Wood Adhesives Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

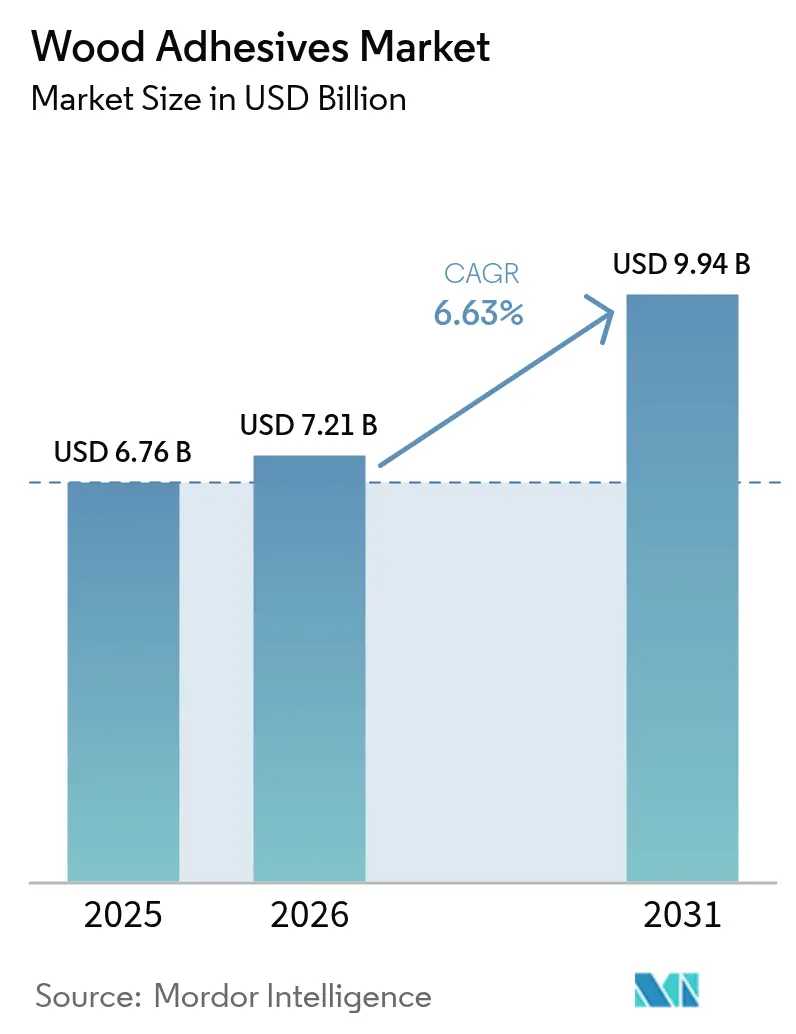

| Market Size (2026) | USD 7.21 Billion |

| Market Size (2031) | USD 9.94 Billion |

| Growth Rate (2026 - 2031) | 6.63% CAGR |

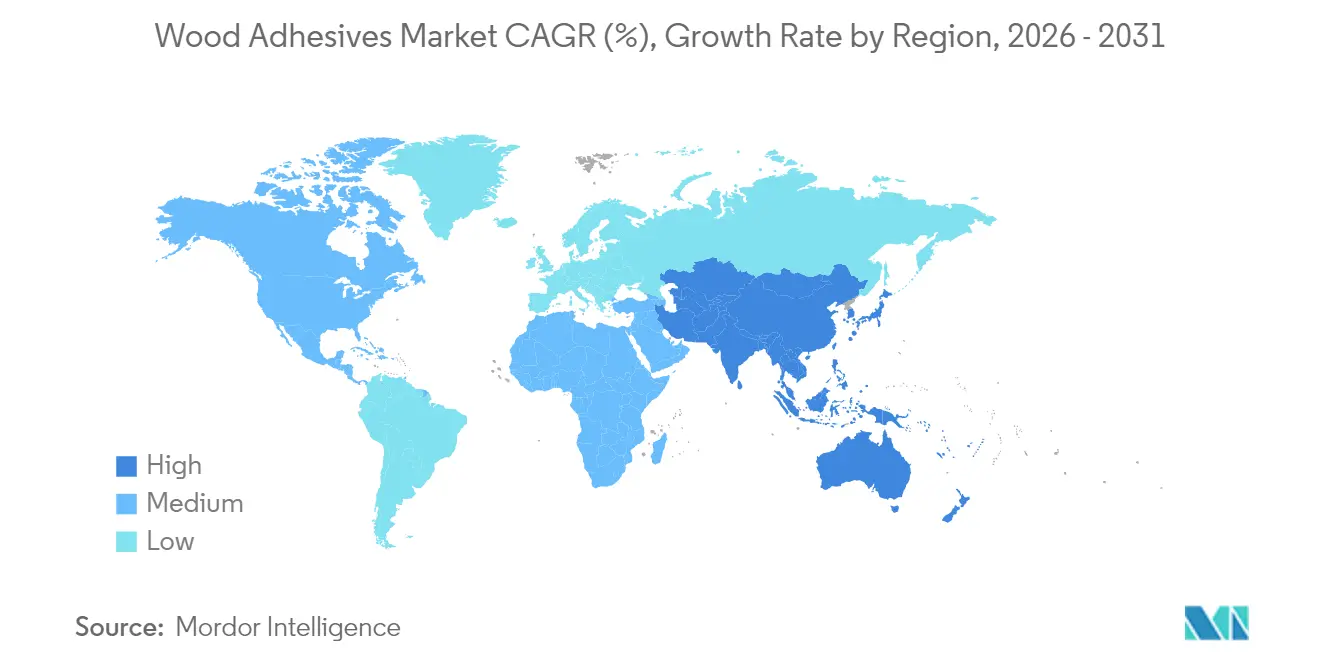

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wood Adhesives Market Analysis by Mordor Intelligence

The Wood Adhesives Market size was valued at USD 6.76 billion in 2025 and estimated to grow from USD 7.21 billion in 2026 to reach USD 9.94 billion by 2031, at a CAGR of 6.63% during the forecast period (2026-2031).

The steadily rising output of engineered wood, especially in Asia Pacific where capacity climbed 8% to 221 million m³ in 2024, anchors demand for high-performance bonding solutions. Rapid migration toward low-VOC, water-based chemistries and the accelerating adoption of mass-timber structures sustain growth momentum, while incremental innovations in synthetic and bio-based resins broaden application windows. Competitive intensity remains moderate, with scale leaders investing in Industry 4.0 process control and targeted M&A to protect share amid tightening environmental rules. Long-term opportunities center on structural adhesives for cross-laminated timber (CLT), reversible bonding chemistries for circular design, and region-specific formulations that optimize cost-to-performance metrics.

Key Report Takeaways

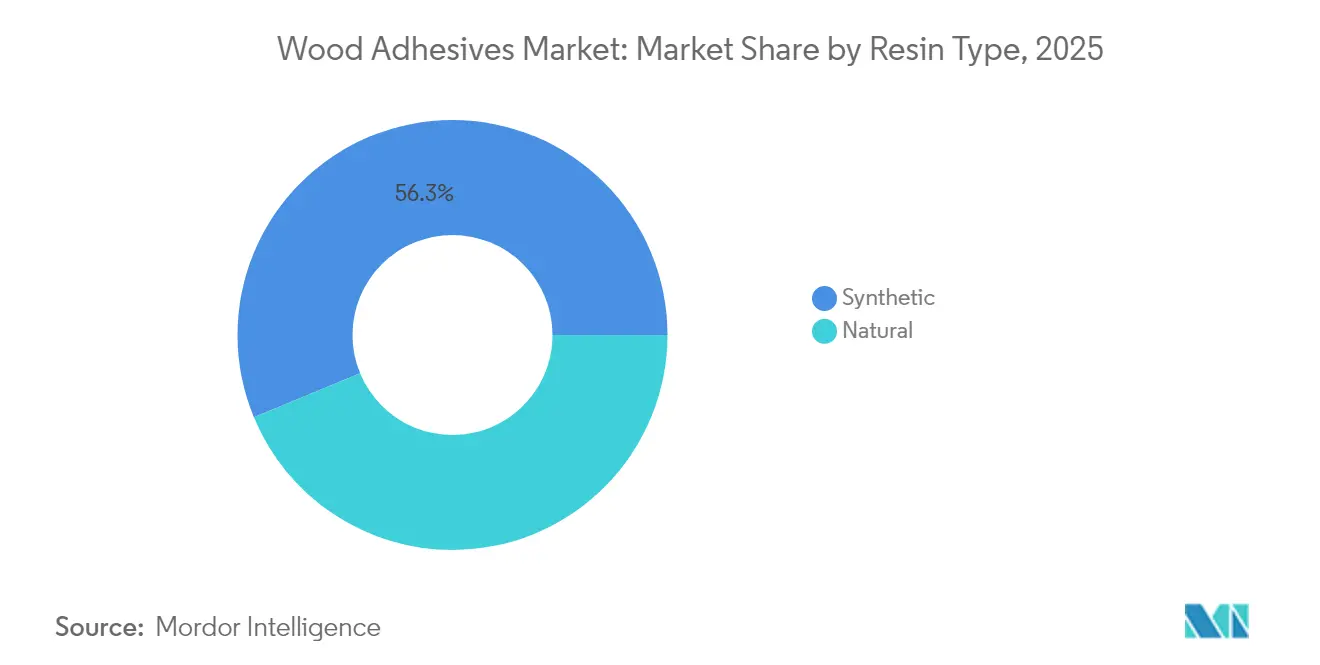

- By resin type, synthetic resins led with 56.25% revenue share in 2025, and are advancing at a 7.05% CAGR to 2031.

- By technology, water-based systems captured 37.90% of the wood adhesives market share in 2025, and are projected to expand at 6.95% CAGR through 2031.

- By application, furniture commanded 30.10% of the wood adhesives market size in 2025; cabinets is the fastest-growing end-user at 6.72% CAGR through 2031.

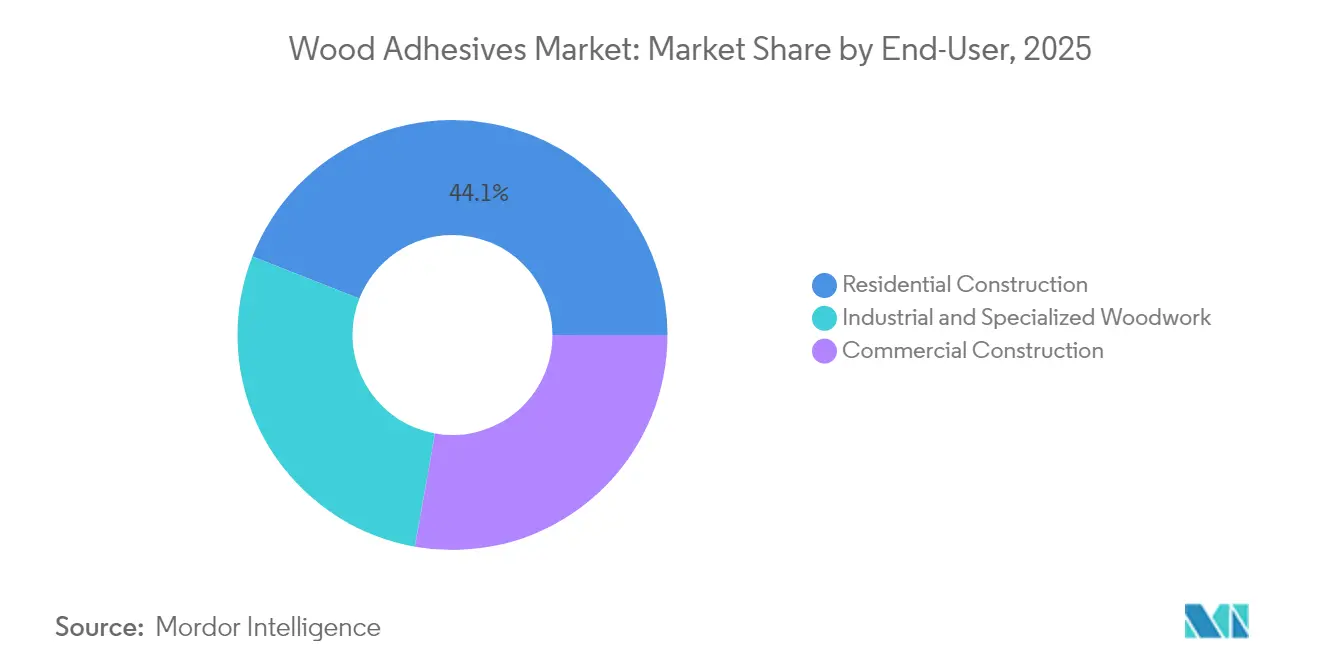

- By end-user, the residential construction segment commanded 44.05% of the wood adhesives market size in 2025; industrial and specialized woodwork is the fastest-growing end-user at 7.55% CAGR through 2031.

- By geography, Asia Pacific held 41.70% revenue share of the wood adhesives market in 2025 and is forecast to grow at 7.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Wood Adhesives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging engineered-wood production in Asia Pacific | +2.10% | Asia Pacific core, spill-over to global supply chains | Medium term (2-4 years) |

| Rapid shift to low-VOC, water-based systems | +1.80% | Global, with regulatory leadership in California & EU | Short term (≤ 2 years) |

| Renovation boom in Europe furniture sector | +1.30% | Europe, with secondary impact in North America | Medium term (2-4 years) |

| Mass-timber (CLT & glulam) adoption in high-rise projects | +1.10% | North America & EU, emerging in Asia Pacific | Long term (≥ 4 years) |

| Integration of Industry 4.0 technologies enhancing precision in adhesive application and curing. | +0.60% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Engineered-Wood Production in Asia Pacific

China’s plywood capacity rose 8% to 221 million m³ in 2024 even as producer numbers fell 19%, revealing scale efficiencies that heighten demand for sophisticated adhesives. Vietnam’s record wood-product exports to the United States and China’s 13.27 million m³ plywood export volume show r egional output feeding worldwide value chains. Local growth drives domestic consumption, while export-oriented manufacturing multiplies volumes for water-resistant, heat-stable bonding agents. Concurrent bio-polymer investments across China, Thailand, and India further stimulate sustainable resin development.

Rapid Shift to Low-VOC, Water-Based Systems

Water-based chemistries already command 38.12% share and are growing 7.14% as regulations tighten. California’s CARB Phase II limits formaldehyde to 0.05 ppm for hardwood plywood, while the EU will cap emissions at 0.062 mg/m³ by August 2026[1]California Air Resources Board, “Composite Wood Products Regulation,” California ARB, arb.ca.gov . Producers, notably H.B. Fuller, now allocate 60% of R&D budgets to sustainable formulations such as Swiftmelt 1850 for recyclable packaging. Water-based systems lower handling costs and improve shop-floor safety while advances in polymer cross-linkers are closing historical performance gaps.

Renovation Boom in Europe Furniture Sector

European furniture demand is stabilizing at 4-6% annual growth as homeowners prioritize sustainability and flexible interiors. In 2024, German OSB prices experienced a slight increase. signifying steady consumption despite macro headwinds. Homann Holzwerkstoffe posted EUR 354.5 million revenue in 2024 and targets 50% bio-based adhesive use by 2030, reflecting tighter circular-economy criteria. Renovation projects challenge formulators with dissimilar substrates, accelerated cure cycles, and salvageable joints for future recycling.

Mass-Timber (CLT & Glulam) Adoption in High-Rise Projects

More than 2,100 US mass-timber projects are registered, up from 1,650 one year earlier. Code revisions now recognize timber skyscrapers such as Milwaukee’s 32-story Edison building, catalyzing specialized structural-grade adhesives. Hexion offers melamine and resorcinol resins tailored for CLT panels that pass Green certification and withstand prolonged fire exposure. Demand centers on long-life strength, moisture tolerance, and heat-stable bonds across massive surface areas.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile petro-feedstock (phenol, formaldehyde) prices | -1.40% | Global, with particular impact on cost-sensitive markets | Short term (≤ 2 years) |

| Stricter indoor-air VOC caps in California & EU | -1.20% | California & EU core, with global supply chain implications | Short term (≤ 2 years) |

| Limited supply of bio-based polyols/starches | -0.80% | Global, with supply constraints in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Petro-Feedstock Prices

Phenol-formaldehyde resin costs fluctuated sharply in 2024, squeezing margins when feedstock represents 75% of cost of sales as reported by H.B. Fuller. Smaller manufacturers struggle to hedge volatility, prompting contract revisions and greater reliance on spot markets. Price spikes pass through the supply chain unevenly, risking demand substitution when rising adhesive costs cannot be absorbed by furniture or panel producers.

Limited Supply of Bio-Based Polyols/Starches

USDA pinpoints infrastructure gaps that restrict biomass flow for industrial biochemicals. Pilot-scale breakthroughs, such as Beijing Forestry University’s xylan-based hot-melt with 30 MPa lap-shear strength, illustrate performance viability yet remain hindered by feedstock scarcity[2]Phys.org, “Xylan-Based Hot-Melt Adhesive Breakthrough,” Phys.org, phys.org . Stora Enso’s NeoLigno lignin binder demonstrates commercial intent but faces capex and sourcing hurdles[3]Stora Enso Oyj, “NeoLigno® Binder Launch,” Stora Enso, storaenso.com . Supply deficits slow the wood adhesives industry’s transition to fully renewable inputs, tempering potential CAGR upside.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Synthetic Dominance Drives Innovation

Synthetic resins accounted for 56.25% of 2025 revenue, underscoring cost-to-performance leadership even as environmental scrutiny intensifies. This segment is expected to clock 7.05% growth through 2031 as ultra-low-emitting (ULEF) and no-added-formaldehyde (NAF) chemistries reach commercial maturity. Makers are blending bio-fillers—such as modified corn-cob powder that hikes bond strength up to 19.6%—to curb emissions by 27.8%. Synthetic platforms thus set performance benchmarks while steadily lowering environmental footprints, sustaining their primacy in the wood adhesives market.

Eco-adoption is fastest in jurisdictions with tight indoor-air codes, channeling R&D toward phenol substitutes without compromising structural integrity. Acorn-enhanced phenolic resins attaining 0.93 MPa shear strength show that hybrid chemistry can marry bio-content with proven curing behavior. As IoT-enabled reactors optimize reaction kinetics and feed precision, manufacturers unlock further gains in consistency and throughput.

By Technology: Water-Based Systems Lead Environmental Transition

Water-based processes held 37.90% share in 2025 and will scale at 6.95% as global emission caps converge. These formulations reduce plant energy loads because they forgo high-temperature flash-off and lower solvent recovery expenses. Celanese and Henkel now convert captured CO₂ into polymer backbones, shrinking cradle-to-gate footprints by 25%. Application equipment has evolved, using laser-guided nozzles that meter thin, uniform films to offset historically higher water weight.

Reactive hot-melts, UV-curable dispersions, and digital-tailored hybrid emulsions round out the technology mix, each suited to niche throughput and environmental profiles. Continuous inline monitoring enables real-time viscosity adjustments, ensuring bond repeatability at speed and elevating the wood adhesives market’s operational efficiency.

By Application: Furniture Leadership Amid Cabinet Growth

Furniture remained the largest consumer at 30.10% in 2025, anchored by standardized production lines that favor high-output, cost-efficient adhesives. Cabinet manufacturing is rising at 6.72% CAGR as remodelers opt for premium finishes that demand stronger, invisible joints. Green adhesives for oriented strand board now achieve 94% of traditional bending strength benchmarks, signaling viable uptake for low-emission substrates.

Retail buyers increasingly request traceability for indoor-air compliance, pressing suppliers to validate every bonding layer. Adhesives that enable end-of-life dismantling gain traction in Europe’s take-back schemes, giving rise to reversible cross-link technologies that can be de-activated at moderate heat without damaging surface veneers.

By End-User: Residential Construction Dominance with Industrial Growth

Residential building absorbed 44.05% of adhesive volume in 2025. Home renovations lean on water-based, fast-grab products to shorten downtime. Industrial and specialized woodwork, however, will post the fastest 7.55% CAGR through 2031 because cross-laminated timber, acoustical panels, and energy-efficient façades require precision bonding delivered by automated lines.

AI-guided robots like those integrated after Hexion’s Smartech acquisition modulate spread rates and UV-intensity in real time, trimming scrap and elevating structural reliability. Industrial users thus treat adhesive capability as a core quality lever, reinforcing steady scaling of the wood adhesives market.

Geography Analysis

Asia Pacific accounted for 41.70% of 2025 spending and is tracking 7.12% CAGR to 2031 due to export-oriented panel plants and vast domestic infrastructure programs. China shipped 13.27 million m³ of plywood worth USD 5.271 billion in 2024, servicing buyers in Taiwan, Vietnam, and the Middle East. North America’s wave of mass-timber towers and federal infrastructure packages fuels specialty structural adhesive uptake. Europe’s stricter chemical and recycling mandates push rapid conversion to low-VOC systems, often catalyzing technology spillovers into other regions.

Brazil and Chile continue to invest in forestry mills, inviting entrants such as Sika to add local blending units. Middle East capacity additions in engineered-wood lines underscore global supply interdependencies, where feedstock, technology, and end-use trends cross-pollinate to advance the wood adhesives market worldwide.

Competitive Landscape

The competitive field is moderately fragmented. Henkel’s Adhesive Technologies unit registered EUR 10.97 billion revenue in 2024, illustrating scale leverage on purchasing and R&D intensity. H.B. Fuller allocates 60% of new-product spending to sustainability-linked solutions, defending share amid tightening VOC norms. Sika uses bolt-on acquisitions and regional plant debottlenecking to capture growth from Asia and South America.

Strategic collaborations are rife. Dow, Henkel, and Kraton achieved a 25% carbon-footprint cut in TECHNOMELT hot-melts through bio-materials substitution. Hexion’s Smartech deal injects AI process control that boosts press-line yield by up to 6% while minimizing resin waste. Emerging specialists in lignin-based resins or reversible bonds address niches that large incumbents prefer to partner with rather than build from scratch.

Regional challengers exploit logistics proximity and local compliance knowledge to outmaneuver global brands on service. Nonetheless, innovation capital and brand trust still advantage multinationals, especially in long-cycle structural projects where liability risk skews purchaser preference to historically vetted suppliers.

Wood Adhesives Industry Leaders

Henkel AG & Co. KGaA

H.B. Fuller Company

Arkema Group (Bostik)

Sika AG

Akzo Nobel N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2023: Sika has launched MB EZ Rapid, a single-component, fast-drying moisture barrier and adhesive substrate consolidator designed for residential and commercial flooring installations. The product is compatible with plywood, thereby enhancing the wood adhesives market.

- May 2023: Henkel's Engineered Wood division presented its advanced portfolio of solutions for the mass timber industry at LIGNA 2023. The presentation highlighted sustainable innovations and adhesives designed to enhance fire performance.

Global Wood Adhesives Market Report Scope

Wood adhesives are polymeric compounds capable of reacting with the surface of the wood in such a way that stresses are passed between bonded elements. Wood adhesives manufacture windows, doors, furniture, wooden flooring, and others. The wood adhesives market is segmented by resin type, technology, application, and geography. By resin type, the market is segmented into natural and synthetic. By technology, the market is segmented into solvent-based, water-based, and other technologies. By application, the market is segmented into furniture, plywood, cabinets, doors, windows, and other applications. The report also covers the market size and forecasts in 15 countries across major regions. Market sizing and forecasts are based on each segment's revenue (USD million).

| Natural |

| Synthetic |

| Water-based |

| Solvent-based |

| Other Technologies |

| Furniture |

| Plywood |

| Cabinets |

| Doors and Windows |

| Other Applications |

| Residential Construction |

| Commercial Construction |

| Industrial and Specialized Woodwork |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Middle East and Africa |

| By Resin Type | Natural | |

| Synthetic | ||

| By Technology | Water-based | |

| Solvent-based | ||

| Other Technologies | ||

| By Application | Furniture | |

| Plywood | ||

| Cabinets | ||

| Doors and Windows | ||

| Other Applications | ||

| By End-User | Residential Construction | |

| Commercial Construction | ||

| Industrial and Specialized Woodwork | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the wood adhesives market?

The wood adhesives market stands at USD 7.21 billion in 2026.

How fast is the wood adhesives market expected to grow?

The market is forecast to expand at a 6.63% CAGR, reaching USD 9.94 billion by 2031.

Which resin type holds the largest share in the wood adhesives market?

Synthetic resins lead with 56.25% revenue share in 2025.

Why are water-based adhesives gaining popularity?

Tight VOC and formaldehyde limits in California and the EU, coupled with comparable performance, drive 6.95% CAGR in water-based systems.

Which region dominates the wood adhesives market?

Asia Pacific captured 41.70% of global revenue in 2025, supported by robust engineered-wood capacity.

What are the main challenges for bio-based wood adhesives?

Limited feedstock supply and scaling constraints temper adoption despite strong regulatory and customer pull.

Page last updated on: