Heart Rate Monitor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.78 Billion |

| Market Size (2031) | USD 4.52 Billion |

| Growth Rate (2026 - 2031) | 10.22% CAGR |

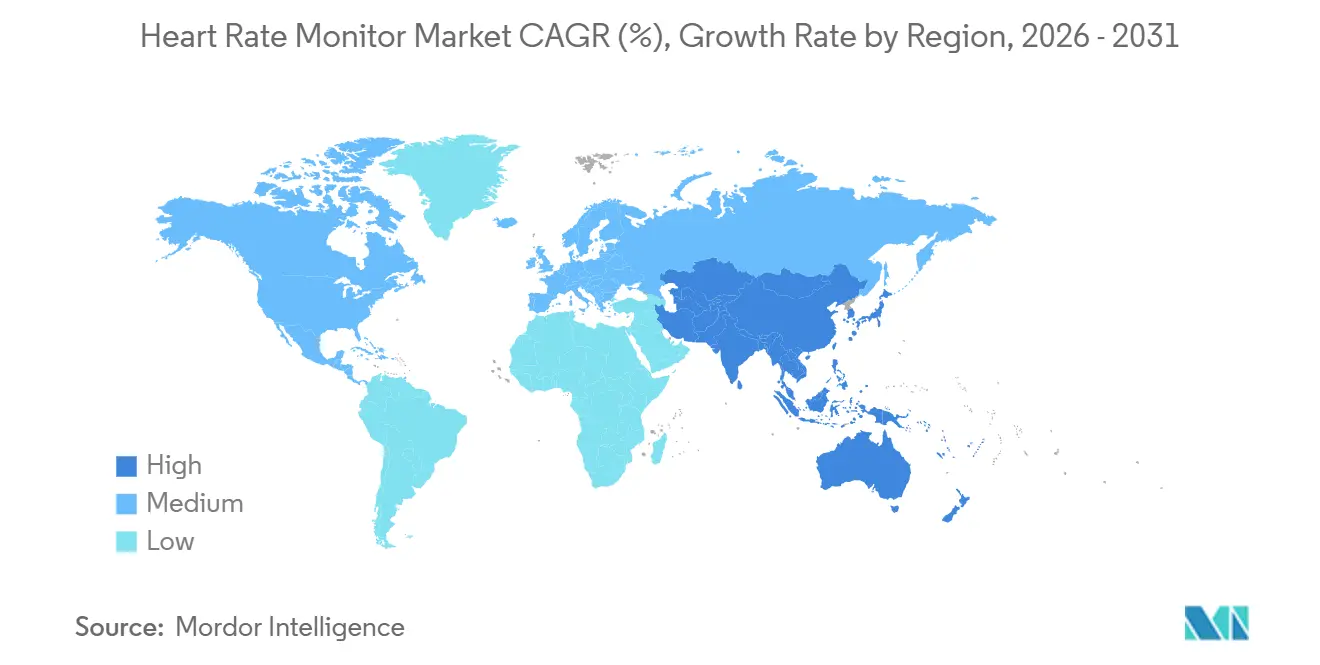

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

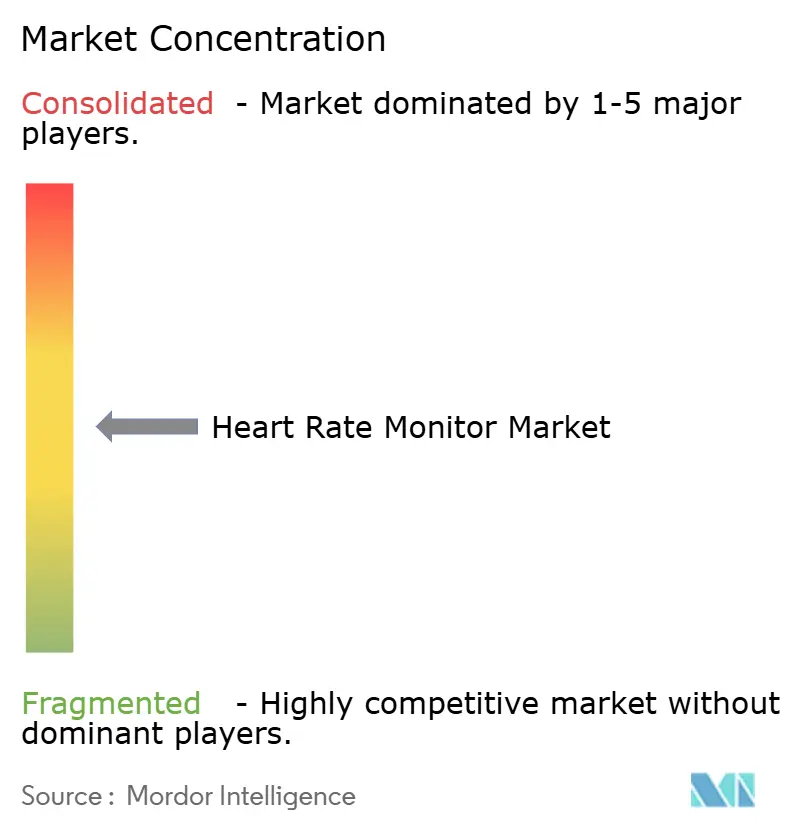

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Heart Rate Monitor Market Analysis by Mordor Intelligence

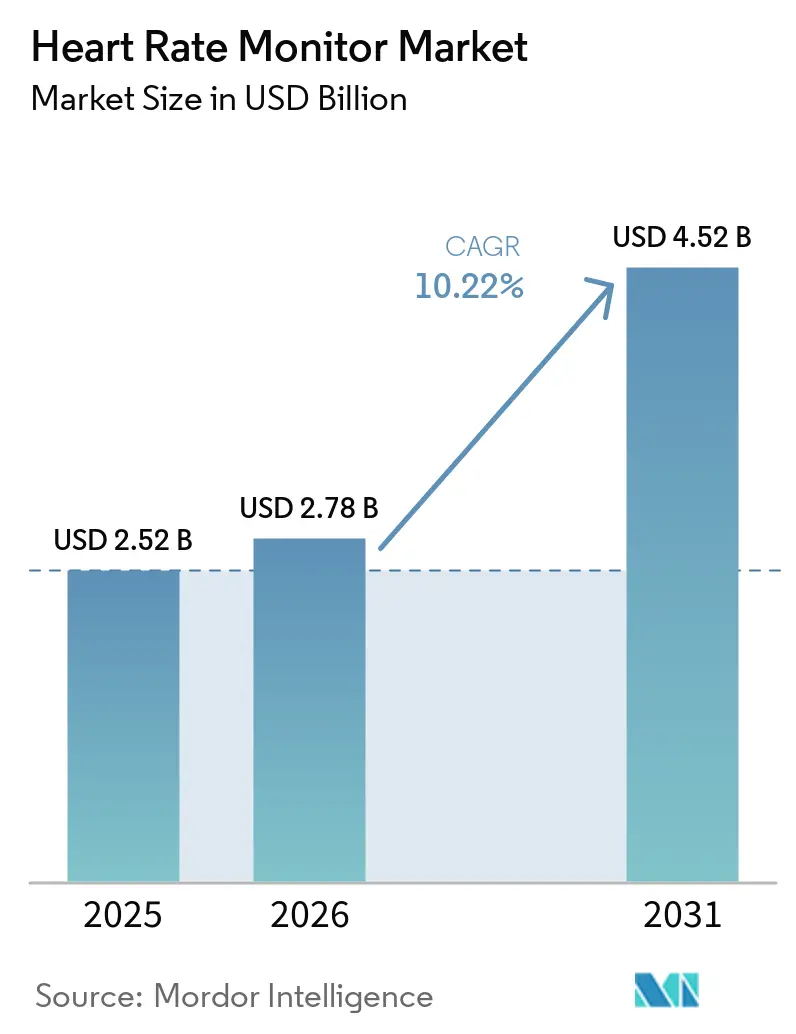

The Heart Rate Monitor Market size is expected to increase from USD 2.52 billion in 2025 to USD 2.78 billion in 2026 and reach USD 4.52 billion by 2031, growing at a CAGR of 10.22% over 2026-2031.

The global burden of cardiovascular diseases continues to drive the heart rate monitor market, emphasizing the need for continuous monitoring in personal health and formal care settings. The market benefits from advancements such as smaller optical sensors, improved ECG interpretation software, and cloud tools that enable monitoring beyond hospitals. Consumer devices now integrate more health functions, while clinical systems are becoming easier to deploy in outpatient and home settings, expanding the customer base. The growing overlap between wellness devices and clinical screening is increasing price competition for traditional clinical vendors. Additionally, the market remains competitive as subscription-based wearable platforms and regulated cardiac monitoring providers diversify revenue models, product offerings, and customer expectations.

Key Report Takeaways

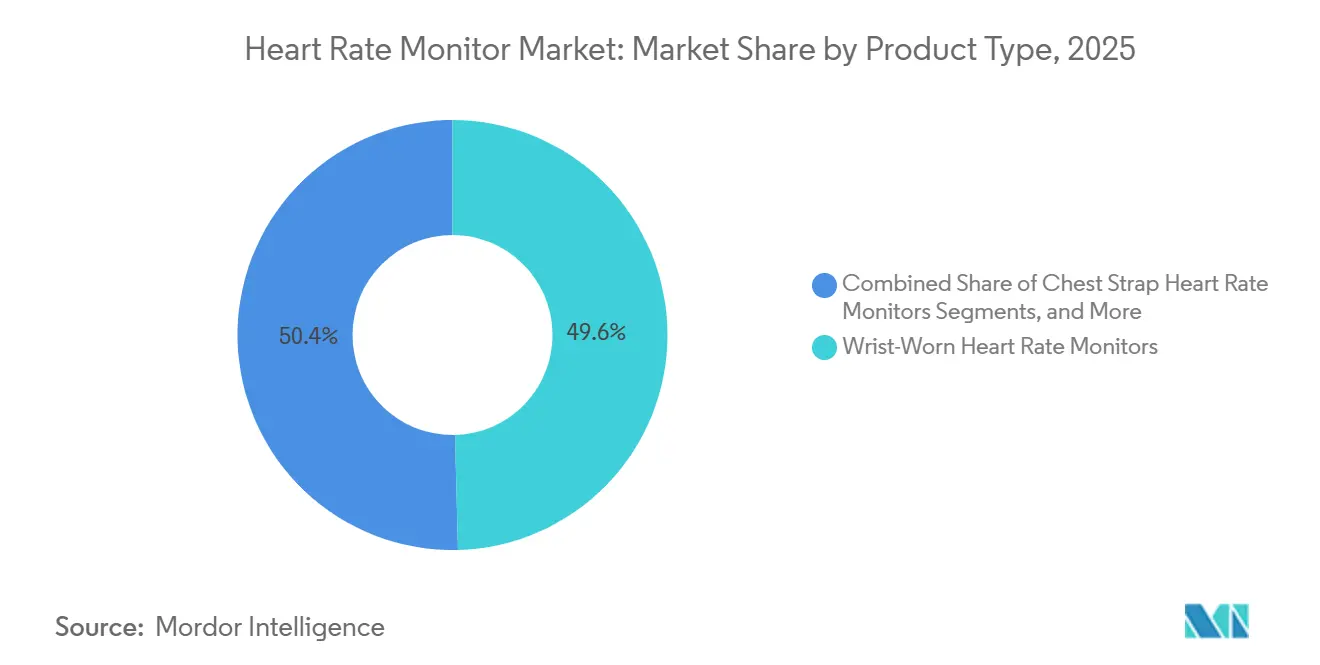

- By product type, wrist-worn devices held 49.6% share in 2025, while chest straps are projected to grow at an 11.3% CAGR through 2031.

- By technology, optical photoplethysmography monitoring accounted for 59.8% share in 2025, while hybrid sensing is projected to advance at an 11.8% CAGR through 2031.

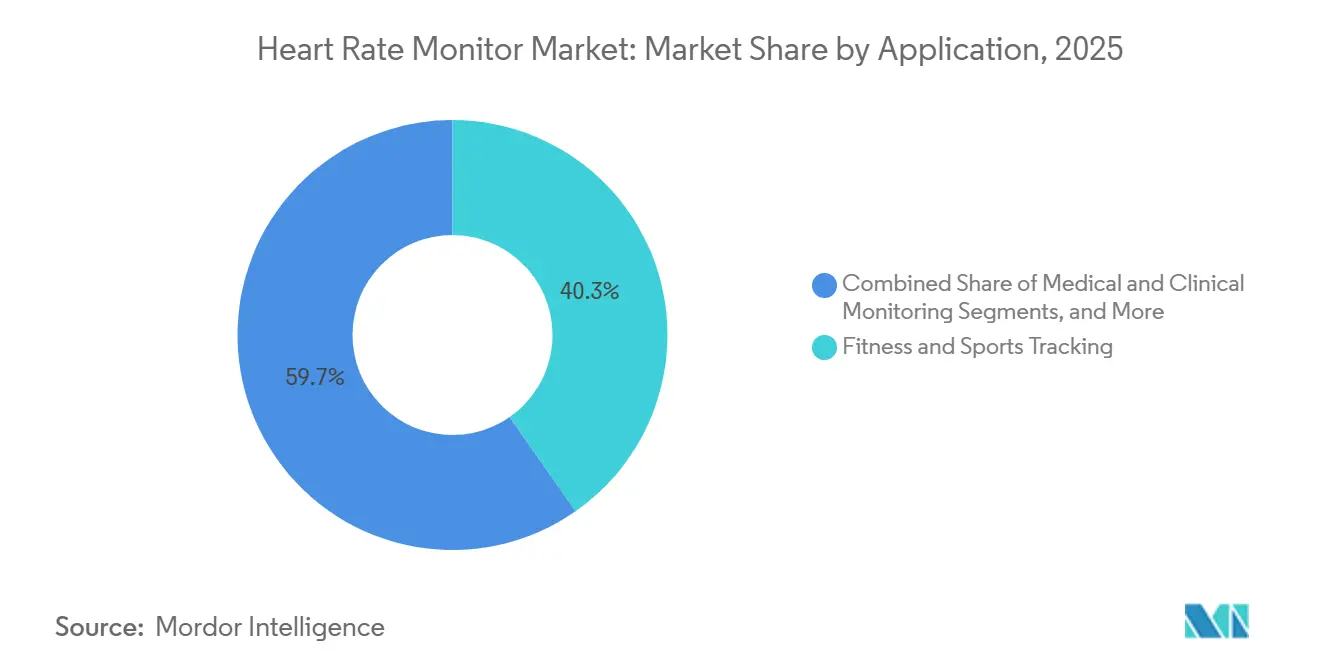

- By application, fitness and sports tracking represented 40.3% share in 2025, while remote patient monitoring is expected to expand at a 12.7% CAGR through 2031.

- By end user, individual consumers held 45.6% share in 2025, while home healthcare is projected to record an 11.5% CAGR through 2031.

- By geography, North America held 41.2% share in 2025, while Asia-Pacific is projected to grow at a 13.0% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Heart Rate Monitor Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising cardiovascular screening in non-acute settings | +2.5% | Global, with early concentration in North America and Western Europe | Medium term (2-4 years) |

| Continuous heart rate tracking becomes a core wellness feature | +2.8% | Global, led by North America, China, and India | Short term (≤ 2 years) |

| Remote patient monitoring expands reimbursement-based demand | +1.8% | North America dominant, with spillover into core Europe and Asia-Pacific | Short term (≤ 2 years) |

| Sensor fusion improves accuracy across activity and rest | +1.2% | Global, with stronger pull in the United States, Japan, and South Korea | Medium term (2-4 years) |

| Subscription analytics and coaching create repeat demand | +0.8% | North America and Europe, with early expansion in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Cardiovascular Screening in Non-Acute Settings

The heart rate monitor market is experiencing a shift as cardiac screenings transition from hospital settings to routine use in community and home environments. The high prevalence of cardiovascular diseases is driving the adoption of tools that enable frequent heart health monitoring with minimal clinical intervention. A clinical model from the Basel Wearable Clinic demonstrated the feasibility of remote ECG reviews and teleconsultations outside hospital settings. This shift positions employer programs, pharmacy screenings, and direct-to-consumer channels as key growth avenues, expanding the customer base beyond diagnosed cardiac patients and catering to various price points. Over time, this model is expected to drive market growth across consumer and clinical segments, particularly where remote follow-up care is feasible.

Continuous Heart Rate Tracking Becomes a Core Wellness Feature

Consumer expectations have evolved, with continuous heart rate tracking now considered a standard feature rather than a premium offering. In September 2025, Apple introduced chronic hypertension notifications and 24-hour continuous heart rate battery life in its Apple Watch Series 11. Samsung followed in March 2026 with blood pressure monitoring for Galaxy Watch users in the U.S. WHOOP reported that its 2.5 million members engage with its app over eight times daily, with consistent users recording increased exercise and heart rate variability. This shift highlights a market transition from sensor competition to a focus on guidance, adherence, and daily engagement. Brands integrating monitoring with coaching and habit reinforcement are better positioned for subscriber retention and revenue growth.

Remote Patient Monitoring Expands Reimbursement-Based Demand

The heart rate monitor market is seeing increased demand due to remote patient monitoring, as connected care models integrate seamlessly into formal health pathways. In April 2026, Withings joined the CMS ACCESS Model across all U.S. states, with Medicare beneficiary enrollments starting on July 5, 2026.[1]American Heart Association, “2025 Heart Disease and Stroke Statistics Update At-a-Glance Fact Sheet,” American Heart Association, heart.org This trend is steering the market toward an integrated model where device sales, software, physician reviews, and care coordination form a unified service chain. The demand for medical-grade wearables is also rising, particularly for post-discharge deployment and shorter observation periods, driving innovation in product design and data integration.

Sensor Fusion Improves Accuracy Across Activity and Rest

The heart rate monitor market is leveraging sensor fusion technology to address the accuracy limitations of optical monitoring during movement or sweating. Research has shown that combining ECG, PCG, and PPG in a single wearable enables the simultaneous capture of pulse transit time, arterial stiffness indicators, and electromechanical coupling. Another study found that multi-site PPG reduced mean heart rate errors by 46% compared to single-site devices, paving the way for improved optical monitoring. Apple has confirmed that its watch algorithms integrate multiple PPG sensors, accelerometer data, and machine learning models trained on extensive datasets. These advancements are narrowing the gap between consumer wearables and clinical monitors, intensifying competition across product categories.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Accuracy limitations in motion-heavy and high-sweat conditions | -1.2% | Global, most acute in cardiac patient and high-intensity sport segments | Short term (≤ 2 years) |

| Fragmented interoperability across health platforms | -0.9% | North America and Europe, with rising relevance in Asia-Pacific as remote monitoring scales | Medium term (2-4 years) |

| Battery life and form-factor tradeoffs limit premium adoption | -0.7% | Global, especially in clinical remote monitoring and overnight use | Medium term (2-4 years) |

| Consumer privacy concerns around physiological data | -0.6% | North America and Europe, with added influence from evolving health data rules | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accuracy Limitations in Motion-Heavy and High-Sweat Conditions

Heart rate monitors, particularly optical wrist-worn devices, face accuracy challenges in motion-heavy environments. A 2025 study highlighted that a medically certified wrist-worn PPG device showed poor accuracy and moderate responsiveness in monitoring heart rate and energy expenditure in patients with stable coronary artery disease and chronic heart failure during daily activities.[2]P. Badertscher and N. Brasier, “Wearable Technology in Clinical Practice, The Basel Wearable Clinic,” Nature Reviews Bioengineering, nature.com This limitation is critical as device performance in cardiac patients holds greater importance for care decisions than in healthy athletes. Many consumer wearable claims surpass the evidence available for complex physiological conditions, leading to cautious adoption by physicians and reimbursement entities. Without advancements in patient-specific algorithms and broader clinical validations, the market will continue to face challenges in high-value use cases requiring precise motion-state monitoring.

Consumer Privacy Concerns Around Physiological Data

The heart rate monitor market faces long-term challenges due to privacy concerns as biometric data like heart rate, recovery metrics, and sleep patterns become commercially valuable. With devices expanding into screening and preventive care, users may hesitate to share continuous physiological data with platforms, insurers, employers, and app ecosystems. Subscription models heighten this concern as they rely on consistent data collection, increasing compliance costs for smaller vendors managing consent, storage, security, and cross-platform access. If privacy expectations outpace platform improvements, adoption may slow in certain user groups despite advancements in device performance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Wrist-Worn Commands Volume, Chest Straps Gain on Performance Demand

In 2025, wrist-worn devices held 49.6% of the heart rate monitor market share, maintaining their leadership position. This dominance is driven by brands like Apple, Samsung, Garmin, Xiaomi, and WHOOP, which have a strong foothold in consumer wearables. Garmin's fitness segment reported Q1 2026 revenue of USD 547 million, a 42% year-over-year increase, reflecting sustained demand for advanced wrist-based platforms. Premium watches now offer always-on tracking and advanced cardiovascular features, attracting users who previously relied on separate wellness devices.

Chest straps, growing at an 11.3% CAGR from 2026 to 2031, highlight the market's focus on precision for intense activities or cleaner ECG-style signals. Their adoption is supported by athletes, structured training programs, and clinical use cases requiring enhanced signal fidelity. Finger-based monitors are gaining traction, while ear-based devices show potential with multimodal designs improving accuracy. Standalone monitors remain relevant for ambulatory diagnostics and short-term monitoring. The market reflects a diverse product mix, with wrist-worn devices dominating scale and chest straps and emerging formats addressing accuracy and form factor needs.

By Technology: PPG Anchors Volume, Hybrid Sensing Closes the Clinical Gap

Optical photoplethysmography (PPG) monitoring accounted for 59.8% of technology revenue in 2025, driven by its cost-effectiveness, ease of integration, and consumer familiarity. Apple’s use of multiple PPG sensors, accelerometers, and machine learning models has enhanced scalability, though challenges remain in improving accuracy during intense movement or in specific patient groups. PPG remains the volume leader but faces pressure for clinical validation.

Hybrid sensing, projected to grow at an 11.8% CAGR from 2026 to 2031, combines PPG with ECG and other sensors to enhance reliability and diagnostic value. WHOOP’s FDA-cleared ECG hardware and premium platforms from brands like Withings highlight the shift toward multi-sensor solutions. Research indicates software advancements can reconstruct ECG-like outputs from PPG signals, emphasizing the importance of algorithm quality. While ECG-based systems dominate clinical workflows today, hybrid sensing is poised for growth in premium clinical and consumer markets, ensuring a competitive and layered technology landscape.

By Application: Remote Patient Monitoring Sets the Growth Pace

Fitness and sports tracking held 40.3% of application revenue in 2025, reflecting strong consumer demand for training intensity, recovery tracking, and activity-linked heart rate data. Garmin’s fiscal 2025 revenue reached USD 7.25 billion, a 15% year-over-year increase, with FY2026 guidance of USD 7.9 billion, indicating continued investment in performance-oriented wearables. Fitness tracking is evolving into a gateway for preventive care and clinical referrals as devices incorporate medical-grade screening features.

Remote patient monitoring, growing at a 12.7% CAGR from 2026 to 2031, is gaining traction as connected platforms align with reimbursable care models. Enhanced ECG analytics and simplified outpatient deployments are driving adoption, particularly for arrhythmia screening. Wellness applications are expanding beyond athletes to include adults managing hypertension, metabolic risks, and sleep concerns. This shift broadens the market’s appeal, integrating home monitoring with daily lifestyle tracking and fostering continuous care applications.

By End User: Individual Consumers Hold Scale, Home Healthcare Scales Fastest

Individual consumers accounted for 45.6% of end-user revenue in 2025, driven by the scale of consumer wearables offering comprehensive health features. Garmin shipped over 20 million units in fiscal 2025, reflecting the potential of combining brand strength with health-focused innovations. Subscription models, such as WHOOP’s annual membership and Oura’s premium plans, are reshaping the market by emphasizing retention, engagement, and software quality over unit sales.

Home healthcare, growing at an 11.5% CAGR from 2026 to 2031, is emerging as a key growth driver. This trend is supported by post-acute care needs, remote monitoring programs, and the integration of connected tracking in clinical workflows. Partnerships like Philips and Masimo’s collaboration to connect wearables with hospital ecosystems illustrate the shift toward home and outpatient care. Ambulatory care centers are also gaining prominence, emphasizing ease of use, comfort, and reliable data transfer in non-hospital settings. This evolution is redefining the heart rate monitor market, moving beyond traditional hospital-centric models.

Geography Analysis

In 2025, North America held a 41.2% share of the heart rate monitor market, maintaining its leadership position. This dominance stems from high healthcare spending, a significant population with chronic cardiovascular risks, and a mature base of wearable and ambulatory monitoring devices. The region benefits from strong integration of remote monitoring services, physician oversight, and connected device usage in routine care.

Asia-Pacific is the fastest-growing region in the heart rate monitor market, projected to grow at a 13.0% CAGR from 2026 to 2031. Strong consumer adoption of wearables and rising demand for remote and home-based monitoring drive this growth. China and India benefit from telehealth expansion and affordable devices, while Japan's aging population increases demand for long-term health tracking. India is also advancing with ECG-enabled wearable innovations tailored to local needs. South Korea and Australia contribute through advanced sensor technologies and insured demand, while Southeast Asia offers potential for higher adoption as prices decline. This diverse regional mix supports growth across premium and affordable product segments.

Europe and other global regions show varied growth patterns in the heart rate monitor market, influenced by regulations, aging populations, and digital health adoption. Europe favors medically validated products, benefiting established brands with strong compliance and clinical positioning. In the Middle East and Africa, GCC digital health initiatives and high cardiovascular risks in younger populations drive demand. South America, led by Brazil and Argentina, sees growth through urban middle-class expansion and public monitoring programs, enabling affordable wearable adoption. These regions collectively add depth to the market beyond the dominant centers.

Competitive Landscape

In the heart rate monitor market, two distinct business models coexist: consumer platforms thrive on engagement and subscription revenue, while clinical monitoring firms prioritize evidence, regulation, and provider adoption. This division keeps the market vibrant, spanning both retail channels and formal care pathways. Major players like Apple, Samsung, Garmin, Xiaomi, and HUAWEI dominate the high-volume consumer segment. In contrast, iRhythm, Philips (via BioTelemetry), and Masimo have carved out significant niches in medical monitoring. Positioned between these two groups, WHOOP, Oura, and Withings blend consumer-friendly designs with in-depth health insights and increasing clinical relevance.

The consumer segment of the heart rate monitor market remains moderately fragmented, while clinical ambulatory monitoring is more concentrated. iRhythm, focusing on ambulatory ECG monitoring, has projected FY2026 revenues between USD 875 million and USD 885 million, highlighting the strength of evidence-based cardiac monitoring. Danaher targeted Masimo in a deal valued at nearly USD 9.9 billion, aiming to strengthen its monitoring position if completed. These developments show the market is increasingly shaped by data scale and portfolio consolidation rather than just new device launches.

Opportunities remain in the heart rate monitor market. Ear-based monitoring with enhanced clinical accuracy is still in its early stages, with limited players establishing a foothold. Post-discharge monitoring is another untapped area, as providers seek compact, easy-to-use, and reliable devices for short-term home observation. Research on reconstructing ECG-quality outputs from PPG signals suggests future competition may focus more on interpretation software and proprietary data than on sensor hardware. Companies that excel in managing device data, patient engagement, and clinically relevant interpretations are likely to lead as the market shifts toward integrated monitoring services.

Heart Rate Monitor Industry Leaders

Apple Inc.

Fitbit LLC

Garmin Ltd.

Polar Electro Oy

Koninklijke Philips N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: AliveCor partnered with WELL Health Technologies to offer Canadians AI-powered cardiac monitoring and cardiologist review services through AliveCor's Kardia platform, which has recorded over 350 million ECGs. This collaboration establishes a clinical services revenue stream for WELL Health's physician network.

- April 2026: Abbott shared key findings from four trials at Heart Rhythm Society 2026. The FlexPulse IDE study reported six-month results showing 87% of patients free from documented arrhythmias. Additionally, new data supported the Volt PFA System's posterior wall ablation. The TactiFlex Duo Ablation Catheter received its EU CE mark in January 2026.

- March 2026: Samsung began a phased US rollout of blood pressure monitoring for Galaxy Watch users. The Samsung Health Monitor app now enables simultaneous measurement of systolic and diastolic blood pressure along with heart rate. A passive blood pressure trend feature is planned for later in 2026.

- September 2025: Apple introduced the Apple Watch Series 11, Ultra 3, and SE 3. The Series 11 featured hypertension notifications and 24-hour continuous heart rate tracking. The Ultra 3 offered 42-hour standard and 72-hour low-power battery life with full GPS and heart rate tracking capabilities.

Global Heart Rate Monitor Market Report Scope

As per the scope of the report, a heart rate monitor is a device that tracks and displays your heart's beating speed in real-time, measured in beats per minute (bpm). They are widely used for optimizing athletic training, tracking daily fitness, and monitoring cardiovascular health.

The heart rate monitor market is segmented by product type, technology, application, end-user, and geography. By product type, the market includes wrist-worn heart rate monitors, chest strap heart rate monitors, finger-based heart rate monitors, ear-based heart rate monitors, and standalone and portable heart rate monitors. By technology, the market is segmented into optical photoplethysmography monitoring, electrocardiogram-based monitoring, and hybrid sensing technology. By application, the market is categorized into fitness and sports tracking, medical and clinical monitoring, remote patient monitoring, and wellness and preventive health. By end-user, the market is segmented into hospitals and clinics, home healthcare settings, fitness centers and sports institutes, ambulatory care centers, and individual consumers. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Wrist-Worn Heart Rate Monitors |

| Chest Strap Heart Rate Monitors |

| Finger-Based Heart Rate Monitors |

| Ear-Based Heart Rate Monitors |

| Standalone and Portable Heart Rate Monitors |

| Optical Photoplethysmography Monitoring |

| Electrocardiogram-Based Monitoring |

| Hybrid Sensing Technology |

| Fitness and Sports Tracking |

| Medical and Clinical Monitoring |

| Remote Patient Monitoring |

| Wellness and Preventive Health |

| Hospitals and Clinics |

| Home Healthcare Settings |

| Fitness Centers and Sports Institutes |

| Ambulatory Care Centers |

| Individual Consumers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Wrist-Worn Heart Rate Monitors | |

| Chest Strap Heart Rate Monitors | ||

| Finger-Based Heart Rate Monitors | ||

| Ear-Based Heart Rate Monitors | ||

| Standalone and Portable Heart Rate Monitors | ||

| By Technology | Optical Photoplethysmography Monitoring | |

| Electrocardiogram-Based Monitoring | ||

| Hybrid Sensing Technology | ||

| By Application | Fitness and Sports Tracking | |

| Medical and Clinical Monitoring | ||

| Remote Patient Monitoring | ||

| Wellness and Preventive Health | ||

| By End User | Hospitals and Clinics | |

| Home Healthcare Settings | ||

| Fitness Centers and Sports Institutes | ||

| Ambulatory Care Centers | ||

| Individual Consumers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 size of the heart rate monitor space?

The heart rate monitor market size stands at USD 2.8 billion in 2026 and is projected to reach USD 4.5 billion by 2031 at a 10.2% CAGR.

Which product category leads revenue generation?

Wrist-worn devices led with 49.6% share in 2025, supported by scale from large consumer wearable brands and growing health feature depth.

Which application is growing the fastest through 2031?

Remote patient monitoring is the fastest-growing application, with a projected 12.7% CAGR from 2026 to 2031.

Which region is the largest and which is the fastest growing?

North America led with 41.2% share in 2025, while Asia-Pacific is projected to expand at a 13.0% CAGR through 2031.

Why are subscription wearables becoming more important?

Subscription models help vendors generate recurring revenue and improve retention through coaching, readiness scores, recovery insights, and daily engagement tools.

What is the main technical challenge for wider clinical adoption?

The biggest technical constraint remains accuracy under movement-heavy conditions, especially for optical wrist-worn devices used in cardiac patient populations.

Page last updated on: