Sterilization Wraps Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

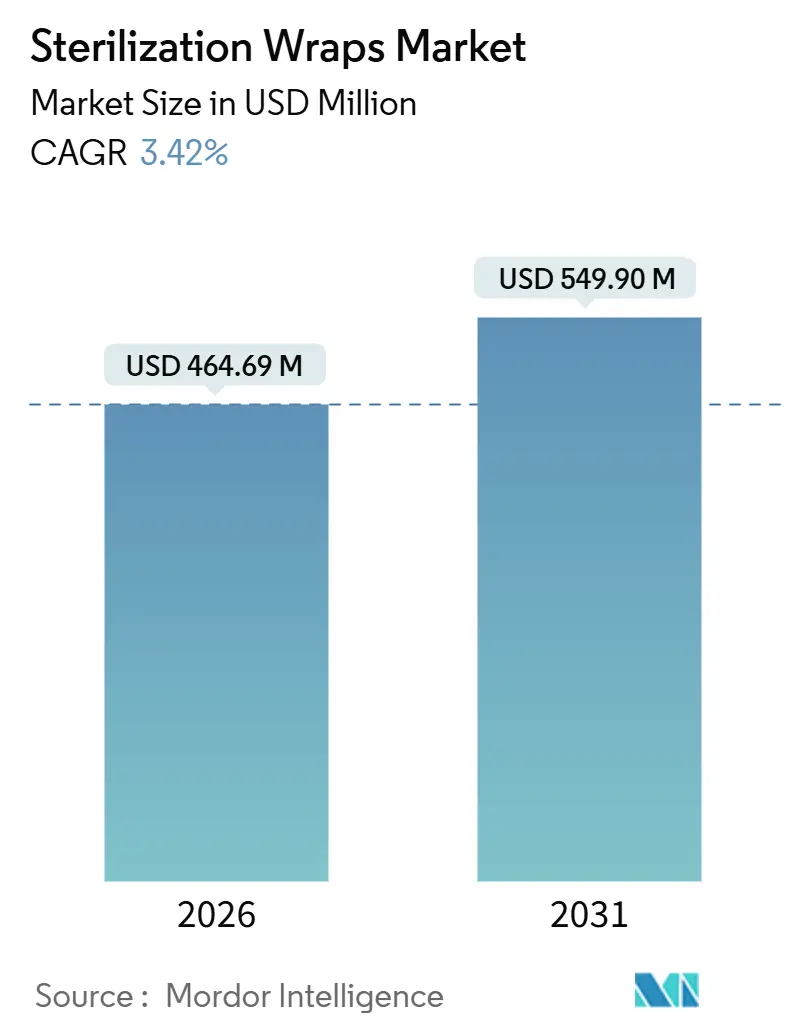

| Market Size (2026) | USD 464.69 Million |

| Market Size (2031) | USD 549.90 Million |

| Growth Rate (2026 - 2031) | 3.42% CAGR |

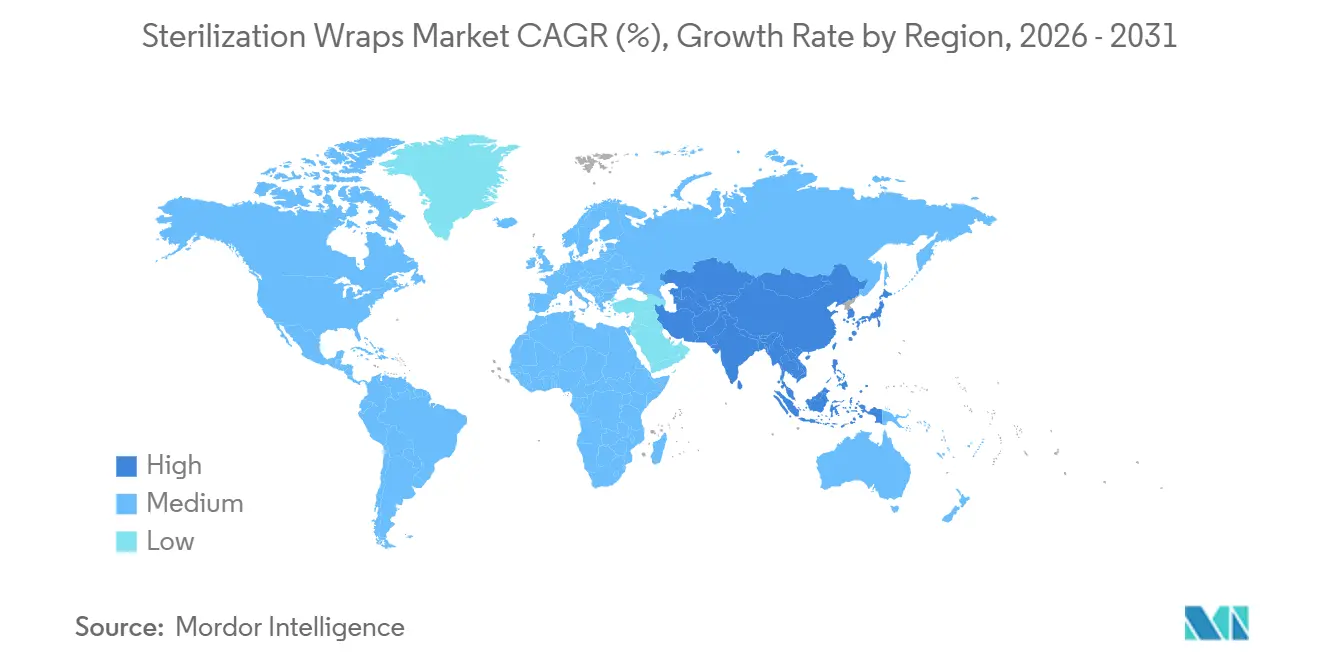

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sterilization Wraps Market Analysis by Mordor Intelligence

The Sterilization Wraps Market size is estimated at USD 464.69 million in 2026, and is expected to reach USD 549.90 million by 2031, at a CAGR of 3.42% during the forecast period (2026-2031).

Momentum stems from a rebound in surgical procedure volumes, wider adoption of low-temperature sterilizers, and tightening infection-control standards that demand validated sterile-barrier performance. Hospitals are weighing the carbon footprint of single-use supplies, prompting procurement teams to scrutinize wrap recyclability and resin origin alongside price. Polypropylene price swings between 2024 and 2025 underscored supply-risk exposure for synthetic wraps, while pulp-based alternatives benefited from more stable input costs. Vendor consolidation has harmonized spunbond-meltblown (SMS/SMMS) specifications worldwide, shrinking lead times but increasing buyer dependence on a small group of suppliers. These interlocking forces keep the sterilization wraps market on a steady yet sub-5% growth trajectory despite substitution pressure from reusable rigid containers.

Key Report Takeaways

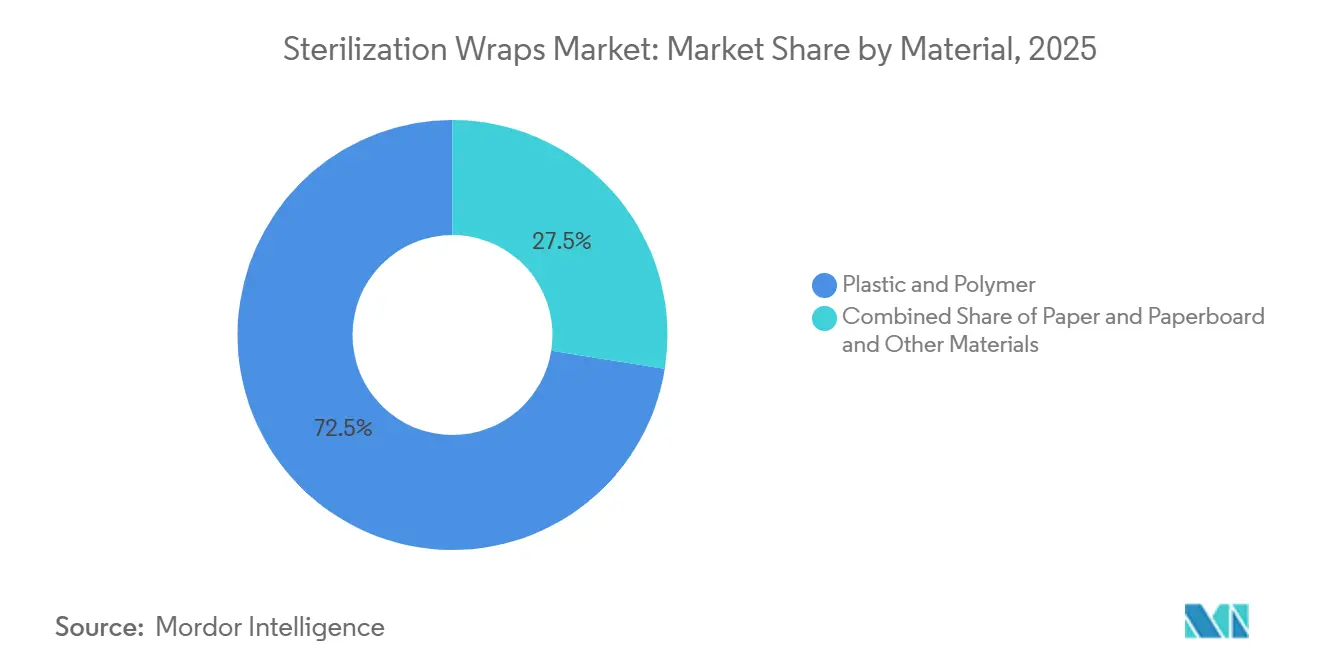

- By material, plastic and other polymer wraps led with 72.55% sterilization wraps market share in 2025, whereas paper and paperboard variants are forecast to expand at a 6.25% CAGR through 2031.

- By end user, hospitals and clinics accounted for 66.53% of 2025 revenue; ambulatory surgical centers are set to grow at a 6.85% CAGR through 2031.

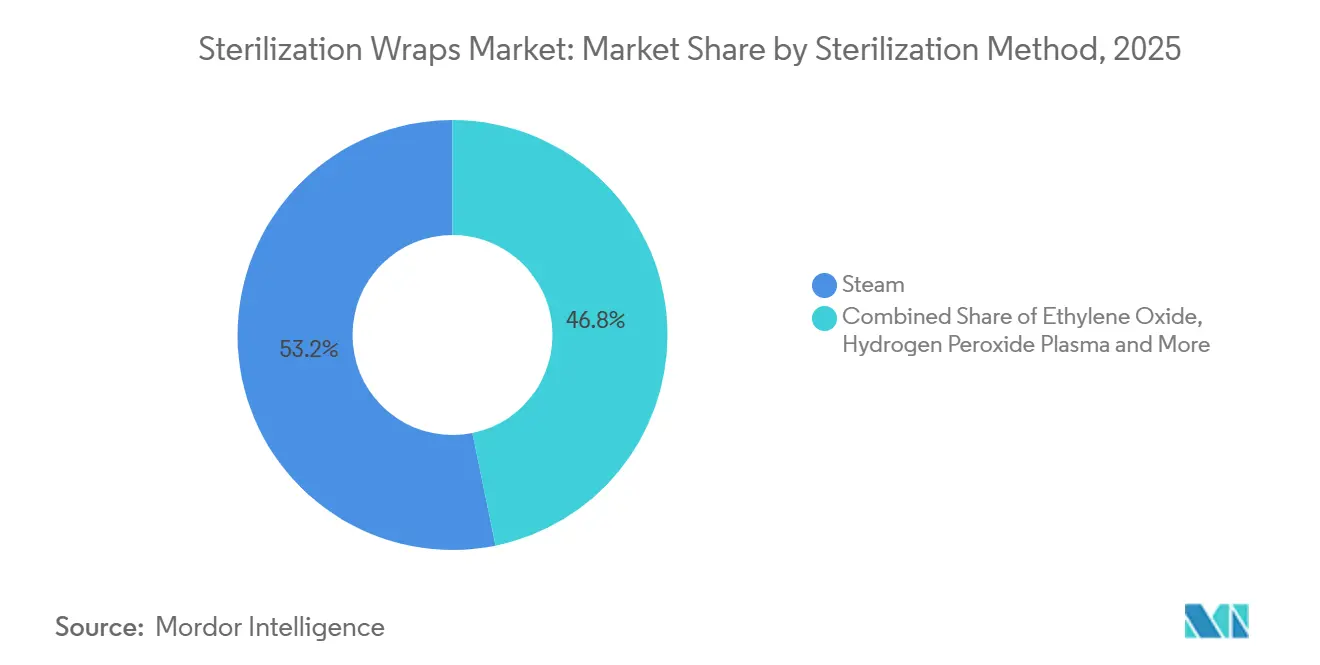

- By sterilization method, steam accounted for 53.23% of the 2025 volume, while hydrogen-peroxide plasma is projected to grow at a 7.55%.

- By geography, North America accounted for 38.13% of 2025 revenue, while Asia-Pacific is expected to log a 7.51% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sterilization Wraps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Surgical Procedure Volumes Worldwide | +0.8% | Global, with acute gains in Asia-Pacific and Middle East | Medium term (2-4 years) |

| Stringent Infection-Control Regulations in Acute-Care Facilities | +0.6% | North America & EU, extending to APAC core markets | Short term (≤ 2 years) |

| Shift From Reusable Textiles to Single-Use SMS & SMMS Wraps | +0.5% | Global, led by North America and Western Europe | Medium term (2-4 years) |

| Vendor Consolidation Driving Product Standardization & Global Roll-Outs | +0.4% | Global, particularly North America and Europe | Long term (≥ 4 years) |

| Hospital Decarbonization Targets Accelerating Demand for Recyclable Paper-Based Wraps | +0.3% | Europe and select North American health systems | Medium term (2-4 years) |

| Growth Of Hydrogen-Peroxide-Plasma Sterilizers in ASCs, Spurring Need for Compatible Synthetic Wraps | +0.2% | North America, with early adoption in urban ASC clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Surgical Procedure Volumes Worldwide

Global surgical throughput rebounded in 2024 after pandemic deferrals, with United States inpatient procedures up 4.2% and same-day surgeries up 6.1%. Each tray requires at least one wrap, and many facilities double-wrap to extend shelf life, anchoring baseline demand in the sterilization wraps market. The World Health Organization counted 12,400 new operating theaters added in lower-middle-income nations from 2020 to 2024, a 9% capacity jump that further expands addressable volume. Elective orthopedics and bariatrics, which use larger-format wraps, climbed 7.3% year-on-year across OECD hospitals, shifting the mix toward higher-priced SKUs. Approximately 28 million procedures occur annually in U.S. ambulatory surgical centers, and facility counts are rising 3.8% per year, ensuring durable growth for the sterilization wraps market.

Stringent Infection-Control Regulations in Acute-Care Facilities

The Centers for Disease Control and Prevention’s March 2024 update requires Class II devices to remain sterile for at least 6 months during ambient storage[1]Centers for Disease Control and Prevention, “Updated Sterilization Guidelines for Healthcare Facilities,” CDC.gov. The mandate pushes wraps to meet ASTM F1608 bacterial filtration standards and pass peel force validation, curbing low-cost imports with limited traceability. Europe enforces similar documentation under its Medical Device Regulation, prompting several second-tier converters to exit rather than fund quality-system upgrades. ISO 11607 remains the global benchmark, and a 2024 corrigendum clarified accelerated-aging protocols that affect paper wraps in particular. Financial penalties for surgical-site infections under U.S. value-based reimbursement models intensify hospital scrutiny of wrap performance, reinforcing premium demand within the sterilization wraps market.

Shift from Reusable Textiles to Single-Use SMS & SMMS Wraps

AAMI’s 2024 technical brief showed that reusable textiles require 18–22 minutes of technician time, compared with under 2 minutes for single-use disposal. SMS and SMMS nonwovens deliver sub-micron filtration while remaining lint-free, meeting AAMI PB70 Level 4 liquid-barrier performance. Berry Global’s healthcare films division grew revenue 11.2% in 2024, reflecting ongoing textile-to-synthetic conversion. Infection-prevention surveys reveal 82% of practitioners consider single-use wraps more reliable than textiles, sustaining conversion momentum in the sterilization wraps market.

Vendor Consolidation Driving Product Standardization & Global Roll-Outs

Cardinal Health, Medline Industries, and Owens & Minor collectively own 45% of North American wrap revenue, enabling global contracts but concentrating supply risk. Cardinal Health’s Medical segment posted 5.8% organic growth in 2024 on standardized wrap kits. A 2024 fire at a Midwest nonwoven mill stalled production for six weeks, forcing group-purchasing organizations to activate secondary suppliers at premium rates. Standardized SKUs accelerate ISO-11607 validation yet expose buyers to polypropylene cost volatility, a dual effect that shapes competitive dynamics in the sterilization wraps market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Polypropylene & Pulp Prices Inflating Wrap Costs | -0.4% | Global, with acute exposure in Asia-Pacific converters | Short term (≤ 2 years) |

| Rising Medical-Plastic Waste Regulations Limiting Single-Use Volumes | -0.3% | Europe, select U.S. states, and emerging APAC markets | Medium term (2-4 years) |

| Emergence of Rigid Container Systems Cannibalizing High-Value Wrap Demand | -0.2% | North America and Europe, concentrated in high-volume surgical specialties | Long term (≥ 4 years) |

| Validation Burden for New Wrap Materials with Low-Temperature Sterilizers | -0.2% | Global, affecting paper-based and bio-based wrap entrants | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Polypropylene & Pulp Prices Inflating Wrap Costs

Spot polypropylene hit USD 1,510 per metric ton in mid-2025 before easing to USD 1,380, a 28% swing that compressed converter margins. Medical-grade kraft pulp moved similarly, rising 19% in 2024. Contract cover shields only about two-thirds of demand, leaving converters exposed on the remainder. Some Tier 2 suppliers passed mid-cycle increases through to customers, prompting health systems to trial thinner gauges or reduce double-wrapping, actions that can endanger sterility assurance if not validated.

Rising Medical-Plastic Waste Regulations Limiting Single-Use Volumes

The European Union extended its Single-Use Plastics Directive to healthcare in 2024, aiming to reduce waste by 25% by 2030[2]European Commission, “Single-Use Plastics Directive: Healthcare Applications,” ec.europa.eu. The United States, including California and New York, has enacted extended producer responsibility fees on disposable medical devices. China’s draft rules would levy CNY 0.50 per polypropylene wrap from 2027. These policies raise the total cost of ownership for disposables and accelerate trials of reusable containers, tempering expansion in the sterilization wraps market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Paper Gains Momentum as Carbon Targets Tighten

Plastic and polymer substrates held a 72.55% share of the sterilization wrap market in 2025 and remain indispensable for high-temperature steam, ethylene oxide, and plasma cycles due to their consistent tensile properties and ISO 11607 compliance. However, paper and paperboard wraps are projected to grow 6.25% annually through 2031, outpacing synthetics by nearly two points as European and select U.S. hospitals integrate carbon scoring into tenders. The sterilization wraps market size for paper-based solutions is forecast to expand steadily, supported by Ahlstrom’s FSC-certified kraft launch that channels post-use material into recycling streams. Dupont’s Tyvek, a flash-spun polyethylene, offers a hybrid option with lower carbon intensity than polypropylene, though its 30–40% price premium limits penetration beyond implant packaging.

Second-tier converters continue to explore bio-based polymers, but high validation costs and uncertain shelf-life performance restrain scale-up. Steam cycles over 132 °C remain a technical hurdle for paper, confining adoption to gravity displacement and ethylene oxide processes. Still, procurement policies that assign up to 30% tender weight to sustainability tilt future growth toward recyclable substrates, safeguarding paper’s ascent within the sterilization wraps market.

By End User: Ambulatory Surgical Centers Lead Growth Curve

Hospitals and clinics accounted for 66.53% of 2025 revenue, anchored by 28 million inpatient procedures and double-wrapping protocols that boost wrap consumption. Yet ambulatory surgical centers, aided by payer steering toward outpatient settings, are projected to grow at a 6.85% CAGR and represent the fastest-expanding demand pool in the sterilization wraps market. Each United States ASC cycles 40–60 trays daily, consuming up to 22,000 wraps per year. Hydrogen-peroxide plasma sterilizers dominate ASC sterile processing because 28- to 75-minute cycles facilitate same-day instrument turnaround, reinforcing SMS/SMMS demand. Long-term acute-care hospitals, dental clinics, and veterinary practices contribute niche volume but grow at a slower clip, constrained by limited surgical-suite expansion.

Value-based purchasing penalties for surgical-site infections drive hospitals to favor wraps with batch-level traceability and ISO 13485 quality-system certification. These premium attributes, combined with supplier consolidation, sustain pricing power despite competitive pressure from rigid containers. As ASCs multiply and adopt standardized cellulose-free wraps, their influence on product design and contract specifications will intensify across the sterilization wraps market.

By Sterilization Method: Plasma Systems Claim Future Share

Steam accounted for 53.23% of 2025 sterilization cycles and remains the economic workhorse for heat-stable instruments. The sterilization wraps market size tied to steam applications will rise modestly in line with overall surgery volumes, yet its share will gradually cede ground to hydrogen-peroxide plasma. The plasma segment is forecast to post a 7.55% CAGR, catalyzed by ISO 22441’s Category A status and ASC demand for rapid turnaround. Plasma-compatible wraps must be cellulose-free to avoid peroxide absorption, favoring SMS/SMMS substrates and limiting the role of paper in this modality.

Ethylene oxide continues to process roughly half of heat-sensitive devices at OEM plants, but regulatory scrutiny over emissions and extended validation timelines impede hospital adoption. Gamma and electron-beam sterilization occupy niche roles for pre-sterilized implants and disposable kits, requiring radiation-stabilized materials. Ozone, peracetic acid, and formaldehyde remain subscale alternatives with limited impact on the sterilization wraps market share outlook.

Geography Analysis

North America accounted for 38.13% of revenue in 2025, driven by high surgical throughput, strict infection-control mandates, and early adoption of cellulose-free wraps. CMS logged a 4.2% rise in inpatient surgical discharges in 2024, maintaining core demand even as rigid containers displaced premium wraps in orthopedic and cardiovascular practice. More than 6,150 ASCs in the United States grew 3.8% in 2024, reinforcing SMS/SMMS demand. Canada and Mexico expand more gradually but are benefiting from public investments in operating-room capacity.

Europe’s sterilization wraps market is smaller in absolute terms yet uniquely shaped by aggressive decarbonization targets and single-use plastic levies. Germany, the United Kingdom, France, Italy, and Spain account for roughly two-thirds of regional demand. The EU’s 2024 directive extension drove trials of recyclable paper wraps that cost 15–25% more yet score higher on carbon assessments. Hospitals in Scandinavia and the Netherlands now include carbon metrics explicitly in tenders, accelerating pilot deployments of FSC-certified paper.

Asia-Pacific is poised for the fastest expansion, with a 7.51% CAGR projected through 2031 as China, India, and Southeast Asia add surgical infrastructure. The WHO documented 12,400 new operating theaters in the region from 2020–2024. Draft Chinese regulations that label polypropylene wraps “restricted medical plastics” from 2027 could nudge high-volume hospitals toward rigid containers or recyclable substrates. Japan and Australia remain steady adopters but experience substitution risk in high-volume specialties due to containers.

The Middle East and Africa, and South America contribute smaller shares yet register localized growth. Gulf Cooperation Council nations are building JCI-accredited hospitals that specify ISO 11607-compliant wraps from global suppliers. South Africa’s tertiary centers and Brazil’s private hospitals are replacing textiles with single-use wraps, though budget and tariff complexities slow penetration. Currency volatility in several markets complicates long-term polypropylene supply contracts, pushing some buyers toward pulp-based alternatives that offer greater pricing stability

Competitive Landscape

The market’s top five vendors, Cardinal Health, Medline Industries, Owens & Minor (Halyard Health), Kimberly-Clark, and STERIS, account for a significant share of global revenue, indicating moderate concentration. Cardinal Health realized 5.8% organic growth in its Medical segment in 2024 by bundling standardized wrap kits[3]Cardinal Health, “Fiscal 2024 Form 10-K,” cardinalhealth.com. STERIS leveraged its installed base of sterilizers to drive 16.2% growth in consumables, underscoring the cross-selling benefits of equipment integration. Berry Global, a key polypropylene film supplier, reported an 11.2% revenue increase in 2024, underscoring upstream influence on downstream wrap pricing.

Regional specialists fill niches with gamma-compatible wraps or ultra-lightweight papers for minimally invasive sets but often lack ISO 13485 certification, limiting tender eligibility in North America and Europe. Sustainability differentiation is emerging: Ahlstrom markets FSC-certified kraft, while Kimberly-Clark pilots post-consumer recycled polypropylene. Validation cost, estimated at USD 50,000–150,000 per material-sterilizer pairing, remains a barrier to new entrants. Container makers add indirect pressure: Getinge’s 2024 consumables revenue increased 14.6% on plasma systems, while its rigid-container sales grew double digits. These dynamics keep competitive intensity moderate but push incumbents to invest in eco-friendly substrates and digital traceability.

Sterilization Wraps Industry Leaders

Cardinal Health

Medline Industries

Owens & Minor (Halyard Health)

Kimberly-Clark

STERIS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Healthmark, a Getinge company, introduced SafeGuard Dry, a sterilization wrap formulated to reduce wet-pack incidence in sterile processing departments.

- January 2024: Ahlstrom secured FDA 510(k) clearance for Reliance Fusion, a next-generation wrap designed to accelerate tray turnaround in hospital sterilization units.

Global Sterilization Wraps Market Report Scope

As per the report's scope, sterilization wraps are protective barrier materials used to enclose surgical instruments, trays, and medical devices before they undergo steam, EO, or plasma sterilization. Their job is to keep the contents sterile from the moment they leave the sterilizer until point‑of‑use, preventing microbial contamination, dust, and moisture ingress. They are typically made from nonwoven polypropylene, cellulose blends, or reinforced multilayer materials that allow sterilant penetration but block microorganisms. In hospitals, they are a core part of CSSD sterile packaging systems and are validated for strength, breathability, and microbial barrier performance.

The sterilization wraps market segmentation includes material, end user, sterilization method, and geography. By material, the market is segmented into plastic & polymer, paper & paperboard, and other materials. By end user, the market is segmented into hospitals & clinics, ambulatory surgical centers, and other healthcare facilities. By sterilization method, the market is segmented into steam, ethylene oxide (EtO), hydrogen peroxide plasma, gamma/E-beam, and others. By geography, the global market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Plastic & Polymer |

| Paper & Paperboard |

| Other Materials |

| Hospitals & Clinics |

| Ambulatory Surgical Centers |

| Other Healthcare Facilities |

| Steam |

| Ethylene Oxide (EtO) |

| Hydrogen Peroxide Plasma |

| Gamma / E-Beam |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Material | Plastic & Polymer | |

| Paper & Paperboard | ||

| Other Materials | ||

| By End User | Hospitals & Clinics | |

| Ambulatory Surgical Centers | ||

| Other Healthcare Facilities | ||

| By Sterilization Method | Steam | |

| Ethylene Oxide (EtO) | ||

| Hydrogen Peroxide Plasma | ||

| Gamma / E-Beam | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the sterilization wraps market in 2026?

The sterilization wraps market size is USD 464.69 million in 2026 and is forecast to reach USD 549.9 million by 2031.

Which material segment is growing fastest?

Paper and paperboard wraps are projected to expand at a 6.25% CAGR as hospitals weigh recyclability and carbon scoring in purchasing decisions.

Why are ambulatory surgical centers important for wrap demand?

ASCs are expanding procedure volumes at 3.8% annually and favor hydrogen-peroxide plasma sterilizers, which require cellulose-free SMS/SMMS wraps.

What is driving adoption of hydrogen-peroxide plasma sterilization?

ISO 22441’s Category A designation and cycle times under 75 minutes support rapid instrument turnaround, spurring demand for compatible wraps.

How are sustainability regulations affecting single-use wraps?

EU and U.S. rules impose waste-reduction targets and producer-responsibility fees, nudging hospitals toward recyclable paper wraps or reusable containers.

Page last updated on: