U.S. Pulse Oximeters Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.98 Billion |

| Market Size (2026) | USD 1.03 Billion |

| Market Size (2031) | USD 1.33 Billion |

| Growth Rate (2026 - 2031) | 5.10% CAGR |

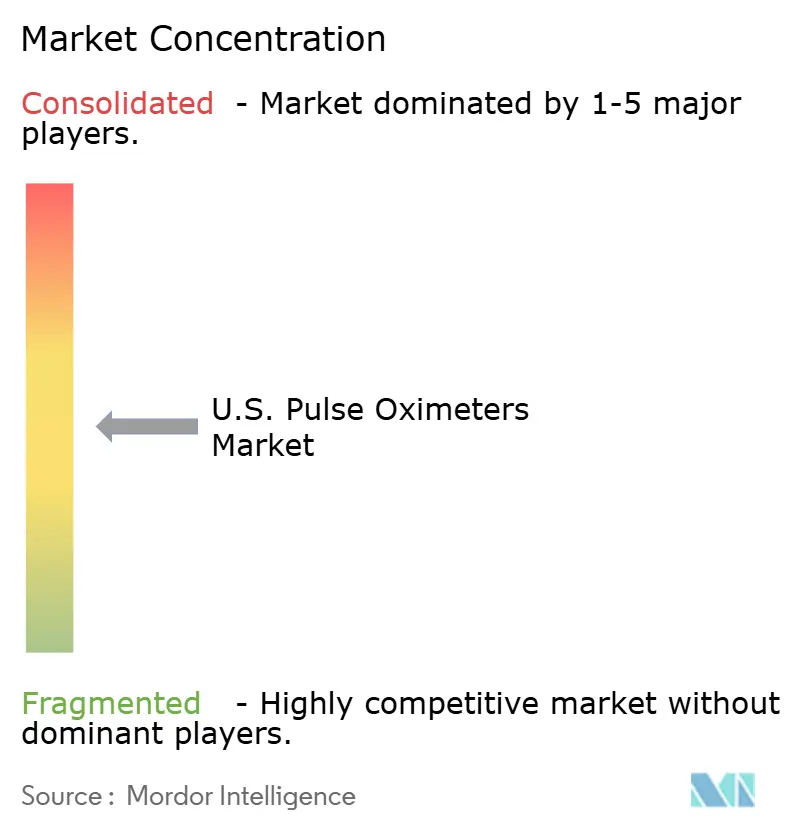

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

U.S. Pulse Oximeters Market Analysis by Mordor Intelligence

The U.S. Pulse Oximeters Market size is projected to expand from USD 0.98 billion in 2025 and USD 1.03 billion in 2026 to USD 1.33 billion by 2031, registering a CAGR of 5.10% between 2026 to 2031.

In 2024, 4.2% of adults in the United States reported COPD, emphysema, or chronic bronchitis, while an estimated 83.7 million adults were affected by obstructive sleep apnea, with many cases undiagnosed.[1]CDC National Center for Health Statistics, “Chronic Obstructive Pulmonary Disease FastStats,” CDC, cdc.gov This ongoing disease burden continues to drive demand for oxygen saturation monitoring across hospitals, clinics, and home settings. The United States pulse oximeters market is undergoing changes due to stricter FDA requirements on skin-tone accuracy, prompting hospitals and post-acute providers to replace older devices with higher-accuracy models. Additionally, the market is transitioning from one-time spot checks to continuous monitoring, driven by remote patient monitoring, home care, and digital clinical workflows.

Key Report Takeaways

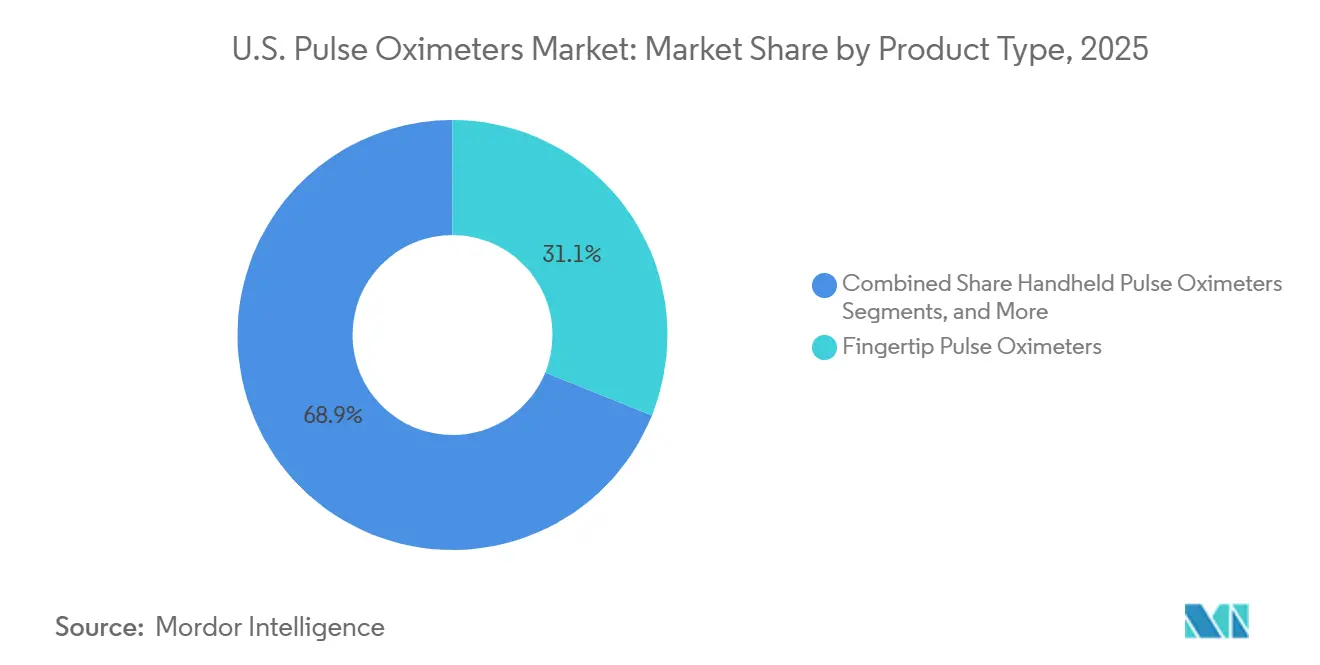

- By product type, fingertip pulse oximeters led with 31.1% revenue share in 2025, while handheld devices are forecasted to expand at a 6.55% CAGR through 2031.

- By technology, wearable pulse oximeters held 25.6% share in 2025, while connected and wireless pulse oximeters recorded the highest projected CAGR at 7.45% through 2031.

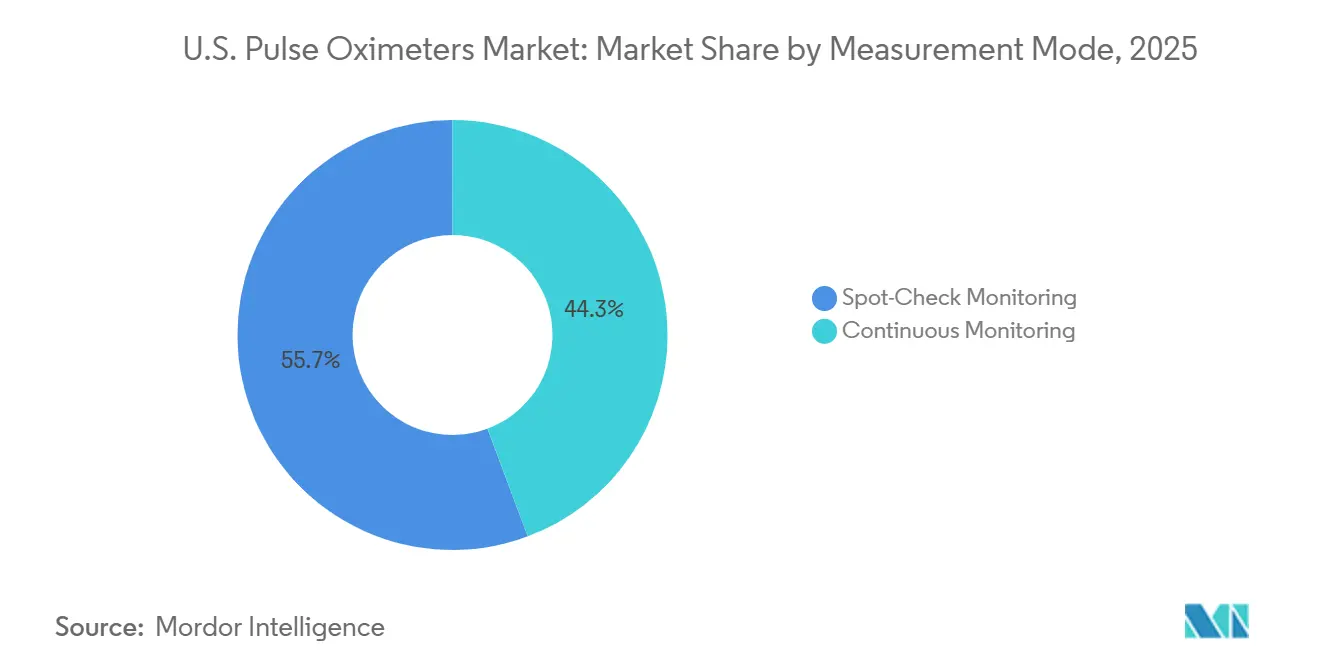

- By measurement mode, spot-check monitoring accounted for 55.66% of revenue in 2025, while continuous monitoring is expected to grow at a 7.12% CAGR through 2031.

- By patient age group, adults represented 63.78% of revenue in 2025, while the pediatric segment is projected to grow at a 7.98% CAGR through 2031.

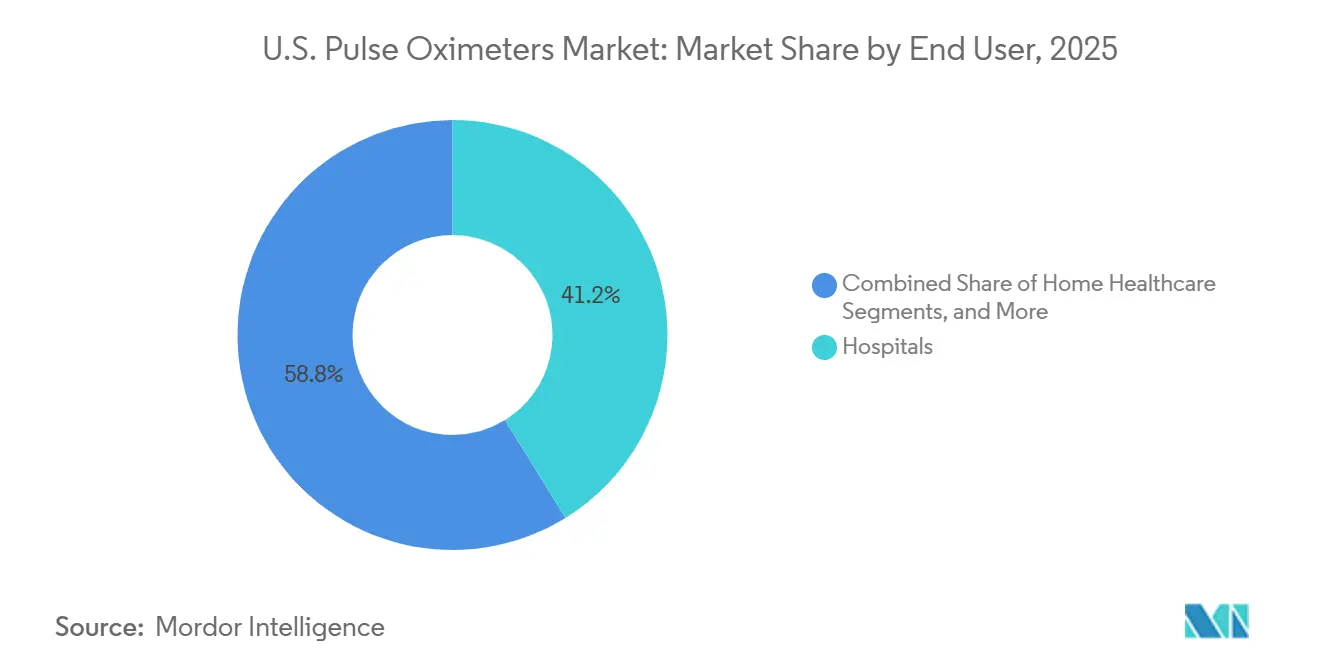

- By end user, hospitals held 41.23% of the U.S. pulse oximeters market share in 2025, while home healthcare posted the fastest growth at an 8.10% CAGR through 2031.

- By application, respiratory disease monitoring captured 35.45% of the U.S. pulse oximeters market size in 2025, while sleep apnea screening is expected to grow at a 6.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

U.S. Pulse Oximeters Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising COPD, asthma, and sleep apnea burden requiring oxygen saturation screening | +1.3% | National, with disproportionate impact in Southern non-metro areas and Appalachian states where COPD prevalence peaks at 10.6% | Long term (≥ 4 years) |

| Shift from spot-check devices to continuous monitoring in home and post-acute care | +0.9% | National, with early gains in Northeast and Midwest post-acute networks | Medium term (2-4 years) |

| Fda pressure for better accuracy across skin tones elevates premium device replacement | +0.8% | National, with concentrated impact in high-diversity urban healthcare markets such as New York, Los Angeles, Houston, and Chicago | Medium term (2-4 years) |

| Remote patient monitoring reimbursement expands connected pulse oximeter adoption | +0.9% | National, strongest in states with high Medicare Advantage penetration and robust telehealth infrastructure | Short term (≤ 2 years) |

| Hospital standardization toward integrated monitoring platforms improves sensor pull-through | +0.6% | National, concentrated in large health systems and IDNs in Northeast and Sun Belt | Medium term (2-4 years) |

| Consumer awareness of silent hypoxemia sustains OTC and retail demand | +0.5% | National, strongest in the 65+ demographic concentrated in Florida, Arizona, and retirement-heavy Sun Belt metros | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising COPD, Asthma, and Sleep Apnea Burden Driving Oxygen Saturation Monitoring

Chronic respiratory diseases are driving demand in the United States pulse oximeters market. In 2024, 4.2% of adults in the United States were diagnosed with COPD, emphysema, or chronic bronchitis. Additionally, 83.7 million adults, or 32.4% of the adult population, were estimated to have obstructive sleep apnea, with many cases undiagnosed. Severe and moderate cases, accounting for 18% and 30% respectively, are increasing the need for clinical-grade overnight pulse oximetry.[2]Respiratory Medicine, “Unmasking Obstructive Sleep Apnea, Estimated Prevalence and Impact in the United States,” Respiratory Medicine, resmedjournal.com Sleep apnea screening is the fastest-growing application, with a 6.98% CAGR projected through 2031. Nonin Medical’s 2025 launch of its Nonin Health platform addresses remote overnight testing for over 1.5 million Americans requiring supplemental oxygen. Broader diagnoses and protocol adoption are expected to sustain long-term device demand.

FDA Pressure for Accuracy Across Skin Tones Elevating Premium Device Replacement

The FDA’s 2025 draft guidance significantly impacts the United States pulse oximeters market by increasing clinical study pool requirements and mandating diverse skin tone representation. These changes favor advanced multi-wavelength systems over older products, prompting hospitals to replace low-cost devices with next-generation platforms.[3]U.S. Census Bureau, “Older Adults Outnumber Children in Many States,” U.S. Census Bureau, census.gov This shift is transforming routine replacement cycles into premium upgrade opportunities. Masimo’s MightySat Medical, cleared by the FDA in 2024, highlights the rising clinical expectations for consumer-accessible devices.

Remote Patient Monitoring Reimbursement Expanding Connected Pulse Oximeter Adoption

Medicare reimbursement policies are driving growth in the United States pulse oximeters market. Remote patient monitoring payments reached USD 536 million in 2024, a 31% increase from 2023, with nearly 1 million beneficiaries receiving services. CPT codes 99453 and 99454 support payments for device setup and monitoring, improving the economic case for connected device investments. Allowing auxiliary personnel to perform device setup further reduces onboarding costs, making connectivity features essential for manufacturers.

Shift From Spot-Check to Continuous Monitoring Restructuring the Device Mix

The United States pulse oximeters market is shifting toward continuous monitoring, projected to grow at a 7.12% CAGR through 2031, compared to spot-check mode, which held 55.66% of revenue in 2025. Demand for wearable devices in step-down units, hospital-to-home programs, and sleep testing is driving this growth. Connected and wireless technology is expanding at a 7.45% CAGR, integrating clinical monitoring with data transmission. Masimo’s Radius PPG, used with GE HealthCare’s Portrait Mobile platform, exemplifies this transition. Home healthcare, growing at an 8.10% CAGR, is also benefiting from the aging population, with 61.2 million Americans aged 65 and older in 2024.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Persistent accuracy variability in motion, low perfusion, and darker skin tones | -0.7% | National, with acute sensitivity in high-acuity hospital settings across all U.S. regions | Long term (≥ 4 years) |

| Intensifying regulatory review increases validation cost and time to market | -0.6% | National, disproportionately affecting smaller manufacturers and OTC entrants | Medium term (2-4 years) |

| Reimbursement pressure in basic commodity oximeters compresses margins | -0.4% | National, most acute in home health and retail OTC channels | Short term (≤ 2 years) |

| Substitution from multi-parameter wearables and smart rings limits standalone unit growth | -0.5% | National, concentrated in consumer and wellness-oriented OTC demand | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Accuracy Variability Limiting Clinical Confidence in Edge Populations

Accuracy issues remain a significant challenge in the United States pulse oximeters market, particularly in scenarios involving motion, low perfusion, and darker skin tones. A 2026 study revealed that the Masimo MightySat Rx, a leading clinical fingertip device, recorded an Arms of 3.52% at oxygen saturation levels below 88%. This result approaches the upper limit of clinical acceptability, highlighting variability in confidence across patient groups and care settings. These challenges are most evident in ICUs, post-surgical wards, and home respiratory monitoring, where factors like poor circulation, movement-related noise, and skin-tone biases impact reliability. Additionally, a 2024 meta-analysis by the FDA reported a pooled mean overestimation of 1.52% in Black and African American patients, further emphasizing equity concerns. The market remains divided between premium devices with advanced algorithms and commodity products facing reliability issues.

Intensifying Regulatory Review Compressing Entry Windows and Raising Validation Costs

Increasing regulatory scrutiny is driving up entry costs in the United States pulse oximeters market. Under the FDA’s January 2025 draft guidance, companies must recruit at least 150 participants for desaturation studies and demonstrate performance across diverse skin tones using both objective and subjective methods. Large players like Masimo and Nonin Medical are better positioned to manage these requirements due to their established validation infrastructure. Smaller and mid-tier suppliers face greater challenges, especially with lower price points limiting cost recovery. Additionally, connected devices face stricter expectations regarding cybersecurity and interoperability. These factors are likely to reduce the number of new entrants in the market during the later years of the forecast period.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Fingertip Dominance Coexists With Handheld-Driven Field Expansion

In 2025, fingertip pulse oximeters captured 31.1% of the U.S. pulse oximeters market by product type, establishing themselves as the top revenue format. Their dominance stems from being cost-effective, easy to operate, and versatile for both clinical spot-checks and home monitoring. The segment gained traction when Masimo’s MightySat Medical, received FDA clearance for OTC sale in February 2024, marking a significant milestone in consumer accessibility. However, this broader access doesn't diminish the demand for hospital-grade products, as many clinical settings still prioritize stronger validation and seamless workflow integration.

Forecasted to grow at a 6.55% CAGR through 2031, handheld pulse oximeters are emerging as the fastest-growing product format in the U.S. market. Their primary users include home health aides, visiting nurses, and staff at ambulatory surgical centers, all of whom seek portability combined with enhanced functionality over basic fingertip models. Meanwhile, tabletop and bedside systems maintain their essential role in ICUs and step-down units, where fixed-position monitoring is routine.

By Technology: Connected and Wireless Devices Outpace Incumbents on Hospital Adoption

In 2025, wearable pulse oximeters dominated the U.S. market, accounting for 25.6% of the revenue. Their prominence is largely attributed to the surge in home monitoring adoption during the pandemic. Wearables have carved a niche for themselves, excelling in continuous patient monitoring, sleep diagnostics, and remote care, outpacing traditional fixed or episodic formats. This established presence has also helped integrate home-based SpO2 tracking into routine monitoring, moving it away from being solely an emergency measure.

Forecasted to grow at a 7.45% CAGR through 2031, connected and wireless pulse oximeters are leading the charge among technology categories in the U.S. market. Health systems are gravitating towards devices that seamlessly transfer data into electronic medical records, nurse alert systems, and remote patient monitoring workflows, minimizing manual intervention. Masimo’s expanded partnership with Philips in September 2025 is a testament to this trend, as it weaves SET, Radius PPG, and AI-driven monitoring into Philips’ patient monitoring ecosystem, extending through 2026 and beyond.

By Measurement Mode: Continuous Monitoring Compressing Spot-Check’s Share Lead

In 2025, spot-check monitoring commanded 55.66% of the revenue, solidifying its status as the leading mode in the U.S. pulse oximeters market. This dominance is a testament to the widespread use of periodic vital sign assessment tools in hospitals, emergency departments, and outpatient clinics. In many of these environments, episodic measurements suffice for the clinical pathways in use. Thus, while the growth of spot-check devices may decelerate in comparison to more connected models, they will continue to play a pivotal role in daily care delivery.

Continuous monitoring is set to outpace spot-check usage, with projections indicating a 7.12% CAGR growth through 2031 in the U.S. pulse oximeters market. The increasing need for uninterrupted oxygen saturation data in scenarios like post-surgical observation, COPD management, and home sleep testing drives this demand. Furthermore, support from CMS for remote patient monitoring bolsters this trend, as continuous data transmission aligns with reimbursable care workflows.

By Patient Age Group: Pediatric and Neonatal Validation Requirements Elevating Complexity

In 2025, adults accounted for 63.78% of revenue, solidifying their dominant position in the U.S. pulse oximeters market. This aligns with the U.S. demographic trends and the concentration of chronic respiratory diseases among middle-aged and older adults. As of 2024, Americans aged 65 and older numbered 61.2 million, constituting 18% of the total population, underscoring the sustained demand for adult monitoring. Data from the CDC highlighted that in 2024, 4.2% of U.S. adults were affected by conditions like COPD, emphysema, and chronic bronchitis, with prevalence rates being notably higher in nonmetropolitan areas.

Projected to grow at a 7.98% CAGR through 2031, the pediatric segment is the fastest-growing age group in the U.S. pulse oximeters market. This growth is driven by needs in neonatal intensive care, evaluations for pediatric sleep apnea, and post-operative monitoring. However, pediatric and neonatal devices come with heightened design and validation challenges. Factors like smaller fingers, thinner tissue, and variable perfusion necessitate distinct sensor designs compared to adult platforms.

By End User: Home Healthcare’s Structurally Superior Growth Reflects Care-Setting Shift

In 2025, hospitals commanded 41.23% of the revenue, reinforcing their leading position in the U.S. pulse oximeters market. This dominance is attributed to the extensive use of hospital-grade monitoring in surgical suites, ICUs, recovery units, and vital sign workflows. Hospital procurement is often influenced by long replacement cycles, standardization choices, and multi-device contracts with integrated delivery networks. While hospitals remain a significant and stable value pool, their unit growth has plateaued in the broader U.S. pulse oximeters market.

Forecasted to expand at an 8.10% CAGR through 2031, home healthcare is emerging as the fastest-growing end-user category in the U.S. pulse oximeters market. This surge is bolstered by factors like Medicare's support for remote patient monitoring, earlier patient discharges, an aging population, and a growing preference for at-home recovery. In 2024, nearly 1 million Medicare beneficiaries availed of RPM services, with oxygen saturation monitoring being a key parameter.

By Application: Sleep Apnea Screening Leads Growth as Respiratory Monitoring Anchors Revenue

In 2025, respiratory disease monitoring accounted for 35.45% of the revenue, making it the leading application in the U.S. pulse oximeters market. This segment encompasses a range of activities, from monitoring COPD exacerbations and managing asthma to ongoing respiratory surveillance in both institutional and home environments. The demand is underscored by the significant burden of respiratory diseases, with conditions like COPD, emphysema, and chronic bronchitis affecting 4.2% of U.S. adults in 2024. Given the recurring nature of respiratory disease management, there's a sustained demand for longer device use cycles and ongoing sensor replacements.

Forecasted to grow at a 6.98% CAGR through 2031, sleep apnea screening is emerging as the fastest-growing application in the U.S. pulse oximeters market. This growth is fueled by the vast pool of undiagnosed obstructive sleep apnea (OSA), estimated at 83.7 million U.S. adults in 2024. The application is also reaping benefits from a shift towards home sleep diagnostics, moving away from exclusive lab testing, with overnight oximetry playing a pivotal role.

Geography Analysis

The United States pulse oximeters market exhibits regional demand variations. The South and Appalachian corridor face a higher respiratory disease burden, with 2024 COPD prevalence at 10.6% in nonmetropolitan areas compared to 5.4% in large metropolitan areas. States like West Virginia, Kentucky, Mississippi, and Alabama show increased per-capita demand for home monitoring devices and oxygen-related follow-ups. However, connected device adoption in rural Southern markets has been slower due to uneven RPM infrastructure, though cellular-enabled devices are bridging this gap by reducing reliance on fixed broadband.

The Northeast significantly influences procurement trends in the United States pulse oximeters market. States such as New York, Massachusetts, Pennsylvania, and New Jersey benefit from dense hospital networks, consolidated health systems, and early adoption of integrated monitoring platforms. These regions often set procurement benchmarks for the rest of the country. Additionally, an aging population, with older adults outnumbering children in states like Delaware and Pennsylvania in 2024, drives demand for hospital-grade devices and home healthcare monitoring solutions.

The Midwest is emerging as a growth hub for post-acute and home health applications in the United States pulse oximeters market. Aging rural populations, strong durable medical equipment networks, and high Medicare Advantage penetration are expanding RPM adoption. In the West, states like California, Washington, and Oregon lead in telehealth integration and app-connected monitoring. California’s diverse population emphasizes skin-tone accuracy in procurement, aligning with the FDA’s updated standards and pushing health systems toward compliant next-generation platforms with stricter data and privacy protocols.

Competitive Landscape

Premium clinical settings dominate the United States pulse oximeters market, surpassing consumer and lower-acuity channels. Masimo has established itself as a leader in hospital-grade pulse oximetry through its SET platform, which was utilized by all top-10 United States hospitals in 2025, as ranked by Newsweek. This dominance strengthens Masimo's position in acute care, while the broader market remains fragmented across home, retail, and basic monitoring segments. Danaher’s USD 9.9 billion acquisition of Masimo in February 2026 is a significant strategic move, further integrating Masimo’s intellectual property into a larger diagnostics group with extensive clinical reach.

Recent developments indicate that platform depth is driving competition more than standalone device sales. In September 2025, Masimo and Philips expanded their partnership to integrate pulse oximetry, Radius PPG, and AI-based monitoring into Philips' patient monitoring systems and future wearable solutions. Baxter’s launch of the Welch Allyn Connex 360 in September 2025 highlights this trend by combining SpO2 capture with vital signs monitoring and cloud-based workflow integration. Nonin Medical also enhanced its position in August 2025 by introducing the Nonin Health cloud platform for home overnight oximetry, linking hardware to DME and sleep workflow management.

Opportunities remain in the United States pulse oximeters market, particularly for cellular-native RPM devices and neonatal-specific high-accuracy products, which address workflow and validation gaps not fully resolved by Bluetooth and adult-focused devices. Smart rings and wellness wearables face clinical limitations, with independent research showing a 3.55% RMSE for ring-worn devices compared to clinical references. This accuracy gap underscores the distinction between FDA-cleared pulse oximeters and consumer wellness devices. Established players with regulatory expertise, hospital relationships, and connected workflow capabilities continue to dominate higher-value segments of the market.

U.S. Pulse Oximeters Industry Leaders

Masimo Corporation

Medtronic plc

GE HealthCare

Koninklijke Philips N.V.

Nihon Kohden Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Danaher Corporation finalized an agreement to acquire Masimo Corporation for an enterprise value of approximately USD 9.9 billion. The transaction, valued at nearly 18 times the estimated 2027 EBITDA, underscores the strategic importance of Masimo's sensor intellectual property and its established clinical pulse oximetry presence in U.S. acute care settings.

- September 2025: Masimo and Royal Philips expanded their strategic partnership, extending through 2026 and beyond. The collaboration focuses on integrating Masimo's SET pulse oximetry, Radius PPG, and AI-based monitoring into Philips' multi-parameter patient monitors and next-generation wearable solutions, as well as co-developing advanced AI monitoring technologies.

- September 2025: Baxter International launched the Welch Allyn Connex 360 Vital Signs Monitor in the United States after receiving FDA 510(k) clearance. The device, designed for adults, pediatrics, and neonates, incorporates a Masimo SpO2 module, transmits data to hospital EMR systems via Baxter's DeviceBridge cloud platform, and is intended for use in hospitals, health systems, and ambulatory care settings.

- August 2025: Nonin Medical introduced the Nonin Health cloud platform in the United States, enabling home overnight pulse oximetry. The platform connects the WristOx2 Model 3150 via Bluetooth to a mobile app and is tailored for the U.S. DME, sleep lab, and home health markets.

U.S. Pulse Oximeters Market Report Scope

As per the scope of the report, a pulse oximeter is a painless, non-invasive device used to measure your heart rate and the oxygen saturation level (SPO2) in your blood. It shines light through your skin (usually on a fingertip) to estimate how efficiently your body is transporting oxygen.

The U.S. pulse oximeters market is segmented by product type, technology, measurement mode, patient age group, end-user, and application. By product type, the market includes fingertip pulse oximeters, handheld pulse oximeters, tabletop and bedside pulse oximeters, wrist-worn pulse oximeters, and portable and palm-sized pulse oximeters. By technology, the market is segmented into conventional pulse oximeters, smart pulse oximeters, connected and wireless pulse oximeters, and wearable pulse oximeters. By measurement mode, the market is categorized into spot-check monitoring and continuous monitoring. By patient age group, the market is segmented into adult, pediatric, and neonatal. By end-user, the market includes hospitals, home healthcare, ambulatory surgical centers, and others. By application, the market is segmented into respiratory disease monitoring, cardiac monitoring, perioperative monitoring, sleep apnea screening, and others. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Fingertip Pulse Oximeters |

| Handheld Pulse Oximeters |

| Tabletop and Bedside Pulse Oximeters |

| Wrist-Worn Pulse Oximeters |

| Portable and Palm-Sized Pulse Oximeters |

| Conventional Pulse Oximeters |

| Smart Pulse Oximeters |

| Connected and Wireless Pulse Oximeters |

| Wearable Pulse Oximeters |

| Spot-Check Monitoring |

| Continuous Monitoring |

| Adult |

| Pediatric |

| Neonatal |

| Hospitals |

| Home Healthcare |

| Ambulatory Surgical Centers |

| Others |

| Respiratory Disease Monitoring |

| Cardiac Monitoring |

| Perioperative Monitoring |

| Sleep Apnea Screening |

| Others |

| By Product Type | Fingertip Pulse Oximeters |

| Handheld Pulse Oximeters | |

| Tabletop and Bedside Pulse Oximeters | |

| Wrist-Worn Pulse Oximeters | |

| Portable and Palm-Sized Pulse Oximeters | |

| By Technology | Conventional Pulse Oximeters |

| Smart Pulse Oximeters | |

| Connected and Wireless Pulse Oximeters | |

| Wearable Pulse Oximeters | |

| By Measurement Mode | Spot-Check Monitoring |

| Continuous Monitoring | |

| By Patient Age Group | Adult |

| Pediatric | |

| Neonatal | |

| By End User | Hospitals |

| Home Healthcare | |

| Ambulatory Surgical Centers | |

| Others | |

| By Application | Respiratory Disease Monitoring |

| Cardiac Monitoring | |

| Perioperative Monitoring | |

| Sleep Apnea Screening | |

| Others |

Key Questions Answered in the Report

What is the current value of the U.S. pulse oximeters market in 2026?

The U.S. pulse oximeters market is valued at USD 1.03 billion in 2026 and is forecast to reach USD 1.33 billion by 2031 at a 5.10% CAGR.

Which product category leads pulse oximeter demand in the United States?

Fingertip pulse oximeters led by product type with a 31.1% revenue share in 2025 because they remain low cost and easy to use across clinical and home settings.

Which end-user group is growing fastest for pulse oximeters in the United States?

Home healthcare is the fastest-growing end-user segment with an 8.10% CAGR through 2031, supported by RPM reimbursement, aging demographics, and earlier hospital discharge.

Why is sleep apnea important for pulse oximeter demand in the United States?

Sleep apnea screening is growing at a 6.98% CAGR through 2031, supported by an estimated 83.7 million U.S. adults with OSA in 2024, many of whom were undiagnosed.

How is FDA regulation changing the pulse oximeter landscape in the United States?

The FDA's revised expectations on skin-tone accuracy and larger validation studies are encouraging hospitals to replace older devices with premium, better-validated systems.

Which technology trend is shaping future demand for pulse oximeters?

Connected and wireless pulse oximeters are projected to grow at a 7.45% CAGR through 2031 because providers increasingly want devices that link directly to EMR and RPM workflows.

Page last updated on: