Farm Animal Healthcare Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Market Size (2026) | USD 24.77 Billion |

| Market Size (2031) | USD 31.69 Billion |

| Growth Rate (2026 - 2031) | 5.06% CAGR |

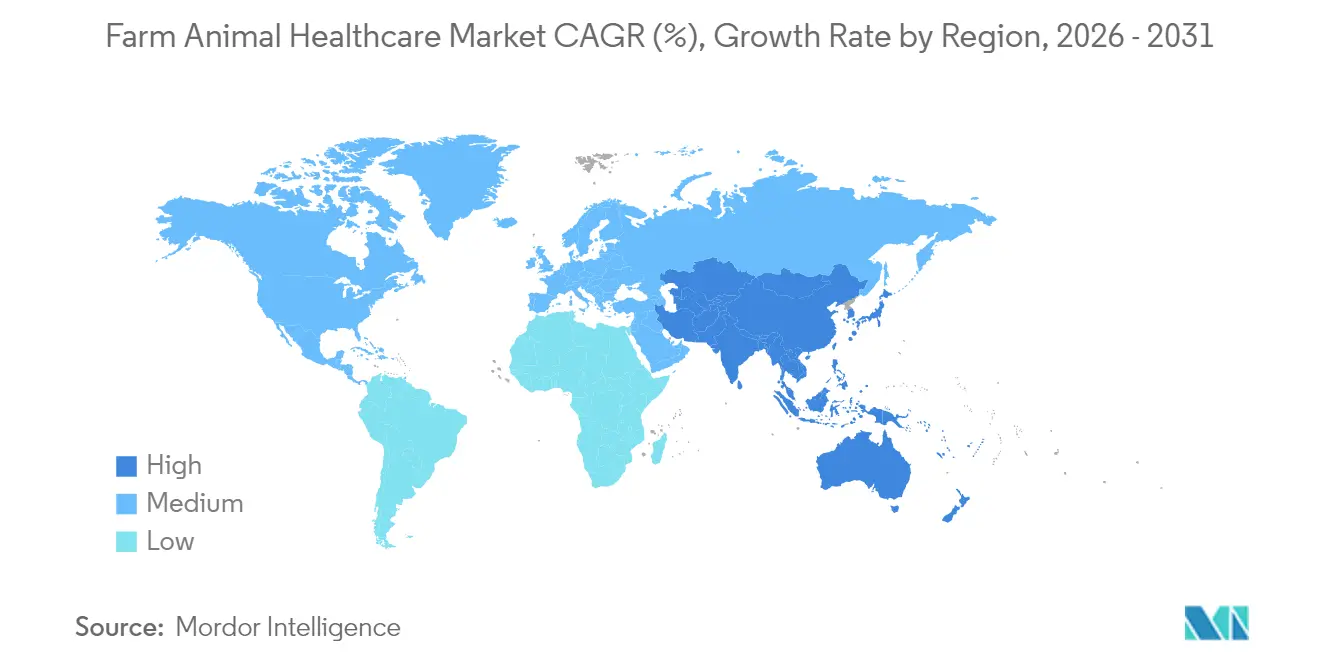

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

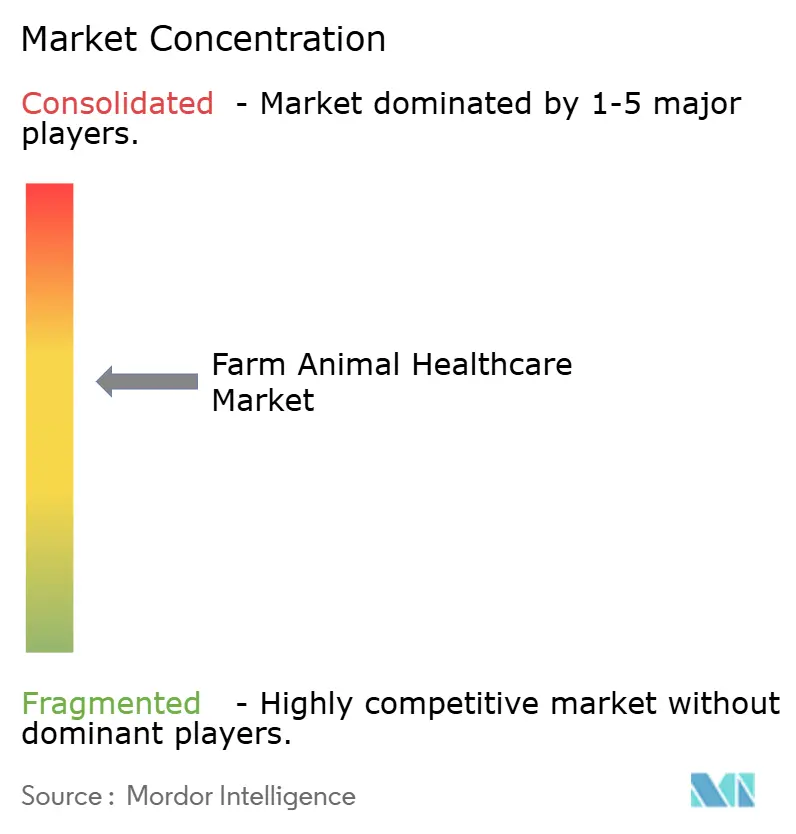

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Farm Animal Healthcare Market Analysis by Mordor Intelligence

The Farm Animal Healthcare market size was valued at USD 23.58 billion in 2025 and estimated to grow from USD 24.77 billion in 2026 to reach USD 31.69 billion by 2031, at a CAGR of 5.06% during the forecast period (2026-2031). Expansion reflects the decisive move toward preventive biologics, wider use of AI-enabled disease-surveillance platforms, and tighter welfare rules that restrict routine antibiotic therapy in favor of vaccination programs. Rapid uptake of precision livestock tools, rising protein demand in emerging economies, and concerted regulatory efforts against zoonotic outbreaks further reinforce growth prospects. Competitive dynamics now hinge on the ability of manufacturers to integrate diagnostics with therapeutics and to supply region-specific vaccines that satisfy heightened compliance standard. At the same time, counterfeit-medicine risks, veterinary workforce gaps, and uneven regulatory alignment across low- and middle-income countries temper overall momentum.

Key Report Takeaways

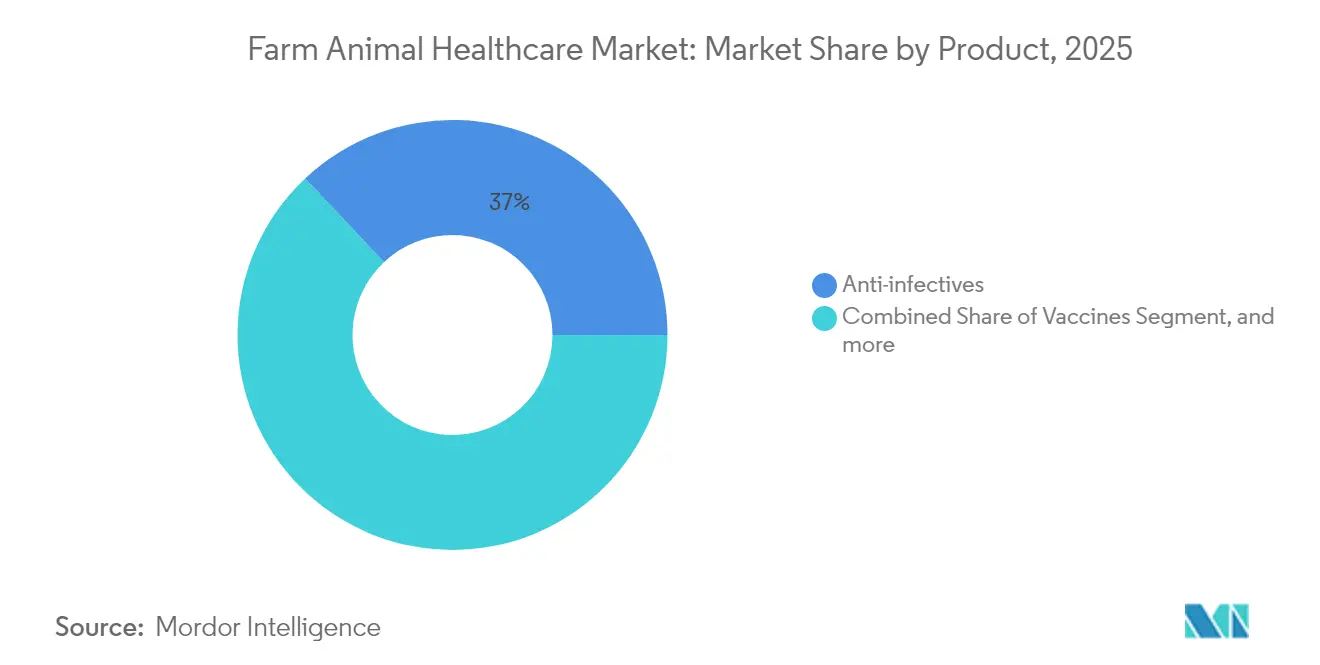

- By product category, anti-infectives led with 37.02% of Farm Animal Healthcare market share in 2025 while vaccines are expanding at a 7.31% CAGR through 2031.

- By animal type, poultry captured 38.10% revenue in 2025 whereas the cattle segment shows the fastest 6.61% CAGR through 2031.

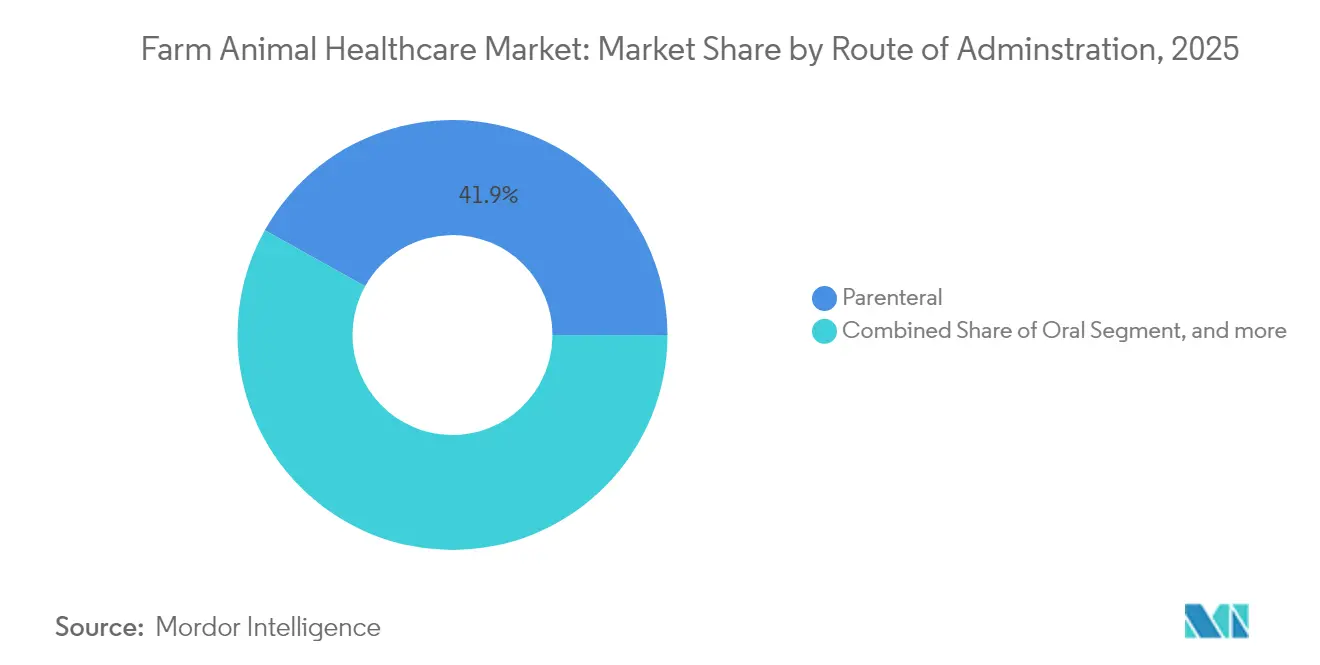

- By route of administration, parenteral products held 41.90% revenue in 2025, and topical formats are rising at a 7.19% CAGR through 2031.

- By geography, North America accounted for 42.70% revenue in 2025, yet Asia-Pacific is advancing at a 6.39% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Farm Animal Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | % (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advanced Technology Accelerating On-Farm Diagnostics | +1.2% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Government & Animal-Welfare Vaccination Mandates | +0.9% | Global, strongest in EU & North America | Short term (≤ 2 years) |

| Growing Threat Of Emerging Zoonoses | +0.8% | Global, with hotspots in APAC & Africa | Long term (≥ 4 years) |

| Shift Toward Preventive Biologics & Integrated Health Plans | +1.1% | Global, led by developed markets | Medium term (2-4 years) |

| AI-Enabled Real-Time Disease-Surveillance Platforms | +0.7% | North America, EU, select APAC markets | Long term (≥ 4 years) |

| Autogenous-Vaccine CDMO Investments In Emerging Markets | +0.5% | APAC, Latin America, MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Advanced Technology Accelerating On-Farm Diagnostics

Portable PCR units and smartphone biosensors now allow barn-side pathogen detection within minutes, reducing outbreak response time from 72 hours to under 12 hours in systems such as Korea’s KAHIS platform[1]Korean Ministry of Agriculture, “KAHIS Annual Performance,” moa.go.kr. Faster diagnosis drives timely treatment, curbs losses, and lifts demand for connected devices that integrate seamlessly with herd-management software. Adoption is most pronounced in North America and Western Europe where capital budgets and broadband coverage are strong. Device makers enjoy recurring revenue through reagent cartridges and data-subscription services. Wider rollout to remote regions hinges on affordable hardware and robust cold-chain logistics for test kits.

Government and Animal Welfare Vaccination Mandates

The European Union’s African Swine Fever program and the USDA National Poultry Improvement Plan obligate commercial farms to follow strict immunization schedules[2]EFSA, “African Swine Fever Control Measures,” efsa.europa.eu. These rules create steady vaccine demand, favor firms with regulatory compliance expertise, and raise entry barriers for generic suppliers. Mandatory programs also spur investment in cold-chain infrastructure and automated mass-vaccination equipment. Emerging economies mirror these policies to secure export certifications, further enlarging the Farm Animal Healthcare market. However, smallholders face higher operating costs and need subsidies or cooperative models to comply.

Growing Threat of Emerging Zoonoses

Climate change and habitat encroachment heighten spillover risk, with 75% of new infectious diseases originating in animals and costing over USD 20 billion yearly[3]WOAH, “Emerging Disease Outlook,” woah.org. Recent HPAI waves across North America and Europe underline the vulnerability of intensive production systems. As a result, governments underwrite rapid-response vaccine stockpiles and push for broad-spectrum biologics. Manufacturers with flexible mRNA or vector platforms can re-formulate quickly, gaining a margin edge. Insurance providers increasingly link policy premiums to farm vaccination status, reinforcing the pivot from treatment to prevention.

Shift Toward Preventive Biologics and Integrated Health Plans

USDA Veterinary Feed Directive rules curbing antibiotic use have accelerated investment in vaccines, probiotics, and biosecurity bundles. Producers now purchase multi-year service contracts that blend immunizations, nutrition plans, and environmental audits. The bundled model promotes long-term relationships between manufacturers, veterinarians, and farmers, raising switching costs. Firms with wide portfolios and field-support teams dominate while single-product specialists hunt for partnerships or niche indications. Integrated programs also generate valuable real-world data that feed AI engines for predictive analytics.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit & Sub-Standard Medicines | -0.6% | Global, concentrated in APAC & Africa | Short term (≤ 2 years) |

| Rising Costs Of Veterinary Services & Testing | -0.4% | Global, most acute in developed markets | Medium term (2-4 years) |

| Acute Rural-Veterinarian Shortage After U.S. FDA GFI-263 | -0.3% | North America, spreading to other regions | Long term (≥ 4 years) |

| Fragmented Regulatory Harmonisation In LMICs | -0.2% | APAC, Africa, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Counterfeit and Sub-Standard Medicines

Substandard products account for 10-15% of global veterinary supply, eroding farmer confidence and fostering antimicrobial resistance. Enforcement raids, such as a USD 2.4 million vaccine seizure in Texas, spotlight the scale of illicit trade. Legitimate firms must invest in serialization, blockchain tracking, and education campaigns, raising operating costs. Emerging markets bear the brunt due to limited oversight and porous borders, which slows legitimate market entry and keeps the Farm Animal Healthcare market from achieving its full potential.

Rising Costs of Veterinary Services and Testing

Average veterinary fees climbed 8.3% per year from 2020-2024, outpacing farm-gate prices and squeezing margins for smaller operations. Molecular diagnostics cost up to five times more than culture methods, yet are increasingly required for trade certification. High costs spur demand for at-home test kits and tele-consulting, but they also force some producers to forgo recommended interventions, limiting revenue upside for suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Vaccines Drive Biologics Revolution

The vaccine segment’s 7.31% CAGR through 2031 underscores a decisive transition to prevention as anti-infectives, despite a 37.02% 2025 revenue lead, face stewardship pressure. Farm Animal Healthcare market size gains stem from mRNA platforms, novel adjuvants, and automated delivery systems that cut labor costs. Manufacturers leverage premium pricing on differentiated biologics, offsetting margins lost to generic antibiotics. Parasiticides keep stable growth as expanding vector ranges threaten grazing herds, while medicinal feed additives face stricter residue rules that trim demand.

Autogenous vaccines expand quickly within the wider vaccine portfolio. Facilities in Brazil and Australia shorten supply chains and customize antigens to farm-specific pathogens, enhancing efficacy and commanding higher prices. Anti-infectives pivot to combination formulations and slow-release injectables to sustain differentiation. Diagnostic manufacturers partner with biologics suppliers to bundle herd-health packages, further boosting Farm Animal Healthcare market penetration.

By Animal Type: Cattle Segment Accelerates Despite Poultry Dominance

Poultry maintained a 38.10% revenue share in 2025 as intensive broiler and layer systems standardize vaccination and biosecurity protocols. The cattle segment, however, leads future growth at a 6.61% CAGR, driven by dairy consolidation and precision farming tools that pinpoint mastitis or respiratory flare-ups early. Farm Animal Healthcare market size for cattle products is set to expand as wearable sensors and AI analytics enable targeted dosing and optimize reproductive performance.

Swine producers grapple with persistent African Swine Fever risks, steering investment toward robust biosecurity and multivalent vaccines. Sheep and goat health remains niche, though targeted parasite control products find traction in arid regions. Aquaculture cross-over technologies gain attention as land-based farmers diversify, enlarging the Farm Animal Healthcare market beyond terrestrial species.

By Route of Administration: Topical Innovation Challenges Parenteral Dominance

Parenteral products commanded 41.90% revenue in 2025 because injectables remain the gold standard for vaccines and critical therapeutics. Topical formats, however, are rising at a 7.19% CAGR as pour-on and microneedle patches deliver long-acting parasiticides without causing injection-site lesions. Farm Animal Healthcare market share for topical solutions will climb as labor shortages intensify and welfare certifications prioritize low-stress treatments.

Oral therapies face tighter controls, yet probiotics and prebiotics retain appeal as antibiotic alternatives. Implantable and inhalation devices are early-stage technologies promising precise dosing and minimal residue, positioning innovators for future Farm Animal Healthcare market disruption.

By Distribution Channel: Digital Transformation Reshapes Traditional Networks

Veterinary hospitals still dominate but direct-to-farm e-commerce climbs rapidly, cutting procurement costs and offering subscription replenishment. Large integrators negotiate bulk rates and favor suppliers that provide data dashboards and remote support. Pharmacies thrive in peri-urban areas, yet on-farm direct sales outpace all channels because manufacturers package products with service contracts that include on-site training. This evolution raises Farm Animal Healthcare market barriers for firms lacking digital infrastructure or field teams.

Supply-chain integrity initiatives such as blockchain tracing strengthen trusted distributors while squeezing gray-market operators. Regulatory audits now scrutinize temperature-logging records, making cold-chain compliance a competitive differentiator across the Farm Animal Healthcare industry.

Geography Analysis

North America, holding 42.70% revenue in 2025, benefits from strong R&D ecosystems, established reimbursement for veterinary services, and early adoption of AI-based surveillance. Ongoing rural veterinarian shortages, though, threaten service coverage and may temper Farm Animal Healthcare market growth in frontier counties. Federal loan-forgiveness programs and mobile clinic initiatives aim to mitigate the gap.

Asia-Pacific leads growth with a 6.39% CAGR through 2031 as China modernizes mega-farms and India scales dairy cooperatives. Regulatory reforms that streamline dossier reviews and recognize international Good Manufacturing Practice certificates improve market entry timelines. Yet diverse languages and non-uniform biosecurity rules continue to complicate commercialization strategies.

Europe sustains moderate gains under strict welfare legislation and comprehensive vaccination mandates. Producers invest in premium biologics and diagnostics to satisfy export-market residue tolerances. Eastern member states allocate EU recovery funds to upgrade cold-chain logistics, broadening Farm Animal Healthcare market access.

South America and the Middle East and Africa represent high-potential, early-stage markets. Brazil and Argentina deploy autogenous vaccine capacity aimed at endemic strains, while Gulf states invest in food-security programs that include large-scale dairy and poultry ventures. Regulatory capacity constraints and counterfeit-product infiltration remain hurdles yet gradual harmonization under trade blocs such as Mercosur offers a clearer path for Farm Animal Healthcare market expansion.

Competitive Landscape

The farm animal healthcare market exhibits moderate concentration as global majors leverage scale, vertical integration, and broad portfolios to retain competitive edges. Zoetis, Merck Animal Health, and Boehringer Ingelheim supplement in-house pipelines with acquisitions of niche technology firms to accelerate time-to-market for novel delivery platforms. Regional leaders such as Ceva Santé Animale and Huvepharma strengthen their positions through autogenous vaccine sites that tailor products to local pathogens, reinforcing customer loyalty.

Digital transformation is the new battleground. Companies integrate IoT sensors, machine-learning analytics, and blockchain tracing into end-to-end health solutions that promise measurable return on investment. Strategic collaborations between vaccine developers and diagnostic innovators create bundled offerings that lock in customers over multi-year contracts and lift switching costs for farms. Smaller players differentiate through deep specialization or geographic focus, often partnering with contract manufacturers to offset scale disadvantages.

Competitive rivalry intensifies around precision livestock farming where hardware, software, and biologics converge. Early-mover advantages accrue to firms that secure patent coverage on data-driven treatment algorithms and seamless device interoperability. Regulatory compliance expertise remains a decisive barrier; established firms maintain dedicated teams versed in filing standards across over 100 jurisdictions, shielding them from fast-moving challengers. Still, disruptive entrants offering low-cost AI platforms or synthetic biology vaccines present credible long-term threats to incumbent Farm Animal Healthcare market leaders.

Farm Animal Healthcare Industry Leaders

Zoetis Inc

Ceva Animal Health

Boehringer Ingelheim GmbH

Elanco

Vetoquinol

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: MSD Animal Health, a division of Merck & Co., Inc., announced that the European Commission has granted the marketing authorization for the INNOVAX-ND-H5 vaccine for chickens.

- March 2024: Zoetis completed a USD 350 million biologics expansion in Australia, adding capacity for autogenous vaccine manufacturing aimed at Asia-Pacific demand.

Global Farm Animal Healthcare Market Report Scope

As per the scope of the report, farm animals are animals that are raised and kept for agricultural purposes. They include cows, chickens, pigs, geese, and horses. The market consists of the prevention and treatment of diseases in farm animals. The scope employs more innovative methods for effective monitoring and tracking of livestock health data, which positively impacts the growth of the market studied.

The farm animal healthcare market is segmented by product (vaccines, parasiticides, anti-infectives, medicinal feed additives, other products), animal type (cattle, swine, poultry, sheep & goats, other animal types), route of administration (oral, parenteral, topical, other routes), distribution channel (veterinary hospitals, veterinary clinics, pharmacies & drug stores, e-commerce, on-farm direct), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The report offers the value (in USD million) for the above segments.

| Vaccines |

| Parasiticides |

| Anti-infectives |

| Medicinal Feed Additives |

| Other Products |

| Cattle |

| Swine |

| Poultry |

| Sheep & Goats |

| Other Animal Types |

| Oral |

| Parenteral |

| Topical |

| Other Route of Administrations |

| Veterinary Hospitals |

| Veterinary Clinics |

| Pharmacies & Drug Stores |

| E-commerce |

| On-farm Direct |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | GCC | |

| By Product | Vaccines | ||

| Parasiticides | |||

| Anti-infectives | |||

| Medicinal Feed Additives | |||

| Other Products | |||

| By Animal Type | Cattle | ||

| Swine | |||

| Poultry | |||

| Sheep & Goats | |||

| Other Animal Types | |||

| By Route of Administration | Oral | ||

| Parenteral | |||

| Topical | |||

| Other Route of Administrations | |||

| By Distribution Channel | Veterinary Hospitals | ||

| Veterinary Clinics | |||

| Pharmacies & Drug Stores | |||

| E-commerce | |||

| On-farm Direct | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East & Africa | GCC | ||

| South Africa | |||

| Rest of Middle East & Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | GCC | ||

Key Questions Answered in the Report

What is the expected value of the Farm Animal Healthcare market in 2031?

The Farm Animal Healthcare market is projected to reach USD 31.69 billion by 2031.

Which product category is growing fastest in livestock health?

Vaccines are advancing at a 7.31% CAGR as producers pivot to preventive care.

Which region shows the fastest growth in animal healthcare demand?

Asia-Pacific is growing at a 6.39% CAGR thanks to livestock sector modernization and rising protein consumption.

What challenge most limits rural livestock health services in North America?

An acute shortage of large-animal veterinarians following FDA prescription changes limits service coverage.

How are counterfeit medicines affecting farm animal health?

Sub-standard products account for up to 15% of supply, undermining treatment efficacy and driving antimicrobial resistance.

Page last updated on: