Narcolepsy Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

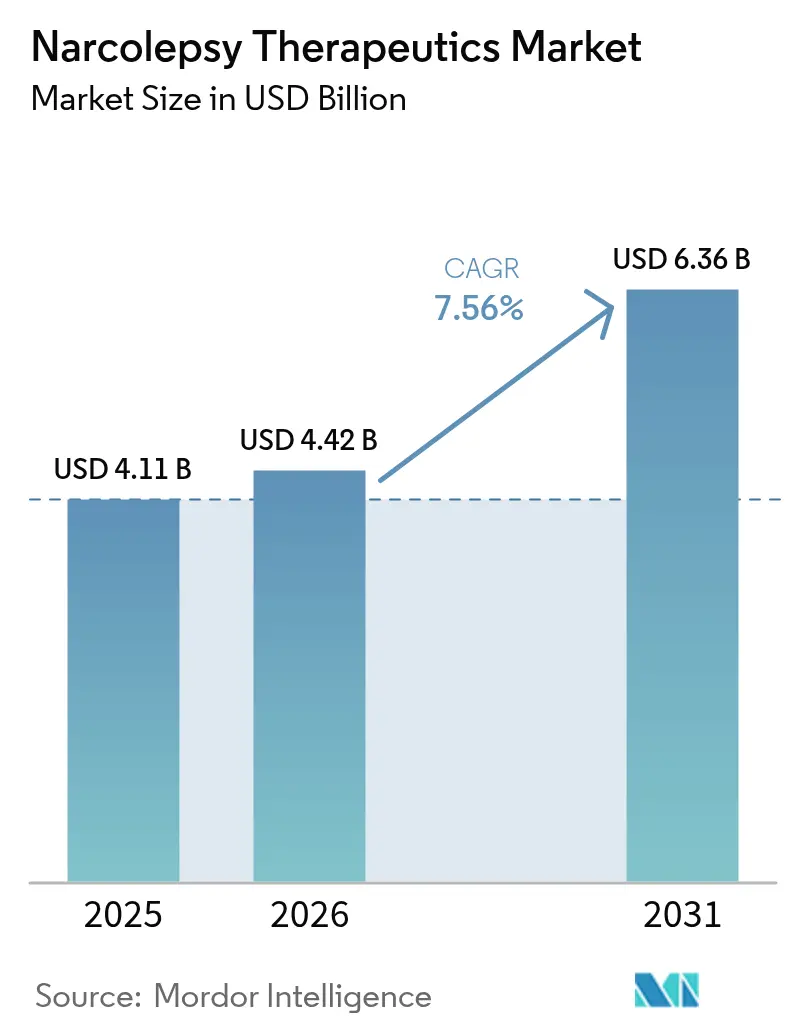

| Market Size (2026) | USD 4.42 Billion |

| Market Size (2031) | USD 6.36 Billion |

| Growth Rate (2026 - 2031) | 7.56% CAGR |

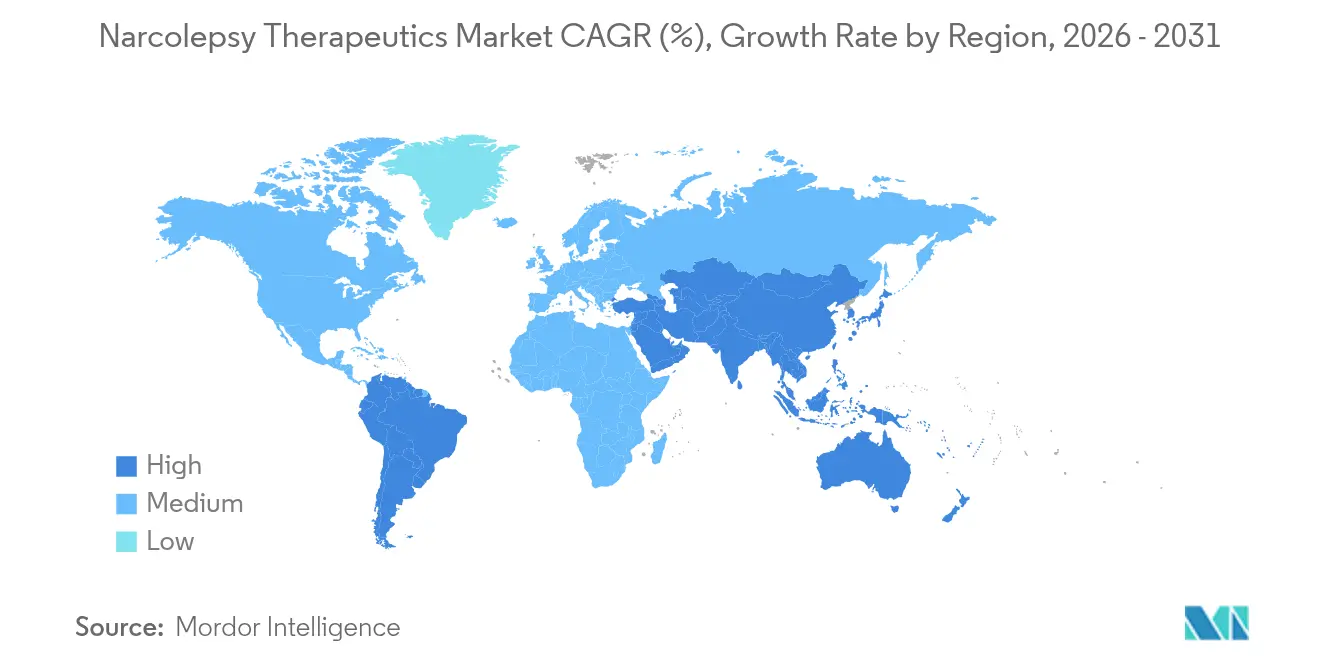

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Narcolepsy Therapeutics Market Analysis by Mordor Intelligence

The Narcolepsy Therapeutics Market size is expected to grow from USD 4.11 billion in 2025 to USD 4.42 billion in 2026 and is forecast to reach USD 6.36 billion by 2031 at 7.56% CAGR over 2026-2031.

Momentum comes from orexin receptor agonists that target disease biology, extended-release sodium oxybate that removes nocturnal dosing, and expanded pediatric approvals that enlarge the treatable pool. Digital distribution widens patient access, while trial data on once-nightly formulations changes prescriber preferences. Competitive pressure increases as authorized generics chip away at legacy brands and as histamine H3 antagonists grow in specialist clinics. Venture funding and cross-border licensing accelerate product launches in Asia-Pacific, turning regulatory harmonisation into a sales catalyst for innovators.

Key Report Takeaways

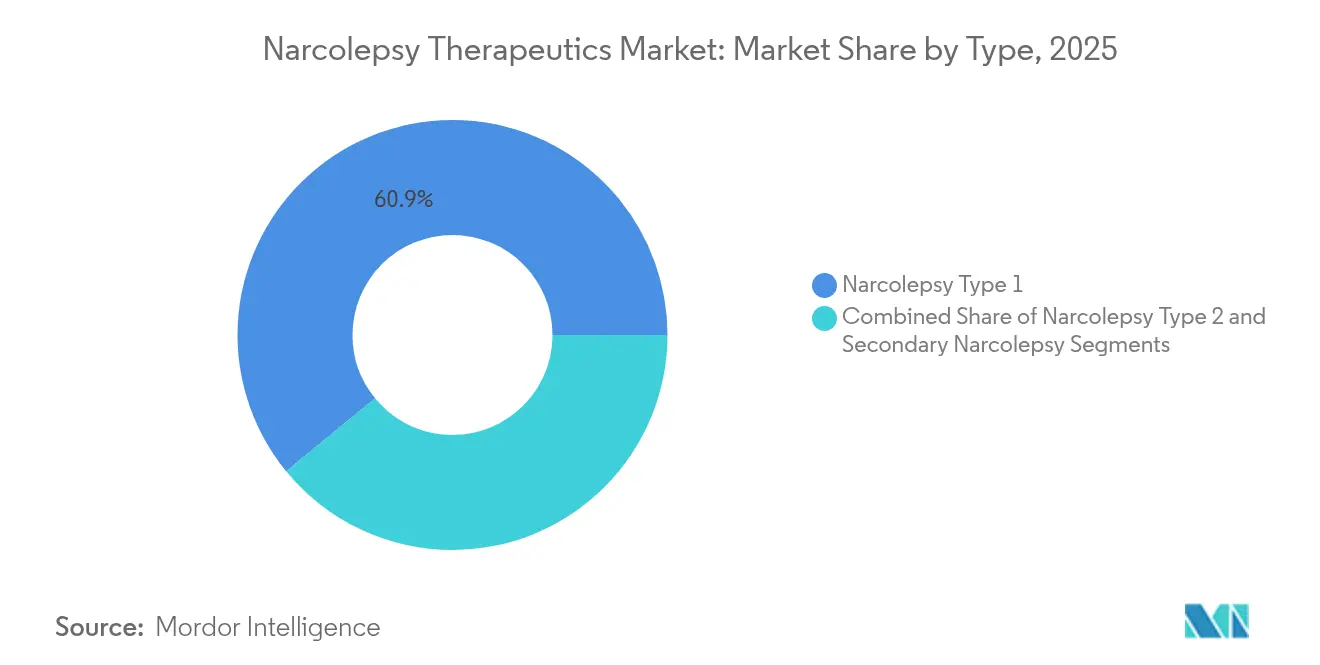

- By type, Narcolepsy Type 1 held 60.92% of narcolepsy therapeutics market share in 2025, whereas Type 2 is on track for an 10.79% CAGR to 2031.

- By product class, sodium oxybate commanded 48.67% share of the narcolepsy therapeutics market size in 2025; histamine H3 antagonists are projected to expand at a 13.41% CAGR through 2031.

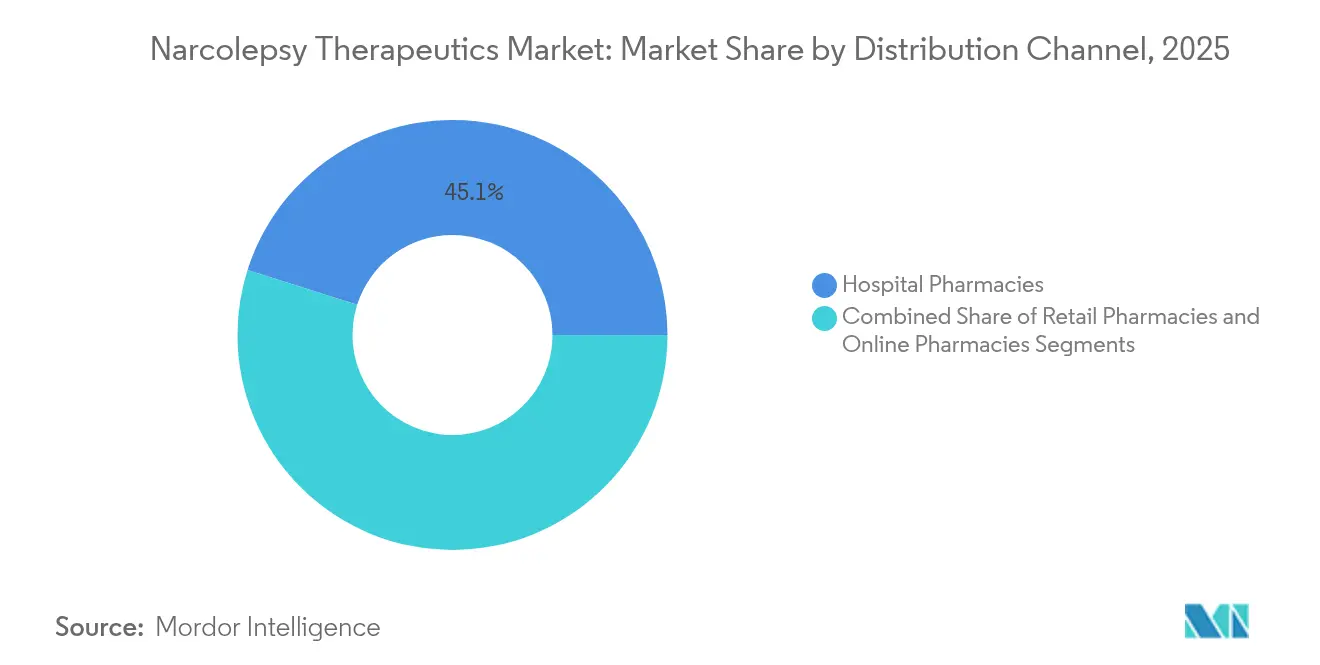

- By distribution channel, hospital pharmacies accounted for 45.12% of the narcolepsy therapeutics market size in 2025, while online pharmacies record the highest projected CAGR at 13.68% to 2031.

- By geography, North America led with 42.05% revenue share in 2025; Asia-Pacific is the fastest growing region at a 11.87% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Narcolepsy Therapeutics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Support and Reimbursement Expansion | +1.5% | North America and EU, spill-over to emerging markets | Short term (≤ 2 years) |

| Personalised and Combination-therapy Protocols | +0.9% | Global, led by developed markets | Medium term (2-4 years) |

| FDA/EMA Approvals of Novel Agents | +1.8% | Global, precedent in US/EU | Short term (≤ 2 years) |

| Increasing Clinical Trials for Narcolepsy Therapies | +1.1% | US, EU, Japan | Medium term (2-4 years) |

| Rising Prevalence of Narcolepsy | +1.2% | Global, highest in APAC | Medium term (2-4 years) |

| Awareness Programmes and Improving Diagnosis Rates | +0.8% | North America and EU, expanding to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

FDA/EMA Approvals of Novel Agents

New approvals validate orexin biology beyond stimulants. Lumryz gained clearance as the first once-nightly extended-release sodium oxybate and demonstrated efficacy in the REST-ON Phase 3 trial. Pediatric approvals broaden reach, with extended-release sodium oxybate now indicated from age 7 years. TAK-861 showed significant improvements in sleep latency and cataplexy in Phase 2b trials, encouraging a Phase 3 global programme.[1]Daniel A. Gottlieb et al., “Orexin-2 Receptor Agonist TAK-861 in Type 1 Narcolepsy,” The New England Journal of Medicine, nejm.org Orphan-drug exclusivity offers seven-year protection and fuels R&D pipelines.[2]Food and Drug Administration, “Designating Orphan Products and Granting Market Exclusivity,” federalregister.gov EMA alignment reduces duplicate testing and accelerates European launches for sodium oxybate and histamine H3 antagonists.

Increasing Clinical Trials for Narcolepsy Therapeutics

Industry confidence rises as trials pursue disease-modifying goals rather than symptom control. AXS-12 met SYMPHONY Phase 3 endpoints with an 83% cataplexy reduction, prompting NDA preparation. Alkermes’ ALKS-2680 improved sleep latency by up to 34 minutes in early studies. Harmony Biosciences acquired HBS-102, expanding into MCHR1 antagonism to tackle REM dysregulation. Beacon Biosignals partners with Takeda to apply neuro-biomarkers that sharpen endpoints and may cut trial time. Investment in CNS imaging rises, evidenced by Clario’s NeuroRx acquisition that brings fMRI capacity to late-stage programmes.

Regulatory Support and Reimbursement Expansion

Policy evolution boosts affordability. The Czech Republic covers 84% of annual sodium oxybate cost, setting a benchmark for emerging Europe. Telehealth reimbursement parity is championed by the American Academy of Sleep Medicine and supports rural follow-up visits. Orphan-drug spending may hit 20% of prescription sales by 2026, compelling payers to deploy value-based contracts that reward real-world outcomes. Patent settlements, such as Sunosi litigation that schedules Hikma entry by 2040, illustrate controlled erosion of exclusivity. Central and Eastern Europe implement OMP-specific HTA processes, yet timelines differ, leaving white-space for flexible pricing models.

Growing Focus on Personalised and Combination-Therapy Protocols

Treatment tailoring gains speed. High-performance HPLC reveals that radioimmunoassay overestimates inactive hypocretin fragments, supporting better patient stratification. Combination therapy is common, with sodium oxybate plus stimulants improving both cataplexy and daytime sleepiness.[3]Stanford Center for Sleep Research, “Combination Therapy Outcomes in Cataplexy,” stanford.edu AI-enabled cognitive behavioural therapy platforms add moderate to large sleep benefits when layered on drugs. Patient surveys show 94% preference for once-nightly Lumryz, influencing design of adherence-friendly regimens. Biomarker-driven dose adjustment is under study within Beacon Biosignals and Takeda collaboration, bridging diagnostics with therapeutics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse-event Profile and Abuse Potential | -1.1% | Global, strictest in US/EU | Long term (≥ 4 years) |

| High Therapy Cost and Orphan-Drug Pricing | -1.8% | Global, pronounced in emerging markets | Medium term (2-4 years) |

| Patent Cliffs Versus Litigation Delaying Generics | -0.9% | North America and EU | Short term (≤ 2 years) |

| Reimbursement Gaps in Emerging Regions | -1.3% | APAC, Latin America, MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Therapy Cost and Orphan-Drug Pricing

Lumryz carries an annual US list price of USD 177,034, which, while competitive with legacy oxybate, remains many times higher than stimulants and poses affordability challenges. Xyrem rose from USD 11,169 in 2007 to USD 182,804, triggering investigation into anti-competitive tactics. Payers note that 51% of 2023 drug approvals were orphan, adding urgency to align prices with measurable benefit. Emerging markets find US-centric pricing untenable, delaying launches or limiting reimbursement scope. Outcomes-based contracts start to appear, linking payment to improved Epworth Sleepiness Scale scores and reduced cataplexy episodes.

Adverse-Event Profile and Abuse Potential of Sodium Oxybate

Sodium oxybate’s Schedule III status means Risk Evaluation and Mitigation Strategy controls with single-source distribution and compulsory prescriber certification. Its structural similarity to GHB invites social stigma and heightened surveillance, driving some clinicians toward non-controlled options such as pitolisant. Twice-nightly dosing can fragment sleep, yet missing the second dose risks rebound cataplexy. Global regulatory diversity complicates logistics, with some jurisdictions requiring additional import licences that delay product availability. Monitoring for tolerance and withdrawal adds cost and deters borderline candidates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Diagnostic Innovation Lifts Type 2 Adoption

The Narcolepsy therapeutics market size for Type 1 remained dominant in 2025 as 60.92% of total therapy spending, driven by cataplexy-targeted sodium oxybate prescriptions. Type 2 is growing fastest at an 10.79% CAGR, supported by refined multiple sleep latency testing that differentiates it from idiopathic hypersomnia. Cerebrospinal fluid analysis via HPLC now discerns inactive hypocretin fragments, cutting misclassification risk and boosting accurate therapy alignment. Clinicians often reserve oxybate for Type 1 while favouring stimulants or histamine H3 antagonists for Type 2, creating separate pricing ladders and payer policies. Secondary narcolepsy from structural brain injuries forms a niche but clinically significant slice that draws attention to rehabilitation protocols and neuro-imaging referral pathways.

Improved diagnostic throughput also widens the Narcolepsy therapeutics market, with community neurologists adopting simplified scoring that flags abnormal REM transitions. Academic centres pilot tele-polysomnography which reduces waitlists and facilitates earlier start of disease-modifying trials. Type 2 patient-reported outcomes show faster work productivity gains once correctly classified, strengthening the economic rationale for payers to fund confirmatory CSF testing. Awareness campaigns run by patient groups increase research registries, offering real-world evidence that supports label expansion for novel agents. Regional variance persists, though, with Asia-Pacific under-diagnosing Type 2 due to limited MSLT capacity, signalling opportunity for portable diagnostic devices.

By Product Class: H3 Antagonists Pressure Oxybate Leadership

Sodium oxybate generated nearly half of 2025 revenue, yet its Narcolepsy therapeutics market share trajectory with 48.67% faces erosion from histamine H3 antagonists that grow by 13.41% CAGR through 2031. Pitolisant’s non-scheduled status eliminates REMS hurdles and pharmacy lock-in, letting clinicians write e-prescriptions the same day as diagnosis. Orexin-2 receptor agonists such as TAK-861 and ALKS-2680 promise disease modification and could up-end current treatment algorithms once approved. CNS stimulants retain first-line use for excessive daytime sleepiness, but their commoditised pricing offers limited revenue upside.

The Narcolepsy therapeutics market size premium commanded by oxybate depends on adherence support, yet 94% of patients prefer once-nightly Lumryz that avoids 3 a.m. awakenings. That preference is driving payers to revisit step-therapy rules that once mandated twice-nightly formulations first. Category innovation continues, with HBS-102 in Phase 1 tackling REM dysregulation, potentially expanding addressable symptoms beyond cataplexy. Patent cliffs loom: Xywav holds exclusivity until 2028, while authorised generics of Xyrem already compete on price. These forces motivate Jazz Pharmaceuticals to pursue next-generation oxybate that combines deuteration with extended release to defend its core franchise.

By Distribution Channel: Digital Dispensing Gains Momentum

Hospital pharmacies captured 45.12% of revenue in 2025, reflecting strict handling rules for controlled oxybate, yet online pharmacies post a 13.68% CAGR as care teams embrace virtual follow-up visits. Retail outlets serve chronic stimulant supply but seldom stock oxybate due to storage constraints. Telemedicine legislation enacted in 2024 permits Schedule III refills after a single in-person visit, removing a major barrier for rural patients. Pitolisant’s non-controlled classification allows full e-commerce fulfilment, and platforms like Klinic integrate symptom diaries, refill prompts, and pharmacist video counselling.

The Narcolepsy therapeutics market further benefits from digital wrap-around services such as AI-guided CBT modules that integrate with dose-reminder apps. Pharmacy benefit managers pilot direct-to-patient shipping bundled with wearable sleep trackers, generating real-world adherence datasets for producers. Regulatory authorities adjust guidelines on temperature-controlled packaging for oxybate that streamline last-mile delivery. Payment systems embed electronic prior-authorisation, accelerating approval times from weeks to hours. Geographically, US and EU lead adoption, but Singapore and South Korea have enacted sandbox frameworks that may create exportable templates for other APAC markets.

Geography Analysis

North America retained 42.05% of the Narcolepsy therapeutics market in 2025 on the back of favourable reimbursement, specialist density, and early uptake of once-nightly oxybate. Payer formularies prioritise value-based contracts that hinge on Epworth Sleepiness Scale reduction, a policy that encourages rapid cycling toward clinically superior regimens. Digital health regulations allow continuous remote monitoring, facilitating adherence tracking by sleep centres and plugging gaps between urban and rural care.

Europe contributes steady growth as orphan-drug incentives and EMA centralised procedures shorten time from approval to reimbursement. Co-payment caps in Western Europe sustain broad access, while Central and Eastern Europe gradually close reimbursement gaps through HTA reforms that benchmark outcomes data from larger markets. EU cross-border healthcare rules have spurred patient travel for complex sleep studies, indirectly boosting diagnostic throughput.

Asia-Pacific is the fastest expanding region at a 11.87% CAGR, thanks to rising diagnosis rates, regulatory reforms, and urban hospital investment. China’s recent endorsement of lemborexant for insomnia signals growing acceptance of sleep therapeutics and sets a regulatory precedent for orexin agents. Japan reports USD 2,531 annual healthcare spend per narcolepsy patient versus USD 266 for controls, illuminating the economic benefit of effective therapy. Australia widens coverage under the Pharmaceutical Benefits Scheme, and India’s private insurers experiment with bundled tele-sleep packages. Middle East, Africa, and Latin America still struggle with reimbursement asymmetry and neurologist shortages, yet pilot telemedicine projects funded by development banks hint at latent demand once cost barriers ease.

Competitive Landscape

The narcolepsy therapeutics market is moderately consolidated. Jazz Pharmaceuticals remains the benchmark, generating USD 1.27 billion from Xywav in 2023, yet its dominance is challenged on multiple fronts. Harmony Biosciences achieved USD 714.7 million in 2024 from pitolisant and is diversifying into REM-modulating assets to broaden its sleep franchise. Avadel’s Lumryz secured 94% patient preference over twice-nightly oxybate, a statistic that reshapes brand messaging and formulary positioning.

Patent expirations catalyse generic entry. Hikma and Amneal began selling authorised generics of Xyrem, nudging average selling prices downward and forcing Jazz to shift volume to Xywav before its own exclusivity ends in 2028. Axsome’s AXS-12 and Takeda’s TAK-861 compete for first-in-class positioning in disease-modifying therapy, with Takeda advancing to Phase 3 on strong Phase 2b data. Centessa gained IND clearance for ORX-142, illustrating a widening field of orexin-focused biotech.

Strategic partnerships proliferate. Beacon Biosignals supplies digital biomarkers to Takeda, while Clario’s acquisition of NeuroRx strengthens imaging readouts. In-licensing deals expand portfolios: Neuraxpharm acquired Provigil and Nuvigil for established brand leverage, whereas Apotex secured US rights to bolster stimulant offerings. M&A valuations reflect competitive interest; Harmony paid undisclosed double-digit millions for HBS-102, underscoring appetite for differentiated mechanisms.

Narcolepsy Therapeutics Industry Leaders

Jazz Pharmaceuticals plc

Harmony Biosciences

Teva Pharmaceuticals Industries Ltd

Azurity Pharmaceuticals, Inc.

Avadel Pharmaceuticals

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Centessa's OX2R agonist ORX-142 received IND clearance from the FDA, enabling clinical trials for this novel orexin receptor 2 agonist targeting narcolepsy's underlying pathophysiology. This approval represents a significant milestone in the race to develop orexin replacement therapies that could address the root cause of Type 1 narcolepsy rather than merely managing symptoms.

- May 2025: Takeda published Phase 2b trial results for oveporexton (TAK-861) in The New England Journal of Medicine, demonstrating statistically significant improvements in sleep latency and cataplexy reduction in narcolepsy Type 1 patients. The company announced plans to initiate global Phase 3 trials, positioning this oral orexin receptor 2 agonist as a potential breakthrough therapy.

- May 2025: Avadel Pharmaceuticals presented 14 abstracts and 4 oral presentations at SLEEP 2025, showcasing LUMRYZ's clinical superiority with interim REFRESH study results indicating significant improvements in excessive daytime sleepiness for patients switching from traditional oxybate formulations.

- February 2025: Apotex acquired US rights to PROVIGIL (modafinil) and NUVIGIL (armodafinil) from Neuraxpharm, expanding its specialty pharmaceutical portfolio in the narcolepsy treatment space. This acquisition strengthens Apotex's position in the stimulant segment while ensuring continued patient access to these established therapies.

- June 2024: Harmony Biosciences secured FDA approval for its supplemental New Drug Application (sNDA) concerning WAKIX (pitolisant) tablets, targeting excessive daytime sleepiness (EDS) in pediatric narcolepsy patients aged 6 and above.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the narcolepsy therapeutics market as all prescription medicines, whether branded or generic, that are indicated to manage excessive daytime sleepiness, cataplexy, hypnagogic hallucinations, or sleep paralysis linked to narcolepsy type 1, narcolepsy type 2, or secondary narcolepsy across retail, hospital, and online pharmacy channels worldwide. We map revenues in USD at ex-manufacturer level and include pipeline molecules from Phase III onward once regulatory approval becomes reasonably probable.

Scope exclusion: diagnostic tests, wearable sleep trackers, and behavioral therapy services are outside this value chain.

Segmentation Overview

- By Type

- Narcolepsy Type 1

- Narcolepsy Type 2

- Secondary Narcolepsy

- By Product Class

- CNS Stimulants

- Sodium Oxybate

- Histamine H3 Antagonists

- Dopamine

- Antidepressants

- OX2R Agonists

- Other Therapies

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We supplemented desk findings through structured interviews with neurologists, payor advisers, and senior executives at regional distributors across North America, Europe, and Asia-Pacific. These conversations clarified prevalence adjustments, emerging orexin-agonist pricing expectations, and refill adherence, enabling us to fine-tune uptake curves and discount trajectories.

Desk Research

Our analysts first assembled foundational data from open sources such as the World Health Organization Global Health Observatory, the National Institute of Neurological Disorders and Stroke, U.S. FDA Orange Book, ClinicalTrials.gov, and OECD Health Stats. Trade statistics from UN Comtrade helped us track sodium oxybate and modafinil active ingredient flows, while corporate disclosures, investor decks, and specialist journals supplied average selling prices and launch timelines. Subscription databases, including D&B Hoovers and Dow Jones Factiva, supported cross-checks on company revenues and news flow. This list is illustrative; many additional references were consulted to verify and enrich the dataset.

Market-Sizing & Forecasting

A top-down prevalence to treated patient pool model anchors the baseline, after which a selective bottom-up roll-up of supplier sales, channel checks, and sampled ASP times dispensed volumes validates the totals. Key variables tracked include diagnosed prevalence, stimulant to oxybate therapy mix, orphan drug exclusivity expiry dates, median time to diagnosis, healthcare reimbursement depth, and regional generic penetration. Forecasts to 2030 rely on multivariate regression blended with scenario analysis, with parameter weights informed by primary research consensus; missing bottom-up inputs are bridged using analog country proxies and price erosion heuristics before final reconciliation.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated variance flags, peer review by another analyst, and a senior domain lead sign-off. Models refresh annually, with interim revisions triggered by major approvals, label expansions, or unexpected safety actions. Clients receive material event updates within eight weeks of occurrence.

Why Mordor's Narcolepsy Therapeutics Baseline Commands Reliability

Published estimates often diverge because firms adopt different inclusion criteria, patient funnel assumptions, and currency conversions.

Key gap drivers include whether over-the-counter melatonin is counted, the timing of generic sodium oxybate entry, and the cadence at which pipeline assets are modeled; Mordor analysts refresh these levers each year, while some publishers lock their view for longer cycles.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.11 B | Mordor Intelligence | - |

| USD 3.52 B (2023) | Global Consultancy A | excludes Asia generics, applies flat ASP until 2030 |

| USD 3.83 B (2024) | Industry Journal B | counts only cataplexy cases, omits online pharmacy channel |

These comparisons show that our regularly refreshed scope, explicit channel coverage, and mixed method modeling deliver a balanced, transparent baseline that decision makers can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current valuation of the Narcolepsy therapeutics market?

The market is valued at USD 4.42 billion in 2026 and is expected to reach USD 6.36 billion by 2031.

Which therapy class generates the highest revenue today?

Sodium oxybate remains the top revenue generator, accounting for 48.67% of 2025 sales.

How fast is the Asia-Pacific region growing?

Asia-Pacific is forecast to expand at a 11.87% CAGR between 2026 and 2031, outpacing all other regions.

Why are orexin receptor agonists attracting attention?

They target the root biological deficit of Type 1 narcolepsy and showed clinically meaningful improvements in Phase 2b trials.

What digital channels are changing drug distribution?

Online pharmacies and telemedicine platforms are growing at a 13.68% CAGR, driven by policy support for remote prescribing.

How does pricing affect patient access?

High orphan-drug prices can limit uptake; outcomes-based contracts and national reimbursement schemes aim to close affordability gaps.

Page last updated on: