traditional immunoassays because they deliver higher sensitivity and faster turnaround, while cartridge-based point-of-care (POC) tests are reshaping daily clinical workflows. Vendors are differentiating through integrated ecosystems that combine AI image analysis, cloud data management, and reference-laboratory networks, allowing clinics to offer same-visit diagnoses that improve therapeutic outcomes and client satisfaction. Headwinds include rising veterinary-care costs and a widening veterinarian workforce gap, both of which may limit diagnostic uptake in price-sensitive segments and rural geographies.

Key Report Takeaways

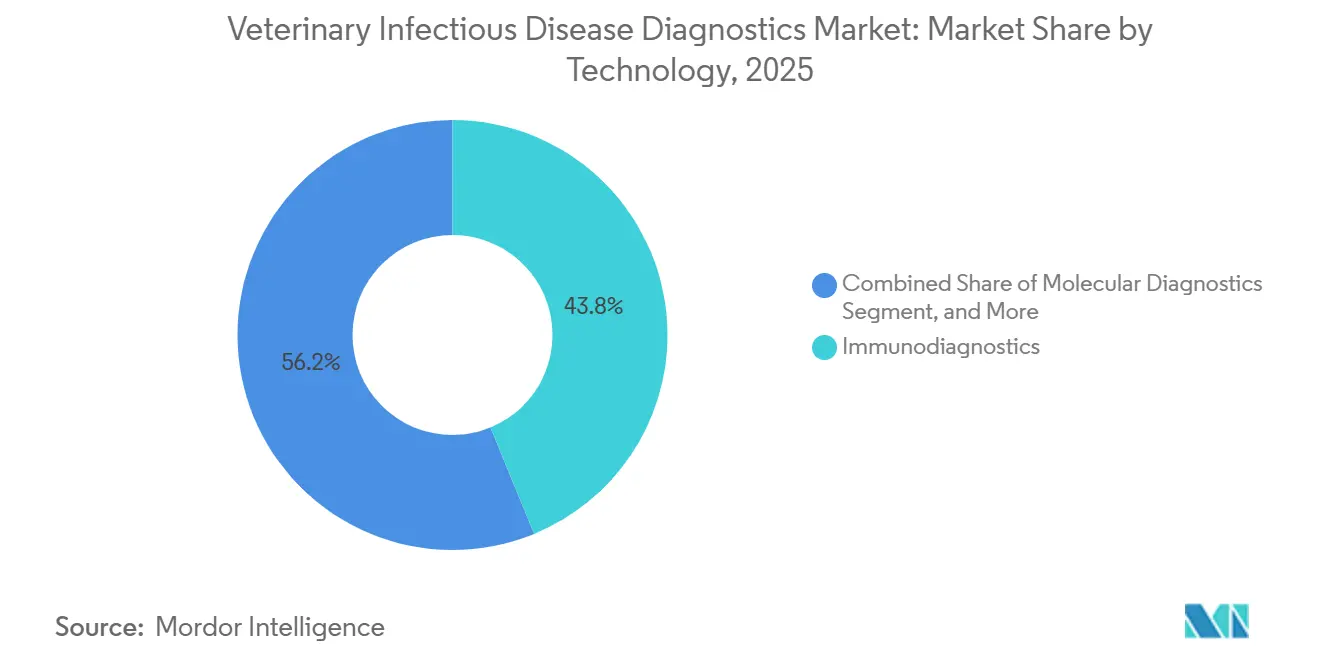

- By technology, immunodiagnostics held 43.78% of veterinary infectious disease diagnostics market share in 2025, while molecular diagnostics are projected to expand at a 10.07% CAGR through 2031.

- By animal type, companion animals accounted for 56.92% of the veterinary infectious disease diagnostics market size in 2025; food-producing animals represent the fastest-growing group at an 11.69% CAGR to 2031.

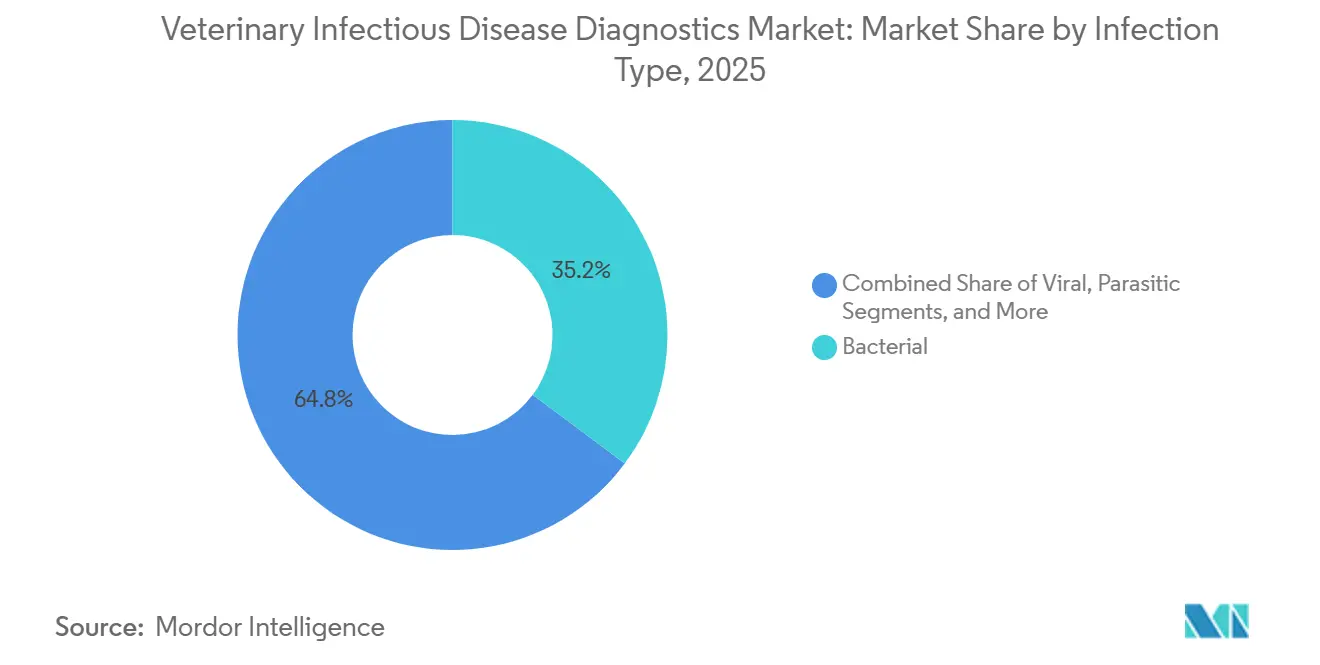

- By infection type, bacterial pathogens dominated with 35.21% market share in 2025; viral diagnostics are forecast to rise at a 9.22% CAGR.

- By end user, reference laboratories led with 45.02% revenue share in 2025, whereas POC and in-house testing will post the strongest growth at a 10.12% CAGR.

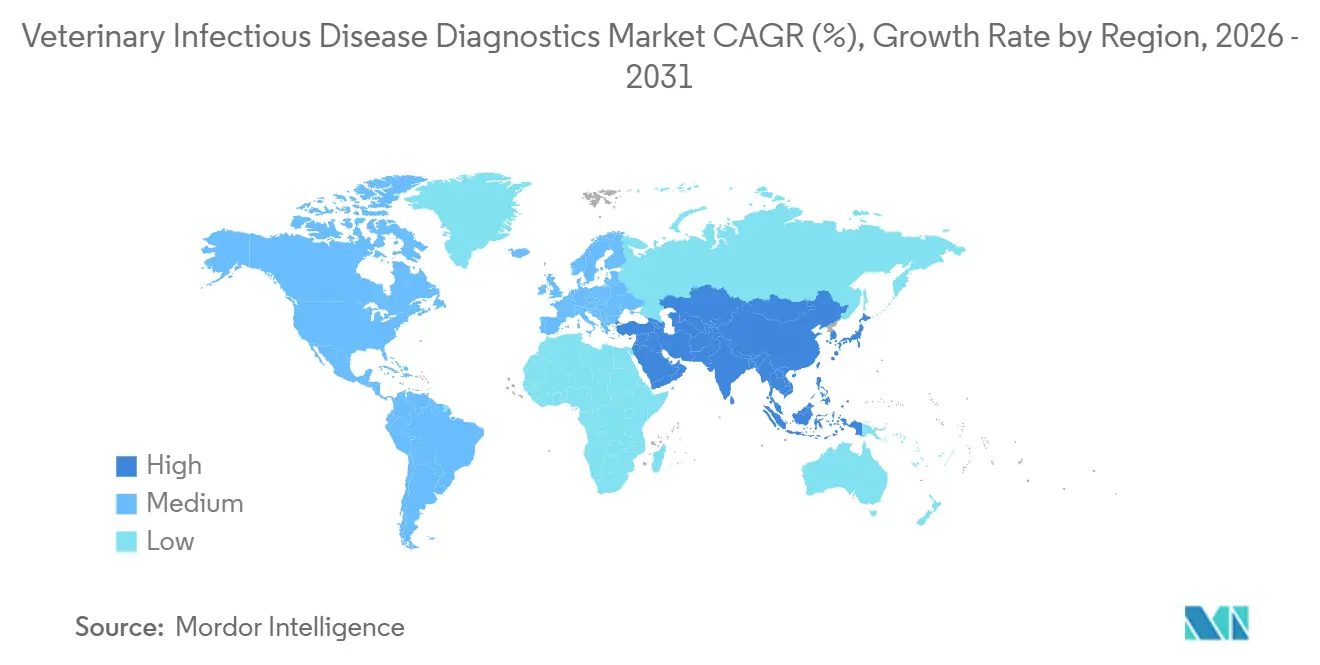

- By geography, North America captured 40.12% of global revenue in 2025; Asia-Pacific is set to grow the fastest at 9.16% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Veterinary Infectious Disease Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advanced diagnostic devices for animals | +1.8% | Global, led by North America & Europe | Medium term (2-4 years) |

| Growing demand for pet insurance | +1.2% | North America & Europe primary, Asia-Pacific emerging | Long term (≥ 4 years) |

| Increasing companion animal population | +2.1% | Global, strongest in Asia-Pacific | Long term (≥ 4 years) |

| AI-powered image analysis adoption in vet labs | +1.5% | North America & Europe core, expanding globally | Short term (≤ 2 years) |

| One Health AMR surveillance regulations | +1.0% | Global, EU & North America lead | Medium term (2-4 years) |

| Tele-veterinary sample-collection networks | +0.9% | North America primary, developed markets next | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI-Powered Image Analysis Adoption In Vet Labs

AI integration is moving laboratory interpretation from subjective, manual review to data-driven automation. Platforms such as Zoetis’ Vetscan Imagyst now screen lymph-node and skin-mass aspirates in minutes, a process that previously required days at external labs, enabling faster treatment decisions and improving client adherence. Nearly 30% of U.S. veterinarians already apply AI for imaging or record management tasks. Regulatory bodies, however, insist on rigorous validation before broad clinical use, promoting collaborative studies that benchmark AI accuracy against board-certified radiologists. Early adopters report sharper diagnostic confidence, a crucial benefit given the looming shortage of skilled practitioners. As reimbursements remain procedure-driven, AI tools that speed results without compromising quality are expected to shift from competitive advantage to baseline requirement, fuelling demand across the veterinary infectious disease diagnostics market.

Advanced Diagnostic Devices For Animals

Multiplex PCR and cartridge-based POC systems are compressing test windows from days to minutes, helping clinics avoid follow-up visits and reduce antibiotic misuse. A 2025 triplex real-time PCR assay for swine respiratory diseases achieved 100% agreement with national standards, underlining molecular reliability. Zoetis’ Vetscan OptiCell extends this efficiency to complete blood counts in less than 10 minutes, offering reference-lab precision in-clinic.[1]Zoetis, “Zoetis to Preview AI-Powered Cytologic Analysis Technology at VMX,” zoetisus.com Genomic selection tools embedded within herd-health programs reduce disease susceptibility and antibiotic dependency, directly tying diagnostics to improved production metrics. Clinics that invest in such devices report higher client retention and the ability to charge premium service fees, reinforcing capital-investment cycles that sustain the veterinary infectious disease diagnostics market.

Increasing Companion Animal Population

U.S. households hosted 89.7 million dogs and 73.8 million cats in 2024, up 45%. Similar growth trajectories in China and India are boosting first-time vet visits for vaccinations and baseline health screens. Yet average U.S. veterinary spending fell 4% in the same period, proving that larger pet populations do not guarantee revenue if price sensitivity rises. Diagnostics firms therefore segment offerings into core and premium panels, ensuring essential coverage at competitive price points while upselling genomic or AI-enhanced tests to affluent owners. Population density in megacities also elevates zoonotic-disease risk, heightening demand for rapid communicable-disease screening and sustaining momentum in the veterinary infectious disease diagnostics market.

One-Health AMR Surveillance Regulations

The World Organisation for Animal Health warns that AMR could slash USD 575 billion from global GDP by 2050 if unchecked.[2]World Organisation for Animal Health, “Forecasting the Fallout from AMR,” woah.org Governments are mandating genomic surveillance of livestock pathogens and harmonized data exchange with human-health agencies. Real-time sequencing is now embedded in outbreak response protocols, driving laboratories to acquire high-throughput sequencers and bioinformatics pipelines. Vendors that bundle instruments, reagents, and cloud analytics into turnkey AMR-monitoring suites gain a compliance-driven market entry route. Developing regions are racing to upgrade lab capacity, creating multi-year revenue streams for diagnostic suppliers that provide training and maintenance services alongside tests, thereby enlarging the veterinary infectious disease diagnostics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High pet-care costs | -1.4% | Global, strongest in price-sensitive markets | Short term (≤ 2 years) |

| Shortage of skilled veterinarians | -1.8% | North America & Europe primary, expanding globally | Long term (≥ 4 years) |

| Cross-border specimen-shipping regulations | -0.7% | Global, complex EU & U.S. rules | Medium term (2-4 years) |

| Data-privacy risks in digital lab platforms | -0.5% | Developed markets with strict data laws | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled Veterinarians

The United States alone is projected to lack 70,092 veterinarians by 2032, with only 52,926 graduates expected, a gap driven by rural attrition and lifestyle preferences.[3]American Association of Veterinary Medical Colleges, “Demand for and Supply of Veterinarians in the U.S. to 2032,” aavmc.org Large-animal practice is hardest hit; livestock-focused vets have declined 90% since World War II, now representing under 2% of the profession. Fewer clinicians limit test ordering, especially in remote areas where mobile labs or tele-diagnostics must compensate. Technology that automates sample collection or streamlines interpretation partly offsets manpower gaps, but sustained shortages weigh on long-term volumes and slow expansion of the veterinary infectious disease diagnostics market.

High Pet-Care Costs

Veterinary fees are rising faster than general inflation across Europe and North America, with routine procedures such as pyometra surgery posting the steepest increases. Average U.S. household spending slid to USD 580 for dogs and USD 433 for cats in 2024, reflecting cost-averse behaviour. Owners often defer comprehensive panels in favour of minimal tests, pressuring clinics to offer tiered pricing or wellness plans. POC devices that reduce follow-up visits help ease total episode cost, but capital investment is hard to justify for low-volume practices. This price sensitivity tempers revenue growth, especially for emerging-market clinics, and curbs overall momentum in the veterinary infectious disease diagnostics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Molecular Diagnostics Drive Innovation Despite Immunodiagnostics Dominance

Immunodiagnostics retained a 43.78% revenue share in 2025 due to entrenched ELISA and chemiluminescent assays across routine screening. Nevertheless, molecular diagnostics recorded the quickest gains and are forecast to post a 10.07% CAGR, mirroring the broader shift toward precision medicine. Clinics adopting multiplex PCR report fewer inconclusive results and lower antibiotic misuse, boosting client confidence and strengthening loyalty within the veterinary infectious disease diagnostics market. Cartridges that integrate extraction and amplification simplify workflows, allowing smaller practices to perform formerly complex assays. Vendors further add AI-driven result interpretation, reducing error rates and training demands. Over the forecast window, integrated workstations that merge serology, PCR, and hematology functionalities are expected to dominate new-equipment purchases, underscoring the sector’s convergence trend.

Market momentum also stems from next-generation sequencing (NGS) rollouts that enable pathogen discovery and AMR gene tracking. While cost per sample remains high, pooled testing strategies in herd health make NGS economically viable for high-value livestock operations. Cloud-based bioinformatics reduces on-premise infrastructure needs, fostering adoption across resource-constrained geographies. Immunodiagnostics will persist for high-throughput surveillance and cost-sensitive settings; however, their share is projected to decline gradually as rapid molecular platforms become ubiquitous across the veterinary infectious disease diagnostics market.

By Animal Type: Food-Producing Animals Accelerate Growth Through Regulatory Compliance

Companion animals generated 56.92% of global revenue in 2025, anchored by rising pet humanization and insurance uptake. Yet food-producing animals will expand fastest at 11.69% CAGR to 2031 as regulators impose stringent monitoring after incidents such as the H5N1 dairy-cattle outbreak that affected 989 U.S. herds. Livestock producers increasingly embed diagnostics in herd-health protocols to avoid culling losses and export bans. Governments subsidize surveillance kits, narrowing cost barriers and enlarging install bases for barn-side PCR readers, which, in turn, fuel the veterinary infectious disease diagnostics market size for this segment.

Genomic selection augments diagnostics by identifying disease-resistance alleles, reducing long-term medication costs and residue risks. Integrated platforms that merge pathogen detection with genetic profiling help producers comply with AMR-reporting mandates and sustainability certifications. Companion-animal growth will continue, albeit at a lower rate, as economic pressures spur selective testing behaviour. Clinics that offer bundled vaccination-plus-diagnostic packages should preserve volumes even in cost-sensitive markets, sustaining their position within the veterinary infectious disease diagnostics market.

By Infection Type: Viral Diagnostics Gain Momentum Through Outbreak Response

Bacterial diseases represented 35.21% of 2025 revenue because established protocols and high incidence keep test volumes stable. The viral segment, however, is poised for the highest 9.22% CAGR as global trade, migration, and climate change heighten outbreak frequency. The H5N1 episode underscored the need for rapid multi-species viral panels capable of detecting emergent strains. Labs investing in high-throughput PCR and sequencing can pivot quickly during crises, generating surges in consumable demand and driving incremental growth across the veterinary infectious disease diagnostics market.

Parasitic and fungal pathogens still represent niche but rising sub-segments thanks to improved screening accuracy. Antech’s advanced parasite panel detects low-abundance infections that were often missed previously, enabling early intervention and reducing zoonotic risk. Holistic panels covering bacterial, viral, and parasitic targets on the same cartridge are emerging, lowering per-sample costs and simplifying inventory, thereby enhancing value for mixed-practice clinics.

By End User: Point-of-Care Testing Transforms Practice Workflows

Reference laboratories controlled 45.02% of global sales in 2025, leveraging their breadth of assays and quality-control rigor. Yet POC and in-house testing will outpace all other segments at 10.12% CAGR because immediate results eliminate return visits and boost treatment compliance. Platforms such as Vetscan Imagyst provide on-site cytology that historically required external review, shortening time to diagnosis from two days to under 10 minutes. For emergencies, same-visit diagnostics directly influence survival rates and client satisfaction, reinforcing uptake across the veterinary infectious disease diagnostics market.

Research institutes and universities remain innovation engines, validating assays and training veterinarians in advanced techniques. Collaboration with commercial vendors accelerates technology transfer, with spin-outs often targeting specialised niches such as exotic-animal diagnostics or wildlife disease surveillance. Over the forecast period, hybrid models that link POC devices to central lab networks via cloud reporting will offer the best of both worlds—fast preliminary insights backed by reference-level confirmation—bolstering confidence in POC adoption.

Geography Analysis

North America led the veterinary infectious disease diagnostics market in 2025 with 40.12% share due to mature veterinary infrastructure, high pet-insurance penetration, and robust livestock surveillance funding. Federal H5N1 mitigation programs drive continual demand for avian and bovine panels, sustaining consumable sales. Europe follows closely, characterised by stringent welfare rules and near-universal canine insurance in nations like Sweden, which support comprehensive diagnostic uptake. Pan-EU AMR directives also bolster molecular and genomic test adoption.

Asia-Pacific stands out with the quickest 9.16% CAGR, fuelled by rising disposable incomes and rapid urbanisation in China, India, and Southeast Asia. Government-backed livestock modernisation programs require continuous pathogen monitoring, while middle-class pet owners increasingly demand Western-style preventive care, expanding the veterinary infectious disease diagnostics market. Partnerships with local distributors and price-tiered product lines are essential for penetration, given heterogeneous regulatory regimes and price sensitivity. Latin America, the Middle East, and Africa offer incremental growth via livestock disease-control initiatives and rising companion-animal ownership, but infrastructure limitations necessitate mobile-lab or satellite-network models to unlock full potential.

Competitive Landscape

The veterinary infectious disease diagnostics market is moderately fragmented. IDEXX, Zoetis, and Thermo Fisher Scientific leverage economy-of-scale R&D budgets and global distribution to maintain leadership. IDEXX broadened its Catalyst test menu in 2025 to include pancreatitis markers, offering quantitative results in under 10 minutes and seamless VetConnect PLUS integration. Zoetis deepened vertical integration by opening a 32,000-square-foot Louisville reference lab co-located with UPS Healthcare, ensuring overnight specimen logistics and enhanced customer retention. Thermo Fisher extends reach through OEM agreements that bundle reagents with existing automated platforms in mixed-practice clinics.

Emerging firms concentrate on AI algorithms, species-specific panels, and cost-efficient POC devices, often partnering with academic labs for validation. Mergers and acquisitions are expected as top players seek proprietary AI models or geographic expansion, compressing development timelines. Competitive advantage now hinges on ecosystem breadth—hardware, consumables, software, and analytics—rather than standalone assays. Companies that deliver subscription-based reagent replenishment plus cloud analytical upgrades are positioned to lock in recurring revenue across the veterinary infectious disease diagnostics market.

Veterinary Infectious Disease Diagnostics Industry Leaders

bioMerieux

IDEXX Laboratories

Zoetis Inc.

Thermo Fisher Scientific

Antech Diagnostics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: With no approved vaccine currently available for the ongoing Ebola outbreak, experts are considering testing alternative options. An animal study has suggested that Merck’s Ervebo, a vaccine originally designed for a different strain of the virus, may provide partial protection. This development highlights both the urgency of finding effective preventive measures and the potential of repurposing existing vaccines to address emerging health crises.

- April 2026: Co-Diagnostics, a molecular diagnostics company with a patented platform for developing advanced molecular diagnostic tests, announced its participation in the Congress of the European Society of Clinical Microbiology and Infectious Disease (ESCMID Global) 2026 in Munich, Germany. This marks a significant milestone for the company, highlighting its commitment to expanding global visibility and engaging with leading experts in infectious disease diagnostics.

- May 2025: Zoetis strengthened its U.S. diagnostics network by launching a 32,000 square-foot Louisville reference laboratory adjacent to UPS Healthcare for faster specimen processing and next-day reporting.

Global Veterinary Infectious Disease Diagnostics Market Report Scope

As per the scope of this report, the veterinary disease diagnostic means the act or process for identifying or determining the nature and cause of a disease/injury through evaluation of patient history, examination, and review or analysis of laboratory data. The veterinary diagnostics devices include diagnostic test kits, needles, and syringes. The diagnostic technique should be rapid, specific, sensitive, and cost-effective.

The Veterinary Infectious Disease Diagnostics Market is segmented by Technology (Immunodiagnostics, Molecular Diagnostics, and Others), Animal Type (Companion Animals and Food-Producing Animals), Infection Type (Bacterial Infections, Viral Infections, Parasitic Infections, and Others), End User (Reference Laboratories, Veterinary Laboratories, and Clinics and Point of Care/In House Testing) and Geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Immunodiagnostics (ELISA, CLIA) |

| Molecular Diagnostics (PCR, RT-PCR, NGS) |

| Rapid / Point-of-Care Tests |

| Hematology & Clinical Chemistry |

| Companion Animals | Canines |

| Felines | |

| Equines | |

| Food-Producing Animals | Bovine |

| Porcine | |

| Poultry | |

| Ovine & Caprine |

| Bacterial |

| Viral |

| Parasitic |

| Others |

| Reference Laboratories |

| Veterinary Hospitals & Clinics |

| Point-of-Care / In-house Testing |

| Research Institutes & Universities |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Immunodiagnostics (ELISA, CLIA) | |

| Molecular Diagnostics (PCR, RT-PCR, NGS) | ||

| Rapid / Point-of-Care Tests | ||

| Hematology & Clinical Chemistry | ||

| By Animal Type | Companion Animals | Canines |

| Felines | ||

| Equines | ||

| Food-Producing Animals | Bovine | |

| Porcine | ||

| Poultry | ||

| Ovine & Caprine | ||

| By Infection Type | Bacterial | |

| Viral | ||

| Parasitic | ||

| Others | ||

| By End User | Reference Laboratories | |

| Veterinary Hospitals & Clinics | ||

| Point-of-Care / In-house Testing | ||

| Research Institutes & Universities | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the veterinary infectious disease diagnostics market?

The market is worth USD 2.49 billion in 2026 and is projected to climb to USD 3.73 billion by 2031.

Which technology segment is growing the fastest?

Molecular diagnostics, including PCR and next-generation sequencing, are forecast to expand at a 10.07% CAGR between 2026 and 2031.

Why is Asia-Pacific attracting attention in this market?

Rising household incomes, rapid urbanisation, and government-funded livestock-health programs are propelling Asia-Pacific to the highest regional CAGR of 9.16% through 2031.

How are AI tools influencing veterinary diagnostics?

AI platforms such as Vetscan Imagyst automate image interpretation, cut turnaround times from days to minutes, and enhance diagnostic consistency across experience levels.

What challenges could slow market growth?

Escalating pet-care costs and a projected shortage of over 70,000 veterinarians in the U.S. alone by 2032 may limit test adoption, particularly in rural and price-sensitive settings.

Page last updated on: