Coronary Stent Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 8.66 Billion |

| Market Size (2031) | USD 10.75 Billion |

| Growth Rate (2026 - 2031) | 4.42% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Coronary Stent Market Analysis by Mordor Intelligence

Coronary stents market size in 2026 is estimated at USD 8.66 billion, growing from 2025 value of USD 8.29 billion with 2031 projections showing USD 10.75 billion, growing at 4.42% CAGR over 2026-2031. Healthy expansion is supported by steady procedure volumes, a shift toward value-based care, and rapid integration of AI-guided imaging that improves precision and reduces complications. Hospitals continue favoring drug-eluting platforms with ultrathin struts that shorten dual antiplatelet therapy, while public procurement reforms in Asia alter global pricing dynamics. Supply-chain constraints for cobalt-chromium alloys place a ceiling on high-end production, yet material innovation is narrowing that gap. Consolidation among diversified med-tech firms signals a maturing field where adjacent technologies such as intravascular lithotripsy augment core stent portfolios.

Key Report Takeaways

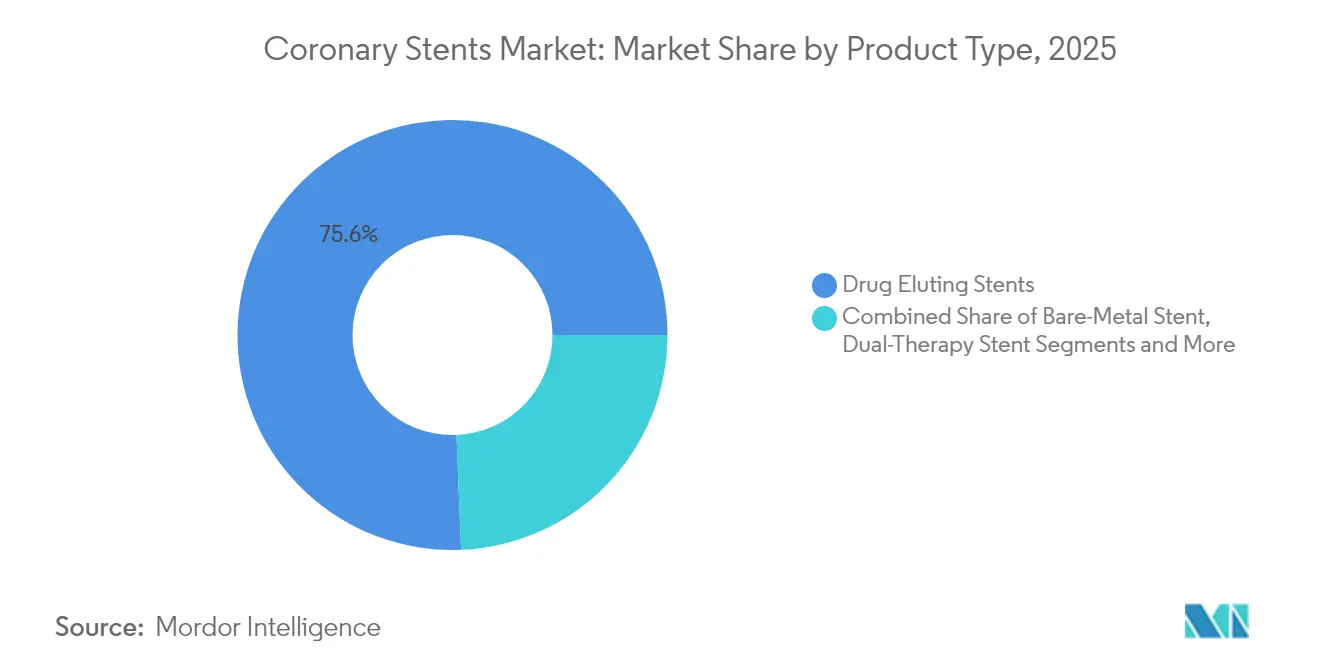

- By product type, drug-eluting stents held 75.64% of the coronary stents market share in 2025, while bioabsorbable vascular scaffolds are forecast to expand at a 7.52% CAGR to 2031.

- By biomaterial, metallic platforms accounted for 67.10% of the coronary stents market size in 2025; polymeric scaffolds are projected to grow at an 7.91% CAGR through 2031.

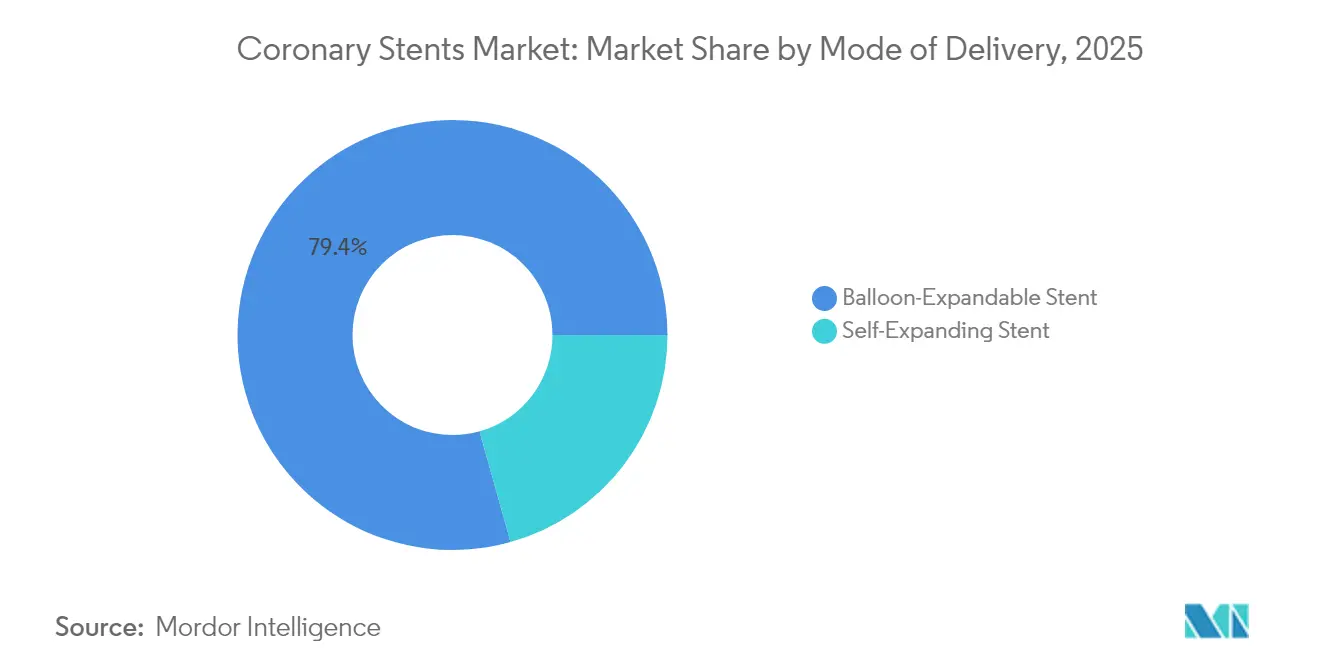

- By mode of delivery, balloon-expandable systems commanded 79.35% revenue share in 2025; self-expanding systems exhibit the fastest CAGR of 6.44% to 2031.

- By end user, hospitals represented 58.35% of procedures in 2025, whereas ambulatory surgical centers are expected to post a 6.71% CAGR over the same horizon.

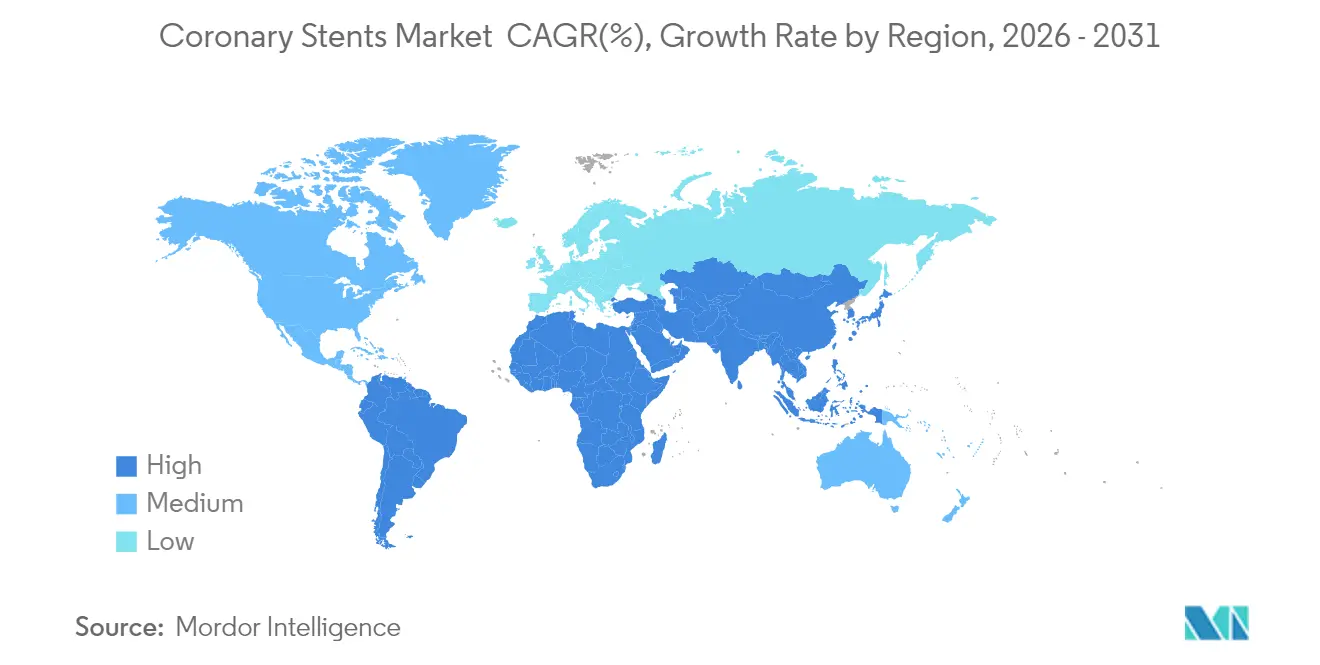

- By geography, North America led with 34.90% revenue share in 2025; Asia-Pacific is advancing at a 7.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Coronary Stent Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence CAD and Aging Population | +1.2% | Global, with concentrated impact in North America & Europe | Long term (≥ 4 years) |

| Shift Toward Early PCI In Acute Coronary Syndrome Guidelines | +0.8% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Rapid Uptake Of Ultrathin-Strut & Biodegradable-Polymer DES | +0.9% | North America & EU core, expanding to APAC | Medium term (2-4 years) |

| Integration Of AI-Guided Imaging & Sizing Tools | +0.7% | North America & EU, with selective adoption in APAC urban centers | Short term (≤ 2 years) |

| Hospital Preference For Day-Care Radial PCI Programs | +0.5% | Global, with accelerated adoption in cost-conscious healthcare systems | Short term (≤ 2 years) |

| Government Tenders Favoring Domestic DES and Innovation Incentives | +0.4% | APAC core, with spillover to MEA and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of CAD and Aging Population

Cardiovascular disease incidence continues climbing as populations age and metabolic syndrome becomes widespread, pushing steady demand for interventions in the coronary stents market. Diabetes now appears in roughly one quarter of PCI cases, and dedicated stent designs for hyperglycemic patients demonstrate lower restenosis. Higher life expectancy means more multivessel disease presentations that once were managed conservatively. Payers see upfront stenting as a cost-saving alternative to repeat hospitalization, prompting policy support. Emerging economies feel the shift faster because urban lifestyles compress disease onset timelines. All these factors combine to maintain a robust pipeline of eligible patients through 2030.

Shift Toward Early PCI in Acute Coronary Syndrome Guidelines

Guideline committees increasingly support immediate revascularization, reflected in PREVENT showing target-vessel failure of 0.4% when preventive PCI accompanies medical therapy.[1]American College of Cardiology, “Preventive PCI Combined With Optimal Medical Therapy,” acc.org This stance coexists with nuanced evidence from ISCHEMIA, so clinicians rely on risk stratification algorithms to balance mortality and quality of life. Urgent cases are typically complex, favoring premium devices with improved deliverability. Stable disease volumes may plateau, but acute interventions grow, creating a predictable product mix. Manufacturers fine-tune supply chains for rapid response to emergent demand.

Rapid Uptake of Ultrathin-Strut & Biodegradable-Polymer DES

Meta-analysis of more than 103,000 patients confirms ultrathin-strut platforms cut target-lesion failure over three years.[2]European Journal of Medical Research, “Comparative Effectiveness of Ultrathin vs Standard Strut DES,” biomedcentral.comDevices like Orsiro Mission with 60-micrometer struts offer better navigability in tortuous anatomies while biodegradable polymers ease late-stage inflammation. Engineering complexity raises manufacturing costs, yet hospitals accept premiums when clinical benefits are clear. Early adopters gain reputation advantages in treating calcified lesions. The trend reinforces the segmentation of the coronary stents market into technology tiers.

Integration of AI-Guided Imaging & Sizing Tools

Artificial intelligence applied to angiography yields real-time, reproducible measurements that correlate with intravascular ultrasound, leading to fewer unnecessary implants. Systems such as AngioFFR help operators choose optimal diameters, cutting complication rates by double digits. Hospitals value reduced contrast use and shorter procedure times. Vendors with strong software ecosystems enhance device stickiness, as stents pair with proprietary analytics modules. This convergence blurs lines between hardware and digital therapy.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price Caps & Centralized Procurement Squeezing ASPs | -0.8% | APAC core, with policy spillover to MEA and Latin America | Medium term (2-4 years) |

| Safety Signals Around Late Scaffold Thrombosis In BVS | -0.3% | Global, with heightened regulatory scrutiny in developed markets | Short term (≤ 2 years) |

| Supply-Chain Shortages Of High-Purity Co-Cr Alloy | -0.4% | Global, with acute impact on premium stent manufacturing | Short term (≤ 2 years) |

| Clinical Pushback On Routine Stenting Post-ISCHEMIA Trial | -0.5% | North America & EU, with gradual adoption in evidence-based healthcare systems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Caps and Centralized Procurement Squeezing ASPs

Regulated pricing stripped 85-90% from drug-eluting stent tags in India and China, forcing distributors out of the chain and compressing margins. Volume increases only partially offset revenue declines, prompting factories to automate and relocate. Premium technologies see disproportionate pressure, challenging ROI calculations on next-generation platforms. Worldwide buyers now cite Asian benchmarks to negotiate, creating sustained deflation in the coronary stents market.

Safety Signals Around Late Scaffold Thrombosis in BVS

Registries still report 1.3–3.3% scaffold thrombosis, higher than many metallic DES comparators. AIDA highlighted 30 cases of device thrombosis for BVS versus 5 for conventional stents across three years, so regulators demand longer follow-ups. Added scrutiny stretches development timelines and costs. Operators restrict indications to experienced centers, slowing mass adoption until second-generation designs prove durable safety.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: DES Dominance Faces BVS Innovation

Drug-eluting stents generated 75.64% of revenue in 2025, establishing the largest share of the coronary stents market. The segment benefits from a continuous flow of data supporting low restenosis and thrombosis rates with ever thinner struts. Competition now focuses on polymer chemistry, drug kinetics, and radial strength, areas that expand margins even under price pressure. Bioabsorbable vascular scaffolds, while only a fraction of sales today, record a 7.52% CAGR through 2031 as safety profiles improve. Recent trials like INFINITY-SWEDEHEART that showed 0.6% target-vessel failure for DynamX bioadaptor validate renewed clinical confidence.

Next-generation BVS seek to merge temporary scaffolding with the radial performance of metals. Regulatory acceptance widens indications beyond coronary arteries into peripheral territories, such as Abbott’s Esprit BTK receiving FDA nod for below-the-knee lesions. This broadens platform potential, spurring incremental R&D. Meanwhile, bare-metal stents retain utility in scenarios needing short antiplatelet regimens, and dual-therapy stents address high bleeding-risk patients. The varied lineup allows physicians to tailor therapy rather than apply a one-size-fits-all approach.

By Biomaterial: Metallic Platforms Drive Polymer Innovation

Metallic designs controlled 67.10% of sales in 2025, reflecting physician preference for cobalt-chromium and platinum-chromium alloys that deliver strong radial support. Advances in metallurgy enable 60-micrometer struts without compromising fatigue resistance, meeting demand for high deliverability. Polymeric scaffolds, though smaller today, are gaining at an 7.91% CAGR as biocompatible materials alleviate chronic inflammation. Boston Scientific’s SYNERGY bioabsorbable-polymer DES demonstrated low thrombosis in a pooled cohort of 18,000 patients, bolstering payer confidence.

Research into recombinant collagen type III coatings shows promise in eliminating drug dependence while fostering endothelial healing. These innovations align with sustainability mandates and patient preference for reduced permanent implants. Manufacturers also explore hybrid constructs, pairing metallic frameworks with resorbable outer layers, to capture the best of both worlds. The biomaterial shift keeps the coronary stents market competitive for suppliers that can blend mechanical robustness with biological harmony.

By Mode of Delivery: Balloon-Expandable Systems Lead Innovation

Balloon-expandable models captured 79.35% of the coronary stents market in 2025 thanks to versatility across vessel sizes and physician familiarity. Medtronic’s Resolute Onyx showcases a single-wire design that improves radiopacity and supports one-month dual antiplatelet therapy for high bleeding-risk cohorts. These refinements sustain relevance despite maturity. Self-expanding devices, advancing at 6.44% CAGR, win favor in large proximal vessels and bifurcations where vessel diameter variability challenges fixed-size balloons. Their nitinol frameworks endow conformability that protects against malapposition.

Technological convergence is evident as manufacturers combine balloon-assisted self-expansion for precise initial placement and adaptive sizing. AI-guided deployment tools improve accuracy for both modes. Procedural planning software simulates expansion profiles, guiding device selection. Such integrations push the delivery-mode conversation beyond hardware specs into ecosystem capabilities.

By End User: Hospitals Adapt to Outpatient Trends

Hospitals carried 58.35% of 2025 procedure volumes but are transitioning toward complex interventions that demand hybrid operating theaters, intracoronary imaging, and surgical backup. Routine stable cases increasingly migrate to ambulatory surgical centers, which are forecast to grow at 6.71% CAGR. These centers benefit from radial access and rapid discharge protocols, aligning with payer cost containment. Cardiac catheterization laboratories operate as high-throughput hubs within integrated networks, balancing inpatient acuity with outpatient efficiency.

Same-day discharge feasibility at 78% for elective PCI underscores shifting patient pathways. Facility design now incorporates patient education zones and remote monitoring integration to support early release. End-user diversification influences procurement preferences: hospitals value multifunctional systems, while ambulatory centers focus on low inventory costs and quick case turnover. Vendors segment offerings accordingly, reinforcing downstream differentiation within the coronary stents market.

Geography Analysis

North America retained 34.90% of global revenue in 2025, underpinned by early adoption of AI-guided imaging and favorable reimbursement for high-performance DES. Hospitals leverage comprehensive insurance coverage to select premium platforms, and regulatory pathways remain predictable. Supply-chain instability tied to cobalt-chromium is partly offset by domestic alloys and streamlined FDA emergency pathways that prioritize critical cardiovascular devices. Clinical trial density further entrenches regional leadership.

Asia-Pacific is the fastest riser with a 7.32% CAGR through 2031, fueled by public procurement that widens access while compressing prices. China’s monopsony purchasing model, combined with industrial policy, accelerates domestic champion emergence. India mirrors this trajectory through price ceilings that catapult local firms past 60% share. Urbanization and rising incomes expand PCI eligibility, while public insurance schemes close affordability gaps. These factors create a volume-driven growth pattern distinct from the value-centric North American model.

Europe shows measured expansion as Medical Device Regulation harmonizes quality standards and environmental considerations shape tender scores. Brexit disruptions are settling as mutual recognition agreements stabilize cross-border supply. Sustainability criteria encourage polymers with lower life-cycle impact, nudging R&D toward degradable constructs. Meanwhile, shared-decision frameworks influenced by ISCHEMIA temper elective PCI volumes but elevate demand for best-in-class devices when intervention proceeds.

Competitive Landscape

Top Companies in Coronary Stent Market

The coronary stents market is moderately consolidated. Their extensive patent estates and long-term outcome data create high switching barriers. Nonetheless, national tenders in Asia reward local sourcing, enabling companies such as Sahajanand Medical Technologies in India and Lepu Medical in China to erode incumbents’ price segments. These challengers scale rapidly, aided by state incentives and centralized procurement.

Strategic M&A activity between 2024 and 2025 illustrates convergence around complementary technologies. Johnson & Johnson’s USD 12.5 billion takeover of Shockwave Medical integrates intravascular lithotripsy that fractures calcified plaques before stent placement, enhancing outcomes in complex lesions. Teleflex’s USD 791 million purchase of Biotronik’s vascular intervention unit brings drug-coated balloons and resorbable magnesium scaffolds under one roof, creating end-to-end coronary portfolios. Players also seek digital edges, partnering with AI firms that provide imaging analytics and decision support.

Competitive pressure intensifies from supply-chain volatility. Firms with secured cobalt-chromium contracts or alternative alloy R&D avoid bottlenecks that delay rivals. Simultaneously, hospital networks weigh vendor consolidation to negotiate bulk discounts, favoring companies that bundle stents with guidewires, balloons, and imaging consoles. Such dynamics keep pricing fluid while sustaining innovation incentives.

Coronary Stent Industry Leaders

Boston Scientific Corporation

Medtronic Plc

Abbott

Terumo

B. Braun SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Teleflex finalized its USD 791 million acquisition of Biotronik’s vascular intervention unit, adding drug-coated balloons and sirolimus-eluting resorbable magnesium scaffolds.

- September 2024: FDA approved the Minima Stent System for pediatric coarctation of the aorta and pulmonary artery stenosis, extending cobalt-chromium frameworks to younger cohorts.

- August 2024: INFINITY-SWEDEHEART reported DynamX bioadaptor’s 0.6% target-vessel failure at one year versus 1.8% for Resolute Onyx.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the coronary stent market as every new metallic or polymeric scaffold engineered for percutaneous placement inside coronary arteries to re-establish patency. Revenue is tracked at ex-factory average selling price for bare-metal, drug-eluting, bioabsorbable, and dual-therapy stents delivered through balloon-expandable or self-expanding systems and implanted in hospitals, cardiac cath labs, and ambulatory surgical centers across 26 major economies.

Scope Exclusions: Valve repair devices and all peripheral or neurovascular stents are not evaluated.

Segmentation Overview

- By Product Type

- Drug-Eluting Stent (DES)

- Bare-Metal Stent (BMS)

- Bioabsorbable Vascular Scaffold (BVS)

- Dual-Therapy Stent (DTS)

- By Biomaterial

- Metallic

- Polymeric

- Natural / Bio-derived

- By Mode of Delivery

- Balloon-Expandable Stent

- Self-Expanding Stent

- By End User

- Hospitals

- Cardiac Catheterization Labs

- Ambulatory Surgical Centers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Analysts interview interventional cardiologists, cath-lab managers, hospital procurement leads, and reimbursement specialists across North America, Europe, and Asia-Pacific to validate PCI procedure growth, average stents per case, and emerging preferences such as thinner-strut DES and scaffold resorption timelines. Insights refine adoption curves and stress-test pricing and utilization assumptions.

Desk Research

We first compile open data from tier-one public sources such as the WHO Global Health Observatory, OECD Health Statistics, Europe's EHN databank, the CDC's NIS discharge files, and regional customs export tallies that report catheter and scaffold shipments. Regulatory registries (US FDA PMA, EU MDR EUDAMED, Japan PMDA) supply approval timelines that signal commercial launch dates, while financial filings and investor decks broaden visibility on product mix and price corridors.

Subscription tools, including D&B Hoovers for company revenues and Dow Jones Factiva for transaction news, help our analysts benchmark supplier share and triangulate price dispersion across geographies before numbers feed the model. The reference list above is illustrative; additional journals, association papers, and procurement portals are screened as needed.

Market-Sizing & Forecasting

A top-down construct starts with national PCI volumes, CAD prevalence, and typical stents-per-procedure ratios, which are then multiplied by blended ASPs to recreate 2025 demand. Supplier roll-ups from sampled invoices plus regional channel checks form a bottom-up lens that adjusts for gray-market leakages or bulk tenders.

Key variables like annual PCI growth, DES versus BMS share shifts, ASP erosion (bps), aging population increments, and reimbursement tariff changes enter a multivariate regression that projects value through 2030 under base, mild, and aggressive scenarios. Gaps where bottom-up evidence is thin are capped with sensitivity bands agreed during expert callbacks.

Data Validation & Update Cycle

Outputs pass two-level analyst review, variance screens versus external procedure trackers, and senior sign-off. The model refreshes every twelve months; interim updates trigger if recalls, landmark trial read-outs, or reimbursement resets move the market materially.

Why Mordor's Coronary Stents Baseline Commands Confidence

Published figures often diverge because each firm chooses different product baskets, price anchors, and refresh speeds.

Our disciplined scope, live PCI tracking, and annual recalibration minimize such drift.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.29 B (2025) | Mordor Intelligence | - |

| USD 8.3 B (2024) | Global Consultancy A | Counts outpatient kits only and omits self-expanding platforms |

| USD 7.02 B (2025) | Industry Publisher B | Excludes bioabsorbable scaffolds and applies single-price band across all regions |

The comparison shows that headline gaps stem less from 'who is right' and more from what is measured. By aligning stent types, delivery modes, and country baskets with real procedure volumes, Mordor delivers a balanced, transparent baseline clients can replicate and stress-test with confidence.

Key Questions Answered in the Report

What is the current value of the coronary stents market?

The coronary stents market stands at USD 8.66 billion in 2026 and is set to reach USD 10.75 billion by 2031.

Which product segment dominates the coronary stents market?

Drug-eluting stents lead with 75.64% revenue share in 2025 due to proven safety and efficacy.

Why is Asia-Pacific the fastest-growing region?

Public procurement reforms, expanding healthcare infrastructure, and rising cardiovascular disease prevalence drive a 7.32% CAGR in Asia-Pacific.

How are AI technologies influencing stent procedures?

AI-guided imaging improves vessel assessment and sizing, cutting complication rates and optimizing resource use in cath labs.

What impact do government price caps have on manufacturers?

Price ceilings in markets such as India and China compress margins by up to 90%, pushing companies to localize production and streamline costs.

Are bioabsorbable vascular scaffolds gaining traction?

Yes, next-generation scaffolds show improved safety, leading to a projected 7.52% CAGR, although late thrombosis remains a watch point.

Page last updated on: