U.S. Companion Animal Health Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

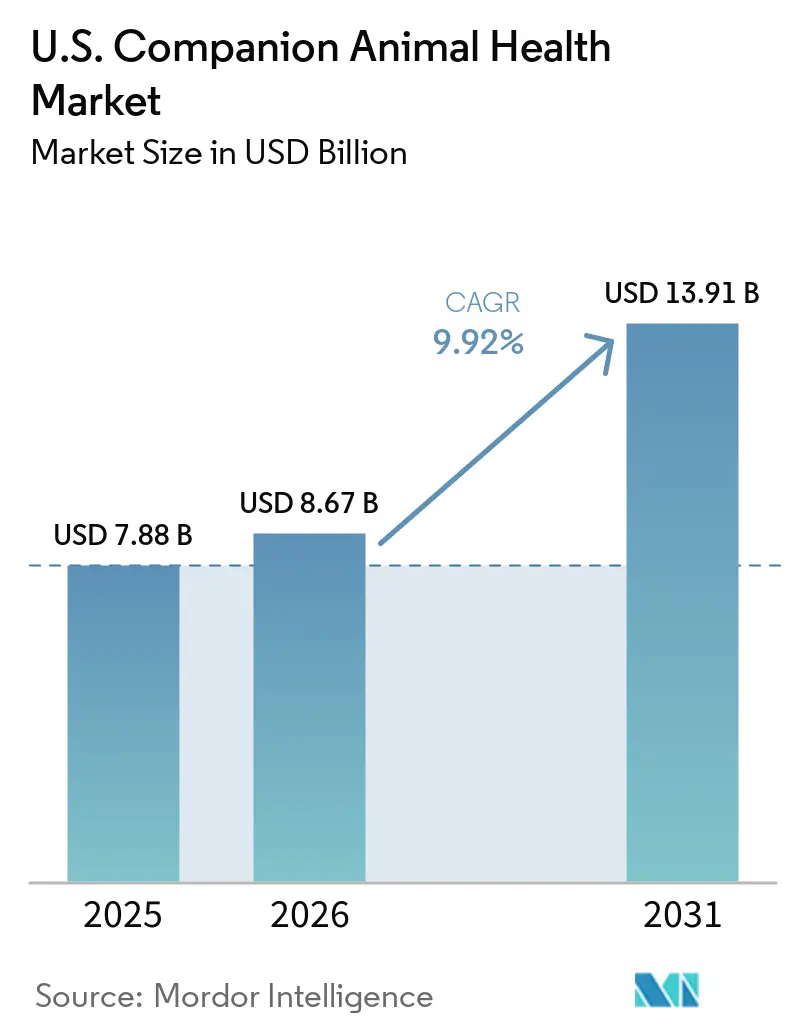

| Base Year Market Size (2025) | USD 7.88 Billion |

| Market Size (2026) | USD 8.67 Billion |

| Market Size (2031) | USD 13.91 Billion |

| Growth Rate (2026 - 2031) | 9.92% CAGR |

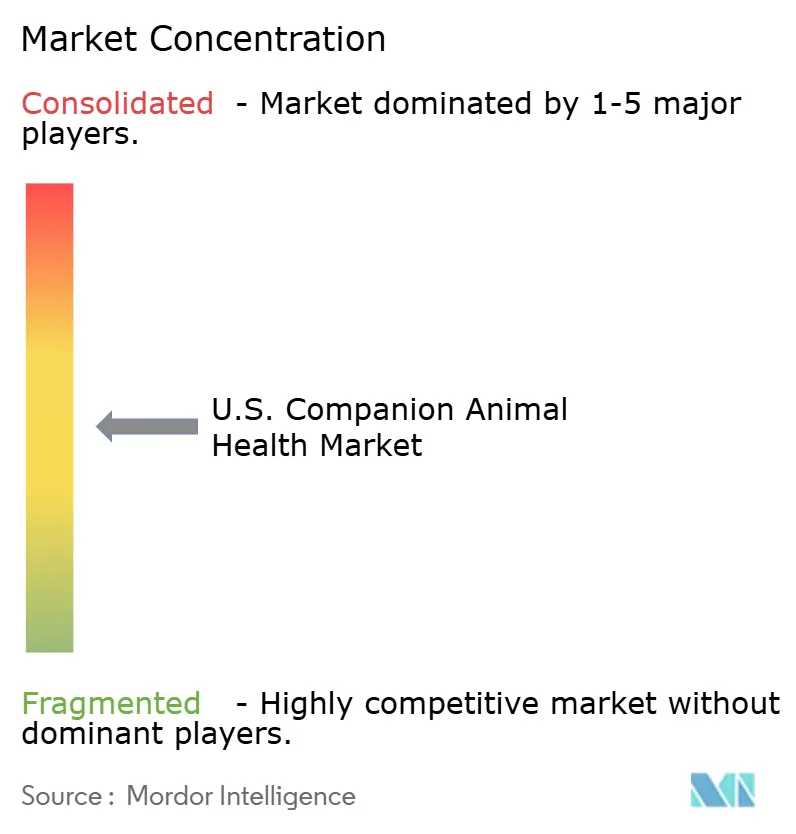

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

U.S. Companion Animal Health Market Analysis by Mordor Intelligence

The U.S. Companion Animal Health Market size is projected to be USD 7.88 billion in 2025, USD 8.67 billion in 2026, and reach USD 13.91 billion by 2031, growing at a CAGR of 9.92% from 2026 to 2031.

In 2025, pet ownership in the United States remained extensive, with 95 million households owning pets. Total pet industry spending reached USD 158 billion, including USD 41.4 billion on veterinary care. This trend highlights a sustained increase in treatment intensity within the companion animal health market rather than a temporary recovery cycle. Premium diagnostics, biologics, and chronic disease management are driving higher average revenue per treated animal. Growing acceptance of specialist care is expanding the range of procedures approved by pet owners. Additionally, pet insurance is broadening access to higher-cost treatments, with direct premiums written in the United States reaching USD 5.47 billion in 2025, continuing a multi-year growth trajectory.

Key Report Takeaways

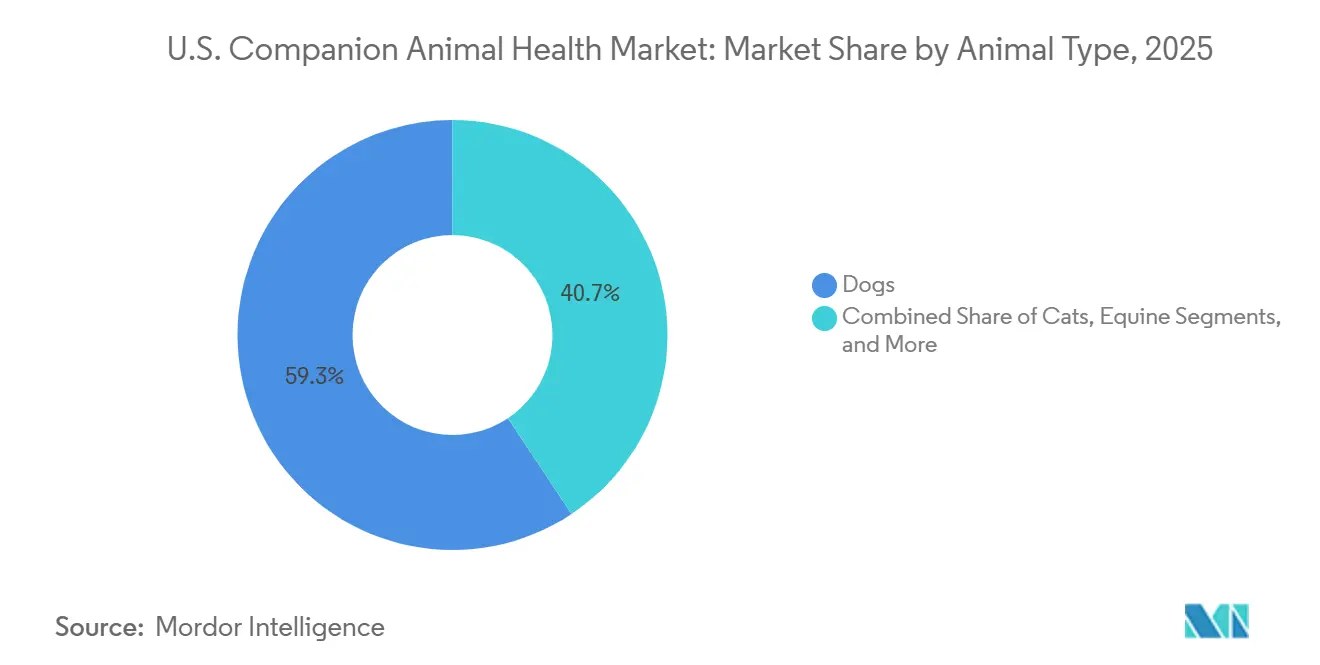

- By animal type, dogs held 59.35% of revenue in 2025, while cats are projected to expand at an 11.15% CAGR through 2031.

- By product type, therapeutics accounted for 43.25% of revenue in 2025, while diagnostics is projected to grow at a 12.75% CAGR through 2031.

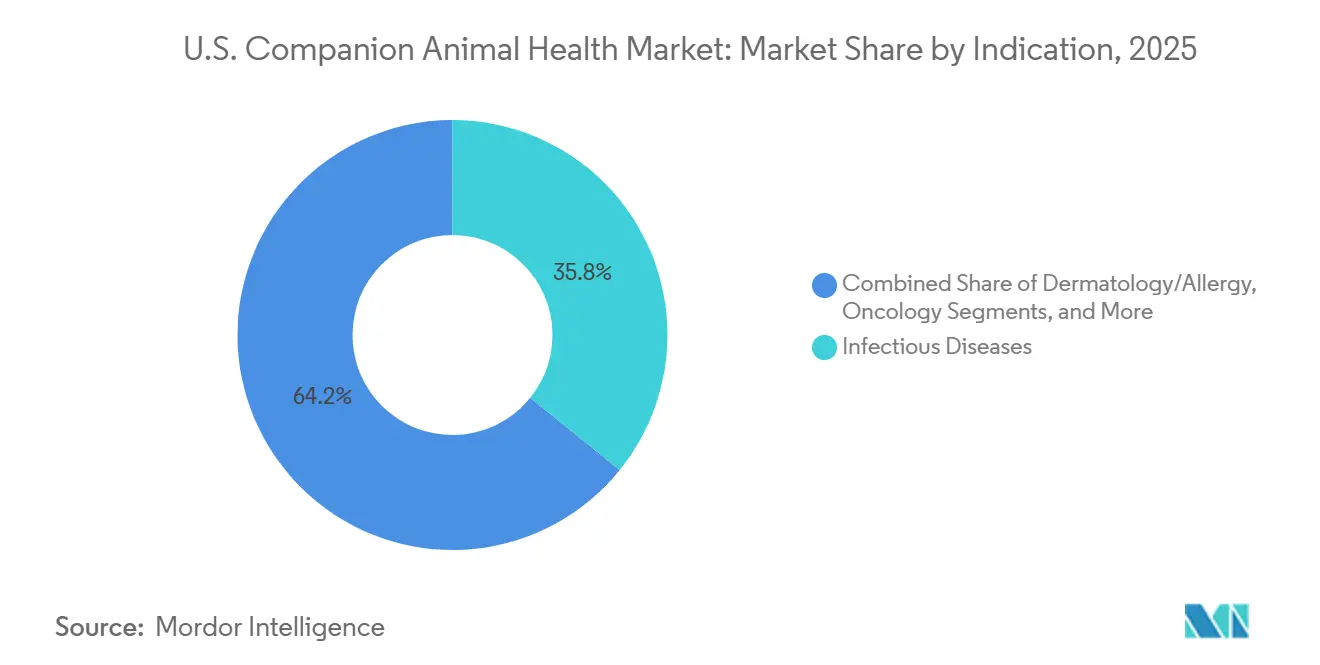

- By indication, infectious diseases represented 35.78% of revenue in 2025, while oncology is forecasted to advance at an 11.63% CAGR through 2031.

- By distribution channel, veterinary hospital and clinic pharmacies held 65.89% of revenue in 2025, while e-commerce and online pharmacies are expected to grow at a 10.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

U.S. Companion Animal Health Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Premiumization and humanization of pet healthcare | +2.8% | National, with premium concentration in coastal metros, including California, New York, Texas, and Florida | Long term (≥ 4 years) |

| Preventive parasiticide and vaccine compliance | +1.5% | National, with acute demand in Southern and mid-Atlantic states for tick and heartworm prevention | Medium term (2-4 years) |

| Pet insurance expansion and financing-led care acceptance | +1.8% | National, with early gains in urban high-income ZIP codes and slower uptake in rural areas | Medium term (2-4 years) |

| AI-enabled diagnostics and workflow integration | +1.6% | National, concentrated in multi-site corporate practices and specialty referral centers | Short term (≤ 2 years) |

| Vector-borne disease preparedness and screwworm resilience | +1.2% | Southern border states, Gulf Coast, and Southwest, with spillover risk across the broader South | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Premiumization and Humanization of Pet Healthcare

The United States companion animal health market is experiencing a shift as households increasingly prioritize pets and invest in their care. By 2025, the pet industry spending reached USD 158 billion, with veterinary care contributing USD 41.4 billion, making it a key category.[1]American Pet Products Association, “U.S. Pet Industry Reaches USD 158 Billion in 2025, Poised for Continued Growth in 2026,” APPA News, americanpetproducts.org This trend drives demand for advanced diagnostics, chronic disease treatments, and specialty services, moving beyond routine wellness. Clinics are adopting comprehensive treatment plans, while manufacturers and service providers expand premium offerings in oncology, pain management, dermatology, and long-term monitoring.

Pet Insurance Expansion and Financing-Led Care Acceptance

Pet insurance is becoming a critical driver of treatment acceptance in the United States companion animal health market. In 2025, direct premiums written reached USD 5.47 billion, reflecting double-digit growth. Expanding coverage enables pet owners to access advanced imaging, specialist referrals, and multi-drug protocols, particularly in high-cost treatments.[2]Insurance Information Institute, “Triple-I Highlights Growing Insurance Needs for Pet Owners and Pet Care Businesses,” Morningstar, morningstar.com Financing tools at clinics further support this trend by making expensive care more accessible at the decision point.

AI-Enabled Diagnostics and Workflow Integration

The integration of AI into diagnostics and workflows is advancing the United States companion animal health market. In 2026, IDEXX expanded its oncology testing portfolio with mast cell tumor testing for dogs, complementing its Cancer Dx Panel. Faster interpretations and seamless workflow integration encourage in-clinic testing over outsourcing. However, limited transparency in veterinary AI products highlights the need for stronger standards, which could benefit established suppliers. AI adoption in imaging, pathology, and clinical management is expected to enhance productivity and revenue consistency.

Vector-Borne Disease Preparedness and Screwworm Resilience

Vector-borne diseases are driving demand for parasiticides, vaccines, and screenings in the United States companion animal health market. In 2026, Zoetis emphasized screwworm preparedness, while Merck Animal Health received FDA approval for BRAVECTO QUANTUM, offering expanded tick protection. Disease mapping is becoming critical for product strategies, especially in high-risk regions like Southern states and border areas. Longer-duration preventive products are gaining traction, ensuring better compliance and reducing missed treatments.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High out-of-pocket treatment costs | -1.6% | National, most acute in low-income and rural markets | Long term (≥ 4 years) |

| Affordability gaps and uneven routine-care access | -1.0% | Rural South, Appalachian, and Great Plains regions, including veterinary shortage areas | Medium term (2-4 years) |

| Consolidator formulary discipline and online pharmacy competition | -0.8% | National, with sharper pressure in suburban practice clusters near e-commerce distribution centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Out-of-Pocket Treatment Costs

Affordability remains a key challenge in the United States companion animal health market. High treatment costs delay wellness visits, reduce diagnostic follow-through, and limit specialist procedure adoption despite clinical demand. Missed routine visits impact service revenue and related product sales. Specialty care faces the greatest pressure as costs outpace household budgets, restricting access to premium offerings. Without broader insurance and financing options, out-of-pocket expenses will continue to constrain growth outside higher-income households.

Consolidator Formulary Discipline and Online Pharmacy Competition

The United States companion animal health market is experiencing a channel shift that affects branded product sales. Large veterinary groups are tightening procurement processes, while online pharmacies capture refill demand previously retained by clinics. This reduces in-clinic sales of oral therapies and maintenance products, especially with easy price comparisons. However, clinic-administered injectables and biologics remain less exposed to retail competition, driving manufacturers to focus on categories where clinics retain control over prescribing and administration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Animal Type: Feline Spending Accelerates as Canine Base Matures

In 2025, dogs held 59.35% of the United States companion animal health market share, driven by higher treatment frequency in areas like orthopedics, dental care, and cardiology. The adoption of biologic therapies further boosted revenue, with over 1 million dogs treated with Librela by early 2025, showcasing the rapid scaling of high-value pain management products. Dogs remain the primary revenue anchor, even as growth stabilizes.

Cats are projected to grow at an 11.15% CAGR from 2026 to 2031, making them the fastest-growing segment in the United States companion animal health market. This growth is supported by species-specific innovations, such as a feline liquid biopsy prototype with 97% specificity for lymphoma detection and the launch of RapidRead Dental for Feline. Equine and other companion animals maintain stable demand through preventive care and specialized treatments.

By Product Type: Diagnostics Redefines the Revenue Architecture of the Clinic

Therapeutics accounted for 43.25% of the United States companion animal health market revenue in 2025, benefiting from new approvals and label expansions for chronic and specialty conditions. Key developments include VETMEDIN's clearance for preclinical myxomatous mitral valve disease and NUMELVI's approval for managing pruritus in dogs. The focus is shifting toward pain management, monoclonal antibodies, and chronic disease treatments.

Diagnostics is forecast to grow at a 12.75% CAGR from 2026 to 2031, becoming the fastest-growing product category. Clinics are adopting tools that streamline workflows, such as SDMA kidney biomarker testing integrated into Catalyst chemistry profiles. While digital health platforms are emerging, diagnostics stands out as a key driver of revenue growth through workflow integration.

By Indication: Oncology Pipeline Converts Unmet Need into Market Value

Infectious diseases led the United States companion animal health market in 2025, accounting for 35.78% of revenue, driven by vaccine compliance, parasite prevention, and tick-borne disease management. Expanded tick coverage in products like BRAVECTO QUANTUM highlights the industry's response to evolving risks. Pain and inflammation treatments are also growing due to longer treatment pathways for aging animals.

Oncology is projected to grow at an 11.63% CAGR from 2026 to 2031, driven by earlier detection and expanded diagnostic and treatment windows. IDEXX's Cancer Dx Panel for canine lymphoma has reached nearly 6,000 veterinary practices, establishing a strong diagnostic base. Endocrine and metabolic disorders and cardiology are also advancing with new approvals and label expansions.

By Distribution Channel: Clinic-Led Dispensing Faces Structural Pressure

Veterinary hospital and clinic pharmacies held 65.89% of the United States companion animal health market revenue in 2025, supported by integrated diagnosis, prescription, and administration processes. High-value products like monoclonal antibodies and in-clinic diagnostics reinforce the clinic's role, while retail pharmacies cater to routine OTC items and supplements.

E-commerce and online pharmacies are forecast to grow at a 10.95% CAGR from 2026 to 2031, driven by refill convenience, auto-ship programs, and price transparency. Chewy's acquisition of Modern Animal reflects the shift toward a comprehensive care model combining clinics, pharmacies, and virtual support. Smaller channels like compounding pharmacies and mobile veterinary services address niche needs effectively.

Geography Analysis

High veterinary spending, a strong network of clinics, and a favorable product approval environment drive consistent launches in diagnostics, biologics, and therapeutics. The broader United States pet industry is expected to grow from USD 158 billion in 2025 to USD 165 billion in 2026, supporting continued healthcare investments. Premium demand is strongest in metropolitan areas like California, New York, Texas, and Florida, where higher pet density, household income, and access to specialty care enable greater adoption of advanced treatments.

Regional disparities in access limit market growth, particularly in rural areas of the South, Appalachia, and the Great Plains, where routine-care access gaps, longer travel times, and fewer specialty providers persist. These challenges delay diagnoses, hinder follow-up care, and restrict treatment adoption outside urban centers. Virtual support and care navigation tools are expanding to address these gaps. For instance, whiskerDocs announced in May 2026 its focus on chronic and preventive care as pets live longer.

Regional disease exposure also shapes market demand. Southern border states, the Gulf Coast, and the Southwest face higher risks of vector-borne diseases, driving demand for parasiticides, vaccines, and screening. In 2026, Zoetis emphasized screwworm preparedness, while Merck's BRAVECTO QUANTUM approval reflected the industry's response to evolving tick exposure patterns. Insurance adoption and digital service availability remain stronger in urban markets, with slower growth in rural areas.

Competitive Landscape

The United States companion animal health market is moderately concentrated, with a few large companies leading in therapeutics, biologics, diagnostics, and workflow systems. In 2025, Zoetis reported USD 6.59 billion in companion animal revenue, a 5% increase. IDEXX achieved USD 4.304 billion in revenue, up 10%, while Elanco recorded USD 4.7 billion, reflecting a 6% rise. Scale provides these companies a competitive edge by spreading costs across extensive customer bases and introducing new products into established clinic platforms. The market favors firms with broad portfolios and strong relationships with clinics, hospitals, and referral networks, particularly where clinical workflows, testing, and treatment are interconnected.

Strategic execution is becoming a key differentiator over product volume. Zoetis, in its Q1 2026 report, identified over 12 potential blockbuster candidates targeting chronic kidney disease, oncology, cardiology, anxiety, obesity, and other high-demand areas. IDEXX is strengthening its workflow integration by incorporating SDMA biomarker testing into Catalyst chemistry profiles and expanding its cancer testing portfolio. Merck Animal Health is enhancing its preventive care offerings with longer-duration parasite protection, addressing needs in regions with high vector exposure.

Competition is expanding beyond traditional manufacturers. Chewy's acquisition of Modern Animal in April 2026 highlights the integration of pharmacies, clinics, and virtual care into a unified healthcare model. Opportunities remain in feline-focused therapeutics and diagnostics, precision monitoring, and AI-driven tools to help clinics manage chronic conditions more effectively.

U.S. Companion Animal Health Industry Leaders

Boehringer Ingelheim International GmbH

Ceva Animal Health, LLC

IDEXX Laboratories, Inc.

Virbac S.A.

Zoetis Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Dechra received FDA approval for CosACTHen, the first cosyntropin specifically approved for canine use to improve the diagnosis and monitoring of Cushing's and Addison's diseases in dogs.

- May 2026: FDA approved Tessie from Orion Animal Health for treating noise aversion and separation anxiety in dogs, with Zoetis planning its U.S. launch by mid-2027.

- May 2026: MSD Animal Health gained FDA approval for NUMELVI, a second-generation JAK inhibitor for managing pruritus in dogs aged six months and older, with availability starting in spring 2026.

- May 2026: IDEXX Laboratories integrated SDMA renal biomarker testing into Catalyst CLIPs, enabling advanced kidney function assessment in U.S. clinics from June 2026.

- April 2026: Chewy acquired Modern Animal, expanding its veterinary footprint from 18 to 47 clinics and adding over USD 125 million in annualized revenue.

- January 2026: IDEXX launched the ImageVue DR50 Plus Digital Imaging System, offering AI-powered imaging with significantly reduced radiation levels for U.S. clinics.

U.S. Companion Animal Health Market Report Scope

As per the scope of the report, the companion animal health industry encompasses the industry dedicated to the medical care, prevention, and overall well-being of household pets like dogs, cats, and horses. It includes pharmaceuticals, vaccines, diagnostic tools, and digital therapies, primarily driven by the increasing "humanization of pets" and a rising demand for advanced veterinary care.

The U.S. Companion Animal Health Market is segmented by animal type, product type, indication, and distribution channel. By animal type, the market includes dogs, cats, equine, and other companion animals. By product type, the market is segmented into therapeutics (vaccines, parasiticides, anti-infectives, NSAIDs & pain management, monoclonal antibodies, medical feed additives, and other therapeutics), diagnostics (immunodiagnostic tests, molecular diagnostics, diagnostic imaging, point-of-care devices, and other diagnostics), and digital health & services (telemedicine platforms, practice management software, and wearable monitoring devices). By indication, the market is categorized into infectious diseases, dermatology/allergy, pain & inflammation, endocrine & metabolic disorders, oncology, cardiology, and others. By distribution channel, the market is segmented into veterinary hospital and clinic pharmacies, retail pharmacies, e-commerce and online pharmacies, and others. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Dogs |

| Cats |

| Equine |

| Other Companion Animals |

| Therapeutics | Vaccines |

| Parasiticides | |

| Anti-Infectives | |

| NSAIDs & Pain Management | |

| Monoclonal Antibodies | |

| Medical Feed Additives | |

| Other Therapeutics | |

| Diagnostics | Immunodiagnostic Tests |

| Molecular Diagnostics | |

| Diagnostic Imaging | |

| Point-of-Care Devices | |

| Other Diagnostics | |

| Digital Health & Services | Tele-medicine Platforms |

| Practice-Management Software | |

| Wearable Monitoring Devices |

| Infectious Diseases |

| Dermatology/Allergy |

| Pain & Inflammation |

| Endocrine & Metabolic Disorders |

| Oncology |

| Cardiology |

| Others |

| Veterinary Hospital and Clinic Pharmacies |

| Retail Pharmacies |

| E-commerce and Online Pharmacies |

| Others |

| By Animal Type | Dogs | |

| Cats | ||

| Equine | ||

| Other Companion Animals | ||

| By Product Type | Therapeutics | Vaccines |

| Parasiticides | ||

| Anti-Infectives | ||

| NSAIDs & Pain Management | ||

| Monoclonal Antibodies | ||

| Medical Feed Additives | ||

| Other Therapeutics | ||

| Diagnostics | Immunodiagnostic Tests | |

| Molecular Diagnostics | ||

| Diagnostic Imaging | ||

| Point-of-Care Devices | ||

| Other Diagnostics | ||

| Digital Health & Services | Tele-medicine Platforms | |

| Practice-Management Software | ||

| Wearable Monitoring Devices | ||

| By Indication | Infectious Diseases | |

| Dermatology/Allergy | ||

| Pain & Inflammation | ||

| Endocrine & Metabolic Disorders | ||

| Oncology | ||

| Cardiology | ||

| Others | ||

| By Distribution Channel | Veterinary Hospital and Clinic Pharmacies | |

| Retail Pharmacies | ||

| E-commerce and Online Pharmacies | ||

| Others | ||

Key Questions Answered in the Report

What is the size of the U.S. companion animal health market in 2026 and 2031?

The U.S. companion animal health market size is USD 8.67 billion in 2026 and is forecast to reach USD 13.91 billion by 2031, growing at a CAGR of 9.92% over 2026-2031.

What is driving growth in companion animal healthcare in the United States?

Growth is being supported by high pet ownership, rising veterinary spending, premium treatment adoption, stronger chronic disease management, expanding pet insurance, and faster diagnostic integration in clinics.

Which animal type generates the most revenue in U.S. companion animal healthcare?

Dogs led the market with a 59.35% share in 2025, supported by higher treatment intensity across orthopedics, dental care, parasiticides, cardiology, and oncology.

Which product category is growing the fastest in the U.S. companion animal health space?

Diagnostics is the fastest-growing product type, with a projected 12.75% CAGR through 2031, helped by point-of-care adoption, AI-enabled tools, and easier workflow integration.

Which indication is expanding the fastest in U.S. veterinary care for companion animals?

Oncology is the fastest-growing indication, with an 11.63% CAGR through 2031, supported by earlier detection tools and a wider downstream treatment pathway.

How is online pharmacy changing the U.S. companion animal care landscape?

E-commerce and online pharmacies are projected to grow at a 10.95% CAGR through 2031 as refill convenience, auto-ship programs, and integrated care models such as Chewy's clinic and pharmacy strategy gain traction.

Page last updated on: