Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

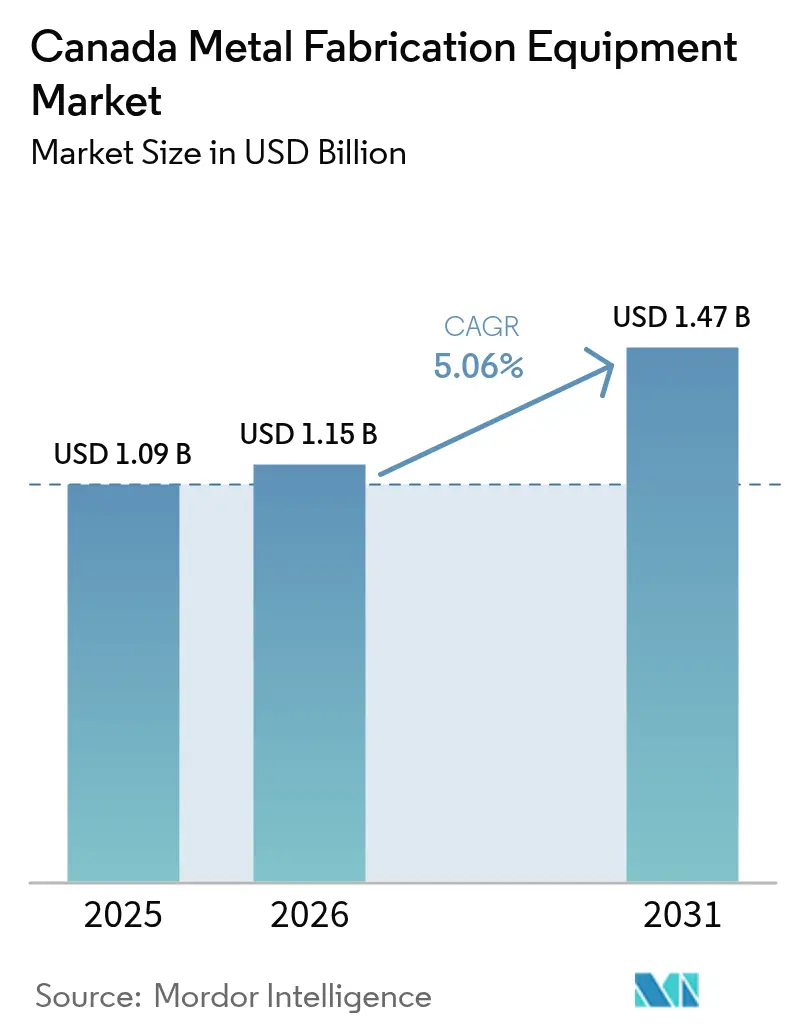

| Base Year Market Size (2025) | USD 1.09 Billion |

| Market Size (2026) | USD 1.15 Billion |

| Market Size (2031) | USD 1.47 Billion |

| Growth Rate (2026 - 2031) | 5.06% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Metal Fabrication Equipment Market Analysis by Mordor Intelligence

The Canada metal fabrication market size is projected to be USD 1.09 billion in 2025, USD 1.15 billion in 2026, and reach USD 1.47 billion by 2031, growing at a CAGR of 5.06% from 2026 to 2031. A surge of federally backed infrastructure spending, clean-economy tax credits aligned with the U.S. Inflation Reduction Act, and strict Buy Clean sourcing rules are steering new orders toward energy-efficient equipment and domestic-content-compliant projects. EV battery and hydrogen investments in Ontario and British Columbia are pulling welding and sheet-metal capacity away from legacy oil-and-gas jobs, creating a two-speed landscape that rewards shops positioned in clean-tech supply chains. Meanwhile, escalating labor shortages and electricity costs are compressing margins for firms slow to automate, even as turnkey automation packages from localized equipment suppliers such as TRUMPF and AMADA narrow delivery times and raise service expectations. Competitive focus is therefore shifting toward uptime reliability, traceability, and the ability to meet rapidly evolving public-sector specifications rather than lowest purchase price.

Key Report Takeaways

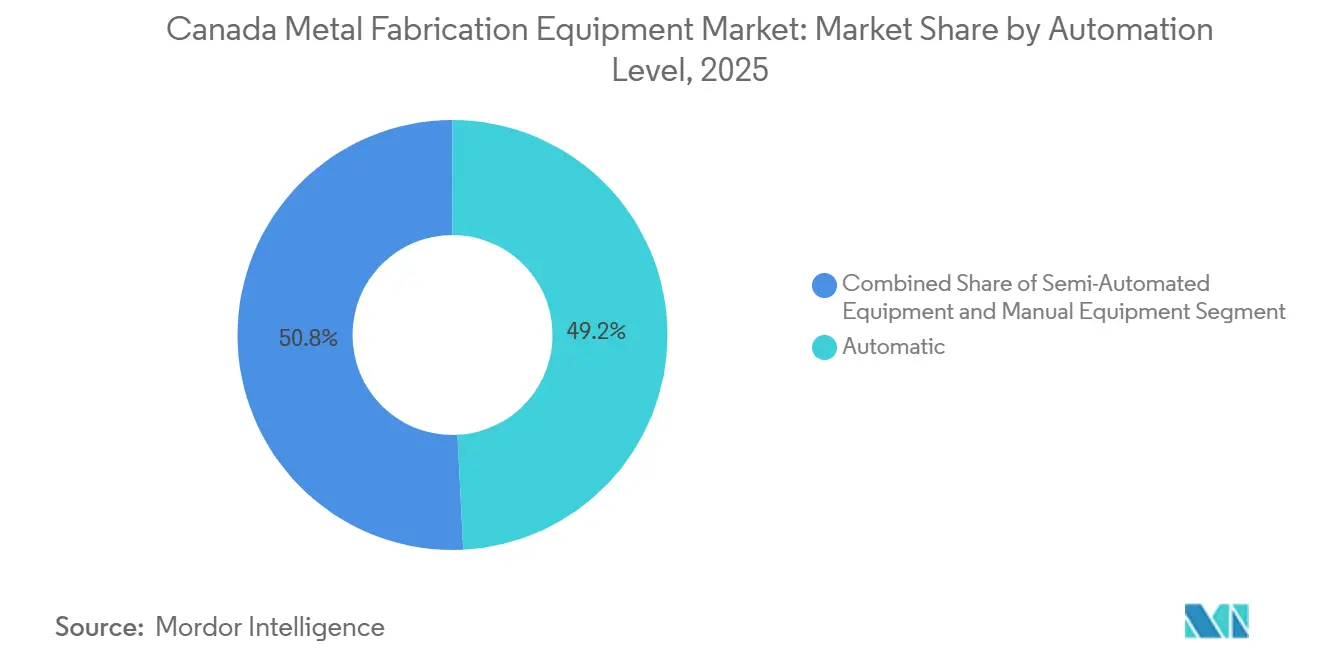

- By automation level, automatic equipment held 49.20% of the Canada metal fabrication market share in 2025, while the semi-automated category is projected to expand at a 6.10% CAGR through 2031.

- By equipment type, cutting systems captured 35.07% revenue share in 2025; finishing, handling, and tooling equipment is forecast to advance at a 7.01% CAGR to 2031.

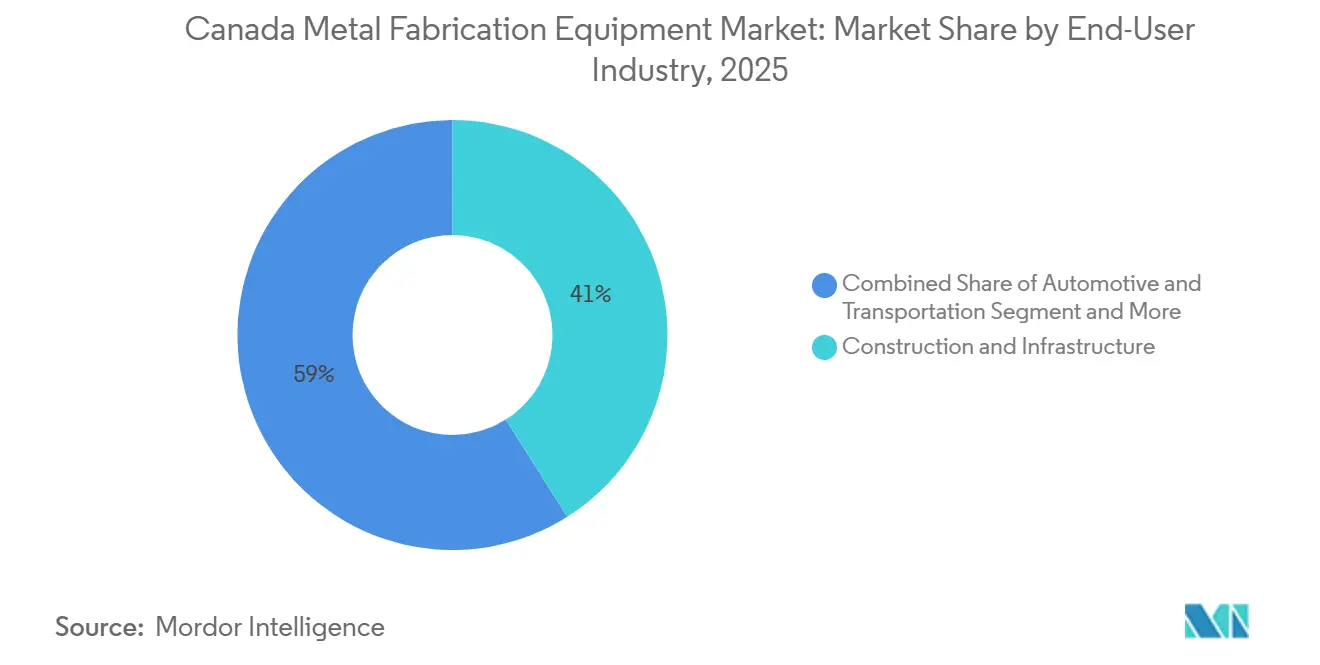

- By end-user, construction and infrastructure accounted for 41.04% of the Canada metal fabrication market size in 2025, whereas the “others” category is growing fastest at 6.20% through 2031.

- By province, Ontario led with a 44% share of the Canada metal fabrication market in 2025, while British Columbia is set to post the highest CAGR at 6.50% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Metal Fabrication Equipment Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Clean-Economy tax credits (IRA-aligned) boosting domestic EV & battery component fabrication | +1.5% | Ontario and Quebec automotive clusters; British Columbia hydrogen hubs | Medium term (2-4 years) |

| Expanded federal-provincial Infrastructure Canada 2030 pipeline funding | +1.2% | National, with concentration in Ontario, Quebec, and British Columbia urban corridors | Medium term (2-4 years) |

| Modular fabrication for small modular reactors & green-hydrogen projects | +0.9% | Ontario (nuclear), Alberta and British Columbia (hydrogen), Saskatchewan (SMR pilot) | Long term (≥ 4 years) |

| Mandatory "Buy Clean" procurement raising demand for high-efficiency metal-fab equipment | +0.8% | National, strongest in provinces with large public-works pipelines (Ontario, Quebec, Alberta) | Short term (≤ 2 years) |

| AI-driven digital-twin & predictive-analytics integration | +0.6% | National, led by Ontario and Quebec advanced-manufacturing centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Clean-Economy Tax Credits Boosting Domestic EV & Battery Component Fabrication

A 30% Investment Tax Credit for clean-tech manufacturing, plus a 15-40% credit for clean hydrogen, are redirecting cutting and welding capacity toward battery enclosures and electrolyzer frames.[1]Government of Canada, “Budget 2025: Clean Technology Investment Tax Credit,” canada.caMegaprojects such as Volkswagen’s USD 5.25 billion St. Thomas battery plant and Stellantis-LG’s USD 3.75 billion Windsor facility have already contracted local fabricators for precision housings that meet IATF 16949 standards. Immediate expensing for machinery introduced in Budget 2025 lets shops write off laser cutters or robotic cells in year one, improving cash flow and shortening payback periods. Suppliers positioned in these clean-tech clusters report order books stretching to 2028, while conventional oil-and-gas fabricators face project deferrals. The uneven incentive structure is therefore bifurcating the Canada metal fabrication market, rewarding firms aligned with electric-vehicle and hydrogen value chains.

Expanded Federal–Provincial Infrastructure Canada 2030 Pipeline Funding

Massive public-works allocations of USD 24.75 billion for the Investing in Canada Infrastructure Program, USD 38.25 billion for Build Communities Strong, and USD 4.50 billion for the Housing Infrastructure Fund are locking in multi-year backlogs for structural steel, railings, and modular building frames.[2]Infrastructure Canada, “Investing in Canada Infrastructure Program,” infrastructure.gc.caThe Policy on Prioritizing Canadian Materials now obliges projects over USD 18.8 million to source domestic steel and aluminum, pushing fabricators to invest in traceability software and ISO 9001 systems or risk exclusion. Larger shops are acquiring niche specialists to add capacity without duplicating compliance overhead, while mills such as ArcelorMittal Dofasco plan USD 1.32 billion DRI-EAF upgrades that will feed low-carbon flat-rolled steel into these projects by 2028. Collectively, these measures funnel demand toward domestic value chains and raise the performance bar for suppliers. The funding stream, therefore, provides both a revenue floor and a consolidation catalyst for the Canada metal fabrication market.

Modular Fabrication for SMR & Green-Hydrogen Projects

Ontario Power Generation’s Darlington small modular reactor and HTEC’s USD 354 million hydrogen hub in British Columbia require nuclear-grade pressure vessels and cryogenic stainless-steel pipe spools that exceed conventional tolerances. BWXT has invested USD 60 million to expand capacity for 48 steam generators, while Westinghouse has signed supply MOUs with Canadian firms to localize AP300 components. Fabricators entering this space must secure ASME U-stamp or CSA N299 quality programs, adding both cost and long-term service revenue. Green-hydrogen projects such as World Energy GH2’s Newfoundland facility also demand embrittlement-resistant alloys, opening high-margin niches for qualified welders. Although the project pipeline is still emerging, its multidecade horizon offers a stable growth vector that offsets cyclical swings in traditional sectors.

Mandatory Buy Clean Procurement Raising Demand for High-Efficiency Equipment

Buy Clean rules require federal projects to disclose and often minimize embodied carbon, compelling fabricators to upgrade to fiber-laser cutters, all-electric press brakes, and energy-efficient welding systems that lower both operating costs and emissions. Equipment OEMs have responded by localizing production: TRUMPF opened a USD 30 million smart factory in Connecticut and will assemble press brakes for North America from summer 2026 to cut delivery times for Canadian buyers. AMADA’s U.S. plants are supplying higher-kilowatt VENTIS lasers that pair with automated load-unload towers, giving buyers turnkey packages that meet performance specifications under Buy Clean tenders. Smaller shops without capital budgets for such upgrades risk disqualification from lucrative public contracts, accelerating technology adoption and market share shifts toward early adopters. The regulation, therefore, acts as both a carrot and a stick in modernizing the Canada metal fabrication market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute skilled-labour deficit despite higher immigration targets | -0.9% | National, most acute in Ontario, Alberta, and British Columbia | Short term (≤ 2 years) |

| Escalating electricity tariffs & carbon levies increasing operating costs | -0.7% | National, highest impact in Alberta and Ontario (carbon-intensive operations) | Medium term (2-4 years) |

| Higher cost of capital amid sustained 2025-26 interest rates curbing SME capex | -0.5% | National, disproportionately affecting small and medium enterprises | Short term (≤ 2 years) |

| Cybersecurity & data-sovereignty compliance burden for connected CNC systems | -0.3% | National, concentrated in firms serving defence and critical infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Acute Skilled-Labor Deficit Despite Higher Immigration Targets

Statistics Canada shows the trades workforce shrank 5.7% between 2016 and 2021, even as structural-metal employment rose, leaving fewer welders and machinists to meet rising demand.[3]Statistics Canada, “2021 Census: Trades Workforce,” statcan.gc.ca Vacancy-to-hire ratios for welders tightened to 1.5 in 2025, forcing employers to pay 15-25% wage premiums or poach staff. Federal programs earmarking USD 56 million for Red Seal training cover only a fraction of the 1.4 million workers that Canadian Manufacturers & Exporters says will be needed by 2033. Shops are therefore fast-tracking robotic welding cells, yet many lack in-house integration skills, resulting in under-utilized assets and slower ROI. The talent gap thus acts as a drag on capacity expansion and could mute the growth trajectory of the Canada metal fabrication market.

Escalating Electricity Tariffs & Carbon Levies Increasing Operating Costs

The federal carbon price rose from USD 48 per tonne in 2023 toward a scheduled USD 128 by 2030, inflating power costs for laser-cutting, induction heating, and resistance-welding operations. Although the Decarbonization Incentive Program handed out USD 112.5 million to 38 projects in 2025, most grants covered only part of furnace upgrades or efficiency retrofits, leaving residual costs for smaller fabricators. Ontario and Alberta shops report monthly utility bills climbing 8-12% year over year, squeezing margins on fixed-price contracts. Steel price volatility deepens the strain, as hot-rolled coil posted double-digit percent swings during 2025, forcing just-in-time inventory strategies that increase exposure to spot energy prices. Persistently high operating costs therefore erode competitiveness and deter fresh capital investment in the Canada metal fabrication market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Automation Level: Labor Scarcity Accelerates Robotics

Automatic equipment captured 49.20% of the Canada metal fabrication market size in 2025. Labor shortages are pushing even small shops to install robotic welding cells that can run unattended overnight, multiplying output without adding headcount. ACOA’s USD 0.56 million grant helped Atelier Gérard Beaulieu triple its laser-cutting capacity and create sixty new jobs, proving that subsidized automation eases wage pressure.[4]Atlantic Canada Opportunities Agency, “AGB Laser-Cutting Expansion,” acoa-apec.gc.ca Early adopters also gain from the immediate expensing introduced in Budget 2025, which lets buyers deduct a fiber-laser purchase in year one instead of over five years.

Vacancy-to-hire ratios for welders tightened to 1.5 in 2025, so shops unable to recruit programmers often buy turnkey robotic cells that arrive pre-tuned to a standard part library. TRUMPF’s Connecticut smart factory will assemble press brakes for North America from mid-2026, cutting lead times for Canadian buyers to days rather than weeks. Automation, therefore, moves from “nice to have” to “must have,” anchoring the fastest 6.10% CAGR among all automation tiers through 2031.

By Equipment Type: Finishing and Handling Gain Momentum

Cutting systems accounted for 35.07% of the Canada metal fabrication market size in 2025, reflecting the installed base of fiber lasers across automotive and aerospace supply chains. Yet finishing, handling, and tooling units are forecast to rise at 7.01% annually because Buy Clean tenders now specify powder-coated surfaces with low-VOC paints that demand enclosed spray lines and robotic deburring. Groupe Support Plus used a USD 0.49 million repayable loan to install a laser, cutting robot, folding press, and bending cell, illustrating the one-stop equipment packages common in new tenders.

Energy costs also shape buying habits. All-electric press brakes use up to 50% less power than hydraulic predecessors, a key benefit when Ontario bills climbed 8-12% year over year. Material-handling robots that sort cut parts reduce back injuries and compensation premiums, helping owners justify six-figure investments. As turnkey automation becomes standard, OEMs that bundle laser, bend, and deburr cells under a single service contract edge ahead of niche tool suppliers.

By End-User Industry: Infrastructure Still Commands the Largest Slice

Construction and infrastructure represented 41.04% of the Canada metal fabrication market size in 2025, secured by USD 24.75 billion in Investing in Canada Infrastructure funding and strict domestic-content rules for steel. Structural beams, bridge railings, and transit-station panels drive steady plant loading, while the Policy on Prioritizing Canadian Materials raises demand for traceability software that smaller shops often lack.

The fastest 6.20% CAGR comes from the “others” bucket such as electronics, marine, rail, and data-center cooling, because firms are diversifying away from cyclical oil-and-gas work. Wabi Iron & Steel’s USD 2.44 million foundry upgrade will triple revenue by 2027 as critical minerals mining lifts demand for ore-handling gear. Similar niche plays in rail-car refurbishing and hydrogen compression widen the customer base and cushion revenue swings tied to housing cycles.

Geography Analysis

Ontario retained 44% of 2025 output because its automotive corridor and nuclear refurbishment programs supply year-round orders for precision sheet-metal, stamping, and ASME Section III components. Volkswagen’s USD 5.25 billion battery plant in St. Thomas and Stellantis–LG’s USD 3.75 billion cell factory in Windsor each require millions of welded busbar brackets and coolant trays, locking in multi-year purchase orders for local fabricators. GM’s USD 46 million Oshawa stamping upgrade and Martinrea’s USD 26.25 million press installation further concentrate demand along Highway 401.

Quebec ranks second, buoyed by aerospace clusters around Montréal and hydropower overhaul projects. Bombardier broke ground on a USD 75 million, 126,000 ft² business-jet center that will employ 330 staff by 2027, adding to the flow of formed aluminum skins and complex sub-assemblies. Hydro-Québec’s USD 150 billion 2035 Action Plan catalyzes transformer-tank and turbine-housing orders, while aluminium smelter investments in Deschambault feed local extrusion shops that supply green-building facades.

British Columbia is projected to grow fastest at 6.50% through 2031 on the back of LNG export terminals, hydrogen liquefiers, and remote-site modular construction. HTEC’s USD 354 million H2 Gateway alone calls for cryogenic stainless-steel piping and pressure-rated skids that regional fabricators are retooling to supply. PacifiCan’s USD 1.88 million IIoT grant to MAKR Group shows provincial focus on connected production lines that can validate quality in real time, a must for hydrogen service hardware. Together, these trends lift Western Canada’s profile from resource-extraction back office to clean-energy fabrication hub.

Competitive Landscape

Global OEMs dominate high-ticket lasers and press brakes, yet no single vendor tops 15%, so the Canada metal fabrication industry retains moderate concentration. TRUMPF’s USD 30 million smart factory in Connecticut lets it ship turnkey cells to Toronto in under 48 hours, eroding the legacy advantage of Asian imports that arrive in six weeks by sea. AMADA counters with U.S. production of 12 kW VENTIS lasers and all-electric press brakes, bundling on-site training and cloud analytics to raise switching costs.

Second-tier players focus on software rather than steel. AMADA’s Virtual Prototype Simulation System captures part-flow data for days, then prescribes the most efficient mix of laser, punch, and bend operations, often cutting cycle time by 30%. Suppliers that cannot integrate software, sensors, and service risk relegation to commodity status. Cyber-security rules add another moat: defence contracts will require Canadian Program for Cyber Security Certification Level 2 audits by 2027, favoring larger shops with in-house IT and squeezing mom-and-pop welders.

M&A has begun to rise. Larger integrators are buying niche specialists to bolt on painting, powder-coating, or robotic handling and sell turnkey “lights-out” lines under one invoice. Investors cite the 20-30% margin premium captured by shops that guarantee uptime and single-source warranty. As these roll-ups accelerate, the Canada metal fabrication market may see the top five suppliers control roughly 55% of equipment revenue by 2031, still far from oligopoly but tighter than today’s fragmented field.

Canada Metal Fabrication Equipment Industry Leaders

TRUMPF Canada Inc.

AMADA Canada Ltd.

DMG MORI Canada

Lincoln Electric Canada

Atlas Copco Manufacturing Canada

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Titus Steel received undisclosed federal funding to modernize its specialty-plate operation, aligning with Buy Clean rules that favor domestic mills.

- January 2026: Bombardier began building a USD 75 million jet-assembly center in Dorval, Québec, adding 330 jobs by 2027.

- January 2026: PacifiCan invested USD 1.88 million in MAKR Group for an IIoT production network that will cut scrap and energy use.

- September 2025: Hitachi Energy committed an extra USD 202.5 million to triple transformer output at its Varennes plant, creating 500 jobs.

Canada Metal Fabrication Equipment Market Report Scope

Metal fabrication equipment refers to a machine or tool used in the manufacturing of various metal products or components. This equipment is often utilized in different business segments, where the development of metal components plays a crucial role. Furthermore, due to various technological advancements in the industry, metal fabrication equipment produces better results than traditional equipment.

The Canada Metal Fabrication Equipment Market is segmented by service type (Machining and Cutting, Forming, Welding, and Other Service Type), product type (automatic, semi-automatic, and manual), and end-user industry (Manufacturing, Power and Utilities, Oil and Gas, Construction, and Other End User Industries). The report offers market size and forecast values (USD billion) for all the above segments.

By Automation Level

| Automatic |

| Semi-Automated Equipment |

| Manual Equipment |

By Equipment Type

| Cutting (Laser, Plasma, Waterjet, Oxy-fuel, etc.) |

| Machining (Lathes, Milling, Drilling, etc.) |

| Forming (Press Brakes, Bending Machines, etc.) |

| Welding (Arc Welding, Laser Welding, etc.) |

| Other Equipment Types (Finishing, Handling, Tooling, etc.) |

By End-User Industry

| Automotive & Transportation |

| Construction & Infrastructure |

| Oil & Gas / Energy |

| Aerospace & Defense |

| Heavy Machinery & Industrial Equipment |

| Others (Electronics, General Manufacturing, Marine, Railways, etc.) |

By Province

| Ontario |

| Québec |

| Alberta |

| British Columbia |

| Others |

| By Automation Level | Automatic |

| Semi-Automated Equipment | |

| Manual Equipment | |

| By Equipment Type | Cutting (Laser, Plasma, Waterjet, Oxy-fuel, etc.) |

| Machining (Lathes, Milling, Drilling, etc.) | |

| Forming (Press Brakes, Bending Machines, etc.) | |

| Welding (Arc Welding, Laser Welding, etc.) | |

| Other Equipment Types (Finishing, Handling, Tooling, etc.) | |

| By End-User Industry | Automotive & Transportation |

| Construction & Infrastructure | |

| Oil & Gas / Energy | |

| Aerospace & Defense | |

| Heavy Machinery & Industrial Equipment | |

| Others (Electronics, General Manufacturing, Marine, Railways, etc.) | |

| By Province | Ontario |

| Québec | |

| Alberta | |

| British Columbia | |

| Others |

Key Questions Answered in the Report

What is the projected value of the Canada metal fabrication market in 2031?

The market is forecast to reach USD 1.47 billion by 2031.

Which province is expected to grow fastest to 2031?

British Columbia is projected to post a 6.50% CAGR, driven by LNG and hydrogen projects.

Which automation tier shows the strongest growth?

Automatic equipment is advancing at a 6.10% CAGR as firms deploy robotic welding and lights-out cells.

What end-user segment supplies the largest revenue today?

Construction and infrastructure hold 41.04% of 2025 demand thanks to federal pipeline funding.

How are Buy Clean rules influencing equipment purchases?

They push shops toward energy-efficient lasers and press brakes that document low embodied carbon.

What is the biggest hurdle facing fabricators besides labor?

Rising electricity tariffs and carbon levies that lift operating costs 8-12% per year in some provinces.

Page last updated on: