Long Term Care Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

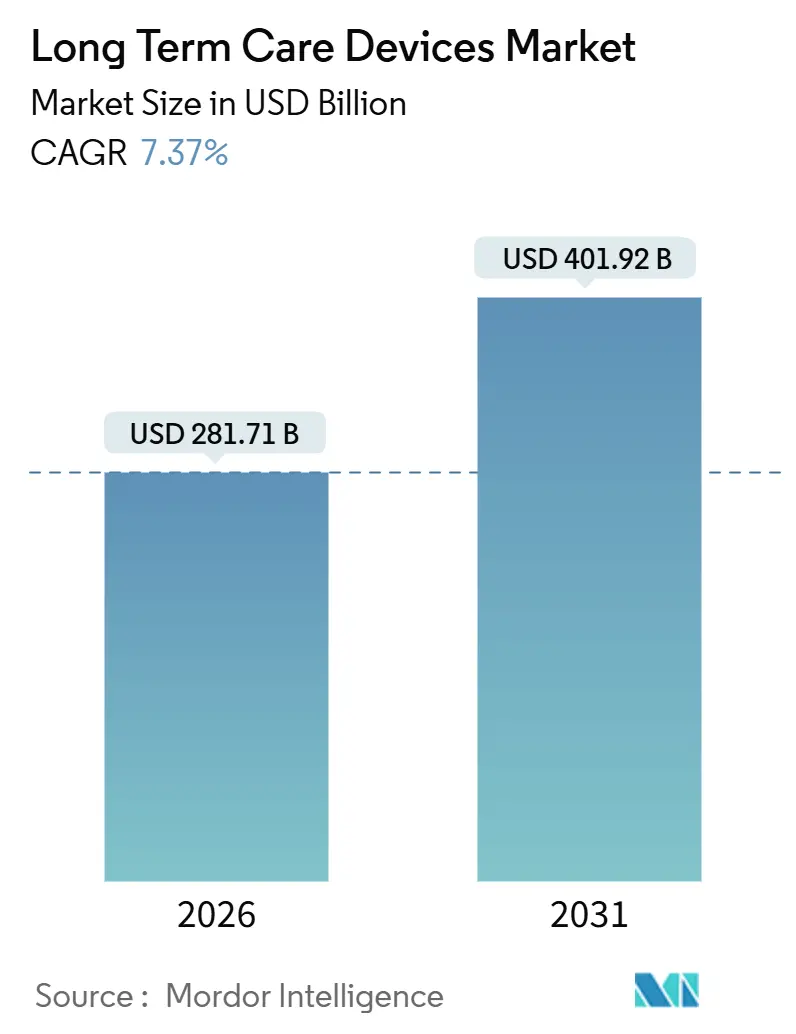

| Market Size (2026) | USD 281.71 Billion |

| Market Size (2031) | USD 401.92 Billion |

| Growth Rate (2026 - 2031) | 7.37% CAGR |

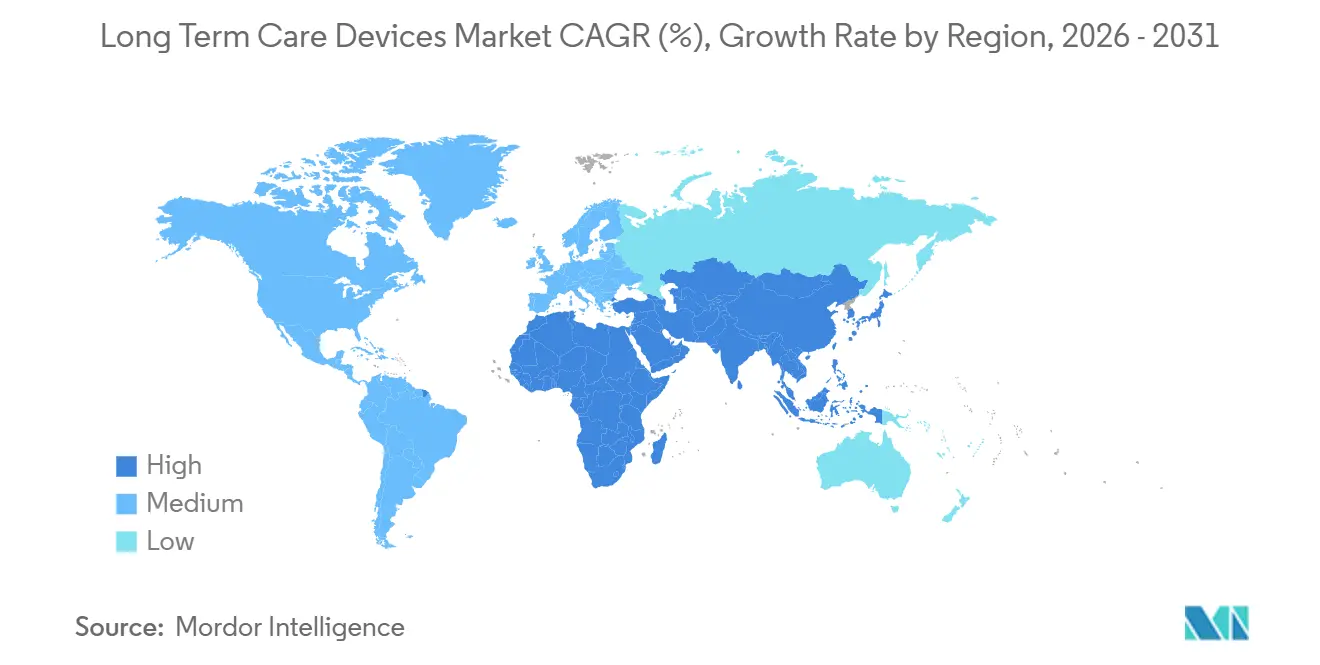

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Long Term Care Devices Market Analysis by Mordor Intelligence

The Long Term Care Devices Market size is estimated at USD 281.71 billion in 2026, and is expected to reach USD 401.92 billion by 2031, at a CAGR of 7.37% during the forecast period (2026-2031).

Demographic inversion, with adults aged 65+ set to outnumber children under 5 by 2030, combines with the reality that 6 in 10 U.S. adults now live with at least one chronic condition to accelerate demand for connected devices that support aging-in-place models. Lithium and rare-earth supply constraints are forcing battery redesigns, while data-sovereignty rules fragment cross-border remote-monitoring deployments. Device-as-a-service contracts, AI-based predictive maintenance, and decarbonization-weighted tenders are reshaping purchasing priorities throughout the long term care devices market.

Key Report Takeaways

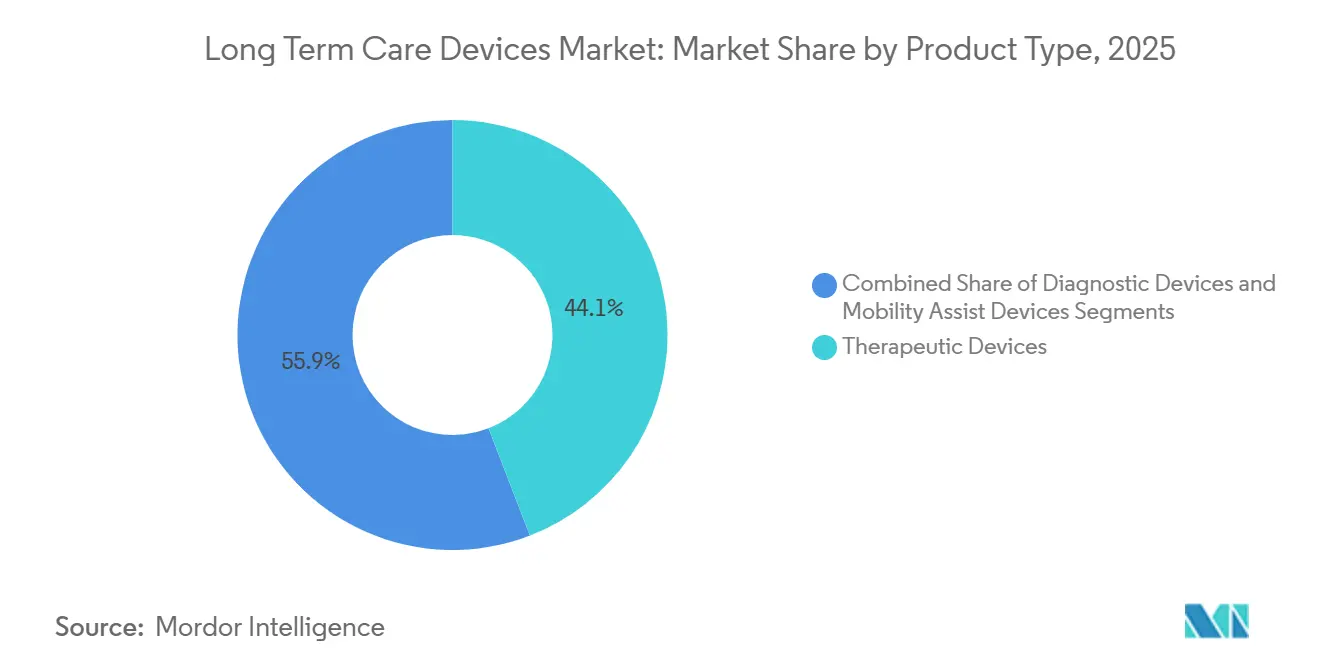

- By product type, Therapeutic Devices led with 44.14% of 2025 revenue, whereas Mobility Assist Devices are forecast to grow at a 9.24% CAGR through 2031.

- By indication, Chronic-Disease Management accounted for 53.67% of demand in 2025, while Rehabilitation and Mobility Impairment is set to advance at a 9.54% CAGR to 2031.

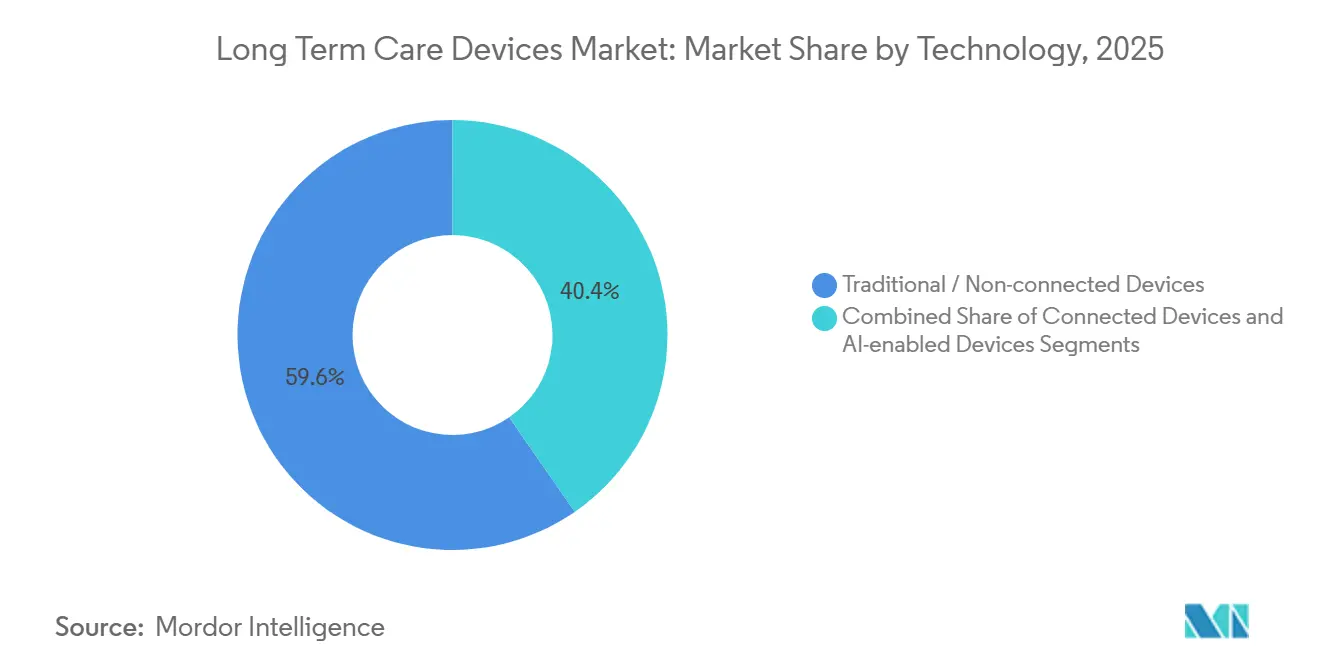

- By technology, Traditional Non-connected Devices represented 59.62% of 2025 volume; however, AI-enabled Smart-Analytics Devices will expand at an 11.44% CAGR through 2031.

- By device portability, Stationary Installed Equipment held 44.85% of 2025 sales, whereas Wearable Body-worn Devices are expected to accelerate at an 11.64% CAGR through 2031.

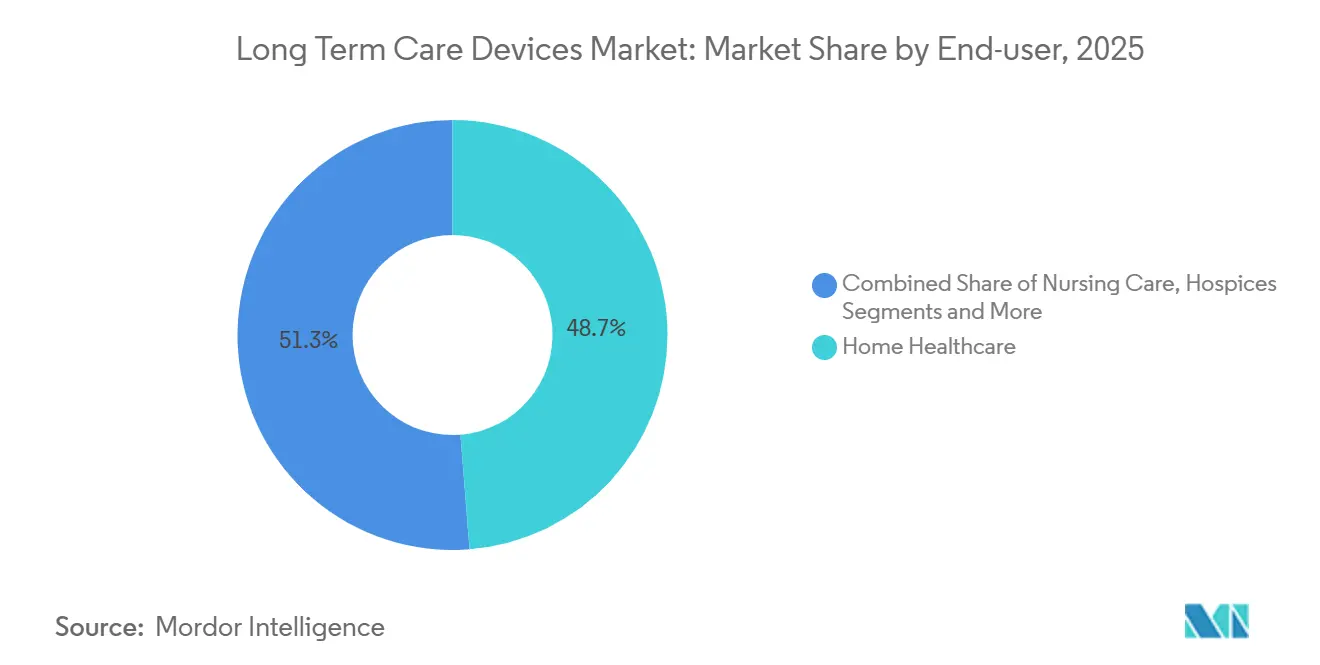

- By end user, Home Healthcare captured 48.74% share in 2025; Assisted Living Facilities will post the fastest growth at a 10.53% CAGR through 2031.

- By geography, North America commanded 36.13% of the long term care devices market share in 2025, but Asia-Pacific is projected to record a 9.76% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Long Term Care Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapidly Ageing Population & Chronic-Disease Burden | 1.8% | Global, with highest intensity in Japan, Italy, Germany, South Korea | Long term (≥ 4 years) |

| Rising Home-Healthcare / Ageing-In-Place Models | 1.5% | North America & EU core, expanding to urban APAC | Medium term (2-4 years) |

| Breakthroughs In Portable & Connected Devices | 1.3% | Global, led by North America and Western Europe, rapid adoption in China | Medium term (2-4 years) |

| AI-Based Predictive Maintenance Lowering TCO | 0.9% | North America & EU, pilot deployments in GCC | Medium term (2-4 years) |

| Decarbonization Procurement Mandates | 0.7% | EU (UK, Germany, France), emerging in Canada and Australia | Long term (≥ 4 years) |

| Device-As-A-Service Subscription Offerings | 1.1% | North America & Western Europe, early traction in Brazil, UAE | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapidly Ageing Population & Chronic-Disease Burden

The global population aged 60+ will reach 2.1 billion by 2050, double 2020 levels, while Japan already spends 40% more per capita on fall-detection wearables than the OECD average. Chronic diseases drive 90% of U.S. healthcare costs, urging payers to reimburse devices that curb readmissions.[1]CDC, “Chronic Diseases in America,” Centers for Disease Control and Prevention, cdc.gov Physician shortages projected at 124,000 in the United States intensify reliance on technology-enabled coordination.[2]AMA, “The Complexities of Physician Supply and Demand,” American Medical Association, ama-assn.org

Rising Home-Healthcare / Aging-in-Place Models

Medicare’s ACCESS Model rewards tech-enabled home care, and remote physiologic monitoring claims rose tenfold from 2019-2022. Scotland is investing GBP 300 million to outfit 50,000 homes with telehealth infrastructure[3]CMS, “Guide: Home Health Value-Based Purchasing Model,” Centers for Medicare & Medicaid Services, cms.govwhile 77% of U.S. adults over 50 prefer aging in place.

Breakthroughs in Portable & Connected Devices

The FDA cleared 21 novel RPM devices in 2024, including Abbott’s FreeStyle Libre 3 and Medtronic’s Simplera CGM, both streaming glucose data to smartphones. Wearable BioButton patches track multiple vitals for 90 days, replacing Holter monitors in long term care settings. Predetermined change-control plans now allow in-field AI updates without new 510(k) filings.

AI-Based Predictive Maintenance Lowering TCO

GE Healthcare’s OnWatch forecasts component failure 30 days in advance and cut unplanned downtime by 22% in German hospital pilots. Philips’ IntelliVue monitors offer similar analytics bundled within subscription contracts. These tools eliminate emergency service calls worth USD 15,000 per nursing home annually.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost of Advanced Devices | -1.2% | Global, most acute in emerging markets and small operators | Short term (≤ 2 years) |

| Fragmented Reimbursement Frameworks | -0.9% | Global, particularly EU intra-country variation and U.S. state Medicaid | Medium term (2-4 years) |

| Lithium & Rare-Earth Supply Constraints | -0.6% | Global, supply concentrated in China, Australia, Chile | Medium term (2-4 years) |

| Data-Sovereignty Limits on Cross-Border RPM | -0.5% | EU under GDPR, China, Russia, India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Advanced Devices

Cellular blood-pressure monitors cost USD 300-500 versus USD 50 for basic units, pushing payback to 18-24 months for 100-bed facilities. Integration, middleware, and IT add 20-30% to ownership costs, and rural India lacks broadband at 88% of primary centers

Lithium & Rare-Earth Supply Constraints

China controls 60% of rare-earth refining and 80% of lithium-ion cell production, while lithium carbonate prices peaked at USD 80,000/ton in 2022. U.S. domestic lithium refining only began in 2024 at 30,000 tons capacity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Therapeutic Devices Anchor Revenue, Mobility Aids Accelerate

Therapeutic Devices held 44.14% share in 2025, buoyed by infusion pumps and dialysis systems that boost the long term care devices market size for capital equipment. Mobility Assist Devices will rise at 9.24% CAGR as falls remain the top cause of fatal injury among older adults.

Smart wheelchairs like Permobil’s M5 Corpus integrate tilt and elevation via smartphone control, illustrating the shift toward sensor-rich mobility aids. Diagnostic devices benefit from home-based testing, yet reimbursement gaps slow uptake in some regions.

By Indication: Chronic-Disease Management Dominates, Rehabilitation Gathers Pace

Chronic-Disease Management commanded 53.67% of demand in 2025, fueled by 537 million adults living with diabetes. Rehabilitation and Mobility Impairment will register a 9.54% CAGR through 2031, supported by AI-guided exoskeletons like Ekso NR that shorten therapy time by 30%. Palliative care remains smaller yet grows as intrathecal pumps such as Medtronic’s SynchroMed II allow hospice patients to remain at home longer.

By Technology: AI-Enabled Platforms Disrupt Legacy Installations

Traditional Non-connected Devices still represent 59.62% of volume, but AI-enabled Smart-Analytics Devices will expand at 11.44% CAGR, driven by FDA guidance that eases algorithm updates. Cybersecurity requirements now mandate software bills of materials for networked devices

By Device Portability: Wearables Redefine Continuous Monitoring

Stationary Installed Equipment retains high-value share, yet Wearable Body-worn Devices will log the quickest CAGR at 11.64%, led by Abbott’s FreeStyle Libre 3 and BioIntelliSense’s BioButton. Mobile Portable Devices remain critical for oxygen therapy and mobile imaging.

By End User: Home Healthcare Leads, Assisted Living Gains Momentum

Home Healthcare secured 48.74% share in 2025 thanks to reimbursement that rewards in-home monitoring. Assisted Living Facilities will grow at 10.53% CAGR, adopting radar-based fall detection from providers like Vayyar Care. Hospices and nursing homes prioritize devices with clear ROI, particularly RPM platforms that cut emergency transfers.

Geography Analysis

North America accounted for 36.13% of 2025 revenue, propelled by USD 4.1 trillion in U.S. healthcare spending and FDA pathways for home-use devices. Canada pilots rural RPM programs, while Mexico’s growing middle class boosts chronic-care device demand.

Asia-Pacific is expected to deliver a 9.76% CAGR through 2031, underpinned by China’s 280 million citizens over 60 and Japan’s subsidies for monitoring devices in 3,000 facilities. India’s Ayushman Bharat plans 150,000 wellness centers with telemedicine kits by 2027.

Europe benefits from universal coverage and stricter MDR evidence requirements that favor incumbents. The UK’s carbon-weighted tenders and France’s expanded RPM reimbursement broaden demand, while GCC investments and Brazil’s telehealth pilots lift emerging-market adoption.

Competitive Landscape

The long-term care devices market is moderately concentrated. Medtronic, Philips, and Abbott lock customers into multi-year device-as-a-service arrangements that blend hardware, software, and maintenance. Stryker’s USD 1.2 billion purchase of a mobility-assist robotics firm typifies acquisition-driven capability expansion.

Start-ups such as CarePredict and Vayyar Care target ambient sensing niches, raising significant Series C funding in 2024. MDR compliance costs and carbon-accounting pressures are expected to propel further consolidation among mid-tier manufacturers.

Long Term Care Devices Industry Leaders

Baxter International Inc.

Cardinal Health Inc.

Koninklijke Philips N.V.

Medtronic plc

B. Braun Melsungen AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: ResMed secured FDA clearance for Smart Comfort, the first AI-enabled CPAP feature that recommends personalized therapy settings.

- August 2025: The FDA approved Nyxoah’s Genio bilateral neurostimulation system for moderate-to-severe obstructive sleep apnea.

- August 2025: Terumo India launched Terufusion Advanced Infusion Systems with remote monitoring and dose-mode customization.

- July 2025: IIT Madras unveiled YD One, an ISO-certified active wheelchair weighing just 8.5 kg.

Global Long Term Care Devices Market Report Scope

Long-term care (LTC) devices are defined as specialized tools, technologies, and equipment designed to assist individuals with chronic illnesses, disabilities, or age-related limitations in maintaining independence and safety. These devices support Activities of Daily Living (ADLs) and Instrumental Activities of Daily Living (IADLs) in homes, assisted living, or skilled nursing facilities.

The Long Term Care Devices Market Report is segmented by Product Type, Indication, Technology, Device Portability, End User, and Geography. By Product Type, the market is segmented into Therapeutic, Diagnostic, and Mobility Assist. By Indication, the market is segmented into Chronic-Disease Management, Rehabilitation & Mobility Impairment, and Palliative & End-of-Life Care. By Technology, the market is segmented into Traditional/Non-connected, Connected/IoT-enabled, and AI-enabled/Smart-Analytics. By Device Portability, the market is segmented into Stationary/Installed, Mobile/Portable, and Wearable/Body-worn. By End User, the market is segmented into Home Healthcare, Nursing Care, Assisted Living, and Hospices. By Geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Therapeutic Devices |

| Diagnostic Devices |

| Mobility Assist Devices |

| Chronic-Disease Management | Diabetes & Metabolic Disorders |

| Cardiovascular & Hypertension | |

| Respiratory | |

| Others | |

| Rehabilitation & Mobility Impairment | |

| Palliative & End-of-Life Care |

| Traditional/Non-connected Devices |

| Connected/IoT-enabled Devices |

| AI-enabled / Smart-Analytics Devices |

| Stationary / Installed Equipment |

| Mobile / Portable Devices |

| Wearable / Body-worn Devices |

| Home Healthcare |

| Nursing Care |

| Assisted Living Facilities |

| Hospices |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Therapeutic Devices | |

| Diagnostic Devices | ||

| Mobility Assist Devices | ||

| By Indication | Chronic-Disease Management | Diabetes & Metabolic Disorders |

| Cardiovascular & Hypertension | ||

| Respiratory | ||

| Others | ||

| Rehabilitation & Mobility Impairment | ||

| Palliative & End-of-Life Care | ||

| By Technology | Traditional/Non-connected Devices | |

| Connected/IoT-enabled Devices | ||

| AI-enabled / Smart-Analytics Devices | ||

| By Device Portability | Stationary / Installed Equipment | |

| Mobile / Portable Devices | ||

| Wearable / Body-worn Devices | ||

| By End User | Home Healthcare | |

| Nursing Care | ||

| Assisted Living Facilities | ||

| Hospices | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What will the long term care devices market be worth by 2031?

It is projected to reach USD 401.92 billion.

Which product category shows the fastest growth?

Mobility Assist Devices are expected to rise at a 9.24% CAGR through 2031.

How is AI improving maintenance for long-term care devices?

Predictive analytics cut unplanned downtime by over 20% and are bundled into subscription contracts.

Which region is poised for the highest growth rate?

Asia-Pacific, with a forecast 9.76% CAGR through 2031.

Why are assisted living facilities adopting IoT sensors?

Staffing shortages and liability caps make AI-based fall detection attractive, fueling a 10.53% CAGR for the segment.

How do carbon-reduction mandates affect procurement?

UK and German tenders weight bids toward suppliers with verified carbon-reduction plans and refurbishing programs.

Page last updated on: