Medical Device Regulatory Affairs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

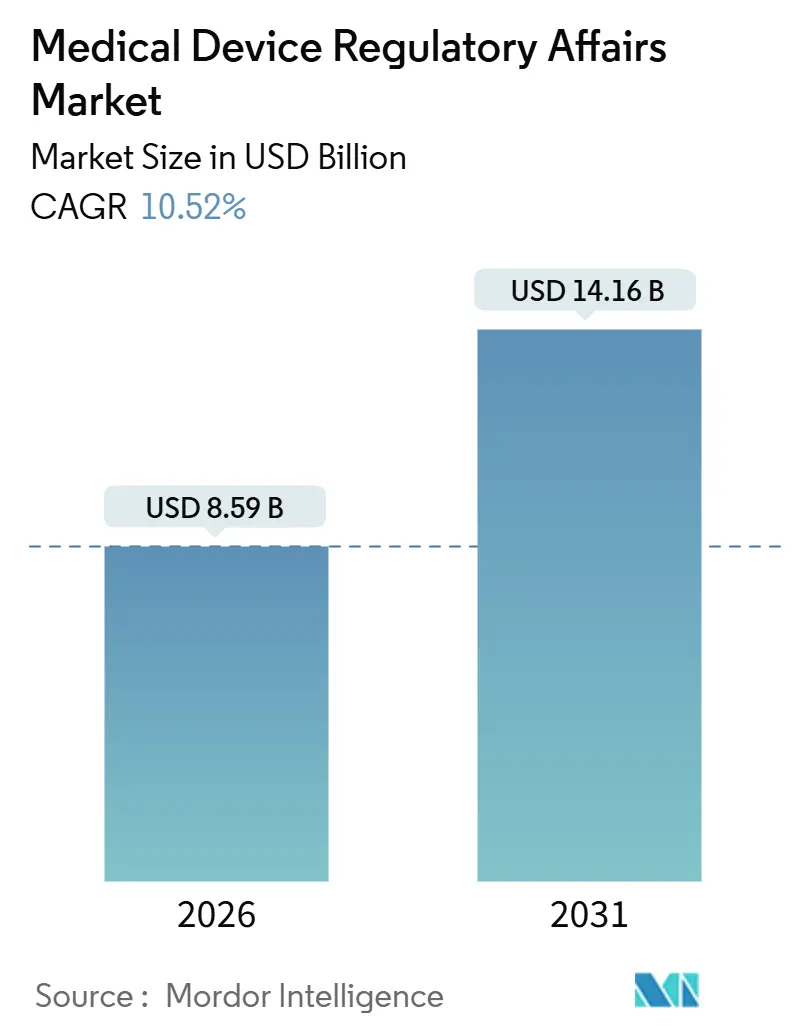

| Market Size (2026) | USD 8.59 Billion |

| Market Size (2031) | USD 14.16 Billion |

| Growth Rate (2026 - 2031) | 10.52% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Device Regulatory Affairs Market Analysis by Mordor Intelligence

The Medical Device Regulatory Affairs Market size is estimated at USD 8.59 billion in 2026, and is expected to reach USD 14.16 billion by 2031, at a CAGR of 10.52% during the forecast period (2026-2031).

Continued regulatory tightening, accelerating submission volumes, and the race to commercialize digital health innovations are prompting manufacturers to seek specialized guidance across every major geography. Outsourcing remains the dominant operating model because variable-cost consulting contracts insulate budgets from the cyclical spikes in workload triggered by new rules such as the FDA’s March 2024 cybersecurity mandate. Cloud-native regulatory information management (RIM) platforms are reshaping day-to-day workflows by automating document compilation and real-time gap checks. At the same time, demographic pressures in aging economies sustain device pipelines, which, in turn, lengthen the list of required regulatory filings. Competitive intensity is moderate, yet first-mover advantages accrue to providers that can synchronize U.S., EU, and Asia-Pacific submissions without compromising speed or quality.

Key Report Takeaways

- By service provider, outsourced specialists captured 58.65% of the medical device regulatory affairs market share in 2025. Product Registration & Clinical Trial Applications accounted for 12.76% of the medical device regulatory affairs market size CAGR through 2031, the highest of all service categories.

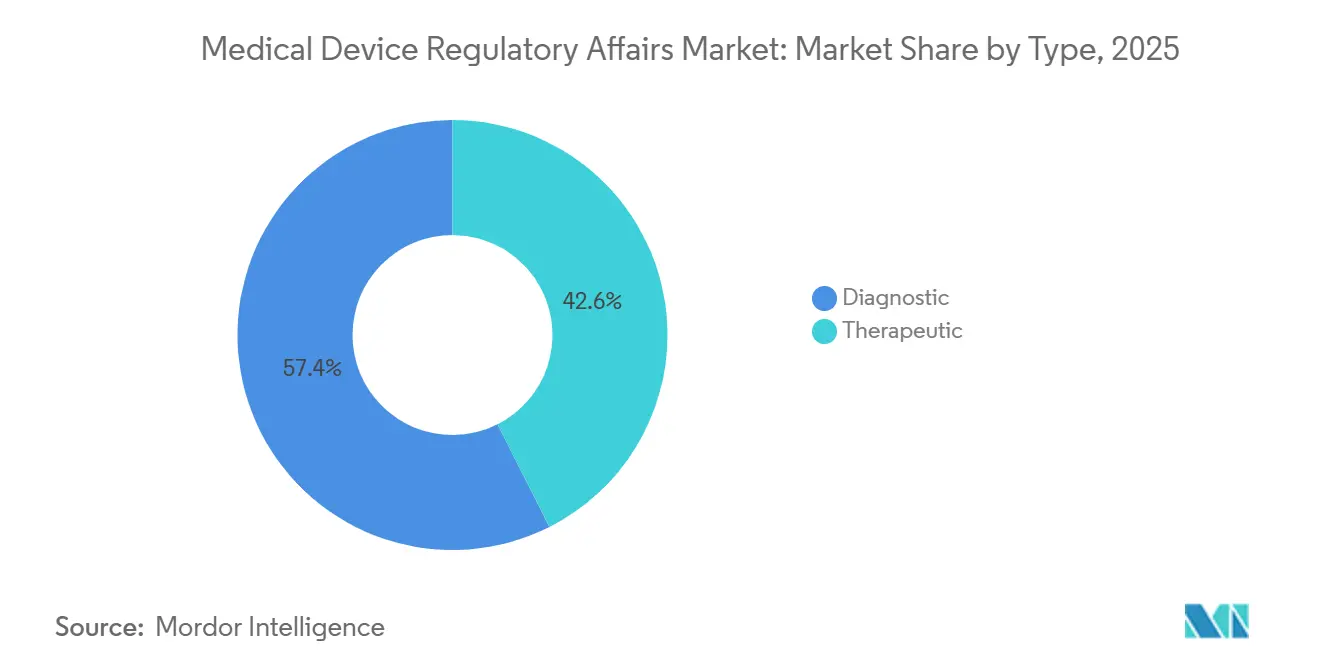

- By type, therapeutic devices accounted for 42.56% of revenue in 2025, whereas diagnostic platforms are advancing at a market-leading 12.87% CAGR through 2031.

- By service provider, outsourced accounted for 58.65% of revenue in 2025, whereas in-house is advancing at a market-leading 13.54% CAGR through 2031.

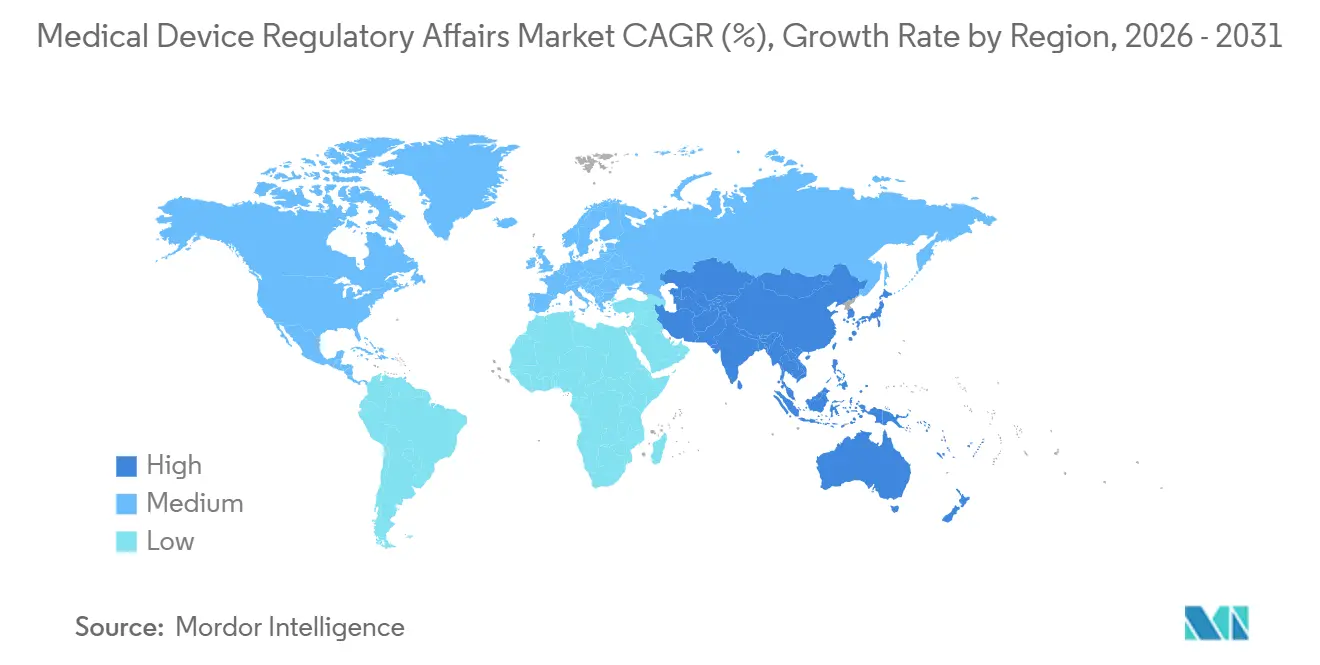

- By geography, North America led spending with 42.48% of global revenue in 2025; Asia-Pacific is expanding fastest at an 11.54% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Medical Device Regulatory Affairs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Demand for Innovative Medical Devices | +2.3% | Global, North America & EU concentration | Medium term (2–4 years) |

| Stringent Regulatory Frameworks Enhancing Patient Safety | +2.1% | North America, EU, Japan | Short term (≤ 2 years) |

| Growing Burden of Chronic Diseases and Aging Populations | +1.8% | Global, peak in APAC & North America | Long term (≥ 4 years) |

| Expansion of Device Manufacturers in Emerging Markets | +1.6% | APAC core, MEA & South America spill-over | Medium term (2–4 years) |

| Proliferation of AI-Driven Regulatory Intelligence Platforms | +1.4% | North America, EU, advanced APAC | Short term (≤ 2 years) |

| Post-Merger Integration Demands for Harmonized Compliance | +1.3% | Global, North America & EU concentration | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Global Demand for Innovative Medical Devices

The surge of software-enabled diagnostics and minimally invasive therapeutics shortens product life cycles and multiplies filing events. The FDA issued 89 De Novo authorizations for novel diagnostic algorithms in 2025, up 102% versus 2023, and Software as a Medical Device submissions climbed 34% year over year. Europe’s Medical Device Coordination Group expanded validation guidance in February 2025, requiring complete lifecycle documentation and extending average engagement durations by six months. Manufacturers, therefore, lean on consulting firms to synchronize U.S., EU, and Asia-Pacific dossiers simultaneously, safeguarding first-to-market positioning.

Growing Burden of Chronic Diseases and Aging Populations

Noncommunicable diseases accounted for 74% of global deaths in 2024, according to the World Health Organization. Japan’s share of citizens aged 65 and older reached 29.1% in 2024, driving a 15% rise in device applications for elder care. The FDA’s 2025 Real-World Evidence guidance allows the integration of electronic health record data into submissions, expanding the evidence-generation workload that consulting teams must orchestrate.

Expansion of Device Manufacturers in Emerging Markets

Fast-track pathways are compressing approval timelines across Asia-Pacific and Latin America. China’s priority review channel halves the assessment time for Class III devices to 9 months. India’s August 2024 rule alignment trimmed foreign dossier requirements by 30%, and Brazil cut small-enterprise fees by 30% in March 2025 while accepting specific FDA clearances for mutual recognition. These reforms drive outsourced demand where local regulatory skill sets are limited.

Post-Merger Integration Demands for Harmonized Compliance

Device industry consolidation is creating multi-jurisdictional portfolios that require unified quality systems. Medtronic’s USD 738 million purchase of EOFlow combined dossiers governed by disparate regulations, necessitating a 14-month harmonization project managed by a blended in-house and outsourced team. The International Medical Device Regulators Forum outlined a common template for adverse-event reporting in November 2025, pushing acquirers to invest upfront in data architecture that allows enterprise-wide surveillance[1]International Medical Device Regulators Forum, “Harmonized Adverse Event Reporting,” imdrf.org.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex and Divergent Global Regulatory Requirements | -1.2% | Global, acute in emerging APAC & MEA | Medium term (2–4 years) |

| High Costs of Regulatory Compliance | -0.9% | Global, North America & EU concentration | Short term (≤ 2 years) |

| Shortage of Experienced Regulatory Affairs Talent Pool | -0.7% | Global, peak in North America & EU | Long term (≥ 4 years) |

| Cybersecurity Mandates Increasing Documentation Burden | -0.6% | North America, EU, advanced APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Complex and Divergent Global Regulatory Requirements

The International Medical Device Regulators Forum counted 23 unique classification schemes in 2024, often forcing duplicate tests when a device shifts categories across borders. India’s risk-based framework diverges from both FDA and EU rules, while Brazil demands Portuguese-language labeling and local clinical data, adding up to six months of extra work[2]India CDSCO, “Medical Device Rules Amendment 2024,” cdsco.gov.in. Such fragmentation erodes the economic rationale for global launch strategies and tempers consulting revenue in lower-priority geographies.

Shortage of Experienced Regulatory Affairs Talent Pool

Global membership in the Regulatory Affairs Professionals Society reached only 18,500 in 2025 after 3.1% growth, far below the 10.52% expansion in workload[3]Regulatory Affairs Professionals Society, “Membership Statistics 2025,” raps.org. Senior manager vacancies sit open for 89 days on average in North America, inflating labor costs by 6.8% at firms like IQVIA. Scarcity elevates pricing but also caps the number of concurrent projects that consultancies can accept.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Services: Documentation Complexity Fuels Writing Demand

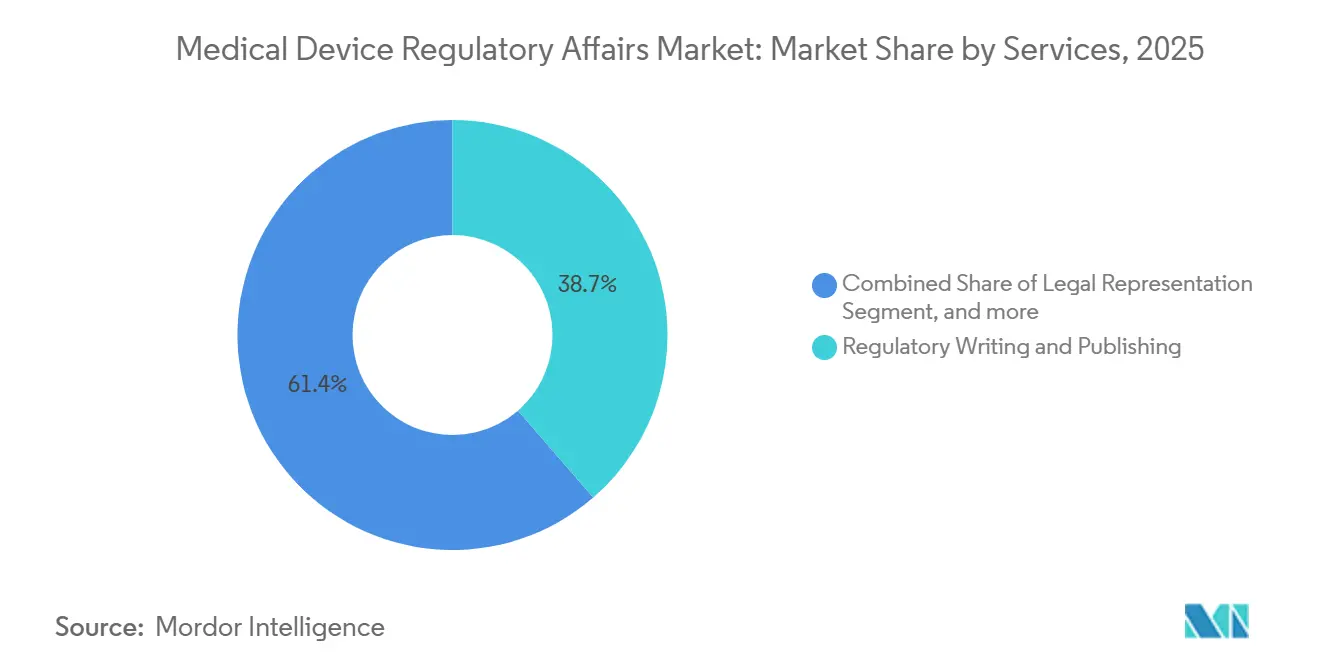

Regulatory writing & publishing captured 38.65% of 2025 revenue, mirroring the document-heavy obligations created by cybersecurity addenda and software lifecycle controls. Product Registration & Clinical Trial Applications services, advancing at a 12.76% CAGR, are the chief growth engine, as reforms in China and India have halved or reduced review times, enticing manufacturers to file earlier and across more countries. Regulatory Consulting, which covers strategy road-mapping and gap analyses, recorded solid expansion as clients transitioned to EUDAMED and updated U.S. cybersecurity dossiers. Legal Representation rose alongside a 19% jump in FDA warning letters citing post-market surveillance gaps. Automation is changing the service mix: Veeva’s Vault RIM cuts routine checklist labor, freeing writers for high-value narrative tasks and heightening demand for advanced clinical evaluation reports. The medical device regulatory affairs market for Product Registration now scales directly with submission velocity rather than solely on headcount, encouraging providers to adopt cloud tools to maintain margins.

A second-order shift involves the blending of training, audits, and post-market surveillance deliverables. The FDA’s 2025 Real-World Evidence guidance opened doors for hybrid data models that pair randomized trials with observational datasets, requiring specialized biostatistics. Providers that marry RIM automation with statistical services are poised to out-perform, even as documentation volumes continue to climb. Collectively, these forces secure an enduring advantage for consulting firms that reinvest in workflow technologies, AI-driven writing aids, and globally accredited quality systems.

By Type: Diagnostic Devices Outpace Therapeutic Growth

Therapeutic devices held 42.56% of 2025 revenue, propelled by high-value cardiac, orthopedic, and insulin delivery implants that demand extensive pre-market trials and consequently large regulatory budgets. Diagnostic platforms, particularly in vitro diagnostics and algorithmic decision-support tools, are expanding at a faster 12.87% CAGR because development cycles are shorter and evidence thresholds lower. Europe’s backlog in the In Vitro Diagnostic Regulation forced widespread re-certifications through 2025, materially lifting consulting revenue for test-kit makers. The FDA approved 89 De Novo diagnostic algorithms in 2025, double the 2023 count, signaling a sustained pipeline that multiplies writing assignments. The medical device regulatory affairs market for diagnostic filings shows a favorable balance between volume and complexity, making the segment attractive for mid-tier consultancies armed with AI-enabled template libraries.

Therapeutic submissions remain labor-intensive, especially after the FDA embraced hybrid evidence models that require the orchestration of both randomized and real-world datasets. Japan’s demographic profile intensified demand for therapeutic approvals, reflected in a 12% rise in PMDA filings during fiscal 2024. Even so, diagnostics retain the numeric upper hand because each platform typically spawns multiple software updates that warrant regulatory supplements. Providers that master rapid sprints for iterative diagnostic releases will therefore pick up share inside the broader medical device regulatory affairs market.

By Service Provider: Outsourcing Gains as Compliance Burden Escalates

Outsourced vendors amassed 58.65% of 2025 revenue, confirming manufacturers’ preference for elastic cost structures amid unpredictable workload spikes. IQVIA’s Technology & Analytics Solutions segment posted USD 15.4 billion in 2025, advancing 8.2% organically, driven by cybersecurity and EUDAMED engagements. LabCorp’s Covance arm opened a 200-person center in Hyderabad in November 2025, targeting India’s low labor costs to serve the 12.76% CAGR Product Registration segment. Nonetheless, in-house teams are projected to climb at 13.54% annually as conglomerates like Medtronic internalize integration projects to safeguard proprietary datasets. The medical device regulatory affairs market share balance will therefore evolve into a dual-track system: outsourced partners dominate routine filings and resource-heavy peaks, whereas internal departments assume stewardship of strategic, IP-sensitive dossiers.

Smaller innovators, lacking scale to justify dedicated staff, will continue to lean on consultants who offer pay-as-you-go access to AI-supported templates and multi-jurisdictional expertise. Freyr and Promedica typify this model, licensing RIM technology to compress timelines and undercut larger CROs on price without sacrificing quality. The strategic bifurcation suggests that outsourced specialists will maintain majority share, yet the revenue mix will favor those willing to reinvest in automation.

Geography Analysis

North America generated 42.48% of global spending in 2025, underpinned by the FDA’s 4,143 cleared 510(k) submissions and an unparalleled ecosystem of contract research organizations. Average U.S. review cycles stretched to 147 days after cybersecurity provisions took effect in March 2024, a delay that enlarged consulting hours linked to remediation and resubmission. Health Canada aligned Software as a Medical Device guidance with U.S. expectations in June 2025, compelling cross-border dossier harmonization and boosting bilateral consulting engagements. Mexico shortened its Class II approvals to seven months in September 2024, encouraging firms to regionalize compliance workflows within a North American hub and amplifying the total addressable spend within the medical device regulatory affairs market.

Asia-Pacific represents the fastest-growing region at an 11.54% CAGR to 2031, driven by sweeping reforms in China, India, Japan, and South Korea. China’s nine-month priority review for innovative Class III devices reallocates budget from clinical delays to upfront regulatory strategy, lifting demand for Beijing- and Shanghai-based consultants. India’s 2024 rule overhaul reduced documentation by 30%, but the need to interpret localized templates keeps foreign manufacturers reliant on local advisory firms. Japan’s PMDA processed 1,247 applications in fiscal 2024 as its aging population fuels therapeutic device adoption. South Korea’s March 2025 mutual recognition pact with the FDA shaved 20% off average costs for dual filings, channeling incremental projects to Seoul-based consultants.

Europe remained a heavy spender in 2025 owing to the phased rollout of the Medical Device Regulation, In Vitro Diagnostic Regulation, and EUDAMED’s May 2026 go-live. Germany, the United Kingdom, France, Italy, and Spain accounted for more than 60% of regional consulting outlays as local notified-body queues increased reliance on external dossier authors. Brazil’s 30% fee reduction for small firms and its recognition of FDA clearances revitalized South American spending, while Saudi Arabia and the UAE pushed forward with Gulf Health Council harmonization, consolidating Middle East compliance under unified templates. Collectively, these moves expand the geographic footprint of the medical device regulatory affairs market without diluting the primacy of North America and Europe in total dollars.

Competitive Landscape

The sector remains moderately fragmented; the 10 most significant vendors hold about 35% of 2025 revenue. IQVIA, ICON, and LabCorp lead the outsourced tier, leveraging end-to-end offerings spanning regulatory consulting, clinical trial oversight, and post-market surveillance. IQVIA’s 8.2% organic expansion during 2025 underscores the magnet effect of one-stop solutions for cybersecurity documentation and EUDAMED uploads. Intertek and SGS diversified from testing into regulatory advisory during 2024-2025, marketing bundled audits and submission packages that appeal to medium-sized manufacturers seeking simplicity. Freyr, Promedica, and other niche specialists employ AI-driven templates to slice completion times and win mid-tier contracts.

White-space opportunities reside in AI-enabled regulatory intelligence and emerging-market localization. Veeva handled 12,000 submissions via Vault RIM, demonstrating that automation equalizes scale advantages and deters commoditization. Talent scarcity is the constraining variable; RAPS membership growth of 3.1% trails demand, forcing firms to set up offshore hubs and robust internal training academies. Acquisition pipelines remain active as larger CROs scout technology-rich boutiques to plug expertise gaps, exemplified by SGS’s majority stake in a Bangalore consultancy and Medtronic’s platform roll-up.

Medical Device Regulatory Affairs Industry Leaders

ICON, Plc

IQVIA, Inc.

Laboratory Corporation of America Holdings

Integer Holdings Corporation

SGS Société Générale de Surveillance SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: The UK’s Medicines and Healthcare Products Regulatory Agency (MHRA) launched a new Early Access service to support the faster adoption of innovative medical devices, particularly in areas with unmet clinical needs.

- June 2024: IMed Consultancy has released a white paper detailing the regulatory landscape for AI/ML medical devices across the US, UK, and EU, highlighting unique challenges like the EU AI Act's high-risk classification conflicting with MDR/IVDR for self-learning systems, the FDA's growing approvals, and the UK's evolving framework post-Brexit, with key issues focusing on safety, transparency, and lifecycle management for these dynamic technologies.

Global Medical Device Regulatory Affairs Market Report Scope

As per scope of the report, medical device regulatory affairs involves ensuring that medical devices comply with national and international regulations and standards. It includes managing approvals, registrations, and documentation needed for market access. This field ensures the safety, efficacy, and legal compliance of medical devices throughout their lifecycle.

The Medical Device Regulatory Affairs Market is Segmented by Services (Regulatory Consulting, Legal Representation, Regulatory Writing & Publishing, Product Registration & Clinical Trial Applications, and Other Services), Type (Diagnostic and Therapeutic), Service Provider (In-house and Outsource), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Regulatory Consulting |

| Legal Representation |

| Regulatory Writing & Publishing |

| Product Registration & Clinical Trial Applications |

| Other Services |

| Diagnostic |

| Therapeutic |

| In-house |

| Outsource |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Services | Regulatory Consulting | |

| Legal Representation | ||

| Regulatory Writing & Publishing | ||

| Product Registration & Clinical Trial Applications | ||

| Other Services | ||

| By Type | Diagnostic | |

| Therapeutic | ||

| By Service Provider | In-house | |

| Outsource | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the medical device regulatory affairs market by 2031?

The market is forecast to reach USD 14.16 billion by 2031.

Which service segment is expected to grow fastest through 2031?

Product Registration & Clinical Trial Applications, expanding at a 12.76% CAGR.

Which region is growing quickest in regulatory affairs spending?

Asia-Pacific, advancing at an 11.54% CAGR.

What share did outsourced providers hold in 2025?

Outsourced vendors secured 58.65% of 2025 revenue.

How are cybersecurity mandates affecting submission size?

New rules add 40-60 pages to typical 510(k) filings and extend review timelines by up to four weeks.

Which device category is expanding faster, diagnostic or therapeutic?

Diagnostic platforms are growing faster at a 12.87% CAGR versus therapeutic devices.

Page last updated on: