Low Temperature Sterilization Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

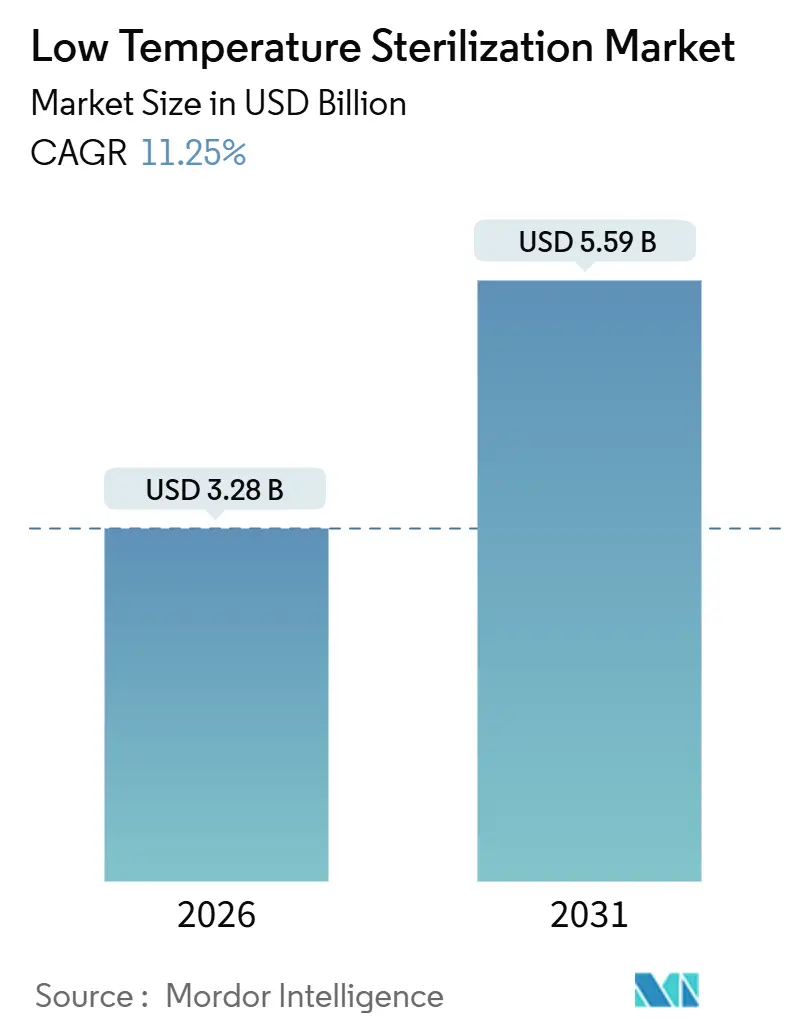

| Market Size (2026) | USD 3.28 Billion |

| Market Size (2031) | USD 5.59 Billion |

| Growth Rate (2026 - 2031) | 11.25% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

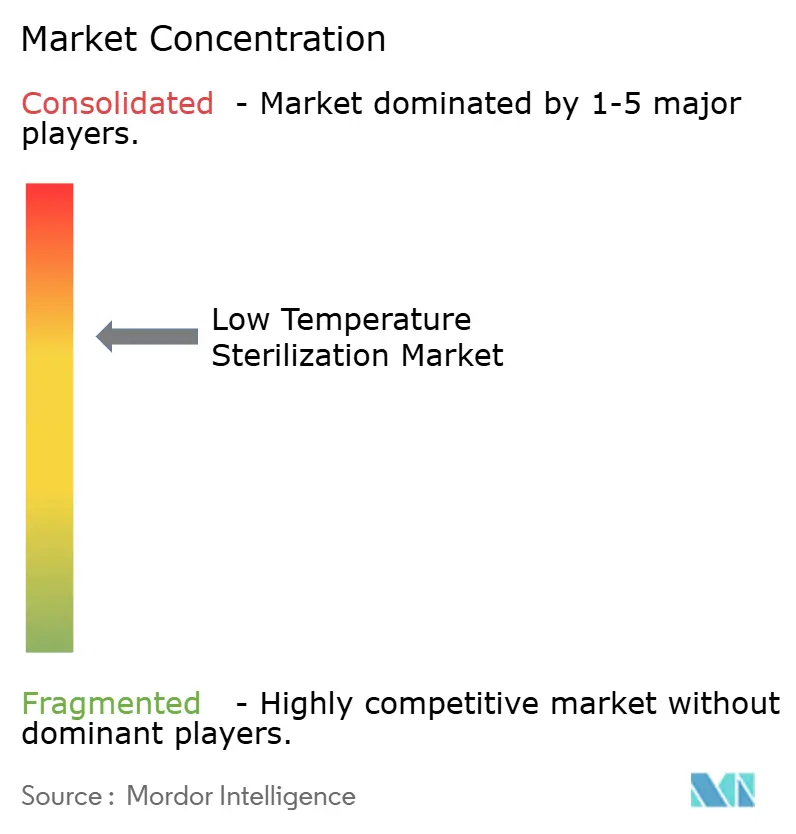

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Low Temperature Sterilization Market Analysis by Mordor Intelligence

The low temperature sterilization market size is estimated at USD 3.28 billion in 2026 and is projected to reach USD 5.59 billion by 2031, growing at a CAGR of 4.71%. Growth stems from hospitals and contract sterilizers shifting away from steam autoclaves toward ethylene oxide, hydrogen peroxide gas-plasma, and vaporized hydrogen peroxide systems that protect heat-sensitive endoscopes, robotically articulated tools, and polymer-based surgical instruments[1]U.S. Food and Drug Administration, “Vaporized Hydrogen Peroxide Sterilization. Demand is further buoyed by regulatory pressure tightening ethylene oxide emission limits, accelerating technology substitution toward hydrogen-peroxide platforms[2]U.S. Environmental Protection Agency, “Ethylene Oxide Emissions Standards for Sterilization Facilities. Asia-Pacific contract hubs are expanding capacity to serve Japanese and Chinese device exporters, while North American ambulatory surgical centers invest in rapid-cycle systems to turn instruments around in under 75 minutes[3]STERIS plc, “Investor Presentations 2024–2025. Integration of IoT-enabled analytics is reducing documentation errors and downtime, prompting hospitals to favor vendors that bundle hardware with software-as-a-service dashboards[4]Getinge AB, “Integrated Workflow Solutions. Competitive intensity has risen as distributors and equipment makers pursue mergers that combine sterilization hardware, consumables, and cycle-monitoring software into one offering.

Key Report Takeaways

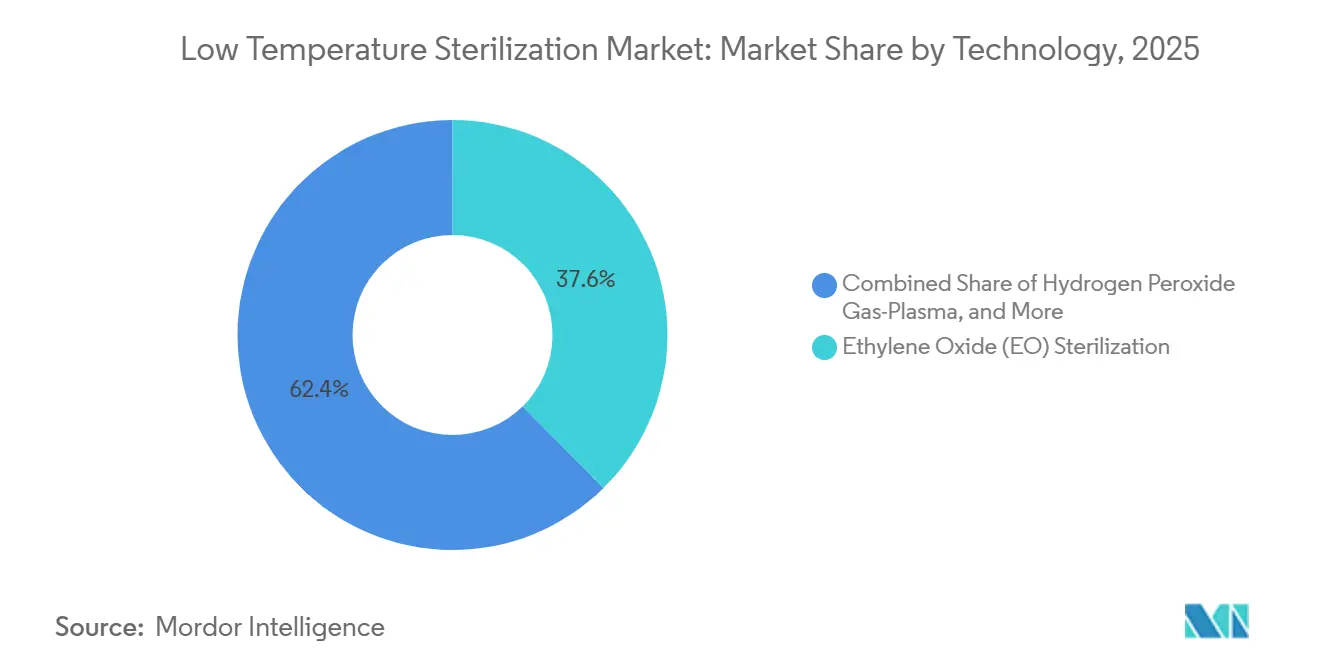

- By technology, ethylene oxide held 37.55% of the low temperature sterilization market share in 2025. Hydrogen peroxide gas-plasma is expanding at a 12.25% CAGR through 2031.

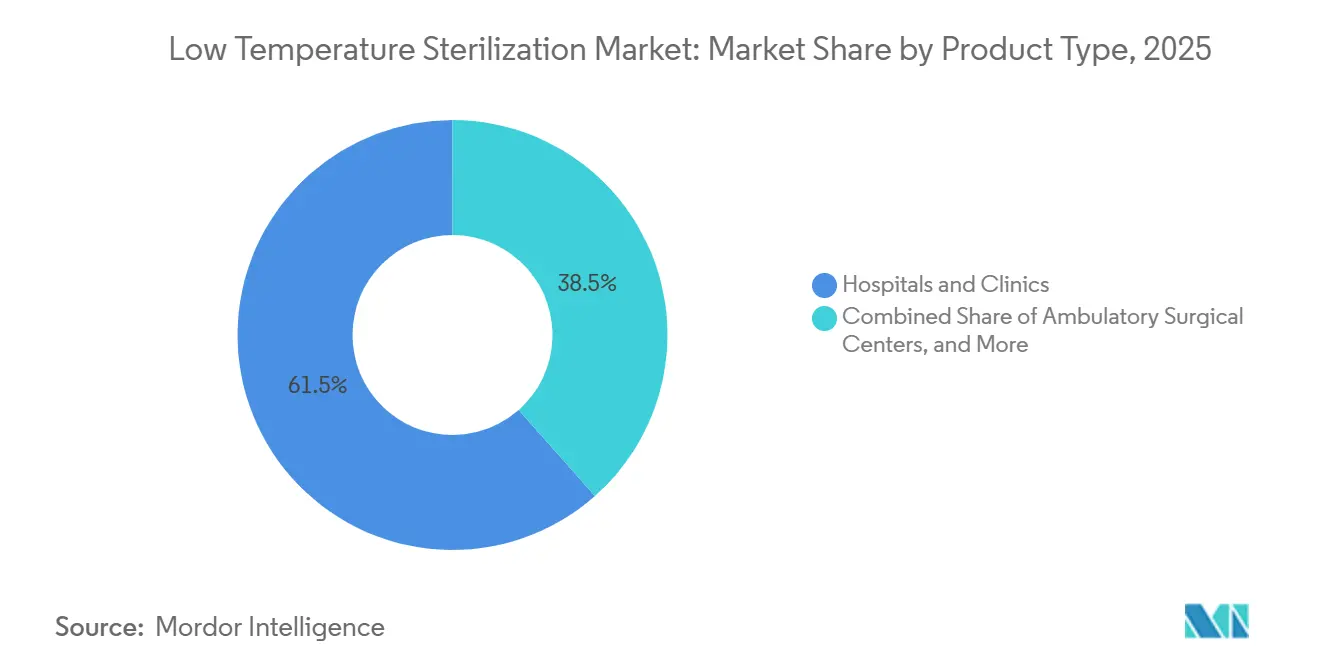

- By end user, hospitals and clinics accounted for the largest revenue share at 61.53% in 2025. Contract sterilizers are forecast to grow at an 11.85% CAGR to 2031.

- By application, reusable medical devices accounted for 35.23% of the low temperature sterilization market size in 2025. Single-use disposables pre-pack sterilization is advancing at a 12.55% CAGR through 2031.

- By geography, North America captured 36.25% of 2025 revenue; Asia-Pacific is projected to post a 12.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Low Temperature Sterilization Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Healthcare-Associated Infections and Surgical Volume | +2.8% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Regulatory Crackdown on Ethylene Oxide Emissions Spurring Uptake of Hydrogen Peroxide And Plasma Systems | +3.1% | North America, Europe, APAC spillover | Short term (≤ 2 years) |

| Rapid Capacity Additions in APAC Contract-Sterilization Hubs | +2.2% | Asia-Pacific | Medium term (2-4 years) |

| Integration of IoT-Enabled Cycle Analytics Improving Sterile-Processing Throughput | +1.5% | North America, Europe, Tier-1 APAC | Long term (≥ 4 years) |

| Growing Demand for Endoscope-Safe, Low-Temperature Methods in Minimally Invasive Surgery | +2.0% | Global, high in North America and Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Healthcare-Associated Infections and Surgical Volume

Healthcare-associated infections cost U.S. hospitals more than USD 28 billion annually, and surgical site infections account for almost one-third of those infections[5]Centers for Disease Control and Prevention, “NHSN Report 2024. Deferred orthopedic and cardiovascular procedures rebounded in 2024, driving a 12% jump in inpatient surgeries and straining legacy steam sterilization capacity that can damage heat-sensitive robotics and articulated instruments. Low-temperature modalities maintain polymer strength, lens clarity, and electrical integrity without the 121 °C exposure that degrades advanced devices. United Kingdom guidance issued in March 2025 now requires flexible endoscopes to undergo low-temperature sterilization or high-level disinfection within 4 hours of use, eliminating manual reprocessing backlogs. As elective surgery volumes normalize, automated, traceable systems that meet these stricter timelines will continue to displace labor-intensive manual methods in hospitals worldwide.

Regulatory Crackdown on Ethylene Oxide Emissions Spurring Uptake of Hydrogen Peroxide and Plasma Systems

The U.S. Environmental Protection Agency cut permissible ethylene oxide emissions from commercial sterilizers to 0.2 ppm, averaged over 12 months, in March 2024, and mandated continuous monitoring by December 2027. Compliance retrofits range from USD 2 million to USD 8 million, prompting operators to idle legacy chambers and install hydrogen peroxide vapor systems that generate no carcinogenic off-gas. In parallel, the Food and Drug Administration’s January 2024 recognition of vaporized hydrogen peroxide as an Established Category A method shortened 510(k) review times by roughly 90 days, incentivizing device designers to prioritize hydrogen peroxide compatibility. European regulators harmonized residual-limit guidance with ISO 10993-7 in October 2024, signaling trans-Atlantic alignment that simplifies validation for multinationals. Together, these moves accelerate substitution toward plasma and vapor technologies despite ethylene oxide’s superior material compatibility for certain catheters and paper packaging.

Rapid Capacity Additions in APAC Contract-Sterilization Hubs

STERIS added 48 ethylene oxide and hydrogen peroxide chambers across Singapore, Malaysia, and Thailand between January 2024 and September 2025, lifting regional throughput by 12 million device units annually. Southeast Asian labor costs run roughly 40% below Japan, while new GMP certification pathways in Singapore cut approval times to nine months, attracting overseas device firms seeking faster market entry. Japan’s aging population pushed total knee arthroplasty procedures up 9% in 2024, yet domestic sterilization capacity remains constrained by stringent environmental permits. Contract hubs absorb this overflow, bundling multilingual regulatory documentation with validation services that small manufacturers cannot fund internally. The result is a network of APAC facilities that can flexibly switch between sterilization modes, ethylene oxide for cellulosic packaging, and hydrogen peroxide plasma for rapid-turnaround hospital sets, while filling global supply gaps.

Integration of IoT-Enabled Cycle Analytics Improving Sterile Processing Department Throughput

Getinge’s 8668 washer-disinfectant embeds sensors that monitor temperature, detergent concentration, and cycle time, transmitting encrypted data to cloud dashboards. A 14-hospital study showed a 28% drop in documentation errors and a 15% faster instrument turnaround after deployment, underscoring how automated alerts prevent incomplete loads from reaching operating rooms. The 2024 revision of AAMI ST79 now recommends electronic cycle tracking for all high-volume departments, effectively elevating IoT connectivity from nice-to-have to best practice. U.S. Bureau of Labor Statistics projections show a 7% decline in sterile-processing technicians through 2029, making automation critical to sustain throughput with fewer staff. Vendors that pair capital equipment with analytics subscriptions create sticky relationships because predictive-maintenance algorithms reduce unplanned downtime that can cancel surgeries.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Global Caps on Sterilant Residuals Driving Validation Complexity | -1.8% | Global, acute in North America and Europe | Medium term (2-4 years) |

| High Upfront Capital Expenditure for Advanced Low-Temperature Units Limits Adoption in Tier-2 Hospitals | -1.5% | Emerging APAC, Middle East, Africa, South America | Long term (≥ 4 years) |

| Device-Material Incompatibility with Some Hydrogen Peroxide and Plasma Cycles | -0.9% | Global | Medium term (2-4 years) |

| Consolidation of Disposable Single-Use Devices Reducing Reprocessing Volumes | -1.2% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Global Caps on Sterilant Residuals Driving Validation Complexity

ISO 10993-7 limits ethylene oxide residuals to 4 mg per device and hydrogen peroxide to 1 mg, forcing multi-week aeration studies that add USD 50,000–150,000 per new product family and delay launches by up to four months. European guidance in October 2024 added worst-case biofilm testing with Pseudomonas aeruginosa, increasing microbiology workload for small manufacturers. Contract research pricing for these expanded protocols now exceeds USD 200,000, prompting startups to cede sterilization science to larger partners. The resulting consolidation marginally drags on low-temperature sterilization market growth as validation roadblocks deter investment in novel polymer devices while favoring incumbents that amortize compliance costs across broad portfolios.

High Upfront Capital Expenditure for Advanced Low-Temperature Units Limits Adoption in Tier-2 Hospitals

Hydrogen peroxide gas-plasma chambers range from USD 180,000 to USD 350,000, and installation plus annual service pushes the total cost of ownership up by 20%. Forty-two percent of rural U.S. hospitals operated at negative margins in 2024, prioritizing imaging and robotics over sterilization upgrades. Reimbursement gaps persist internationally: only 3 of 18 low- and middle-income countries surveyed by the World Health Organization in 2024 had billing codes for low-temperature sterilization, so hospitals treat the expense as overhead. Leasing pilots like Getinge’s “Sterilization-as-a-Service” in India spread payments across per-cycle fees, yet uptake remains limited to a handful of tertiary centers. Consequently, Tier-2 and Tier-3 facilities will likely continue using steam autoclaves for another 5 to 7 years, creating an adoption divide within the low-temperature sterilization market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Ethylene Oxide Dominance Erodes as Hydrogen Peroxide Plasma Gains Share

Ethylene oxide retained 37.55% of the low temperature sterilization market share in 2025, underscoring its unrivaled compatibility with cellulosic packaging and long-lumen devices. Hydrogen peroxide gas-plasma, however, is recording a 12.25% CAGR to 2031, propelled by sub-60-minute cycles and zero toxic residuals that eliminate aeration-room bottlenecks. The low-temperature sterilization market for hydrogen peroxide chambers is on track to double between 2026 and 2031 as hospitals replace legacy autoclaves and retrofit ethylene oxide units. Vaporized hydrogen peroxide occupies third place and dominates pharmaceutical aseptic fills because it leaves no condensate on glass syringes, while ozone and low-temperature steam formaldehyde remain a niche. Nitrogen dioxide sterilization, commercialized in Canada and Europe, shows promise for cellulosic packages yet awaits U.S. 510(k) clearance, a hurdle that constrains its immediate revenue potential. The technology mix will therefore continue to tilt toward hydrogen peroxide in hospital settings, with ethylene oxide persisting in high-volume contract sites that require broad material compatibility.

Hospitals weigh cycle time, regulatory scrutiny, and material breadth when replacing legacy systems, pushing vendors to engineer multipurpose chambers capable of running both vaporized and plasma configurations. Competitive advantage increasingly lies in integrated cycle analytics rather than core sterilant chemistry, because real-time dashboards help facilities optimize load density and maintenance schedules. Over the forecast horizon, ethylene oxide is projected to relinquish roughly 5 percentage points of share yet remain critical for complex cardiovascular catheters and bulky orthopedic kits that exceed plasma load dimensions. As emission standards tighten further, growth opportunities will favor hybrid platforms that toggle between sterilants, offering facilities a compliance hedge without duplicating capital investment.

By Application: Single-Use Disposables Pre-Pack Sterilization Surges on Pharmaceutical Demand

Reusable medical devices retained 35.23% of application revenue in 2025, reflecting frequent reprocessing cycles for surgical trays, endoscopes, and power tools. Single-use disposables pre-pack sterilization, however, is climbing at 12.55% annually, propelled by biologics makers that fill pre-sterilized syringes and autoinjectors. Vaporized hydrogen peroxide achieved a 6-log reduction in Bacillus atrophaeus on filled monoclonal-antibody syringes without protein oxidation, confirming the modality's viability for high-value biologics. Hospitals are simultaneously adopting sterile single-use kits in orthopedic and cardiology suites to reduce infection risk, offsetting some of the reusable volume. Nonetheless, the low-temperature sterilization market for pharmaceutical pre-packs is forecast to overtake the reusable surgical instruments market by 2030.

Surgical instrument manufacturers respond by designing hybrid portfolios: reusable core tools complemented by disposable adjuncts such as cutting guides and drill sleeves that arrive terminally sterilized. “Other applications” include isolator glove sterilization in cleanrooms and biological safety cabinet decontamination, both of which benefit from vapor-phase technologies that can penetrate semi-rigid glove materials without leaving condensate. Over the forecast horizon, platform flexibility that allows chambers to switch between reusable trays and pre-pack loads will command premium pricing, especially among contract providers serving diversified client rosters.

By End User: Contract Sterilizers Outpace Hospitals as Outsourcing Economics Shift

Hospitals and clinics generated 61.53% of 2025 revenue, but contract service providers are expanding at a 11.85% CAGR, accelerating the growth of the low-temperature sterilization market driven by outsourcing. Validation costs for new device geometries can reach USD 10 million in aggregate, and contract sterilizers amortize those expenses across hundreds of clients, whereas an individual 300-bed hospital might process only a few dozen instrument families. As a result, hospital executives increasingly outsource complex loads while retaining simple steam-compatible sets, shortening in-house replacement cycles to 8–10 years. Ambulatory surgical centers, the fastest-growing care setting, lack space for ethylene oxide aeration rooms and therefore rely on hydrogen peroxide plasma, further reinforcing the outsourcing trend.

Pharmaceutical and biotechnology companies occupy a mid-teen share, relying on vaporized hydrogen peroxide to sterilize drug-device combinations that cannot tolerate steam or gamma irradiation. Research laboratories and academic institutes maintain a single-digit stake, primarily for BSL-3 and BSL-4 waste decontamination before incineration. The structural shift toward contract models also redistributes bargaining power: large providers negotiate bulk pricing on consumables, lowering per-cycle costs and pressuring hospitals that continue in-house processing. Consequently, the low temperature sterilization industry is witnessing supply-chain realignment favoring regionally clustered contract hubs near manufacturing centers.

Geography Analysis

North America accounted for 36.25% of 2025 revenue, supported by 6,100 acute-care hospitals and 6,308 Medicare-certified ambulatory surgical centers that completed 51 million surgical procedures in 2024. Joint Commission accreditation standards and high per-capita healthcare spending facilitate rapid adoption of hydrogen peroxide plasma systems, especially in institutions that aim for instrument turnaround times of under 60 minutes. The low-temperature sterilization market in North America is projected to expand steadily as emission caps tighten and ambulatory centers proliferate.

Asia-Pacific is advancing at a 12.21% CAGR and will account for one-third of the absolute global growth through 2031. Contract-sterilization hubs in Singapore, Malaysia, and Thailand feed Japanese and Chinese device exporters; STERIS alone added 48 new chambers in the region between 2024 and 2025. Singapore’s expedited GMP pathway reduced certification times to 9 months, providing a regulatory gateway for devices entering Japan’s PMDA approval process. China’s regulator approved 47 sterilization equipment models in 2024, up from 31 the year prior, signaling domestic capacity expansion that supports rural healthcare build-outs while also enabling exports. Consequently, the low-temperature sterilization market in Asia-Pacific benefits from both domestic consumption and contract services for manufacturers targeting high-income regions.

Europe maintained a significant share in 2025. Germany, the United Kingdom, and France account for a major share of regional revenue, leveraging statutory insurance reimbursements that explicitly cover validated low-temperature cycles. The European Medicines Agency harmonized residual guidance with ISO 10993-7 in October 2024, streamlining validation for multinationals and encouraging cross-border equipment standardization. Middle East and Africa, currently single-digit, will grow as Gulf Cooperation Council hospitals mandate hydrogen peroxide or ethylene oxide systems for new builds, exemplified by the United Arab Emirates’ February 2025 sterilization standards. South America’s low temperature sterilization market expansion is tempered by import tariffs topping 30% on capital equipment and patchy reimbursement, although Brazil’s ANVISA approved 12 new models in 2024, hinting at gradual growth.

Competitive Landscape

Competition is moderate, with STERIS, Getinge, and Advanced Sterilization Products (ASP) dominating hospital equipment, while Sotera Health’s Sterigenics division controls a major share of North American ethylene oxide contract capacity. Getinge’s 2024 launch of the IoT-enabled 8668 washer-disinfectant marked a pivot toward software-driven value propositions that reduce documentation labor and forecast maintenance. Medline’s April 2024 acquisition of Ecolab’s Bioquell vapor platform illustrates distributor consolidation aimed at bundling equipment, consumables, and service contracts into integrated sterile-processing offerings.

White-space opportunities include nitrogen dioxide systems that solve hydrogen peroxide’s cellulosic constraints, portable low-temperature units for ambulatory centers and military field hospitals, and AI-powered cycle optimization that tunes sterilant concentration in real time. TSO3’s Health-Canada-cleared nitrogen dioxide platform positions the firm as an early mover, though U.S. clearance remains pending. Start-ups like Plasmapp market benchtop plasma units under USD 100,000, undercutting incumbents by up to 50% and appealing to research institutes with limited budgets. Regulatory compliance remains a moat: ISO 10993-7 validation can run USD 150,000 per device family, deterring under-capitalized entrants and reinforcing share among companies with global laboratory infrastructure. As AAMI ST79 makes electronic tracking mandatory, vendors offering cloud ecosystems will increasingly differentiate themselves from hardware-only competitors.

Low Temperature Sterilization Industry Leaders

Advanced Sterilization Products (Fortive)

Cantel Medical

Solventum Corporation

STERIS plc

Getinge AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Genist Technocracy introduced a low-temperature plasma sterilizer aimed at hospitals, laboratories, and research centers, expanding affordable options for emerging markets.

- June 2025: Solventum launched the Attest Super Rapid Vaporized Hydrogen Peroxide Clear Challenge Pack, combining biological and chemical indicators in one transparent, single-use test pack for faster sterilizer validation.

Global Low Temperature Sterilization Market Report Scope

As per the report's scope, low temperature sterilization is a method used to sterilize heat‑ and moisture‑sensitive medical instruments at temperatures below 60 °C. It employs chemical agents such as ethylene oxide, hydrogen peroxide, gas plasma, or peracetic acid to destroy microorganisms, including spores. This process ensures effective sterilization without damaging delicate devices that cannot withstand traditional high‑temperature steam sterilization. It is widely used for endoscopes, plastics, electronics, and other advanced surgical tools.

The low-temperature sterilization market segmentation includes technology, application, end user, and geography. By technology, the market is segmented into ethylene oxide (EO) sterilization, hydrogen peroxide gas plasma, vaporized hydrogen peroxide (VHP), ozone sterilization, low-temperature steam formaldehyde, nitrogen dioxide & other emerging methods. By application, the market is segmented into reusable medical devices, surgical instruments, single-use disposables, pre-packaged, and other applications. By end user, the market is segmented into hospitals & clinics, ambulatory surgical centers, pharmaceutical & biotechnology companies, contract sterilization service providers, and research & academic institutes. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report covers estimated market sizes and trends for 17 countries across major regions worldwide. The report offers the value (in USD) for the above segments.

| Ethylene Oxide (EO) Sterilization |

| Hydrogen Peroxide Gas-Plasma |

| Vaporized Hydrogen Peroxide (VHP) |

| Ozone Sterilization |

| Low-Temp Steam Formaldehyde |

| Nitrogen Dioxide & Other Emerging Methods |

| Reusable Medical Devices |

| Surgical Instruments |

| Single-use Disposables Pre-pack |

| Other Applications |

| Hospitals & Clinics |

| Ambulatory Surgical Centers |

| Pharmaceutical & Biotechnology Companies |

| Contract Sterilization Service Providers |

| Research & Academic Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Ethylene Oxide (EO) Sterilization | |

| Hydrogen Peroxide Gas-Plasma | ||

| Vaporized Hydrogen Peroxide (VHP) | ||

| Ozone Sterilization | ||

| Low-Temp Steam Formaldehyde | ||

| Nitrogen Dioxide & Other Emerging Methods | ||

| By Application | Reusable Medical Devices | |

| Surgical Instruments | ||

| Single-use Disposables Pre-pack | ||

| Other Applications | ||

| By End User | Hospitals & Clinics | |

| Ambulatory Surgical Centers | ||

| Pharmaceutical & Biotechnology Companies | ||

| Contract Sterilization Service Providers | ||

| Research & Academic Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the low temperature sterilization market by 2031?

It is forecast to reach USD 5.59 billion in 2031, expanding at an 11.25% CAGR.

Which technology segment is growing fastest within low temperature sterilization?

Hydrogen peroxide gas-plasma is advancing at a 12.25% CAGR due to sub-60-minute cycles and zero toxic residuals.

Why are contract sterilizers gaining share over hospital sterilization departments?

Outsourcing spreads high validation costs across large device volumes, offers regulatory expertise, and alleviates capital burdens on hospitals.

How are regulatory changes influencing technology adoption?

Emission caps on ethylene oxide and expedited FDA pathways for vaporized hydrogen peroxide are driving rapid substitution toward hydrogen peroxide systems.

Which region is expected to deliver the highest growth?

Asia-Pacific is projected to post a 12.21% CAGR, aided by new contract-sterilization hubs in Singapore, Malaysia, and Thailand.

What factors limit adoption of advanced low-temperature units in Tier-2 hospitals?

High upfront costs, limited reimbursement, and financing constraints deter smaller facilities from upgrading to hydrogen peroxide or plasma systems.

Page last updated on: