Monoclonal Antibodies In Veterinary Health Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

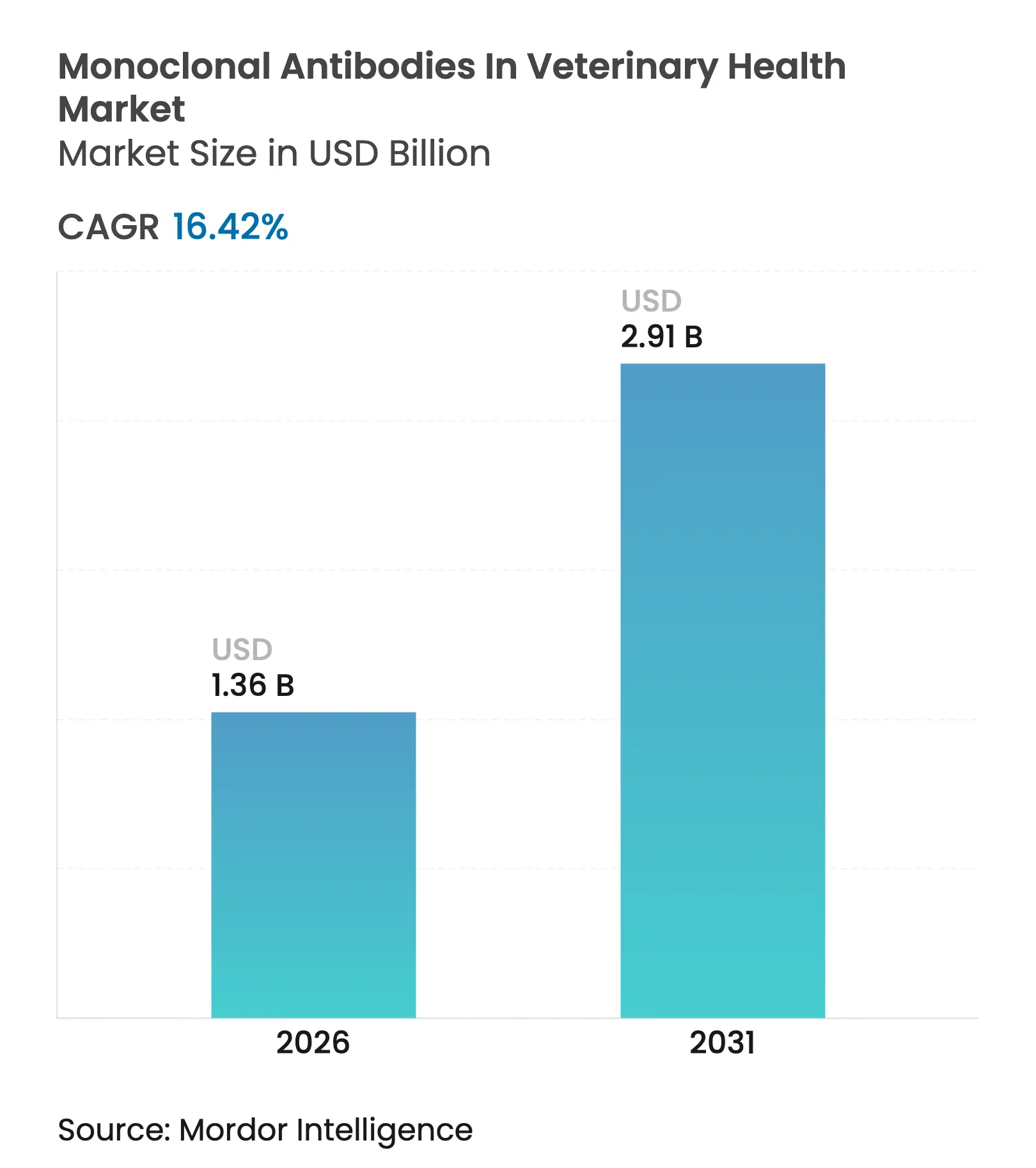

| Market Size (2026) | USD 1.36 Billion |

| Market Size (2031) | USD 2.91 Billion |

| Growth Rate (2026 - 2031) | 16.42 % CAGR |

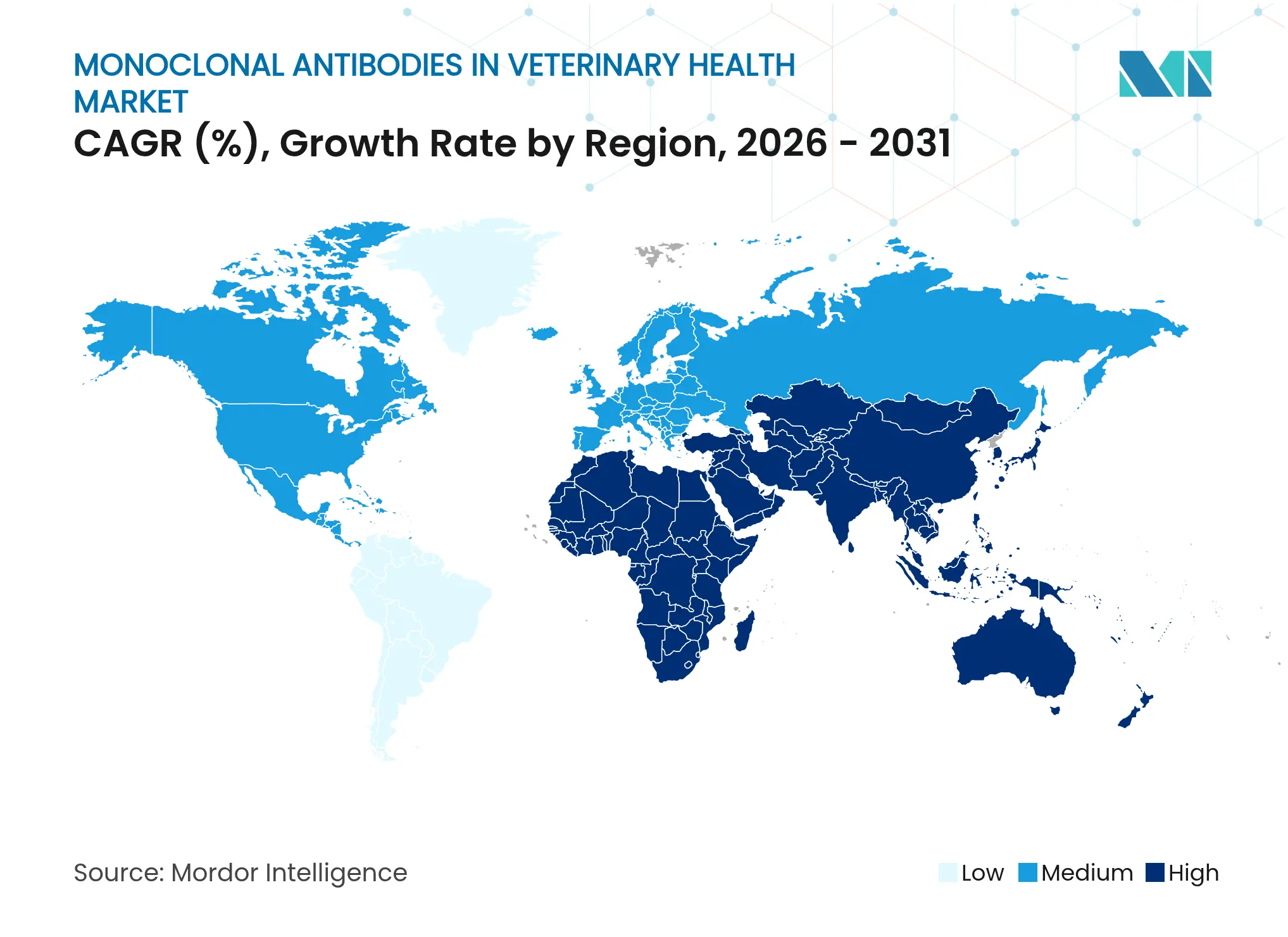

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Monoclonal Antibodies In Veterinary Health Market Analysis by Mordor Intelligence

This powerful trajectory stems from chronic-disease prevalence in aging pets, a surge of first-in-class regulatory approvals, and the rapid build-out of purpose-built biomanufacturing capacity. Early commercial successes, such as bedinvetmab for canine osteoarthritis and frunevetmab for feline osteoarthritis, have demonstrated strong efficacy-to-safety ratios and inspired confidence among veterinarians, payers, and pet owners. Pipeline visibility has also improved as conditional and fast-track pathways shorten development timelines while contract development and manufacturing organizations (CDMOs) scale single-use bioreactor footprints to meet demand.

Key Report Takeaways

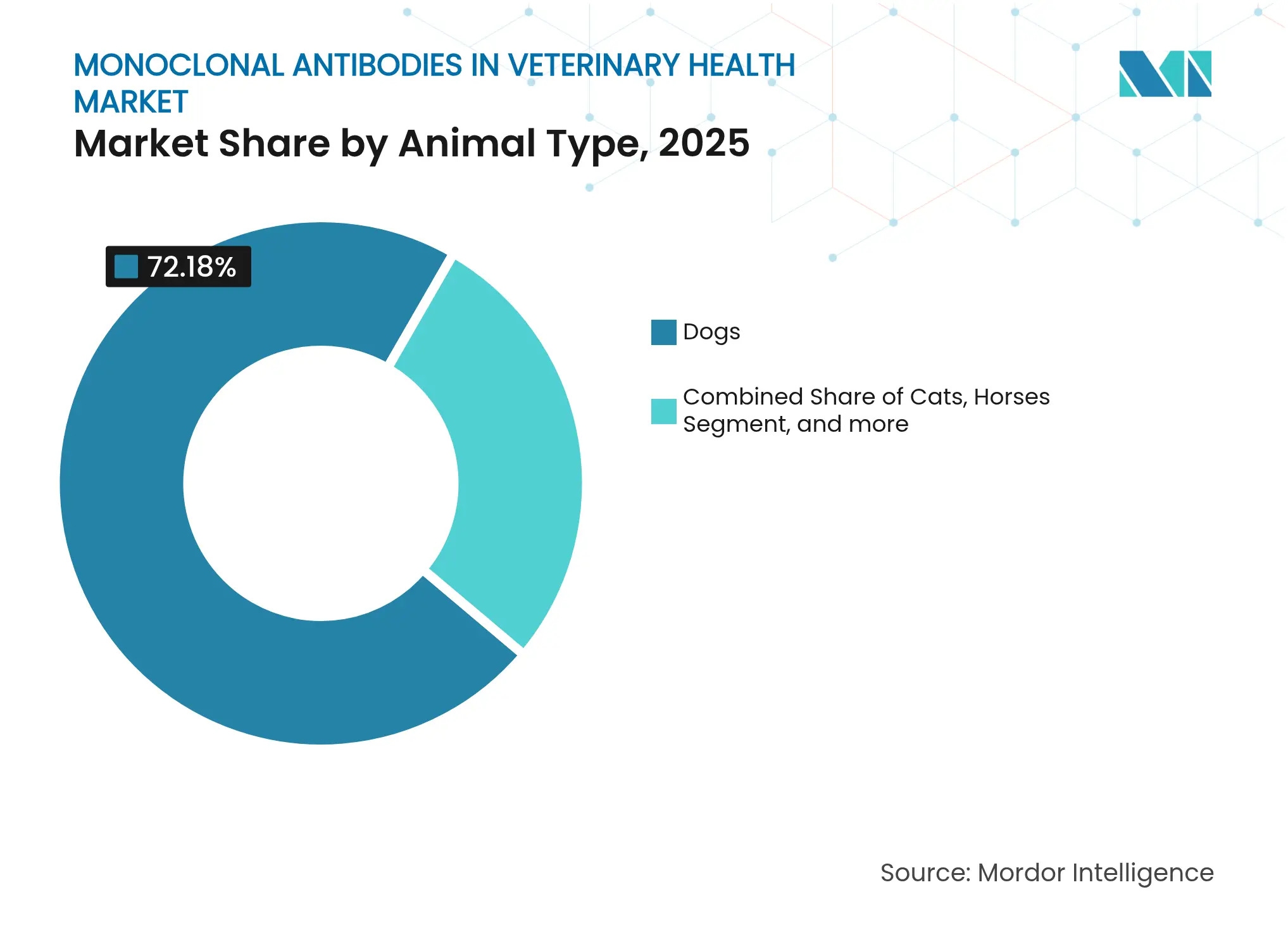

- By animal type, dogs held 72.18% of the monoclonal antibodies in veterinary health market share in 2025, while cats are forecast to post an 18.73% CAGR to 2031.

- By application, dermatology led with 58.75% revenue share in 2025; oncology is expected to expand at a 19.42% CAGR through 2031.

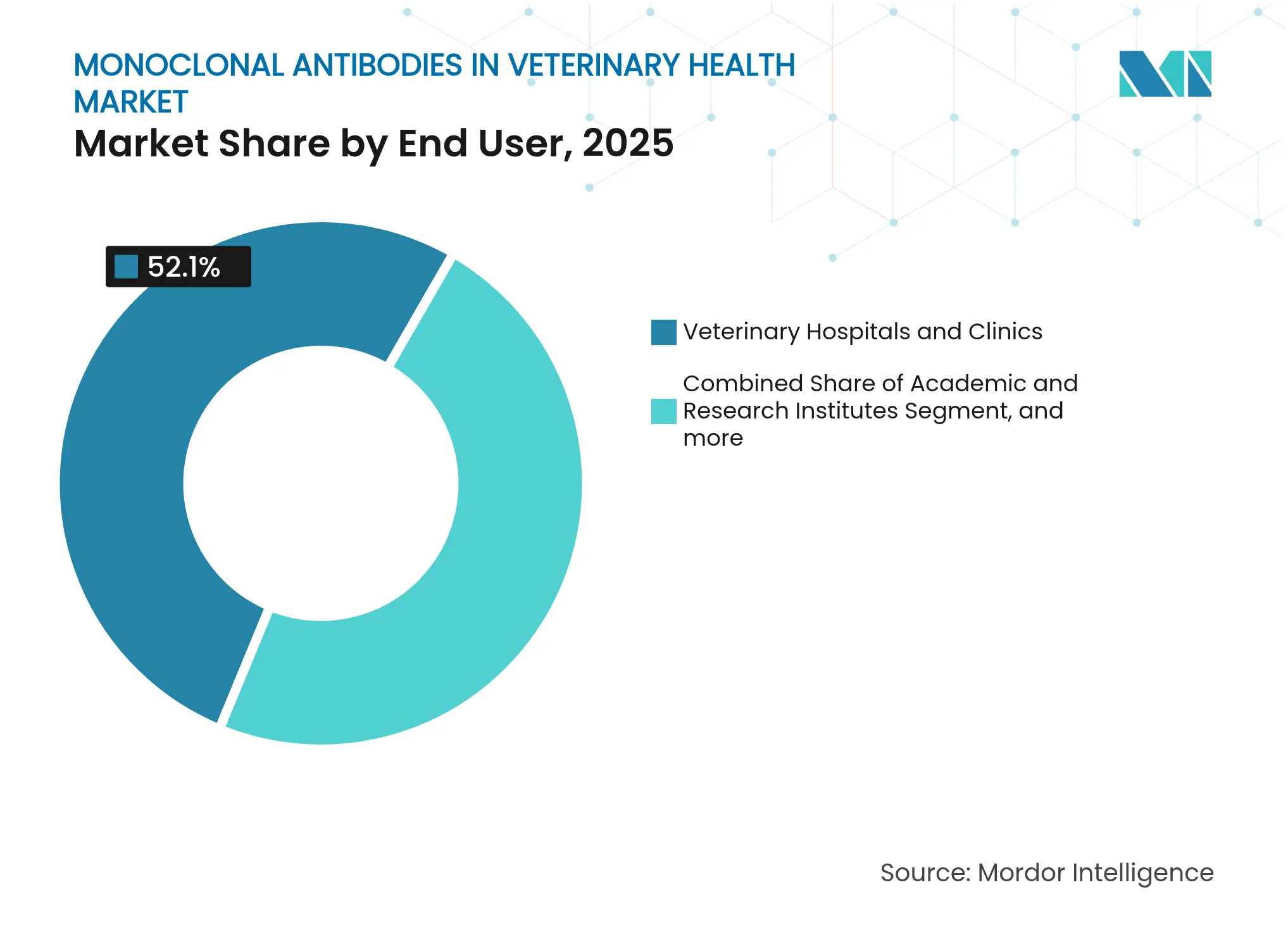

- By end user, veterinary hospitals and clinics accounted for 52.10% of the monoclonal antibodies in veterinary health market size in 2025; academic and research institutes show the highest projected CAGR at 23.25% to 2031.

- By geography, North America commanded 44.30% revenue share in 2025, whereas Asia-Pacific is projected to climb at a 21.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Monoclonal Antibodies In Veterinary Health Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising burden

of chronic disorders among companion animals

Rising burden

of chronic disorders among companion animals

| +3.2% | Global; highest in North America & Europe | Long term (≥ 4 years) |

(~) %

Impact on CAGR Forecast

:

+3.2%

|

Geographic

Relevance

:

Global;

highest in North America & Europe

|

Impact

Timeline

:

Long term (≥

4 years)

|

Increasing

pet ownership & expenditure on advanced care

Increasing

pet ownership & expenditure on advanced care

| +2.8% | Global; fastest in Asia-Pacific | Medium term (2-4 years) | |||

Rapid

approval pipeline of novel veterinary mAbs

Rapid

approval pipeline of novel veterinary mAbs

| +2.1% | North America & Europe; Asia-Pacific gaining | Short term (≤ 2 years) | |||

Favourable

USDA/EMA fast-track pathways for biologics

Favourable

USDA/EMA fast-track pathways for biologics

| +1.9% | North America & Europe | Short term (≤ 2 years) | |||

Expansion of

dedicated CDMO capacity for vet-mAbs

Expansion of

dedicated CDMO capacity for vet-mAbs

| +1.7% | Global; hubs in North America & Europe | Medium term (2-4 years) | |||

AI-driven

precision-dosing platforms boosting efficacy

AI-driven

precision-dosing platforms boosting efficacy

| +1.4% | Initially North America & Europe; global later | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Burden of Chronic Disorders Among Companion Animals

One in four dogs now develops osteoarthritis during its lifetime, creating persistent therapeutic demand that favors antibody-guided pain control over daily NSAIDs. Bedinvetmab’s targeted nerve-growth-factor blockade produced fewer adverse events than meloxicam in head-to-head trials, with only four adverse-event reports versus seventeen in the control arm.[1]Frontiers in Veterinary Science, “Comparison of Bedinvetmab and Meloxicam in Dogs,” frontiersin.org Large post-marketing studies covering France, Germany, Italy, Spain, and the United Kingdom confirmed high veterinarian satisfaction, reinforcing the product-class halo.[2]MDPI, “Veterinarian Satisfaction with Bedinvetmab in Europe,” mdpi.com Comparable disease loads exist for allergic dermatitis and certain cancers, expanding the clinical runway for additional species-specific monoclonal antibodies in veterinary health market therapies.

Increasing Pet Ownership & Expenditure on Advanced Care

Millennial and Generation Z owners treat pets as family and routinely purchase premium therapeutics despite macro-economic slowdowns, propelling companion-animal health spending to record levels in 2025.[3]Harris Williams, “Pet Industry Outlook 2024,” harriswilliams.com The willingness to pay aligns with monthly injectable regimens that reduce pill fatigue. Zoetis disclosed double-digit revenue growth in canine and feline pain franchises in 2024, with monoclonal antibodies a principal contributor. Broader pet-insurance penetration further offsets out-of-pocket costs, lifting adoption across income tiers.

Rapid Approval Pipeline of Novel Veterinary mAbs

Regulatory momentum is robust: the USDA granted conditional approval for Elanco’s canine parvovirus monoclonal antibody, the first targeted antiviral with 100% survival in challenge studies. Boehringer Ingelheim’s acquisition of Saiba Animal Health expanded its checkpoint-inhibitor pipeline, signaling an industry pivot toward immune-oncology. Parallel investments, such as Elanco’s USD 130 million biologics expansion in Kansas, underscore growing confidence in the class.

Favourable USDA/EMA Fast-Track Pathways for Biologics

Conditional licensure and priority review designations now shave multiple years off development timelines and unlock earlier revenue streams. The FDA’s expanded conditional approval pathway, combined with the USDA’s priority zoonotic-drug framework, has already accelerated several first-in-class launches. VICH guideline harmonization facilitates multi-region submissions, reducing duplicative study requirements and smoothing international rollouts.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High cost of

development & therapy

High cost of

development & therapy

| -2.3% | Global; deeper in emerging markets | Long term (≥ 4 years) |

(~) %

Impact on CAGR Forecast

:

-2.3%

|

Geographic

Relevance

:

Global;

deeper in emerging markets

|

Impact

Timeline

:

Long term (≥

4 years)

|

Complex

multi-jurisdictional regulatory compliance

Complex

multi-jurisdictional regulatory compliance

| -1.8% | Global; toughest on SMEs | Medium term (2-4 years) | |||

Weak

cold-chain logistics in emerging markets

Weak

cold-chain logistics in emerging markets

| -1.2% | Asia-Pacific, MEA, Latin America | Medium term (2-4 years) | |||

Competition

from long-acting small-molecule analgesics

Competition

from long-acting small-molecule analgesics

| -1.1% | Global; usage varies by region | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

High Cost of Development & Therapy

Species-specific antibody engineering, multi-arm field trials, and GMP-grade production can drive pre-commercial spend above USD 200 million, placing a ceiling on addressable volumes in price-sensitive regions. Developers such as PetMedix and Adivo have invested heavily in phage-display libraries that produce fully canine or feline sequences, yet these platforms also prolong time-to-proof-of-concept. Smaller firms often out-license assets early to balance risk, which can dilute future upside and restrain innovation velocity within the monoclonal antibodies in veterinary health market.

Complex Multi-Jurisdictional Regulatory Compliance

Dual oversight by the USDA and FDA in the United States, EMA in Europe, PMDA in Japan, and NMPA in China forces sponsors to tailor dossiers to divergent definitions of “biologic,” raising costs and extending lead times. New data-exclusivity rules in China and an online submission mandate in India add further procedural layers that can stall smaller entrants.

Segment Analysis

By Animal Type: Canine Strength and Accelerating Feline Uptake

Dogs generated 72.18% of the monoclonal antibodies in veterinary health market size in 2025 thanks to early-acting blockbusters like bedinvetmab and lokivetmab. Strong brand equity, a large installed base of canine patients, and straightforward weight-based dosing frameworks keep uptake resilient in the face of competing analgesics. Dermatology, orthopedic, and emerging oncology studies in breeds such as Labrador Retrievers and Golden Retrievers cement clinical relevance, while the breed-specific data also help refine AI-supported dosing algorithms. Stable reimbursement policies from leading pet insurance providers further bolster long-term renewal rates of canine biologics.

Cats, although historically underserved, now deliver the highest growth trajectory at an 18.73% CAGR as frunevetmab proves that feline-specific antibodies can match canine benchmarks in pain relief and owner adherence. Expanded research into feline stomatitis, chronic kidney disease, and lymphoma widens therapeutic horizons. Developers must navigate distinct feline immune-system architecture, yet AI-enabled epitope mapping is cutting discovery cycles in half, speeding time-to-clinic. Horses and other specialty species presently account for a small slice of revenue, mostly in performance-medicine contexts, but could gain if bio-similarity rules evolve to embrace larger-animal indications.

Note: Segment shares of all individual segments available upon report purchase

By Application: Dermatology Dominance with Oncology Rising

Dermatology contributed 58.75% of the monoclonal antibodies in veterinary health market size in 2025, anchored by lokivetmab’s robust global sales and multiple label expansions into chronic pruritus. Monthly injections have replaced corticosteroid cycles in many clinics, lowering adverse-event incidence and reinforcing positive adherence loops. Cross-discipline evidence showing shared inflammatory pathways between atopic dermatitis and osteoarthritis has encouraged off-label exploration, broadening end-user familiarity with antibody solutions.

Oncology is scaling rapidly at a 19.42% CAGR as checkpoint-inhibitor science migrates from human medicine to pets through programs such as Akston Biosciences’ anti-cPD-L1 for canine bladder cancer. Comparative-oncology grants from the National Cancer Institute support parallel trials, generating translational data that improves both human and veterinary outcomes. Infectious-disease antibodies like Elanco’s parvovirus candidate reinforce the modality’s versatility, while immune-mediated disorders such as pemphigus foliaceus present frontier indications likely to materialize late in the decade.

By End User: Hospital Lead and Academic Outperformance

Veterinary hospitals and clinics retained 52.10% of the monoclonal antibodies in the veterinary health market share in 2025, driven by routine wellness visits that align with monthly dosing schedules and in-house inventory management. Clinic networks employ board-certified specialists who champion early adoption and actively integrate AI-tailored dosing schemes into practice management software, tightening client retention. Emergency and specialty referral centers account for growing secondary demand as complex oncology and immune-mediated cases cluster.

Academic and research institutes, although smaller in revenue today, are expanding at a 23.25% CAGR through 2031 as universities leverage comparative oncology funding to run randomized controlled trials at scale. Grant-funded studies accelerate evidence generation and create educated cohorts of new veterinarians already fluent in biologic protocols, which cascades back into commercial practice. Diagnostic labs embedded within teaching hospitals also refine biomarker panels that feed AI-powered dosing engines, bolstering real-world efficacy data feedback loops.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America captured 44.30% of 2025 revenue within the monoclonal antibodies in veterinary health market, reflecting a mature reimbursement culture, deep pet-insurance penetration, and an accommodating FDA-USDA dual-pathway framework. Robust practice networks allow manufacturers to stage direct-to-veterinarian education campaigns that translate swiftly into prescription growth. Canada leverages similar product-registration rules, while Mexico’s expanding middle class supports premium pet care, albeit from a lower base.

Europe remains a high-value but more regulated arena. EMA centralized procedures standardize quality, safety, and efficacy criteria, fostering predictable launch timelines. Germany, France, and the United Kingdom anchor demand, yet Southern and Eastern European markets are catching up as disposable incomes rise. Strict antimicrobial-use reduction targets underscore the strategic importance of targeted biologics as alternatives to conventional drugs.

Asia-Pacific is the fastest climber with a 21.90% CAGR, propelled by China’s approval of 93 therapeutic biologics in 2024, including multiple monoclonal antibodies. Urbanization and single-child household dynamics boost pet adoption, and tier-one Chinese cities already mirror Western spending patterns. Japan blends rigorous PMDA scrutiny with an aging pet population, spawning steady antibody uptake. India adopts an online regulatory portal that signals future acceleration once cold-chain gaps narrow.

Latin America, the Middle East, and Africa collectively remain nascent but improving. Brazil and Saudi Arabia champion higher-end veterinary clinics that stock biologics, while South Africa leads Sub-Saharan adoption. Long-haul supply chains and intermittent power supply challenge cold-storage integrity, restricting near-term volume but prompting local fill-finish investments slated for completion after 2027.

Competitive Landscape

Market Concentration

The market for monoclonal antibodies in veterinary health is highly consolidated due to the high competitiveness and limited number of players. The monoclonal antibodies in veterinary health market features an oligopolistic top tier and a vibrant cohort of platform biotechs. Zoetis dominates on the strength of Librela and Solensia, supported by a global diagnostic-lab network that feeds post-marketing surveillance and reinforces veterinary confidence. Merck Animal Health’s USD 895 million Kansas expansion underscores the capital intensity required to scale GMP suites for veterinary doses. Boehringer Ingelheim’s animal-health division leverages virus-like-particle know-how acquired through Saiba to enter immune-oncology faster.

Elanco is repositioning through a USD 130 million biologics campus designed to cut cycle times for canine and feline antibodies. Dechra’s acquisition of Invetx expands half-life-extension IP, giving the mid-cap player longer patent tails and fewer injections per treatment course. OmniAb licenses transgenic-animal platforms to more than 80 partners, generating a royalty stream while seeding the next wave of assets.

AI collaborations add another competitive dimension. Absci applies generative algorithms to de-risk affinity maturation while predicting manufacturability, letting partners advance candidates with built-in developability scores. CDMOs courting veterinary clients tout platform readiness levels now comparable to human programs, compressing time from cell-line development to engineering runs to under six months. Collectively, these moves elevate entry barriers and favor firms with integrated discovery-to-commercial capabilities.

Monoclonal Antibodies In Veterinary Health Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Absci Corporation and Invetx announced a strategic partnership to develop a generative AI drug creation platform specifically for animal health applications, focusing on half-life extension technology for monoclonal antibodies targeting canines with potential expansion to other companion animals.

- May 2025: Merck Animal Health and the State of Kansas announced an USD 895 million investment in manufacturing and research & development facilities in De Soto, aimed at enhancing veterinary monoclonal antibody production capabilities and supporting future biologics development.

- August 2024: Elanco Animal Health Incorporated has revealed plans for a 25,000-sq. ft expansion of its biologics manufacturing site in Kansas, United States. This anticipated USD 130 million investment, set to be completed by 2026, aims to enhance the company's monoclonal antibody (mAb) platform for canine parvovirus monoclonal antibody (CPMA), leveraging the existing strong expertise at this facility.

- July 2024: Invetx Inc. introduced its agreement to be acquired by Dechra Pharmaceuticals Limited (Dechra) for up to USD 520 million on a cash-free and debt-free basis. This acquisition aims to enhance the portfolio of high-value monoclonal antibody therapeutics for companion animals.

Table of Contents for Monoclonal Antibodies In Veterinary Health Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Burden of Chronic Disorders Among Companion Animals

- 4.2.2Increasing Pet Ownership & Expenditure on Advanced Care

- 4.2.3Rapid Approval Pipeline of Novel Veterinary mAbs

- 4.2.4Favourable USDA/EMA Fast-Track Pathways for Biologics

- 4.2.5Expansion of Dedicated CDMO Capacity for Vet-mAbs

- 4.2.6AI-Driven Precision-Dosing Platforms Boosting Efficacy

- 4.3Market Restraints

- 4.3.1High Cost of Development & Therapy

- 4.3.2Complex Multi-Jurisdictional Regulatory Compliance

- 4.3.3Weak Cold-Chain Logistics in Emerging Markets

- 4.3.4Competition from Long-Acting Small-Molecule Analgesics

- 4.4Regulatory Landscape

- 4.5Porter’s Five Forces Analysis

- 4.5.1Threat of New Entrants

- 4.5.2Bargaining Power of Buyers

- 4.5.3Bargaining Power of Suppliers

- 4.5.4Threat of Substitutes

- 4.5.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value in USD)

- 5.1By Animal Type

- 5.1.1Dogs

- 5.1.2Cats

- 5.1.3Horses

- 5.1.4Livestock

- 5.1.4.1Cattle

- 5.1.4.2Swine

- 5.1.4.3Poultry

- 5.1.5Others

- 5.2By Application

- 5.2.1Dermatology

- 5.2.2Osteoarthritis & Pain Management

- 5.2.3Oncology

- 5.2.4Infectious Diseases

- 5.2.5Immunological Disorders

- 5.2.6Others

- 5.3By End User

- 5.3.1Veterinary Hospitals & Clinics

- 5.3.2Academic & Research Institutes

- 5.3.3Others

- 5.4By Geography

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.2Europe

- 5.4.2.1Germany

- 5.4.2.2United Kingdom

- 5.4.2.3France

- 5.4.2.4Italy

- 5.4.2.5Spain

- 5.4.2.6Rest of Europe

- 5.4.3Asia-Pacific

- 5.4.3.1China

- 5.4.3.2Japan

- 5.4.3.3India

- 5.4.3.4Australia

- 5.4.3.5South Korea

- 5.4.3.6Rest of Asia-Pacific

- 5.4.4Middle East & Africa

- 5.4.4.1GCC

- 5.4.4.2South Africa

- 5.4.4.3Rest of Middle East & Africa

- 5.4.5South America

- 5.4.5.1Brazil

- 5.4.5.2Argentina

- 5.4.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Zoetis Inc.

- 6.3.2Merck Animal Health

- 6.3.3Elanco Animal Health Inc.

- 6.3.4Boehringer Ingelheim Vetmedica GmbH

- 6.3.5Virbac SA

- 6.3.6Indian Immunologicals Ltd.

- 6.3.7Ceva Santé Animale

- 6.3.8Dechra Pharmaceuticals PLC

- 6.3.9Nextmune AB

- 6.3.10Kindred Biosciences, Inc.

- 6.3.11Invetx, Inc.

- 6.3.12Bayer Animal Health GmbH

- 6.3.13PetMedix Ltd.

- 6.3.14Aratana Therapeutics, Inc.

- 6.3.15Torigen Pharmaceuticals, Inc.

- 6.3.16AbCellera Biologics Inc.

- 6.3.17Orion Corp. (Animal Health)

- 6.3.18Northway Biotech CDMO

- 6.3.19Bioatla LLC

- 6.3.20Advio GmbH

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the veterinary monoclonal antibody market as all prescription biologic therapies built on monoclonal antibodies that are already approved or in late-stage regulatory review for systemic or local treatment of companion animals and production livestock across major regions. The value reflects ex-manufacturer revenues, net of typical channel discounts, for therapeutic doses supplied through veterinary hospitals, clinics, and licensed pharmacies.

Scope exclusion: diagnostic antibody kits and early-stage research reagents lie outside this assessment.

Segmentation Overview

- By Animal Type

- Dogs

- Cats

- Horses

- Livestock

- Cattle

- Swine

- Poultry

- Cattle

- Others

- Dogs

- By Application

- Dermatology

- Osteoarthritis & Pain Management

- Oncology

- Infectious Diseases

- Immunological Disorders

- Others

- Dermatology

- By End User

- Veterinary Hospitals & Clinics

- Academic & Research Institutes

- Others

- Veterinary Hospitals & Clinics

- By Geography

- North America

- United States

- Canada

- Mexico

- United States

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Germany

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- China

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- GCC

- South America

- Brazil

- Argentina

- Rest of South America

- Brazil

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed practicing veterinarians, regulatory reviewers, procurement leads at hospital chains, and R&D executives across North America, Europe, and Asia-Pacific. These discussions helped us validate treatment penetration, average selling prices, probable launch timelines, and the practical constraints that were flagged during desk work.

Desk Research

We began by screening open regulatory databases such as the FDA Center for Veterinary Medicine, the EMA Union Product Database, and Japan's PMDA for product approvals, then matched those findings with import-export tallies from UN Comtrade and animal health spending tables issued by USDA and Eurostat. Next, our team pulled companion animal population counts and disease prevalence surveys from associations such as AVMA and FEDIAF, combining them with peer-reviewed incidence studies covering atopic dermatitis, osteoarthritis, and oncology.

Company 10-Ks, investor decks, and selected press releases were captured through Dow Jones Factiva, while D&B Hoovers supplied revenue splits that hinted at price bands and shipment volumes. The sources above are illustrative only; many additional references informed data collection, cross-checks, and contextual understanding.

Market-Sizing & Forecasting

A top-down demand pool was built from regional dog, cat, equine, and livestock counts, multiplied by published prevalence rates and by interview-verified treatment uptake. Select bottom-up roll-ups, sampled manufacturer sales, hospital purchase audits, and course-cost benchmarks were layered to align totals. Core variables include animal population growth, chronic disease shift, approval cadence, average treatment duration, and price erosion. Multivariate regression checked by ARIMA trend tests generates the 2025-2030 trajectory, while scenario analysis stress-tests extreme adoption or pricing swings.

Data Validation & Update Cycle

Outputs pass a two-level analyst review; any variance against historical series or peer indicators triggers re-contact with respondents. Models refresh once a year, with interim updates released for material events such as a major approval or safety recall, and an analyst reruns the latest numbers before every client delivery.

Why Mordor's Monoclonal Antibodies In Veterinary Health Baseline Earns Decision-Makers' Confidence

Benchmark comparison

Published estimates often diverge because firms apply different animal coverage, price references, and refresh cadences.

Key gap drivers include whether pipeline drugs are counted, single-region anchoring that misstates global totals, and unverified ASP growth assumptions. By contrast, Mordor applies balanced scope choices, mixed-method validation, and an annual refresh that keeps figures current.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 1.17 B (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 1.38 B (2025) | Global Consultancy A | Excludes livestock yet assumes higher ASP for pets | ||

USD 1.70 B (2025) | International Publisher B | Counts only approved drugs and converts sales at constant 2023 FX rates |