Industrial Labels Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

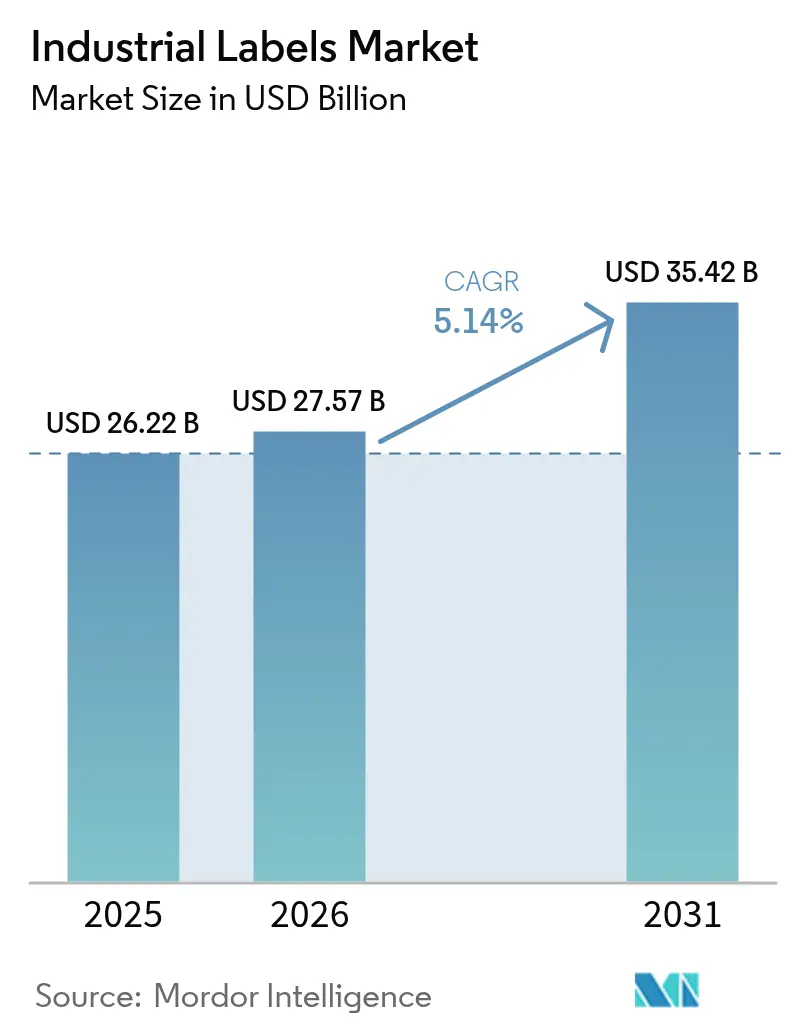

| Market Size (2026) | USD 27.57 Billion |

| Market Size (2031) | USD 35.42 Billion |

| Growth Rate (2026 - 2031) | 5.14% CAGR |

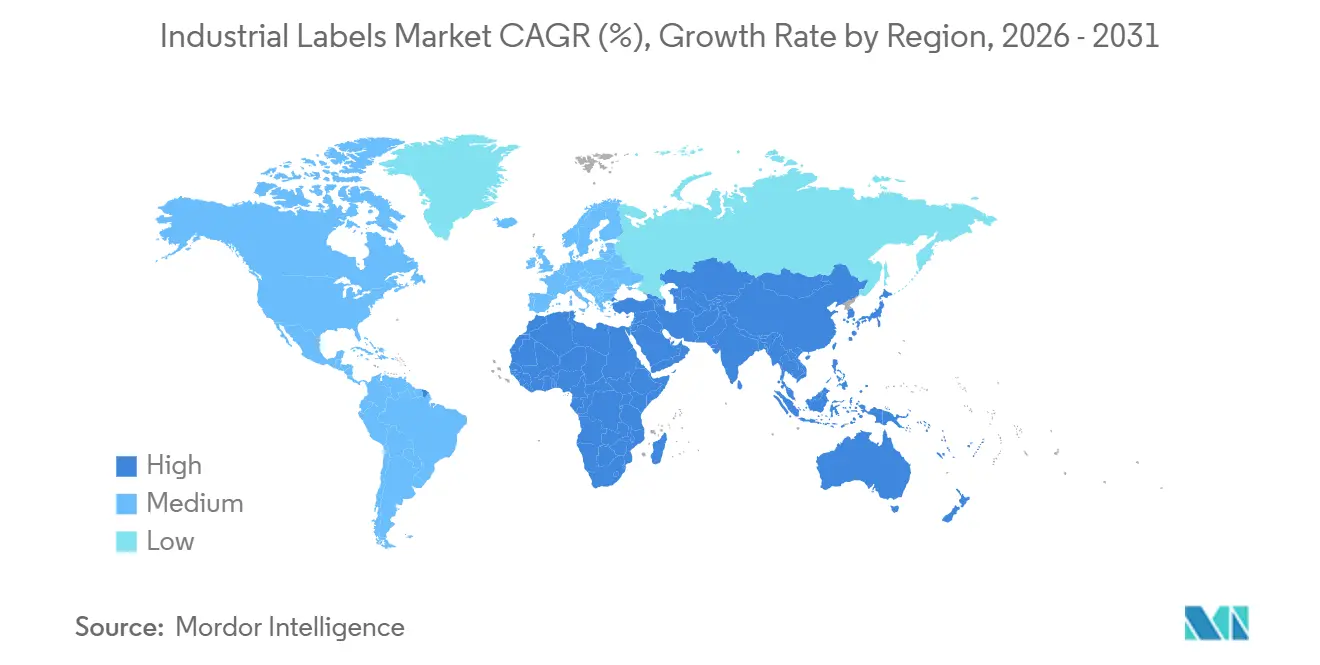

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

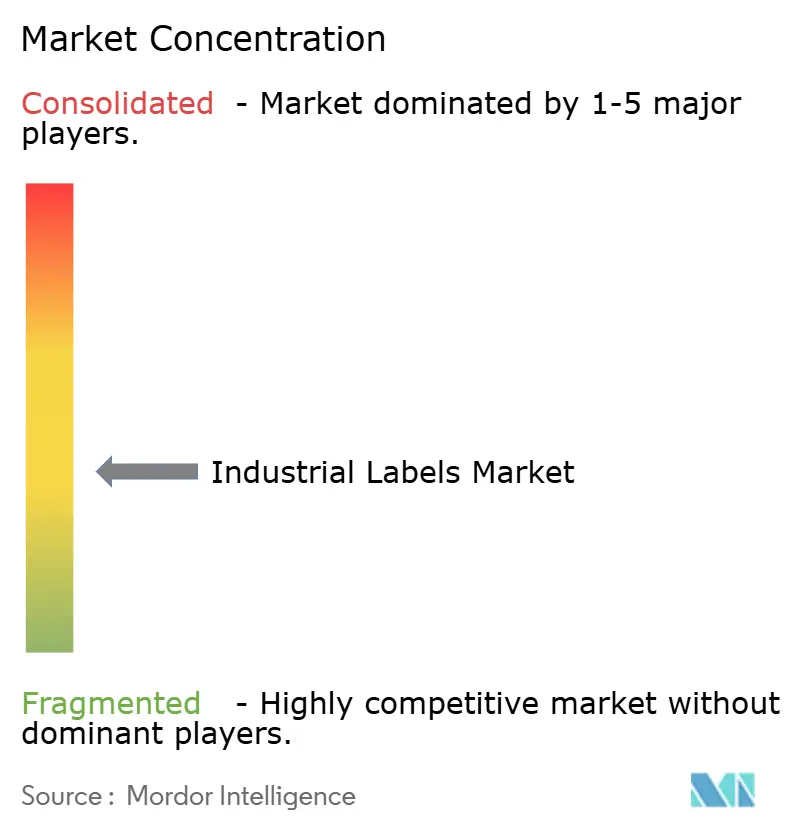

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Labels Market Analysis by Mordor Intelligence

The industrial labels market size is expected to increase from USD 26.22 billion in 2025 to USD 27.57 billion in 2026 and reach USD 35.42 billion by 2031, growing at a CAGR of 5.14% over 2026-2031. Expedited parcel activity, serialization deadlines, and sustainability legislation converge to keep demand resilient even when discretionary spending moderates. Smart-label adoption by brand owners adds higher-value square inches, supporting converter margins. E-commerce creates three to five label touches per shipment, widening the installed base of thermal-transfer and direct-thermal printers. Meanwhile, liner-less rolls and fiber substrates penetrate specifications for food service, logistics, and quick-turn consumer goods, reducing waste fees but requiring adhesive reformulation. Digital and hybrid presses shorten artwork change cycles, allowing compliant updates within days rather than weeks and lowering obsolete inventory write-offs.

Key Report Takeaways

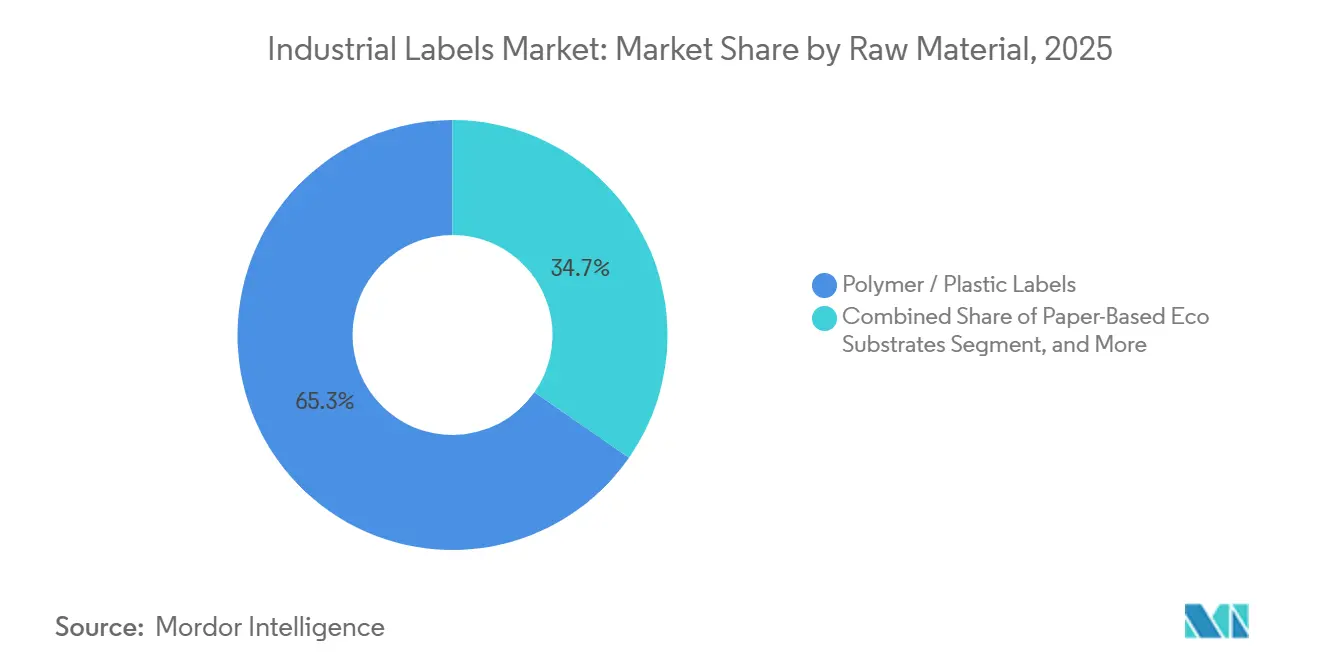

- By raw material, polymer and plastic substrates led with 65.32% of the industrial labels market share in 2025; paper-based eco alternatives are projected to expand at a 5.94% CAGR to 2031.

- By mechanism, pressure-sensitive constructions held 49.83% of the industrial labels market share in 2025, while liner-less formats are forecast to advance at a 6.14% CAGR through 2031.

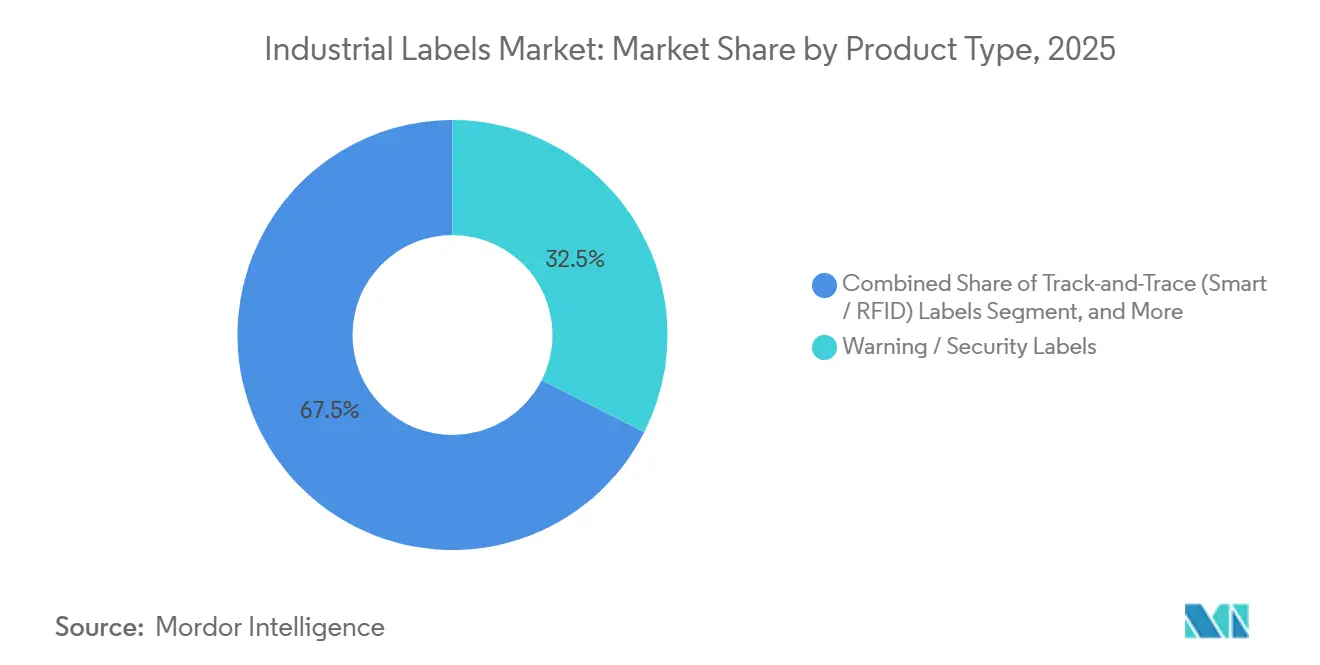

- By product type, warning and security graphics accounted for 32.46% of revenue in 2025; track-and-trace smart labels are expected to grow at a 6.16% CAGR through 2031.

- In the printing technology segment, digital engines accounted for 43.78% of the industrial labels market size in 2025, and hybrid presses are set to post a 5.91% CAGR during 2026-2031.

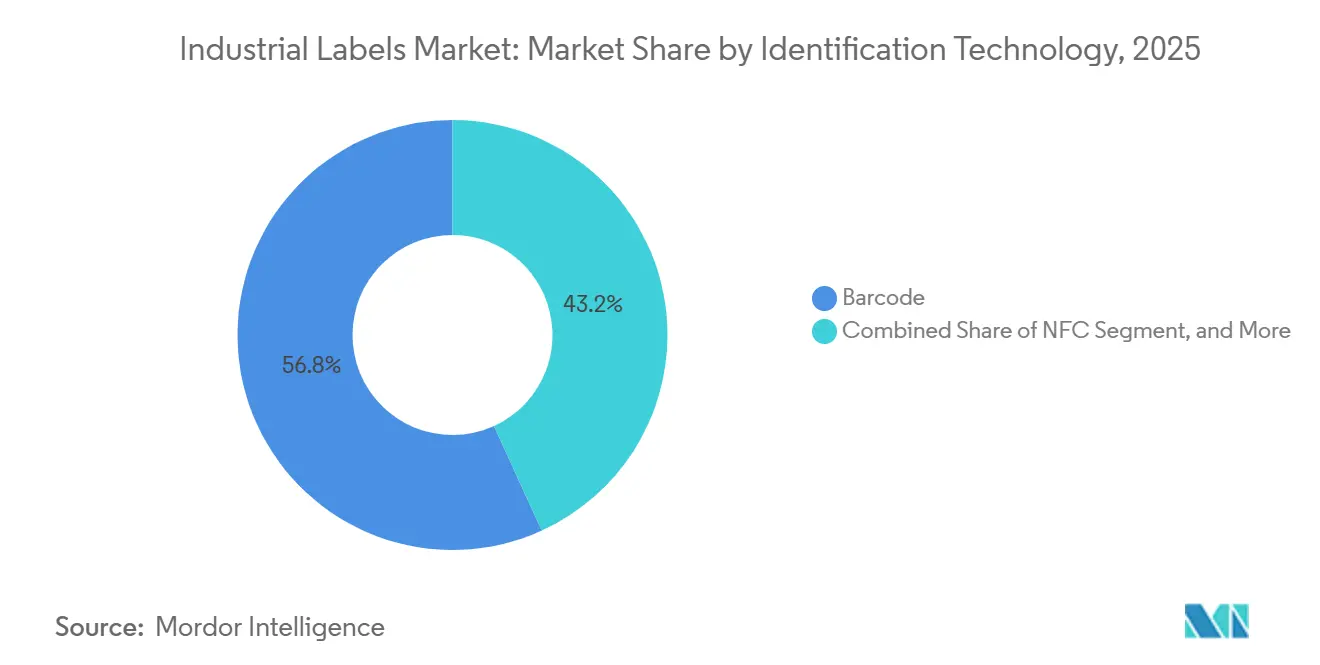

- By identification technology, barcodes dominated the industrial label market with 56.82% market share in 2025; NFC chips are projected to grow at a 6.11% CAGR to 2031.

- By end-user, food and beverage accounted for 29.47% of sales in 2025, while healthcare and pharmaceuticals are expected to register a 6.73% CAGR through 2031.

- By geography, Asia-Pacific accounted for 37.29% of revenue in 2025 and is projected to grow at a 6.19% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Industrial Labels Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Adoption of Near-Field Communication (NFC) Labels for Asset Authentication | +0.9% | Global, with early concentration in North America and Europe luxury goods, Asia-Pacific electronics | Medium term (2-4 years) |

| Rising Demand from Food and Beverage Compliance Labelling | +0.8% | Global, particularly Europe and North America due to allergen and origin disclosure mandates | Short term (≤ 2 years) |

| Accelerating E-Commerce and Logistics Labelling Growth | +0.7% | Global, with highest intensity in Asia-Pacific and North America fulfillment hubs | Short term (≤ 2 years) |

| Regulatory Mandates for Traceability and Safety | +0.7% | Global, led by FDA DSCSA in United States, EU FMD in Europe, GHS globally | Long term (≥ 4 years) |

| Rapid Adoption of Digital and Hybrid Printing Technologies | +0.6% | Global, with faster uptake in North America and Europe brand-owner networks | Medium term (2-4 years) |

| Growth of Closed-Loop Industrial Recycling Bolstering Demand for Removable Liner-Less Labels | +0.5% | Europe and North America, expanding to Asia-Pacific as Extended Producer Responsibility schemes mature | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Adoption of Near-Field Communication Labels for Asset Authentication

Luxury apparel, spirits, and consumer electronics brands increasingly embed NFC chips that prove provenance with a smartphone tap, dissuading counterfeit trade and engaging post-purchase consumers.[1]LVMH, “Innovation Report 2024,” lvmh.com Converters benefit from unit price escalation because an encoded inlay can cost five to ten times as much as a printed barcode. Deployment gained momentum in 2025 after leading handset makers pre-installed reader apps, eliminating software friction. In parallel, automotive OEMs adopted rewritable NFC tags for maintenance logs, extending the addressable pool beyond retail items. Asia-Pacific factories ramped up output as secure-element suppliers partnered with label conglomerates to certify contactless performance across polyester, paper, and foil substrates.

Rising Demand from Food and Beverage Compliance Labelling

Mandatory allergen statements, front-of-pack nutrition scores, and bioengineered-food symbols enlarge text areas, forcing rescaled graphics and multi-panel constructions.[2]U.S. Food and Drug Administration, “Bioengineered Food Disclosure,” fda.gov Brand owners reorder smaller batches to avoid obsolete inventory whenever agencies update reference values, stimulating digital print throughput. Voluntary seals such as Rainforest Alliance push additional iconography, fragmenting SKUs and shortening design life cycles. The net effect is sustained volume growth and a preference for variable-data workflows that serialize batch and best-by codes inline, thereby preventing costly recall exposure.

Accelerating E-Commerce and Logistics Labelling Growth

Global parcel movements topped 200 billion in 2025 and continue to rise, each shipment needing at least one address label, a return tag, and often a duty declaration.[3]Amazon, “2024 Sustainability Report,” amazon.com Fulfillment centers demand polypropylene and polyethylene films that tolerate sub-zero cold-chain lanes and high-speed sortation without abrasion. Carriers also request liner-less options that slash waste tonnage and streamline automatic applicators. Cross-border sellers rely on ribbon-compatible face stocks that preserve print density throughout two-week ocean voyages, nudging converters toward thermal-transfer coatings engineered for ultraviolet resistance.

Regulatory Mandates for Traceability and Safety

The U.S. Drug Supply Chain Security Act, the European Union Falsified Medicines Directive, and United Nations hazard-communication frameworks converge to require unique identifiers, tamper-evident features, and pictograms on millions of industrial labels. Pharmaceutical lines integrate 2D data matrices and RFID to verify provenance, while chemical drums swap generic stickers for standardized GHS icons. Compliance audits intensified in 2025, triggering retrofit projects that boosted sales of durable polyester labels and on-press vision inspection. Long-term, this driver anchors sticky demand even when discretionary sectors soften.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Raw-Material and Adhesive Pricing | -0.6% | Global, with acute exposure in Asia-Pacific and Europe due to import dependency | Short term (≤ 2 years) |

| Stringent Environmental Regulations on Plastics and VOCs | -0.5% | Europe and North America, expanding to Asia-Pacific as Extended Producer Responsibility matures | Medium term (2-4 years) |

| Short Lifecycle of Industrial IoT Label Firmware Leading to Obsolescence Risk | -0.3% | Global, concentrated in North America and Europe early-adopter verticals | Long term (≥ 4 years) |

| Limited Interoperability Standards Across Smart Label Ecosystems Hindering Scale | -0.3% | Global, with highest friction in cross-border supply chains spanning multiple regulatory jurisdictions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Raw-Material and Adhesive Pricing

Label-grade acrylics link directly to crude-oil inputs, so refinery outages or OPEC quota shifts move adhesive costs by double-digit percentages quarter to quarter. Silicone shortages in 2024 raised liner costs, squeezing converters on commodity SKUs with thin margins. Smaller regional printers lack hedging programs and must pass increases downstream, risking order loss to larger vertically integrated rivals. Price swings also delay sustainability projects because converters divert capital from equipment upgrades to feedstock procurement.

Stringent Environmental Regulations on Plastics and VOCs

The European Union Single-Use Plastics Directive penalizes non-recyclable components, and U.S. states cap volatile organic compound emissions from solvent inks. Converters must invest in water-based chemistries, regenerative thermal oxidizers, and life-cycle assessments, thereby raising capital intensity, especially for plants with revenue under USD 100 million. Clients push for proof of compliance, embedding sustainability scores in bid sheets that weaker suppliers cannot satisfy, effectively narrowing the vendor pool.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Raw Material: Fiber Substrates Gain Ground on Plastics

Polymer and plastic substrates represented 65.32% of the industrial labels market share in 2025, favored for their moisture resistance and compatibility with high-speed applicators on beverage and personal-care lines. They continue to dominate hazardous environments where tensile strength and chemical inertness drive specification, yet their use now attracts single-use-plastic fees in Europe and Canada. Major converters respond by qualifying thinner polyethylene and polypropylene films in order to reduce resin consumption without sacrificing run-speed performance. Adhesive suppliers also introduce low-migration acrylics that bond to polyolefins while meeting food-contact limits, a prerequisite for cold-chain grocery and ready-meal trays.

Paper-based eco substrates capture the fastest trajectory, with the industrial labels market size for fiber materials forecast to expand at a 5.94% CAGR through 2031 as brand owners chase recyclability logos and lower landfill levies. Clay-coated kraft stocks absorb water-based inks, allowing compliant front-of-pack nutrition tables to print in a single pass, although they require humidity-tolerant varnishes in refrigerated channels. Hybrid laminates that marry paper to thin polyethylene barriers offer splash protection for fresh meat, but curbside recyclers often reject the composite unless delamination is available. Metal foils hold a narrow niche in engine chambers and hydraulic pumps, where aluminum nameplates withstand 150 °C heat cycles and caustic solvents while maintaining print contrast for 10 or more years.

By Mechanism: Liner-Less Rolls Challenge Pressure-Sensitive Staples

Pressure-sensitive formats retained 49.83% of the industrial labels market share in 2025 because legacy dispensers apply them at more than 1,000 units per minute, and curved containers demand their conformability. Ongoing improvements in UV-cured acrylics boost tack at lower coat weights, so beverage fillers can down-gauge facestock caliper without losing shelf life. Glue-applied wrap-arounds see volume pressure as brewers migrate to aluminum cans that favor shrink-sleeves or pressure-sensitives. Shrink-sleeve graphics deliver 360-degree artwork and tamper evidence, though their PET-G and PVC films incur extended producer responsibility surcharges when they contaminate bottle-recycling streams.

The industrial labels market size for liner-less products is projected to grow at a 6.14% CAGR to 2031, as each roll packs 30-40% more labels, lowering freight and warehouse costs while eliminating silicone-liner disposal fees. Retail distribution centers already mandate liner-less carton tags to meet zero-waste scorecards, and food-service chains adopt coated paper liner-less tickets that withstand grease and freezer burn. In-mold and heat-transfer graphics, while capital-intensive, are steadily gaining ground in appliance housings and tool casings that demand scuff-proof legends baked into the substrate. As multinationals tighten landfill budgets, liner-less penetration accelerates despite its 15% price premium over commodity pressure-sensitives.

By Product Type: Smart Labels Accelerate Beyond Warning Tags

Warning and security graphics accounted for 32.46% of 2025 revenue, meeting OSHA and GHS requirements for chemical, battery, and heavy machinery iconography. They rely on polyester and vinyl films coated with heat-stable inks that resist abrasion in outdoor or engine-compartment use, assuring legibility throughout a product’s service life. Tamper-evident overlays are moving from brittle films to frangible papers that fiber-tear on removal, lowering material costs and meeting recyclability goals. Weather-proof nameplates target marine and construction gear, where UV-absorbing varnishes stop yellowing over a decade of sun exposure.

Track-and-trace smart and RFID constructs are expected to post a 6.16% CAGR, the quickest of all product categories, as luxury goods and pharmaceuticals embed near-field or ultra-high-frequency chips for provenance verification. The industrial labels market for asset tags also grows as warehouse operators tie passive RFID tags and barcodes together for real-time cycle counts, cutting labor hours in half. Branding labels remain premium, using foil stamping, tactile varnish, and holograms to differentiate spirits and cosmetics, but their unit growth lags because embellishment costs limit adoption in value segments. Converters therefore diversify by integrating chip inlays with decorative effects so a single multilayer label satisfies both marketing and compliance objectives.

By Printing Technology: Hybrid Presses Blend Analog Yield with Digital Agility

Digital electrophotographic and inkjet engines captured 43.78% of the industrial labels market share in 2025, eliminating plate logistics and supporting sub-5,000-foot runs for regional SKUs and seasonal promotions. Variable-data capability makes them indispensable for DSCSA pharmaceutical serial numbers and QR-based food recall links, while water-based inks now meet indirect food-contact migration limits. Entry-level leasing below USD 5,000 per month opens doors for small converters, and cloud workflows automate prepress, enabling artwork to move from upload to press in under 2 hours.

Hybrid presses are forecast to expand at a 5.91% CAGR, lifting the industrial labels market size for equipment that couples flexographic stations producing opaque whites and metallic inks with inline inkjet heads applying serialization in the same pass. Long beverage jobs remain cost-efficient on high-speed flexo, yet brand owners increasingly ask suppliers to prove hybrid capacity for mid-range quantities. Screen printing endures in durable nameplates where 25-micron ink deposits fight abrasion and chemicals, but its share inches down as UV-inkjet achieves higher viscosity and opacity. Overall, the choice of technology hinges on balancing make-ready waste, substrate versatility, and the growing frequency of regulatory text edits.

By Identification Technology: NFC Chips Challenge Barcode Primacy

One-dimensional and 2D barcodes still dominated, with 56.82% of the industrial label market share in 2025, thanks to fractions-of-a-cent ink costs and universal scanner support. New symbologies, such as GS1 Digital Link, add web addresses without enlarging the footprint, letting brands keep existing automated lines while unlocking consumer engagement. Logistics giants rely on barcode redundancy even when they deploy RFID, ensuring a visual fallback if a pallet reader fails. Thermal-transfer ribbons advance in pigment load, improving contrast so miniaturized codes remain machine-readable on ampoules and surface-mount electronics.

NFC enjoys the quickest ascent, with the industrial-labels market for contactless chips rising at a 6.11% CAGR as nearly every smartphone ships reader-ready. Luxury fashion, spirits, and automotive spares use encrypted NFC tags to battle counterfeit losses and run loyalty polls at the point of sale. Passive RFID remains vital in big-box retail and warehousing because hundreds of tags can be interrogated in seconds without line of sight, but the per-unit cost still prevents a wide rollout for low-margin groceries. QR codes bridge compliance and marketing, serving upcoming EU digital product passports on textiles and batteries through low-cost, camera-ready graphics.

By End-User Industry: Healthcare Serialization Leads Future Growth

Food and beverage retained 29.47% of 2025 revenue, as every packed item must show allergen information, front-of-pack nutrition data, and best-by dates in tamper-proof packaging. Plant upgrades install automated vision inspection that flags missing Nutri-Scores, while shift-to-paper initiatives reduce packaging taxes in Europe. Private-label expansion, however, trims overall volume growth as retailers streamline graphics and order just-in-time batches using digital presses.

Healthcare and pharmaceuticals are projected to record a 6.73% CAGR, the highest among sectors, because DSCSA and EU FMD deadlines force serialized, tamper-evident labels on every saleable unit. The industrial labels market for hospitals also grows as bedside medication administration uses barcoded wristbands, IV bags, and specimen tubes linked to electronic health records. Electronics producers demand polyimide labels that withstand 260 °C solder reflow, while automotive OEMs require polyester tags with 10-year chemical resistance under hood conditions. Logistics operations drive steady thermal-shipping-label consumption as global parcel counts escalate, and construction fleets embed RFID to automate preventive maintenance schedules, rounding out a diverse, compliance-centric demand base.

Geography Analysis

Asia-Pacific accounted for 37.29% of the industrial labels market share in 2025 and is projected to expand at a 6.19% CAGR through 2031, fueled by electronics assembly in China, pharmaceutical serialization lines in India, and rising contract manufacturing in Vietnam. Converters benefit from tax holidays on imported digital presses and gain volume through localized liner-less and RFID inlay production. Regional governments encourage recycled-content paper by waiving landfill fees, prompting substrate swaps on fast-moving consumer goods. Foreign investors also commission hybrid fleets near Shenzhen and Ho Chi Minh City to serve just-in-time export orders. As a result, the industrial labels market in Asia-Pacific is expected to contribute the largest incremental revenue during the forecast window.

North America ranked second in 2025, supported by FDA serialization audits, OSHA hazard communication rules, and parcel growth tied to same-day delivery services. Brand owners pay premiums for pressure-sensitive facestocks that meet low-migration limits and liner-less formats that cut warehouse waste. Canada adopts extended producer responsibility fees similar to those in Europe, motivating early trials of fiber substrates for chilled foods. Europe shows balanced growth as Germany and France impose eco taxes that favor recyclable constructs, while the United Kingdom’s post-Brexit labeling divergence forces dual artwork streams and doubles short-run print orders. Both regions shift a growing slice of the industrial labels market size toward hybrid presses that accelerate regulatory text updates.

South America posts mid-single-digit gains, led by Brazil’s pharmaceutical clusters and Argentina’s food exporters, yet currency swings lift adhesive and film costs for smaller converters. The Middle East and Africa remain the smallest segment, but pockets such as the United Arab Emirates' logistics hubs and South African automotive plants require multilingual shipping and durable under-hood tags. Supply constraints on silicone liner and thermal ribbon imports limit regional throughput, encouraging joint ventures that localize coating operations. Governments in Kenya and Saudi Arabia introduce barcoding mandates on medical devices, creating new demand for 600-dpi desktop thermal printers. Overall, infrastructure expansion and regulatory enforcement set the tempo of label spend across these emerging markets.

Competitive Landscape

The industrial labels market exhibits moderate concentration, with the top five suppliers accounting for an estimated 35-40% of the market. Avery Dennison, CCL Industries, and 3M leverage captive adhesive and liner plants to buffer raw-material swings and secure service contracts with global brand owners. Brady and Zebra bundle printers, software, and cloud analytics, locking in consumables and maintenance revenue across hospitals and logistics hubs. Regional converters retain customers by stocking local language templates and providing 48-hour reprints when legislation changes.

Strategic investment follows demand migration. In 2026, Avery Dennison opened a USD 50 million RFID inlay facility in Vietnam to shorten lead times for apparel exporters, while CCL bought a EUR 80 million pharmaceutical converter that brings serialized booklet capacity into Central Europe. 3M commercialized a food-contact-safe liner-less adhesive that qualifies for German and French EPR credits, positioning its tapes division for growth in grocery and quick service restaurants. Honeywell expanded ribbon coating in China, and DuPont launched a bio-based polyester film that cuts the carbon footprint by 35%, giving converters new selling points on sustainability scorecards. Hybrid press manufacturers partner with substrate innovators so buyers can certify both the machine and the material in a single factory acceptance test.

Digital-native disruptors intensify price competition by offering web-to-print portals with no minimum order quantity, winning small craft beverage and cosmetics clients. Artificial-intelligence color matching reduces make-ready scrap, and blockchain authentication layers onto NFC and RFID tags for luxury goods, pharmaceuticals, and industrial spares. Patent filings focus on algae-based liners, ultra-thin antenna embedding, and low-migration inks, signaling further differentiation beyond commodity pressure-sensitives. Compliance credentials remain critical, with ISO 9001 and ISO 14001 now table stakes and ISO 22000 a must for food-contact orders. Against this backdrop, the industrial labels market size grows through value-added services rather than pure volume, rewarding suppliers that pair technology with regulatory agility.

Industrial Labels Industry Leaders

Avery Dennison Corporation

CCL Industries Inc.

3M Company

Brady Corporation

DuPont de Nemours Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Avery Dennison commissioned a USD 50 million RFID inlay facility in Ho Chi Minh City to supply apparel and footwear brands implementing item-level tracking.

- January 2026: CCL Industries acquired a European pharmaceutical-label converter with EUR 80 million (USD 90 million) revenue, expanding its serialization footprint with three top-10 pharma contracts.

- December 2025: 3M launched a food-contact-safe liner-less adhesive that cuts package waste by 30% and qualifies for EPR fee reductions in Germany and France.

- November 2025: Brady partnered with a blockchain firm to embed cryptographic signatures in RFID tags for cold-chain pharmaceuticals and high-value industrial assets.

Global Industrial Labels Market Report Scope

The Industrial Labels Market Report is Segmented by Raw Material (Polymer/Plastic Labels, Metal Labels, Paper-Based Eco Substrates, Hybrid Laminates and Other Raw Materials), Mechanism (Pressure-Sensitive Labelling, Glue-Applied Labelling, Shrink-Sleeve Labelling, In-Mold and Heat-Transfer Labelling, Liner-Less Labelling), Product Type (Warning/Security Labels, Asset and Inventory Tags, Branding and Promotional Labels, Weather-Proof and Durable Labels, Track-and-Trace (Smart / RFID) Labels), Printing Technology (Analog Printing, Digital Printing, Hybrid Printing, Screen Printing), Identification Technology (Barcode, RFID, NFC, QR and 2-D Codes, Other Identification Technologies), End-User Industry (Food and Beverage, Electronics and Electricals, Automotive and Transportation, Healthcare and Pharmaceuticals, Chemicals and Hazardous Goods, Construction and Heavy Equipment, Logistics and Warehousing, Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Polymer / Plastic Labels |

| Metal Labels |

| Paper-Based Eco Substrates |

| Hybrid Laminates and Other Raw Materials |

| Pressure-Sensitive Labelling |

| Glue-Applied Labelling |

| Shrink-Sleeve Labelling |

| In-Mold and Heat-Transfer Labelling |

| Liner-Less Labelling |

| Warning / Security Labels |

| Asset and Inventory Tags |

| Branding and Promotional Labels |

| Weather-Proof and Durable Labels |

| Track-and-Trace (Smart / RFID) Labels |

| Analog Printing |

| Digital Printing |

| Hybrid Printing |

| Screen Printing |

| Barcode |

| RFID |

| NFC |

| QR and 2-D Codes |

| Other Identification Technologies |

| Food and Beverage |

| Electronics and Electricals |

| Automotive and Transportation |

| Healthcare and Pharmaceuticals |

| Chemicals and Hazardous Goods |

| Construction and Heavy Equipment |

| Logistics and Warehousing |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Raw Material | Polymer / Plastic Labels | ||

| Metal Labels | |||

| Paper-Based Eco Substrates | |||

| Hybrid Laminates and Other Raw Materials | |||

| By Mechanism | Pressure-Sensitive Labelling | ||

| Glue-Applied Labelling | |||

| Shrink-Sleeve Labelling | |||

| In-Mold and Heat-Transfer Labelling | |||

| Liner-Less Labelling | |||

| By Product Type | Warning / Security Labels | ||

| Asset and Inventory Tags | |||

| Branding and Promotional Labels | |||

| Weather-Proof and Durable Labels | |||

| Track-and-Trace (Smart / RFID) Labels | |||

| By Printing Technology | Analog Printing | ||

| Digital Printing | |||

| Hybrid Printing | |||

| Screen Printing | |||

| By Identification Technology | Barcode | ||

| RFID | |||

| NFC | |||

| QR and 2-D Codes | |||

| Other Identification Technologies | |||

| By End-User Industry | Food and Beverage | ||

| Electronics and Electricals | |||

| Automotive and Transportation | |||

| Healthcare and Pharmaceuticals | |||

| Chemicals and Hazardous Goods | |||

| Construction and Heavy Equipment | |||

| Logistics and Warehousing | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the industrial labels market by 2031?

The value is forecast to reach USD 35.42 billion by 2031.

Which raw-material segment is growing fastest within industrial labels?

Paper-based eco substrates are expected to expand at a 5.94% CAGR through 2031.

Why are liner-less labels gaining popularity?

They remove silicone liners, lower waste fees and meet closed-loop recycling targets while maintaining high application speeds.

Which region will add the most incremental sales for label suppliers?

Asia-Pacific is set to post the highest CAGR at 6.19% as manufacturing output grows in China, India and Vietnam.

How do regulatory mandates shape healthcare label demand?

U.S. DSCSA and EU FMD rules require unique identifiers and tamper evidence, driving a 6.73% CAGR for healthcare and pharmaceutical labels.

What competitive edge do hybrid printing presses provide?

They pair low-cost flexographic base layers with inkjet personalization, cutting waste and enabling compliant artwork changes within hours.

Page last updated on: