Vegan Confectionery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.8 Billion |

| Market Size (2031) | USD 2.91 Billion |

| Growth Rate (2026 - 2031) | 10.08% CAGR |

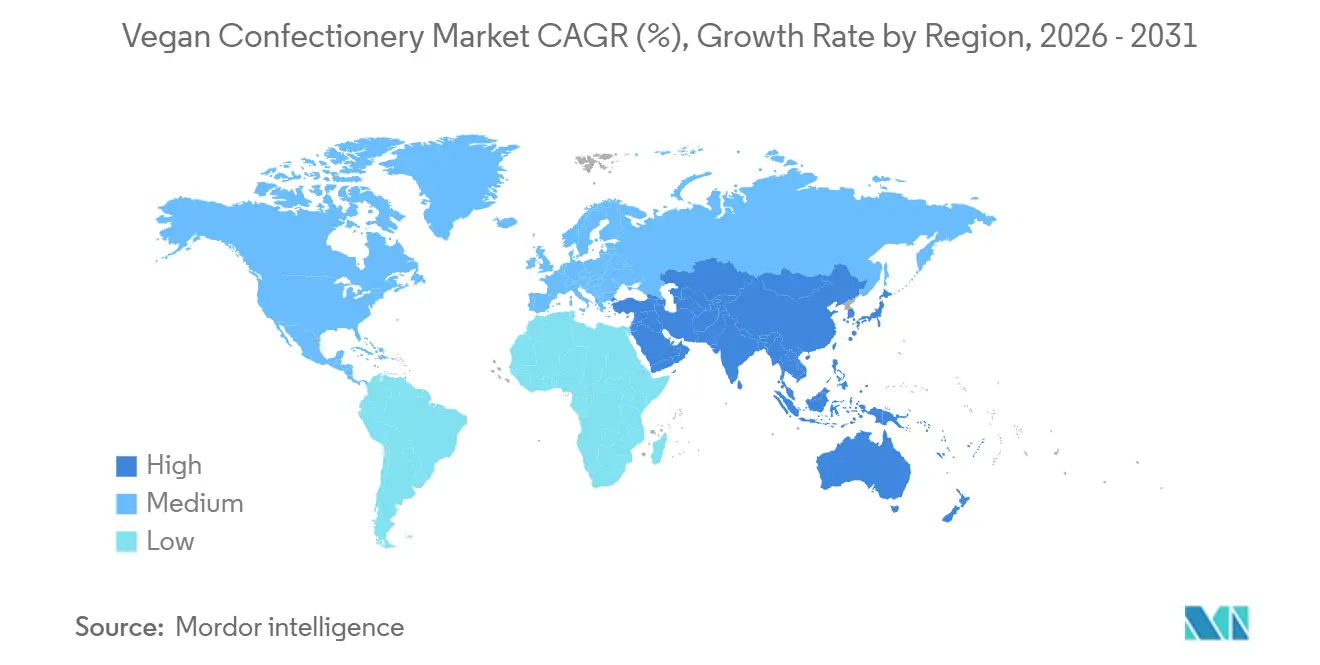

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

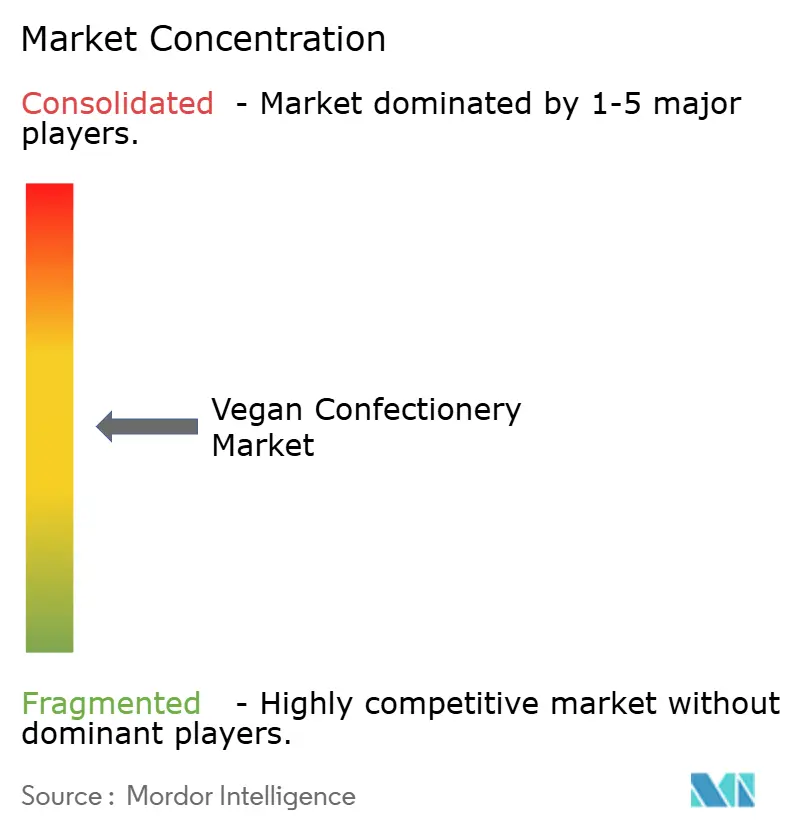

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Vegan Confectionery Market Analysis by Mordor Intelligence

The vegan confectionery market was valued at USD 1.71 billion in 2025 and is projected to grow from USD 1.8 billion in 2026 to USD 2.91 billion by 2031, registering a CAGR of 10.08% during the forecast period (2026-2031). Growth in the market is driven by increasing consumer preference for plant-based treats, stricter sustainability regulations in major supply regions, and advancements in texture replication technologies. The EU Deforestation Regulation, effective December 2024, has accelerated the development of cocoa-free products, prompting manufacturers to explore innovative alternatives to traditional cocoa-based ingredients [1]Source: European Union," Cocoa under the Deforestation Regulation", europa.eu. Additionally, investments in precision fermentation in Asia and North America are expanding the availability of plant-derived sweeteners and fats, enabling manufacturers to develop more sustainable and versatile product offerings. Further momentum is provided by advancements in pectin gel systems, which improve product texture and stability, rising interest in functional botanicals catering to health-conscious consumers, and the growth of direct-to-consumer (DTC) channels, which allow brands to connect directly with their target audience. In 2024, China launched an initiative to diversify its food supply system, with a focus on promoting plant-based innovations. Supported by government research programs, this initiative is expected to drive the growth of vegan confectioneries in the country[2]Source: Ministry of Ecology and Environment of the People's Republic of China, "Opinions of the General Office of the State Council on practicing the big food concept and building a diversified food supply system", gov.cn. In response, market leaders are expanding their plant-based product portfolios, increasing investments in alternative ingredient capacities, and accelerating acquisitions of specialty brands to strengthen their market position and address evolving consumer preferences.

Key Report Takeaways

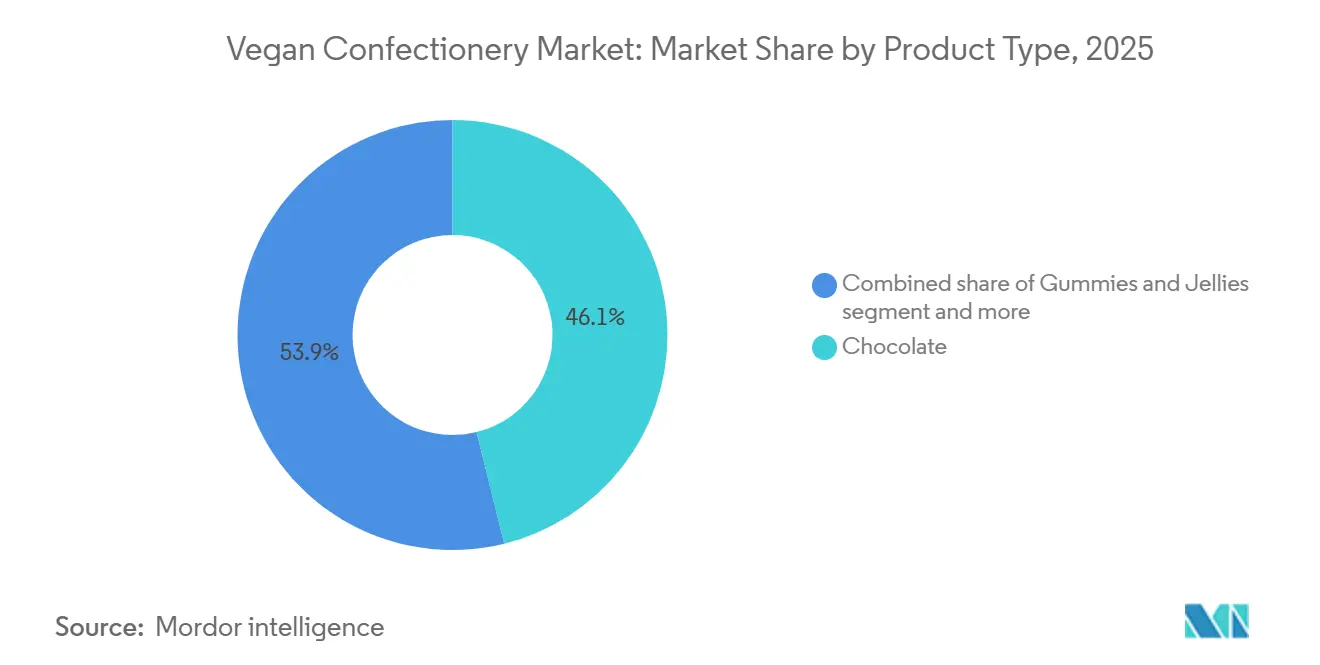

- By product type, chocolate held 46.13% of the vegan confectionery market share in 2025, and gummies and jellies are projected to post the fastest 10.18% CAGR through 2031.

- By category, sugar-based lines accounted for 68.19% of the vegan confectionery market size in 2025, while sugar-free alternatives are expected to grow at an 10.58% CAGR between 2026-2031.

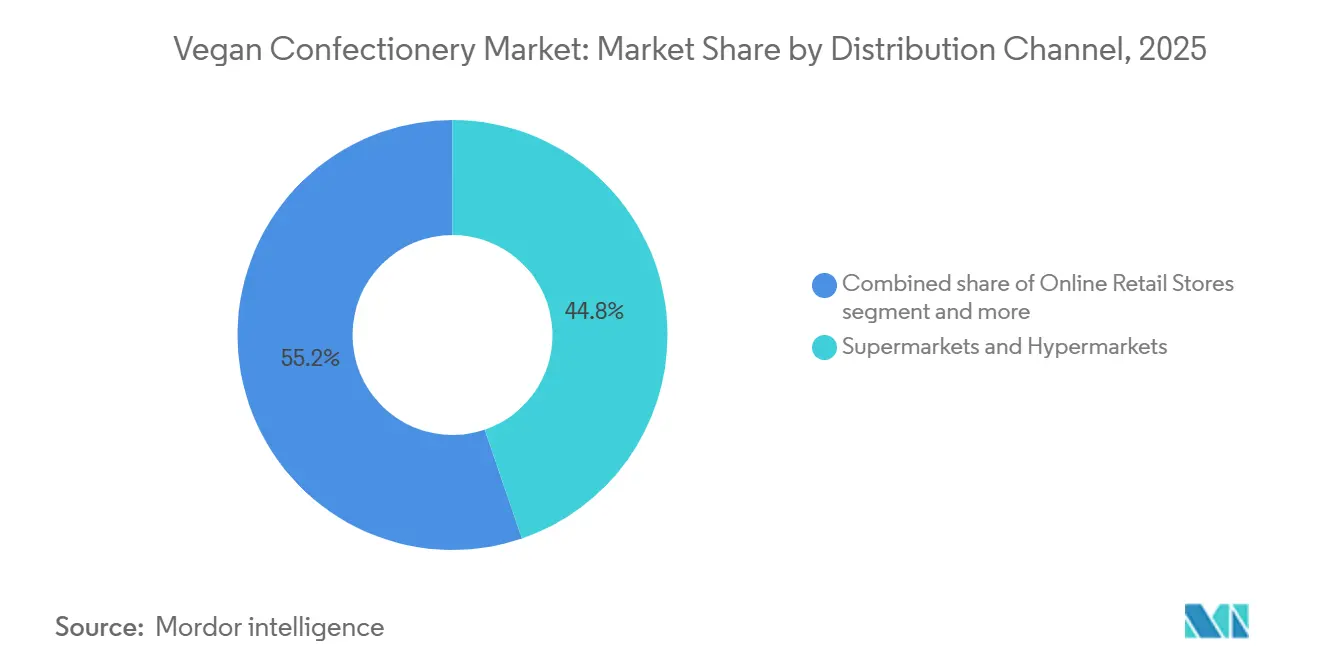

- By distribution channel, supermarkets and hypermarkets led with 44.76% revenue share in 2025; online retail is forecast to expand at a 11.07% CAGR to 2031.

- By geography, North America commanded 38.40% revenue share in 2025, whereas the Asia-Pacific is anticipated to record the highest 10.41% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Vegan Confectionery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising vegan and flexitarian demographics | +2.1% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Growing lactose-intolerant/allergy population | +1.8% | Global, higher impact in Asia-Pacific and North America | Long term (≥ 4 years) |

| Ethical and environmental sustainability push | +1.5% | Europe and North America core, expanding to Asia-pacific | Long term (≥ 4 years) |

| Innovation in functional and fortified vegan confectionery | +1.2% | North America and Europe, emerging in Asia-Pacific | Short term (≤ 2 years) |

| Innovation in plant-based ingredients | +0.9% | Global, led by European innovation hubs | Medium term (2-4 years) |

| Retailer private-label vegan lines squeeze price premium | +0.6% | North America and Europe, niche segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising vegan and flexitarian demographics

Flexitarian consumers are increasingly contributing to the growth of the vegan confections market, alongside core vegans. This trend reflects heightened awareness of health, environmental, and ethical factors associated with plant-based diets. The primary demographic comprises individuals aged 16-44, with women adopting plant-based diets at nearly twice the rate of men. According to research by The Vegan Society, 3% of Great Britain's population, approximately 2 million people, identify as vegan[3]Source: The Vegan Society, "Nationwide trends highlight growing shift towards plant-based diets," vgansociety.com. Additionally, 10% of the population is actively reducing or eliminating animal products from their diets, presenting a significant opportunity for market expansion. Regions such as London and North-East England, which have the highest rates of vegan identification, are emerging as key areas for new product launches due to concentrated demand. In the context of rising cost-of-living pressures, many consumers are transitioning from traditional animal-based confections to more affordable plant-based alternatives. This shift highlights the potential for price-sensitive segments to drive market growth, particularly when plant-based products are competitively priced and deliver comparable taste and quality to conventional options.

Growing lactose-intolerant/allergy population

In many Asian communities, over 70% of individuals experience lactose intolerance, a condition also prevalent among Hispanic and African American populations in North America. According to the Agency for Healthcare Research and Quality, lactose intolerance rates are particularly high in African American, Hispanic, Asian, and American Indian communities. However, most individuals with lactose intolerance can tolerate up to 12 grams of lactose, especially when consumed with food. For these consumers, vegan confectionery provides a suitable alternative, offering a "free-from" option that meets their dietary requirements while maintaining expected sensory qualities. This segment of the confectionery market is expanding as it appeals to both health-conscious consumers and those with dietary restrictions. Furthermore, manufacturers are addressing key dietary needs by fortifying their products with calcium and vitamin D, targeting nutrient deficiencies. This approach not only meets consumer health demands but also helps secure prominent shelf space in health-focused categories and achieve premium profit margins, thereby enhancing their market position and driving growth in this niche market.

Ethical and environmental sustainability push

Environmental sustainability concerns are increasingly influencing purchasing decisions in the confectionery market. According to Cargill's 2025 Indulgence Study, 25% of consumers in Southeast Asia prioritize sustainability in product development. With the EU Deforestation Regulation set to take effect in December 2024, cocoa-based products face immediate compliance challenges. This has prompted major manufacturers to adopt alternative ingredients, such as plant-based or synthetic cocoa substitutes, to meet regulatory requirements. Companies leading in deforestation-free supply chains are positioned to gain advantages, including improved brand reputation, increased consumer trust, and potential market share growth. Conversely, traditional manufacturers reliant on cocoa face higher risks of non-compliance penalties and potential loss of competitiveness. Additionally, the market shift is highlighted by 77% of Southeast Asian consumers expressing willingness to pay a premium for gourmet dark chocolate, supporting the viability of sustainable strategies and enhancing profit margins for manufacturers aligning with eco-conscious trends.

Retailer private-label vegan lines squeeze price premium

Retailers are increasingly integrating vegan confectionery items into mainstream channels, moving away from limiting them to specialty health food sections. This transition reflects the category's growth and broader consumer acceptance, as vegan products are now considered part of the general confectionery market. For example, Issei Mochi Gummies, a notable brand in the vegan confectionery segment, plans to launch in over 2,000 locations in 2024, including major retailers such as Walmart and World Market. This expansion highlights the brand's successful entry into mainstream retail and the rising demand for plant-based alternatives in conventional markets. Additionally, retail partnerships are focusing on product innovation and flavor differentiation to meet changing consumer preferences. Leading brands are emphasizing unique value propositions, prioritizing taste, quality, and overall experience rather than relying solely on the vegan label. While North America and Europe benefit from established distribution networks and consumer acceptance, the Asia-Pacific region presents distinct challenges. Retailers in this market must address local taste preferences, cultural differences, and regulatory requirements, necessitating tailored strategies for successful market entry and growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium pricing vs conventional confectionery | -1.4% | Global, more pronounced in price-sensitive markets | Short term (≤ 2 years) |

| Cold-chain/shelf-life constraints for fillings | -0.8% | Global, critical in tropical regions | Medium term (2-4 years) |

| Regulatory ambiguity on vegan claims | -0.6% | Europe and North America, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Scarcity of deforestation-free CBEs | -0.5% | Global, concentrated in cocoa-dependent regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premium pricing vs conventional confectionery

The higher pricing of vegan confectionery poses challenges for market access, particularly among price-sensitive consumers in emerging markets, where cost considerations often take precedence over ethical factors. Research shows that 77% of Southeast Asian consumers are willing to pay a premium for gourmet dark chocolate. However, their purchasing behavior remains highly sensitive to price changes, especially during periods of economic uncertainty. Cost-of-living pressures have a dual effect on the adoption of vegan products. While financial constraints lead some consumers to reduce animal product consumption, these same pressures limit their ability to purchase premium vegan alternatives. Approximately one-third of consumers are reducing animal product consumption due to financial challenges, but are actively seeking affordable substitutes. To successfully enter and compete in the market, businesses must adopt pricing strategies that balance premium branding with affordability. This may include introducing tiered product lines or implementing cost-reduction measures that preserve quality and ethical standards. Additionally, companies could explore localized production or sourcing strategies to reduce costs, align with regional consumer preferences, and enhance affordability, thereby broadening their market reach.

Cold-chain/shelf-life constraints for fillings

Vegan confectionery products encounter logistical challenges due to their sensitivity to temperature, particularly for filled items and chocolate substitutes. These products require specialized storage and distribution systems to preserve quality, leading to increased operational costs. Research indicates that temperature fluctuations during chocolate transport can degrade both product quality and economic value. To address these challenges, effective packaging solutions, such as insulated materials or temperature-controlled containers, are essential. For sugar-based confections, moisture control is critical: while reducing moisture content can extend shelf life, it may adversely affect texture in plant-based formulations that lack traditional stabilizers like gelatin. This issue is further exacerbated in tropical climates, where ambient temperatures often exceed optimal storage conditions. In such regions, brands must implement advanced packaging technologies, such as multilayered barriers or vacuum-sealed options, or reformulate products with heat-resistant ingredients to maintain product integrity without relying on cold-chain logistics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Chocolate Dominance, Faces Gummy Innovation

In 2025, chocolate maintained its position as the leading segment in the vegan confectionery market, accounting for a significant 46.13% market share. This dominance is supported by established brands introducing oat- and sunflower-based recipes that replicate the creamy texture of traditional milk chocolate. These innovations appeal to consumers seeking familiar flavors without animal-derived ingredients, solidifying chocolate's pivotal role in the category. Companies like Planet A Foods are exploring alternative fats and grains to address environmental concerns associated with cocoa production while catering to ethically conscious consumers. However, the chocolate segment faces challenges, including fluctuations in cocoa supply and shifting consumer preferences. Companies that adapt by developing grain-based confections or collaborating with precision-fermentation specialists are better positioned to retain their market share and address rising competition.

Gummies and jellies are emerging as the fastest-growing segment in the vegan confectionery market, with a projected CAGR of 10.18% through 2031. Their popularity is driven by their appeal to children, featuring playful shapes, bright colors, and a chewy texture. Advances in pectin technology, particularly in esterification processes, have enabled manufacturers to create complex, multilayered gummies that are visually appealing and stable without relying on animal gelatin. Additionally, the incorporation of functional ingredients such as vitamins and probiotics has expanded their appeal among health-conscious parents and adults. Their long shelf life and simple production process make gummies especially attractive in regions with limited cold-chain logistics. These innovations and trends position the gummies and jellies segment to surpass chocolate and other vegan confectionery formats in growth rate.

By Category: Sugar-Free Alternatives Accelerate

In 2025, sugar-based SKUs accounted for 68.19% of total revenue in the vegan confectionery market, maintaining their leading position. This segment's success is attributed to its familiarity and widespread consumer appeal, offering the classic taste and texture that shoppers expect. Brands have effectively retained their market share by leveraging traditional recipes and incorporating fruit-juice concentrates and oligosaccharide syrups to achieve incremental sugar reductions without compromising the product's mouthfeel. Despite growing public concerns about sugar consumption, these products continue to serve as comfort foods and impulse purchases for both children and adults. Their affordability is a significant advantage, as refined sugar's lower cost compared to alternative sweeteners enables brands to keep retail prices competitive. As a result, sugar-based vegan confections remain a reliable revenue driver, even in the face of increasing health and regulatory challenges.

The sugar-free vegan confectionery segment is experiencing rapid growth, with a projected CAGR of 10.58% through 2031. This expansion is fueled by stricter regulatory limits on added sugars and a growing consumer focus on metabolic health and calorie reduction. The FDA's 2025 approval of brazzein has provided formulators with access to high-intensity, low-calorie sweeteners, enabling sugar-free products to feature clean labels and authentic sweetness while avoiding the drawbacks of earlier alternatives. Brands are increasingly utilizing sweeteners such as allulose and next-generation stevia glycosides to deliver rich flavors while significantly reducing sugar content. However, the higher cost of these innovative sweeteners compared to refined sugar presents challenges in achieving mass-market pricing. Despite this, sugar-free vegan SKUs that balance health benefits with appealing taste are carving out a significant and rapidly expanding niche, particularly among health-conscious and diet-focused consumers.

By Distribution Channel: Digital Upswing Reshapes Reach

In 2025, supermarkets and hypermarkets accounted for 44.76% of the total market revenue in vegan confectionery distribution. These physical outlets play a significant role in product discovery, allowing consumers to encounter new brands and innovations during routine grocery shopping. The in-store environment encourages impulse purchases and provides immediate product availability. Additionally, strategic shelf placements enhance brand visibility and build consumer trust. Supermarkets often implement cross-category promotions, benefiting both mainstream and premium vegan products. Their established logistics networks and consistent consumer traffic make them essential for major product launches. As a result, supermarkets and hypermarkets remain critical for distributing vegan confectionery, supporting both established brands and new entrants seeking rapid market penetration.

Online retail is emerging as the fastest-growing distribution channel for vegan confectionery, with a projected CAGR of 11.07% through 2031. This growth is driven by the convenience of home delivery and the ability of brand websites and online marketplaces to provide detailed product information. Digital platforms offer unique advantages, such as comprehensive ingredient transparency, ethical branding, and user reviews, which help address consumer concerns and encourage informed purchasing decisions. Direct-to-consumer (DTC) brands utilize clickstream analytics to adapt product offerings, introduce new flavors, and create personalized bundles. Subscription services further strengthen brand loyalty by ensuring repeat purchases, increasing customer lifetime value, and maintaining consistent engagement. While convenience stores remain relevant for spontaneous purchases, their growth is outpaced by the extensive and tailored options available through online platforms.

Geography Analysis

In 2025, North America accounted for 38.40% of sales, driven by increased vegan awareness and a well-established omnichannel distribution network. The United States serves as a hub for major corporations, leveraging its plant-based research and development centers. In Canada, government-supported innovation grants are contributing to the market's growth. The introduction of precision fermentation is expected to support steady growth in the region's vegan confectionery market by reducing raw material costs for dairy-free chocolates and sugar-reduced gummies.

Asia-Pacific is projected to grow at a 10.41% CAGR, supported by a lactose intolerance rate exceeding 70% in several populations and government investments in alternative proteins. In 2024, Singapore allocated USD 14.8 million to develop a precision fermentation hub. At the same time, China's comprehensive food-supply strategy is funding university research on plant-based confectionery. Retailers across the region are increasingly allocating mainstream shelf space to vegan products, reflecting growing consumer acceptance.

In Europe, sustainability initiatives are driving market trends, with the EU Deforestation Regulation encouraging a shift toward cocoa-free formulations. Germany and Nordic countries are leading efforts with pilot plants testing innovative fats and starches to improve vegan chocolate viscosity. Southern Europe is also experiencing growth, fueled by rising tourism-related demand for ethical souvenirs. While South America and the Middle East and Africa currently exhibit modest adoption rates, they present significant growth potential as logistics challenges decrease and local ingredient supply chains develop.

Competitive Landscape

The sector's moderate fragmentation indicates significant potential for consolidation. Major global companies are acquiring niche innovators to enhance their research and development capabilities and expand their digital brand portfolios. Mars is in the process of completing a USD 35.9 billion acquisition of Kellanova's North American plant-based assets. This move aims to strengthen Mars' position in the sustainable snacking market by incorporating innovative platforms and broadening its distribution network. Similarly, Cargill, in collaboration with Voyage Foods, is accelerating the development of cocoa alternatives. This initiative addresses deforestation-related supply challenges while diversifying its ingredient portfolio to align with changing consumer preferences.

Regional players are also taking strategic steps. Regal Confections expanded its gummy product range by acquiring Mondoux Confectionery in mid-2024, a move designed to enhance its product offerings and increase its share in the confectionery market. In Japan, Ovgo Inc. achieved B-Corp certification, boosting its brand reputation by setting higher environmental standards and appealing to environmentally conscious consumers.

Venture capital is increasingly supporting platform technologies, as demonstrated by Planet A Foods' USD 15.4 million Series A funding for its ChoViva cocoa-free chocolate. This investment underscores the rising interest among investors in sustainable and innovative food solutions. The current competitive landscape emphasizes the importance of proprietary ingredients, sustainability credentials, and agile omnichannel marketing strategies over mere scale. These shifts reflect evolving consumer preferences and growing regulatory pressures shaping market dynamics.

Vegan Confectionery Industry Leaders

-

Mondelez International

-

Nestlé S.A.

-

Mars Incorporated

-

Barry Callebaut

-

The Hershey Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Candy Kittens has introduced its new vegan chocolate range in the UK. The brand emphasizes that all vegan snacks offered on its platform will maintain the same quality, taste, and ethical standards as its existing products. The new range includes Crunchy Corn, Salted Peanuts, and Crispy Rice, each coated with the plant-based ChoViva coating.

- March 2025: Trupo has introduced its newest product, vegan candy bars made with a dairy-free caramel nougat. These candy bars address the increasing demand for plant-based alternatives, offering a flavorful option for consumers looking for vegan-friendly treats.

- July 2024: Regal Confections expanded its Canadian gummy and seasonal chocolate portfolios through the acquisition of Mondoux Confectionery. This strategic acquisition is anticipated to strengthen Regal Confections' market presence and broaden its product range in the confectionery market.

Global Vegan Confectionery Market Report Scope

| Chocolate |

| Gummies and Jellies |

| Hard Candy and Lollipops |

| Others |

| Sugar based |

| Sugar Free |

| Supermarkets and Hypermarkets |

| Convenience stores |

| Online Retail Stores |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Chocolate | |

| Gummies and Jellies | ||

| Hard Candy and Lollipops | ||

| Others | ||

| By Category | Sugar based | |

| Sugar Free | ||

| By Distribution Channel | Supermarkets and Hypermarkets | |

| Convenience stores | ||

| Online Retail Stores | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the vegan confectionery market in 2026?

The vegan confectionery market size reached USD 1.80 billion in 2026 and is on track to hit USD 2.91 billion by 2031.

Which region leads the vegan confectionery market today?

North America holds the top position with a 38.40% revenue share in 2025, supported by mature retail networks and strong vegan consumer bases.

What product segment is growing the fastest?

Gummies and jellies are forecast to post the fastest 10.18% CAGR during 2026-2031 due to advances in pectin texturization and functional add-ins.

Why is sugar-free vegan confectionery gaining ground?

Regulatory pressure to limit added sugars and greater consumer focus on metabolic health are propelling sugar-free lines, which are expected to grow at an 10.58% CAGR.

Page last updated on: