Europe Polycarbonate Sheets Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

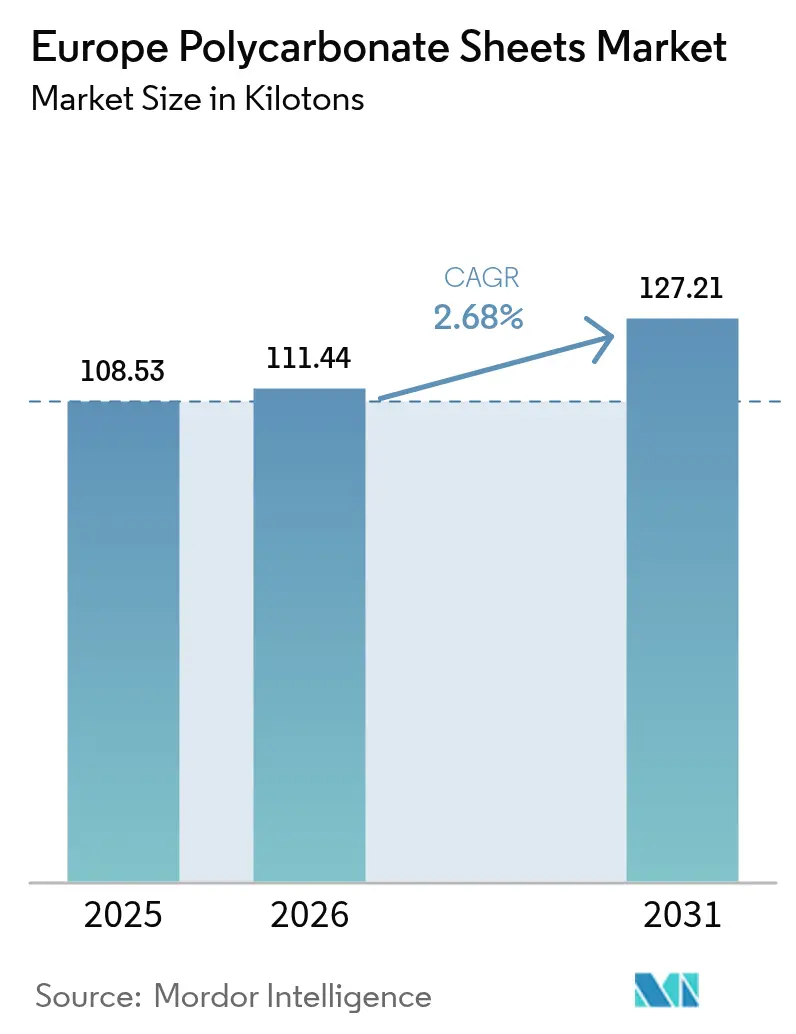

| Base Year Market Size (2025) | 108.53 kilotons |

| Market Volume (2026) | 111.44 kilotons |

| Market Volume (2031) | 127.21 kilotons |

| Growth Rate (2026 - 2031) | 2.68% CAGR |

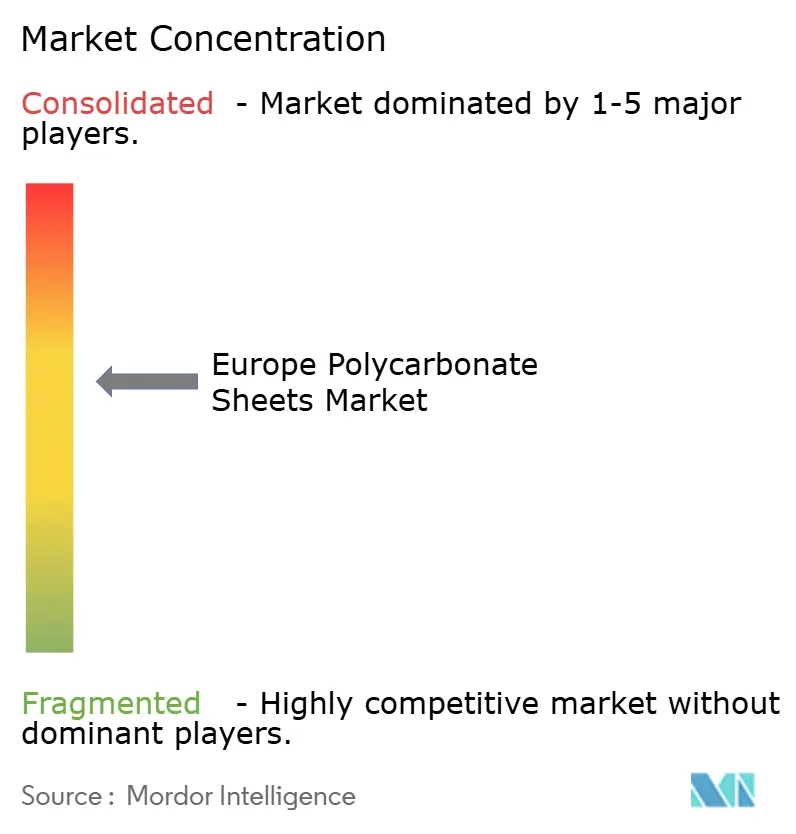

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Polycarbonate Sheets Market Analysis by Mordor Intelligence

Europe Polycarbonate Sheets Market size in 2026 is estimated at 111.44 kilotons, growing from 2025 value of 108.53 kilotons with 2031 projections showing 127.21 kilotons, growing at 2.68% CAGR over 2026-2031. Demand advances despite a 7.7% contraction in 2024 residential renovation activity and a further 3.9% drop forecast for 2025, as energy-efficiency mandates under the revised Energy Performance of Buildings Directive (EPBD (EU) 2024/1275) push architects toward daylight-optimized, thermally efficient roof and façade solutions Multiwall sheets, favored for Ug values down to 0.85 W/m²K, dominate specifications for conservatories, industrial skylights, and greenhouse glazing. Corrugated formats are expected to benefit from a 5.8% surge in 2024 civil-engineering outlays, finding use in transport shelters and noise barriers, where lightweight, translucent roofing speeds up installation and reduces structural loads. Agriculture emerges as the fastest-growing end-user as diffusive multiwall panels raise tomato yields by approximately 8%, a performance increasingly documented in peer-reviewed horticultural studies. Competitive intensity is moderate: the top 10 producers command roughly 60-70% of the worldwide volume, yet mid-tier European extruders continue to integrate into panel systems, cap profiles, and specialty coatings to expand their margins beyond commodity sheet supply.

Key Report Takeaways

- Multiwall sheets captured 59.18% polycarbonate sheets market share in 2025, while corrugated sheets are forecast to expand at a 3.12% CAGR through 2031.

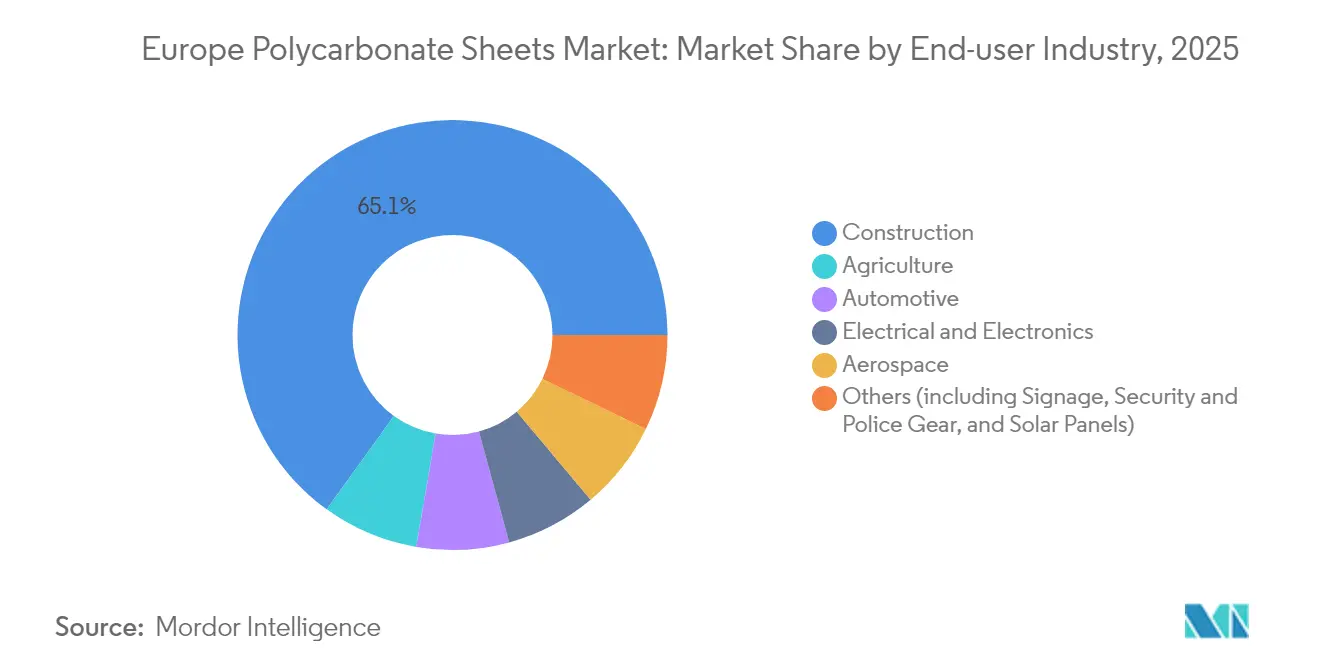

- Construction accounted for 65.05% of the polycarbonate sheets market size in 2025; agriculture is expected to advance at a 2.92% CAGR between 2026 and 2031.

- Germany held 22.10% of 2025 regional demand and is projected to grow at a 3.28% CAGR to 2031, the highest among major European economies.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Polycarbonate Sheets Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-pandemic rebound of commercial re-roofing demand | +0.6% | Southern Europe, UK | Medium term (2-4 years) |

| Mandatory EU energy-efficiency codes boosting daylight-roof usage | +0.8% | EU-27, strongest in Germany, France, Netherlands, Nordics | Long term (≥ 4 years) |

| Automotive lightweighting and panoramic glazing adoption | +0.4% | Germany, France, Italy | Medium term (2-4 years) |

| Government incentives for high-tech greenhouse horticulture | +0.5% | Netherlands, Spain, France, Belgium | Medium term (2-4 years) |

| OEM shift to chemically recycled PC sheets | +0.3% | Belgium, Germany, Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Post-Pandemic Rebound of Commercial Re-Roofing Demand

EU non-residential construction investment in 2024 reached EUR 1,422 billion, edging up 0.1%, with civil-engineering work rising 5.8%, reopening a backlog of skylight and roof-light retrofits in logistics hubs, transport terminals, and retail centers[1]European Construction Industry Federation, “FIEC Statistical Report 2025,” fiec.be . Southern Europe leads: Spain’s non-residential activity expanded 5.5% and Portugal maintained growth as deferred projects from 2020-2022 moved forward. Corrugated polycarbonate sheets provide installers with a drop-in replacement for aging asbestos or metal roofing, reducing weight by up to 60% and enabling daylighting that lowers warehouse electricity bills. Growth could accelerate if EU Recovery and Resilience Facility funding, which underpinned Italy’s 21% civil-engineering jump in 2024, is extended beyond 2026. However, France (-1.4%) and Germany (-1.9%) saw declines, underscoring the importance of regional mix for sheet producers.

Mandatory European Union Energy-Efficiency Codes Boosting Daylight-Roof Usage (EN 17037, EPBD)

The EPBD (EU) 2024/1275 now requires life-cycle global-warming-potential disclosure and tighter energy-performance thresholds for roof glazing[2]Energy Directorate-General, “Directive (EU) 2024/1275 of the European Parliament and of the Council,” europa.eu. EN 17037 daylighting standards require designers to demonstrate adequate natural-light distribution, driving demand for low-Ug multiwall panels that diffuse light while meeting structural loads. EXOLON Group’s Hybrid-X multiwall sheet achieves a thermal conductivity of 0.85 W/m²K at a 50 mm thickness, while maintaining≥45% light transmission. This product offers a 20-year weathering warranty that aligns with German and Dutch building insurance requirements. The directive’s renovation-passport mechanism will compel upgrades of legacy single-skin polycarbonate installed in the 1990s and 2000s, triggering a cyclical replacement wave by 2030.

Automotive Lightweighting and Panoramic Glazing Adoption

Premium OEMs are adopting polycarbonate panoramic roofs to trim 40-50% of the weight compared to laminated glass, thereby increasing EV range and integrating LiDAR housings within a single, molded component. Covestro’s roof sensor module concept, unveiled in 2024, embeds camera fittings directly into the glazing to enhance aerodynamics. Current uptake is limited to high-end models—BMW iX, Mercedes EQS—because sheet costs run 15-20% higher than tempered glass. AGC counters with photovoltaic glass roofs, exposing polycarbonate to substitution in the mass market. If Volkswagen and Stellantis choose polycarbonate for compact EVs planned for 2026-2028, annual sheet demand could triple.

Government Incentives for High-Tech Greenhouse Horticulture

Diffusive multiwall panels scatter incoming radiation, improving canopy penetration and increasing tomato yields by ≈approximately 8% compared to clear glazing, according to peer-reviewed Dutch greenhouse trials. Spain’s national horticulture strategy, launched in 2024, offers grants for greenhouse modernization, while Dutch and Belgian growers target embodied-carbon cuts to offset high energy bills. Brett Martin’s 2025 Marlon CS Longlife Diffuser Opal sheet offers 50% PAR diffusion at 85% transmission, accompanied by a 10-year warranty, making it well-suited for Mediterranean hail risk. Limited subsidy support in Eastern Europe still favors cheaper polyethylene film, hindering the adoption of more expensive alternatives outside grant-funded projects.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Bisphenol-A price volatility and feedstock supply shocks | -0.40% | EU-27, with acute exposure in Germany, Poland, Czech Republic (resin import-dependent) | Short term (≤ 2 years) |

| Competition from lower-cost PMMA and glass in low-spec roofs | -0.50% | Southern Europe (Spain, Italy, Greece), Eastern Europe | Medium term (2-4 years) |

| Limited recycling streams for multilayer sheets | -0.30% | EU-27, particularly Germany, France, Netherlands (strict circular-economy mandates) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Bisphenol-A Price Volatility and Feedstock Supply Shocks

European BPA spot prices swung 20% intra-year, reaching USD 1,320/t in March 2025, as Chinese oversupply met sluggish resin demand, compressing extruder margins locked into fixed-price construction contracts. German, Polish, and Czech sheet producers import BPA and diphenyl carbonate, making them vulnerable to freight cost spikes through Rotterdam or Hamburg. Sinopec and Wanhua's capacity additions of 500 kt/y through 2026 may further depress prices; yet, any outage could lift BPA costs by 30-40% within weeks, as European converters carry lean inventories.

Competition from Lower-Cost PMMA and Glass in Low-Spec Roofs

Polyvantis, created in September 2024 by merging Röhm’s Plexiglas and SABIC’s Functional Forms, underscores acrylic’s 15-20% cost advantage in residential conservatories where impact resistance matters less. Glass still dominates flat glazing in price-sensitive Southern Europe, while polycarbonate corrugated panels win only when installers value weight savings and shatter resistance. Arla Plast reported intensified price competition in 2024, noting weaker demand from the automotive and construction sectors despite broader product diversification. Scratch resistance and long-term clarity keep glass competitive in low-spec applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Multiwall Dominance Driven by Thermal Mandates

Multiwall sheets contribute 59.18% of the polycarbonate sheets market share in 2025, buoyed by Ug ≤ 1.1 W/m²K performance that satisfies EPBD thresholds. The EXOLON Hybrid-X range, certified to EN 16153 and warrantied for 20 years, exemplifies five- and seven-wall configurations that balance insulation and achieve≥45% light transmission. Corrugated sheets are forecast to lead growth at 3.12% CAGR through 2031 as civil-engineering capex rises, with transport shelters and noise barriers favoring higher stiffness-to-weight ratios. Solid sheets remain a niche market—machine guards, EN 45545-2 rail interiors, and UL94 V-0 electrical enclosures—where optical clarity and flame resistance justify premiums.

Corrugated formats increasingly replace polyethylene films in Mediterranean horticulture, extending greenhouse cover life to 10-15 years. Brett Martin’s new cap-and-base connector profile for 6-10 mm multiwall sheets addresses historical leak concerns that have limited adoption in high-exposure roofing, offering a 10-year water-tightness guarantee. The solid sheet trajectory hinges on broader EV adoption of polycarbonate glazing; delays in mass-market model rollouts to 2026-2028 constrain near-term volume, although rising demand for fire-retardant sheets in Europe’s rail modernization pipeline offers a substitute growth avenue.

By End-User Industry: Construction Share Pressured by Renovation Slowdown

Construction held 65.05% of 2025 polycarbonate sheets market size, yet a 7.7% drop in 2024 residential renovation and a further 3.9% fall expected for 2025 temper near-term outlook. Non-residential and civil-engineering segments lend resilience, with translucent roofing retrofits in logistics and transport hubs supported by EU recovery funds. Agriculture is set to grow the fastest at a 2.92% CAGR (2026-2031) as diffusive multiwall panels lift tomato yields by ≈8% and national greenhouse strategies in Spain and France subsidize modernization.

Automotive glazing, although small in tonnage, remains strategic: Covestro’s Antwerp copolymer plant, opened in March 2024, targets OEM demand for panoramic roofs, sensor covers, and haptic touch panels. Arla Plast noted “further weakened” 2024 automotive demand, reinforcing reliance on industrial LED diffusers and machine-guard applications. Aerospace remains negligible due to lengthy FAR 25.853 approvals and substitution by advanced PMMA or acrylic-silicone blends.

Geography Analysis

Germany accounts for 22.10% of 2025 consumption and a 3.28% CAGR forecast to 2031, driven by greenhouse upgrades in North Rhine-Westphalia and Lower Saxony, as well as steady procurement for noise-barrier panels along federal highways. Yet housing weakness (-1.9% in 2024) caps growth in conservatory and skylight retrofits. France’s construction investment declined by 3.9% in 2024, but modest public infrastructure work sustained multiwall demand. Italy experienced 6.5% growth in non-residential and 21% growth in civil engineering, thanks to EU recovery funds, which drove an increase in corrugated uptake in logistics terminals.

Spain, Portugal, and Greece outpace Western peers as deferred 2020-2022 maintenance converts into re-roofing contracts. Spain’s greenhouse cluster in Almería adopts near-infrared-reflective polycarbonate to limit internal temperatures above 40°C, while Portuguese installers replace asbestos panels with corrugated sheets to meet EPBD mandates. The Benelux nations serve as innovation hubs: SABIC’s Bergen op Zoom plant supplies ISCC PLUS-certified TRUCIRCLE resin, and Covestro reinforces its copolymer capacity in Antwerp. Nordic countries enforce EN 17037 strictly, favoring diffusive glazing for north-facing rooflights even as private housing starts fall sharply. Turkey’s extrusion sector, led by Sümer Plastik and Isik Plastik, exports low-cost corrugated sheets to Southern Europe. The UK, post-Brexit, aligns with Building Regulations Part L rather than EPBD, yet Brett Martin’s Northern Ireland plant supplies both markets, benefiting from reduced tariffs on EU exports. Central-Eastern Europe—Romania, Poland, Czech Republic—gains from EU-financed infrastructure, particularly Romania’s projected 21% construction growth in 2025, boosting corrugated panel demand for transport corridors.

Value Chain Analysis

The value chain starts with upstream petrochemical and chlor-alkali inputs that feed bisphenol A (BPA) and polycarbonate resin production, followed by compounding (UV stabilizers, flame-retardant packages, colorants) and sheet extrusion (solid, corrugated, and multiwall). European resin production is concentrated around large integrated sites in Germany, the Netherlands, Belgium, and Spain, with anchors including Covestro (Antwerp, Belgium and Krefeld-Uerdingen, Germany) and SABIC (Bergen op Zoom, Netherlands and Cartagena, Spain). Covestro inaugurated a new polycarbonate copolymer production plant at its Antwerp site in March 2024, signaling ongoing capability investment in higher-value grades that flow into glazing and specialty sheet applications.

Midstream, European sheet extruders convert resin into standardized and application-engineered panels (co-extruded UV layers, diffusive/IR-reflective structures, and certified multiwall products aligned with EN 16153). They increasingly bundle installation systems (profiles, connectors, and warranties) to protect margins. Distribution typically runs through building-material wholesalers, plastics distributors, and fabricators or roofing-system integrators, while larger construction and mobility customers increasingly use direct sourcing and project-based specification. Key bottlenecks and risk points include sensitivity to BPA price swings and logistics constraints for hazardous intermediates such as phosgene, along with reliance on specialized additive packages for fire and weathering performance.

Competitive Landscape

The European Polycarbonate Sheets Market is moderately consolidated. Covestro, SABIC, and Palram anchor resin production and large-format extrusion, but European capacity continues to decentralize. Polyvantis, formed in September 2024, unites Plexiglas and Lexan brands across 15 sites, hedging polycarbonate with PMMA as price-sensitive applications migrate toward lower-cost acrylic. Arla Plast’s EUR 9.5 million acquisition of Spain’s Nudec added SEK 670 million (≈ USD 64 million) in sales and strengthened its southern reach, while EXOLON upgraded its portfolio with ECOplus variants containing up to 89% sustainable content.

Europe Polycarbonate Sheets Industry Leaders

SABIC

EXOLON GROUP GMBH

Brett Martin

Corplex

Palram Industries Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Energy-efficiency and daylighting compliance in the building envelope keep specification-led whitespace open for premium multiwall and system solutions, especially where EN 17037 daylighting documentation and EPBD-driven renovation pathways favor low-Ug, diffusive roof and facade elements. With construction already accounting for 65.05% of 2025 demand and multiwall holding 59.18% share, producers can expand value per square meter through integrated panel systems, longer warranties, and application-tailored coatings (anti-drip, IR-reflective, and enhanced UV protection) that target installer pain points such as leakage and long-term clarity.

Circularity and compliance are also becoming more operationally material across the chain, creating opportunities for recycled-content and mass-balance offerings, improved pellet-handling practices, and traceability services for OEMs and distributors. Regulation (EU) 2025/2365 (adopted November 12, 2025) introduces stricter requirements to prevent plastic pellet losses across the supply chain, affecting processors and recyclers, and strengthening the business case for upgraded handling, containment, and auditing. On the supply side, capability and footprint consolidation creates room for service-led competition: Exolon Group signed an agreement in July 2025 to acquire Corplex’s AkyVer polycarbonate sheet business and integrate production into Nera Montoro, Italy, reflecting customer pull for regionalized supply, shorter lead times, and consistent sheet quality for construction and agricultural glazing programs.

Recent Industry Developments

- June 2026: Brett Martin introduced Marlon R-Glaze Diamond, a premium canopy glazing system using diamond-embossed polycarbonate sheets for outdoor living and light-roof structures. The launch expands differentiation beyond commodity sheet supply by packaging performance, aesthetics, and system-level fit for installers and fabricators.

- August 2025: Brett Martin announced a new manufacturing joint venture, American Polycarbonate Company (APC), in De-Pere, Wisconsin, to support growth in North America. Building additional capacity outside Europe helps rebalance supply and improves resilience for global customers that source polycarbonate sheet solutions across regions.

- December 2024: SIA Ultraplast EU unveiled a new extrusion line dedicated to multiwall polycarbonate sheets, doubling the company’s manufacturing capacity. Added local output supports faster fulfillment for construction and greenhouse projects where multiwall specifications are tied to thermal and daylighting requirements.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers polycarbonate sheet products sold in Europe, measured as the volume of sheets consumed across major end uses such as construction, agriculture, automotive, and electrical and electronics.

Scope exclusions: Excludes polycarbonate resin and compounds that are not converted and sold as sheet, and it also excludes non-polycarbonate sheet materials used as substitutes.

Segmentation Overview

- By Type

- Solid

- Corrugated

- Multi-walled

- By End-user Industry

- Aerospace

- Agriculture

- Automotive

- Construction

- Electrical & Electronics

- Others (including Signage, Security and Police Gear, and Solar Panels)

- By Geography

- Germany

- France

- Italy

- Spain

- Benelux Countries

- Nordic Countries

- Turkey

- United Kingdom

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building the fact base on supply, trade, and end use activity for polycarbonate sheets in Europe. We refer to public sources such as Eurostat for construction and industrial indicators, UN Comtrade style customs statistics for trade flows, EU regulatory publications on building energy performance, and national statistics offices for housing and infrastructure activity.

To translate those signals into a usable model, we also check company annual reports and investor presentations to understand product mix and regional exposure, and we use reputable press and association websites for capacity additions, plant outages, and downstream demand notes. Where needed, paid subscriptions for company financials and intelligence, patent databases, and shipment-level import and export data help confirm directionality and reduce gaps in country splits. The sources listed here are illustrative, and many additional public and paid references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating sheet demand by type and end use, and on stress-testing assumptions such as typical thickness mix and ordering patterns through distribution channels. We spoke with a mix of manufacturers, converters, distributors, and large end users across key European countries, so that pricing movements and volume changes could be checked against real buying cycles and project pipelines.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 17% | |

| Mid tier: 54% | Functional/Unit leaders: 33% | |

| Smaller Players: 18% | Managers: 50% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where construction activity, greenhouse coverage additions, and industrial production indicators are converted into an addressable demand pool for polycarbonate sheets, and then filtered by usage intensity for typical applications like roofing, facades, glazing, and protection panels. To keep totals realistic, we corroborate the outcome with selective bottom-up checks, including sampled supplier volume ranges by country, distributor channel checks, and spot validations of average sheet thickness mix that drives tonnage.

Key inputs shaping the model include new building and renovation intensity, infrastructure and civil engineering outlays that favor corrugated formats, agricultural protected cultivation expansion that supports multiwall demand, and substitution trends versus glass and acrylic in common applications. For forecasting, we run scenario analysis, guided by what industry participants expect for construction starts, retrofit pace, and energy-efficiency driven adoption in major countries. Where country data is thin, proxy indicators and trade flows are used to fill the gap, followed by a consistency pass so country totals align with the regional story.

Data Validation & Update Cycle

Validation is done through several checks so results do not rely on one data stream. We compare modeled consumption with independent signals such as import and export direction, capacity change announcements, and end use momentum, and then review and correct any large variances with clear notes on what changed.

Before final sign-off, the model is reviewed in steps by another analyst to catch unit errors, timing mismatches, and unusual price or volume jumps. The report is refreshed annually, and interim updates are triggered when material events occur, such as major capacity shifts, regulatory changes affecting building envelopes, or sharp demand shocks. Right before delivery, a final update pass is completed so clients receive the latest adjusted view.

Mordor Intelligence's Europe Polycarbonate Sheets Market Sizing Compared With Other Published Estimates

It is normal to see different market sizes for the same topic because publishers do not always measure the same thing, in the same unit, or for the same time period. Differences also come from how pricing is treated versus volume, which countries are included in Europe, and whether the scope stays limited to sheets or widens to adjacent plastics formats.

By tracking unit-consistent tonnage across countries and end uses, and then refreshing the cross-checks in the model, Mordor Intelligence keeps the estimate tied to physical sheet consumption rather than mixing revenue assumptions that can swing with short-term price cycles.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.11 M (2025) | |

| Industry Publisher A | USD 1.89 B (2024) | Uses a revenue-based frame, which can embed ASP assumptions by thickness, coating, and channel margins, and it can also capture price inflation effects that do not change underlying sheet tonnage. |

| Consultancy B | USD 0.55 B (2020) | An older base year and a shorter horizon can understate recent construction retrofit demand, and the Europe boundary and end-use mix can differ, which shifts totals even when product types look similar. |

The spread in the table mainly reflects unit choice and time alignment, and it also reflects how tightly the scope stays on polycarbonate sheets versus broader revenue pools. When inputs are anchored to clear demand indicators and checked with supply and trade signals, the final number becomes easier to reproduce and to explain in a planning discussion.

Key Questions Answered in the Report

How large is the polycarbonate sheets market in Europe in 2026?

The market is 111.44 kilotons in 2026 and is projected to reach 127.21 kilotons by 2031.

Which product type leads demand in Europe?

Multiwall sheets hold 59.18% share, favored for low Ug values required by EU energy codes.

What end-use segment is growing fastest?

Agriculture posts a 2.92% CAGR as diffusive glazing boosts greenhouse crop yields.

Why are corrugated sheets gaining traction?

A 5.8% rise in civil-engineering spending drives demand for lightweight roofing in transport shelters and noise barriers.

How do EU directives influence sheet demand?

The revised EPBD and EN 17037 daylighting standards mandate energy-efficient, naturally lit building envelopes, favoring multiwall polycarbonate.

Page last updated on: