Pulse Lavage Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

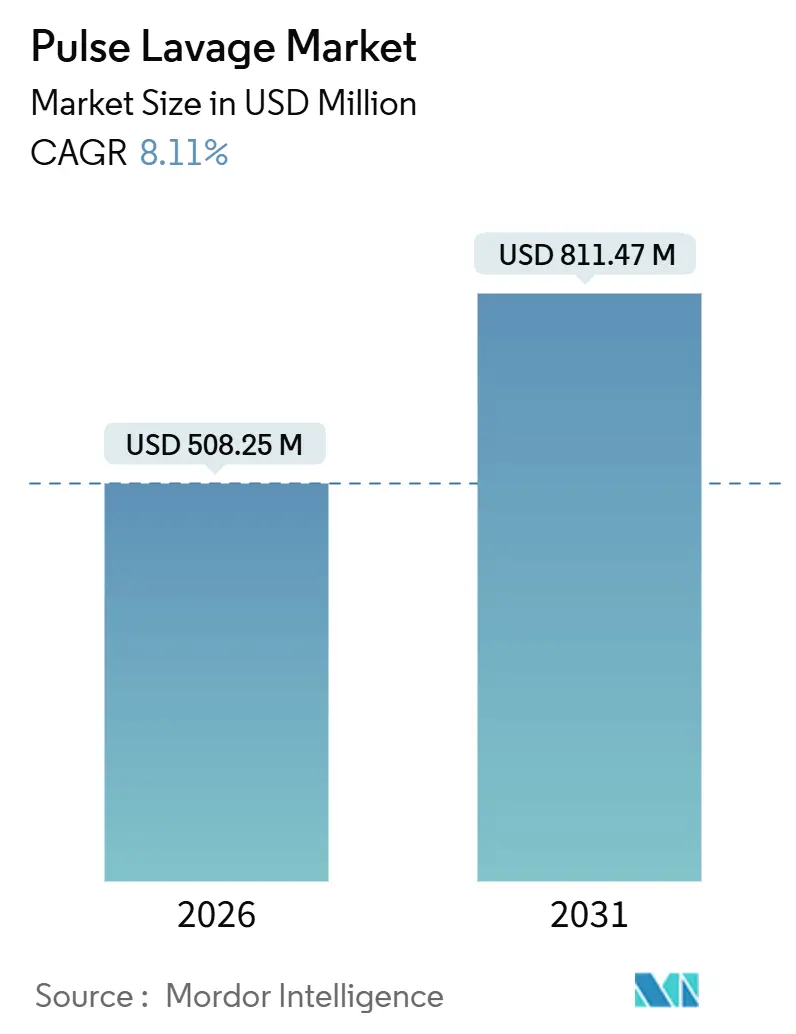

| Market Size (2026) | USD 508.25 Million |

| Market Size (2031) | USD 811.47 Million |

| Growth Rate (2026 - 2031) | 8.11% CAGR |

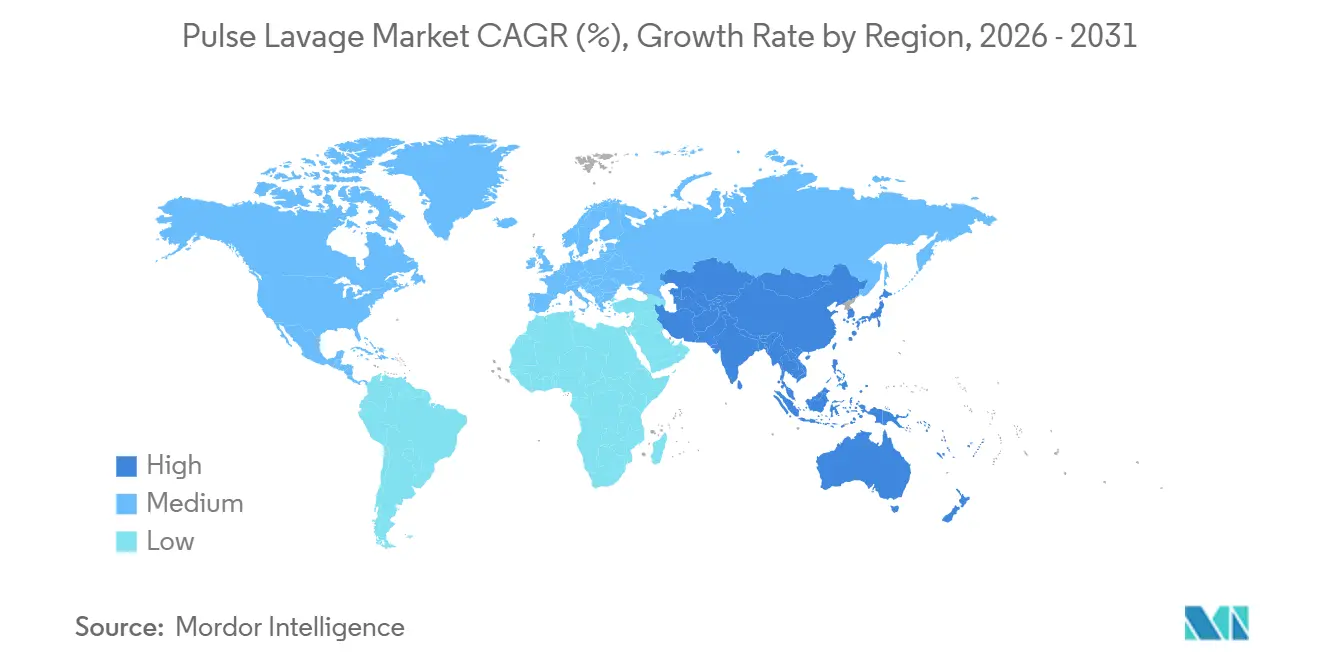

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

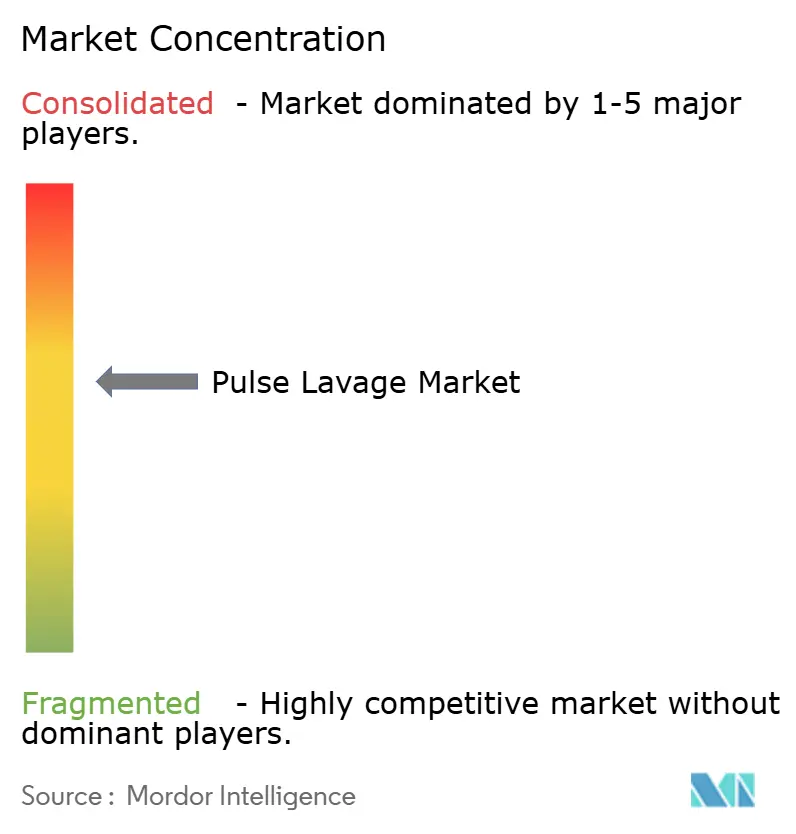

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pulse Lavage Market Analysis by Mordor Intelligence

The Pulse Lavage Market size is estimated at USD 508.25 million in 2026, and is expected to reach USD 811.47 million by 2031, at a CAGR of 8.11% during the forecast period (2026-2031).

Demand is being propelled by growing global surgery volumes tied to population aging, stricter infection-control protocols that mandate mechanical irrigation on checklists, and a decisive shift from corded reusable units to battery-powered disposable or semi-disposable platforms that reduce cross-contamination risk in outpatient settings. Rising procedure counts in orthopedics and trauma continue to provide the revenue base, yet the sharper growth curve in chronic wound care is diversifying use cases beyond joint theaters. Hospitals remain the largest buyers, but ambulatory surgery centers (ASCs) are the fastest-expanding channel as outpatient joint replacements and wound debridement shift to lower-cost care settings. Meanwhile, technology differentiation is migrating to irrigant chemistry, with citrate-based and no-rinse antimicrobial solutions poised to influence purchasing decisions once pivotal trials read out.

Key Report Takeaways

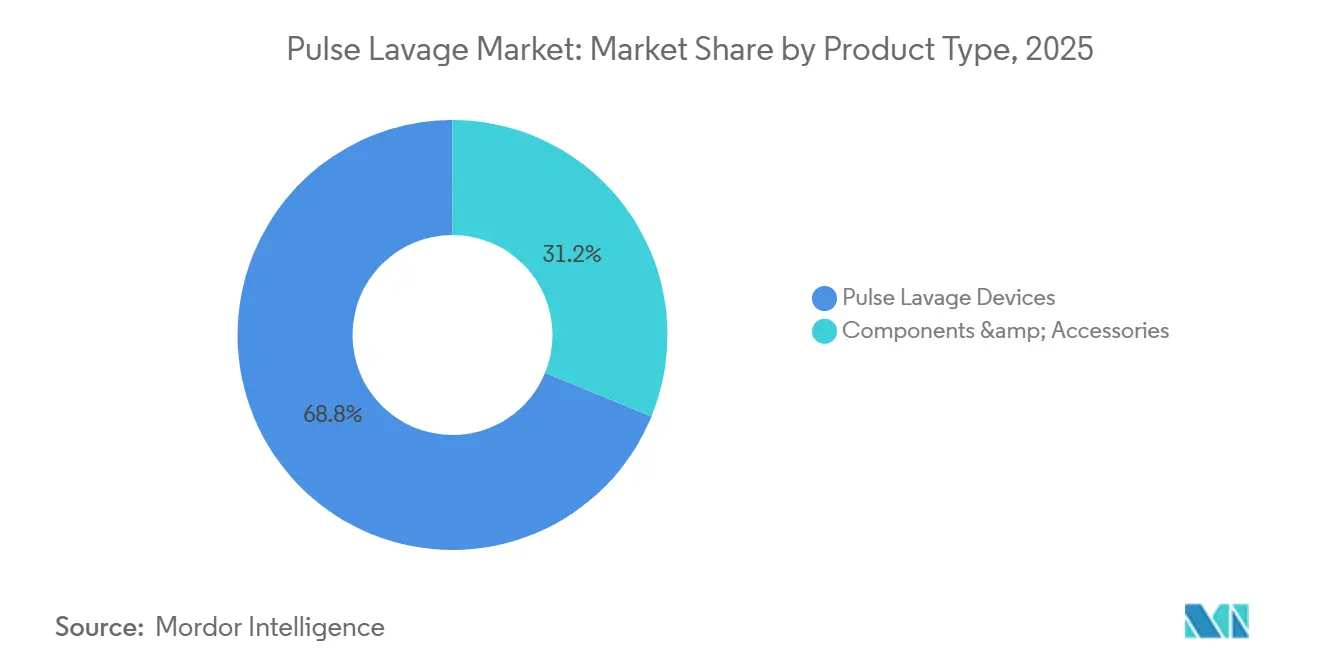

- By product type, pulse lavage devices led with 68.82% revenue share in 2025, while accessories are projected to expand at a 10.34% CAGR through 2031.

- By usability, disposable systems held 60.254% of the pulse lavage market share in 2025, whereas semi-disposables are forecast to post the fastest 10.76% CAGR to 2031.

- By power source, battery-powered units accounted for 55.43% of revenue in 2025 and are anticipated to grow at a 10.21% CAGR during the outlook period.

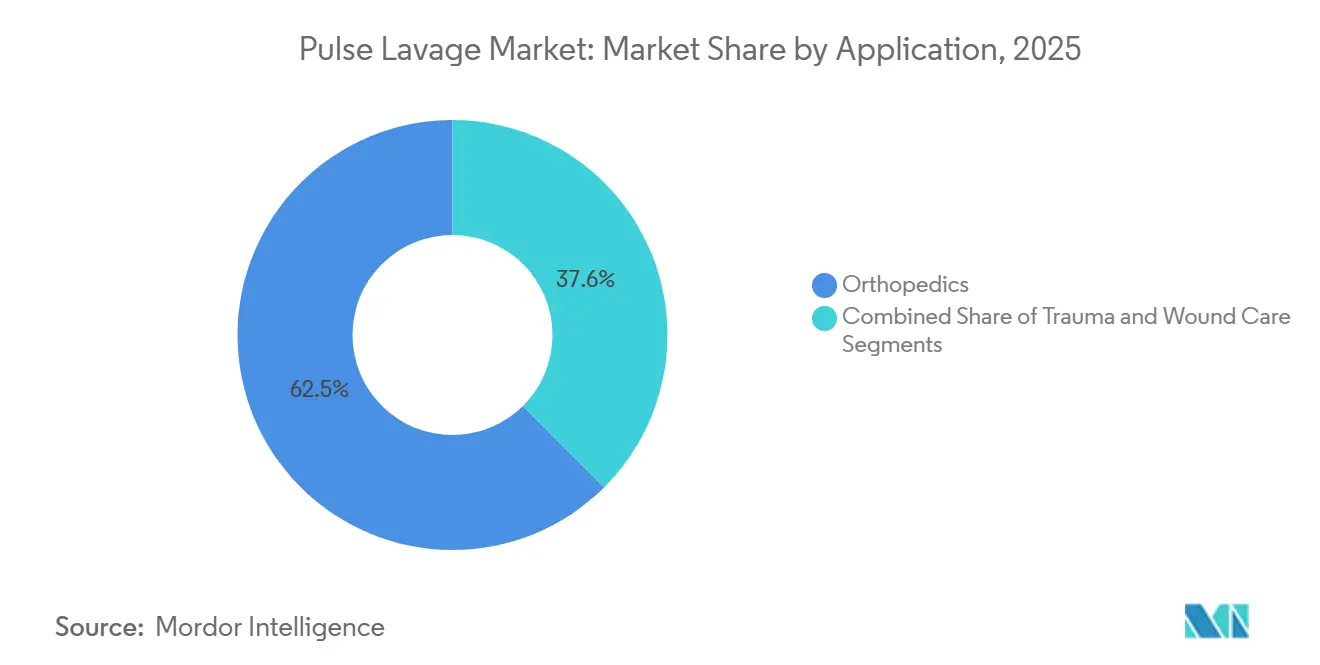

- By application, orthopedics accounted for 62.45% of 2025 revenue, while wound care is growing at a 11.65% CAGR through 2031.

- By end user, hospitals accounted for 69.76% in 2025, yet ASCs are advancing at a 11.54% CAGR through 2031.

- By geography, North America led with 43.21% revenue in 2025, while Asia-Pacific is on track for a 9.54% CAGR, steadily rebalancing global demand.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pulse Lavage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Surgical Procedure Volumes | +2.1% | Worldwide, largest absolute gains in Asia-Pacific and North America | Medium term (2-4 years) |

| Shift Toward Minimally Invasive Orthopedic and Trauma Techniques | +1.4% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Advancements in Pulse Lavage Device Technology and Ergonomics | +1.0% | Global, early uptake in North America and Western Europe | Medium term (2-4 years) |

| Aging Population and Growing Chronic Wound Burden | +1.8% | High-income aging nations and diabetes-endemic regions | Long term (≥ 4 years) |

| Strengthening Infection-Control Regulations | +1.5% | North America, Europe, expanding Asia-Pacific | Short term (≤ 2 years) |

| Expansion of Ambulatory Surgery Centers | +1.2% | Core Asia-Pacific, Middle East, Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Global Surgical Procedure Volumes

The world counted 1.4 billion people aged 60 and older in 2025, a cohort projected to reach 2.1 billion by 2050, which is swelling orthopedic and trauma caseloads[1]World Health Organization, “Ageing and Health,” who.int. In China, orthopedic surgeries are rising at a double-digit clip, while in India they are growing at high single digits as insurance coverage broadens. Trauma centers in emerging economies confront heavier bacterial loads in open fractures, prompting the use of battery units that deliver up to nine liters of irrigant per case. The FLOW trial found no outcome gap between high- and low-pressure saline lavage, so hospitals now weigh portability and ease of use above sheer pressure ratings. Together, these trends widen the installed base of pulse lavage systems from flagship hospitals to mid-tier trauma facilities.

Shift Toward Minimally Invasive Orthopedic and Trauma Techniques

Smaller incisions lower soft-tissue disruption yet intensify bacterial concentration in the wound bed, spurring surgeons to employ antiseptic lavage in every joint case[2].American Academy of Orthopaedic Surgeons, “Guideline for the Prevention of Surgical Site Infection,” aaos.org Battery-powered cordless handpieces help irrigate hard-to-reach pockets without repositioning patients or drapes. No-rinse citrate formulations deliver residual antimicrobial activity for up to five hours, cutting the need for repeated flushes that prolong operating time. Hospitals therefore screen new systems for irrigant compatibility alongside ergonomics. Early adopters in North America and Western Europe are driving this preference into procurement checklists across the wider market.

Advancements in Pulse Lavage Device Technology and Ergonomics

Handpieces are 30% lighter than prior generations and now integrate digital flow counters that log volume per case for compliance audits. Lithium-ion batteries supply 90–120 minutes of runtime with more than 500 charge cycles, erasing fears of mid-procedure power loss. Dual-mode platforms that accept battery or AC inputs let facilities standardize on one device across operating rooms and trauma bays. These upgrades shorten setup time, improve surgeon comfort, and strengthen infection-control by removing cords from sterile fields. As a result, technology improvements contribute about one percentage point to the projected market CAGR.

Aging Population and Growing Chronic Wound Burden

More than 8 million Americans live with diabetic foot, venous leg, or pressure ulcers that together cost USD 28 billion annually. Pulse lavage mechanically disrupts biofilm without excising viable tissue, accelerating granulation before negative-pressure or advanced dressings are applied. Clinical guidelines for chronic wounds now rank low-pressure lavage above syringe irrigation when heavy biofilm is suspected. Demand is rising in long-term-care and outpatient wound clinics, sites previously outside the irrigation device market. Consequently, soft-tissue-optimized low-pressure systems are expanding the customer base beyond orthopedic theaters.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Total Cost of Ownership for Disposable Systems | -1.3% | Global, sharpest in cost-sensitive markets | Short term (≤ 2 years) |

| Inconsistent Reimbursement Policies | -0.9% | North America, Europe, emerging markets | Medium term (2-4 years) |

| Environmental Pressures on Single-Use Plastics | -0.7% | Europe, North America, widening Asia-Pacific | Long term (≥ 4 years) |

| Shortage of Skilled Personnel | -0.5% | Emerging markets and rural zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Ownership for Disposable Systems

Lifecycle analyses show reusable platforms can slash per-case costs by up to 60% once annual procedure counts top 500, mainly by avoiding recurring handpiece purchases PRA[3]Practice Greenhealth, “Medical Waste Generation Report,” practicegreenhealth.org. Budget-constrained centers in Asia-Pacific and Latin America therefore consider semi-disposable hybrids that pair reusable motors with single-use tips. Yet smaller ASCs lacking sterilization departments still default to disposables, keeping a demand floor despite the price premium. Net impact is a 1.3 percentage-point drag on the global CAGR.

Environmental Pressures on Single-Use Plastics

Medical devices account for an estimated 5.9 million tons of U.S. hospital waste each year, and NHS England’s net-zero-by-2040 pledge has empowered sustainability officers to veto high-plastic consumables. The EU Single-Use Plastics Directive exempts medical products, but member states are trialing take-back mandates that could add compliance costs. Vendors are redesigning kits so only patient-contact components are discarded, but every configuration change needs fresh 510(k) clearance, slowing time-to-market. This sustainability headwind subtracts 0.7 percentage points from projected growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Devices Anchor Revenue While Accessories Accelerate

Devices accounted for the largest share of revenue at 68.82% in 2025, underscoring their role as the capital backbone of irrigation systems. Accessories, however, are expected to post a 10.34% CAGR through 2031, benefiting from predictable reorder cycles that lift overall pulse lavage market profitability. Premium-priced antimicrobial irrigant cartridges generate recurring revenue streams that are three to five times higher than those of saline equivalents, a dynamic that positions accessories as growth leaders. Hospitals with mixed device fleets often standardize on a single consumable brand to consolidate inventory, an approach that further enlarges accessory volumes.

Razor-and-blade strategies are shaping vendor economics. Entry-level device prices of USD 2,000–4,000 seed the installed base, while proprietary tips, canisters, and irrigants lock in customers for multiyear consumable agreements. This revenue mix cushions manufacturers against hospital capital-spending cycles. In emerging markets, generic consumables threaten that model, yet clinical protocols mandating antiseptic irrigants give brand-name suppliers an evidence-based edge. As accessory sales swell, they are set to raise the pulse of the lavage market by adding predictable annuity-like cash flows.

By Usability: Semi-Disposables Bridge Cost and Sterility

Disposable platforms held 60.254% of 2025 revenue, reflecting clinician preference for ready-to-use sterile kits. Still, semi-disposables are the fastest risers, with a 10.76% CAGR, as hospitals balance sterility rules with fiscal restraint. The hybrid model reduces consumable spend by 30–40% per case yet preserves a single-use contact pathway. Large orthopedic centers with central sterile supply departments can amortize the modest rise in reprocessing activity across multiple instrument categories, making semi-disposables an attractive compromise.

FDA recalls tied to sterilization lapses in reusable devices earlier in the decade pushed risk-averse hospitals toward disposables, but mounting environmental and budget pressures are reversing that swing. Vendors now market modular systems that let buyers toggle between disposable and reusable components to fit their capacity and sustainability ambitions. This flexibility is poised to boost the hybrid platform market share in the pulse lavage market, particularly in developed regions with explicit waste-reduction targets.

By Power Source: Battery Dominance Reflects Portability Premium

Battery-driven units secured 55.43% of revenue in 2025 and are forecast to grow at 10.21% CAGR, outpacing AC models despite higher upfront costs. Portability lets trauma teams use lavage in field environments with unreliable grid power, while cable-free operation reduces tripping hazards and contamination from cords in constrained operating rooms. Improved lithium-ion packs now offer two hours of uninterrupted runtime, dismantling earlier objections over power endurance.

Dual-mode systems that accept either batteries or wall power are gaining traction. Hospitals equipped with stable electricity can trim consumable costs by plugging in, yet retain batteries for transport or emergency use. In developing regions, where voltage fluctuations can damage medical electronics, battery platforms protect against downtime, making them the default choice for new installations and elevating the pulse lavage market size in those territories.

By Application: Wound Care Accelerates Amid Orthopedic Dominance

Orthopedics continued to dominate with 62.45% revenue in 2025, but wound-care applications are charting an 11.65% CAGR that outstrips the broader market trajectory. Biofilm-heavy diabetic foot and pressure ulcers require mechanical disruption before dressings or negative-pressure therapy, and pulse lavage delivers that action efficiently. Clinical societies now recommend low-pressure high-volume lavage as standard practice in chronic wound protocols, redirecting device placements into outpatient clinics and long-term care.

Trauma indications remain steady, aligned with global road-traffic injury trends rather than technological leaps. However, as randomized trials examine whether antimicrobial irrigants can reduce periprosthetic joint infection rates below the 1–2% baseline, the boundary between orthopedics and trauma may blur. If irrigant chemistry eclipses device ergonomics as the primary buying criterion, suppliers adept at bundling solution cartridges with hardware could capture a larger share of the pulse lavage market across both applications.

By End-User: ASCs Outpace Hospitals as Outpatient Migration Continues

Hospitals owned 69.76% of revenue in 2025 but ASCs are expanding at 11.54% CAGR, reflecting payer incentives to shift joint replacements and wound care to lower-cost venues. Disposable battery kits are the workhorses in ASCs because they avoid installation of reprocessing rooms and accelerate turnover. Specialty wound clinics and podiatry offices are also adopting smaller, lighter devices tailored for office-based debridement, further reinforcing the outpatient tilt.

Meanwhile, high-volume tertiary hospitals are scrutinizing per-case costs under bundled payments and may adopt reusable or hybrid systems. This divergence is segmenting the pulse lavage market into two pricing tiers: premium convenience-oriented disposable bundles for outpatient settings and cost-optimized, reprocessable setups for inpatient orthopedics. Device makers able to serve both tiers with a unified modular platform stand to maximize reach.

Geography Analysis

North America accounted for 43.21% of global revenue in 2025, driven by high orthopedic procedure volumes, strict infection-control mandates, and coverage for adjunctive irrigation consumables. Adoption in U.S. ASCs is particularly brisk as surgeons shift primary joint replacement to outpatient suites. Payer models that bundle payments, however, are nudging hospitals toward semi-disposable or reusable solutions to trim supply costs, potentially tempering growth rates in mature facilities.

Europe ranks second with sustainability policy acting as a differentiator. NHS England’s net-zero commitment is pushing providers to audit single-use plastics, boosting demand for hybrid platforms. Germany, France, and Italy are trialing citrate-based irrigants following recent FDA clearances and expected CE marks. Eastern Europe is expanding faster than the western core thanks to infrastructure upgrades and aging demographics, but budget sensitivity steers buyers toward value-priced reusable systems.

Asia-Pacific is the fastest-growing region at a 9.54% CAGR. China’s orthopedic surgery count is rising by a double-digit clip under universal insurance expansion, while India is adding ASCs in urban hubs where middle-class patients seek affordable care. Japan and South Korea feature high per-capita procedure rates and early adoption of antimicrobial irrigants. Southeast Asian nations gravitate to dual-power or battery units because of power-grid variability. These dynamics collectively enlarge the pulse lavage market size in the wider region.

Competitive Landscape

Competition is moderate and fragmenting. Orthopedic majors such as Stryker, Zimmer Biomet, and Smith+Nephew leverage bundled reconstruction portfolios and group-purchasing contracts to anchor share. Mid-tier specialists like MicroAire, DeRoyal, and Heraeus compete on ergonomic upgrades and flexible accessory ecosystems. Emerging players, including Next Science and Mölnlycke, focus on antimicrobial irrigant chemistry that promises clinical outcome gains beyond mechanical cleansing.

Margin pressure stems from two fronts. Hospitals demand lower total cost of ownership, prompting vendors to launch semi-disposable lines that meet sterility requirements while cutting consumable spend. Concurrently, infection-prevention committees are trialing irrigants that deliver 4–8 log reductions in biofilm, forcing device makers to validate chemical compatibility or risk obsolescence. Zimmer Biomet’s Bactisure and Next Science’s XPERIENCE are in pivotal trials enrolling more than 8,500 patients. Positive results could pivot procurement criteria toward solution chemistry, realigning competitive hierarchies.

Pricing tactics mirror the razor-and-blade model: devices are sold at near-breakeven prices while proprietary tips and irrigants secure recurring profits. Asian manufacturers offer FDA-registered systems at 40–60% discounts, winning share in cost-sensitive markets but facing barriers in premium segments that demand robust clinical evidence and compliance with EU MDR. Over 2025–2026, acquisitions—such as Mölnlycke’s wound-cleansing deal—signal vertical integration as suppliers chase higher-margin consumables linked to infection-reduction endpoints.

Pulse Lavage Industry Leaders

Stryker Corporation

Zimmer Biomet Holdings Inc.

Smith & Nephew plc

Mölnlycke Health Care AB

BD (Becton, Dickinson and Company)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Heraeus Medical has launched the palaJet AC Pulse Lavage System, a new version that operates with an AC adapter instead of batteries, eliminating the need for rechargeable power. This update expands the existing palaJet Pulse Lavage System and is now available in multiple European countries and the UK. The launch aims to provide a more reliable and cost-effective solution for wound irrigation.

- November 2023: Sonoma Pharmaceuticals, Inc., one of the global healthcare leader launched its intraoperative pulse lavage irrigation treatment, which can replace commonly used IV bags in a variety of surgical procedures in the United States.

Global Pulse Lavage Market Report Scope

As per the scope of the report, pulse lavage is a medical procedure that uses a high-pressure jet of sterile fluid to clean and irrigate wounds, removing debris, bacteria, and necrotic tissue. It is commonly used in wound management to promote healing and reduce infection risk. The device delivers pulsating bursts of fluid, providing effective and controlled irrigation.

The Pulse Lavage Market is Segmented by Product Type (Pulse Lavage Devices, Components & Accessories), Usability (Disposable, Reusable, Semi-Disposable), Power Source (Battery-Powered, AC-Powered), Application (Orthopedics, Trauma, Wound Care), End-User (ASCs, Hospitals, Specialty Clinics, Other End-Users), and Geography (North America, Europe, Asia-Pacific, MEA, South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Pulse Lavage Devices |

| Components & Accessories |

| Disposable Pulse Lavage Systems |

| Reusable Pulse Lavage Systems |

| Semi-Disposable Pulse Lavage Systems |

| Battery-Powered |

| AC-Powered |

| Orthopedics |

| Trauma |

| Wound Care |

| Ambulatory Surgery Centers |

| Hospitals |

| Specialty Clinics |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest Of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Product Type | Pulse Lavage Devices | |

| Components & Accessories | ||

| By Usability | Disposable Pulse Lavage Systems | |

| Reusable Pulse Lavage Systems | ||

| Semi-Disposable Pulse Lavage Systems | ||

| By Power Source | Battery-Powered | |

| AC-Powered | ||

| By Application | Orthopedics | |

| Trauma | ||

| Wound Care | ||

| By End-User | Ambulatory Surgery Centers | |

| Hospitals | ||

| Specialty Clinics | ||

| Other End-Users | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest Of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

How big will the pulse lavage market be by 2031?

The pulse lavage market size is projected to reach USD 811.47 million by 2031, reflecting an 8.11% CAGR over the forecast period.

Which segment is growing fastest within pulse lavage?

Wound-care applications are advancing at an 11.65% CAGR as chronic ulcer management increasingly incorporates mechanical biofilm disruption.

Why are battery-powered pulse lavage systems gaining share?

Portability, reduced infection risk from cords, and reliability in settings with unstable electricity drive a 10.21% CAGR for battery-based units.

How are sustainability goals affecting purchasing decisions?

Environmental targets such as NHS England's net-zero pledge are shifting procurement toward reusable or semi-disposable systems that lower plastic waste.

What role do antimicrobial irrigants play in adoption?

Emerging citrate-based solutions showing 4Ð8 log biofilm reductions could redefine value propositions, making irrigant compatibility a key buying criterion once large trials report.

Page last updated on: