Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.31 Billion |

| Market Size (2026) | USD 1.36 Billion |

| Market Size (2031) | USD 1.67 Billion |

| Growth Rate (2026 - 2031) | 4.23% CAGR |

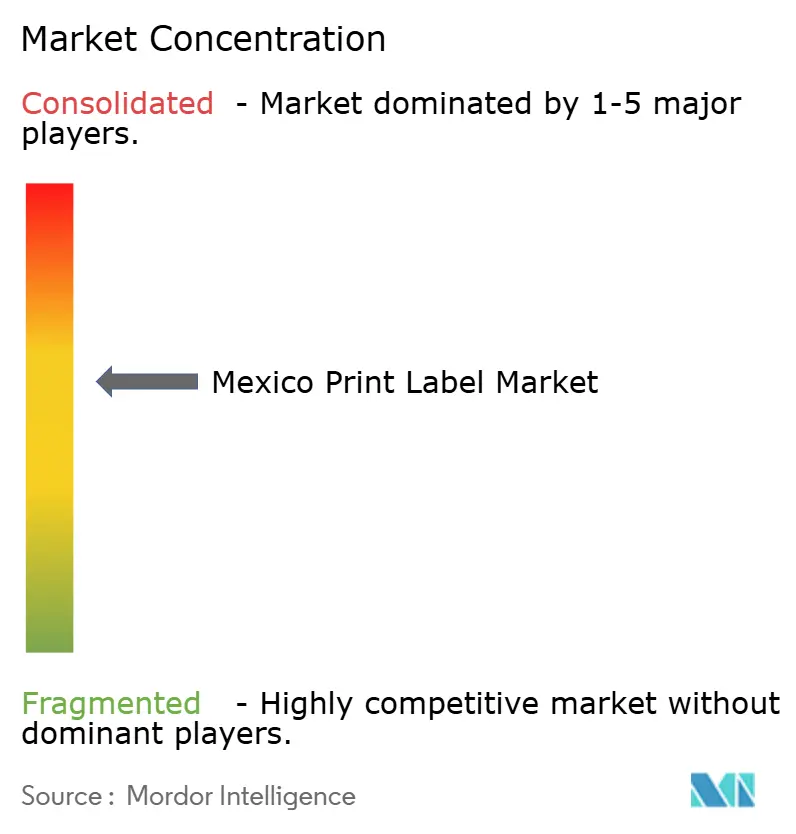

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Print Label Market Analysis by Mordor Intelligence

The Mexico print label market size is projected to expand from USD 1.31 billion in 2025 and USD 1.36 billion in 2026 to USD 1.67 billion by 2031, registering a CAGR of 4.23% between 2026 to 2031. Over the forecast horizon, brand owners that relocated production from Asia to Mexico after the United States-Mexico-Canada Agreement drove incremental label demand that outpaced historical averages. Converter order books lengthened because near-shore factories require replenishment in hours rather than in weeks, which shifted pricing power toward suppliers that operate plants inside major industrial corridors. Rising e-commerce parcel volumes, regulatory mandates for circular packaging, and serialized pharmaceutical track-and-trace labels further expand application breadth, encouraging capital spending on hybrid digital-flexo presses and liner-less converting lines. Competitive intensity remains moderate, yet recent mergers show that scale, software integration, and sustainable substrate portfolios now dictate margin resilience rather than low labor costs.

Key Report Takeaways

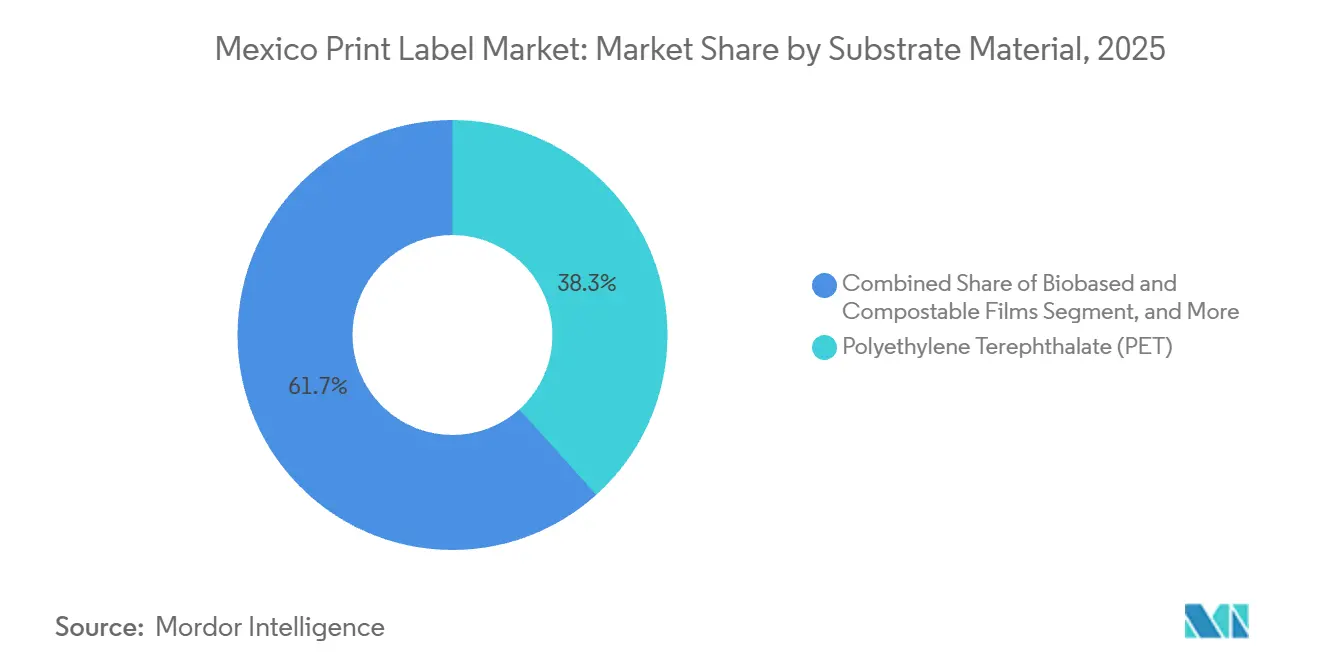

- By substrate material, polyethylene terephthalate captured 38.34% of the Mexico print label market share in 2025, while biobased and compostable films are projected to expand at a 5.68% CAGR through 2031.

- By print technology, flexography held 46.32% market share in 2025, whereas digital printing is forecast to grow at a 5.12% CAGR to 2031.

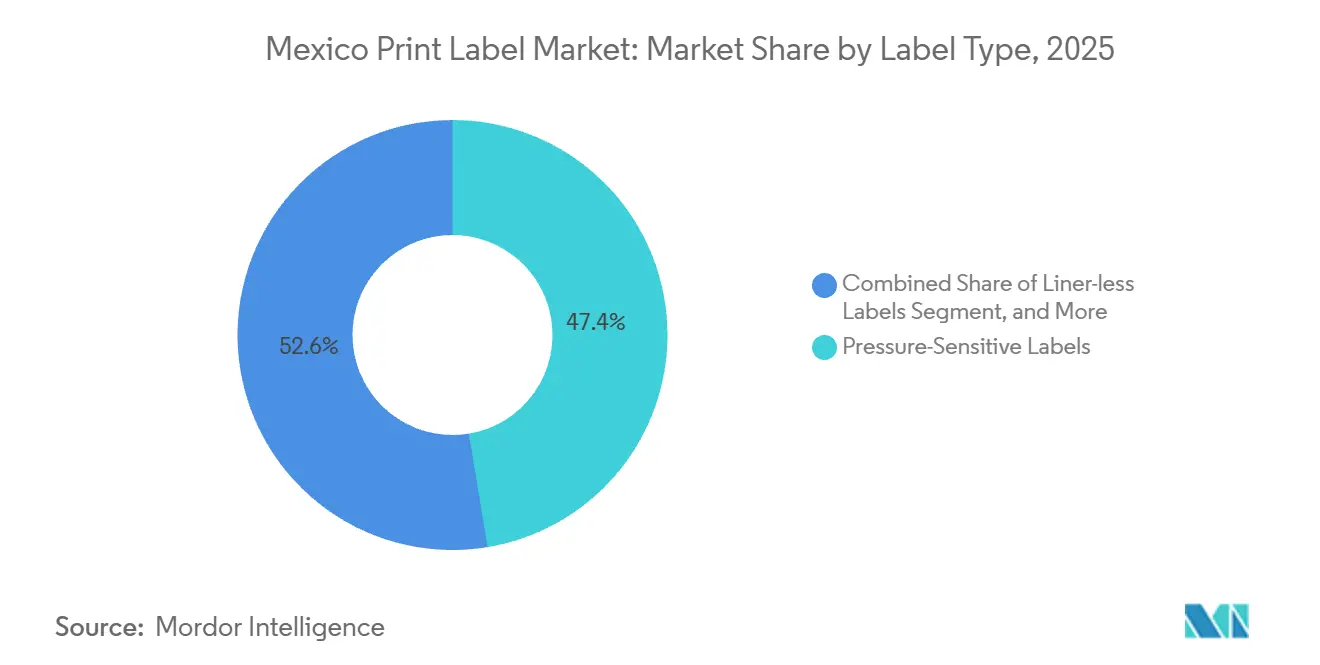

- By label type, pressure-sensitive formats accounted for 47.39% of the Mexico print label market size in 2025, and liner-less labels are expected to advance at a 5.76% CAGR during the outlook period.

- By end-user industry, food applications led with 28.64% share in 2025, while healthcare and pharmaceutical labels are poised to record the fastest 5.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Print Label Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reshoring-Driven Surge in Local Label Demand | +1.2% | National, concentrated in Nuevo León, Guanajuato, Querétaro, Jalisco industrial corridors | Short term (≤ 2 years) |

| Growth of E-Commerce and Logistics Automation | +0.9% | National, with early gains in Mexico City, Monterrey, Guadalajara metropolitan zones | Medium term (2-4 years) |

| Sustainability Mandates Boosting Liner-Less and Wash-Off Labels | +0.8% | National, compliance-driven in export-oriented facilities | Medium term (2-4 years) |

| Expansion of Mexican Craft Beverage Exports | +0.6% | Jalisco, Oaxaca, Guanajuato tequila and mezcal production zones; Baja California craft beer clusters | Long term (≥ 4 years) |

| Smart Labeling and Traceability Regulations | +0.5% | National, pharmaceutical and food sectors under COFEPRIS and Secretaría de Economía oversight | Medium term (2-4 years) |

| Corporate Near-Term CAPEX Incentives (Green Tax Credits) | +0.4% | National, immediate-deduction provisions favor Monterrey, Querétaro, Tijuana manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Reshoring-Driven Surge in Local Label Demand

Multinational manufacturers that transferred final assembly from Asia to Mexico now require label converters located inside the same industrial parks, because just-in-time systems tolerate only a few hours of lead time. Average labor costs of USD 3.50-5.00 per hour in Tijuana, Monterrey, and Hermosillo strengthen the business case for proximity, while tariff-free USMCA access eliminates customs delays.[1]Boston Consulting Group, “The New Economics of Global Manufacturing,” bcg.com Avery Dennison’s USD 100 million RFID plant in Querétaro demonstrates how embedded production, prototyping, and fulfillment converge inside one campus to deliver sub-24-hour replenishment.[2]Avery Dennison, “Avery Dennison Opens World’s Largest RFID Facility in Querétaro, Mexico,” Averydennison.com Brand owners now sign 18- to 24-month contracts instead of multi-year supply agreements, preserving flexibility when footprints shift. Converters that cannot guarantee overnight delivery lose bids even when they offer lower unit prices. As a result, the Mexico print label market rewards geographic density and agile scheduling rather than sheer output tonnage.

Growth of E-Commerce and Logistics Automation

Parcel hubs operated by Amazon and Mercado Libre in Mexico City, Monterrey, and Guadalajara deploy high-speed sortation lines that run at 200 units per minute, which pushes demand toward liner-less and pressure-sensitive labels engineered for automated application. South America’s logistics sector totaled USD 426.2 billion in 2024 and is expanding rapidly, with Mexico capturing an outsized share thanks to cross-border traffic into the United States. Liner-less rolls eliminate silicone-coated waste and lower material usage by 15-20%, giving fulfillment operators both cost and sustainability benefits. Technical specifications around die-cut tolerances and adhesives that perform across humidity swings raise entry barriers for small converters lacking R&D labs. Consequently, the Mexico print label market consolidates e-commerce volume into suppliers that bundle software, printers, and consumables in one contract.

Sustainability Mandates Boosting Liner-Less and Wash-Off Labels

The Circular Economy Law, which took effect in January 2026, obliges producers to register packaging materials, meet recycled-content thresholds, and demonstrate circular design, thereby forcing label redesign for recyclability. Liner-less formats remove non-recyclable release liners, while wash-off adhesives allow PET recyclers to recover clean flake. UPM Raflatac’s Carbon Action portfolio quantifies cradle-to-gate emissions, enabling brand owners to meet Scope 3 targets. Biofase scales 500 tons per month of avocado-seed resin that feeds compostable films, aligning with food-service labels disposed of with organic waste.[3]Biofase, “Sustainable Bioplastics from Avocado Seeds,” biofase.com.mx Converters that invest early capture premium pricing from global brands, whereas laggards risk exclusion from export supply chains once enforcement tightens.

Expansion of Mexican Craft Beverage Exports

Tequila, mezcal, and craft beer rely on labels as brand assets, demanding metallic foils, tactile varnishes, and security holograms that add 15-25% to unit cost. Grupo Flexográfico purchased a Nilpeter FA-17 press to supply 5,000-10,000-lot orders for premium tequila runs. Marbetes and precintos issued by the Consejo Regulador del Tequila embed serialized QR codes that deter counterfeits in export channels. Currency exposure emerges because distillers invoice in U.S. dollars but pay suppliers in pesos, squeezing converter margins when the peso strengthens. Companies that can hedge or invoice in dollars win cross-border contracts, splitting the Mexico print label market along financial-risk capabilities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Petro-Based Film Prices | -0.6% | National, acute in import-dependent converters lacking hedging mechanisms | Short term (≤ 2 years) |

| Shortage of Skilled Flexo and Digital Press Operators | -0.4% | National, concentrated in Monterrey, Guadalajara, Querétaro industrial zones | Medium term (2-4 years) |

| High Upfront Cost of Hybrid Digital Presses | -0.3% | National, capital-access constraints in regional converters | Long term (≥ 4 years) |

| Fragmented Recycling Infrastructure | -0.2% | National, urban-rural disparity in collection and sortation capacity | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Petro-Based Film Prices

Polypropylene and PET film costs track Brent crude with a 60-90-day lag, yet Mexican converters often sign fixed-price contracts that run 12-18 months. When Brent rose 22% in early 2025, film prices jumped 18%, but suppliers passed through only 40% of the spike, eroding gross margins. Limited access to futures markets leaves converters exposed, forcing cuts in R&D and maintenance that eventually impair quality. Multinationals with global purchasing desks hedge exposure, leaving local independents vulnerable and tilting the Mexico print label market toward players with treasury sophistication.

Shortage of Skilled Flexo and Digital Press Operators

The Flexographic Technical Association Mexico certifies fewer than 200 new operators each year, while the industry needs 500-700 to staff expansions.[4]Flexographic Technical Association Mexico, “Certification Programs,” flexography.org Poaching drives 20-30% wage escalation and disrupts smaller converters. Mark Andy partnered with Canvitech in March 2025 to broaden training access, yet coverage remains thin outside main corridors. Consequently, converters with in-house academies maintain uptime and color consistency, whereas under-resourced rivals suffer waste and missed SLAs, ultimately conceding share inside the Mexico print label market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Substrate Material: PET Dominance Meets Biobased Disruption

Polyethylene terephthalate generated 38.34% of market 2025, affirming its clarity, barrier strength, and compatibility with high-speed applicators that underpin the Mexico print label market share leadership in beverages and personal care. Cost-per-square-meter and robust supply chains keep PET the baseline choice even as resin volatility rises. The Mexico print label market size derived from biobased and compostable films is projected to grow fastest at a 5.68% CAGR, because retailer scorecards and corporate net-zero pledges favor substrates that support circular claims. Biofase supplies 500 tons per month of avocado-seed resin for compostable films, and Innovia Films upgraded its Zacapú coating line to boost oxygen and moisture barriers, positioning biobased stocks for mainstream adoption.

The strategic dilemma centers on economics. Biobased webs command 30-50% premiums over petro-based equivalents, limiting uptake to premium SKUs or export packs facing strict environmental audits. Converters that scale early build process know-how and secure feedstock under long-term agreements, lowering future conversion costs. Should regulators impose minimum biocontent thresholds by 2028, installed capacity on compostable lines will convert into defensible advantage across the Mexico print label market.

By Print Technology: Hybrid Digital Systems Narrow Flexo’s Lead

Flexography accounted for 46.32% of market share in 2025, due to superior cost efficiency on runs exceeding 10,000 linear meters and steady gains in water-based ink performance. However, digital engines are forecast to advance at 5.12% per year as marketing teams demand late-stage artwork changes, serialized codes, and regional promotions. Labelexpo Mexico 2025 showcased HP Indigo, Durst, and Xeikon units capable of 80 m per minute, demonstrating that print quality gaps with offset have closed at typical viewing distances. The Mexico print label market, tied to digital output, is expanding as pharmaceutical and craft-beverage customers value versioning over unit cost.

Hybrid configurations that embed UV-inkjet heads into servo-driven flexo frames enable converters to toggle between digital and analog lanes in a single pass, capturing both scale and personalization margins. Although sticker prices range from USD 1.2-2.5 million, Plan Mexico depreciation incentives shorten paybacks and unlock financing. Converters lacking capital risk relegation to commodity SKUs, shrinking relevance inside the Mexico print label market.

By Label Type: Pressure-Sensitive Leadership Faces Liner-Less Challenge

Pressure-sensitive constructions accounted for 47.39% of the market share in 2025, spanning the food, logistics, and personal-care segments, as peel-and-stick convenience matches automated application speeds. Liner-less alternatives, supported by the Circular Economy Law, are projected to rise 5.76% annually, outpacing all other forms. E-commerce fulfillment lines value the 15-20% material reduction and 40% faster application that liner-less rolls enable. Shrink sleeves and in-mold labels retain strongholds where 360-degree graphics or high chemical resistance are vital.

Adoption hinges on adhesive chemistry. Liner-less stocks require formulas that remain tacky yet avoid ooze or blocking, constraining supply to a handful of multinational substrate makers. Early movers that master coating and slitting specifications secure multi-year contracts with parcel carriers and third-party logistics firms. The Mexico print label market, therefore, rewards converters that integrate applicator retrofits with consumables, transferring switching costs from the brand owner to the converter.

By End-User Industry: Healthcare Outpaces Food’s Volume Base

Food labels captured 28.64% of market share in 2025 because NOM-051 octagon warnings forced redesigns across snack, dairy, and beverage lines. Yet, healthcare and pharmaceutical demand is set to log a 5.41% CAGR from 2026-2031 as COFEPRIS serialization moves from pilot to full enforcement. The Mexico print label market size related to serialized vials, blister packs, and medical devices expands faster than grocery staples because regulation, rather than consumption, drives turnover.

Pharma lines require ISO 13485 clean-room environments, vision-system verification, and integration with enterprise resource planning for real-time data capture. Converters that invested in compliant clean rooms and validation protocols already quote 20-30% pricing premiums, shielding margins from resin volatility. Food converters with basic GMP credentials face steep CapEx to pivot, prompting joint-venture discussions with multinational label groups that seek rapid market entry.

Geography Analysis

Central and northern industrial corridors anchor activity inside the Mexico print label market, with Monterrey, Guadalajara, Querétaro, and Guanajuato accounting for the majority of installed converting horsepower. Monterrey hosts Avery Dennison’s RFID campus, Oben Group’s new BOPP line, and multiple medicine-pack contract manufacturers, generating steady demand that keeps machine utilization above 80%. Guadalajara leverages consumer-electronics clusters and proximity to tequila heartlands, drawing craft-beverage converters who value quick truck runs to bottling plants.

Querétaro and Guanajuato benefit from aerospace and automotive OEMs that mandate just-in-sequence label deliveries at hourly cadences, reinforcing the need for converters within 50 km of assembly sites. Mexico City and Estado de México add volume through consumer-goods factories and the nation’s largest e-commerce fulfillment centers, both of which intensify demand for pressure-sensitive and liner-less labels. Border cities such as Tijuana and Ciudad Juárez handle medical-device labeling destined for the U.S. market, leveraging FDA familiarization to command price premiums in the Mexico print label market.

Emerging secondary hubs include Puebla and San Luis Potosí, where new EV and aerospace investments call for specialty labeling in high-temperature and chemical-resistant formats. Infrastructure shortfalls in Oaxaca and Chiapas limit scalability despite buoyant mezcal growth, as substrate trucks face long transit times and intermittent power supply. Converters with binational footprints, notably AGH Labels and Valley, run plants on both sides of the frontier to synchronize cross-border replenishment, a capability increasingly requested by multinational brand owners.

Competitive Landscape

The Mexico print label market sits in a mid-concentration tier where the top five multinational converters, Avery Dennison, CCL Industries, UPM Raflatac, Multi-Color Corporation, and Amcor, dominate high-value niches such as RFID, security holograms, and pharmaceutical serialization. Regional family-owned firms, including Papeles y Conversiones de México, AGH Labels, Grupo Sigma Q, and Grupo Flexográfico, chase volume work by leveraging proximity, bilingual service, and quick changeovers. Recent M&A Multi-Color’s purchase of Eximpro and ProMach’s takeover of Etiflex signals that scale and proprietary software are now prerequisites for sustainable margins.

Technology investments create a widening gap. Avery Dennison’s USD 100 million RFID campus in Querétaro elevates label functionality from static identification to data infrastructure. Converters installing hybrid presses and LED-UV curing systems lock in craft-beverage and cosmetics business that values tactile and variable-data effects. Firms that rely solely on legacy flexo presses struggle to match color consistency at fast turnaround, pushing them toward commoditized food applications with thin spreads.

Financing capacity divides the field further. Plan Mexico tax incentives favor entities that can front large checks and document structured training, effectively handing a subsidy to well-capitalized multinationals. Local independents unable to access low-cost credit become acquisition targets or retreat to niche jobs. Over the outlook period, competitive dynamics in the Mexico print label market will depend less on labor cost and more on the ability to integrate software, smart substrates, and circular-economy compliance into a single value proposition.

Mexico Print Label Industry Leaders

Avery Dennison Corporation

CCL Industries Inc.

Amcor plc

UPM Raflatac Oy

Brady Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Mexico’s Circular Economy Law entered force, obliging extended producer responsibility registries and recycled-content thresholds for all packaging and labels.

- December 2025: Secretaría de Economía released PROY-NOM-051-SE/SSA1-2025, proposing additional front-of-pack modifications that extend redesign cycles to 2027.

- August 2025: Grupo Corporativo Papelera committed MXN 1,700 million (USD 95 million) toward sustainable packaging and labeling capacity upgrades.

- July 2025: SIG Combibloc injected USD 35 million into its Querétaro plant to add aseptic carton and labeling lines.

Mexico Print Label Market Report Scope

The print label is a piece of paper, plastic film, cloth, metal, or other material affixed to a container or product with printed information or symbols about the product or item. Information may also be printed directly on a container or article.

The Mexico Print Label Market Report is Segmented by Substrate Material (Paper and Paperboard, PET, PP and BOPP, PVC, Biobased and Compostable Films, and Other Substrate Materials), Print Technology (Offset, Flexography, Screen, Digital Printing, and Other Technologies), Label Type (Wet-glued, Pressure-Sensitive, Liner-less, In-mold, Shrink Sleeve, and Other Label Types), End-user Industry (Food, Beverage, Healthcare and Pharmaceutical, Cosmetics and Personal Care, Industrial, and Other End-users). The Market Forecasts are Provided in Terms of Value (USD).

By Substrate Material

| Paper and Paperboard |

| Polyethylene Terephthalate (PET) |

| Polypropylene (PP and BOPP) |

| Polyvinyl Chloride (PVC) |

| Biobased and Compostable Films |

| Other Substrate Materials |

By Print Technology

| Offset |

| Flexography |

| Screen |

| Digital Printing |

| Other Print Technologies |

By Label Type

| Wet-glued Labels |

| Pressure-Sensitive Labels |

| Liner-less Labels |

| In-mold Labels |

| Shrink Sleeve Labels |

| Other Label Types |

By End-user Industry

| Food |

| Beverage |

| Healthcare and Pharmaceutical |

| Cosmetics and Personal Care |

| Industrial |

| Other End-user Industries |

| By Substrate Material | Paper and Paperboard |

| Polyethylene Terephthalate (PET) | |

| Polypropylene (PP and BOPP) | |

| Polyvinyl Chloride (PVC) | |

| Biobased and Compostable Films | |

| Other Substrate Materials | |

| By Print Technology | Offset |

| Flexography | |

| Screen | |

| Digital Printing | |

| Other Print Technologies | |

| By Label Type | Wet-glued Labels |

| Pressure-Sensitive Labels | |

| Liner-less Labels | |

| In-mold Labels | |

| Shrink Sleeve Labels | |

| Other Label Types | |

| By End-user Industry | Food |

| Beverage | |

| Healthcare and Pharmaceutical | |

| Cosmetics and Personal Care | |

| Industrial | |

| Other End-user Industries |

Key Questions Answered in the Report

How large will the Mexico print label market be by 2031?

It is forecast to reach USD 1.67 billion by 2031, expanding at a 4.23% CAGR between 2026 and 2031.

Which substrate grows fastest inside Mexican label converting?

Biobased and compostable films are projected to post a 5.68% CAGR through 2031, outpacing petro-based options.

Why are liner-less labels gaining ground in Mexico?

Fulfillment centers favor their 15-20% material savings and 40% faster application speeds, while the Circular Economy Law penalizes waste-generating liners.

What makes healthcare labeling attractive for converters?

COFEPRIS serialization rules and near-shored pharmaceutical plants create steady demand for high-margin variable-data and RFID-enabled labels.

How do Plan Mexico tax incentives influence press investments?

Immediate depreciation plus a 25% training deduction shorten paybacks by roughly 15-20%, encouraging hybrid digital-flexo press adoption.

Which regions offer the strongest growth prospects for converters?

Industrial corridors in Monterrey, Guadalajara, Querétaro, and Guanajuato lead demand thanks to automotive, aerospace, and e-commerce expansions.

Page last updated on: