Variable Data Printing Labels Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 21.79 Billion |

| Market Size (2031) | USD 29.37 Billion |

| Growth Rate (2026 - 2031) | 6.14% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

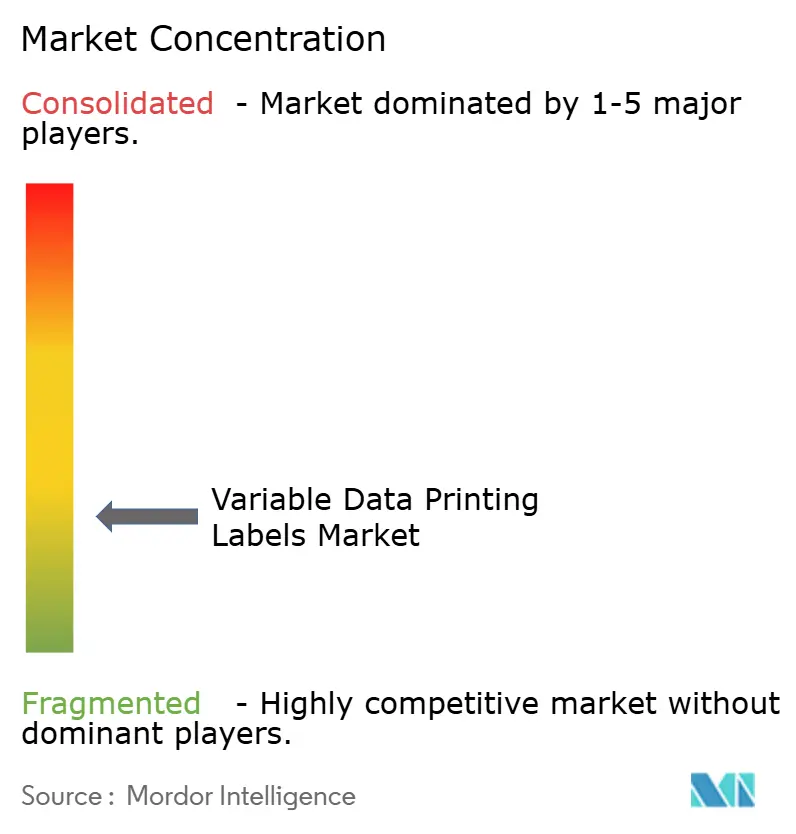

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Variable Data Printing Labels Market Analysis by Mordor Intelligence

The variable data printing labels market size is expected to grow from USD 20.53 billion in 2025 to USD 21.79 billion in 2026 and is forecast to reach USD 29.37 billion by 2031 at 6.14% CAGR over 2026-2031. Digital press breakthroughs, tighter traceability laws, and e-commerce parcel volumes elevate labels from simple identifiers to intelligent data carriers. Suppliers invest in higher-speed inkjet and electrophotographic lines to balance cost, quality, and security needs, while regulators push permanent serialization and recyclability codes. Hardware vendors respond with AI-enabled automation that cuts make-ready times, widening access for mid-volume converters. Concurrently, sustainability mandates fuel linerless adoption, and cloud-native label management platforms lower entry barriers for brand owners seeking dynamic campaigns.

Key Report Takeaways

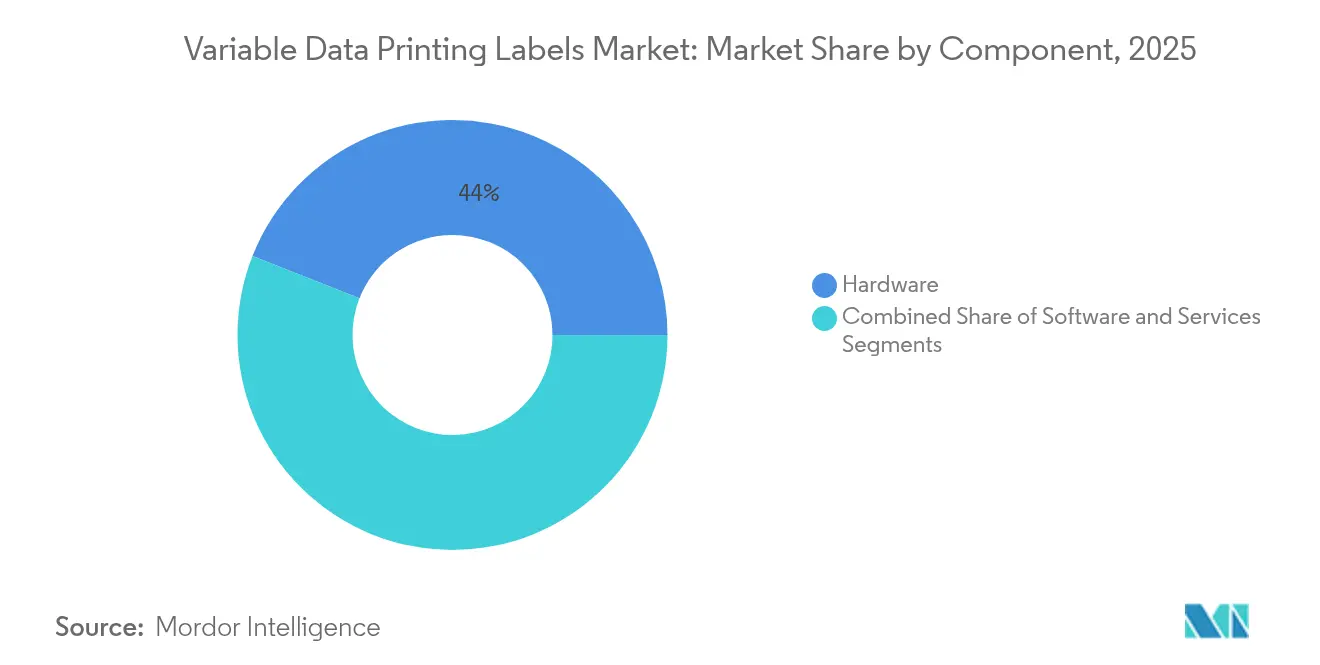

- By component, hardware led with a 44.02% revenue share in 2025 and also posted the highest projected 9.88% CAGR through 2031.

- By label type, release liner formats commanded 64.78% of 2025 revenues, whereas linerless solutions are set to expand at an 10.82% CAGR to 2031.

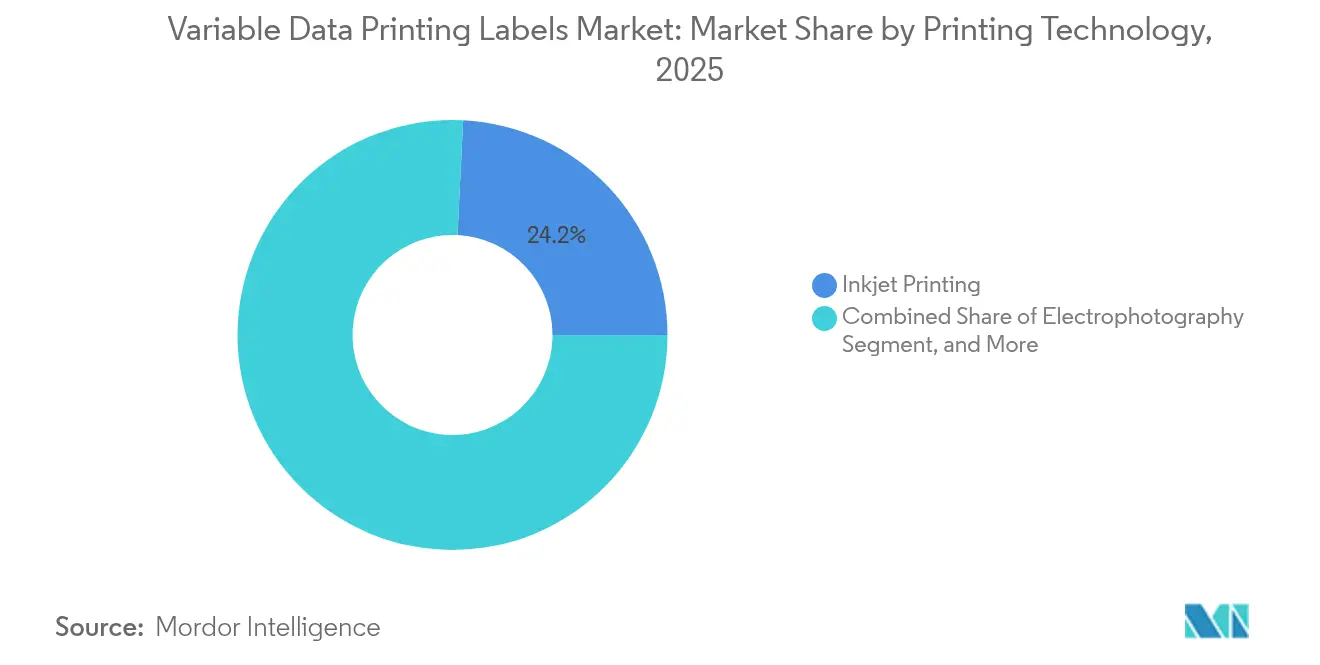

- By printing technology, inkjet systems captured 24.21% revenue share in 2025, while electrophotography is forecast to rise at a 9.54% CAGR on pharmaceutical serialization demand.

- By end-use industry, the food & beverage segment held 31.02% share in 2025, whereas retail and e-commerce applications are projected to record a 9.63% CAGR to 2031.

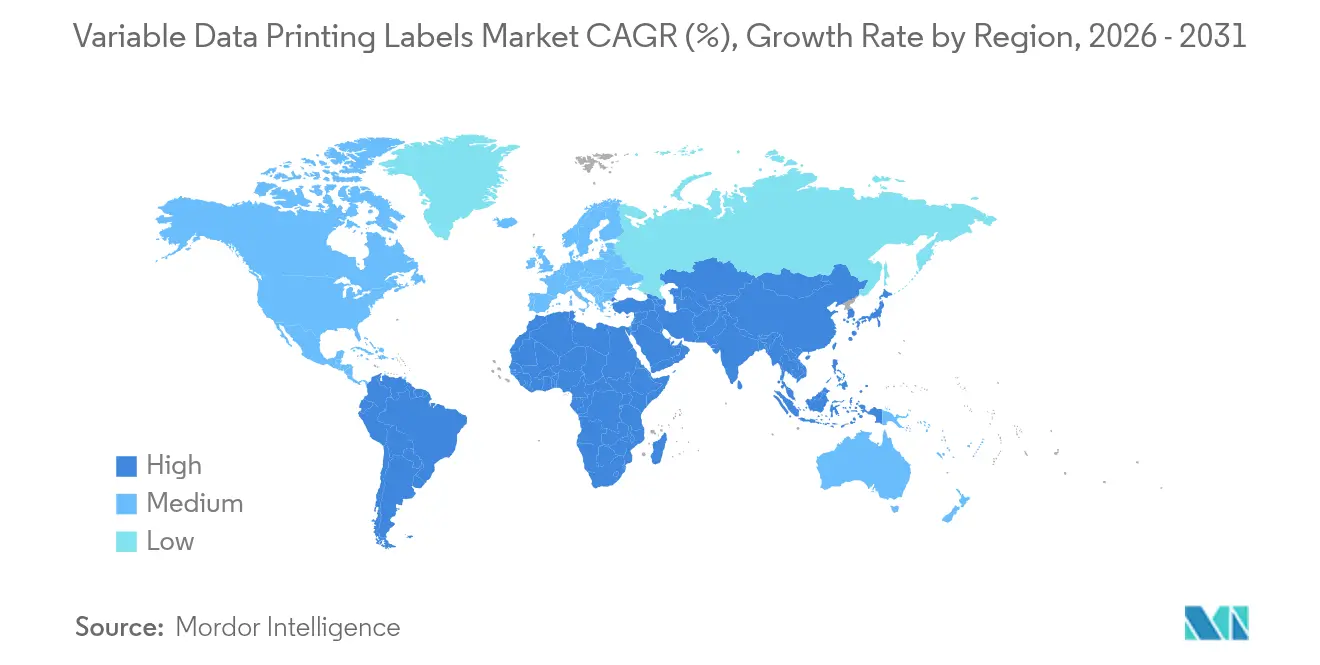

- By geography, North America dominated with a 37.96% revenue share in 2025, while Asia-Pacific is anticipated to grow the fastest at a 9.29% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Variable Data Printing Labels Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital printing technology breakthroughs (inkjet, UV-LED, LEP) | +1.8% | Global, concentrated in North America & Europe | Medium term (2-4 years) |

| Global anti-counterfeit and traceability regulations (UDI, DSCSA, EU-FMD) | +1.5% | North America & EU primary, expanding to APAC | Long term (≥ 4 years) |

| Explosive e-commerce and 3PL parcel volumes | +1.2% | Global, led by North America & APAC | Short term (≤ 2 years) |

| Brand-owner shift to mass-personalised packaging campaigns | +0.9% | Global, early adoption in North America & Europe | Medium term (2-4 years) |

| Cloud-native label management and SaaS VDP platforms | +0.6% | Global, technology hubs leading | Medium term (2-4 years) |

| Blockchain-enabled smart labels for provenance | +0.4% | EU & North America, pilot implementations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Digital Printing Technology Breakthroughs Drive Market Transformation

Next-generation inkjet, UV-LED, and liquid electrophotographic presses now reach 1600 dpi at 120 m/min, a speed-to-quality ratio that narrows the gap with flexography. Investments such as Epson’s USD 5.1 billion printhead facility to quadruple output by 2025 underline sustained hardware demand.[1]Tohoku Epson Corporation, “Tohoku Epson to Begin Construction on a 5.1-Billion yen Inkjet Printhead Production Plant,” corporate.epson Canon’s sheet-fed varioPRESS iV7 extends variable data into security print, enhancing anti-counterfeit measures. AI-driven press automation now predicts maintenance windows and auto-calibrates color, cutting downtime and waste. These shifts let converters replace static inventories with on-demand runs, enabling true mass customization across consumer segments.

Global Anti-Counterfeit and Traceability Regulations Accelerate Adoption

Unique device identifiers, serialized drug packages, and recyclability labels are no longer discretionary. The DSCSA compels U.S. pharma firms to print machine-readable codes on each saleable unit. EU Packaging and Packaging Waste rules effective 2025 add recyclability and material origin disclosures on all consumer packaging. Italy’s deadline for EU Regulation 2016/161 demands serialized Data Matrix codes on medicines. Food handlers must implement FSMA 204 QR codes to track critical ingredients across the supply chain. Each mandate pushes converters toward digital presses capable of variable, high-resolution, and verified data output.

E-Commerce and 3PL Parcel Volume Explosion Fuels Demand

Online retail parcels require real-time labels that merge fulfillment data, marketing content, and carrier codes. Sealed Air’s AutoPrint wraps print variable graphics on up to 15 boxes per minute, eliminating pre-printed SKU stocks. Domino’s on-cap printing stations now code 44,000 water bottles per hour, supporting label-less packaging in beverage logistics. American Packaging installed HP Indigo 200K presses to chase short-run flexible jobs tied to direct-to-consumer launches. Demand forecasting tools integrate with press queues, ensuring just-in-time label output that aligns with live inventory snapshots.

Brand-Owner Shift to Mass-Personalised Packaging Campaigns

Consumer brands use variable data to regionalize promotions and personalize unboxing. Ranpak’s Print’it! system custom-prints void-fill to boost customer engagement and reduce waste. Smart Cups prints beverage ingredients directly on disposable surfaces, illustrating how formula and design can co-exist within a single printed layer. Cloud SaaS platforms orchestrate graphics, language variants, and compliance data across SKUs in real time, shortening campaign cycles. The result is SKU-level agility that supports premium pricing strategies and controlled regional trials without stranded inventory.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex and TCO of industrial digital presses | -0.8% | Global, particularly affecting SMEs | Short term (≤ 2 years) |

| Data-privacy and cyber-risk in variable customer content | -0.5% | EU & North America, strict data protection | Medium term (2-4 years) |

| Shortage of skilled VDP pre-press/data-prep talent | -0.4% | Global, acute in developed markets | Long term (≥ 4 years) |

| Liner-waste recycling mandates raising compliance cost | -0.3% | EU primary, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure and Total Cost of Ownership Challenges

Presses such as the Indigo 120K carry seven-figure price tags that smaller converters struggle to amortize without consistent high volumes. Ricoh’s workforce reduction highlights the margin pressure that arises when firms juggle upgrade cycles and profit expectations. Integration expenses for color servers, variable data toolkits, and MIS connectivity raise the breakeven threshold further. Consequently, some converters delay adoption, tempering the near-term growth of the variable data printing labels market.

Data Privacy and Cybersecurity Risks in Variable Content Processing

Handling consumer data and serialized healthcare information exposes converters to GDPR fines and IP theft. Blockchain-enabled passports promise immutable audits but introduce new attack surfaces that demand skilled oversight. Cloud-based label management centralizes assets but forms single points of failure if not hardened. Pharmaceutical code streams carry authentication keys that hackers could exploit to infiltrate supply-chain records, adding layers of compliance cost for printers seeking defense-in-depth architectures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Dominance Drives Infrastructure Modernization

Hardware accounted for 44.02% of 2025 revenues and is projected to compound at 9.88% annually to 2031, anchoring the variable data printing labels market size gains in capital equipment upgrades. Epson’s multi-billion-dollar printhead expansion signals confidence in a sustained hardware refresh cycle. Software revenues grow from a smaller base as converters migrate workflow and color management to SaaS suites. Services, though modest today, scale rapidly through predictive maintenance and data-driven optimization. The variable data printing labels market share for hardware stays large because converters need dedicated presses rather than retrofits. AI-ready sensors embedded in new lines extend service contracts, tying OEMs to customers over longer lifecycles. Software vendors capitalize on subscription models that democratize variable data layouts for mid-tier brands. Services firms exploit skills gaps in data preparation, a pain point intensified by personalized artwork requirements. Together, the three components form a symbiotic ecosystem that reinforces capital and recurring revenue streams across the variable data printing labels industry.

By Label Type: Linerless Innovation Challenges Traditional Formats

Release liner labels held 64.78% of 2025 revenue, dominating applications requiring precise die-cuts and extended shelf life. Linerless alternatives, however, are forecast at an 10.82% CAGR, supported by mandates to lower packaging waste. OptiCut WashOff and other wash-off adhesives help beverage brands reach reuse targets while enabling circular models. Linerless rolls offer up to 50% more labels per roll, improving logistics density and reducing downtime. Brands adopting linerless cut landfill fees tied to silicone liners, a hidden cost increasingly captured in sustainability audits. Zebra and Avery Dennison now supply micro-perforated liners that further stretch roll yield. The accelerated uptake widens the variable data printing labels market, especially as press OEMs refine tension control systems suited to linerless webs. However, release-liner formats remain entrenched in curved or irregular surfaces where positional accuracy overrides waste concerns. This coexistence ensures both label types continue to attract R&D budgets, each optimized for specific performance criteria within the broader variable data printing labels market.

By Printing Technology: Electrophotography Accelerates Despite Inkjet Leadership

Inkjet accounted for 24.21% of 2025 revenues, favored for substrate flexibility and economical short runs. Electrophotography, though smaller, is projected to expand at 9.54% CAGR due to its 1600 dpi accuracy suited to pharmaceutical security printing. Hybrid UV-inkjet units like Domino’s N610i achieve 1 million 3-inch labels in six hours, merging speed with digital variability. Thermal transfer infrastructures persist in chemical and automotive labels demanding chemical resistance. Direct thermal dominates parcel and grocery receipts where shelf life is short. Flexography loses share as converters eschew plate costs when SKUs proliferate. Despite competition, inkjet OEMs integrate expanded gamut inks, while electrophotography leverages liquid toners to reach offset-grade smoothness. Both technologies tap cloud analytics for uptime gains, reinforcing their twin roles inside the variable data printing labels market.

By End-Use Industry: Retail E-Commerce Disrupts Food & Beverage Leadership

Food & beverage retained 31.02% share in 2025 thanks to stringent traceability and freshness codes. Retail and e-commerce, however, are on track for a 9.63% CAGR, mirroring parcel growth and personalization campaigns. QR-enabled labels now link shoppers to authenticity sites, product origins, and dynamic promotions. Healthcare, driven by DSCSA serialization, pursues smudge-proof, overt-covert security features. Logistics segments deploy variable barcodes that sync with WMS data for real-time routing. Cosmetics brands exploit micro-batch wraps for influencer collaborations that demand rapid artwork swaps. This multi-industry pull broadens the variable data printing labels market, enabling converters to diversify revenue risk while exploiting cross-sector synergies in software and substrate procurement.

Geography Analysis

North America controlled 37.96% of 2025 revenues as FDA serialization and USPS technology refresh programs unlocked steady hardware demand. Large CPGs leverage scale economics to roll out mass-customized campaigns that keep press utilization high. Europe’s regulatory wave on packaging recyclability turns label lines into compliance engines; converters race to embed material disclosures in multiple languages. Pharmaceutical hubs in Italy and Germany adopt high-resolution coding to meet FMD deadlines, sustaining electrophotography uptake.

Asia-Pacific grows fastest at 9.29% CAGR. India’s Multi-Label Tech-Print added Domino N610i capacity to serve booming direct-to-consumer brands. China’s textile sector expects 4.7 billion meters of digital print by 2025, signaling a wider migration to variable techniques in adjacent label niches. Southeast Asian 3PLs adopt linerless to cut parcel waste, while Japanese electronics exporters integrate blockchain-backed provenance labels to bolster global trust.

Latin America and the Middle East enter growth curves later as food safety and agriculture export rules tighten. Mexico’s Etiflex acquisition by ProMach expands pressure-sensitive and RFID capacity, laying groundwork for regional serialization adoption. GCC states pilot smart halal-compliance labels, pairing QR codes with cloud certificates. Africa’s emerging pharmaceutical clusters evaluate digital presses to leapfrog analog, but funding gaps slow deployment, tempering the variable data printing labels market size trajectory there.

Competitive Landscape

The variable data printing labels market remains moderately fragmented. Legacy equipment giants like HP, Xeikon, and Canon integrate AI diagnostics to protect installed bases. The Xeikon-EFI partnership pools inkjet IP and service networks, giving users a single stack for hardware and RIP software. Xerox’s USD 1.5 billion acquisition of Lexmark expands printhead manufacturing depth and opens Asian sales channels, signaling a tilt toward scale consolidation. Zebra and Merck co-develop the M-Trust platform that fuses mobile scan devices with chemical authentication, differentiating on security.

Digital-native challengers focus on cloud orchestration, delivering label-as-a-service models that bypass capex barriers for niche brands. Arrow Systems bundles Fiery Impress workflow into ArrowJet UV engines to push inline varnish and automation downmarket. Service consolidators such as Propelis merge design, pre-press, and fulfillment to offer turnkey personalization to multinationals. Patent filings on blockchain digital certificates by Alibaba and others underline an innovation race centered on anti-tamper and trace-back value propositions.[3]USPTO, “System and Method for Implementing Blockchain-Based Digital Certificates,” uspto.report Overall, competition pivots on ecosystem completeness rather than raw press speed, with successful players knitting hardware reliability, SaaS workflows, and security IP into defensible bundles across the variable data printing labels market.

Variable Data Printing Labels Industry Leaders

Canon Inc.

Xerox Corporation

Ricoh Company Ltd.

Seiko Epson Corporation

Konica Minolta Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Zebra Technologies and Merck KGaA unveiled the M-Trust cyber-physical trust solution for anti-counterfeiting applications.

- February 2025: Xeikon and EFI formed an exclusive strategic partnership for digital label printing.

- January 2025: American Packaging Corporation installed two HP Indigo 200K presses at its Wisconsin site to serve flexible packaging markets.

- January 2025: Arrow Systems partnered with Fiery Impress to automate ArrowJet UV workflows.

Global Variable Data Printing Labels Market Report Scope

Variable data printing labels allows businesses to personalize labels in a high-quality, cost-effective manner. VDP labels are used in many industries, including food and beverage, pharmaceuticals, and consumer goods. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrived at top-down and bottom-up approaches.

Variable data printing labels market is segmented by component (Hardware, Software and Services), by Label (Release Liner Labels and Linerless Labels), by printing method (Thermal Transfer Printing, Direct Thermal Printing, Inkjet Printing, Electrophotography, Flexographic Printing and Other Methods), by end-use industry (Healthcare, Retail & E-Commerce, Food & Beverage, Logistics and Other End-Use Industries), and by geography (North America, Europe, Asia Pacific, South America and Middle East and Africa). The market sizing and forecasts are provided in terms of value (USD) for all the above segments.

| Hardware |

| Software |

| Services |

| Release Liner Labels |

| Linerless Labels |

| Thermal Transfer Printing |

| Direct Thermal Printing |

| Inkjet Printing |

| Electrophotography |

| Flexographic Printing |

| Healthcare |

| Retail and E-Commerce |

| Food and Beverage |

| Logistics and Transportation |

| Industrial Manufacturing |

| Personal Care and Cosmetics |

| Other End-use Industry |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Label Type | Release Liner Labels | ||

| Linerless Labels | |||

| By Printing Technology | Thermal Transfer Printing | ||

| Direct Thermal Printing | |||

| Inkjet Printing | |||

| Electrophotography | |||

| Flexographic Printing | |||

| By End-use Industry | Healthcare | ||

| Retail and E-Commerce | |||

| Food and Beverage | |||

| Logistics and Transportation | |||

| Industrial Manufacturing | |||

| Personal Care and Cosmetics | |||

| Other End-use Industry | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the variable data printing labels market?

The variable data printing labels market size stands at USD 21.79 billion in 2026 and is projected to reach USD 29.37 billion by 2031.

Which component segment leads the market?

Hardware dominates with a 44.02% revenue share in 2025, reflecting ongoing press modernization cycles.

Why are linerless labels gaining traction?

Linerless formats cut waste, boost roll yield by up to 50%, and comply with new recyclability mandates, driving an 10.82% CAGR through 2031.

Which region is growing the fastest?

Asia-Pacific is forecast to expand at a 9.29% CAGR thanks to manufacturing digitization and rising e-commerce demand.

What technological trend is most influential?

High-speed inkjet and electrophotographic presses equipped with AI-driven automation enable mass personalization while maintaining offset-grade quality.

How is regulation influencing market growth?

Laws such as the DSCSA, EU Packaging & Waste rules, and FSMA 204 mandate serialized or recyclable labels, making variable data capabilities a compliance necessity.

Page last updated on: