USB Flash Drive Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.35 Billion |

| Market Size (2031) | USD 8.77 Billion |

| Growth Rate (2026 - 2031) | 6.66% CAGR |

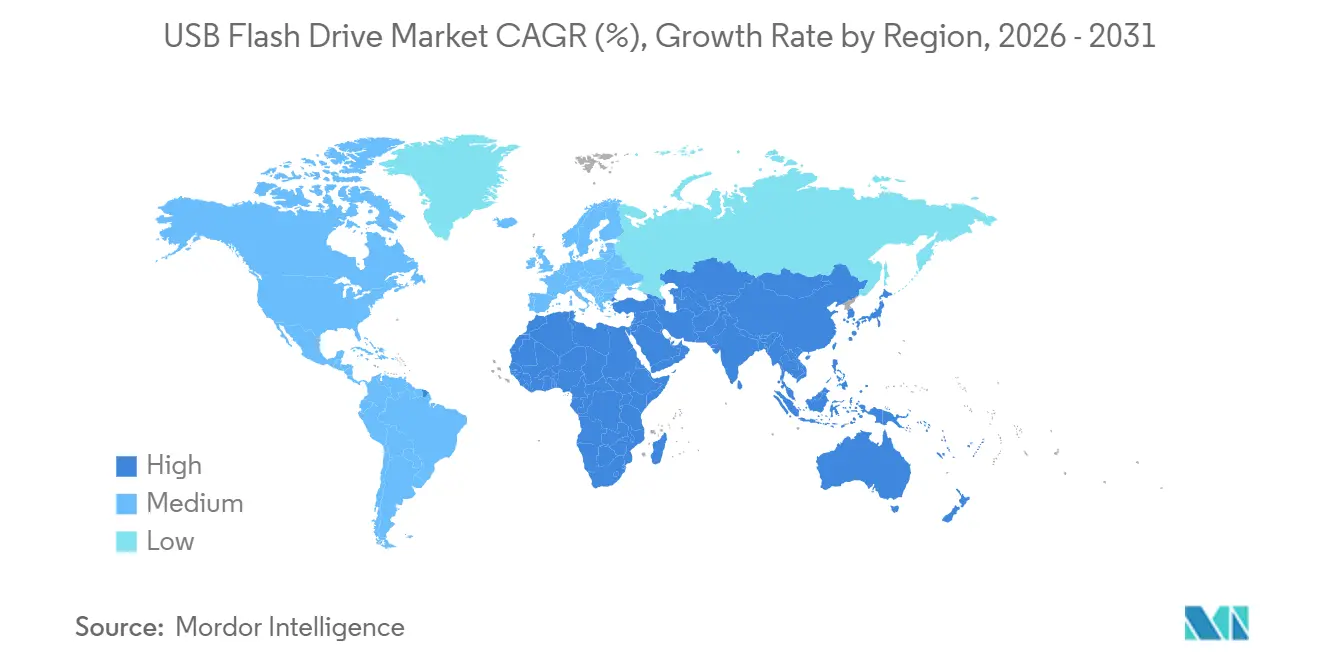

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

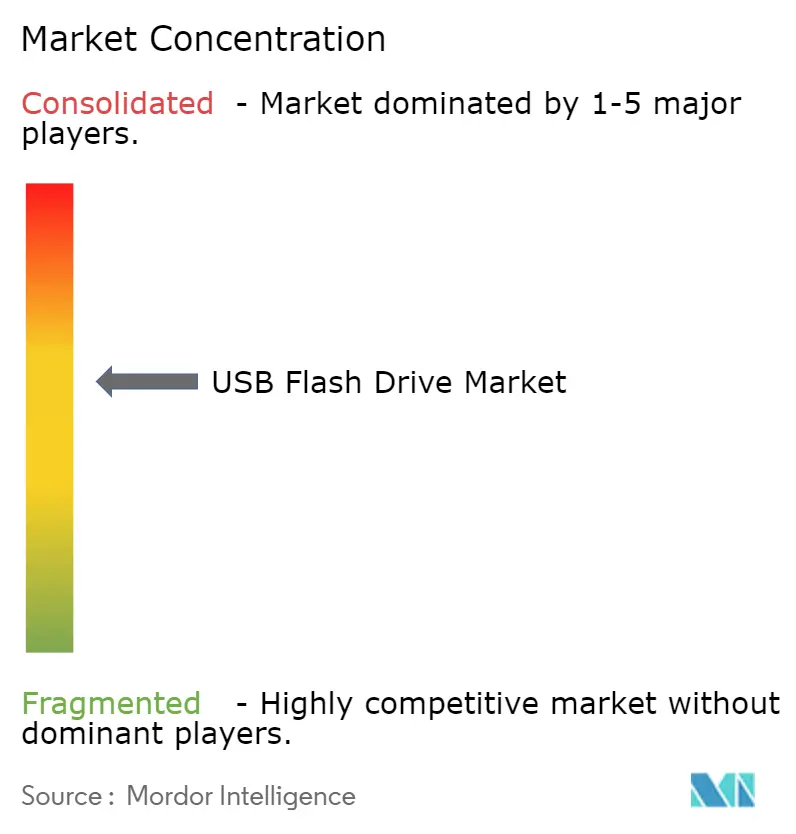

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

USB Flash Drive Market Analysis by Mordor Intelligence

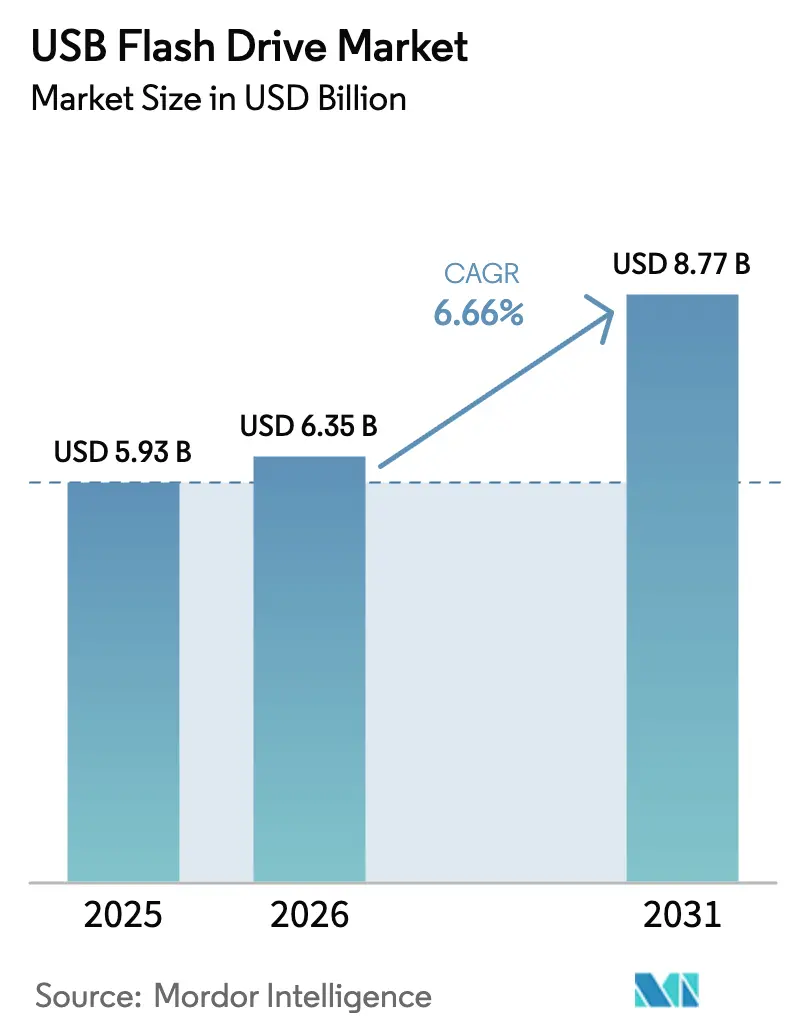

The USB Flash Drive Market size is projected to be USD 5.93 billion in 2025, USD 6.35 billion in 2026, and reach USD 8.77 billion by 2031, growing at a CAGR of 6.66% from 2026 to 2031.

This growth balances rising demand for secure, high-capacity offline storage and the substitution threat from cloud services. The 64-128 GB capacity tier remained the revenue leader in 2025, yet the 256 GB and above tier is expanding fastest as enterprises consolidate multiple drives into single high-capacity devices. Rapid Type-C adoption following the European Union common-charger directive, India’s parallel standards, and California’s Assembly Bill 1587 accelerates refresh cycles, while NAND cost declines sustain affordable terabyte-class offerings. Competitive intensity stays moderate because vertically integrated NAND players hold fabrication advantages, although Chinese controller suppliers improve yields and widen component availability.

Key Report Takeaways

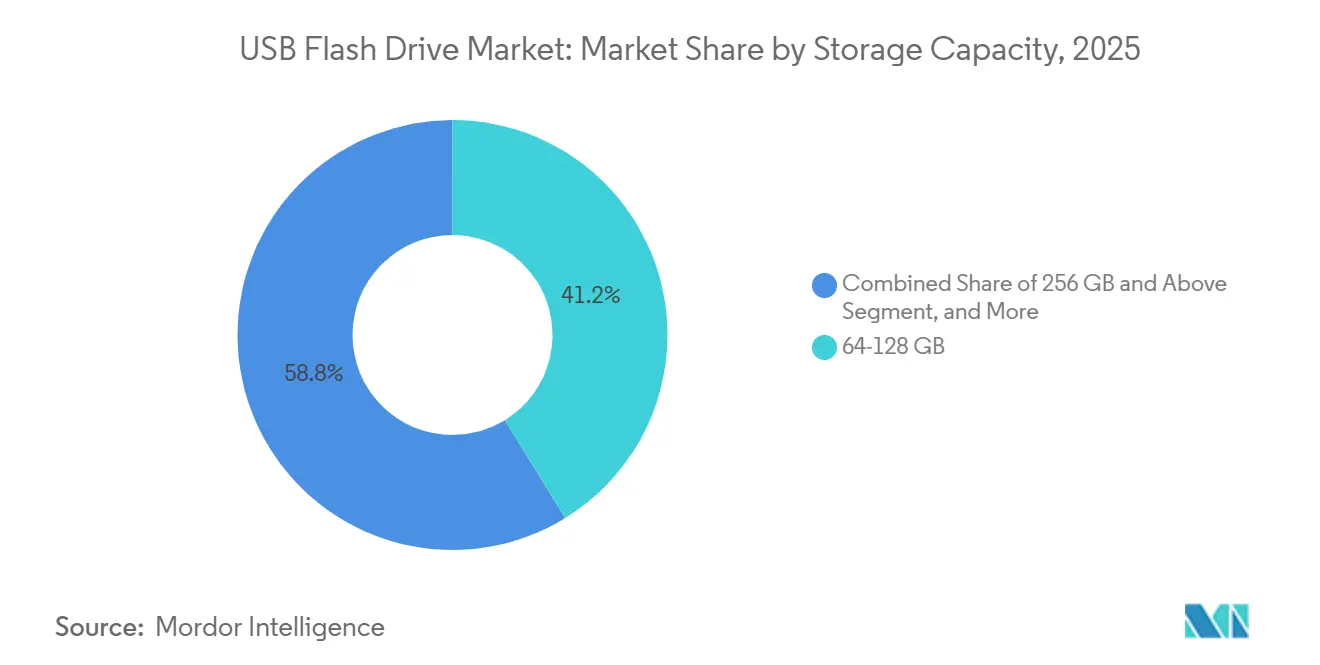

- By storage capacity, 64-128 GB led with 41.22% revenue share in 2025; the 256 GB and above tier is forecast to expand at 7.78% CAGR to 2031.

- By interface, USB 3.0 captured 46.74% revenue share in 2025, while USB Type-C products are expected to post a 7.01% CAGR through 2031.

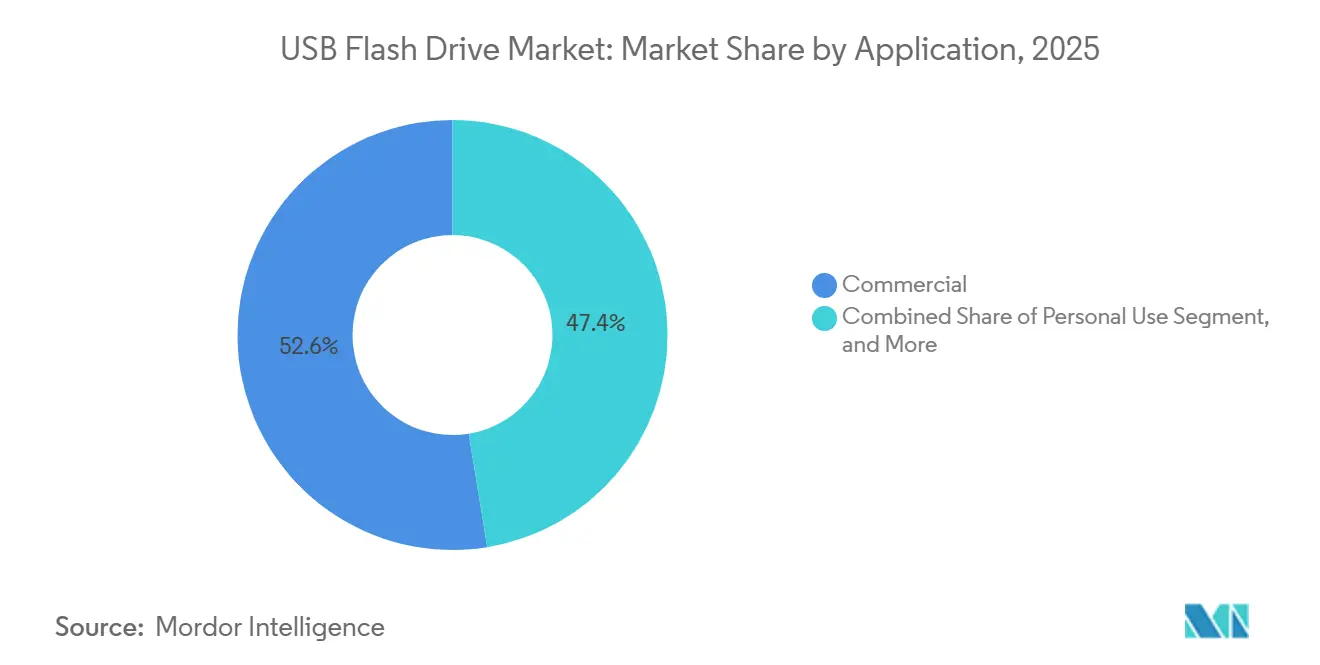

- By application, commercial procurement accounted for 52.58% of demand in 2025, whereas consumer use is projected to record a 7.55% CAGR to 2031.

- By distribution channel, offline retail held 57.37% of sales in 2025; online retail is estimated to grow at 7.61% CAGR over the period.

- By geography, Asia Pacific commanded 38.46% of 2025 revenue, and the Middle East and Africa region is set to register a 6.97% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global USB Flash Drive Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Demand for High-Capacity Portable Storage | +1.20% | Global, with concentration in North America and Asia Pacific | Medium term (2-4 years) |

| Rapid Adoption of USB 3.x and Type-C Interfaces | +1.40% | Global, led by Europe and North America | Short term (≤ 2 years) |

| Growing Enterprise Need for Secure Offline Data Transfer | +1.10% | North America, Europe, GCC | Medium term (2-4 years) |

| Declining Cost per Gigabyte of NAND Flash | +0.90% | Global | Long term (≥ 4 years) |

| Mandates for USB-C Standardization Fueling Replacement Cycles | +1.30% | Europe, India, California | Short term (≤ 2 years) |

| Edge-Device Firmware Flashing Demand in IoT Manufacturing | +0.80% | Asia Pacific core, spill-over to North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for High-Capacity Portable Storage

Enterprise and government buyers are shifting to 256 GB and larger drives to cut physical inventory and simplify chain-of-custody audits for sensitive files. DataLocker’s Sentry 5, listed at USD 422.99 for 256 GB, illustrates how hardware encryption paired with remote-wipe functions commands premium pricing that satisfies NIST SP 800-171r3 rules.[1]National Institute of Standards and Technology, “Special Publication 800-171 Revision 3,” nist.gov Commodity pricing dynamics support the trend: leading Chinese wholesalers offered 256 GB units between USD 30 and USD 50 in 2025, enabling prosumer adoption for 4K footage transfers in bandwidth-limited settings. Micron’s G8 and G9 nodes pushed wholesale cost below USD 0.10 per gigabyte, removing historical price barriers.[2]Micron Technology, “Form 10-K Fiscal Year 2024,” micron.com

Rapid Adoption of USB 3.x and Type-C Interfaces

The European Union directive that took effect in December 2024 mandates USB Type-C ports on smartphones, tablets, and cameras, with laptop compliance required by April 2026.[3]European Commission, “Directive (EU) 2024/1972 on the Common Charger,” europa.eu Complementary regulations from India’s standards body and California’s legislature synchronize a global replacement cycle. SanDisk credited Type-C refreshes for a 27% year-over-year rise in Q1 FY-2026 consumer revenue to USD 652 million. USB 3.2 Gen 2x1 offers 10 Gbps throughput, and benchmark data show fanxiang’s FF951 512 GB drive sustaining 2,088 MB/s reads, matching entry-level NVMe performance at lower cost.

Growing Enterprise Need for Secure Offline Data Transfer

Zero-trust frameworks and air-gapped networks in defense, healthcare, and finance elevate demand for FIPS 140-3 Level 3 products. Kingston’s IronKey D500S, validated in July 2025, meets Trade Agreements Act rules and commands USD 422.99 for 256 GB, proving that certified security offsets commodity price pressure. ISO/IEC 27040:2024 aligns global procurement standards with U.S. requirements, broadening the addressable market for encrypted drives.

Declining Cost per Gigabyte of NAND Flash

Layer-count expansion beyond 200 stacks and QLC technology drop cost curves faster than historical trends. SanDisk’s BiCS8 reached 218 layers and 30% higher bit density by early 2026, allowing 1 TB drives in thumb-sized enclosures without proportional cost increases. China’s Yangtze Memory Technologies Corporation added fresh capacity at the 128-layer node, sustaining downward price momentum even after temporary 2025 supply cuts by Korean competitors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Cloud Storage Substitution | -0.70% | Global, most acute in North America and Europe | Long term (≥ 4 years) |

| Shift Toward Mobile Devices Without USB-A Ports | -0.50% | Global, led by premium smartphone segments | Medium term (2-4 years) |

| EU Right-to-Repair Rules Extending Device Lifecycles | -0.30% | Europe | Long term (≥ 4 years) |

| Foundry Allocation to AI Chips Creating USB Controller Shortages | -0.60% | Global, supply-chain stress in Asia Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating Cloud Storage Substitution

Mainstream adoption of iCloud, Google Drive, and Microsoft OneDrive gradually erodes physical drive usage for daily file transfers. Mobile-memory shipments declined at a -6.0% CAGR from 2020 to 2024, with further contraction forecast through 2029. Internal smartphone capacities of 256 GB and above, plus widespread 5G, reduce consumer reliance on external flash in North America and Europe. The restraint remains less acute in Asia Pacific and the Middle East, where intermittent connectivity and sovereign-data mandates favour offline media.

Foundry Allocation to AI Chips Creating USB Controller Shortages

TSMC reported in November 2025 that advanced-node capacity lags AI-accelerator demand by a factor of three, extending lead times for 28-nm and 16-nm USB controller wafers. Brands without long-term wafer agreements face rising spot prices and delayed Type-C product launches, temporarily slowing interface migration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Storage Capacity: Enterprise Consolidation Drives Terabyte Adoption

The 64-128 GB tier captured 41.22% revenue in 2025, reflecting bulk provisioning by Chinese corporate IT departments for standardized employee kits. Yet the 256 GB and above slice, which commands the quickest 7.78% CAGR, is forecast to lift the USB Flash Drive market size. Declining NAND cost and QLC advances underpin the shift, while security-conscious agencies favour encrypted 256 GB drives priced well above commodity equivalents.

Enterprises consolidate software updates, diagnostic logs, and video capture workflows into single terabyte-class drives to trim physical inventory and shipping overhead. Kingston’s DataTraveler Max 1 TB demonstrates a marketed throughput of 1,000 MB/s, confirming that modern controllers remove the former trade-off between speed and capacity. Premium products like DataLocker’s Sentry 5 capture margins through FIPS-certified encryption, isolating the segment from cut-throat pricing in smaller capacities.

By Interface: Type-C Mandates Accelerate Legacy Displacement

USB 3.0 retained the leading 46.74% revenue share in 2025 owing to the installed base of USB-A ports, but regulatory and OEM shifts are steering buyers toward Type-C. The interface segment’s 7.01% forecast CAGR positions Type-C to overtake USB 3.0 by the decade’s end.

OEM laptop portfolios from Apple, Dell, and Lenovo transitioned premium models to Type-C-only configurations, while the EU directive enforces mass-market compliance. Dual-connector designs like Lexar’s D40E bridge ecosystems during migration, although their higher bill-of-materials narrows margin. The USB4 specification extends headroom to 40 Gbps, future-proofing creative-professional purchases and nudging legacy users toward upgrades.

By Application: Consumer Segment Gains as Dual-Interface Drives Enable Cross-Device Workflows

Commercial procurement dominated with 52.58% of 2025 revenue, but the consumer slice’s 7.55% CAGR will gradually rebalance the USB Flash Drive market share between segments. Viral adoption of dual-interface drives for smartphone-to-desktop transfers supports household demand even as cloud services mature.

Defense and healthcare buyers still anchor commercial volume through encrypted models that meet FIPS 140-3 and ISO/IEC 27040:2024. Meanwhile, education authorities purchase standardized 32 GB and 64 GB units for student assignments, confirming that low-capacity drives retain niche relevance. Ruggedized models rated for -40 °C to 85 °C extend USB Flash Drive market utilization into automotive OBD data logging and industrial IoT gateways.

By Distribution Channel: E-Commerce Platforms Undercut Retail Margins with Bulk Pricing

Offline retail held 57.37% of shipments in 2025 because consumers value immediate ownership and visible packaging. However, online storefronts are tracking a 7.61% CAGR, and their growing weight could push the USB Flash Drive market size attributable to e-commerce.

Amazon sales analytics indicate that Lexar’s D40E achieved 17,137 average monthly units at USD 23.84, spotlighting price-transparent marketplaces that erode brick-and-mortar margins. Alibaba’s wholesale portal empowers small businesses to bypass distributors and source promotional drives from Chinese ODMs at sub-USD 5 prices for 32 GB models, challenging traditional channel economics.

Geography Analysis

Asia Pacific contributed 38.46% of 2025 revenue and anchors manufacturing with China’s NAND assembly and India’s Digital India mandate for offline government backups. Controller independence advances as Huada Semiconductor’s HC31 reaches 98% yield, lessening exposure to Taiwan foundry risk. India’s data-center boom paradoxically sustains offline storage demand because hybrid-cloud controls enforce air-gap backups.

North America and Europe exhibit replacement-cycle driven demand, with security upgrades and Type-C mandates offset by cloud substitution. The EU Right-to-Repair directive could lengthen device lifespans, modestly tempering volume growth while shifting value toward premium, longer-lasting models. Regulatory convergence around storage security elevates FIPS-certified vendors in U.S. federal and NATO procurement.

The Middle East and Africa region shows the fastest 6.97% CAGR, helped by GCC sovereign-data policies and investments in e-commerce logistics. Africa’s connectivity gaps preserve physical media relevance for educational content. South America remains price-sensitive; currency volatility limits adoption of terabyte-class or encrypted offerings, keeping value oriented toward 32 GB and 64 GB lines. Russia sustains local assembly using Chinese NAND to comply with data-localization laws.

Competitive Landscape

The USB Flash Drive market features moderate concentration: Samsung, Micron, and SanDisk collectively own roughly 40% through vertical control of NAND fabrication and branded distribution. SanDisk’s spin-off in February 2025 allows tighter R&D focus on BiCS8 yield, already representing 15% of bit output by early 2026. Kingston leverages the IronKey line to dominate certified secure drives, emphasizing FIPS 140-3 compliance to defend margins in federal contracts.

Chinese challengers such as Netac and fanxiang use domestically sourced HC31 controllers to launch >2 GB/s offerings at entry-level SSD prices, eroding incumbents’ speed advantage. Online-first brands employ aggressive Amazon pricing to bypass retail mark-ups, stimulating intense price competition in North America and Europe. Supply-chain risk arises from AI-chip-related foundry shortages; incumbents with captive fabs or pre-booked wafer supply will preserve volume, while fabless brands face allocation uncertainty.

Patents concentrate on thermal throttling countermeasures and firmware-over-USB update protocols standardized in RFC 9019, ensuring resilience against supply-chain firmware attacks. Automotive-grade vendors such as BYD carve defensible niches in extreme-temperature modules, a space underserved by consumer-electronics giants.

USB Flash Drive Industry Leaders

SanDisk LLC (Western Digital)

Kingston Technology Corporation

Transcend Information, Inc

Samsung Electronics

PNY Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: SanDisk released the T7 Resurrected Portable SSD line (1-4 TB, USB Type-C, recycled aluminium), aligning with EU Ecodesign targets.

- November 2025: Kingston introduced Dual Portable SSD (1050 MB/s, dual USB-A and USB-C) to ease legacy-to-Type-C transition.

- July 2025: Kingston unveiled IronKey D500S, the first FIPS 140-3 Level 3 flash drive, priced USD 422.99 for 256 GB.

- March 2025: DataLocker launched Sentry ONE, a FIPS 140-2 Level 3 encrypted drive with remote wipe.

Global USB Flash Drive Market Report Scope

A USB flash drive is a small, portable data storage device that uses flash memory to store and transfer files. It is connected to computers and other devices via a USB port, enabling quick and convenient access to data. Available in various storage capacities, USB flash drives are widely used for personal, professional, and industrial applications. They are reliable, durable, and reusable, making them ideal for file sharing, backups, and data portability tasks.

The study tracks the revenue generated from the sale of USB flash drives by various manufacturers worldwide. It also tracks the key market parameters, underlying growth influencers, and major manufacturers operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The USB Flash Drive Market Report is Segmented by Storage Capacity (8 GB and Below, 16 GB, 32 GB, 64-128 GB, 256 GB and Above), Interface (USB 2.0, USB 3.0, USB 3.1/USB 3.2, USB Type-C, USB4), Application (Personal Use, Enterprise/Commercial, Government and Military, Education and Public Sector, Other Applications), Distribution Channel (Offline Retail, Online Retail, B2B/OEM Supply, Institutional Procurement), and Geography (North America, South America, Europe, Asia Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| 8 GB and Below |

| 16 GB |

| 32 GB |

| 64 - 128 GB |

| 256 GB and Above |

| USB 2.0 |

| USB 3.0 |

| USB 3.1 / USB 3.2 |

| USB Type-C |

| USB4 |

| Personal Use |

| Enterprise / Commercial |

| Government and Military |

| Education and Public Sector |

| Other Applications |

| Offline Retail |

| Online Retail |

| B2B / OEM Supply |

| Institutional Procurement |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN | |

| Australia and New Zealand | |

| Middle East | GCC |

| Turkey | |

| Israel | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Storage Capacity | 8 GB and Below | |

| 16 GB | ||

| 32 GB | ||

| 64 - 128 GB | ||

| 256 GB and Above | ||

| By Interface | USB 2.0 | |

| USB 3.0 | ||

| USB 3.1 / USB 3.2 | ||

| USB Type-C | ||

| USB4 | ||

| By Application | Personal Use | |

| Enterprise / Commercial | ||

| Government and Military | ||

| Education and Public Sector | ||

| Other Applications | ||

| By Distribution Channel | Offline Retail | |

| Online Retail | ||

| B2B / OEM Supply | ||

| Institutional Procurement | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Australia and New Zealand | ||

| Middle East | GCC | |

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the expected value of global USB Flash Drive sales in 2031?

The USB Flash Drive market size is projected to reach USD 8.77 billion by 2031.

Which capacity tier is growing fastest?

Drives of 256 GB and above are advancing at a 7.78% CAGR through 2031.

How will the EU common-charger directive impact demand?

Mandatory USB Type-C ports drive refresh cycles, lifting Type-C flash drive shipments at a 7.01% CAGR.

Why are encrypted drives gaining share?

FIPS 140-3 and ISO/IEC 27040 requirements in defense and finance favor certified products, supporting premium pricing.

What is the outlook for online retail channels?

E-commerce revenue is forecast to grow at 7.61% CAGR as bulk pricing and next-day delivery undercut traditional stores.

How does AI chip demand affect USB controller supply?

Foundry prioritization of AI accelerators extends USB controller lead times, creating short-term shortages for Type-C drives.

Page last updated on: