Veterinary Antibiotics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

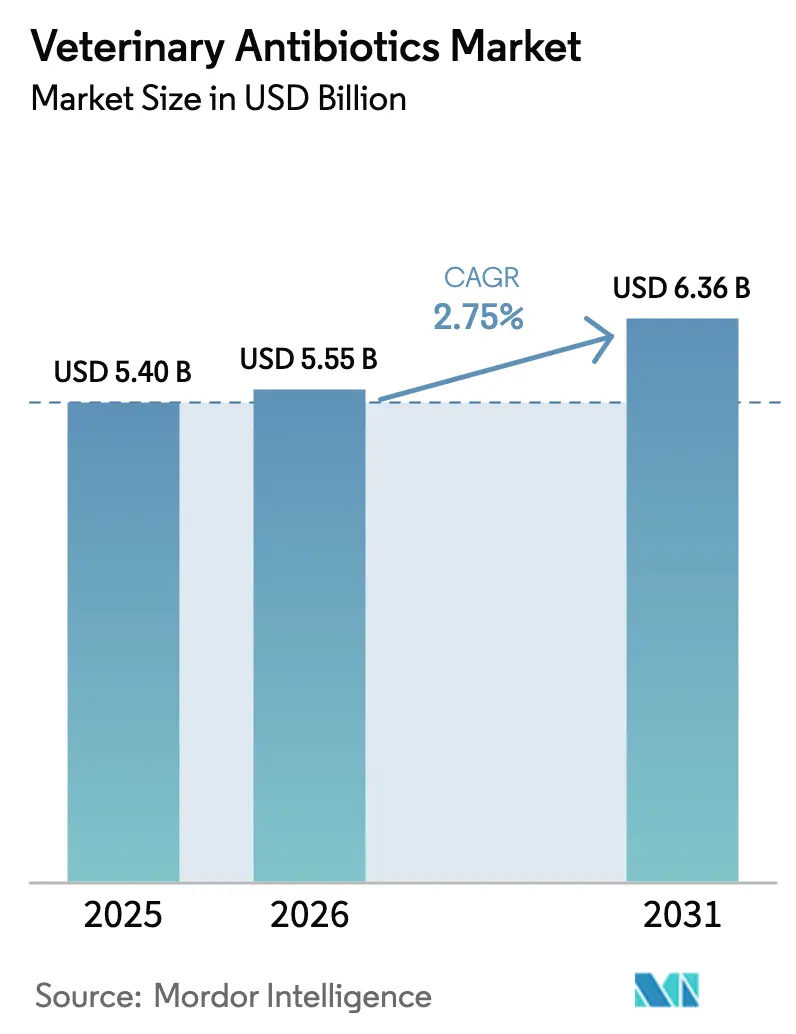

| Market Size (2026) | USD 5.55 Billion |

| Market Size (2031) | USD 6.36 Billion |

| Growth Rate (2026 - 2031) | 2.75% CAGR |

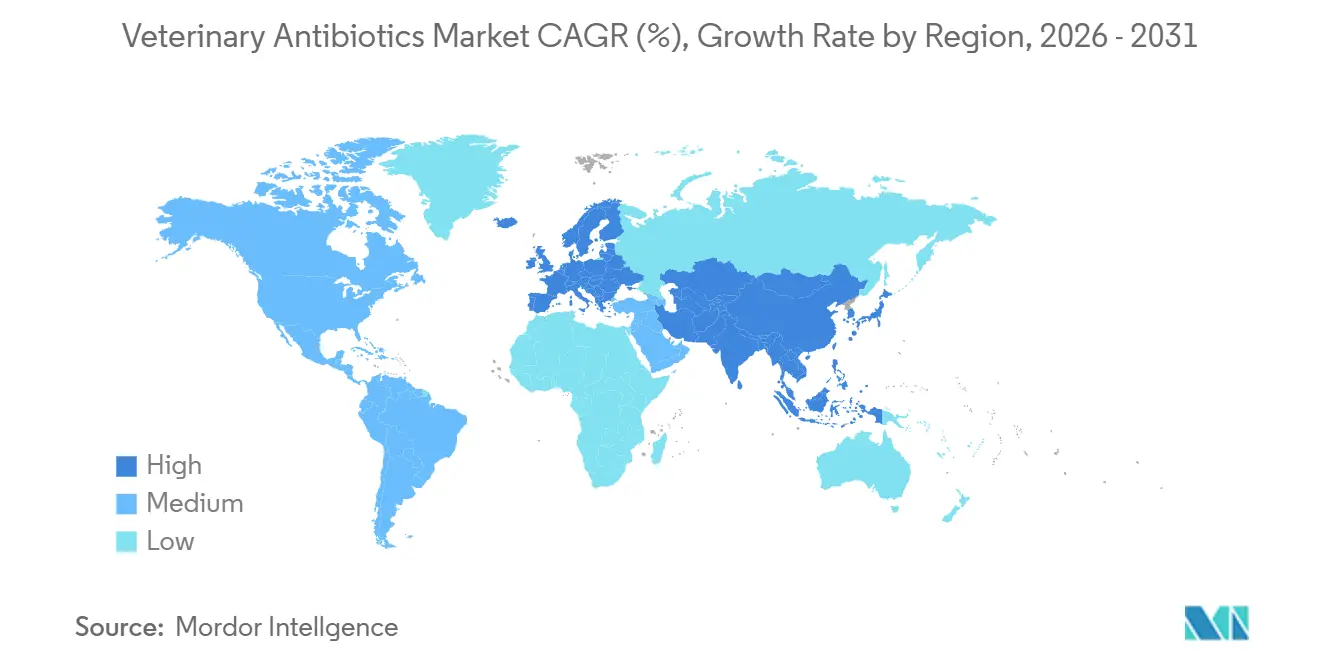

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

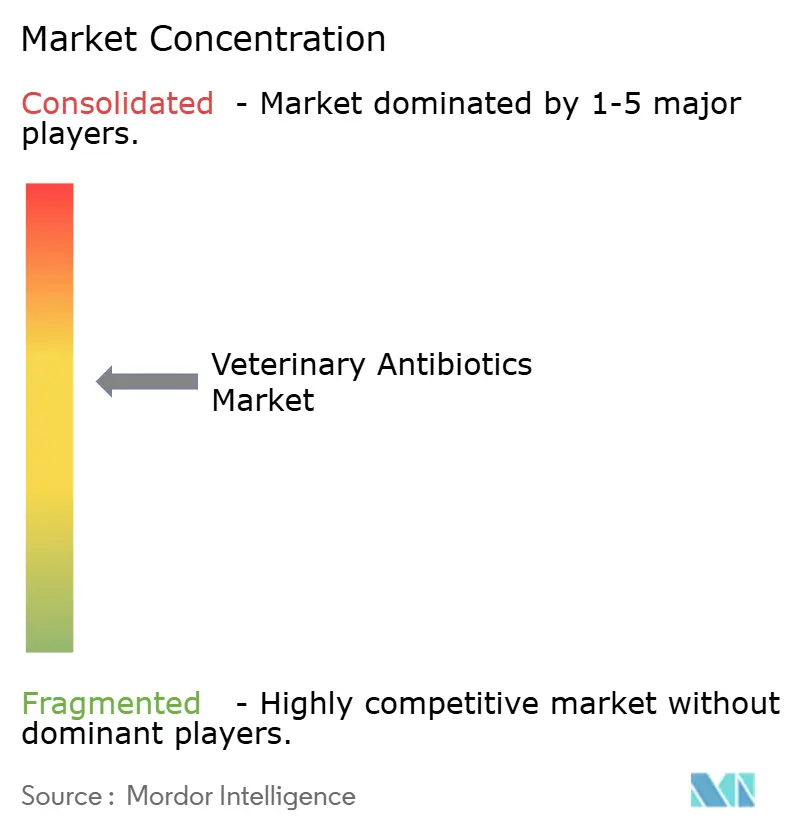

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veterinary Antibiotics Market Analysis by Mordor Intelligence

The veterinary antibiotics market size was valued at USD 5.40 billion in 2025 and is estimated to grow from USD 5.55 billion in 2026 to reach USD 6.36 billion by 2031, at a CAGR of 2.75% during the forecast period. Demand is fragmenting as antimicrobial-resistance stewardship pushes veterinarians toward narrow-spectrum, animal-only molecules while emerging aquaculture hubs maintain high usage of broad-spectrum products[1]European Medicines Agency, “Veterinary Regulatory – Antimicrobial Resistance,” ema.europa.eu . North America currently anchors premium spending, but Asia-Pacific is accelerating on the back of China’s livestock genotyping programs, and India’s dairy intensification plans[2]Reuters Staff, “Healthcare & Pharmaceuticals,” reuters.com . Drug-class realignment is visible as tetracyclines face wastewater-compliance headwinds even as aminoglycosides win share in companion-animal practice. Delivery innovations for heat-stable premixes and long-acting injectables are gaining traction because they reduce labor dependence in regions struggling with veterinarian shortages.

Key Report Takeaways

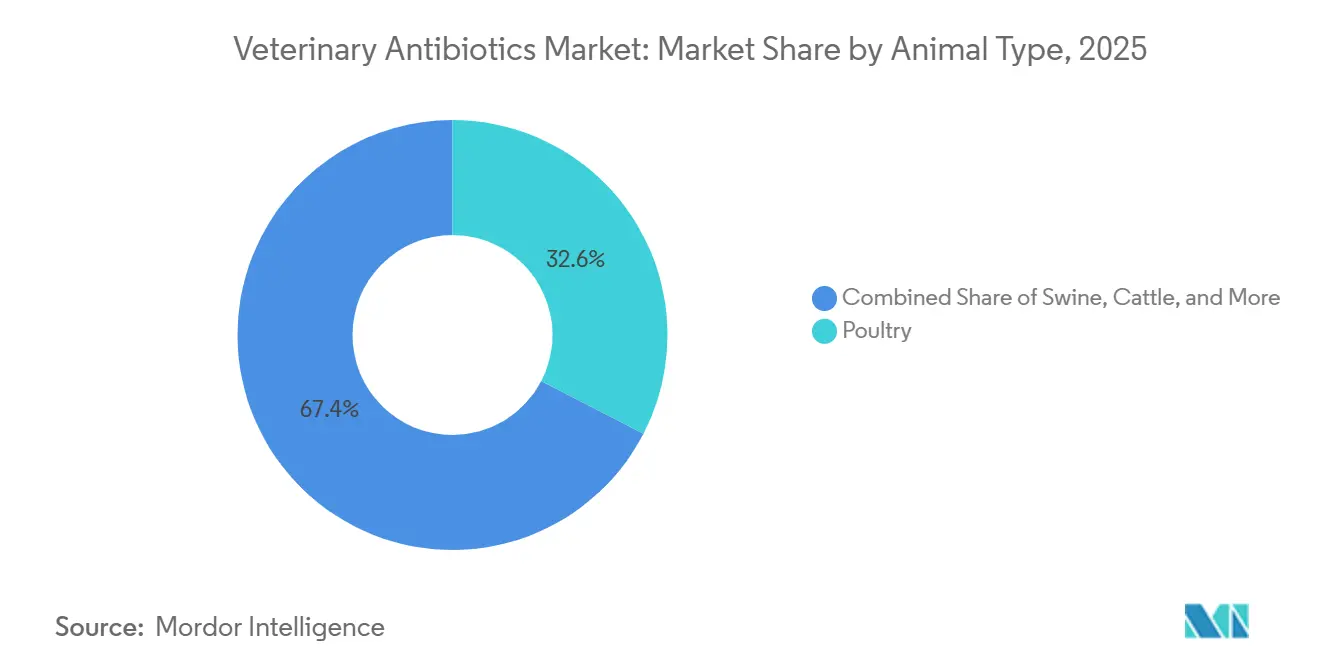

- By animal type, poultry accounted for 32.55% of the veterinary antibiotics market in 2025, while aquaculture is forecast to expand at a 6.85% CAGR through 2031.

- By drug class, tetracyclines commanded 28.53% of the veterinary antibiotics market share in 2025, and aminoglycosides are advancing at a 6.75% CAGR to 2031.

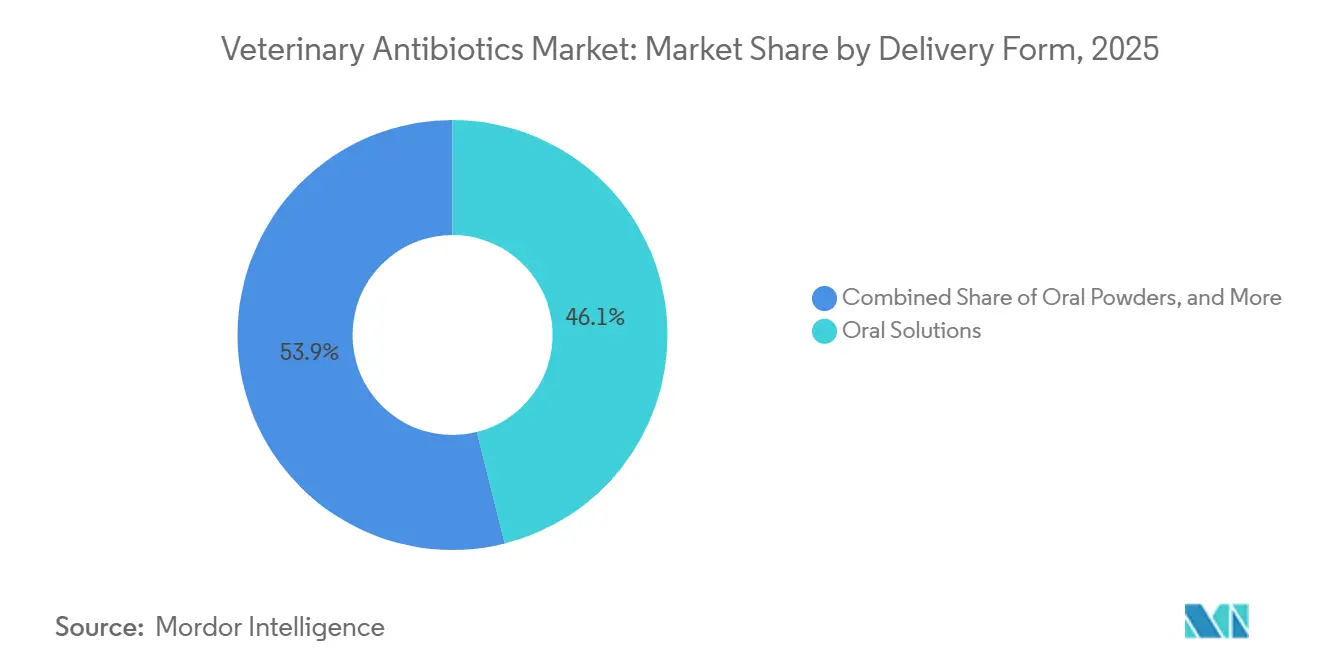

- By delivery form, oral solutions led with 46.15% revenue share in 2025; premixes are projected to grow at a 7.82% CAGR during the forecast window.

- By spectrum of activity, broad-spectrum products represented 66.32% of sales in 2025, whereas narrow-spectrum formulations are increasing at a 6.19% CAGR.

- By end user, food-producing animal producers accounted for 72.21 of % demand in 2025, yet companion-animal owners are rising at a 5.56% CAGR to 2031.

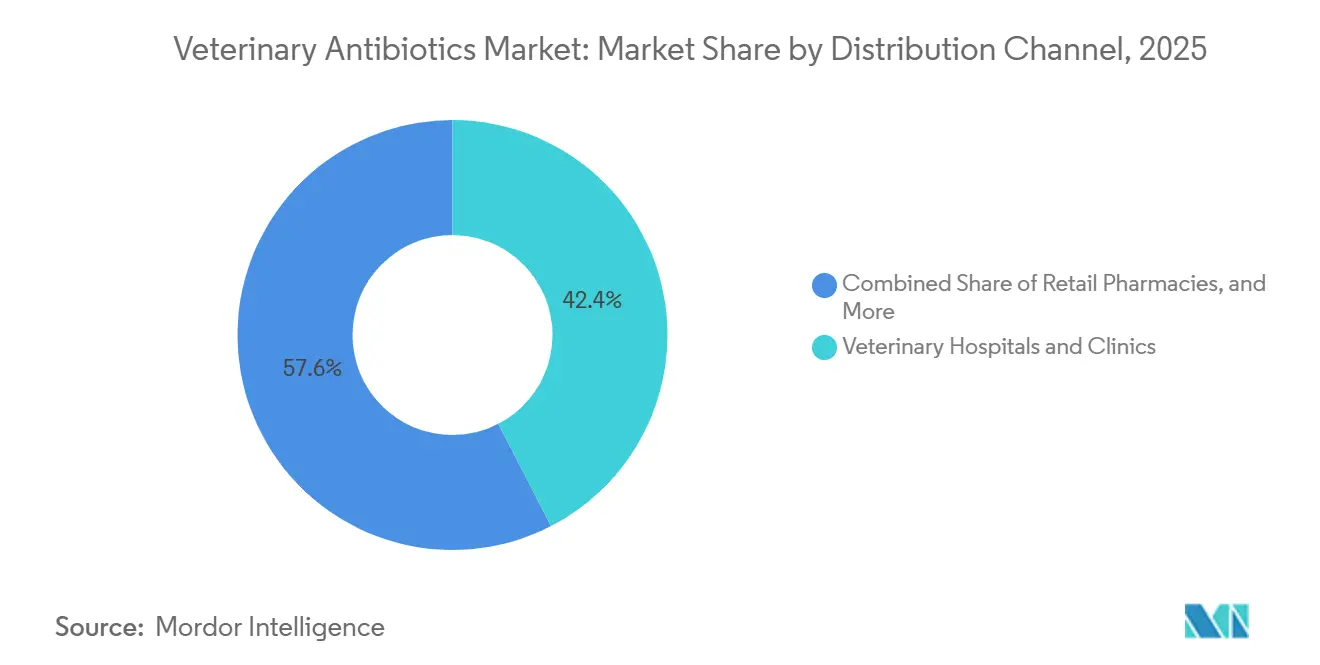

- By distribution channel, veterinary hospitals and clinics captured a 42.42% share in 2025; the online segment is climbing at a 6.32%.

- By geography, North America dominated with 32.52% share in 2025, whereas Asia-Pacific is set to grow at a 6.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Veterinary Antibiotics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Global Demand for Animal-Source Protein Post-Pandemic | +1.2% | Global, Asia-Pacific, Latin America | Medium term (2-4 years) |

| Rebound in Companion-Animal Ownership and Veterinary Expenditure | +0.8% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Regulatory Shift Toward Animal-Only Antibiotic Classes | +0.6% | North America, EU, Australia | Long term (≥ 4 years) |

| Expansion of Injectable, Heat-Stable Long-Acting Formulations | +0.5% | North America, Latin America, India | Medium term (2-4 years) |

| Livestock Genotyping and On-Farm Diagnostics for Precision Dosing | +0.4% | North America, China, EU | Long term (≥ 4 years) |

| Unmonitored Antibiotic Use in ASEAN Aquaculture | +0.9% | Southeast Asia, Bangladesh | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Global Demand for Animal-Source Protein Post-Pandemic

Global meat output rebounded in 2025 with poultry volumes up 4.2% and pork up 3.8% as restaurants reopened and exports recovered[3]Food and Agriculture Organization, “World Food Situation – Meat,” fao.org. Producers in Asia-Pacific and Latin America expanded intensive operations to serve China and Middle Eastern importers, increasing prophylactic antibiotic use in broiler and finishing pig systems. Developed markets are channelling growth into narrow-spectrum, prescription-only therapies, whereas emerging economies still rely on over-the-counter broad-spectrum formulations. This demand bifurcation is shifting volume from highly regulated regions to countries with limited enforcement, sustaining baseline growth for the veterinary antibiotics market. However, mounting scrutiny from global retailers is pressuring exporters to adopt stewardship protocols, accelerating the transition to animal-only molecules.

Rebound in Companion-Animal Ownership & Veterinary Expenditure

The United States recorded 67% household pet ownership in 2025, up four percentage points from 2023, and per-pet veterinary spend rose 6.1% annually during 2024-2025[4]American Pet Products Association, “Pet Ownership Statistics,” americanpetproducts.org . Similar patterns emerged in Europe and urban Asia-Pacific. Diagnostics-guided prescribing in clinics is favouring aminoglycosides and first-generation cephalosporins, narrowing demand for broad-spectrum fluoroquinolones. Online pharmacies linked to tele-veterinary platforms are capturing prescription refills, although state-level telemedicine rules in the U.S. and cross-border licensing limits in the EU temper the scale. The resulting growth in the companion sector underpins premium pricing resilience for the veterinary antibiotics market.

Regulatory Shift Toward Animal-Only Antibiotic Classes

The FDA’s 2024 guidance and Europe’s 2024 Veterinary Medicinal Products Regulation prioritise ionophores and pleuromutilins for livestock use, restricting medically important human antibiotics. U.S. broilers have widely replaced bacitracin with ionophores, while swine producers are adopting pleuromutilins in respiratory-disease protocols. Innovators with proprietary animal-only pipelines are capturing price premiums of 15-20%. Conversely, generic producers reliant on tetracyclines and macrolides face volume erosion and higher compliance costs, reshaping the competitive landscape of the veterinary antibiotics market.

Expansion of Injectable, Heat-Stable Long-Acting Formulations in Ruminants

Long-acting injectables delivering seven-to fourteen-day therapeutic windows reduce labor and animal-handling stress in beef and dairy chains. Boehringer Ingelheim’s tulathromycin formulation, shelf-stable at 30 °C for 24 months, removes cold-chain hurdles for tropical markets and has lifted Latin American sales by 18% year-over-year. India’s smallholder dairies value the single-dose convenience, although uptake is constrained by 40-60% price premiums over oral generics. The gradual shift from daily drenches to depot injections signals a structural move toward value-added formulations inside the veterinary antibiotics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening AMR Regulations Reducing Group Treatments | -0.7% | EU, North America, Australia, spillover to Latin America, Asia-Pacific | Medium term (2-4 years) |

| Rapid Penetration of Probiotic / Phage Growth-Promoter Alternatives | -0.5% | EU, North America, Japan | Long term (≥ 4 years) |

| Chronic Shortage of Rural Veterinarians and Skilled Farm Labor | -0.4% | Global, acute in rural North America, sub-Saharan Africa, South Asia | Medium term (2-4 years) |

| EU Wastewater and ERA Rules Lifting Compliance Costs for Generics | -0.3% | EU, indirect on Indian and Chinese suppliers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tightening AMR Regulations Reducing Group Treatments

The EU’s 2024 prophylaxis ban cut antibiotic volumes 8-10% in Denmark and the Netherlands. The U.S. Veterinary Feed Directive extension eliminated over-the-counter in-feed medication, shaving 30% from historical broiler and hog demand. These shifts curb broad-spectrum tetracycline and sulfonamide sales but raise costs for smallholders that must now secure prescriptions, adding USD 2-4 per head in swine and USD 0.10 per broiler. The result is slower growth for the veterinary antibiotics market in mature regions.

Rapid Penetration of Probiotic / Phage Growth-Promoter Alternatives

Retailer mandates for “antibiotic-free” labels spurred Cargill’s Bacillus probiotic rollout across U.S. broilers, matching feed-conversion gains once attributed to bacitracin. FDA approval of bacteriophage cocktails targeting Salmonella and E. coli is expected by 2026, threatening 3-5% of metaphylactic demand. Yet phage manufacturing costs remain two to three times higher than generics, and strain specificity limits field efficacy. While alternatives erode volume, pricing power in premium-label meat offsets part of the drag on the veterinary antibiotics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Animal Type: Aquaculture Gains Momentum While Poultry Plateaus

The veterinary antibiotics market for poultry accounted for 32.55% of global revenue. Regulatory pressure in the EU and North America is capping prophylactic usage, and ionophore substitution is maturing. In contrast, aquaculture generated only USD 0.62 billion but is advancing at a 6.85% CAGR as Southeast Asian shrimp and tilapia farms continue unmonitored antibiotic dosing. The divergence underscores how enforcement intensity steers volume across species.

Growth in aquaculture is driven by high disease incidence and limited approved fish-specific formulations, prompting farmers to use livestock drugs off-label. Swine demand remains steady as precision-dose pleuromutilins replace bulk tetracyclines, and cattle uptake is bifurcated between long-acting injectables in beef feedlots and intramammary tubes in dairies. Companion-animal antibiotic sales climb on the back of rising pet ownership, with aminoglycosides gaining share for urinary tract infections. Sheep and goats remain niche, reflecting limited commercial farming outside the Mediterranean and Middle-East belts.

By Drug Class: Aminoglycosides Accelerate Amid Tetracycline Headwinds

Tetracyclines accounted for 28.53% of 2025 revenue, making them the largest share of the veterinary antibiotics market. Wastewater discharge limits and feed directives, however, are trimming metaphylactic use. Aminoglycoside revenue stood at USD 0.68 billion and is set to grow at a 6.75% CAGR to 2031, as veterinarians favor gentamicin and amikacin for companion-animal respiratory and urinary infections.

Penicillins and first-generation cephalosporins sustain demand in dairy mastitis protocols, while third-generation cephalosporins face “reserve” designations. Macrolides, spearheaded by tulathromycin, gain in bovine respiratory disease owing to long-acting injectables. Fluoroquinolone volumes contract following aquaculture bans in China and tightened EU rules, and sulfonamide share erodes as combination therapies pack higher efficacy at lower doses.

By Delivery Form: Premixes Surge Through Feed-Mill Integration

Oral solutions contributed 46.15% of 2025 sales, benefiting from flexible dosing via waterlines in poultry and swine. Premixes are witnessing a 7.82% CAGR as integrated feed mills embed microencapsulated actives that survive 85 °C pelleting. This shift streamlines compliance, enabling mill-level veterinary oversight and precise inclusion rates.

Injectables are gaining favor in ruminants due to labor savings from single-dose regimes. Intramammary and intra-uterine tubes see incremental innovation through sustained-release matrices that hold therapeutic levels for up to 96 hours. Oral powders decline as producers migrate to dust-free liquids compatible with automated medicators.

By Spectrum of Activity: Stewardship Pushes Narrow-Spectrum Uptake

Broad-spectrum products generated USD 3.58 billion in 2025, but stewardship guidelines and point-of-care diagnostics are steering practitioners toward targeted agents. Narrow-spectrum revenue is projected to rise at 6.19% CAGR, led by ionophores for coccidiosis prevention and pleuromutilins for swine respiratory complexes.

Companion-animal clinics increasingly rely on culture-and-sensitivity testing, reducing empirical fluoroquinolone prescriptions. In livestock, regulatory fines for non-compliance and residue rejections at export markets are accelerating the pivot, reinforcing the structural evolution of the veterinary antibiotics market.

By End User: Companion-Animal Owners Lift Premium Spending

Food-animal producers have 72.21% in 2025, but tightening AMR rules and alternative growth promoters are moderating growth. The companion cohort is expanding at a 5.56% CAGR as pet humanization boosts demand for diagnostics-led, narrow-spectrum treatments.

Large-scale integrators with in-house veterinarians gain purchasing leverage and absorb compliance costs more easily than smallholders. In aquaculture, fragmented farm structures and limited vet access perpetuate informal sourcing, complicating stewardship efforts.

By Distribution Channel: Online Platforms Disrupt Traditional Retail

Veterinary hospitals and clinics dispensed 42.42% worth of antibiotics in 2025, retaining trust-based purchasing dynamics. Online channels are expanding 6.32% CAGR as tele-veterinary services integrate e-prescriptions and direct-to-farm delivery.

Retail pharmacies face declining share due to prescription mandates, while feed mills emerge as specialised channels for premix products. Regulatory fragmentation remains a drag on pan-regional e-pharmacy scale, but convenience and price transparency sustain digital momentum.

Geography Analysis

North America, accounting for 32.52% of 2025 revenue, is expected to decline due to veterinary feed directive curbs on over-the-counter sales and a rural veterinarian shortage, which limits prescription bandwidth. Nevertheless, premium companion-animal spending and uptake of long-acting injectables for feedlot cattle underpin stable margins.

Asia-Pacific projected to climb 6.12% CAGR to 2031. China’s genotyping mandates and India’s dairy upgrades lift narrow-spectrum demand, while under-regulated aquaculture corridors in Southeast Asia continue broad-spectrum purchases via informal networks. Regulatory gaps facilitate volume growth but raise residual risks for exporters facing stricter EU entry requirements.

Europe is navigating aggressive AMR and wastewater standards that elevate compliance costs. Generic manufacturer consolidation is underway, as smaller firms exit rather than fund EUR 0.2-0.5 million ERA dossiers. Latin America records varied trajectories: Brazil’s export-oriented integrators align with importing-country protocols, while domestic producers continue to use OTC. The Middle East and Africa together contribute significant revenue but remain fragmented; Gulf states import premium formulations, whereas sub-Saharan markets depend on generics sold through co-ops with limited vet oversight.

Competitive Landscape

The top five companies, Zoetis, Elanco, Boehringer Ingelheim, Merck Animal Health, and Ceva, captured a significant share of the 2025 global revenue, reflecting moderate concentration. Innovators emphasize animal-only classes and sustained-release technologies that command premium prices and align with stewardship mandates. Generic players are squeezed by EU wastewater compliance and shrinking metaphylactic volumes, prompting mergers or departures, especially among Indian and Chinese exporters.

Strategic differentiation now hinges on diagnostic integration; Elanco’s 2025 alliance with a Dutch PCR firm packages rapid testing kits alongside its pleuromutilin portfolio, supporting data-driven prescriptions. Boehringer Ingelheim’s heat-stable tulathromycin addresses logistical gaps in tropical markets, while Zoetis leverages its companion-animal franchise to cross-fund R&D in food-animal pipelines. Emerging disruptors such as Cargill’s probiotics and phage-therapy start-ups nibble at the metaphylactic market but face scalability and cost hurdles.

Aquaculture-specific product development remains a white-space opportunity: the absence of labelled antibiotics for shrimp and tilapia perpetuates off-label use, offering upside for companies that can navigate stringent residue thresholds. Tele-veterinary-enabled distribution is another frontier, particularly in sub-Saharan Africa and South Asia where veterinarian density is chronically low.

Veterinary Antibiotics Industry Leaders

Zoetis

Boehringer Ingelheim

Merck Animal Health

Elanco

Ceva Santé Animale

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Dechra launched Solovecin (cefovecin sodium), a long-acting injectable for canine and feline skin infections in the United States.

- May 2025: Merck Animal Health received FDA approval for MOMETAMAX SINGLE, a single-dose otic suspension combining gentamicin, posaconazole, and mometasone furoate for dogs.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the veterinary antibiotics market as the global revenue earned from prescription-strength antibacterial drugs formulated exclusively for animals and supplied as premixes, oral powders, oral solutions, injections, intramammary or intra-uterine infusions, and feed-additive blends for livestock and companion species; we align every figure to ex-factory prices before taxes.

Scope exclusion: Products such as nutraceuticals, ionophore coccidiostats, antivirals, antifungals, probiotic feed additives, and compounded preparations remain outside the baseline.

Segmentation Overview

- By Animal Type

- Poultry

- Swine

- Cattle

- Sheep & Goats

- Companion Animals

- Aquaculture

- Other Livestock

- By Drug Class

- Tetracyclines

- Penicillins

- Sulfonamides

- Macrolides

- Aminoglycosides

- Cephalosporins

- Fluoroquinolones

- Others

- By Delivery Form

- Premixes

- Oral Powders

- Oral Solutions

- Injections

- Intramammary & Intra-uterine

- Feed-Additive Blends

- By Spectrum of Activity

- Broad-Spectrum

- Narrow-Spectrum

- By End User

- Food-Producing Animal Producers

- Companion-Animal Owners

- By Distribution Channel

- Veterinary Hospitals & Clinics

- Retail Pharmacies

- Online Channels

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed practicing veterinarians, farm-integrator procurement leads, wholesale distributors, and regulatory officers across the United States, Brazil, Germany, China, and India. These conversations confirmed typical treatment course volumes, off-label substitution trends, and the real-world impact of antimicrobial-resistance rules, thereby filling gaps that documents alone could not bridge.

Desk Research

We begin with livestock population and slaughter statistics from FAO, USDA, Eurostat, and national ministries, then match usage norms drawn from WOAH and ESVAC surveillance reports. Trade flows from UN Comtrade, import tariff filings, and patent families mined in Questel signal regional supply capacity. Company 10-Ks, investor decks, peer-reviewed articles in Frontiers in Veterinary Science, and news archives in Dow Jones Factiva or D&B Hoovers refine price bands and pipeline outlooks.

Additional triangulation comes from association white papers (Health for Animals, AVMA) and customs shipment trackers such as Volza. The sources cited illustrate our approach and are not exhaustive; numerous other public and paid references informed desk work.

Market-Sizing & Forecasting

A top-down model converts animal-inventory data into demand pools through species-level disease incidence, treatment penetration, and average-course dosage, then values them using blended selling prices. Supplier revenue roll-ups and sampled channel checks provide bottom-up reasonableness tests. Key variables include headcount growth, pet-ownership ratios, regulatory intensity scores, course-cost inflation, and export share of veterinary drugs, each forecast with multivariate regression supported by expert consensus. When bottom-up sums deviate beyond a tolerance band, we adjust dosage or ASP assumptions transparently before lock-in.

Data Validation & Update Cycle

Outputs pass anomaly scans, senior-analyst review, and year-on-year variance checks. Reports refresh each year, with interim revisions triggered by material events such as new residue-limit laws or major disease outbreaks; a final pre-publication sweep ensures clients receive the latest view.

Why Our Veterinary Antibiotics Baseline Earns Stakeholder Confidence

Published estimates often differ because firms apply unique product scopes, pricing ladders, and update cadences. By anchoring to clearly stated antibacterial classes, harmonized price points, and an annual refresh, Mordor offers a dependable starting point for budget planning.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.22 B (2025) | Mordor Intelligence | N/A |

| USD 5.21 B (2025) | Regional Consultancy A | Mixes oral care products with antibiotic totals, inflating certain dosage forms |

| USD 5.26 B (2024) | Trade Journal B | Counts antivirals and antifungals, hence wider product scope |

| USD 2.34 B (2025) | Global Consultancy C | Excludes feed additives and bulk premixes, yielding a narrower view |

The comparison shows that scope choices, dosage-form inclusion, and refresh rhythms drive the widest gaps, while our disciplined variable selection and transparent adjustments keep Mordor's baseline balanced and repeatable for strategic decisions.

Key Questions Answered in the Report

What is the current value of the veterinary antibiotics market?

It was worth USD 5.55 billion in 2026 and is on track to reach USD 6.36 billion by 2031.

Which region is growing fastest?

Asia-Pacific is expanding at a 6.12% CAGR, led by China’s livestock upgrades and Southeast Asian aquaculture demand.

Which animal segment offers the highest growth?

Aquaculture shows the strongest outlook with a 6.85% CAGR through 2031.

How are regulations affecting antibiotic demand?

EU and U.S. stewardship rules are reducing broad-spectrum group treatments and steering use toward narrow-spectrum, animal-only classes.

Which delivery format is gaining the most traction?

Heat-stable premixes are rising 7.82% CAGR as feed-mill integration drives precision dosing at scale.

Page last updated on: