U.S. Sterilization Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

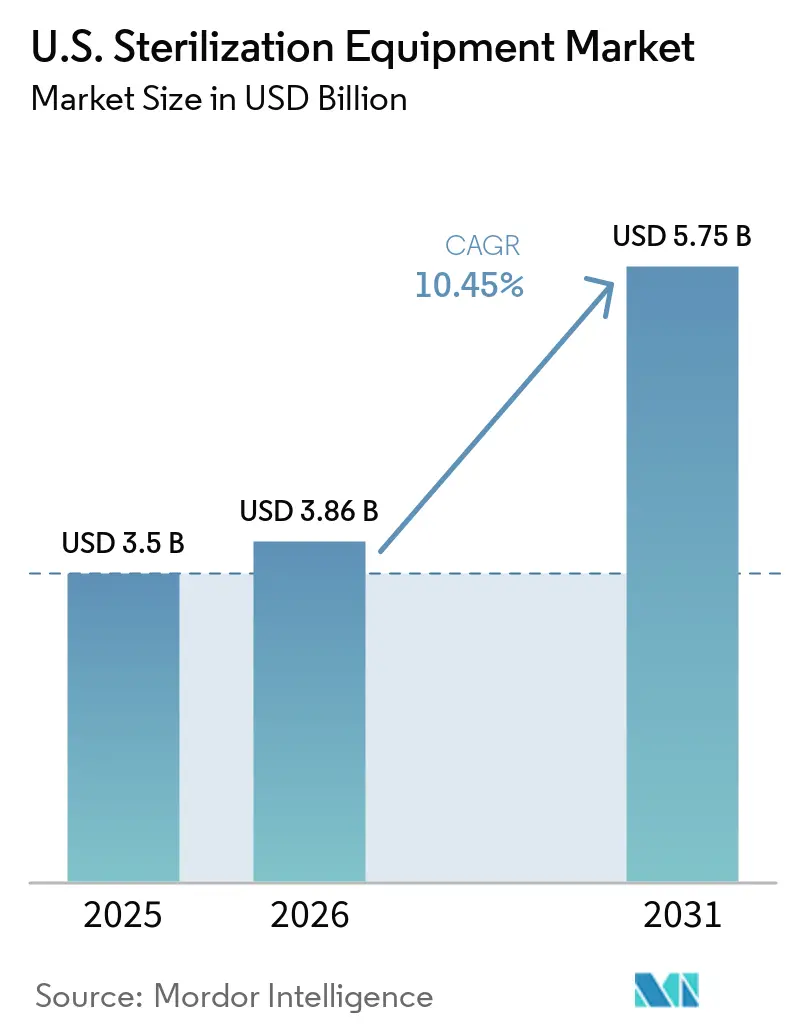

| Base Year Market Size (2025) | USD 3.5 Billion |

| Market Size (2026) | USD 3.86 Billion |

| Market Size (2031) | USD 5.75 Billion |

| Growth Rate (2026 - 2031) | 10.45% CAGR |

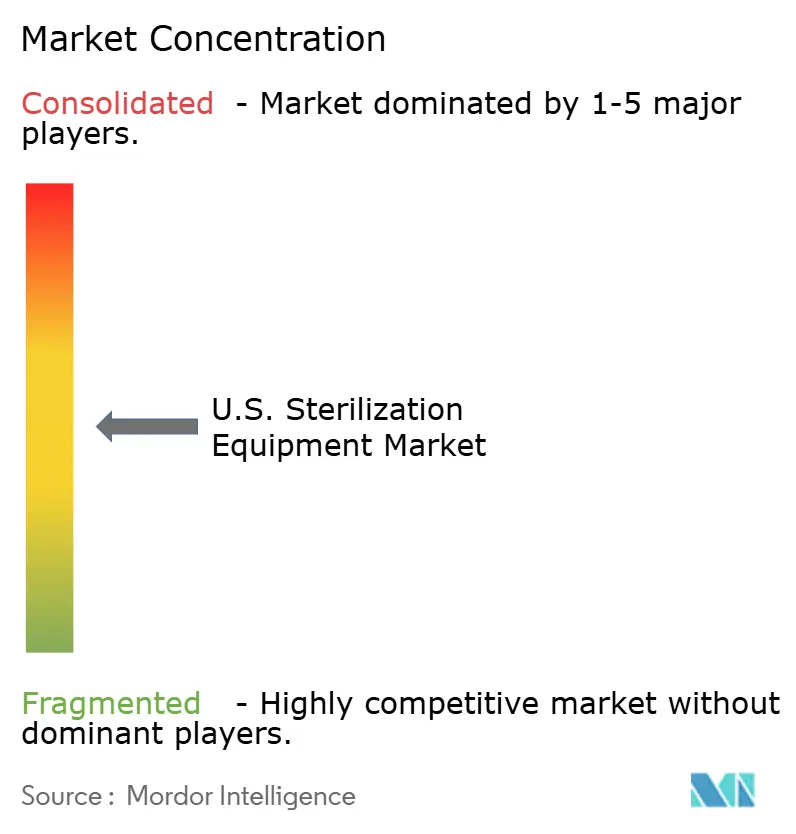

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

U.S. Sterilization Equipment Market Analysis by Mordor Intelligence

The U.S. Sterilization Equipment Market size was valued at USD 3.5 billion in 2025 and is estimated to grow from USD 3.86 billion in 2026 to reach USD 5.75 billion by 2031, at a CAGR of 10.45% during the forecast period (2026-2031).

Infection control remains a key spending priority. The CDC reports that 1 in 31 hospital patients in the United States acquires at least one healthcare-associated infection daily, contributing to nearly 72,000 deaths annually.[1]Centers for Disease Control and Prevention, “CDC Data Show Decline in Hospital-Related Infections in 2024,” CIDRAP, cidrap.umn.edu Despite declining infection rates, investments continue as lower CLABSI and CAUTI rates highlight the importance of validated sterilization and monitoring protocols. The shift toward ambulatory surgery settings is reshaping equipment demand. More procedures are transitioning to facilities requiring compact systems, faster cycles, and stronger documentation, managed by smaller sterile processing teams. This trend is driving innovation in equipment design and functionality. Uncertainty around ethylene oxide regulations and the increasing use of heat-sensitive instruments are influencing purchasing decisions.

Key Report Takeaways

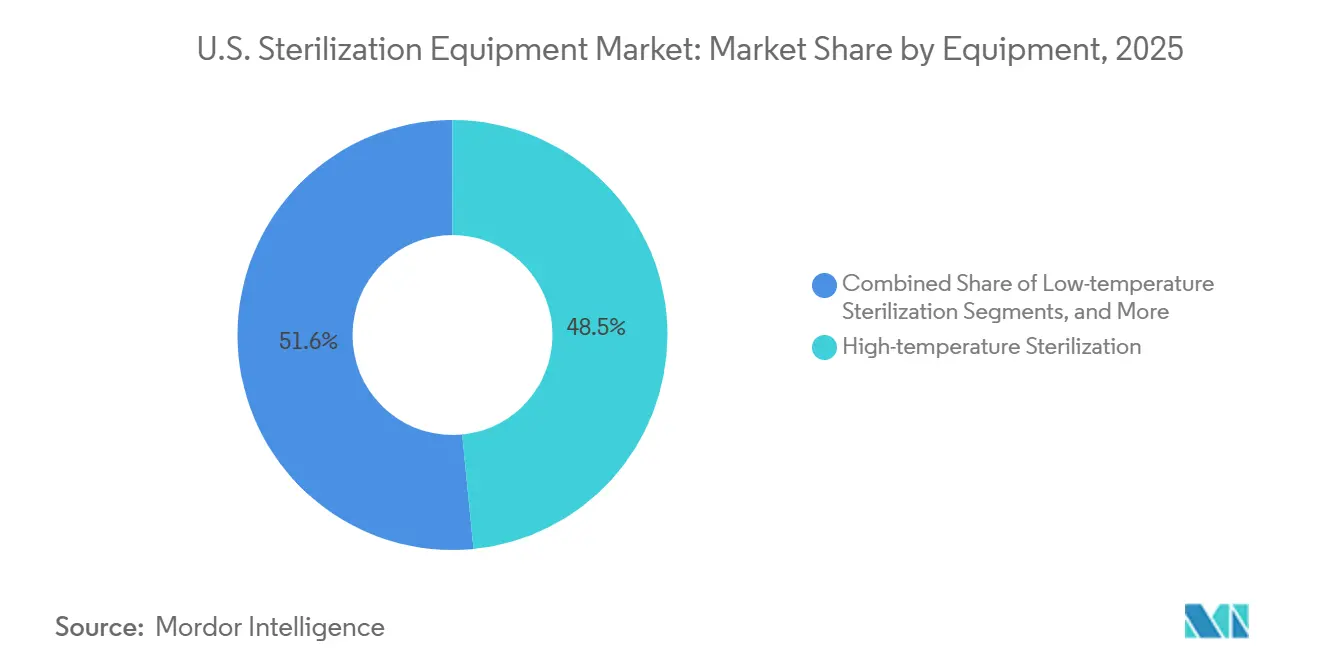

- By equipment, high-temperature sterilization held 48.45% of the U.S. sterilization equipment market share in 2025, while low-temperature sterilization is projected to grow at 11.28% CAGR through 2031.

- By end user, hospitals and clinics accounted for 39.45% of the U.S. sterilization equipment market size in 2025, while ambulatory surgery centers are expected to expand at 11.76% CAGR through 2031.

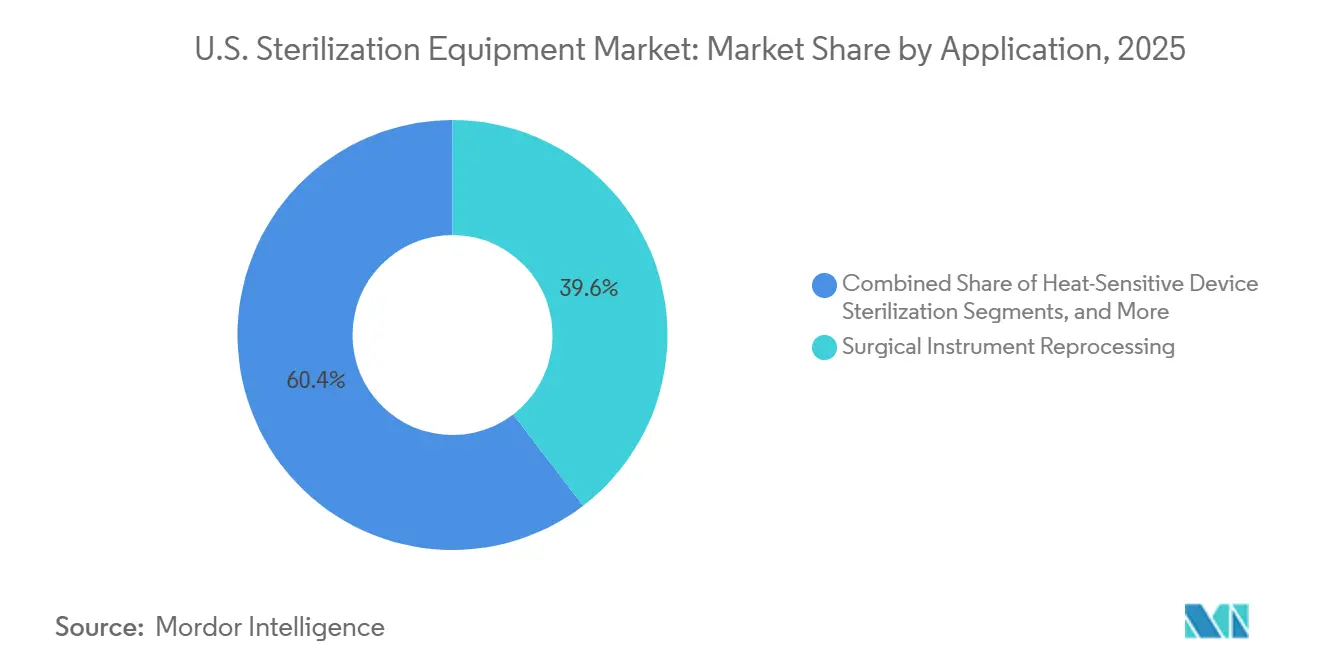

- By application, surgical instrument reprocessing represented 39.60% of the U.S. sterilization equipment market size in 2025, while heat-sensitive device sterilization is forecasted to advance at 12.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

U.S. Sterilization Equipment Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising procedure volumes and instrument complexity | +2.5% | National, with stronger gains in high ASC states such as California, Florida, and Texas | Short term (≤ 2 years) |

| HAI prevention and reprocessing compliance intensity | +2.8% | National, especially acute care hubs in the Northeast and Southeast | Medium term (2-4 years) |

| ASC expansion and compact sterilizer demand | +1.9% | National, led by suburban corridors in the Sun Belt and Mountain West | Medium term (2-4 years) |

| EtO transition driving low-temperature upgrades | +1.7% | National, with concentration in industrial sterilization corridors in the Midwest and Southeast | Medium term (2-4 years) |

| CSSD automation and traceability investments | +1.0% | Urban academic medical centers and large integrated delivery networks nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Procedure Volumes and Instrument Complexity Redefine Sterilization Throughput Requirements

The United States sterilization equipment market is evolving due to increasing surgical volumes and complexity in inpatient and outpatient settings. In 2025, the American Hospital Association reported a 20% higher survival rate for hospitalized surgical patients in early 2024 compared to pre-pandemic benchmarks, reflecting stricter sterility protocols.[2]American Hospital Association, “2026 Environmental Scan,” American Hospital Association, aha.org Higher acuity cases now require advanced instruments like robotic arms and multi-lumen devices, which demand more time and precision for reprocessing. Additionally, a 9.8% rise in outpatient visits in 2025 has increased instrument turnover, driving demand for high-throughput equipment and efficient workflows to optimize space and turnaround times.

HAI Prevention and Reprocessing Compliance Intensity Sustain Baseline Investment

Infection prevention requirements continue to sustain demand for sterilization equipment in the United States. CDC data showed healthcare-associated infections in acute care hospitals dropped from 132,913 in 2023 to 123,204 in 2024, indicating progress but highlighting the need for ongoing investment.[3]Centers for Disease Control and Prevention, “CDC Data Show Decline in Hospital-Related Infections in 2024,” CIDRAP, cidrap.umn.edu Hospitals must maintain improved infection outcomes, increasing the focus on monitoring, validation, and audit readiness. Updated AAMI guidance in 2025 raised standards for chemical and EtO sterilization, making outdated systems harder to justify during quality reviews and driving replacement demand.

ASC Expansion and Compact Sterilizer Demand Reshape Market Geography

The rise of ambulatory surgery centers (ASCs) is reshaping the United States sterilization equipment market. By Q4 2025, there were 10,494 ASCs nationwide, with 6,566 Medicare-certified, performing over 80% of surgeries. ASCs, operating with smaller teams and limited space, prioritize compact equipment and streamlined documentation.[4]ASC Data, “Q4 2025 ASC Insights Report, ASC Market Projected at USD 45.6B, Remains Balanced in Terms of Specialty Composition,” ASC News, ascnews.com High-growth states like California, Florida, and Texas are leading this trend. Meanwhile, inpatient days are projected to rise 10% by 2035, indicating simultaneous growth in hospital and ASC demand, which is diversifying vendor offerings to meet both scalability and compact system needs.

EtO Transition Driving Low-Temperature Equipment Upgrades

The United States sterilization equipment market is shifting toward low-temperature platforms due to uncertainties surrounding EtO regulations. Ethylene oxide sterilizes nearly 50% of medical devices in the country, approximately 20 billion annually, making regulatory changes impactful. In 2024, the EPA mandated over 90% emission reductions for 90 sterilization facilities, prompting stakeholders to explore alternatives. A 2026 proposal to revisit these rules underscores ongoing regulatory fluidity. Buyers are increasingly adopting hydrogen peroxide plasma and vaporized hydrogen peroxide systems to mitigate risks and support heat-sensitive devices, driving replacement demand beyond compliance needs.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High capital, validation, and utility retrofit burden | -0.3% | National, with the strongest pressure on community hospitals and independent ASCs with tighter budgets | Medium term (2-4 years) |

| EtO permitting and compliance-driven downtime risk | -0.1% | States with stricter air quality oversight such as California, Illinois, Texas, and Georgia | Medium term (2-4 years) |

| Single-use substitution reducing in-house reprocessing volume | -0.05% | National, especially in high volume device categories at large health systems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital, Validation, and Utility Retrofit Burden

High acquisition costs remain a significant challenge for providers requiring advanced sterilization platforms but operating with limited capital budgets. Large capacity low-temperature systems and automated CSSD lines often necessitate extensive validation, installation modifications, and utility upgrades, adding to the overall expense. Community hospitals and independent ASCs face additional burdens, such as prolonged revalidation, staff retraining, and workflow redesign.

EtO Permitting and Compliance-Driven Downtime Risk

EtO users encounter regulatory uncertainties that hinder fresh investments in this modality. The EPA's 2024 amendments tightened air toxic standards for commercial sterilizers, and ongoing revisions to the rule create further unpredictability. Facilities in states with stricter environmental oversight face heightened risks, including downtime, permitting delays, and additional monitoring requirements. While EtO remains preferred for certain device categories, these challenges are driving many buyers toward low-temperature alternatives, despite the associated validation and retraining efforts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment: Low-Temperature Platforms Gain Share in New Installations

In 2025, high-temperature sterilization held a 48.45% share of the United States sterilization equipment market, maintaining its position as the largest segment. Steam systems remained the preferred choice for heat-tolerant instruments, wrapped goods, and large surgical tray volumes due to their scalability and integration into central sterile workflows. However, their growth is steady rather than accelerating, as more instruments now include components incompatible with traditional steam cycles.

Low-temperature sterilization is the fastest-growing segment, projected to expand at an 11.28% CAGR through 2031 in the United States market. This growth is driven by the increasing use of robotic instruments, flexible scopes, and heat-sensitive devices requiring validated processing. Getinge’s introduction of the Poladus 150 VHP sterilizer and the expanded capacity of its GSS67N steam platform in 2026 reflect a shift toward addressing throughput and space efficiency needs.

By End User: ASCs Become the Fastest Expanding Customer Base

Hospitals and clinics accounted for 39.45% of the United States sterilization equipment market in 2025, making them the largest end-user group. These facilities rely on centralized sterile departments to handle large instrument volumes and support surgery and acute care needs. Large academic medical centers and integrated delivery networks remain key buyers, influencing platform adoption across hospital networks due to their focus on service consistency and validated workflows.

Ambulatory surgery centers (ASCs) are the fastest-growing end-user segment, forecast to grow at an 11.76% CAGR through 2031. With 10,494 centers reported in Q4 2025 and outpatient surgeries comprising over 80% of procedures, demand for sterilizers outside hospitals is rising. ASCs prioritize compact equipment, responsive service, and remote monitoring, while specialty clinics in dermatology, ophthalmology, and orthopedics are also gaining relevance.

By Application: Heat-Sensitive Device Processing Moves Up the Priority List

Surgical instrument reprocessing represented 39.60% of the United States sterilization equipment market in 2025, maintaining its position as the largest application segment. This reflects the essential need to decontaminate, sterilize, and document instruments and trays after every surgical procedure. Growth in this segment is steady due to the established infrastructure and workflows.

Heat-sensitive device sterilization is the fastest-growing application, expected to grow at a 12.35% CAGR through 2031 in the United States market. The rise in robotic systems, endoscopic accessories, and electronic components, which require validated sterile processing, is driving demand. Facilities are increasingly prioritizing modality flexibility, while terminal sterilization and aseptic processing remain critical in manufacturing and CDMO settings.

Geography Analysis

The sterilization equipment market in the United States exhibits regional demand variations due to differences in infrastructure density, outpatient expansion, and environmental regulations. The South, particularly Texas, Florida, and Georgia, leads growth, driven by population inflows, ASC expansion, and rising procedure demand. California, Florida, and Texas ranked as the top three states for Medicare-certified ASC counts and operating room capacity. This growth benefits equipment suppliers by increasing the installed base for compact systems, service contracts, and replacement cycles. Additionally, population growth and aging demographics in the South support both inpatient complexity and outpatient volume.

The Northeast and Midwest are key regions for large-format hospital sterilization systems and automation investments in the United States. These areas, with a high concentration of academic medical centers and integrated delivery networks, drive advanced CSSD spending. Getinge’s Automatiq platform launch in December 2025 targeted this market with robotics, conveyor systems, and traceability software for sterile reprocessing. In May 2026, STERIS announced a USD 60 million investment in a sterility assurance manufacturing plant in Mentor, Ohio, reinforcing the Midwest’s role in the domestic supply chain. Automation demand is higher in these regions due to the scale of instrument movement, staffing complexity, and documentation requirements.

Competitive Landscape

In the United States sterilization equipment market, STERIS plc and Getinge AB hold leading positions, while ASP, Tuttnauer, MATACHANA Group, and Belimed focus on niche segments based on modality and facility size. The competitive landscape is diverse, as large hospitals, ASCs, manufacturers, and specialty labs prioritize varying needs such as throughput, footprint, compliance support, and service coverage.

In 2026, STERIS focused on capacity expansion and portfolio growth. The company announced a USD 60 million investment in a new plant in Mentor, Ohio, expected to be operational by late 2027, to enhance sterility assurance capacity for healthcare and life sciences clients. Getinge advanced workflow optimization with Automatiq in December 2025 and expanded GSS67N validated throughput in April 2026, emphasizing productivity and traceability within sterile departments. These strategies reflect a focus on manufacturing depth, workflow integration, and category expansion.

Buyers increasingly value documentation quality and audit readiness alongside sterilization capacity. This shift enables smaller technology-driven firms to integrate into larger equipment ecosystems, maintaining competition below the top tier and reinforcing the market's concentrated yet accessible nature.

U.S. Sterilization Equipment Industry Leaders

STERIS plc

Getinge AB

Advanced Sterilization Products, Inc.

Andersen Products, LLC

Astell Scientific Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: STERIS invested USD 60 million in a new sterility assurance manufacturing plant in Mentor, Ohio, expected to begin operations by late 2027. The company also approved a USD 1 billion share buyback program and projected FY2027 revenue growth of 7% to 8%.

- April 2026: Advanced Sterilization Products partnered with ChemDAQ to enhance AAMI ST58-compliant hazardous gas detection and monitoring in sterile processing departments.

- April 2026: Getinge expanded the validated load capacity of its GSS67N steam sterilizer platform, enabling up to 24 trays and 600 lbs of FDA-cleared validated load within the same footprint.

- March 2026: The EPA proposed rolling back the 2024 NESHAP rule for EtO commercial sterilizers, removing permanent total enclosure requirements and related monitoring mandates, impacting nearly 90 facilities.

- March 2025: The FDA recognized updated AAMI sterilization standards, including ANSI/AAMI ST58:2024, ST24:2024, and TIR17:2024, setting a new technical benchmark for chemical sterilization, EtO systems, and materials compatibility in U.S. healthcare facilities.

U.S. Sterilization Equipment Market Report Scope

As per the scope of the report, sterilization equipment refers to any specialized medical, laboratory, or industrial device designed to completely eliminate, kill, or deactivate all forms of microbial life. This includes viruses, fungi, bacteria, and highly resilient bacterial endospores.

The U.S. sterilization equipment market is segmented by equipment, end-user, and application. By equipment, the market includes high-temperature sterilization (wet/steam sterilization and dry heat sterilization), low-temperature sterilization (ethylene oxide (ETO), hydrogen peroxide plasma, ozone, and other low-temperature methods), filtration sterilization, and ionizing radiation sterilization (e-beam, gamma, and other ionizing technologies). By end-user, the market is segmented into hospitals and clinics, ambulatory surgery centers, specialty clinics and office-based care, pharmaceutical and biopharmaceutical manufacturers, medical device manufacturers and CDMOs, and others. By application, the market is categorized into surgical instrument reprocessing, flexible endoscope reprocessing and sterilization, heat-sensitive device sterilization, terminal sterilization of finished medical devices, aseptic processing support and sterile transfer, and biohazard, media, and lab waste sterilization. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| High-temperature Sterilization | Wet/Steam Sterilization |

| Dry Heat Sterilization | |

| Low-temperature Sterilization | Ethylene Oxide (ETO) |

| Hydrogen Peroxide Plasma | |

| Ozone | |

| Other Low-temperature Methods | |

| Filtration Sterilization | |

| Ionizing Radiation Sterilization | E-beam |

| Gamma | |

| Other Ionizing Technologies |

| Hospitals and Clinics |

| Ambulatory Surgery Centers |

| Specialty Clinics And Office-Based Care |

| Pharmaceutical And Biopharmaceutical Manufacturers |

| Medical Device Manufacturers And CDMOs |

| Others |

| Surgical Instrument Reprocessing |

| Flexible Endoscope Reprocessing And Sterilization |

| Heat-Sensitive Device Sterilization |

| Terminal Sterilization Of Finished Medical Devices |

| Aseptic Processing Support And Sterile Transfer |

| Biohazard, Media, And Lab Waste Sterilization |

| By Equipment | High-temperature Sterilization | Wet/Steam Sterilization |

| Dry Heat Sterilization | ||

| Low-temperature Sterilization | Ethylene Oxide (ETO) | |

| Hydrogen Peroxide Plasma | ||

| Ozone | ||

| Other Low-temperature Methods | ||

| Filtration Sterilization | ||

| Ionizing Radiation Sterilization | E-beam | |

| Gamma | ||

| Other Ionizing Technologies | ||

| By End User | Hospitals and Clinics | |

| Ambulatory Surgery Centers | ||

| Specialty Clinics And Office-Based Care | ||

| Pharmaceutical And Biopharmaceutical Manufacturers | ||

| Medical Device Manufacturers And CDMOs | ||

| Others | ||

| By Application | Surgical Instrument Reprocessing | |

| Flexible Endoscope Reprocessing And Sterilization | ||

| Heat-Sensitive Device Sterilization | ||

| Terminal Sterilization Of Finished Medical Devices | ||

| Aseptic Processing Support And Sterile Transfer | ||

| Biohazard, Media, And Lab Waste Sterilization | ||

Key Questions Answered in the Report

What is the projected value of the U.S. sterilization equipment market by 2031?

The U.S. sterilization equipment market is projected to reach USD 5.57 billion by 2031, rising from USD 3.50 billion in 2026 at a CAGR of 10.45% during the forecast period.

Which end user is growing fastest in U.S. sterilization equipment demand?

Ambulatory surgery centers are the fastest-growing end user segment, with an expected CAGR of 11.76% through 2031, supported by rising outpatient surgery volumes and a growing national ASC base.

Which equipment segment leads the U.S. sterilization equipment market?

High-temperature sterilization led the market in 2025 with a 48.45% share, supported by the large installed base of steam systems in hospital sterile processing departments.

Why is low-temperature sterilization growing so quickly in the United States?

Low-temperature sterilization is expanding because hospitals and outpatient facilities are using more heat sensitive robotic, endoscopic, and electronic instruments that cannot be processed through standard steam cycles.

How important are healthcare associated infections to sterilization equipment demand?

They remain very important. CDC data cited in 2026 still showed 123,204 HAIs in acute care hospitals in 2024, which keeps infection prevention and reprocessing compliance high on hospital capital agendas.

What is changing competition among sterilization equipment suppliers in the U.S.?

Competition is shifting beyond base equipment toward automation, traceability, gas monitoring, software integration, and service support, as shown by moves from STERIS, Getinge, and ASP in 2025 and 2026.

Page last updated on: