Companion Animal Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

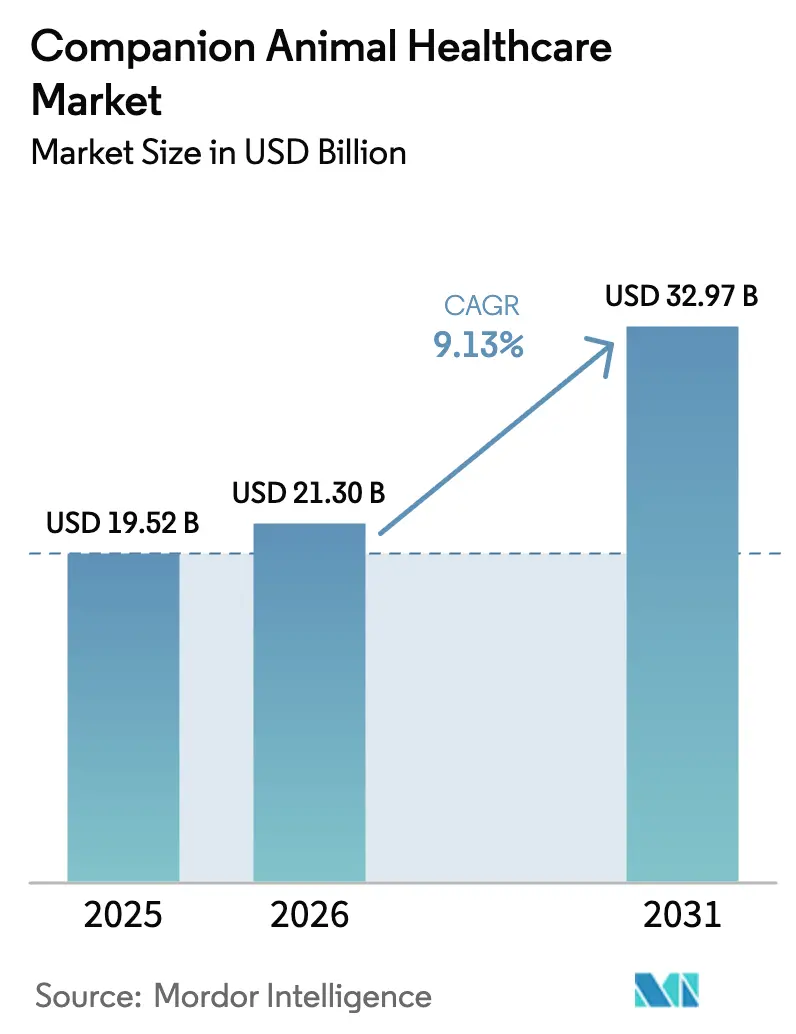

| Market Size (2026) | USD 21.30 Billion |

| Market Size (2031) | USD 32.97 Billion |

| Growth Rate (2026 - 2031) | 9.13% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Companion Animal Healthcare Market Analysis by Mordor Intelligence

The Companion Animal Healthcare Market size was valued at USD 19.52 billion in 2025 and is estimated to grow from USD 21.30 billion in 2026 to reach USD 32.97 billion by 2031, at a CAGR of 9.13% during the forecast period (2026-2031).

Expanding pet insurance coverage, rapid uptake of point-of-care (POC) diagnostics, and the growing acceptance of biologics are collectively reshaping revenue flows across the companion animal healthcare market. Higher disposable incomes among urban households, coupled with the humanization of pets, propel demand for sophisticated interventions ranging from oncology protocols to orthopedic surgeries. Diagnostics that deliver sub-10-minute turnaround times improve clinical decision-making and shorten the gap between symptom onset and therapy initiation, boosting downstream therapeutic sales. At the same time, e-commerce platforms disrupt legacy dispensing models by pairing telehealth consultations with auto-ship subscriptions, while practice-management software integrates diagnostics, billing, and inventory management in a single workflow. Competitive differentiation is shifting from blockbuster drugs toward data-driven services and cloud-connected devices that embed clinics more deeply in the daily routines of pet owners.

Key Report Takeaways

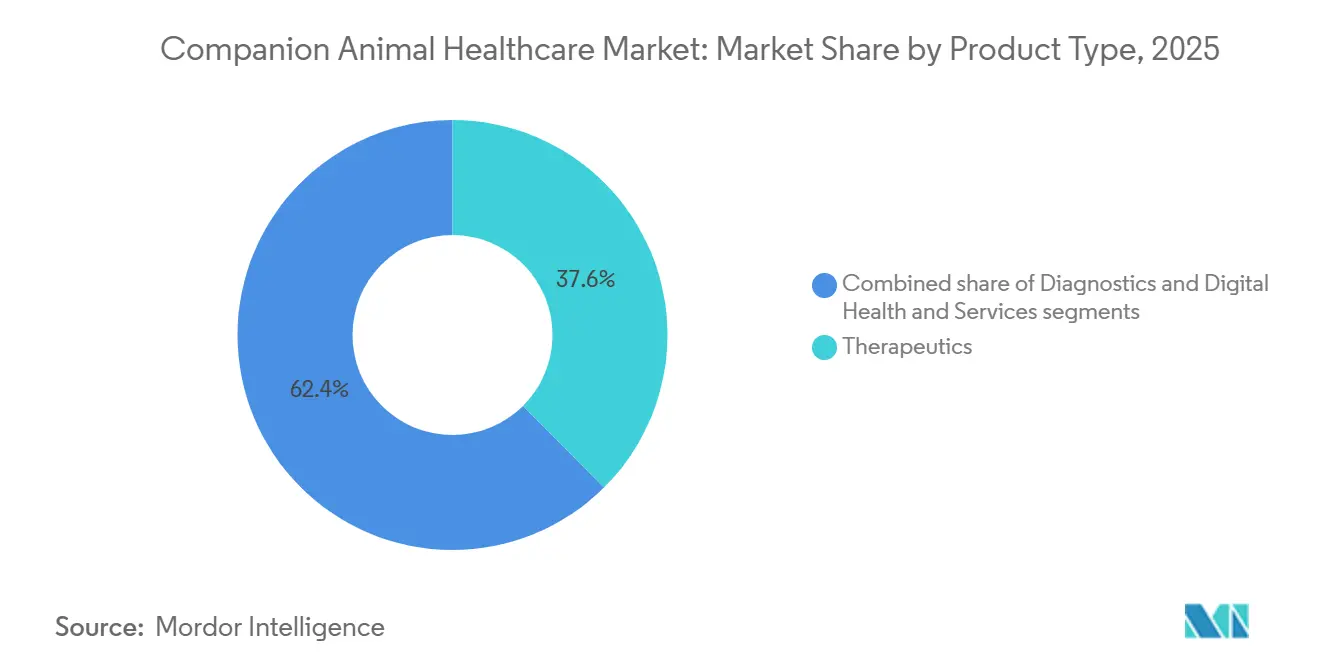

- By product type, diagnostics accounted for the fastest 12.25% CAGR through 2031, whereas therapeutics led the companion animal healthcare market share with 37.56% in 2025.

- By therapeutic area, infectious diseases held 31.53% of the companion animal healthcare market size in 2025, while oncology is forecast to grow at 11.85% CAGR to 2031.

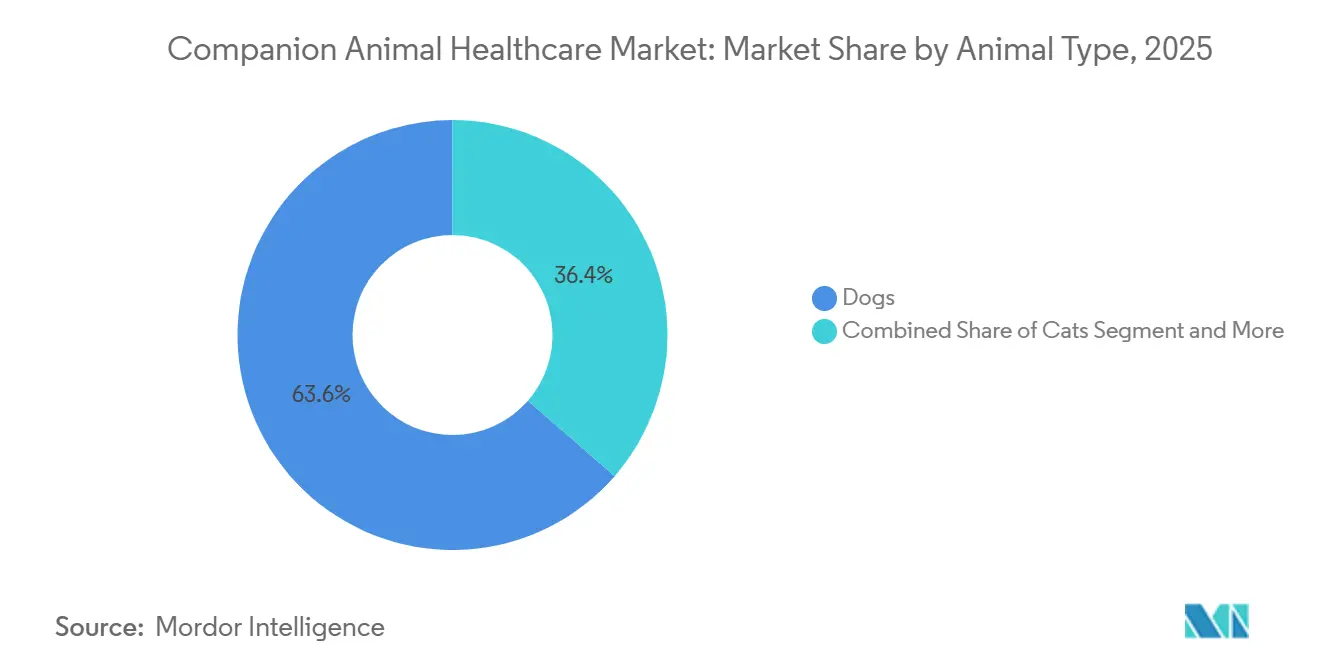

- By animal type, dogs captured 63.63% of the companion animal healthcare market share in 2025; cats will advance at a 10.87% CAGR through 2031.

- By distribution channel, veterinary hospitals retained 75.23% revenue share in 2025, whereas e-commerce is projected to post a 14.7% CAGR to 2031.

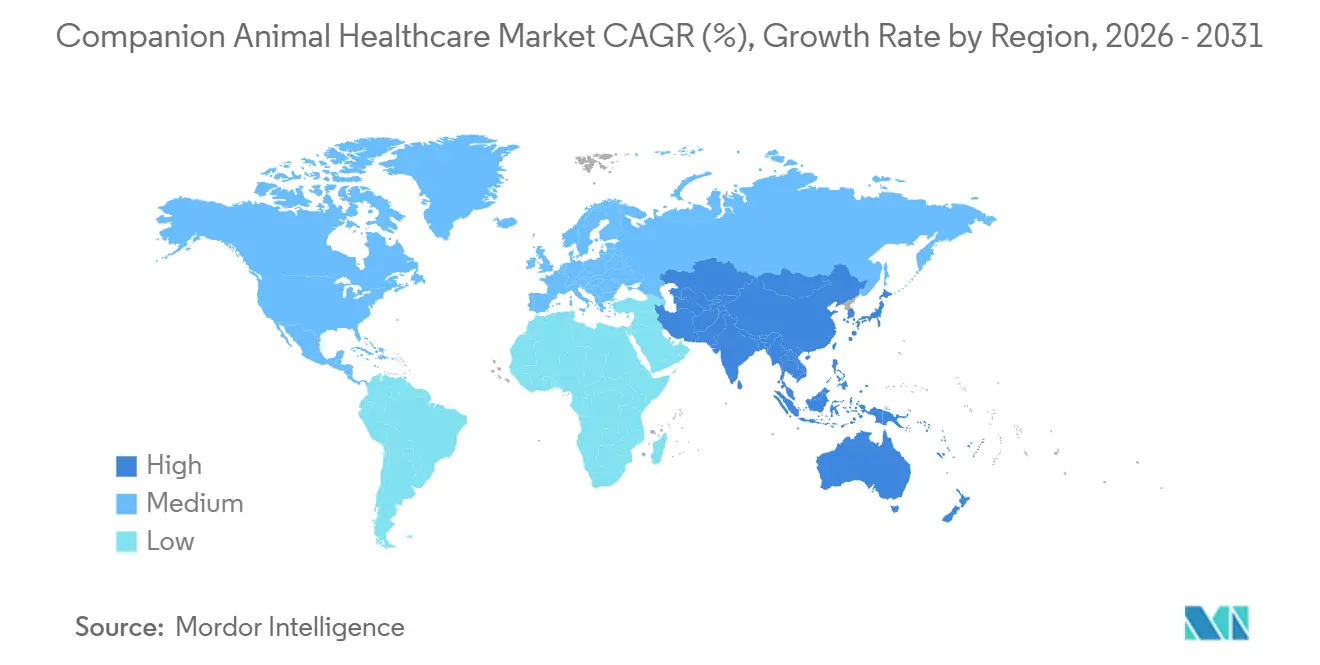

- By geography, North America commanded 36.53% of the companion animal healthcare market in 2025; Asia-Pacific is expanding at 10.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Companion Animal Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increase in Pet Adoption & Humanization | +2.1% | Global, strongest in North America, Western Europe, urban Asia-Pacific | Long term (≥ 4 years) |

| Expanding Penetration of Pet Insurance | +1.8% | North America, Europe, emerging in Japan and Australia | Medium term (2-4 years) |

| Rapid Uptake of Advanced In-Clinic & POC Diagnostics | +1.5% | Global, led by North America and Europe, gaining pace in Asia-Pacific | Medium term (2-4 years) |

| Boom in Chronic-Care Monoclonal Antibodies | +1.2% | North America and Europe, spillover to affluent Asia-Pacific | Long term (≥ 4 years) |

| AI-Powered Predictive Analytics for Preventive Care | +0.9% | North America, Western Europe, pilot programs in Asia-Pacific | Long term (≥ 4 years) |

| Subscription Models Monetizing Wearable Biometrics | +0.7% | North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increase in Pet Adoption & Humanization of Animals

Pet ownership rose to 66% of U.S. households in 2024, with average annual outlays of USD 1,480 per pet, mirroring human wellness budgets[1]American Pet Products Association, “2024–2025 National Pet Owners Survey,” americanpetproducts.org. Owners now opt for procedures once limited to people—organ transplants, chemotherapy, and custom orthopedic implants—thereby elevating average revenue per patient. Millennials and Gen Z show the highest propensity to acquire pet insurance, positioning premium therapies for sustained uptake as these cohorts mature into higher income brackets. Wearable monitors that track heart rate, sleep, and activity create longitudinal datasets that surface conditions earlier, justifying frequent veterinary engagement. Device approvals must align with FDA Center for Veterinary Medicine safety guidelines, which prolong commercialization timelines but fortify consumer confidence. The combined effect is a virtuous cycle where data-driven insights validate higher standards of care and reinforce growth across the companion animal healthcare market.

Expanding Penetration of Pet Insurance

United States pet insurance premiums climbed from USD 3.9 billion in 2023 to USD 4.7 billion in 2024, covering 6.2 million animals and delivering 21.4% year-over-year growth. Insurance uptake enables costly monoclonal antibody injections for osteoarthritis or oncology regimens topping USD 15,000, because 70%-90% reimbursement rates lower owner out-of-pocket exposure. Surgical specialties benefit markedly; orthopedic procedures rose 18% between 2023 and 2024 in lockstep with insurance expansion. Carriers now add preventive diagnostics—annual blood panels and genetic screens—to their formularies, migrating revenue from reactive to proactive care models. The United Kingdom and Sweden already exceed 25% penetration, while Japan’s 2024 tax incentive program is catalyzing regional growth. Increased coverage drives predictable demand, which stabilizes cash flows across the companion animal healthcare market.

Rapid Uptake of Advanced In-Clinic & POC Diagnostics

IDEXX Catalyst One chemistry panels return results in under 10 minutes, allowing same-visit treatment decisions that amplify client satisfaction and clinic throughput. PCR assays for pathogens such as canine parvovirus deliver 24-hour results, down from three to five days in 2020, curbing transmission windows in crowded environments[2]Zoetis, “Zoetis Inc. 2024 Annual Report,” zoetis.com. Integration with electronic health records feeds AI models capable of predicting chronic kidney disease six months ahead of clinician judgment, as documented in a 2024 peer-reviewed study. USDA Center for Veterinary Biologics ensures ≥95% accuracy for diagnostics, providing a compliance floor that weeds out inferior kits. Accelerated diagnostics enlarge the candidate pool for condition-specific drugs, nurturing revenue synergies inside the companion animal healthcare market.

Boom in Chronic-Care Monoclonal Antibodies

Monoclonal antibodies generated USD 1.2 billion in 2024, spearheaded by Librela and Solensia approvals that target nerve growth factor and provide monthly dosing without NSAID side effects. Clinical data show 72% of treated dogs improved mobility after three months, dwarfing the 38% placebo response and justifying USD 150-USD 300 monthly prices at 80% insurance coverage. Oncology biologics are following: USDA granted conditional approval for Gilvetmab in canine lymphoma during 2024, and feline mammary carcinoma trials are progressing. Complex cell-culture production creates a decade-long moat against generics, cementing premium pricing that feeds margins within the companion animal healthcare market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Veterinary Service & Drug Costs | -1.4% | Global, acutest in North America and Western Europe | Short term (≤ 2 years) |

| Global Shortage of Skilled Veterinary Talent | -1.1% | Global, especially rural North America, Europe, emerging Asia-Pacific | Long term (≥ 4 years) |

| Regulatory Lag for Gene-Editing & Cell Therapies | -0.8% | North America and Europe where pipelines are most advanced | Long term (≥ 4 years) |

| Cybersecurity Risks to Connected Vet Devices | -0.6% | North America, Western Europe, urban Asia-Pacific with high IoT adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Veterinary Service & Drug Costs

U.S. veterinary service prices rose 10.2% from 2023 to 2024, dwarfing 3.4% general inflation and lifting routine wellness exams from USD 52 to USD 58. Emergency visits in metro areas now exceed USD 1,500, discouraging timely care among budget-constrained owners. Drug prices mirror this trend: Simparica Trio wholesale cost climbed 8% in 2024 amid API constraints in India and China. Because 94% of U.S. pets remain uninsured, many owners defer elective procedures or pivot to lower-cost generics, tempering near-term growth across the companion animal healthcare market. Price-sensitive regions in Latin America and Southeast Asia feel the strain most acutely, as per-capita veterinary spending stays below USD 50 annually.

Global Shortage of Skilled Veterinary Talent

The United States faced a 15,000-veterinarian shortfall in 2024, with rural vacancies surpassing 30%[3]American Veterinary Medical Association, “Workforce Data 2024,” avma.org . Veterinary school enrollment is rising only 2% annually, insufficient to offset retirements; average practitioner age hit 47 years, foreshadowing further attrition. Appointment wait times stretched to 3.2 weeks for non-urgent visits during 2024, impeding adoption of diagnostics that require specialized training. Europe mirrors the crunch, as the United Kingdom reported a 12% vacancy rate and Germany noted 40% of rural clinics unstaffed. Telemedicine remains constrained by regulations that insist on an existing veterinarian-client-patient relationship, limiting its ability to mitigate workforce gaps. Persistent shortages place a drag on capacity and slow technology diffusion in the companion animal healthcare market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Diagnostics Lead Growth Amid Therapeutic Maturity

Diagnostics represented the fastest-growing category, expanding at 12.25% CAGR through 2031, while therapeutics retained a 37.56% share of the companion animal healthcare market in 2025. Vaccines, parasiticides, and NSAIDs supply a stable base, but their incremental upside is modest as immunization rates plateau in developed economies. Multimodal parasiticides such as Simparica Trio captured owners’ preference for single-dose convenience, yet competitive pressure from generics compresses margins. Monoclonal antibodies for chronic pain and emerging oncology indications are gaining traction, commanding premium pricing and anchoring revenue resilience inside the companion animal healthcare market.

The diagnostics surge is powered by POC devices, immunoassays, and molecular panels that compress turnaround times and facilitate same-visit care. Standard SDMA kidney screenings, once specialty procedures, are now routine during wellness exams. IDEXX alone processes over 200 million tests annually, reinforcing a razor-and-blade model that locks clinics into reagent subscriptions. Cloud integration funnels lab data into practice-management software, supporting AI alerts that flag anomalies in real time. Regulatory oversight by FDA’s Center for Veterinary Medicine ensures ≥95% accuracy, a bar that filters substandard entrants yet lengthens release cycles. Digital health services—telemedicine, wearable analytics, and practice-management platforms—remain smaller but accelerate as clinics seek operational efficiencies.

By Therapeutic Area: Oncology Surges as Infectious Disease Spending Plateaus

Infectious diseases dominated revenue with a 31.53% slice of the companion animal healthcare market size in 2025, fueled by mandated rabies vaccines and endemic parasite control. However, price competition and vaccination saturation restrain future expansion. Oncology, by contrast, is forecast to compound at 11.85% CAGR, riding breakthroughs such as Tanovea-CA1 and Stelfonta that improve survival without the adverse events associated with traditional chemotherapy.

Companion animals exhibit cancer rates comparable to humans, spurring investment in targeted biologics. Tanovea-CA1 achieved a 79% response rate in canine lymphoma, prompting earlier adoption by clinics equipped with in-house diagnostics. Stelfonta offers a non-surgical solution for mast cell tumors, reducing anesthesia risk and recovery time. Dermatology and allergy therapies like Apoquel and Cytopoint enjoy recurring demand, while endocrine disorders deliver predictable insulin and hormone-replacement sales. Together, these dynamics pivot revenue toward chronic disease management, layering predictable cash flows onto the companion animal healthcare market.

By Animal Type: Feline Therapeutics Close the Development Gap

Dogs generated 63.63% of companion animal healthcare market revenue in 2025, driven by a U.S. population of 65 million and higher per-animal spending. Recent launches—Librela, Tanovea-CA1, and Simparica Trio—added USD 800 million in 2024 sales. Canine compliance with diagnostics and imaging is easier owing to temperament, further tilting revenue toward dogs.

Cats, however, are catching up, anticipated to grow 10.87% annually through 2031. Solensia’s approval marks the first feline-only monoclonal antibody, validating a business case for species-specific biologics. Chronic kidney disease affects 30% of cats over age 10, fueling demand for SDMA testing and phosphate binders. Higher incidences of hyperthyroidism and diabetes necessitate lifelong medication, ensuring recurrent revenue. The growing attention to exotic pets, including rabbits and ferrets, signals incremental expansion but remains a small portion of the companion animal healthcare market.

By Distribution Channel: E-Commerce Disrupts Traditional Veterinary Dispensing

Veterinary clinics retained 75.23% share in 2025, yet online channels are scaling at a 14.7% CAGR as convenience and price transparency win favor. Chewy recorded USD 11.15 billion revenue in 2024, with prescriptions hitting 15% of sales after integrating telehealth services that satisfy prescription mandates. Amazon Pharmacy’s 24-hour shipping further erodes clinic dispensing supremacy.

Brick-and-mortar retail pharmacies captured about 5% of dispensing volume within a year of market entry, appealing to owners who consolidate human and pet scripts. Clinics counteract by embedding e-commerce stores into practice-management software, preserving margins while meeting digital expectations. Regulatory safeguards keep controlled substances within licensed channels, but chronic medications—parasiticides, NSAIDs, and diets—migrate swiftly online, reconfiguring revenue distribution across the companion animal healthcare market.

Geography Analysis

North America led with 36.53% share in 2025, benefiting from extensive specialty hospitals and mature insurance penetration. Corporate consolidators such as Mars Veterinary Health operate multi-state clinic networks and central labs that enable same-day diagnostics. Europe contributed roughly 28%, with synchronized EMA approvals expediting monoclonal antibody launches. The United Kingdom’s insurance penetration above 25% sustains high-ticket therapies, whereas Eastern Europe lags on per-pet spending.

Asia-Pacific is poised for 10.21% CAGR, buoyed by rising pet ownership, insurance uptake, and government incentives. China’s urban pet population topped 120 million in 2024, and policies rose 81% to 3.8 million in 2025, signaling willingness to fund preventive and chronic care. Japan’s clinic count rose 8% between 2023 and 2025, underpinned by tax incentives for insurance. India remains nascent but exhibits 15% annual growth in pet adoption across major cities. The Middle East and Africa account for 5% of revenue, and South America represents 6%, with Brazil holding long-term promise despite macro volatility.

Competitive Landscape

Zoetis, Elanco, and Boehringer Ingelheim together account for a meaningful slice of the companion animal healthcare market, yet diagnostics specialists IDEXX and Heska are chipping away by leveraging data ecosystems. Zoetis posted USD 8.5 billion in 2024 animal health sales, with 60% from companion animals, anchored by Librela, Apoquel, and Simparica Trio. Elanco generated USD 4.2 billion after integrating Bayer Animal Health’s portfolio. IDEXX controls more than 70% of U.S. POC diagnostics through subsidized analyzer placements and reagent contracts worth USD 3.7 billion in 2024.

Whitespace innovation targets AI-driven predictive analytics and wearable biometrics. Startups harness electronic health record data to forecast disease onset, while Fi and Whistle monetize subscriptions that alert owners to deviations in activity levels. Zomedica courts independent clinics with ultrasound and assay systems priced 30% below incumbents, narrowing the technology gap for smaller practices.

Corporate practice groups adopt cloud-based software integrating diagnostics, prescriptions, and telemedicine, a capital-intensive undertaking that widens the moat over independent clinics. Concurrently, the Veterinary Hospital Managers Association reported that 12% of clinics experienced cybersecurity incidents in 2024, prompting calls for stricter standards. Regulatory regimes such as USDA’s SECURE rule for gene-edited animals and FDA biologic guidelines protect incumbents but slow pipeline velocity, reinforcing the need for deep pockets and regulatory know-how.

Companion Animal Healthcare Industry Leaders

Zoetis Inc.

Boehringer Ingelheim Animal Health

Elanco Animal Health

Virbac

Merck Animal Health (MSD)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Virbac launched URSOLYX Soft Chews for Cats, extending its muscle-support line following the 2025 debut for dogs.

- December 2025: Vimian Group AB agreed to acquire I-Vet, an Italian diagnostics provider with EUR 5.6 million annual revenue.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the companion animal healthcare market as the total revenue generated worldwide from therapeutics, diagnostics, and digital-health services used to prevent, diagnose, or treat diseases in dogs, cats, and other household pets. Revenues are captured at manufacturer selling price and include prescription as well as over-the-counter products, imaging systems, point-of-care devices, and practice-management platforms.

(Scope exclusion) Products and services aimed solely at livestock, pet food, accessories, or grooming are kept outside this analysis.

Segmentation Overview

- By Product Type

- Therapeutics

- Vaccines

- Parasiticides

- Anti-Infectives

- NSAIDs & Pain Management

- Monoclonal Antibodies

- Medical Feed Additives

- Other Therapeutics

- Diagnostics

- Immunodiagnostic Tests

- Molecular Diagnostics

- Diagnostic Imaging

- Point-of-Care Devices

- Other Diagnostics

- Digital Health & Services

- Tele-medicine Platforms

- Practice-Management Software

- Wearable Monitoring Devices

- Therapeutics

- By Therapeutic Area

- Infectious Diseases

- Dermatology/Allergy

- Pain & Inflammation

- Endocrine & Metabolic Disorders

- Oncology

- Cardiology

- By Animal Type

- Dogs

- Cats

- Other Companion Animals

- By Distribution Channel

- Veterinary Hospitals & Clinics

- Retail Pharmacies

- Online /E-commerce Platforms

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews with small-animal veterinarians, companion-animal pharma managers, pet-insurance actuaries, and procurement heads across North America, Europe, and key Asian economies help us validate utilization rates, average selling prices, and emerging demand triggers. Panel surveys with pet owners and clinic staff further sharpen adoption curves for tele-veterinary platforms.

Desk Research

Mordor analysts begin by mapping the universe through trusted, non-paywalled datasets such as USDA pet population surveys, Eurostat trade files, APPA spending reports, OIE disease notifications, and peer-reviewed journals that track vaccine efficacy or antimicrobial resistance. Company 10-Ks and veterinary hospital filings clarify pricing bands and channel splits, while D&B Hoovers and Dow Jones Factiva enrich company financials and deal flows. We also mine patent families on Questel to spot pipeline biologics and device upgrades. The desk-research list is illustrative; many additional sources are consulted to cross-check figures and definitions.

Market-Sizing & Forecasting

We reconstruct 2024 demand through a top-down pet population × medicalization-rate build, followed by selective bottom-up supplier roll-ups and clinic channel checks that fine-tune averages. Key market fingerprints include vaccination coverage, chronic-disease prevalence, pet-insurance penetration, average vet visit cost, regulatory approval cadence, and e-commerce share. A multivariate regression relates these drivers to historical spend; the model is projected with scenario analysis that flexes GDP-per-capita and insurance uptake. Data gaps in bottom-up counts are bridged by regional proxies adjusted with primary insights.

Data Validation & Update Cycle

Outputs pass three filters: variance check against independent spend benchmarks, peer review by a second analyst, and senior sign-off. Models refresh annually, with interim updates triggered by material events such as major product recalls or pandemics. Before delivery, we rerun the latest quarter's indicators.

Why Mordor's Companion Animal Healthcare Baseline Earns Trust

Published estimates often diverge because firms bucket dissimilar products, apply different base years, or smooth currency swings in unique ways.

Key gap drivers include the inclusion of veterinary service revenue by some publishers, differing cut-offs for production-animal drugs, and variations in assumed ASP inflation. Mordor Intelligence sticks to a clearly defined bundle of goods, applies constant-currency conversions, and refreshes its model every twelve months, which keeps our 2025 baseline of USD 19.52 billion current and comparable.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 19.52 B (2025) | Mordor Intelligence | - |

| USD 19.20 B (2022) | Global Consultancy A | Older base year and narrower digital-health coverage |

| USD 23.08 B (2023) | Regional Consultancy B | Uses retail prices rather than manufacturer prices, inflating totals |

| USD 124.80 B (2024) | Industry Tracker C | Adds veterinary services and certain livestock drugs, greatly widening scope |

The comparison shows that when scope, pricing tiers, and refresh cadence are aligned, Mordor's disciplined framework yields a balanced figure that decision-makers can trace back to transparent variables and reproducible steps.

Key Questions Answered in the Report

What is the projected value of the companion animal healthcare market by 2031?

The market is expected to reach USD 32.97 billion by 2031, reflecting a 9.13% CAGR.

Which product category is expanding the fastest?

Diagnostics lead growth with a projected 12.25% CAGR through 2031.

How large is the pet insurance segment in the United States?

Premiums reached USD 4.7 billion in 2024, covering 6.2 million pets.

Which geographic region will grow the quickest?

Asia-Pacific is forecast to register a 10.21% CAGR, outpacing all other regions.

What factors restrain market expansion?

Rising service costs, a shortage of veterinarians, regulatory delays for gene-editing therapies, and cybersecurity risks are key headwinds.

Page last updated on: