Microdisplay Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

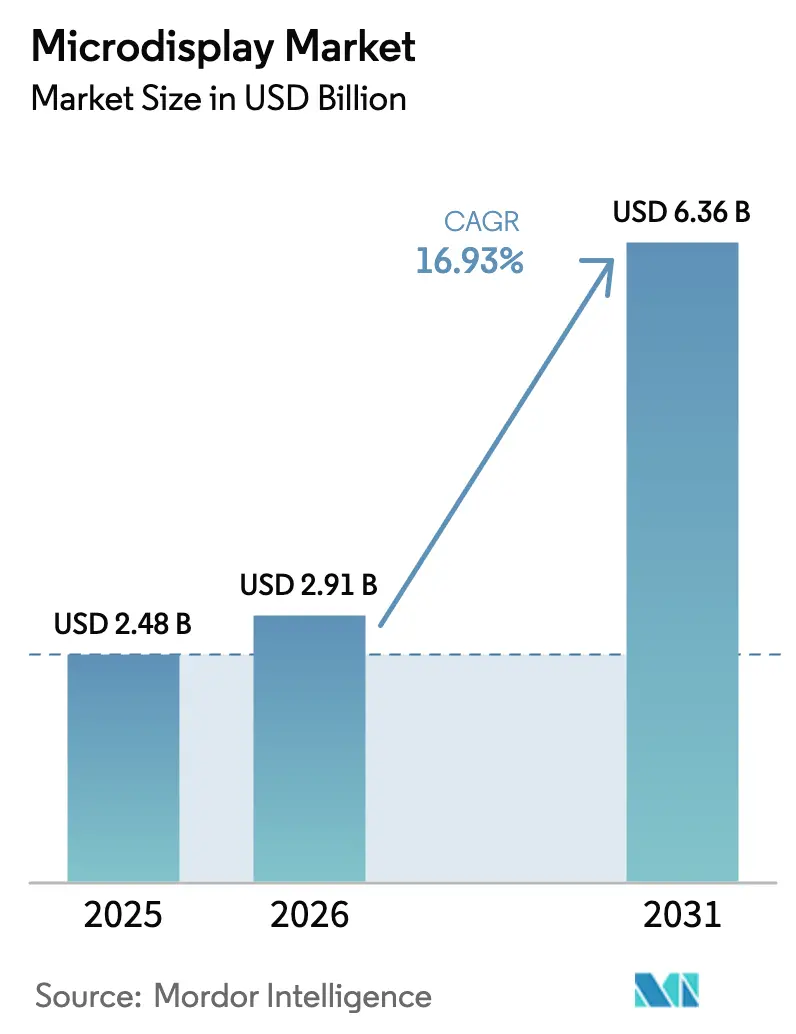

| Market Size (2026) | USD 2.91 Billion |

| Market Size (2031) | USD 6.36 Billion |

| Growth Rate (2026 - 2031) | 16.93% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Microdisplay Market Analysis by Mordor Intelligence

The microdisplay market size is projected to expand from USD 2.48 billion in 2025 and USD 2.91 billion in 2026 to USD 6.36 billion by 2031, registering a 16.93% CAGR between 2026 to 2031. Rising demand for lightweight augmented-reality and virtual-reality headsets, transparent automotive head-up displays, and defense visor systems is reshaping product roadmaps toward pixel densities above 3,000 ppi and brightness levels higher than 5,000 nits. Mini-fab outsourcing is compressing unit costs for camera electronic viewfinders, while Asian panel makers are scaling OLED-on-silicon and microLED capacity at 8-inch and 12-inch wafer nodes. Big-tech alliances are adding volume visibility that de-risks capital spending, and regulatory frameworks such as Euro NCAP visualization protocols are pulling the microdisplay market toward automotive-grade qualification. Supply-chain challenges around sapphire substrates and silicon backplanes, however, continue to pressure gross margins.

Key Report Takeaways

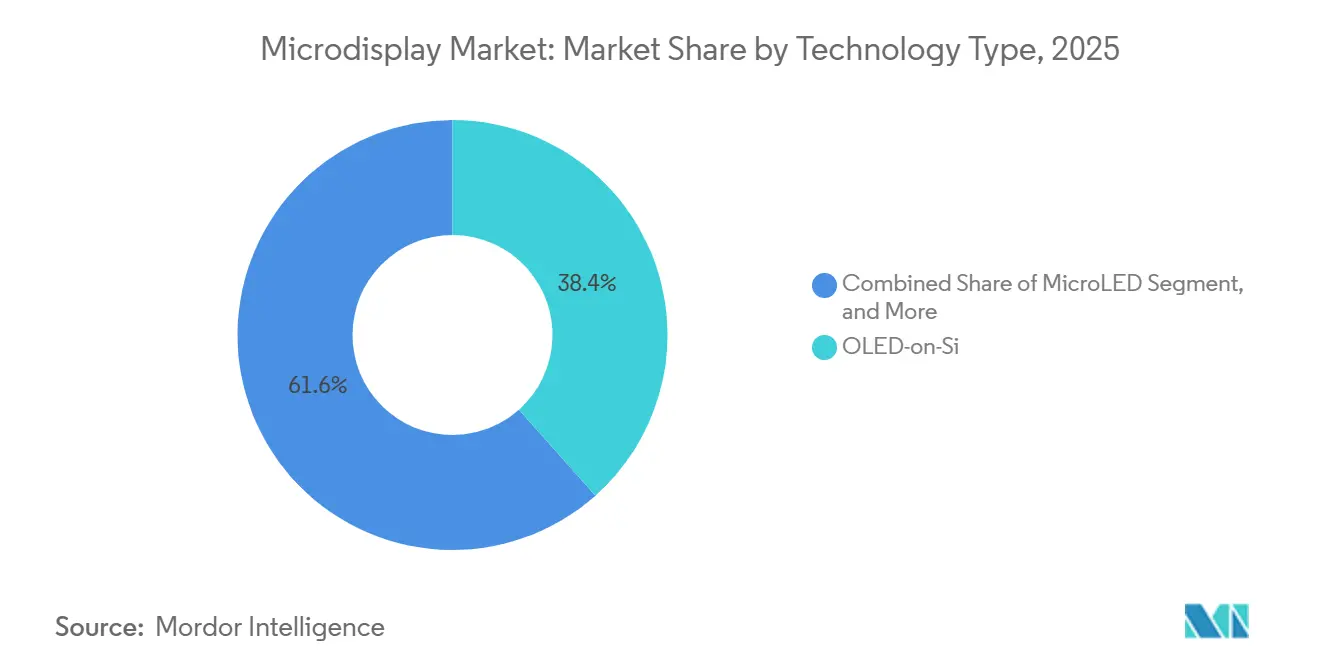

- By technology, OLED-on-silicon led with 38.43% of the microdisplay market share in 2025, while microLED is projected to advance at a 17.27% CAGR through 2031.

- By form factor, near-to-eye head-mounted displays captured 48.37% revenue in 2025, whereas head-up displays are forecast to expand at a 17.69% CAGR to 2031.

- By resolution, the 1024×768 to 1920×1080 class held 53.61% share of the microdisplay market size in 2025, and panels above 1920×1080 are set to grow at a 17.02% CAGR over 2026-2031.

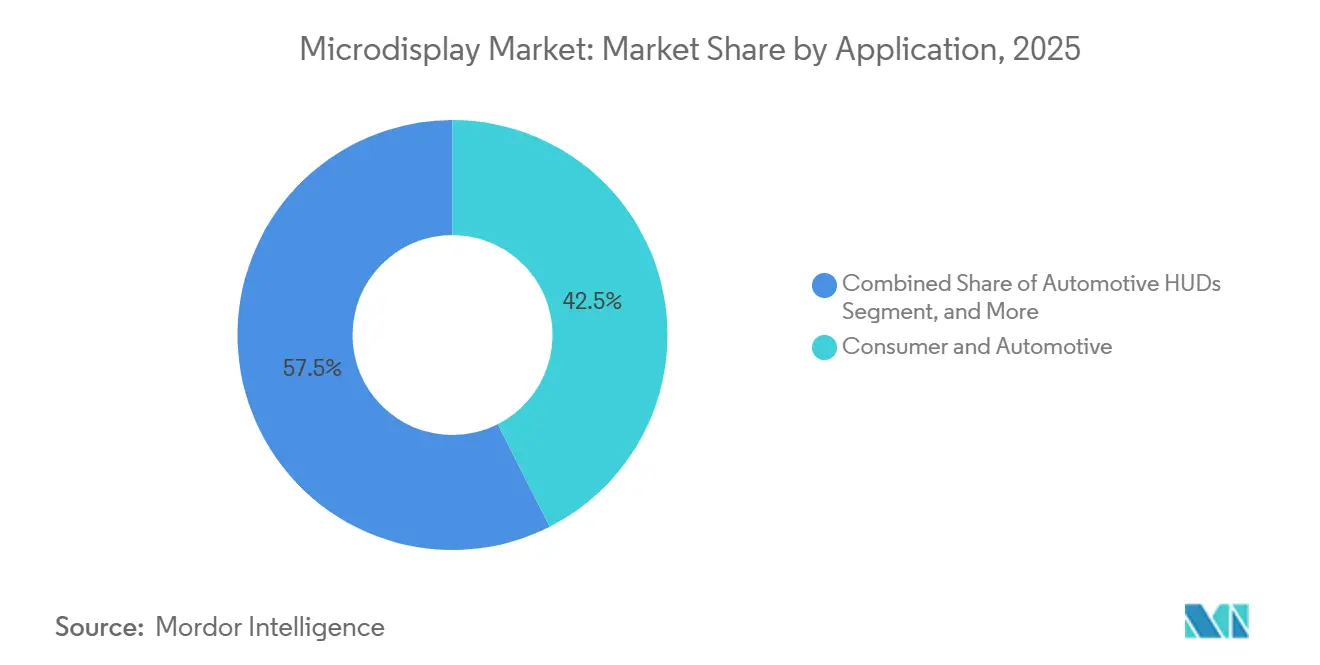

- By application, consumer and automotive uses combined for 42.53% of 2025 revenue, while automotive HUDs alone are expected to log the fastest 18.12% CAGR through 2031.

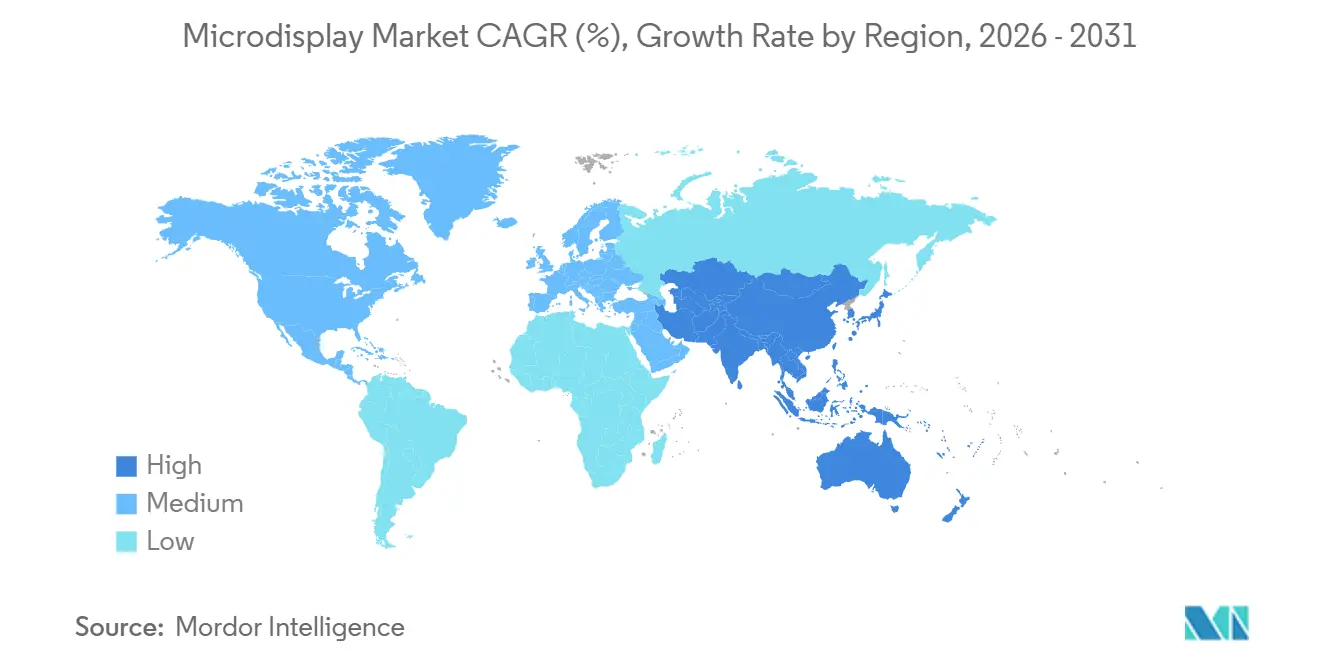

- By geography, Asia Pacific commanded 36.32% revenue in 2025 and remains the fastest-growing region at a 17.36% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Microdisplay Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exploding Demand for Ultra-Compact Displays in AR/VR Wearables across Asia | +4.2% | Asia Pacific core, spill-over to North America and Europe | Medium term (2-4 years) |

| Automotive OEM Shift to Transparent Micro-LED HUDs for Level-3+ ADAS | +3.8% | Europe and North America lead, Asia Pacific follows | Medium term (2-4 years) |

| Defense Modernization Programs Specifying Low-SWaP Visor Displays | +2.9% | North America, Europe, Middle East | Long term (≥ 4 years) |

| Rise of Metaverse-Ready Smart Glasses from Big-Tech Partnerships | +3.1% | Global, concentrated in North America and Asia Pacific | Short term (≤ 2 years) |

| Mini-Fab Outsourcing Enabling Cost-Effective OLED-on-Si for Consumer Cameras | +2.3% | Asia Pacific manufacturing, global end-market | Medium term (2-4 years) |

| Cinematic Drones and Micro-Projectors Driving High-Nits LCoS Adoption | +1.4% | North America, Europe, Asia Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Exploding Demand for Ultra-Compact Displays in AR-VR Wearables Across Asia

Chinese and South Korean consumer-electronics ecosystems are converging on sub-1-inch panels as the enabling component for lightweight headsets, with startups such as Rokid and Nreal field-testing glasses under 80 grams that rely on 0.5-inch OLED-on-silicon modules delivering 1920×1080 resolution per eye. LG Display expanded OLED microdisplay output in late 2025 to serve these brands, while India’s manufacturing incentives are attracting assembly lines that meet indigenous content rules.[1]LG Display, “OLED Microdisplay Capacity Expansion,” lgdisplay.com Joint-ventures are shortening time-to-market, accelerating the transition from prototypes to volume production. Rising disposable incomes in Southeast Asia further stimulate demand for affordable AR wearables, reinforcing the microdisplay market growth trajectory.

Automotive OEM Shift to Transparent Micro-LED HUDs for Level-3+ ADAS

Mercedes-Benz deployed an augmented-reality HUD in the EQS sedan that projects 1280×720 graphics with sub-20 millisecond latency, using a DLP microdisplay engine certified to ISO 26262 ASIL D. BMW followed with similar systems in the iX and 7 Series, while Continental prototypes achieve 10,000-nit brightness on transparent microLED panels, enabling sunlight readability without bulky combiners. Euro NCAP protocols effective 2025 reward driver-assistance visualization, encouraging mid-tier automakers to specify microdisplay HUDs. This automotive pull is reshaping capacity plans and qualification processes across the microdisplay industry.

Rise of Metaverse-Ready Smart Glasses from Big-Tech Partnerships

Meta Platforms shipped over 1 million Ray-Ban smart glasses in 2025 and is migrating to models that embed microdisplays for notification overlays.[2]Meta Platforms, “Ray-Ban Smart Glasses Development,” about.meta.com Apple’s Vision Pro sets a benchmark with dual 1.42-inch OLED-on-silicon panels at 3,391 ppi, supplied by Sony Semiconductor Solutions. Samsung, Google, and Qualcomm launched a cross-platform XR alliance that standardizes sub-10 millisecond motion-to-photon latency, pressuring suppliers to optimize yield and power rather than chase ever-higher resolutions. These multi-year roadmaps expand addressable volumes, anchoring investment decisions in the microdisplay market.

Defense Modernization Programs Specifying Low-SWaP Visor Displays

Kopin won a USD 15.4 million United States Army contract in 2025 for OLED visor displays that fuse night-vision and thermal data into a mixed-reality feed.[3]Kopin Corporation, “OLED Microdisplays for Defense and Aerospace,” kopin.com Elbit Systems provides 5,000-nit, 1280×1024 panels for the F-35 helmet, meeting MIL-STD-810 shock and vibration criteria. Multi-year production cycles guarantee predictable demand, but suppliers must navigate export-control regulations and rigorous environmental testing. These requirements drive R&D into higher thermal conductivity backplanes and extended lifespan materials, differentiating vendors in the microdisplay market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Yield Losses in RGB Micro-LED Mass-Transfer Processes | -2.1% | Global, concentrated in Asia Pacific manufacturing hubs | Medium term (2-4 years) |

| Limited Through-Wafer Heat Dissipation in High-Brightness OLED-on-Si | -1.7% | Global, acute in outdoor AR and automotive HUD applications | Short term (≤ 2 years) |

| Supply-Chain Bottlenecks for High-Purity Sapphire and Silicon Backplanes | -1.3% | Asia Pacific supply, global demand | Medium term (2-4 years) |

| IP Litigation Risk among United States and Chinese Panel Makers | -0.9% | United States and China, spill-over to Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Yield Losses in RGB Micro-LED Mass-Transfer Processes

Achieving 99.99% defect-free placement of sub-10 micron emitters remains elusive, forcing manufacturers to over-provision die counts and run costly repair cycles that inflate microLED panel costs by up to 60%. VueReal’s solid-print method claims 99.995% yield yet has not demonstrated sustained production beyond 10,000 units per month. Until yields stabilize, microLED will stay limited to premium automotive and defense niches, constraining its contribution to broader microdisplay market expansion.

Limited Through-Wafer Heat Dissipation in High-Brightness OLED-on-Si

Sustained drive above 4,000 nits accelerates organic material degradation, cutting panel half-life by two-thirds according to Journal of the Society for Information Display studies. eMagin’s direct-patterned OLED improves efficiency but still cites thermal load as the main ceiling on brightness. Copper heat spreaders and through-silicon vias add USD 20-30 per unit, limiting uptake in cost-sensitive consumer headsets. Thermal constraints therefore temper the microdisplay market’s penetration into sunlight-readable AR and automotive use cases.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Performance and Cost Dynamics

OLED-on-silicon held 38.43% of 2025 revenue within the microdisplay market share, benefiting from mature backplanes that integrate color filters without incurring microLED mass-transfer losses. MicroLED, however, is growing at a 17.27% CAGR as automakers seek transparent, 10,000-nit windscreen overlays for advanced driver-assistance. The microdisplay market size attributable to traditional LCoS and DLP technologies remains stable in projection and camera applications where cost and supply-chain maturity outweigh emissive advantages.

Japanese and Korean vendors monetize premium OLED panels at prices as high as USD 350 per unit for flagship VR headsets, while Chinese start-ups court mid-tier brands with 20% lower pricing. Quantum-dot-on-silicon prototypes from BOE and Samsung Display target long-term color-purity gains, but near-term shipments stay negligible. Consequently, the microdisplay market balances cost-optimized OLED-on-silicon volumes against performance-driven microLED pilots.

By Resolution: Mid-Range Dominates, Ultra-HD Rises

The 1024×768 to 1920×1080 band accounted for 53.61% of 2025 revenue, anchoring the microdisplay market share with workhorse panels used in camera viewfinders, entry-level AR glasses, and legacy projectors. Demand is steady because these resolutions align with battery life and cost targets for mainstream devices, keeping volumes high even as premium tiers shift upward. Panels above 1920×1080, however, are scaling at a 17.02% CAGR, propelled by VR headsets that require sub-pixel rendering to eliminate screen-door artifacts and by automotive HUDs that must display dense driver-assistance graphics. Sony’s 3648×3144 OLED-on-silicon module for a flagship headset underscores how premium buyers absorb higher costs for immersive fidelity, encouraging rivals to roadmap 4K-per-eye products. Component suppliers are therefore splitting production between high-volume mid-range lines and smaller ultra-HD lots that validate new transistor and deposition techniques.

Ultra-HD growth is steering substrate makers to 12-inch wafer formats, boosting economies of scale that gradually compress per-unit costs. Meanwhile, optical-engine designers tweak waveguide combiners and pancake lenses so that higher pixel counts translate into meaningful visual gains without ballooning headset weight. As mid-range volumes fund capex and process learning, breakthroughs in yield and thermal management are expected to trickle into the ultra-HD class, enlarging its slice of the microdisplay market size by the end of the forecast window.

By Application: Consumer Breadth, Automotive Velocity

Consumer and automotive electronics together delivered 42.53% of 2025 revenue, reflecting widespread use of near-to-eye displays in gaming headsets, smart glasses, and infotainment clusters. Unit growth here remains sensitive to retail pricing and content ecosystems, so suppliers emphasize yield improvement and mini-fab outsourcing to hold module costs below USD 50 for camera EVFs and below USD 150 for entry AR glasses. Automotive HUDs, though smaller in 2025 volume, are the fastest-growing niche at an 18.12% CAGR through 2031 as Euro NCAP and IIHS protocols reward in-line driver-assistance visualization.

HUD programs demand 10,000-nit brightness, −40 °C to +85 °C operating ranges, and 15-year service life, which shifts sourcing away from consumer-grade OLED toward microLED and hybrid stacks. Long design cycles and stringent ISO 26262 requirements create sticky, high-margin contracts that offset slower ramp-ups. Defense, industrial, and medical uses sustain premium pricing by valuing night-vision compatibility and sterilization-friendly housings, yet their combined share trails consumer and automotive volumes. Across applications, suppliers balance cost-down pressures in mass markets with performance-driven specs in regulated sectors, ensuring diversified revenue streams that underpin the broader microdisplay market share.

By Form Factor: Immersive Wearables and Automotive Safety Edge

Near-to-eye head-mounted displays contributed 48.37% of 2025 revenue, reflecting strong uptake of consumer VR headsets and enterprise AR glasses. The microdisplay market size generated by automotive head-up displays is smaller today yet rising quickly, with the segment forecast to clock a 17.69% CAGR through 2031. Wearable camera viewfinders and micro-projectors fill convenience-driven niches but lack the scale of HMDs and HUDs.

Innovation vectors diverge across form factors. HMD suppliers emphasize field of view and latency, advancing toward 8K-per-eye targets that demand transistor densities above 10,000 ppi. Automakers instead prioritize brightness, thermal resilience, and operating lifetimes exceeding 15 years, nudging suppliers toward microLED or hybrid OLED-LCD stacks. This split ensures that the microdisplay market drives parallel R&D streams rather than converging on a single technology path.

Geography Analysis

Asia Pacific accounted for 36.32% of 2025 revenue and is projected to retain leadership with a 17.36% CAGR as Chinese firms scale 8-inch and 12-inch wafer lines and South Korean players expand OLED capacity. Government subsidies and vertical integration lower finished-panel prices by up to 30%, prompting global headset brands to qualify Asian sources. India’s incentives draw assembly and test operations that position the country as a future defense supplier.

North America and Europe act primarily as consumption hubs. Premium automotive OEMs integrate microdisplay HUDs to satisfy Euro NCAP visualization requirements, and the United States Army funds ruggedized visor programs that guarantee multi-year demand. Big-tech programs from Apple and Meta lock in high-resolution panel roadmaps, tying supplier fortunes to consumer electronics cycles and regulatory scrutiny around export controls.

The Middle East specifies low-SWaP visor displays for fighter aircraft and special-forces kits, offering stable but modest order volumes at premium pricing. South America and Africa remain nascent markets where disposable incomes and automotive penetration are still developing, though Brazil shows early adoption in drone cinematography. Overall, regional dynamics reinforce Asia Pacific manufacturing dominance while North American and European demand dictates performance specifications for the broader microdisplay market.

Competitive Landscape

Sony Semiconductor Solutions, Kopin, eMagin, Jade Bird Display, and BOE collectively generated about 55% of 2025 revenue, giving them scale advantages in capex and supply-chain leverage. Sony’s vertical integration secures premium margins on flagship VR panels, while Kopin shields itself from consumer cycles by emphasizing defense and automotive contracts that extend over multiple budget periods.

A second competitive tier of VueReal, PlayNitride, and Lumiode pursues microLED mass-transfer breakthroughs promising 99.995% yield, yet each firm must still demonstrate sustained output above 10,000 units per month. Their technology roadmaps attract strategic investors from automotive and smart-glasses ecosystems seeking brightness and power gains unattainable with today’s OLED-on-silicon.

Legal and regulatory dynamics now shape bargaining power. Patent disputes between United States and Chinese panel makers create licensing uncertainty that can freeze joint-venture talks, while ISO 26262 and MIL-STD certifications become gating factors for new contracts. Vendors that lock down safety and environmental credentials early are better positioned to defend share as pricing pressure intensifies at the lower end of the microdisplay market.

Microdisplay Industry Leaders

OLEDWorks

eLux, Inc.

Kopin Corporation

eMagin Corporation

Seiko Epson Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Kopin won a USD 15.4 million United States Army contract to supply OLED visor displays for the Integrated Visual Augmentation System, with deliveries starting Q2 2026.

- August 2025: Haylo Labs acquired Plessey Semiconductors for USD 100 million debt-backed financing, obtaining monolithic microLED IP and the Plymouth fabrication site.

- June 2025: Jade Bird Display raised RMB 1 billion (USD 140 million) to expand its 8-inch microLED line to 50,000 wafers per year and accelerate full-color RGB development.

- March 2025: BOE unveiled a 0.39-inch 1080p OLED microdisplay at 4,032 ppi during SID Display Week, targeting sub-500 milliwatt AR glasses.

Global Microdisplay Market Report Scope

A microdisplay is a very small, high-resolution display panel usually less than 2 inches diagonally designed to show images directly in front of the eye or through an optical system rather than being viewed like a traditional screen.

The Microdisplay Market Report is Segmented by Technology Type (Traditional LCoS, LCD, DLP; OLED-on-Si; MicroLEDs; Quantum-Dot-on-Si), Resolution (Up to 1024×768, 1024×768-1920×1080, Above 1920×1080), Application (Consumer and Automotive, Defense, Industry and Enterprise, Others), Form Factor (Near-to-Eye HMD, HUD, Micro-Projectors, Wearable Viewfinders), and Geography (North America, South America, Europe, Asia Pacific, Middle East, Africa). Market Forecasts are Provided in Terms of Value (USD).

| Traditional (LCoS, LCD, DLP) |

| OLED-on-Si |

| MicroLEDs |

| Quantum-Dot-on-Si |

| Up to 1024 × 768 |

| 1024 × 768 – 1920 × 1080 |

| Above 1920 × 1080 |

| Consumer and Automotive | Augmented Reality / Virtual Reality Headsets |

| Automotive HUDs | |

| Traditional Projection / Camera | |

| Defense | |

| Industry and Enterprise | |

| Other Applications |

| Near-to-Eye Head-Mounted Displays |

| Head-Up Displays |

| Micro-Projectors |

| Wearable Viewfinders and Finders |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Nordics | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Kenya | |

| Rest of Africa |

| By Technology Type | Traditional (LCoS, LCD, DLP) | |

| OLED-on-Si | ||

| MicroLEDs | ||

| Quantum-Dot-on-Si | ||

| By Resolution | Up to 1024 × 768 | |

| 1024 × 768 – 1920 × 1080 | ||

| Above 1920 × 1080 | ||

| By Application | Consumer and Automotive | Augmented Reality / Virtual Reality Headsets |

| Automotive HUDs | ||

| Traditional Projection / Camera | ||

| Defense | ||

| Industry and Enterprise | ||

| Other Applications | ||

| By Form Factor | Near-to-Eye Head-Mounted Displays | |

| Head-Up Displays | ||

| Micro-Projectors | ||

| Wearable Viewfinders and Finders | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Nordics | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How fast is the microdisplay market expected to grow through 2031?

The microdisplay market is projected to register a 16.93% CAGR from 2026 to 2031, rising from USD 2.91 billion in 2026 to USD 6.36 billion by 2031.

Which technology currently leads revenue?

OLED-on-silicon accounted for 38.43% of 2025 revenue, benefiting from mature backplane processes and full-color integration.

Why is microLED considered the fastest-growing segment?

MicroLED panels offer 10,000-nit brightness and transparency that automotive OEMs need for advanced driver-assistance HUDs, driving a 17.27% CAGR.

Which region will expand the quickest?

Asia Pacific is forecast to grow at 17.36% CAGR through 2031 as Chinese and South Korean makers ramp 8-inch and 12-inch wafer capacity.

What restrains OLED-on-silicon brightness?

Limited through-wafer heat dissipation raises panel temperatures above safe thresholds once brightness exceeds 4,000 nits, shortening lifetime.

How concentrated is supplier power today?

The top five companies command roughly 55% of revenue, indicating moderate concentration with ample room for new entrants.

Page last updated on: