Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

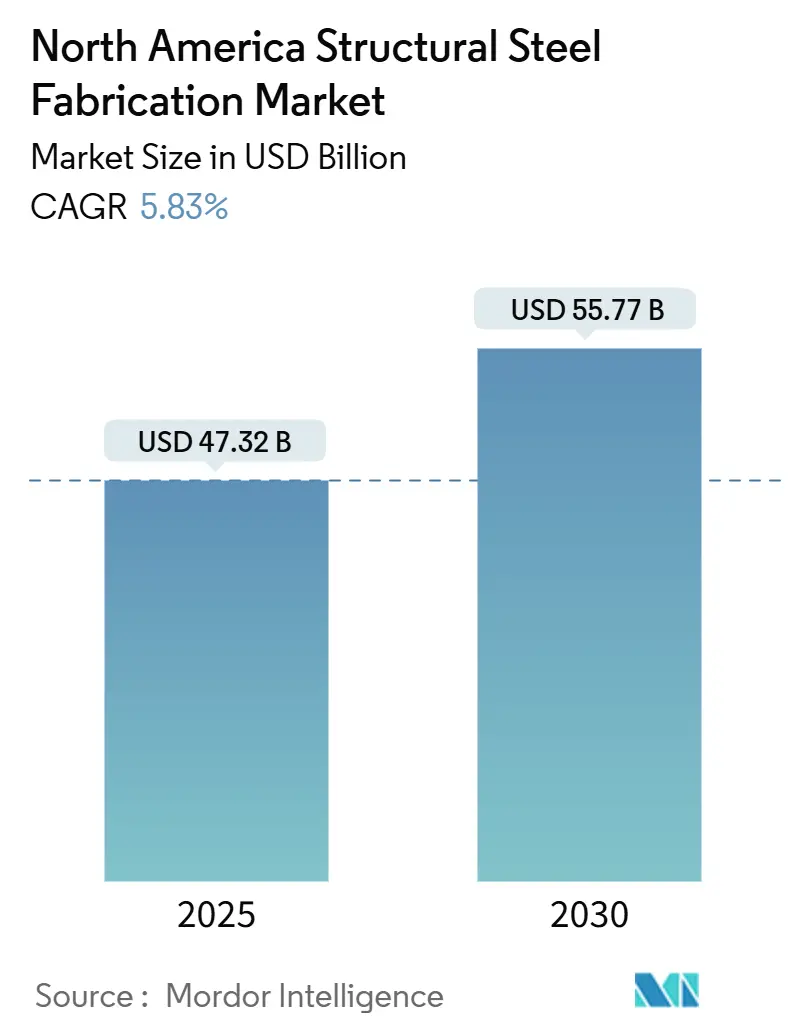

| Market Size (2025) | USD 47.32 Billion |

| Market Size (2030) | USD 55.77 Billion |

| Growth Rate (2025 - 2030) | 5.83% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Structural Steel Fabrication Market Analysis by Mordor Intelligence

The North America structural steel fabrication market size reached USD 47.32 billion in 2025 and is projected to rise to USD 55.77 billion by 2030, reflecting a 3.34% CAGR over the forecast period. Steady federal infrastructure outlays, growing renewable-energy installations, and a shift toward off-site modular methods underpin this measured expansion. Demand remains anchored in transportation, commercial, and industrial construction, while specialty applications in mining, defense, and telecommunications broaden the customer base. Automated laser‐cutting, AI-assisted design, and electric-arc-furnace (EAF) steel adoption are raising productivity and supporting lower-carbon procurement. Fabricators continue to adjust contract terms to hedge raw-material swings and to cope with acute welder shortages through robotics and training partnerships. Regulatory requirements such as Buy America and facility-specific Environmental Product Declarations are shaping sourcing decisions and reinforcing the competitiveness of domestic suppliers.

Key Report Takeaways

- By end-user industry, construction held 58.76% of the North America structural steel fabrication market share in 2024, while Other end-user industries are forecast to expand at a 5.19% CAGR through 2030.

- By product type, heavy structural sections commanded 41.78% of the North America structural steel fabrication market size in 2024; Other Product Types are set to grow at a 4.84% CAGR to 2030.

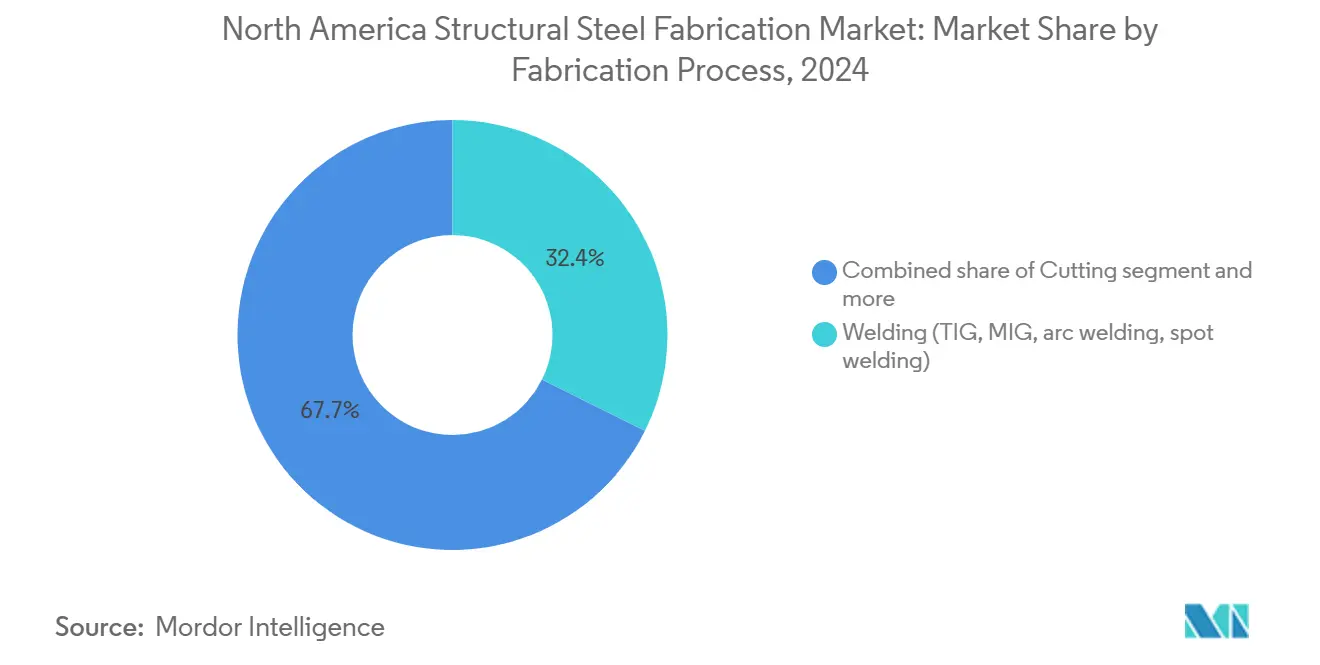

- By fabrication process, welding led with 32.35% share of the North America structural steel fabrication market size in 2024, whereas cutting processes are advancing at a 4.67% CAGR through 2030.

- By geography, the United States captured 85.67% of the North America structural steel fabrication market share in 2024; Canada is progressing at a 4.45% CAGR over 2025-2030.

North America Structural Steel Fabrication Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure bill spending surge | +0.8% | United States; spillover to Canada and Mexico | Medium term (2-4 years) |

| Commercial & residential construction rebound | +0.7% | North America; strongest in U.S. metropolitan areas | Short term (≤ 2 years) |

| Wind-energy tower & solar-tracker build-outs | +0.6% | United States and Canada; concentrated in wind corridors | Long term (≥ 4 years) |

| Modular off-site construction adoption | +0.4% | North America; led by Canada and U.S. West Coast | Medium term (2-4 years) |

| Seismic-resilient retrofit demand | +0.3% | California, Oregon, Washington | Long term (≥ 4 years) |

| AI-driven design optimization | +0.2% | North America; early adoption in large fabricators | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Federal Infrastructure-Bill Spending Surge

Infrastructure Investment and Jobs Act allocations are generating a multi-year pipeline for bridges, highways, and multimodal projects that require vast tonnage of fabricated steel. The USD 1.8 trillion package, combined with Build America Buy America sourcing rules, is funneling work to domestic plants even as high construction costs encourage escalation clauses and reimbursable contracts. The Gordie Howe International Bridge, budgeted at USD 4.7 billion, illustrates how federal requirements can channel more than 11 million lb of rebar and complex structural sections to North American shops.

Re-acceleration of Commercial & Residential Construction

Nonresidential spending rose 3.9% year-over-year in late 2024, with industrial construction up 16.6% to roughly USD 236 billion, surpassing two-decade averages. Anticipated 100 basis-point rate cuts by the U.S. Federal Reserve through 2025 should unlock delayed projects. Canada’s Q3 2024 construction sector returned to 0.1% quarterly growth, and non-residential permits jumped 13.5%, signaling a healthy backlog for fabricators.

Wind-Energy Tower & Solar-Tracker Build-Outs

Utility-scale wind requires about 115 tons of steel per megawatt, while solar trackers consume 41-47 tons. Partnerships such as Nextracker and JM Steel’s USD 100 million upgrade in Pennsylvania add 4 GW of tracker capacity and showcase the structural steel intensity of renewable energy growth. Blade and tower OEMs are also prioritizing EAF-sourced “green steel” to satisfy embodied-carbon thresholds[1]Blake Harris, “Steel Use in Renewable Energy,” Alliance for Innovation and Infrastructure, aii.org.

Modular Off-Site Construction Adoption

Factory-built modules can cut on-site emissions by 43% and reduce waste by up to 70%, completing small multi-unit buildings in roughly 12 weeks. British Columbia promotes “made-in-BC” plants to meet housing goals, creating export opportunities across the region. Modularization benefits fabricators through batch production, higher dimensional accuracy, and fewer field welds.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile steel coil & plate prices | –0.5% | North America; sharper in import-dependent regions | Short term (≤ 2 years) |

| Skilled welder & fitter shortages | –0.4% | North America; acute in specialized segments | Medium term (2-4 years) |

| Hybrid mass-timber competition | –0.3% | Pacific Northwest and major U.S./Canadian cities | Long term (≥ 4 years) |

| Embodied-carbon regulations | –0.2% | United States and Canada; led by California and federal agencies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Steel Coil & Plate Prices

Hot-rolled coil stabilized between USD 700-800 per short ton in late 2024, well below pandemic peaks yet high enough to squeeze fabrication margins. Domestic mills curtailed output to balance inventories, narrowing U.S.–Europe price spreads and limiting import relief. Fabricators are negotiating escalation clauses and exploring futures hedges to protect bid validity[2]Alan Price, “North American Steel Market Update,” Ryerson, ryerson.com.

Skilled Welder & Fitter Shortages

As about 30% of its workforce approaches retirement, the American Welding Society foresees 360,000 job openings by 2027, highlighting a significant demand for skilled professionals in the welding industry. In 2023, wage inflation surged past 5.1%, further intensifying the need for workforce development. To address this challenge, employers are accelerating their robotics initiatives to enhance operational efficiency and reduce dependency on manual labor. Additionally, they are forming strategic partnerships with technical colleges to establish robust talent pipelines, ensuring a steady supply of qualified workers to meet future industry demands[3]Monica Pfarr, “Welder Workforce Outlook,” American Welding Society, aws.org.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Heavy Sections Drive Volume Despite Specialty Growth

Heavy structural sections generated 41.78% of 2024 revenue within the North America structural steel fabrication market size, reflecting their ubiquitous role in frames, bridges, and industrial plants. Commodity availability, established A992 specifications, and predictable lead times sustain leadership. Specialty plate-worked girders, trusses, and custom modules are expanding at a 4.84% CAGR, buoyed by renewable-energy towers, immersed-tube tunnels, and data-center skids. The American Institute of Steel Construction’s new Environmental Product Declarations for beams, plate, and hollow sections provide standardized carbon accounting, further supporting both commodity and specialty offerings.

Accelerated specialty uptake mirrors broader shifts toward engineered, prefabricated systems that cut site labor and compress schedules. AI-enabled detailing, multi-axis robotic welding, and high-power fiber-laser cutting raise precision and throughput. As owners seek lower total installed cost, heavy-section producers are integrating fabrication, galvanizing, and modular assembly to defend share against niche competitors capturing premium margins.

By End-User Industry: Construction Dominance Faces Diversification Pressure

Construction accounted for 58.76% of 2024 spending in the North America structural steel fabrication market, spanning office towers, industrial warehouses, bridges, and transit hubs. Federal and provincial infrastructure pipelines and private-sector factory announcements anchor near-term volume. Yet Other End User Industries, comprising mining, shipbuilding, defense, aerospace, agriculture, and telecom infrastructure, are forecast to grow 5.19% annually, reflecting a pivot toward mission-critical and technology-driven structures. Defense programs benefiting from reshoring initiatives, 5G tower rollouts, and data-center expansions exemplify these emerging pools of demand. Fabricators that secure sector-specific certifications, such as AWS D1.1/D1.5 for bridges or NAVSEA approvals for naval components, are positioned to access higher-margin work.

By Fabrication Process: Welding Leadership Challenged by Cutting Innovation

Welding retained a 32.35% share in 2024 across the North America structural steel fabrication market, underpinning virtually all load-bearing connections. MIG and flux-cored processes lead, while advanced tandem-arc and hybrid laser-arc systems reduce distortion and cycle time. Cutting processes are registering a 4.67% CAGR as automated fiber lasers, bevel plasma, and robotic tube lines scale throughputs. Nextracker’s new Pennsylvania line triples solar-tracker tube capacity via integrated drilling and swedging, underscoring productivity gains when cutting automation dovetails with sector-specific growth. Forming, machining, and casting processes remain essential for specialized geometries but grow more closely in line with overall output.

Geography Analysis

The United States captured 85.67% of the 2024 volume in the North America structural steel fabrication market, anchored by a vast installed infrastructure base, proximity to major steel mills, and deep pools of engineering talent. High-profile projects, such as the USD 4.7 billion Gordie Howe International Bridge, illustrate scale and local content mandates that favor domestic shops. EPA Product Category Rules and the General Services Administration’s low-carbon procurement pilots are steering specifications toward EAF-melted feedstock, reinforcing the U.S. position as a technology and sustainability leader.

Canada represents the fastest-growing geography at a 4.45% CAGR from 2025-2030. The Fraser River Tunnel replacement, valued at CAD 4.15 billion (USD 3.2 billion), and a steady pipeline of wind-energy and hydro projects drive structural demand. Ottawa’s Standard on Embodied Carbon in Construction will require project owners to source steel within the top 20% of carbon performance starting September 2025, steering fabricators toward low-carbon EAF supply chains.

Mexico lags amid weak domestic construction and intensified competition from Asian imports. Nonetheless, United States-Mexico-Canada Agreement rules and near-shoring of industrial OEMs present opportunities for border-region shops offering quick-turn, lower-labor-cost fabrication. Peso depreciation has inflated imported consumable costs, but companies with long-term U.S. offtake contracts are partially shielded from exchange volatility.

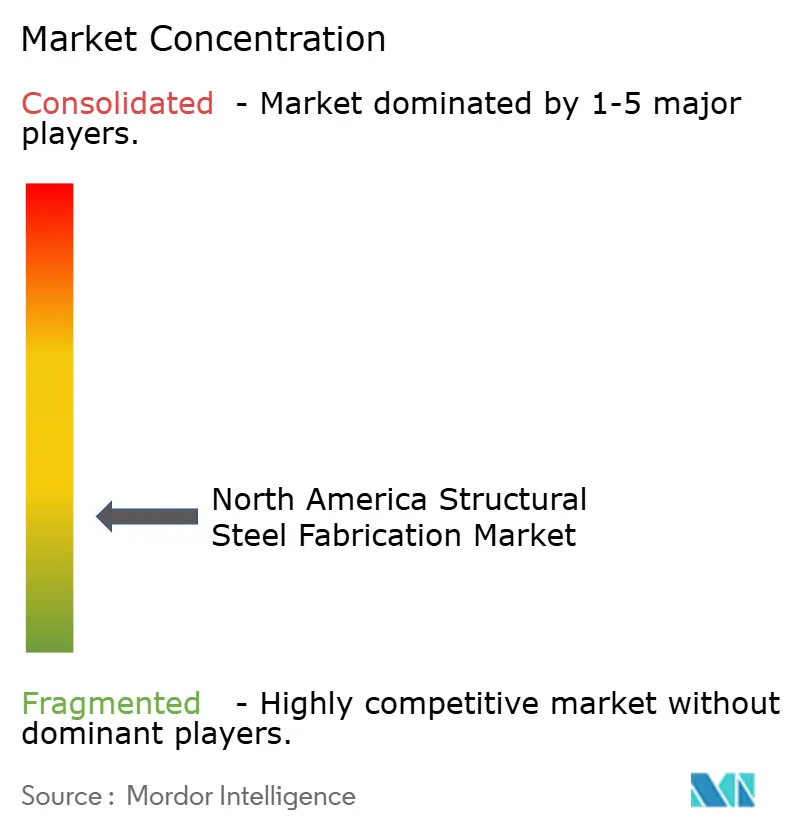

Competitive Landscape

Competition is moderately fragmented. Consolidation is underway: Lorraine Capital created Caldera Manufacturing Group by combining four mid-sized shops into a 170-employee platform spanning Pennsylvania, Maryland, and Oklahoma, enabling cross-plant workload balancing and broader service menus. State Steel Supply’s 2025 merger with SPS Companies expands distribution across 17 U.S. and Mexican sites, ensuring mill-to-market control of coil, plate, and fabricated sections.

Technology is a key differentiator. Early adopters of AI-driven design optimization report up to 75% reduction in estimation hours and 50% quicker material nesting. Robotics helps offset labor scarcity, especially for repeatable welds on solar-tracker tubes and wind-tower ladders. Sustainability credentials also shape bid success. ArcelorMittal’s XCarb 67% lower-carbon roofing sheets expand the menu of EAF-sourced offerings available to fabricators seeking to meet procurement scorecards.

White-space persists in seismic retrofit assemblies, immersed-tube tunnel segments, and pre-assembling modules for remote resource projects. Companies able to combine engineering, fabrication, and on-site erection under fixed-price or progressive design-build contracts are best positioned to capture above-average margins.

North America Structural Steel Fabrication Industry Leaders

Valmont Industries Inc.

DBM Global Inc.

Cornerstone Building Brands Inc.

Groupe Canam Inc.

High Industries Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: ArcelorMittal partnered with Ateliers 3S to launch low-carbon trapezoidal roofing sheets produced from XCarb recycled and renewably powered steel, achieving a 67% carbon-footprint cut versus blast-furnace outputs.

- January 2025: State Steel Supply merged with SPS Companies, combining two top-40 service centers across 17 North American sites while retaining State Steel as a standalone unit.

- October 2024: Federal Steel Supply acquired Venture Pipe and Supply, entering Oklahoma’s oilfield supply chain and diversifying beyond industrial piping.

- September 2024: Beacon bought Chicago Metal Supply & Fabrication, adding custom architectural sheet-metal capacity to support its Ambition 2025 growth program.

North America Structural Steel Fabrication Market Report Scope

By Product Type

| Heavy Section (Beams & Columns) |

| Light Sectional & Cold-Formed Members |

| Tubular & Hollow Structural Sections (HSS) |

| Other Product Types (Plate-worked Girders & Trusses, Custom-built Modules & Skids, etc.) |

By End-user Industry

| Construction | Commercial |

| Residential | |

| Industrial Buildings | |

| Infrastructure (Transport) | |

| Power & Energy (include utilities and renewable energy) | |

| Manufacturing & Industrial Equipment | |

| Oil and Gas | |

| Automotive & Transportation (railways systems, metro components, etc.) | |

| Other End User Industries (Mining, Shipbuilding & Marine, Defense & Aerospace, Agriculture & Food Processing, and Telecommunications) |

By Fabrication Process

| Cutting (Laser cutting, plasma cutting, water jet cutting, sawing, shearing, etc.) |

| Bending (Press brakes, roll bending, rotary bending) |

| Welding (TIG, MIG, arc welding, spot welding) |

| Machining (Milling, turning, drilling, grinding, CNC machining) |

| Forming (Stamping, forging, rolling, hydroforming) |

| Casting (Sand casting, die casting, investment casting) |

| Others (Plating, Surface Treatment, Punching, Finishing, Fastening, Assembly, Heat Treatment, Engraving, Hydroforming, Spinning, etc.) |

By Geography

| United States |

| Canada |

| Mexico |

| By Product Type | Heavy Section (Beams & Columns) | |

| Light Sectional & Cold-Formed Members | ||

| Tubular & Hollow Structural Sections (HSS) | ||

| Other Product Types (Plate-worked Girders & Trusses, Custom-built Modules & Skids, etc.) | ||

| By End-user Industry | Construction | Commercial |

| Residential | ||

| Industrial Buildings | ||

| Infrastructure (Transport) | ||

| Power & Energy (include utilities and renewable energy) | ||

| Manufacturing & Industrial Equipment | ||

| Oil and Gas | ||

| Automotive & Transportation (railways systems, metro components, etc.) | ||

| Other End User Industries (Mining, Shipbuilding & Marine, Defense & Aerospace, Agriculture & Food Processing, and Telecommunications) | ||

| By Fabrication Process | Cutting (Laser cutting, plasma cutting, water jet cutting, sawing, shearing, etc.) | |

| Bending (Press brakes, roll bending, rotary bending) | ||

| Welding (TIG, MIG, arc welding, spot welding) | ||

| Machining (Milling, turning, drilling, grinding, CNC machining) | ||

| Forming (Stamping, forging, rolling, hydroforming) | ||

| Casting (Sand casting, die casting, investment casting) | ||

| Others (Plating, Surface Treatment, Punching, Finishing, Fastening, Assembly, Heat Treatment, Engraving, Hydroforming, Spinning, etc.) | ||

| By Geography | United States | |

| Canada | ||

| Mexico | ||

Key Questions Answered in the Report

How large is the North America structural steel fabrication market in 2025?

The market stands at USD 47.32 billion in 2025, with a 3.34% CAGR projected through 2030.

Which product category leads demand across the region?

Heavy structural sections such as beams and columns lead, representing 41.78% of 2024 revenue.

What is driving faster growth in Canada compared with the United States?

Large infrastructure projects like the Fraser River Tunnel replacement (USD 3.2 billion) and embodied-carbon procurement rules are accelerating Canadian demand.

How are fabricators coping with welder shortages?

Companies are expanding robotics, partnering with technical schools, and offering apprenticeships while raising wages to attract talent.

Page last updated on: