Cardiac Marker Testing Products Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

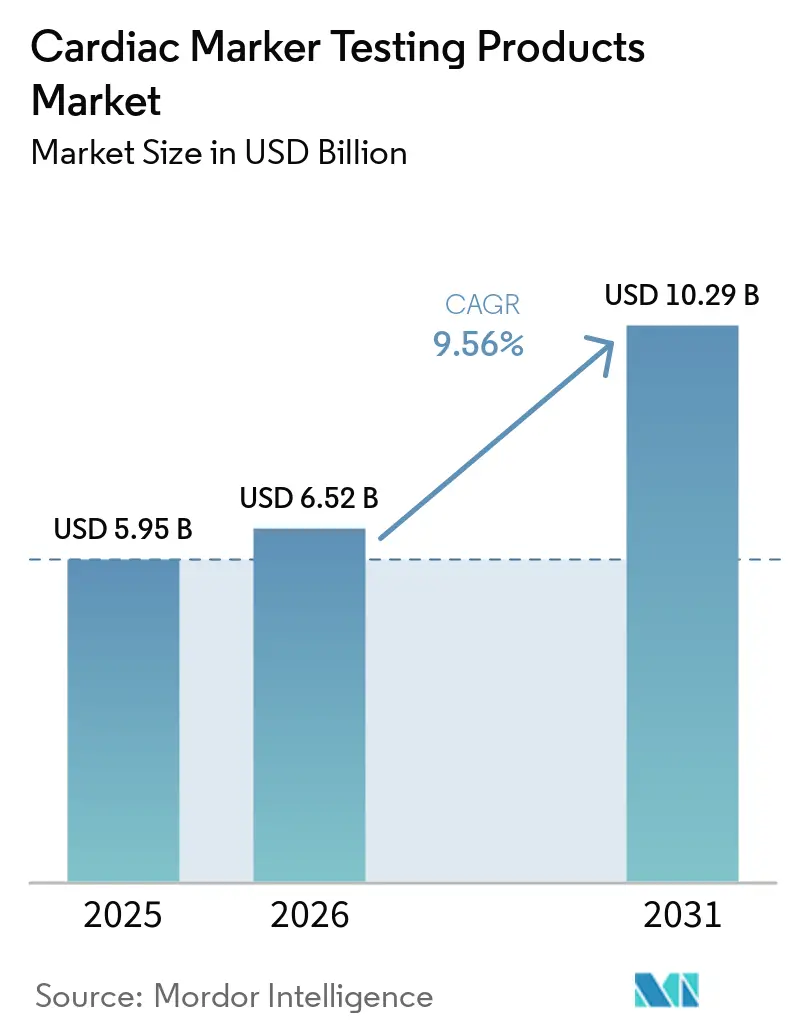

| Market Size (2026) | USD 6.52 Billion |

| Market Size (2031) | USD 10.29 Billion |

| Growth Rate (2026 - 2031) | 9.56% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cardiac Marker Testing Products Market Analysis by Mordor Intelligence

The Cardiac Marker Testing Products Market size was valued at USD 5.95 billion in 2025 and is estimated to grow from USD 6.52 billion in 2026 to reach USD 10.29 billion by 2031, at a CAGR of 9.56% during the forecast period (2026-2031).

The market is expanding against a persistent cardiovascular disease burden that continues to keep acute cardiac evaluation high on hospital priority lists. Faster rule-out pathways are changing how tests are ordered because clinicians now need results sooner and with higher confidence, which is increasing test volumes and shifting demand toward more advanced assay formats. The market is also moving toward care models that support near-patient use, tighter integration with digital workflows, and broader use of multi-marker testing when single-marker approaches are not enough. Competitive activity is centered on platform depth, assay performance, workflow fit, and the ability to serve both centralized laboratories and decentralized settings. That combination is keeping the cardiac marker testing products market attractive for companies that can pair installed platforms with recurring reagent revenue while also widening access across emergency, outpatient, and emerging care environments.

Key Report Takeaways

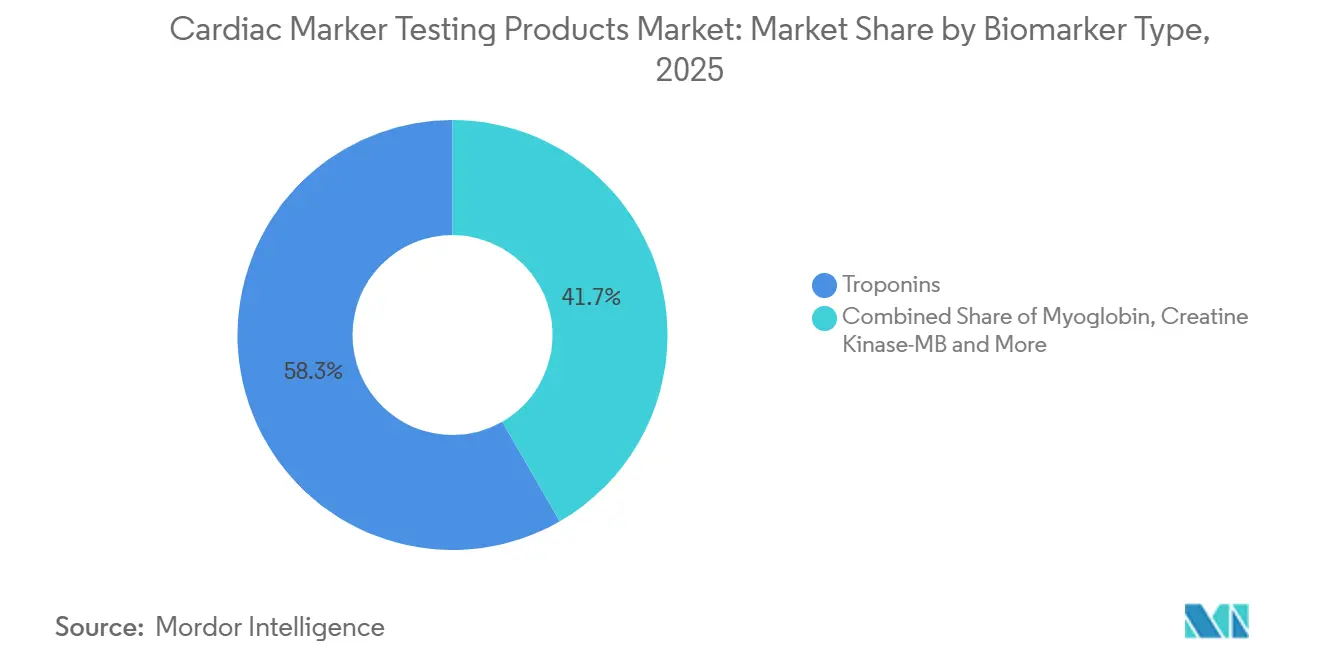

- By biomarker type, troponins held 58.31% of the cardiac marker testing products market share in 2025, while ischemia-modified albumin is forecast to grow at a 12.38% CAGR through 2031.

- By product, reagents and kits accounted for 67.24% of cardiac marker testing products market size in 2025, while instruments are projected to expand at a 10.52% CAGR through 2031.

- By technology, chemiluminescence led with a 40.52% share in 2025, while immunofluorescence is expected to advance at an 11.25% CAGR through 2031.

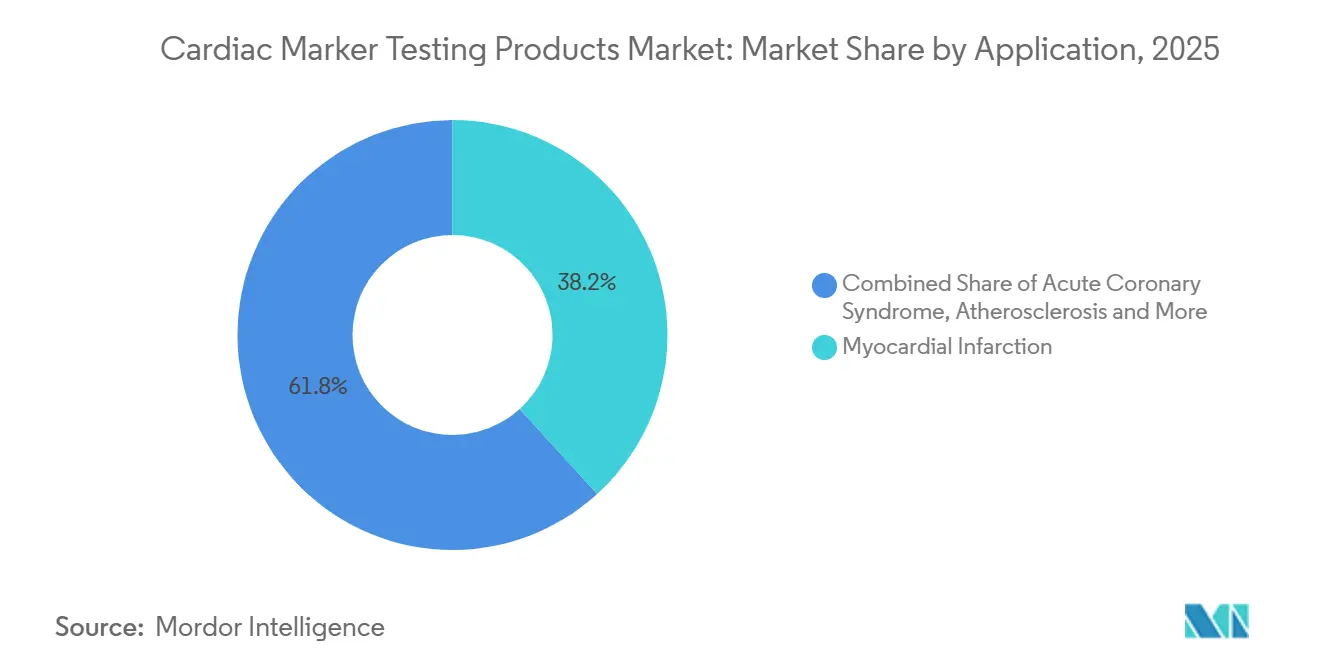

- By application, myocardial infarction represented 38.24% of demand in 2025, while acute coronary syndrome is forecast to grow at a 12.52% CAGR through 2031.

- By location of testing, central laboratory testing captured 59.52% of revenue in 2025, while point-of-care testing is projected to expand at a 13.55% CAGR through 2031.

- By end user, hospitals accounted for 53.56% of revenue in 2025, while home healthcare settings are expected to record a 13.85% CAGR through 2031.

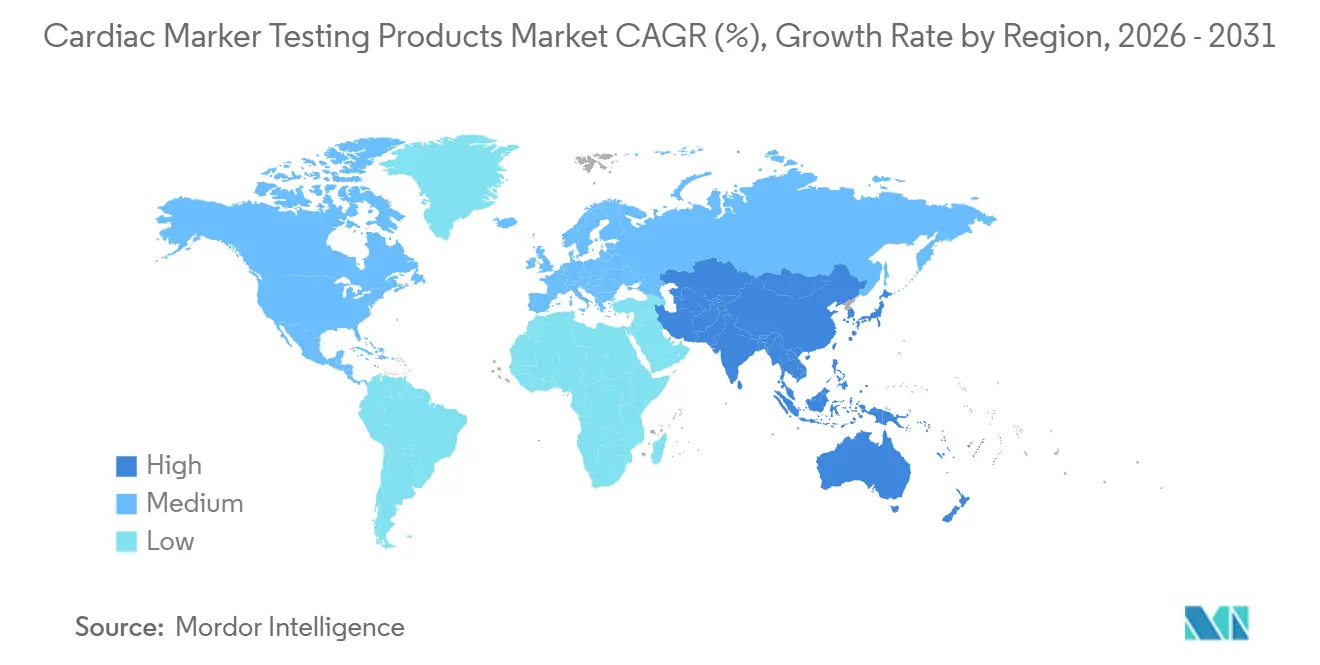

- By geography, North America held 41.22% of the cardiac marker testing products market in 2025, while Asia-Pacific is forecast to grow at a 13.65% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cardiac Marker Testing Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Cardiovascular Disease Burden and Earlier Rule-Out Demand | +2.5% | Global, with highest intensity in North America, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| High-Sensitivity Troponin Adoption Across Emergency Care | +2.2% | North America and Europe, with accelerating spillover into Asia-Pacific | Medium term (2-4 years) |

| Expansion of Point-of-Care and Near-Patient Testing | +1.8% | Global, with fastest uptake in core Asia-Pacific and spillover to the Middle East and Africa | Medium term (2-4 years) |

| Greater Use of Multiplex and Algorithm-Linked Biomarker Panels | +1.0% | North America, Europe, and Japan | Long term (≥ 4 years) |

| AI-Assisted Risk Stratification Linked to EHR Workflows | +0.7% | North America and the European Union, with early adoption in Australia and South Korea | Long term (≥ 4 years) |

| At-Home and Decentralized Cardiac Testing Formats | +0.5% | North America first, with growing adoption in Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Cardiovascular Disease Burden and Earlier Rule-Out Demand

The cardiac marker testing products market is being supported by a large and persistent global cardiovascular disease load that keeps emergency cardiac evaluation central to routine care. A rising share of patients now arrive with multiple metabolic and age-related conditions, which makes clean symptom interpretation harder and pushes clinicians toward broader biochemical assessment. That clinical reality weakens the practicality of single-marker strategies in many presentations and strengthens demand for test menus that can support faster and more reliable decisions. In higher-burden care systems, accelerated diagnostic pathways are becoming part of standard clinical behavior rather than optional practice variation. This shift is especially important for the cardiac marker testing products market because it turns cardiac biomarker ordering into a more regular and protocol-linked activity across emergency settings.

High-Sensitivity Troponin Adoption Across Emergency Care

High-sensitivity cardiac troponin assays are a major demand catalyst because they improve the speed and operational value of cardiac assessment in emergency departments. A 2025 retrospective study covering 32,076 emergency department patient visits found that high-sensitivity troponin I implementation reduced median hospital length of stay from 6.6 hours to 6.0 hours, lowered admission rates from 38.2% to 32.6%, reduced weekly cardiology consultations across 3 emergency departments by 2.8, and supported capacity for 1,600 additional annual visits. These outcomes matter for the cardiac marker testing products market because they link assay adoption to better throughput, lower congestion, and measurable cost relief rather than only to analytical performance. The broad use of accelerated diagnostic algorithms built around high-sensitivity troponin also makes demand more resistant to short-term discretionary spending pressure. Assays that satisfy recognized high-sensitivity performance expectations are gaining added weight in tender and purchasing decisions, which supports premium positioning for a limited group of qualified platforms.

Expansion of Point-of-Care and Near-Patient Testing

The cardiac marker testing products market is also being reshaped by a move from purely centralized testing toward bedside, ambulance, and community-based evaluation. A 2026 study in Light: Science & Applications described a dual-mode multiplexed paper-based optical sensor that detected 3 cardiac biomarkers at the point of care, with a reader that could be assembled for USD 260, showing how affordability is becoming part of future decentralized design. Established vendors are also pushing performance standards higher, and Siemens Healthineers reported that the Atellica VTLi system can deliver high-sensitivity troponin I results from a fingerstick sample in 8 minutes. A 2025 CADTH rapid review found that point-of-care troponin use in rural and remote settings in Australia and New Zealand had clinical utility when supported by clear governance and quality frameworks, which gives health systems a practical model for safe deployment[1]Canadian Agency for Drugs and Technologies in Health, “Troponin Point-of-Care Testing, A Rapid Review,” CADTH, cda-amc.ca. As a result, companies that can support both automated laboratory workflows and compact near-patient platforms are building a stronger position across the cardiac marker testing products market than firms tied to only one testing format.

Greater Use of Multiplex and Algorithm-Linked Biomarker Panels

The cardiac marker testing products market is gaining from wider use of panels that combine several biomarkers when a single analyte cannot capture the full clinical picture. A 2025 Nature Communications study reported that biomarker panels improved cardiovascular risk prediction in atrial fibrillation patients and delivered better discriminatory ability than conventional clinical scores alone. A 2025 individual-participant meta-analysis published in the Journal of the American College of Cardiology and covering more than 62,000 participants confirmed that adding troponin T or I to conventional risk factors materially improved discrimination for first-onset cardiovascular disease. When panel outputs are tied to electronic health record workflows and decision support, clinicians can move faster from result review to care escalation or discharge decisions. That matters commercially because broader panels raise reagent use per encounter and reinforce platform loyalty, which favors companies with menu breadth, workflow integration, and strong installed systems across the cardiac marker testing products market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Clinical Validation and IVDR-FDA Compliance Burden | -1.0% | Europe for IVDR, the United States for FDA laboratory developed test oversight, with wider effects on access timelines | Long term (≥ 4 years) |

| Limited Specificity and False-Positive Interpretations in Real-World Use | -0.8% | Global, especially acute care settings in North America and Europe | Medium term (2-4 years) |

| Reimbursement Pressure on High-Frequency Biomarker Testing | -0.6% | North America, with additional pressure from national assessment bodies in Europe | Medium term (2-4 years) |

| Fragmented Care Pathways That Slow Standardized Adoption | -0.5% | Asia-Pacific, the Middle East and Africa, South America, and rural care segments in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Clinical Validation and IVDR-FDA Compliance Burden

Regulatory compliance has become a heavier operating burden for the cardiac marker testing products market, especially for smaller companies that do not have the same study budgets or regulatory teams as larger incumbents. In the United States, the FDA final rule on laboratory developed tests introduced a phased compliance framework that adds medical device reporting, quality system, complaint handling, and later submission requirements to tests that had previously operated under a different oversight model. These requirements lengthen development planning, raise documentation costs, and can delay the commercial path for novel biomarkers or expanded claims. The burden is even harder when manufacturers must prepare evidence packages that satisfy more than one regulatory framework across key geographies. That delay matters for the cardiac marker testing products market because slower approvals can postpone product launches, limit geographic expansion, and give established vendors more time to defend installed accounts[2]U.S. Food and Drug Administration, “Medical Devices, Laboratory Developed Tests,” Federal Register, govinfo.gov.

Limited Specificity and False-Positive Interpretations in Real-World Use

The growing analytical sensitivity of high-sensitivity troponin assays has improved early detection, but it has also increased the frequency of clinically difficult positive findings that are not caused by acute myocardial infarction. A 2026 case report in JACC: Case Reports described how a false-positive high-sensitivity troponin I result triggered anticoagulation, patient transfer, invasive procedures, and unnecessary hospitalization in a setting without on-site cardiac services. Reviews published in 2024 and 2025 also noted that heterophile antibodies, fibrin clots, rheumatoid factors, and skeletal muscle cross-reactivity can still interfere with interpretation and reduce confidence in real-world use. These issues push hospitals toward repeat measurements, delta calculations, or reflex-testing rules before treatment decisions are made. That response protects patient care, but it can also reduce revenue per low-risk episode and limit volume growth in outpatient and lower-acuity settings across the cardiac marker testing products market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Biomarker Type: Troponins Anchor Revenue as IMA Gains Clinical Ground

Troponins accounted for 58.31% of revenue in 2025, which kept them at the center of the cardiac marker testing products market. Their lead reflects long-standing clinical validation, guideline acceptance, and deep integration into both central laboratory systems and newer point-of-care formats. High-sensitivity versions have widened troponin use because they support earlier detection and faster rule-out in patients who present with suspected acute coronary events. Roche stated that its Gen 5 assay was the first FDA-cleared high-sensitivity cardiac troponin test to meet recognized high-sensitivity criteria, which helped strengthen the commercial case for premium troponin-based workflows[3]Roche Diagnostics, “Elecsys Troponin T Gen 5,” Roche Diagnostics, diagnostics.roche.com. That installed-base advantage continues to support recurring demand in the cardiac marker testing products market as hospitals standardize protocols around assays that can fit both speed and precision requirements.

Ischemia-modified albumin is forecast to expand at a 12.38% CAGR through 2031, which makes it the fastest-growing biomarker segment in the cardiac marker testing products market. Its appeal comes from a clinical gap that troponin does not fully close because ischemia-modified albumin is better aligned with reversible ischemia before myocardial necrosis occurs. This is particularly relevant in transient ischemic episodes and in cases where clinicians want broader risk context before tissue injury becomes more obvious. CK-MB, myoglobin, and related markers still have a role in multiplex panels and in settings where high-sensitivity troponin adoption is slower, but reimbursement behavior is narrowing their standalone value. Blue Cross Blue Shield of Texas stated in its 2025 policy that CK-MB and myoglobin were excluded from reimbursement for acute coronary syndrome diagnosis, which points to a faster move away from legacy marker use in higher-income markets. The cardiac marker testing products market remains anchored in troponin, but future mix improvement depends on whether newer biomarkers can secure a clearer role inside protocol-driven care pathways.

By Product: Reagents Drive Volume, Instruments Expand Platform Footprint

Reagents and kits represented 67.24% of revenue in 2025, which made them the largest product category in the cardiac marker testing products market. This lead reflects the basic economics of immunoassay testing because every patient run requires reagent packs, calibrators, and quality controls regardless of whether the analyzer is already placed. That recurring consumption model gives large vendors a stable revenue floor once a platform is installed inside a hospital or laboratory network. It also explains why capital placement campaigns remain aggressive, since favorable analyzer terms can be recovered over time through predictable consumable demand. The cardiac marker testing products market therefore continues to reward companies that can protect installed analyzers and keep utilization high across routine and urgent testing volumes.

Instruments are projected to grow at a 10.52% CAGR from 2026 to 2031, which makes them the faster-growing product group even though they trail in current revenue. Growth is being supported by new laboratory build-outs, hospital modernization programs, and analyzer placements in regions where diagnostic capacity is still expanding. This is especially relevant in Asia-Pacific, the Middle East, and South America, where new hospitals and independent laboratories are adding automated immunoassay capability. The pull effect is important because once instruments are placed in lower-acuity settings such as clinics and pharmacies, they bring future reagent demand into care environments that were previously underpenetrated. This part of the cardiac marker testing products industry is also shaped by tighter procurement screens because buyers are paying closer attention to quality systems, validation strength, and evidence of regulatory readiness before approving new platforms.

By Technology: Chemiluminescence Leads, Immunofluorescence Grows Through POC Integration

Chemiluminescence held a 40.52% share in 2025, which kept it as the largest technology segment in the cardiac marker testing products market. Its position rests on high analytical precision, broad compatibility with automated systems, and strong suitability for high-throughput central laboratories. These features make chemiluminescence the preferred format in settings where hospitals need rapid processing of large daily cardiac sample volumes. Roche reported at ESC 2025 that its sixth-generation Elecsys Troponin T high-sensitivity Gen 6 assay, a chemiluminescent immunoassay validated in the TSIX study program of more than 13,000 participants, showed high precision for acute myocardial infarction identification and rule-out. That level of evidence helps explain why chemiluminescence remains central to premium laboratory positioning in the cardiac marker testing products market.

Immunofluorescence is forecast to grow at an 11.25% CAGR from 2026 to 2031, which makes it the fastest-growing technology category. Its momentum is tied to compact cartridge-based analyzers that work well in emergency departments, ambulances, and remote facilities where refrigeration and specialized lab staffing may be limited. These formats are well matched to the wider movement toward point-of-care use because they bring faster decisions closer to the patient. ELISA, immunochromatography, and other methods continue to matter in research, lower-cost settings, and selected regional use cases, but they do not carry the same growth profile. The cardiac marker testing products market is therefore moving toward a split model where chemiluminescence remains the backbone for centralized throughput while immunofluorescence captures more decentralized and near-patient demand.

By Application: Myocardial Infarction Dominates, ACS Protocols Drive Fastest Growth

Myocardial infarction accounted for 38.24% of demand in 2025, which made it the largest application in the cardiac marker testing products market. This lead was supported by the fact that suspected or confirmed myocardial infarction remains the most common and most urgent use case for cardiac biomarker testing worldwide. The category benefits from deep clinician familiarity, strong reimbursement support in acute presentations, and clear integration into emergency department protocols. A 2024 analysis cited in JAMA Internal Medicine indicated that cardiac biomarker testing occurred in nearly 7% of all United States emergency department visits and in 25.6% of chest pain presentations, showing the scale of acute use. This makes myocardial infarction the base demand engine that continues to stabilize the broader cardiac marker testing products market.

Acute coronary syndrome is forecast to grow at a 12.52% CAGR through 2031, which makes it the fastest-growing application segment. Its growth is tied to faster rule-in and rule-out pathways that rely on high-sensitivity troponin as the main diagnostic anchor during early evaluation. Because these pathways are becoming more standardized across emergency medicine, demand is becoming less discretionary and more protocol-linked than it was in earlier testing models. That matters commercially because protocol-driven use tends to increase ordering consistency and supports regular reagent pull-through. The cardiac marker testing products market is therefore gaining not only from more patients being tested, but also from the way care pathways are being structured around early biomarker evidence.

By Location of Testing: Central Labs Hold Share as POC Redefines Access

Central laboratory testing held 59.52% of revenue in 2025, which gave it the largest share in the cardiac marker testing products market size. That leadership reflects high sample throughput, automation efficiency, and the tighter quality oversight that large laboratories can maintain. A 2025 peer-reviewed analysis of propensity-matched emergency department patients found that a high-sensitivity cardiac troponin I protocol reduced median emergency department length of stay from 28 hours to 4 hours, lowered cardiology consultations from 30% to 4%, reduced echocardiography use from 39.3% to 6.7%, and kept 30-day acute coronary syndrome readmissions at 0%. Those results show that centralized high-sensitivity protocols can deliver major operational benefits without requiring every site to shift immediately into decentralized testing. For much of the cardiac marker testing products market, central labs therefore remain the core delivery model when volume, oversight, and menu breadth are the main priorities.

Point-of-care testing is projected to grow at a 13.55% CAGR from 2026 to 2031, which makes it the fastest-growing testing-location segment. Growth is being supported by emergency use cases where faster sample-to-answer time can change triage decisions, discharge timing, and transfer needs. The performance gap between laboratory and point-of-care systems is narrowing as vendors bring higher analytical quality into smaller devices. Siemens Healthineers reported 8-minute fingerstick high-sensitivity troponin I results from the Atellica VTLi platform, while bioMérieux's acquisition of SpinChip brought a 10-minute whole-blood high-sensitivity troponin I platform under a larger commercial organization.

By End User: Hospitals Dominate, Home Healthcare Enters the Growth Curve

Hospitals accounted for 53.56% of revenue in 2025, which kept them as the largest end-user segment in the cardiac marker testing products market. Their lead reflects the concentration of acute cardiac presentations, reimbursement support for urgent episodes, and the clinical complexity of in-hospital cardiac care. Hospitals also benefit from laboratory infrastructure that can support broad biomarker menus, serial testing, and confirmatory workflows when results are borderline or clinically ambiguous. Diagnostic laboratories remained the second-largest end-user group, but they are operating under tighter reimbursement scrutiny when outpatient biomarker lists become narrower. This means the cardiac marker testing products market still depends heavily on hospital demand for its base revenue and for ongoing adoption of newer assay formats.

Home healthcare settings are projected to grow at a 13.85% CAGR from 2026 to 2031, making them the fastest-growing end-user segment even from a small base. Growth reflects a real but still early move toward decentralized cardiac assessment where parts of monitoring and triage can move outside hospitals. No major diagnostics vendor has yet secured regulatory clearance for a validated at-home cardiac troponin test, which leaves a visible commercial gap. That gap is important because it creates room for partnership, acquisition, or internal development as technology, regulation, and care pathways continue to align. For the cardiac marker testing products market, home healthcare remains more a strategic growth frontier than a current volume center, but the direction of travel is clearly moving toward greater decentralization over time.

Geography Analysis

North America held 41.22% of the cardiac marker testing products market share in 2025, which kept it as the largest regional market. This lead reflects dense laboratory infrastructure, high emergency department testing intensity, and strong use of validated high-sensitivity troponin pathways in acute cardiac presentations. The United States remains the regional anchor because its hospital networks and accredited laboratories can support both broad menu testing and rapid assay upgrades when clinical protocols change. The FDA final rule on laboratory developed tests is also increasing regulatory rigor for cardiac tests, which can shift utilization toward commercially validated in vitro diagnostics over time. CMS policies add commercial pressure because the 2025 physician fee schedule lowered physician reimbursement and the Clinical Laboratory Fee Schedule allows payment reductions of up to 15% annually on laboratory tests from 2026 through 2028.

Europe's commercial direction is being shaped by compliance requirements that raise the value of vendors with strong regulatory readiness and broad service support. That favors companies that can protect existing placements while updating assay menus and automation layers rather than relying only on first-time adoption. Italy, Spain, and the wider rest of Europe are also contributing growth as community hospitals and regional systems widen access to automated cardiac biomarker testing. The United Kingdom remains supportive because chest pain pathways and digital health initiatives continue to favor biomarker-based clinical decision support inside connected care environments.

Asia-Pacific is the fastest-growing regional segment at a 13.65% CAGR from 2026 to 2031, which reflects both rising disease burden and a fast-expanding healthcare base. China and India are central to this trend because hospital construction, laboratory chain expansion, and broader immunoassay adoption are opening more sites to high-sensitivity troponin and panel testing. Japan also supports regional demand because its aging population keeps cardiac diagnostics clinically important across hospital and ambulatory settings. Outside Asia-Pacific, the Middle East and Africa are seeing stronger procurement of advanced cardiac platforms in the Gulf, while South America is being led by Brazil's private hospital networks and more selective analyzer-compatible purchasing in financially constrained markets. Together, these patterns show that the cardiac marker testing products market is still largest in mature systems but is growing fastest where laboratory capacity, hospital infrastructure, and decentralized access are all expanding at the same time.

Competitive Landscape

The cardiac marker testing products market is moderately consolidated at the global platform level, with Roche Diagnostics, Abbott Laboratories, and Siemens Healthineers holding strong positions in central laboratory cardiac testing. Their advantage comes from broad automated immunoassay menus, long hospital relationships, and the ability to bundle cardiac assays with wider laboratory workflows on the same installed platform. That bundled model raises switching costs because procurement teams often prefer to minimize operational disruption once an analyzer family is in place. Danaher, through Beckman Coulter, remains a significant competitor, while QuidelOrtho is expanding beyond its traditional point-of-care profile toward broader laboratory relevance. The competitive structure of the cardiac marker testing products market therefore combines a stable top tier with a second layer of firms trying to gain share through targeted assay approvals, workflow differentiation, or lower-cost tenders.

Roche strengthened its position in September 2025 when it announced CE Mark approval for the Elecsys Troponin T high-sensitivity Gen 6 assay after validation in the TSIX study program involving more than 13,000 participants. QuidelOrtho added a notable step in November 2025 when it received FDA 510(k) clearance for the VITROS high-sensitivity Troponin I assay, allowing existing VITROS users to upgrade without replacing analyzers. bioMérieux also made a major strategic move in January 2025 through its EUR 138 million (USD 160.6 million) acquisition of SpinChip Diagnostics, bringing a 10-minute whole-blood high-sensitivity troponin I point-of-care platform into a larger regulatory, manufacturing, and commercial structure. These moves show that competition is not only about winning current laboratory contracts but also about controlling the next wave of faster and more distributed cardiac testing formats.

Mid-tier and regional suppliers remain relevant because they can compete on price, localized service, or specific placement opportunities in emerging markets. Shenzhen Mindray Bio-Medical Electronics is increasingly visible in Asia-Pacific and other developing tenders where hospitals want integrated immunoassay systems at lower cost than those of large western vendors. That dynamic pressures the top tier to defend accounts through evidence, workflow fit, post-sales service, and portfolio breadth rather than through list price alone. White-space opportunities still exist in home-based biomarker monitoring and validated consumer-facing cardiac troponin testing, where no major vendor has yet established a dominant position. As a result, the cardiac marker testing products market remains moderately concentrated in core laboratory platforms, but it is still open to competitive change in decentralized care, lower-cost systems, and newer biomarker formats.

Cardiac Marker Testing Products Industry Leaders

Abbott Laboratories

F. Hoffmann-La Roche AG

Siemens Healthineers AG

Danaher Corporation

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Roche received US FDA 510(k) clearance for the cobas c 703 and cobas ISE neo analytical units, next-generation additions to the modular cobas pro integrated solutions delivering up to 1,800 tests per hour; the clearance strengthens Roche's position in high-volume central laboratory cardiac testing workflows across US hospital networks, supporting both throughput efficiency and staff reduction goals amid ongoing laboratory workforce constraints.

- November 2025: QuidelOrtho received US FDA 510(k) clearance for the VITROS hs Troponin I Reagent Pack, intended for quantitative cTnI measurement in plasma to aid MI diagnosis on VITROS immunodiagnostic systems; commercial rollout to US laboratories was targeted for December 2025, expanding the competitive field of FDA-cleared hs-cTnI assays and enabling existing VITROS platform users to upgrade without analyzer replacement.

- September 2025: Roche announced CE Mark approval for the Elecsys Troponin T hs Gen 6 assay, validated in the TSIX study program enrolling more than 13,000 participants; data presented at ESC 2025 and EUSEM 2025 demonstrated high precision for AMI identification and rule-out, setting a new sixth-generation performance benchmark and reinforcing Roche's 30-year troponin heritage as a platform differentiation asset.

Global Cardiac Marker Testing Products Market Report Scope

As per the scope of the report, cardiac marker testing products are diagnostic tools and assays used to detect and measure specific substances in the blood that indicate heart muscle damage or stress. These markers help in diagnosing, assessing, and monitoring cardiac conditions such as myocardial infarction (heart attack), angina, and other acute or chronic heart diseases.

The segmentation of the cardiac marker testing products market is categorized by biomarker type, product, technology, application, testing location, end user, and geography. By biomarker type, the market includes troponins, creatine kinase-MB, myoglobin, ischemia-modified albumin, and other biomarkers. By product, it is segmented into reagents and kits, and instruments. By technology, the market is divided into chemiluminescence, enzyme-linked immunosorbent assay, immunofluorescence, immunochromatography, and other technologies. By application, the segmentation includes myocardial infarction, acute coronary syndrome, congestive heart failure, atherosclerosis, and other applications. By testing location, it is categorized into central laboratory testing and point-of-care testing. By end user, the market is segmented into hospitals, diagnostic laboratories, ambulatory surgery centers and clinics, home healthcare settings, and academic and research institutions. By geography, the market is divided into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Troponins |

| Creatine Kinase-MB |

| Myoglobin |

| Ischemia-Modified Albumin |

| Other Biomarker Types |

| Reagents and Kits |

| Instruments |

| Chemiluminescence |

| Enzyme-Linked Immunosorbent Assay |

| Immunofluorescence |

| Immunochromatography |

| Other Technologies |

| Myocardial Infarction |

| Acute Coronary Syndrome |

| Congestive Heart Failure |

| Atherosclerosis |

| Other Applications |

| Central Laboratory Testing |

| Point-of-Care Testing |

| Hospitals |

| Diagnostic Laboratories |

| Ambulatory Surgery Centers and Clinics |

| Home Healthcare Settings |

| Academic and Research Institutions |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Biomarker Type | Troponins | |

| Creatine Kinase-MB | ||

| Myoglobin | ||

| Ischemia-Modified Albumin | ||

| Other Biomarker Types | ||

| By Product | Reagents and Kits | |

| Instruments | ||

| By Technology | Chemiluminescence | |

| Enzyme-Linked Immunosorbent Assay | ||

| Immunofluorescence | ||

| Immunochromatography | ||

| Other Technologies | ||

| By Application | Myocardial Infarction | |

| Acute Coronary Syndrome | ||

| Congestive Heart Failure | ||

| Atherosclerosis | ||

| Other Applications | ||

| By Location of Testing | Central Laboratory Testing | |

| Point-of-Care Testing | ||

| By End User | Hospitals | |

| Diagnostic Laboratories | ||

| Ambulatory Surgery Centers and Clinics | ||

| Home Healthcare Settings | ||

| Academic and Research Institutions | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current outlook for cardiac marker testing products?

The cardiac marker testing products market stands at USD 6.52 billion in 2026 and is forecast to reach USD 10.29 billion by 2031 at a 9.56% CAGR, supported by sustained cardiovascular disease burden and faster diagnostic workflows.

Which biomarker category leads revenue today?

Troponins remain the leading biomarker type with 58.31% of revenue in 2025 because they are deeply embedded in emergency protocols, laboratory menus, and high-sensitivity assay adoption.

Which testing setting is growing the fastest?

Point-of-care testing is growing the fastest at a 13.55% CAGR through 2031 as hospitals and health systems seek faster triage, broader rural access, and more decentralized care delivery.

Why are reagents and kits larger than instruments?

Reagents and kits held 67.24% of revenue in 2025 because every test run requires recurring consumables, while instrument placements mainly serve as the installed base that drives future reagent pull-through.

Which region has the strongest growth profile?

Asia-Pacific is the fastest-growing region with a 13.65% CAGR from 2026 to 2031, driven by hospital expansion, rising cardiac disease burden, and wider diagnostic investment in China, India, and Japan.

What are the main risks for suppliers and investors?

The main risks are regulatory burden, false-positive interpretation in high-sensitivity assays, and reimbursement pressure, particularly from FDA compliance changes and CMS laboratory payment reductions.

Page last updated on: