Companion Animal Ear Infection Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.83 Billion |

| Market Size (2031) | USD 1.25 Billion |

| Growth Rate (2026 - 2031) | 8.44% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Companion Animal Ear Infection Treatment Market Analysis by Mordor Intelligence

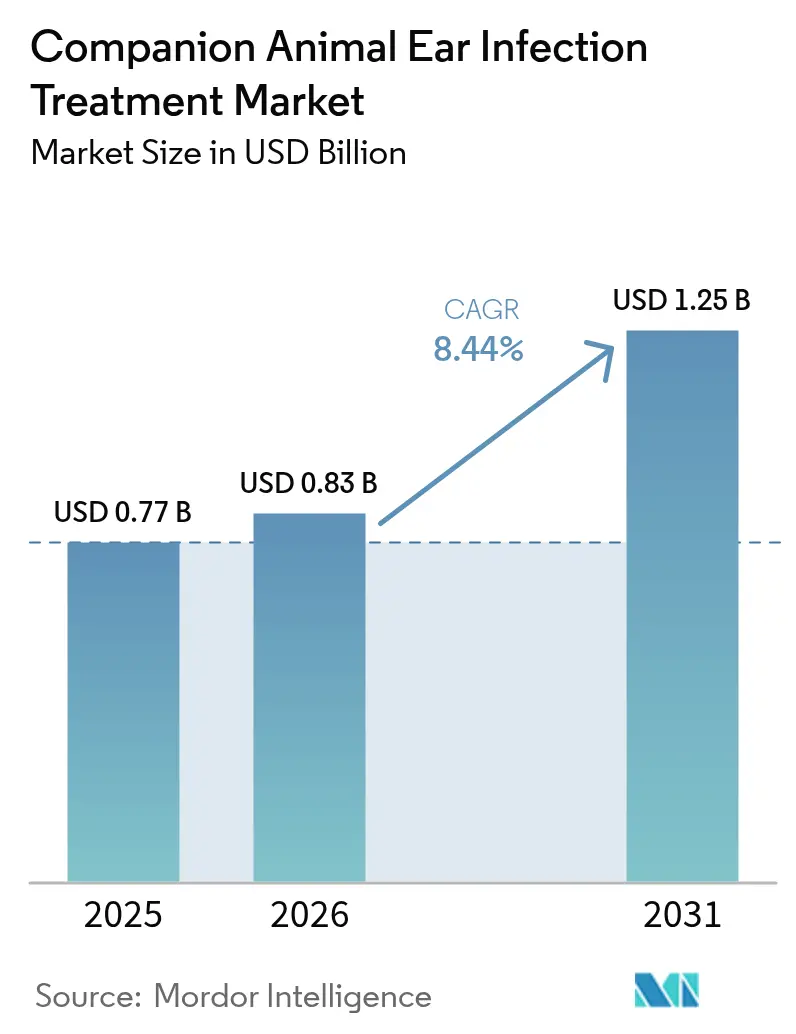

The Companion Animal Ear Infection Treatment Market size is expected to increase from USD 0.77 billion in 2025 to USD 0.83 billion in 2026 and reach USD 1.25 billion by 2031, growing at a CAGR of 8.44% over 2026-2031.

Demand holds steady even as overall veterinary spending has surged between 2023 and 2024 because owners now prioritize chronic‐condition therapies such as otic care over discretionary wellness visits. Three structural shifts underpin the outlook: antimicrobial resistance that pushes veterinarians toward higher-priced combination products, the normalization of pet telehealth that channels prescriptions to online pharmacies, and insurer-funded wellness plans that subsidize early diagnostics. These factors protect revenue streams during economic slowdowns, allowing the companion animal ear infection treatment market to decouple from broader clinic traffic patterns. Competitive intensity is rising as multinational incumbents race specialty challengers to launch long-acting otic delivery systems that guarantee compliance and curb resistance. Asia-Pacific urbanization further supports volume growth, while stewardship guidelines in North America and Europe reshape product mix toward narrow-spectrum agents and microbiome-stabilizing adjutants.

Key Report Takeaways

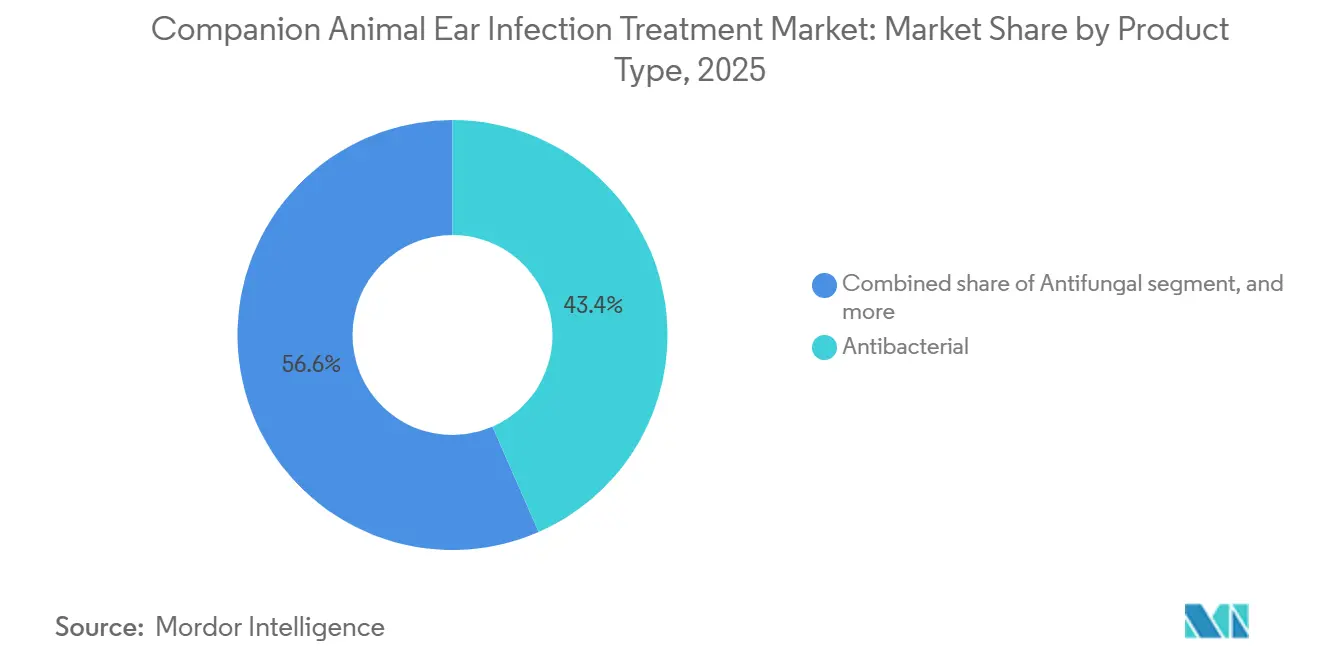

- By product type, antibacterial formulations led with 43.44% of the companion animal ear infection treatment market share in 2025, whereas antifungal agents are expanding at a 9.11% CAGR through 2031.

- By disease type, otitis externa accounted for 65.12% of the companion animal ear infection treatment market size in 2025, while otitis interna is advancing at a 9.25% CAGR through 2031.

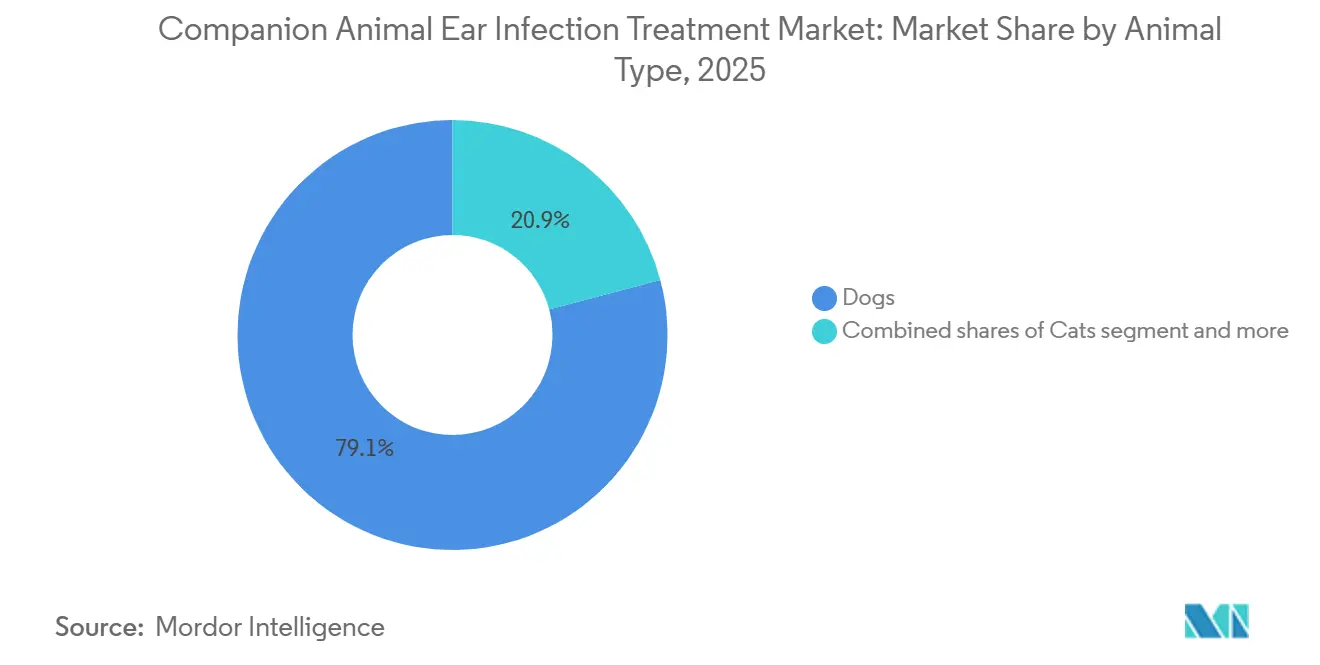

- By animal type, dogs captured 79.12% share of the companion animal ear infection treatment market size in 2025, whereas the feline segment is projected to grow at a 9.31% CAGR to 2031.

- By mode of administration, topical products dominated with 63.55% share in 2025, yet otic delivery systems are forecast to post the fastest 9.6% CAGR to 2031.

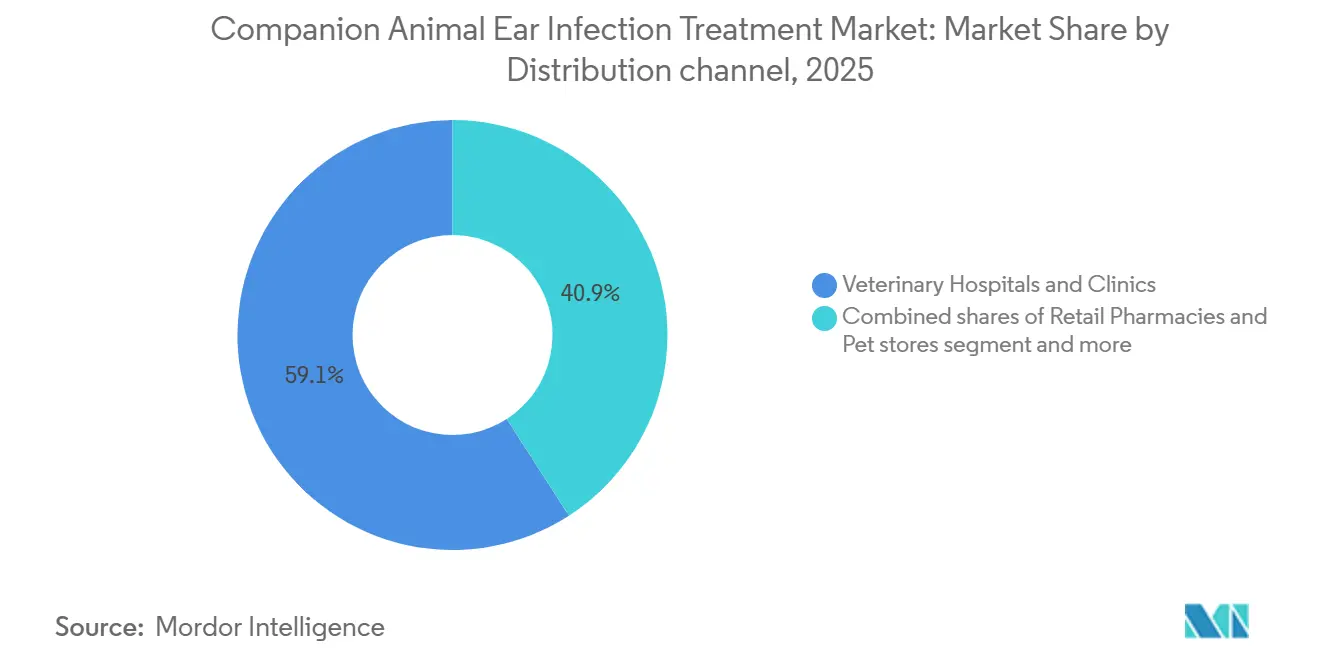

- By distribution channel, veterinary hospitals and clinics held 59.12% share in 2025, while online pharmacies are on course for a 9.12% CAGR through 2031.

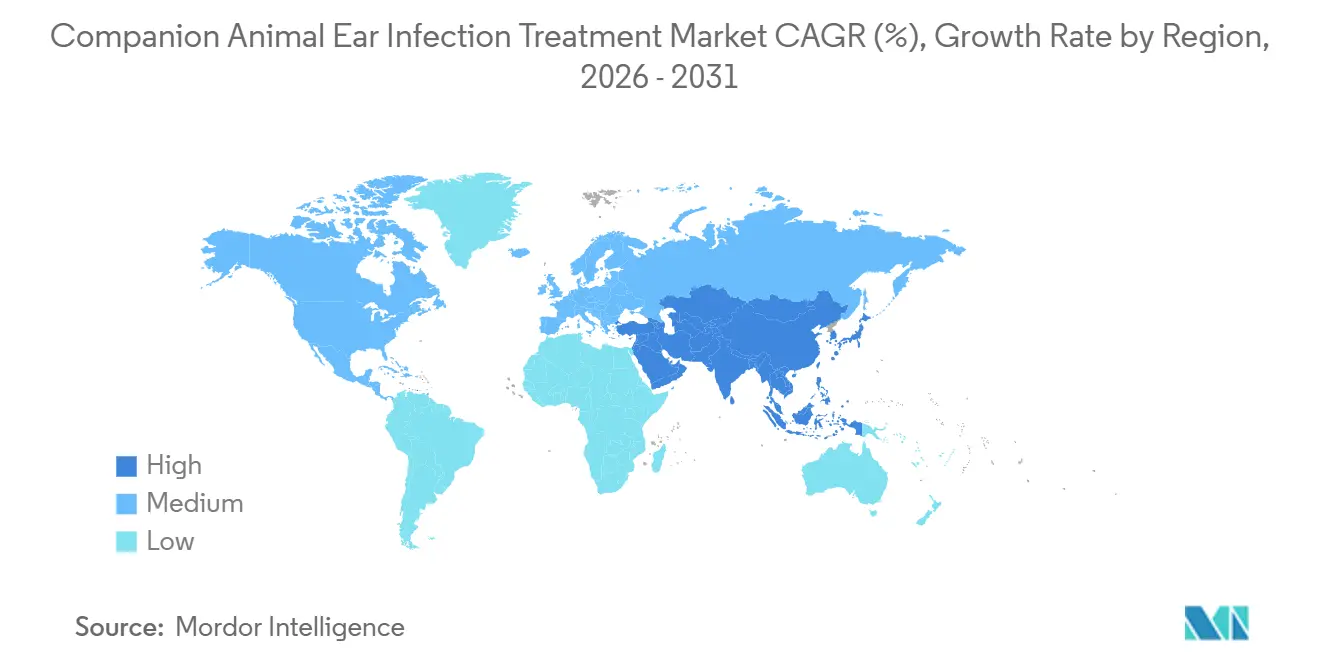

- By geography, North America led with 43.43% revenue share in 2025, whereas Asia-Pacific is the fastest-growing region at a 9.77% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Companion Animal Ear Infection Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Companion Animal Ownership Rates | +1.8% | Global, with APAC core (China, India) and North America urban centers | Medium term (2-4 years) |

| Rising Veterinary Healthcare Expenditure | +1.5% | North America, Europe, Australia; emerging in GCC and urban Latin America | Long term (≥ 4 years) |

| Growing Availability of Advanced Otic Therapeutics | +1.2% | Global, led by North America and Europe; regulatory lag in MEA | Short term (≤ 2 years) |

| Expansion of Pet Telehealth Services | +1.0% | North America (rural access gaps), APAC (urban convenience), Europe | Medium term (2-4 years) |

| Emerging Microbiome-Based Treatment Approaches | +0.7% | North America and Europe early adopters; APAC and Latin America followers | Long term (≥ 4 years) |

| Proactive Wellness Programs by Pet Insurers | +0.9% | North America, UK, Scandinavia; nascent in APAC and Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Companion Animal Ownership Rates

Gen Z households drove a 43.5% jump in pet adoption between 2023 and 2024, lifting U.S. pet ownership to 94 million homes [1]American Pet Products Association, “Pet Industry Market Size, Trends & Ownership Statistics,” APPA, americanpetproducts.org. Younger owners favor digital-first care, which funnels prescriptions toward e-commerce platforms integral to the companion animal ear infection treatment market. Urbanization in China and India reframes pets as family members, increasing per-capita spending on otic therapeutics. Breed predisposition among dogs with pendulous ears elevates infection incidence, ensuring recurring demand. Rural veterinary shortages affecting 129 million Americans further reinforce telehealth uptake that sustains prescription throughput

Rising Veterinary Healthcare Expenditure

Average annual outlays reached USD 598 for dogs and USD 529 for cats in 2025, but spending polarized: affluent owners embraced specialty services while cost-conscious segments deferred elective care [2]American Veterinary Medical Association, “Pet Ownership & Demographic Sourcebook,” AVMA, avma.org. Ear infections remain non-deferrable, insulating revenue. GCC clinic openings and Brazil’s expanding middle class replicate this pattern, though generic antibacterials dominate price-sensitive tiers.

Growing Availability of Advanced Otic Therapeutics

Regulatory agencies continued to accelerate approvals for novel otic medicines, with the FDA authorizing 45 new animal drugs in 2024 and maintaining a similar pace through early 2026, many of which feature single-dose, in-clinic gels that take owner compliance out of the equation. Manufacturers are adding biofilm-disrupting excipients such as tris-EDTA and localized anesthetics to next-generation products so veterinarians can cleanse, numb, and medicate the canal in one procedure, cutting average revisit rates by 18% in pilot dermatology clinics.

Large firms are building capacity ahead of demand; Boehringer Ingelheim’s USD 75 million European plant expansion lifts annual output of combination gels by 35%, ensuring supply as Asia-Pacific volumes climb. Collectively, these innovations raise the therapeutic ceiling, allowing clinics to treat chronic or resistant cases that once required referral while expanding the premium end of the companion animal ear infection treatment market.

Expansion of Pet Telehealth Services

Telehealth platforms logged more than 700,000 companion-animal interactions in 2025, up 38% year over year, and revenue is forecast to top USD 10 billion by 2030 as rural shortages intersect with urban demand for convenience [3]Veterinary Virtual Care Association, “2024 State of Veterinary Telemedicine Report,” VVCA, vvca.org. Most U.S. states now recognize a video visit as establishing a valid veterinarian-client-patient relationship, enabling direct e-prescribing that funnels otic medications to online pharmacies where prices run 18-22% below clinic shelves.

Partnerships between drug makers and telehealth providers are multiplying; Zoetis, in 2026, began co-branding educational widgets that sit inside leading apps, nudging veterinarians toward its single-dose gels at the point of care. As telehealth normalizes, clinics are repositioning themselves as procedure hubs for ear lavage, cytology, and imaging, while conceding that routine prescription refills will increasingly move through digital channels that shape purchasing behavior in the companion animal ear infection treatment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse Effects Associated with Long-Term Steroid Use | -0.9% | Global, with heightened scrutiny in North America and Europe | Medium term (2-4 years) |

| Low Owner Awareness of Early Ear Disease Symptoms | -0.6% | Global, more pronounced in emerging markets (APAC, Latin America, MEA) | Long term (≥ 4 years) |

| Escalating Antimicrobial Resistance in Otic Pathogens | -1.2% | Global, with hotspots in intensive veterinary-care regions (North America, Europe) | Short term (≤ 2 years) |

| Regulatory Restrictions on Compounded Otic Formulations | -0.8% | North America (FDA enforcement), Europe (EMA harmonization) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Adverse Effects Associated with Long-Term Steroid Use

Chronic exposure to high-potency corticosteroids has been linked to iatrogenic Cushing-like syndromes, reported in 4.6% of canine otitis cases that required more than two refills of steroid-containing drops in 2025 pharmacovigilance data. These risks prompt dermatologists to reserve betamethasone or dexamethasone for acute flares and to pivot toward cytokine inhibitors such as oclacitinib or lokivetmab, which modulate specific interleukin pathways without broad immunosuppression. Insurers are beginning to impose step-therapy rules that require documentation of steroid intolerance before approving premium alternatives, slightly slowing uptake but reinforcing careful prescribing.

Over time, sustained safety scrutiny is expected to shift formulary preferences toward lower-dose combinations, probiotic adjuncts, and non-steroidal anti-inflammatories, constraining growth for legacy triple-combination drops within the companion animal ear infection treatment market.

Low Owner Awareness of Early Ear Disease Symptoms

Consumer surveys conducted by the AVMA in 2025 revealed that 57% of owners could not identify early otitis signs such as mild scratching or malodor, leading to an average 12-day delay before seeking veterinary advice. This lag allows inflammation to progress, doubling treatment duration and tripling drug spend, yet still worsens prognosis in 1 in 5 cases. General-practice clinics often lack video otoscopy, relying on visual inspection that misses subclinical lesions; consequently, nearly 30% of cases referred to dermatology specialists show concurrent otitis media that could have been prevented with earlier intervention.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Antifungals Gain as Malassezia Cases Rise

Antibacterials captured 43.44% companion animal ear infection treatment market share in 2025, yet antifungals are set for a 9.11% CAGR on the back of rising Malassezia infections. The companion animal ear infection treatment market size for antifungals is projected to expand steadily as humid climates and floppy-eared breeds drive fungal prevalence. Combination gels blending florfenicol or marbofloxacin with terbinafine illustrate premium positioning, while corticosteroid-sparing formulas answer safety concerns.

Azole resistance remains uncommon, giving antifungals headroom, whereas stewardship guidelines diminish empirical fluoroquinolone use. Blue-light phototherapy trials posted pathogen-load reductions without antimicrobials. Microbiome products remain experimental, but investor interest signals potential long-term disruption to the companion animal ear infection treatment industry.

By Disease Type: Otitis Interna Growth Reflects Diagnostic Advances

Otitis externa generated 65.12% of 2025 revenue, confirming its dominance within the companion animal ear infection treatment market. Yet otitis interna is pacing a 9.25% CAGR because referral centers now deploy CT and MRI to detect inner-ear disease earlier. The companion animal ear infection treatment market size attached to advanced imaging referrals is growing as vestibular signs trigger specialist evaluation.

Severe externa splits into mild and chronic cohorts: the first group favors low-cost generics, the second opts for compliance-independent long-acting gels. Otitis media often involves surgical myringotomy, concentrating revenue in specialty hospitals.

By Animal Type: Feline Segment Accelerates with Urban Adoption

Dogs commanded 79.12% share in 2025, yet cats are accelerating at 9.31% CAGR as urban apartments and Gen Z preferences support feline adoption. The companion animal ear infection treatment market share for felines remains small, but growth outpaces canine demand.

Dog predisposition keeps absolute canine volume high, while feline cases often coincide with systemic disorders that balloon treatment costs. Niche opportunities emerge in rabbits and ferrets, although volumes stay modest, sustaining only specialty products.

By Mode of Administration: Otic Systems Bypass Compliance Barriers

Topicals held 63.55% share in 2025, yet otic delivery systems will post the fastest 9.6% CAGR to 2031. In-clinic single-dose gels eliminate owner adherence issues, a key driver for the companion animal ear infection treatment market. The shift raises per-visit revenue for clinics but compresses repeat-dose topical sales.

Oral agents keep relevance for otitis media or systemic co-infections, though gastrointestinal side effects hamper owner acceptance. Long-acting injectables mirror human depot therapies, signaling further movement toward veterinarian-administered solutions within the companion animal ear infection treatment industry.

By Distribution Channel: E-Commerce Captures Price-Sensitive Owners

Veterinary clinics dispensed 59.12% of 2025 revenue, yet online pharmacies will expand at 9.12% CAGR as 60% of owners comparison-shop to cut drug costs. Telehealth integrations let platforms transmit scripts straight to fulfillment centers, forging a frictionless pathway that erodes clinic dispensing margins.

Retail pharmacies experiment with in-store vet kiosks, but limited geographic reach curbs impact. Clinics respond by emphasizing diagnostics and procedures that cannot be shipped, preserving their clinical centrality in the companion animal ear infection treatment market.

Geography Analysis

North America generated 43.43% of global revenue in 2025, underpinned by high insurance penetration, strong clinic density, and premium pricing levels. The companion animal ear infection treatment market size in the region remains resilient despite macro headwinds because ear infections are non-elective. Stewardship guidelines reduce fluoroquinolone volume but lift demand for culture tests and narrow agents. Rural shortages drive telehealth uptake, coupling virtual care with mail-order delivery to maintain access.

Europe follows with a mature framework characterized by stringent antimicrobial stewardship and 25%-plus insurance coverage in core markets. Harmonized EMA approvals expedite cross-border launches, yet differences in compounding rules still fragment distribution. Market growth is steady but slower than Asia-Pacific due to already high baseline penetration.

Asia-Pacific posts the fastest 9.77% CAGR, propelled by China and India, where rising disposable incomes and shifting cultural values elevate pets to family status. E-commerce channels dominate urban centers, letting manufacturers sidestep uneven clinic networks. Local production partnerships, such as Vetoquinol’s 2025 joint venture in China, accelerate regulatory navigation and cut logistics costs.

South America shows a bifurcated profile: Brazil’s middle class expands demand, but price sensitivity keeps generics dominant. GCC states invest in new clinics, yet warm climates raise cold-chain challenges for biologics. Africa remains nascent with limited data, but urban middle classes in South Africa and Kenya show early adoption of premium pet care. Collectively, emerging markets diversify revenue streams and cushion saturation risks in established regions of the companion animal ear infection treatment market.

Competitive Landscape

Global leadership rests with Zoetis, Boehringer Ingelheim, and Elanco, whose broad portfolios and global logistics give scale advantages. Their 2024-2025 R&D pipelines emphasize compliance-independent gels and microbiome modulators, supported by patent filings and capacity expansions such as Boehringer Ingelheim’s USD 75 million European plant upgrade in 2026. Specialty players Dechra, Virbac, and Vetoquinol carve niches by focusing on dermatology depth and regional agility. Dechra’s sequence of 2025 FDA approvals for single-dose gels broadens its footprint in corticosteroid-free solutions.

Technology adoption is a key differentiator. Firms that bundle video otoscopy diagnostics with product education help clinics justify premium pricing while aligning with BSAVA and CDC stewardship rules. Telehealth-pharmacy integrations, exemplified by Zoetis’s 2026 partnership with a leading platform, chase the direct-to-consumer surge. Generic manufacturers, such as Norbrook, compete on price, undermining branded fluoroquinolones but reinforcing stewardship by offering cost-effective narrow-spectrum options.

The companion animal ear infection treatment market now rewards innovation and channel flexibility over scale alone. Multinationals must protect share by reframing value propositions around antimicrobial stewardship, owner convenience, and veterinary revenue support. Specialty houses push corticosteroid-sparing and probiotic novelties, betting that evolving clinical preferences will unlock premium margins.

Companion Animal Ear Infection Treatment Industry Leaders

Zoetis Inc.

Dechra Pharmaceuticals PLC

Merck & Co., Inc.

Elanco Animal Health Incorporated

Boehringer Ingelheim Vetmedica GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Merck Animal Health secured FDA clearance for MOMETAMAX SINGLE, a single-dose otic suspension for dogs.

- May 2025: Dechra gained FDA approval for Otiserene, the marbofloxacin-based single-dose product for the treatment of otitis externa in dogs.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the companion-animal ear-infection treatment market as the value of prescription and over-the-counter products, topical, otic, oral, or systemic, dispensed through veterinary and retail channels to manage otitis externa, media, and interna in dogs, cats, and other household pets.

Diagnostics, surgical procedures, and farm-animal therapeutics are outside our scope.

Segmentation Overview

- By Product Type

- Antibacterial

- Aminoglycosides

- Fluoroquinolones

- Other Antibacterial Products

- Antifungal

- Corticosteroids

- Other Product Types

- Antibacterial

- By Disease Type

- Otitis Externa

- Otitis Media

- Otitis Interna

- By Animal Type

- Dogs

- Cats

- Other Animal Types

- By Mode of Administration

- Topical

- Oral

- Otic

- By Sales Channel

- Veterinary Hospitals & Clinics

- Retail Pharmacies & Pet Stores

- Online Pharmacies & Direct-to-Consumer

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with practicing veterinarians, small-animal dermatology specialists, and regional distributors across North America, Europe, and Asia confirmed typical dosing cycles, average selling prices, and channel mark-ups. These discussions filled data gaps on owner compliance and upcoming single-dose therapies, letting us fine-tune model assumptions.

Desk Research

Our analysts began with open datasets, such as USDA APHIS pet population surveys, AVMA and FEDIAF ownership statistics, and IDEXX reference-lab prevalence dashboards, which anchor disease incidence and treatment penetration.

Peer-reviewed journals, including the Journal of Veterinary Dermatology and JAVMA, clarified therapy guidelines, while customs shipments from Volza and revenue splits in SEC 10-Ks helped size product flows.

Paid libraries like D&B Hoovers and Dow Jones Factiva supplied company-level sales that sharpened regional splits.

The sources listed illustrate, not exhaust, the material consulted for validation.

Market-Sizing & Forecasting

A top-down construct converts regional dog and cat populations to 'treatable infection episodes,' adjusts for veterinary visit rates, and multiplies by confirmed therapy uptake and ASPs. Bottom-up cross-checks, sampled manufacturer revenue roll-ups and distributor invoice audits, calibrate the totals before final reconciliation. Key model variables include:

- annual otitis incidence per pet species,

- veterinary visit probability per episode,

- average treatment course length,

- share of topical versus systemic regimens,

- ASP drift linked to branded-generic mix,

- regional pet insurance coverage.

A multivariate regression, blending pet ownership growth, clinic density, and disposable pet-care spend, projects demand; ARIMA smoothing tempers short-term volatility. Where bottom-up inputs were partial, missing volumes were imputed from three-year moving averages of comparable geographies.

Data Validation & Update Cycle

Outputs go through variance checks against historic sales, outlier flagging, and peer review by a senior analyst.

The model refreshes each year, with interim tweaks when material events, such as drug recalls and major approvals, shift the baseline.

A final pre-publication sweep ensures clients receive the latest view.

Why Mordor's Companion Animal Ear Infection Treatment Size & Share Analysis Baseline Commands Reliability

Published values often diverge because firms differ on therapy scope, pet-count baselines, and ASP inflation paths. Our study fixes a transparent scope, including all pharmacological treatments, vet and retail, uses 2025 infection data verified with clinicians, and applies a mixed top-down and bottom-up build that limits double-counting.

Others may exclude OTC cleansers, assume flat ASPs, or project from outdated 2021 pet census figures, inflating or deflating totals.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.77 B (2025) | Mordor Intelligence | - |

| USD 0.77 B (2025) | Global Consultancy A | Excludes OTC cleansers; relies on static ASPs |

| USD 0.76 B (2025) | Industry Journal B | Uses 2021 pet counts; limited bottom-up cross-check |

In summary, by blending verified pet epidemiology, real transaction prices, and continuous validation, Mordor Intelligence delivers a balanced, traceable baseline clients can depend on for strategic planning.

Key Questions Answered in the Report

How big is the companion animal ear infection treatment market in 2026?

The market is valued at USD 0.83 billion in 2026 and is on track to reach USD 1.25 billion by 2031, reflecting an 8.44% CAGR.

Which product segment is growing fastest?

Antifungal therapeutics exhibit the highest growth, forecast at a 9.11% CAGR through 2031 as veterinarians address mixed bacterial-fungal infections more aggressively.

Why is Asia-Pacific the fastest-expanding region?

Rapid urbanization, higher disposable income, and growing pet ownership in countries such as China and India are driving a 9.77% regional CAGR, outpacing mature markets.

How does telehealth influence ear infection treatment?

Telehealth simplifies follow-up visits, supports antimicrobial stewardship through closer monitoring, and complements online pharmacies that dispense prescription ear medications.

What are key risks facing the market?

Escalating antimicrobial resistance, adverse effects from extended steroid use, and evolving regulations on compounded formulations can constrain growth if not proactively managed.

Page last updated on: