Vegan Dessert Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

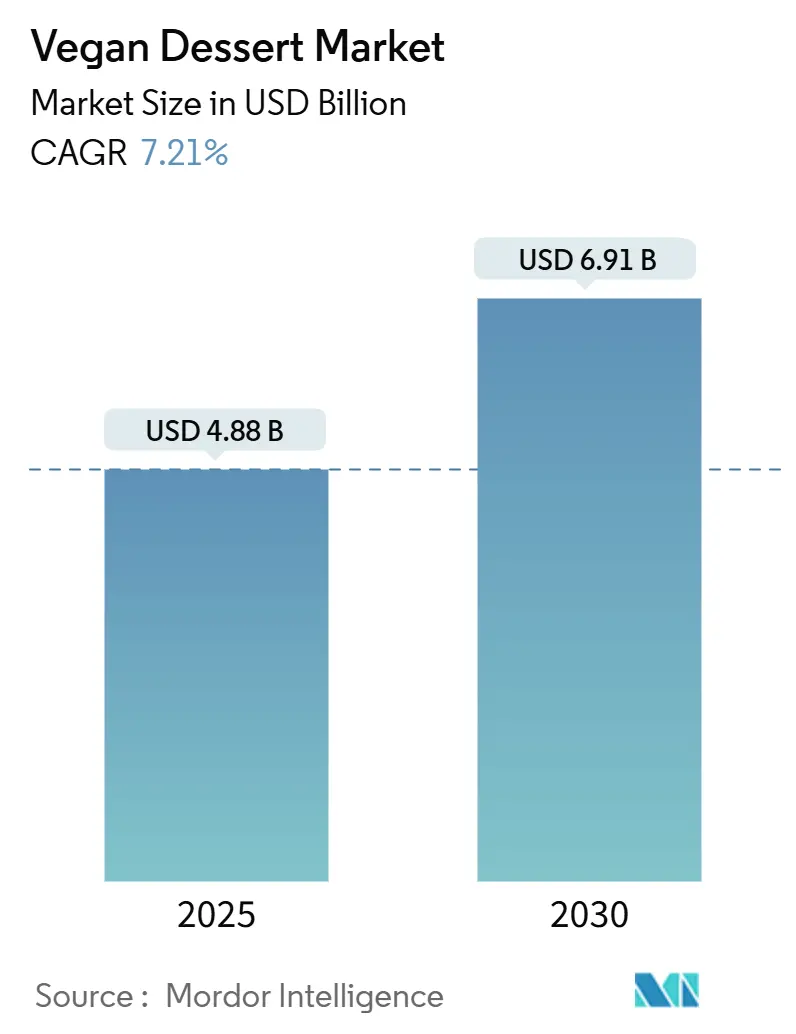

| Market Size (2025) | USD 4.88 Billion |

| Market Size (2030) | USD 6.91 Billion |

| Growth Rate (2025 - 2030) | 7.21% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

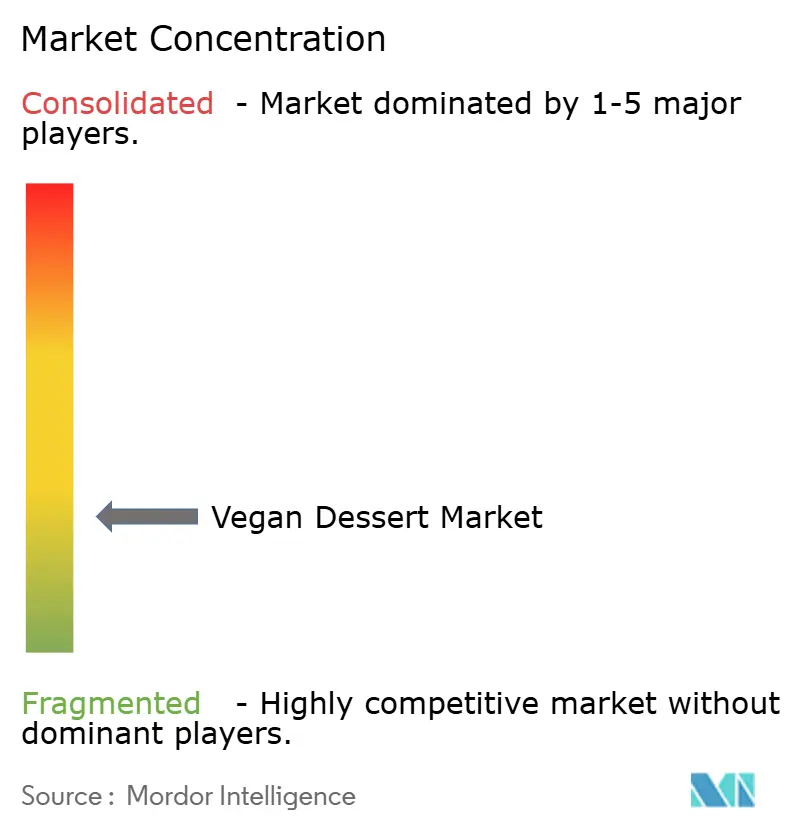

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Vegan Dessert Market Analysis by Mordor Intelligence

The global vegan desserts market reached USD 4.88 billion in 2025 and is expected to grow at a compound annual growth rate (CAGR) of 7.21% through 2030, reaching USD 6.91 billion. This growth reflects increasing consumer adoption of plant-based diets driven by health, ethical, and environmental factors. The market encompasses various products which serve as alternatives to traditional dairy- and egg-based desserts. Market expansion is supported by the increasing prevalence of lactose intolerance and dairy allergies, alongside growing demand for clean-label and natural ingredients. Improvements in plant-based ingredients have enhanced the taste and texture of vegan desserts, increasing their appeal to mainstream consumers. Environmental consciousness and concerns about animal welfare continue to influence consumers' shift toward vegan options. Technological advancements in food processing and a wider range of ingredients enable manufacturers to develop diverse product lines that meet demands for taste, nutrition, and allergen-free options. The market's growth potential is further strengthened by expansion in emerging markets and the increasing global vegan population.

Key Report Takeaways

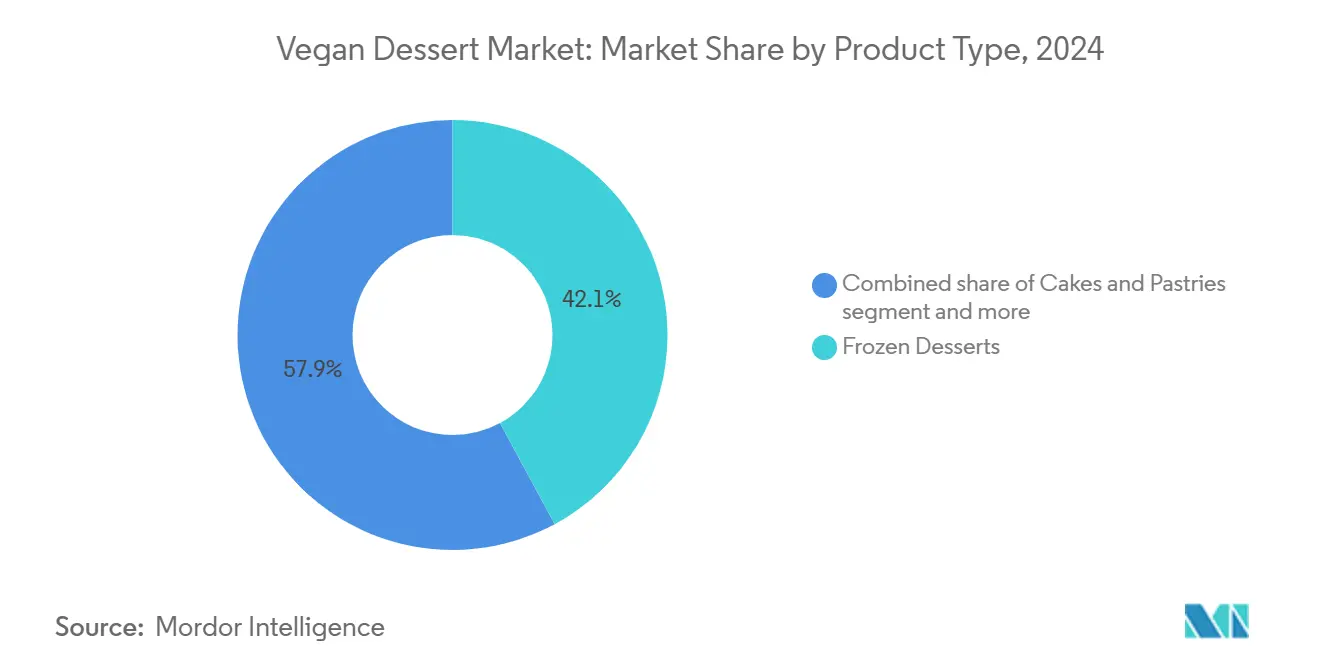

- By product type, frozen desserts led with 42.12% of % vegan desserts market share in 2024, and cakes and pastries are projected to register the fastest 7.67% CAGR through 2030.

- By ingredient base, almond captured 34.23% of the vegan desserts market size in 2024, while oat formulations are expected to post an 8.56% CAGR to 2030.

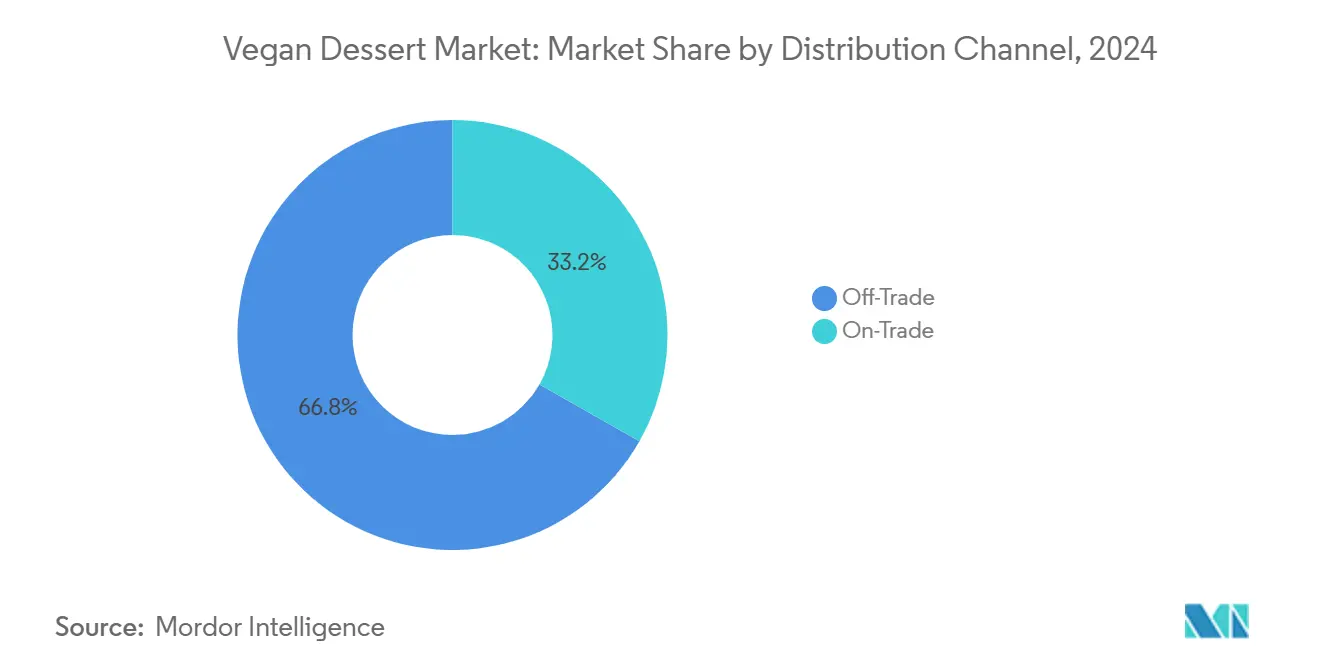

- By distribution channel, the off-trade segment represented 66.78% of value in 2024; on-trade is forecast to expand at a 7.43% CAGR to 2030.

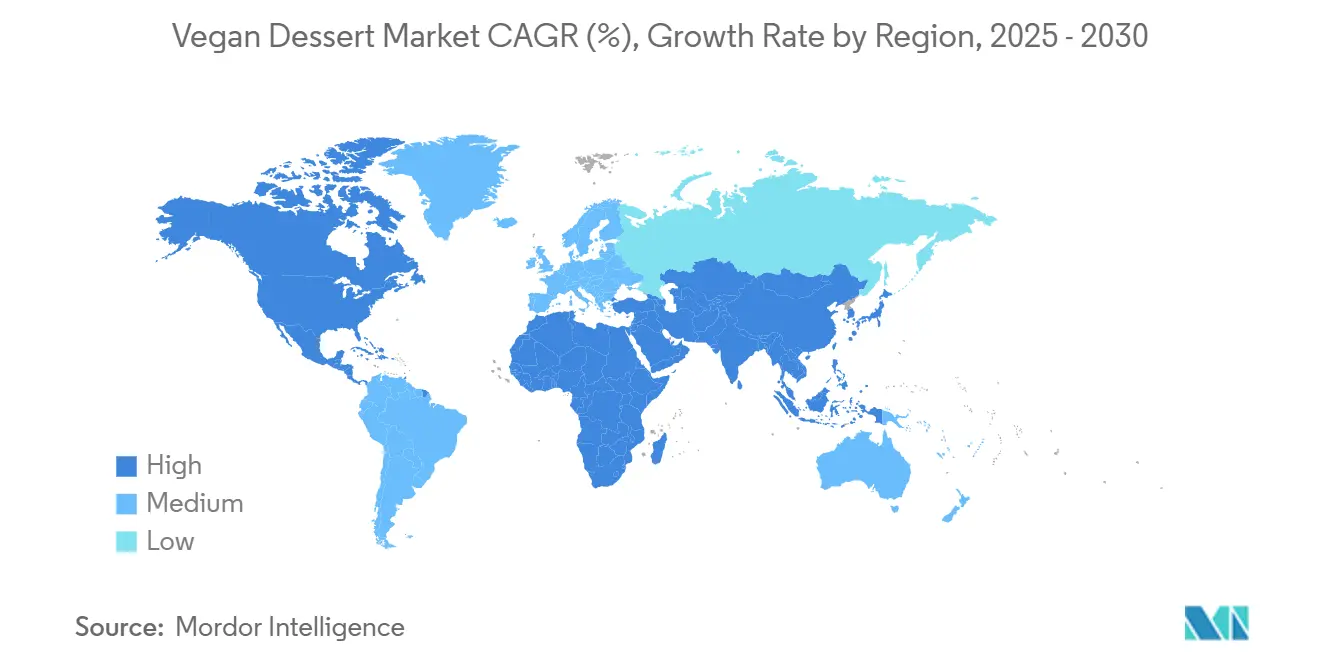

- By geography, North America accounted for 36.65% revenue in 2024, whereas Asia-Pacific is predicted to accelerate at an 8.49% CAGR through 2030.

Global Vegan Dessert Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increase in lactose intolerance and dairy allergies | +1.8% | Global, with the highest impact in Asia-Pacific, the Middle East, and Africa | Medium term (2-4 years) |

| Sustainability and environmental concerns | +1.5% | North America and Europe are the core, expanding to the Asia-Pacific | Long term (≥ 4 years) |

| Clean label and natural ingredients demand | +1.2% | Global, led by developed markets | Short term (≤ 2 years) |

| Innovation in plant-based ingredients | +2.1% | Global, with Research and Development concentration in North America | Medium term (2-4 years) |

| Cultural shift toward flexitarian diets | +0.8% | North America and Europe, emerging in urban Asia-Pacific | Long term (≥ 4 years) |

| Rising popularity of functional desserts | +0.7% | North America and Europe, selective Asia-Pacific markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increase in Lactose Intolerance and Dairy Allergies

The increasing prevalence of lactose intolerance and dairy allergies is a significant driving factor for the global vegan desserts market. Lactose intolerance, characterized by insufficient lactase enzyme production, affects a significant portion of the global adult population, with varying rates across different ethnic groups and geographical regions. According to the Food Standards Agency, approximately 12% of people in England, Wales, and Northern Ireland reported having some form of food intolerance in 2024, with lactose intolerance representing a substantial component [1]Source: Food Standards Agency, "Prevalence of different types of food hypersensitivity", www.food.gov.uk. Consumers who experience severe gastrointestinal discomfort, including persistent bloating, abdominal cramps, and diarrhea from traditional dairy-based desserts, are increasingly gravitating towards vegan desserts as a reliable and satisfying alternative. The market expansion is further accelerated by the high prevalence of milk protein allergies among infants and young children. The heightened awareness of these health conditions, combined with improved understanding of dietary restrictions, has significantly increased consumer demand for innovative plant-based desserts that exclude lactose and dairy proteins while delivering exceptional taste, desirable texture, and comprehensive nutritional benefits.

Sustainability and Environmental Concerns

The global vegan desserts market is experiencing growth driven by increasing environmental and sustainability concerns. Vegan desserts have a reduced environmental impact compared to traditional dairy and animal-based alternatives, requiring fewer natural resources, including water, land, and energy for production. While animal-derived food production contributes to greenhouse gas emissions, deforestation, and water pollution, plant-based dessert manufacturing helps reduce these environmental effects. The younger generation of consumers, particularly those focused on environmental issues, seeks products that support reduced carbon emissions and biodiversity conservation. This consumer behavior is increasing the demand for vegan desserts as an environmentally responsible choice. The industry demonstrates its environmental commitment through sustainable ingredient sourcing, the use of local produce, and eco-friendly packaging. These environmental practices appeal to consumers wanting to combine dessert consumption with environmentally responsible choices, driving the vegan desserts market growth.

Clean Label and Natural Ingredients Demand

Clean label and natural ingredients drive the growth of the vegan desserts market, reflecting consumer preferences for transparency, health, and wellness in food choices. Consumers prefer products with simple, recognizable ingredients that are free from synthetic additives, artificial flavors, preservatives, and allergens. This preference stems from increased awareness of food's health impacts and the demand for minimally processed options that align with ethical and sustainable lifestyles. According to the International Food Information Council (IFIC), in 2024, 36% of American consumers preferred foods labeled as natural, organic, or healthy, indicating strong market demand for clean-label products [2]Source: International Food Information Council (IFIC), "2024 IFIC Food and Health Survey", https://ific.org. Vegan dessert manufacturers respond to this trend by incorporating plant-based, organic, and responsibly sourced ingredients such as almond, oat, coconut, and fruit-based sweeteners. These clean-label formulations ensure product safety and nutritional benefits while meeting regulatory standards and consumer demand for ethical sourcing. The integration of natural ingredients reinforces product authenticity and promotes trust among health-conscious consumers.

Innovation in Plant-Based Ingredients

Innovation in plant-based ingredients is transforming the vegan desserts market by improving flavor, texture, and nutritional profiles, which drives product development and consumer acceptance. Kaiser's launch of oat-based frozen desserts in Quebec in October 2024 demonstrates this advancement, as these products use oat beverages instead of powdered oats to enhance creaminess and mouthfeel. These developments help manufacturers overcome previous texture limitations and create vegan desserts comparable to traditional dairy products. The increased availability of plant-based ingredients such as almond flour, coconut oil, cashew cream, and flax eggs enables food producers to develop various desserts, including mousses, cakes, and cookies, without dairy, eggs, or artificial additives. The market has also integrated nutrient-rich ingredients like chia seeds, matcha, and probiotics to meet consumer demand for healthier dessert options. Food processing improvements, including enzymatic treatments, fermentation, and natural emulsifiers, have enhanced the quality, shelf life, and nutritional content of vegan desserts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of plant-based ingredients | -1.4% | Global, most acute in price-sensitive emerging markets | Short term (≤ 2 years) |

| Taste and texture challenges | -0.9% | Global, with regional flavor preference variations | Medium term (2-4 years) |

| Storage and cold chain dependence | -0.6% | Emerging markets with infrastructure limitations | Medium term (2-4 years) |

| Fragmented vegan certification and labeling rules | -0.4% | Global, with regulatory complexity in multi-market operations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Plant-Based Ingredients

The elevated cost of plant-based ingredients presents a formidable barrier to the global vegan desserts market expansion. Premium ingredients such as almond flour, coconut oil, oat milk, and specialized vegan substitutes like aquafaba or coconut cream command substantially higher prices compared to conventional dairy and egg ingredients. These increased costs originate from multiple critical factors, including limited economies of scale, sophisticated specialized production processes, and intricate supply chain challenges in sourcing premium, organic, and sustainable raw materials. The stringent requirement for dedicated manufacturing facilities and specialized equipment to prevent cross-contamination with animal products further intensifies production costs. Consequently, elevated retail prices substantially restrict market penetration, particularly affecting price-sensitive consumer segments and emerging markets, while small-scale producers face significant challenges competing against established companies due to their limited capacity to achieve cost efficiencies.

Taste and Texture Challenges

The global vegan desserts market faces substantial challenges in taste and texture replication, creating barriers to widespread adoption. While plant-based ingredient technology has advanced, manufacturers encounter persistent difficulties in achieving the distinctive creamy textures and complex flavor profiles inherent in traditional dairy desserts. Common quality issues include pronounced graininess, noticeable dryness, and variable mouthfeel in plant-based alternatives, particularly affecting key product categories like puddings, custards, and baked goods, where texture defines the consumer experience. Market acceptance remains constrained, especially in regions where cultural preferences strongly favor dairy-based desserts. The incorporation of specialized ingredients, including advanced emulsifiers, stabilizers, and sophisticated natural flavor enhancers, significantly increases production complexity and associated costs. These technical limitations substantially impact market expansion and premium brand development as manufacturers navigate the complex balance between maintaining product integrity and meeting heightened consumer expectations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Frozen Innovation Leads Category Expansion

Frozen desserts held the largest share in the global vegan desserts market at 42.12% in 2024. This dominance stems from increased consumer demand for dairy-free alternatives, particularly among individuals with lactose intolerance and those seeking healthier options. The development of plant-based milk alternatives using oat, coconut, almond, and soy has enabled manufacturers to create frozen desserts that replicate the texture and taste of conventional ice creams and sorbets. The transition to vegan frozen desserts is also influenced by consumers' focus on cholesterol management, as these products use plant-based fats instead of animal-derived ingredients.

The cakes and pastries segment is projected to grow at a CAGR of 7.67% through 2030, making it the fastest-growing category in the global vegan desserts market. This growth reflects consumers' increasing preference for indulgent yet health-conscious baked goods that align with vegan and plant-based diets. The rising demand for dairy-free and egg-free cakes corresponds with consumers' desire to balance indulgence with ethical considerations and health objectives. Advancements in plant-based ingredients, including aquafaba, flaxseed, and nut-based creams, have helped manufacturers address traditional vegan baking challenges, successfully replicating conventional cake characteristics. The segment's expansion is further supported by the wider availability of vegan cakes in restaurants, cafes, and at special events.

By Ingredient Base: Oat Ascendancy Challenges Almond Dominance

Almond maintains the largest market share of 34.23% in the global vegan desserts market in 2024, supported by established supply chains, consumer familiarity, and nutritional benefits. Almonds offer versatility and dietary advantages, containing vitamins, antioxidants, and healthy fats. Their capacity to create creamy plant-based milk alternatives makes them essential for vegan desserts, including ice creams, cakes, and custards. The robust supply chain, particularly from major producers like the United States, ensures steady availability for product innovation and market growth. According to the United States Department of Agriculture (USDA), the United States leads global almond production with approximately 1.27 million metric tons in the 2024/2025 season [3]Source: United States Department of Agriculture (USDA), "2024/2025 Almonds Production", www.usda.gov. This production capacity ensures a stable almond supply, allowing manufacturers to meet consumer demand and maintain almond's market leadership in vegan desserts.

Oat-based formulations are transforming the plant-based dessert segment with a CAGR of 8.56% through 2030. This growth stems from oat ingredients' ability to improve texture, creaminess, and mouthfeel in vegan desserts, addressing common challenges in plant-based alternatives. Oat milk effectively replicates dairy milk's viscosity and richness compared to other plant-based options, making it suitable for frozen desserts, cakes, and custards. This results in better sensory experiences, driving consumer acceptance and repeat purchases. Oats also appeal to eco-conscious consumers as a clean-label, sustainable ingredient. The health benefits of oats, including high fiber content and beta-glucan for cholesterol management, increase demand for oat-based vegan desserts.

By Distribution Channel: Foodservice Momentum Accelerates Mainstream Adoption

Off-trade retail holds a 66.78% share in 2024, driven by established frozen food sections and consumer preference for at-home consumption of plant-based alternatives. The retail channel's dominance reflects successful brand development by specialized plant-based companies and the expansion of dairy alternatives portfolios by major food manufacturers. Online retail within the off-trade segment shows significant growth as direct-to-consumer brands use e-commerce to reach specific consumer segments and introduce new products without traditional retail barriers. The digital channel allows brands to effectively communicate ingredient benefits and sustainability messages compared to traditional retail displays. Physical stores remain important discovery points where consumers initially encounter plant-based dessert alternatives before products expand to wider retail distribution.

The on-trade distribution channel in the global vegan desserts market projects a CAGR of 7.43% through 2030. This growth comes from increased demand in restaurants, cafes, hotels, and catering services, which are adding vegan dessert options to serve vegan and health-conscious consumers. On-trade establishments use this trend to attract diverse customers, including flexitarians and younger consumers seeking plant-based options while dining out. The channel benefits from allowing consumers to experience new vegan desserts, building awareness and loyalty. The hospitality sector's focus on ethical sourcing and sustainability aligns with vegan dessert consumer values, supporting continued growth.

Geography Analysis

North America holds 36.65% market share in 2024, supported by widespread plant-based food acceptance, developed cold chain infrastructure, and favorable regulatory frameworks for dairy alternative labeling and marketing. The region's research and development capabilities enable food manufacturers to establish plant-based innovation centers and collaborate with ingredient suppliers. Higher consumer acceptance of premium pricing for sustainable and health-focused products supports market growth despite elevated ingredient costs. Established distribution networks facilitate efficient product launches across various retail channels. The market demonstrates advanced consumer segmentation, with millennials and Gen Z driving adoption, while older consumers choose plant-based alternatives for health reasons.

Asia-Pacific demonstrates the highest growth rate at 8.49% CAGR through 2030, driven by high lactose intolerance rates, increasing urbanization, and rising disposable income in China and India. The region combines traditional acceptance of plant-based ingredients with increasing health and environmental awareness in urban areas. Access to local ingredients such as coconut, rice, and plant proteins enables affordable formulations that match regional taste preferences. Regulatory requirements vary across countries, with some offering streamlined plant-based product approval processes while others maintain strict import and labeling requirements that encourage local production.

Europe maintains a substantial market presence through environmental regulations, established organic food consumption, and demand for sustainable options. The region's regulatory structure benefits plant-based products with transparent supply chains compared to dairy alternatives. South America, the Middle East, and Africa offer growth potential through local ingredient availability and expanding middle-class populations, despite infrastructure constraints and price sensitivity. These regions can utilize native plant ingredients for affordable, culturally appropriate product development while strengthening local supply chains.

Competitive Landscape

The vegan desserts market shows moderate fragmentation, where established food conglomerates leverage their distribution networks while specialized plant-based brands focus on innovation and premium offerings. Market consolidation continues through acquisitions and partnerships. Key market players include Unilever PLC, Nestlé S.A., Danone S.A., Oatly Group AB, and Tofutti Brands Inc. The market structure operates on two levels: large manufacturers provide mainstream market access and operational efficiency, while smaller specialized brands drive product innovation and category expansion.

Technology adoption differentiates market players, with companies investing in advanced processing techniques, ingredient sourcing, and supply chain optimization. These investments aim to achieve cost parity with dairy alternatives while maintaining product quality. Patent activities in plant protein modification, stabilizer systems, and processing methods demonstrate significant research and development efforts to address texture and taste challenges that affect mainstream adoption.

The regulatory environment favors companies with strong quality assurance capabilities and multi-market compliance expertise, particularly as vegan certification standards and labeling requirements become more stringent across key markets. Market opportunities exist in functional desserts, premium artisanal segments, and emerging market localization, where established players have limited presence and local ingredient knowledge offers competitive advantages.

Vegan Dessert Industry Leaders

-

Unilever PLC

-

Nestlé S.A.

-

Danone S.A.

-

Oatly Group AB

-

Tofutti Brands Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Kinish has launched The Rice Creamery, a dairy-free ice cream brand. The product contains a base of rice syrup and cashew paste, combined with sugar, glucose, dietary fiber, salt, an emulsifier, and a stabilizer.

- June 2025: OGGS launched Mega Birthday Cupcakes, which feature sponge cake with raspberry jam filling, icing, and sprinkles. The company also introduced Zesty Lemon Cakes, comprising mini sponges filled with lemon-flavored filling, topped with icing and drizzle.

- April 2025: Oppo Brothers launched a new range of low-calorie, vegan ice cream sticks called Oppo Refreshed. The sticks contain 49 calories each, are Nutriscore A-rated, and come in three flavors.

- March 2025: Magnum relaunched its vegan ice cream range with an innovative soy protein recipe, marking a significant shift from its previous pea protein formulation. This reformulation demonstrates the brand's commitment to enhancing its plant-based offerings.

Global Vegan Dessert Market Report Scope

| Frozen Desserts |

| Cakes and Pastries |

| Puddings and Custards |

| Other Vegan Desserts |

| Soy |

| Almond |

| Coconut |

| Oat |

| Others |

| On-Trade | |

| Off-Trade | Offline Stores |

| Online Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Frozen Desserts | |

| Cakes and Pastries | ||

| Puddings and Custards | ||

| Other Vegan Desserts | ||

| By Ingredient Base | Soy | |

| Almond | ||

| Coconut | ||

| Oat | ||

| Others | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Offline Stores | |

| Online Retail Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the vegan desserts market in 2025?

It is valued at USD 4.88 billion and projected to grow to USD 6.91 billion by 2030.

Which vegan dessert segment holds the biggest share?

Frozen desserts lead with 42.12% of 2024 revenue.

What is the fastest-growing ingredient base?

Oat is expanding at an 8.56% CAGR thanks to its creamy texture advantages.

Why is Asia-Pacific the growth hotspot?

High lactose intolerance rates and rising urban incomes are propelling an 8.49% CAGR.

Page last updated on: