Medical Equipment Calibration Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

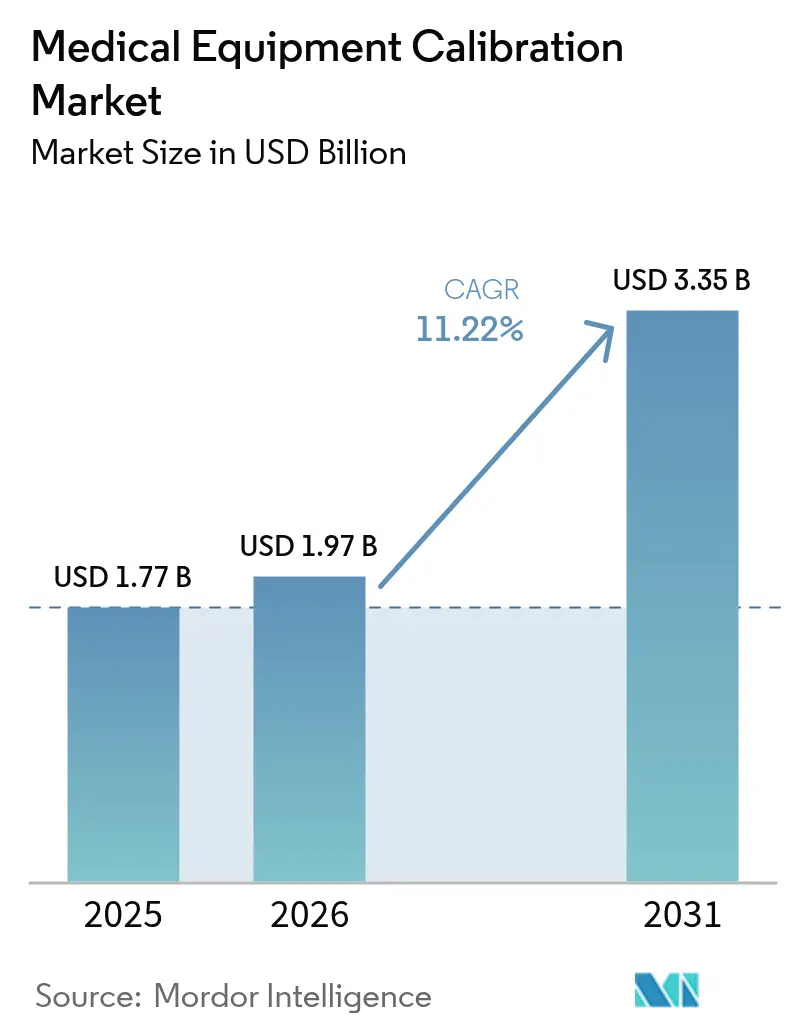

| Market Size (2026) | USD 1.97 Billion |

| Market Size (2031) | USD 3.35 Billion |

| Growth Rate (2026 - 2031) | 11.22% CAGR |

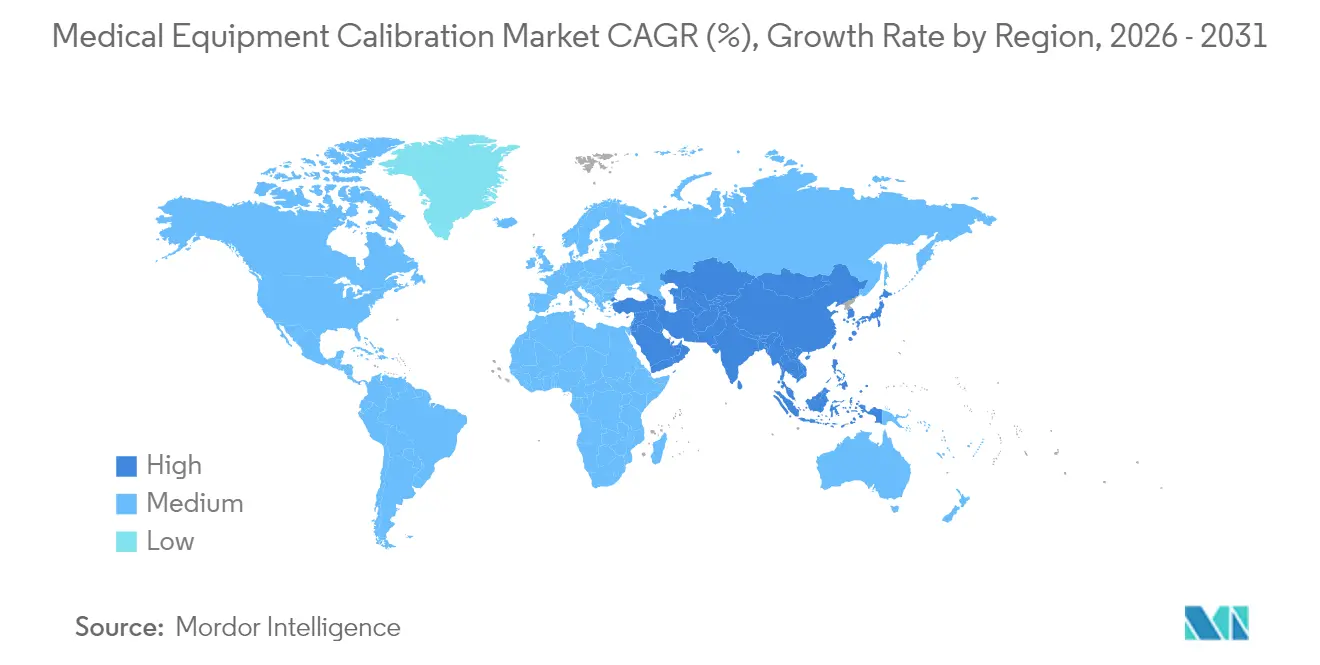

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Equipment Calibration Market Analysis by Mordor Intelligence

Medical Equipment Calibration Market size market size in 2026 is estimated at USD 1.97 billion, growing from 2025 value of USD 1.77 billion with 2031 projections showing USD 3.35 billion, growing at 11.22% CAGR over 2026-2031.

Demand tracks three converging forces: stricter global quality mandates, rapid technology replacement cycles, and the steady spread of advanced healthcare infrastructure. New FDA Quality Management System Regulation amendments taking effect in 2026 will harmonize United States rules with ISO 13485:2016 and reinforce the need for traceable calibration records. Capital spending on AI-enabled imaging, ventilators, and networked monitors expands the medical equipment calibration market because every new device shipped carries a downstream calibration requirement. Hospitals also link reimbursement to device accuracy metrics under value-based care, further embedding calibration into operating budgets.

Key Report Takeaways

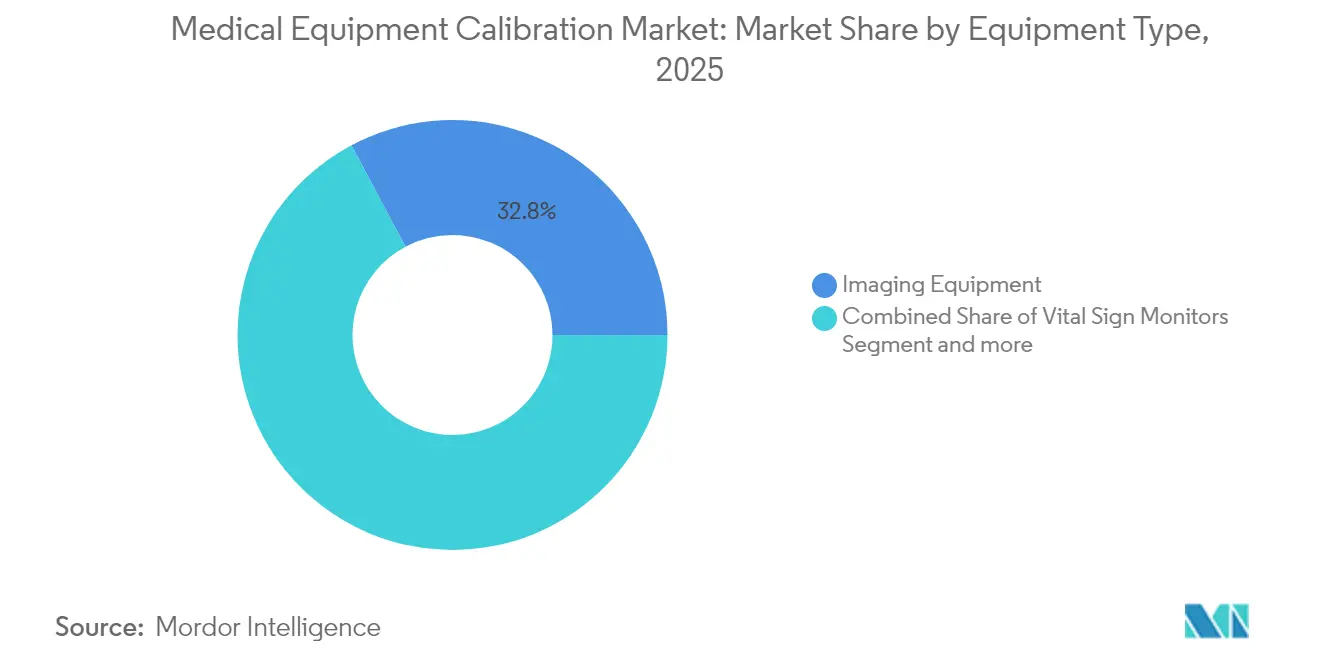

- By equipment type, imaging equipment held 32.78% of the medical equipment calibration market share in 2025; vital-sign monitors are advancing at a 13.73% CAGR to 2031.

- By type of service, OEMs controlled 51.12% of the market in 2025 while third-party firms post the fastest 13.96% CAGR through 2031.

- By end user, hospitals accounted for a 43.95% share of the medical equipment calibration market size in 2025, while home-care and point-of-care settings expand at 15.71% CAGR to 2031.

- By region, North America led with 39.12% revenue in 2025; Asia-Pacific is set to grow at 12.14% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Equipment Calibration Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Global Regulations | +2.8% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Growing Installed Base of High-Value Imaging & Life-Support Systems | +2.1% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Preventive-Maintenance Contracts to Cut Device Downtime | +1.9% | North America & EU primarily, expanding to APAC | Medium term (2-4 years) |

| IoT-Linked Self-Diagnostic Sensors Enabling Micro-Calibration | +1.7% | APAC core, spill-over to North America | Long term (≥ 4 years) |

| Value-Based Procurement Tying Reimbursement to Accuracy KPIs | +1.5% | North America & EU, pilot programs in APAC | Medium term (2-4 years) |

| Home/POC Devices Needing Field-Calibration Kits | +1.2% | Global, with fastest adoption in North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Global Regulations Drive Calibration Standardization

Regulatory harmonization elevates the medical equipment calibration market by embedding calibration traceability into quality audits and device approvals. The FDA QMSR now mirrors ISO 13485:2016, eliminating dual compliance silos and expanding documentation depth.[1]U.S. Food and Drug Administration, “Quality Management System Regulation Final Rule,” fda.gov Europe’s MDR and IVDR impose comparable file-keeping obligations that reach far beyond basic safety checks and push suppliers to maintain chain-of-custody records for every calibration event. China’s NMPA reforms dovetail with the same standards while adding local clinical-trial demands, creating new accreditation work for domestic and multinational laboratories. Regulators also extend oversight to cybersecurity, with draft U.S. guidance requiring a software bill of materials for “cyber devices,” so calibration routines increasingly include security-verification steps.[2]Association for the Advancement of Medical Instrumentation, “Cybersecurity in Medical Devices,” aami.org Collectively, these intertwined rules reshape procurement, service contracting, and technician training.

Growing Installed Base of High-Value Imaging & Life-Support Systems

Hospital capital budgets now revolve around AI-ready CT, MRI, and ventilator platforms. Philips’ helium-free MRI architecture trims running costs yet requires new calibration protocols for a 7-liter magnet in place of traditional 1,500-liter vessels.[3]Philips NV, “BlueSeal Magnet Technology,” philips.com GE HealthCare’s alliance with NVIDIA for autonomous x-ray and ultrasound adds another calibration layer because software models need the same traceability as mechanical parts. These innovations multiply device variants and expand the medical equipment calibration market by shifting the service mix toward algorithm validation, IoT sensor checks, and multi-modal performance tests. Emerging life-support systems embed real-time feedback loops that demand more frequent micro-calibrations to guard patient safety and maintain uptime guarantees negotiated in value-based service contracts.

Preventive-Maintenance Contracts to Cut Device Downtime

Hospitals move away from ad-hoc fixes toward multi-year value partnerships that wrap calibration, software updates, and parts replacement into a flat-rate budget. Siemens Healthineers’ 12-year agreement with University Hospital Nantes (USD 59.9 million equivalent) typifies deals that guarantee uptime and tie penalties to unplanned downtime. Predictive analytics, often delivered through OEM dashboards or third-party platforms such as IBM Maximo, forecast drift weeks before it erodes accuracy. This approach saves labor, improves inventory planning, and locks calibration into a continuous data loop rather than an annual check. As a result, the medical equipment calibration market gains both scope and stickiness.

IoT-Linked Self-Diagnostic Sensors Enabling Micro-Calibration

Embedded sensors give care teams instant feedback on circuit temperatures, flow rates, and voltage stability. Philips e-Alerts for MRI, for instance, flag anomalies in real time and schedule service before faults disrupt patient schedules. Sensor telemetry enlarges the medical equipment calibration market because each alert triggers a targeted micro-calibration that splits the distance between preventive checks and full recalibration. Adoption remains fastest in Asia-Pacific, where new greenfield hospitals specify networked devices from day one, although North American providers follow closely amid staffing shortages. Cybersecurity still tempers full remote-control calibration, especially after reports of back-door access in certain imported monitors, but secure VPN tunnels and zero-trust architectures gradually mitigate risk.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost & Scheduling Complexity in Emerging Markets | -1.8% | APAC emerging markets, Latin America, MEA | Medium term (2-4 years) |

| Scarcity of ISO/IEC 17025-Accredited Technicians | -1.4% | Global, most acute in APAC and emerging markets | Long term (≥ 4 years) |

| Cyber-Security Rules Limiting Remote Calibration Access | -1.1% | Global, with strictest enforcement in North America & EU | Short term (≤ 2 years) |

| AI Autocalibration Data-Integrity Concerns | -0.9% | North America & EU primarily, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost & Scheduling Complexity in Emerging Markets

Healthcare systems in lower-income regions prioritize hardware acquisition over lifecycle services. Supply-chain disruptions raised logistics costs by up to 5% of manufacturer revenue in 2024, inflating calibration expenses for imported reference instruments. Geographic sprawl means a technician may spend two travel days for every service day, which deters routine visits and dampens the medical equipment calibration market. Currency swings further complicate multiyear contracts priced in hard currencies. Large providers respond by pooling demand or inviting global firms like Trescal to set up regional hubs, slowly easing cost burdens.

Scarcity of ISO/IEC 17025-Accredited Technicians

Training pipelines shrink while device complexity climbs. Vacancy rates nearing 20% stretch service lead times and force overtime premiums that lift pricing worldwide. Accreditation paths now require expertise in cybersecurity, risk-based thinking, and cloud analytics, raising the bar for new entrants. Providers fill gaps with automation—Tektronix CalWeb, for example, runs automated test benches and feeds results into compliance dashboards, cutting on-site time by half. Even so, the talent shortage places a ceiling on how fast the medical equipment calibration market can scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Imaging Systems Hold Ground While Monitors Race Ahead

Imaging platforms accounted for 32.78% of the medical equipment calibration market in 2025, reflecting extensive calibration touchpoints from gantry alignment to dose calibration. Each software revision and hardware retrofit drives incremental service revenue and anchors long-term contracts. Algorithmic imaging methods add video-rate adjustments that go beyond classical geometric checks, enlarging scope. Vital-sign monitors, by contrast, post a 13.73% CAGR because home-care adoption multiplies unit volume. Every monitor shipped into a living room extends the medical equipment calibration market to non-institutional settings and triggers portable field-calibration kits. Gradient-free helium MRI, AI-enabled ultrasound, and connected infusion pumps all require bespoke procedures, locking in specialist demand.

Rapid uptake of networked devices means calibration now routinely covers sensors, embedded firmware, and cloud APIs. Infusion pumps rely on gravimetric calibration for flow accuracy, and any firmware patch resets the clock on compliance. Ventilator calibration gained visibility during the pandemic and remains a critical safety hedge in intensive-care units. Surgical tools and laboratory analyzers sustain steady growth, rounding out revenue diversity within the medical equipment calibration market.

By Type of Service: OEM Leads, While Third-Party Niches Expand

OEMs controlled 51.12% of the medical equipment calibration market share in 2025, drawing strength from embedded diagnostics and proprietary software unlocks. Many OEM plans bundle firmware updates, cybersecurity patches, and minor repairs, making them one-stop solutions for hospitals focused on risk avoidance. Third-party providers grow 13.96% per year by pitching lower cost and multi-vendor coverage to independent clinics. They also develop niche expertise laser power calibration or electromedical safety that OEM competitors sometimes outsource.

In-house laboratories thrive inside very large hospital networks where equipment fleets justify dedicated benches. Hybrid arrangements emerge in which routine work stays onsite while complex modalities revert to OEMs or specialty firms, bringing flexibility and spreading risk. Digital portals run compliance documentation and service reminders across all three models, integrating them into a single audit trail and thus widening total spend in the medical equipment calibration market.

By End User: Hospital Core Faces Distributed-Care Momentum

Hospitals remain central with 43.95% revenue in 2025 because high-acuity devices such as cath-lab fluoroscopy and proton therapy machines stay inside bricks-and-mortar campuses. Value-partnership contracts guarantee uptime across hundreds of devices and generate predictable service windows. Laboratories add volume in the form of chemistry analyzers and hematology counters requiring frequent alignment to maintain test accuracy.

Home-care, ambulatory, and OEM labs rise 15.71% per year as payers push care closer to the patient. Portable dialysis, glucose meters, and fetal monitors move into residences or outpatient clinics, triggering new calibration workflows that emphasize lightweight fixtures and cloud-logged certificates. Point-of-care analyzers adopted by ambulance teams introduce calibration tasks in transit environments, broadening the medical equipment calibration industry landscape and demanding ruggedized calibration kits.

Geography Analysis

North America generated 39.12% of global revenue in 2025, supported by early alignment with ISO 13485 and routine FDA surveillance audits. Procurement teams embed service clauses that mandate ISO/IEC 17025 accreditation, cementing a high-entry barrier and rewarding scale operators. Canada’s regulatory modernization and Mexico’s export-oriented device production add regional tailwinds. The medical equipment calibration market size for North America is projected to advance in lockstep with imaging overhauls, tele-ICU rollouts, and cybersecurity mandates.

Asia-Pacific grows at a brisk 12.14% CAGR, propelled by expanding manufacturer hubs in China, India, and South Korea and by fresh hospital construction across Southeast Asia. Government incentives to localize high-end production spur suppliers to build domestic calibration capability, stimulating cross-border joint ventures. Japan’s aging population drives heavy imaging utilization, while the ASEAN Medical Device Directive trims paperwork across 10 countries and speeds vendor onboarding. These factors converge to embed the medical equipment calibration market across the region.

Europe commands a large installed base and a detailed regulatory playbook. MDR and IVDR updates extend calibration from radiology into in vitro diagnostics, inflating task lists and lengthening service contracts. Germany’s export pipeline, France’s hospital investments, and the United Kingdom’s post-Brexit alignment efforts collectively keep demand high. Sustainability preferences open space for newer calibration methods—for instance, helium-free MRI—and render traditional cooling and cryogen checks obsolete. Elsewhere, the Middle East, Africa, and South America register quicker relative growth as they retrofit outdated fleets and build new tertiary centers, though limited technician pools and currency risk temper uptake.

Competitive Landscape

The medical equipment calibration market hosts a mix of diversified industrial groups, OEM service arms, and specialist metrology firms. Trescal, funded by private equity, completed USD 13.1 million in acquisitions across four continents in 2024 to knit a global network able to match multinational device makers’ footprints. OEMs such as GE HealthCare, Siemens Healthineers, and Philips bundle calibration into enterprise-wide imaging refreshes, locking customers for seven-to-twelve-year cycles. Technology firms including IBM and Beamex deploy AI to predict drift, trim turnaround times, and evidence ROI.

Fragmentation persists in emerging economies where dozens of local firms manage electrical safety tests and basic flow meters. Consolidators eye these targets to gain geographic breadth and workforce depth. Cybersecurity credentials now influence award decisions, elevating providers that can validate software hashes and encrypt calibration files.

Medical Equipment Calibration Industry Leaders

JM Test Systems Inc.

Tektronix, Inc.

Godrej.com

ISS Solutions, Inc (Biomed Technologies Inc.)

Fortive (Fluke)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Philips partnered with Evidia to install Ambition BlueSeal MRI and CT 5300 Premium systems at Aleris Elisabeth Hospital in Uppsala, Sweden, introducing sustainability-driven equipment that requires updated calibration routines.

- March 2025: Siemens Healthineers and Tower Health launched a 10-year value partnership to standardize imaging equipment and embed lifecycle calibration across the network.

- March 2025: GE HealthCare and NVIDIA began co-developing autonomous x-ray and ultrasound devices, raising new calibration vectors for AI models.

- February 2025: Philips and Mass General Brigham unveiled a live data framework that streams ventilator and monitor data for real-time analytics, expanding calibration to data-pipeline integrity.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the medical equipment calibration market as all fee-based services that verify and adjust diagnostic, therapeutic, and patient-monitoring devices so that their output falls within manufacturer or ISO-mandated tolerances. Activities range from bench-top verification to on-site multi-parameter recalibration. The global market was valued at about USD 1.77 billion in 2025 and is forecast to reach nearly USD 3.04 billion by 2030, reflecting an 11.4 % compound annual growth rate over the same period.

Scope exclusion: services that recalibrate purely industrial, non-clinical instruments or patient self-testing gadgets sit outside this assessment.

Segmentation Overview

- By Equipment Type

- Vital Sign Monitors

- Ventilators

- Fetal Monitors

- Cardiovascular Monitors

- Imaging Equipment

- Infusion Pumps

- Other Equipment

- By Type of Service

- In-house Calibration Services

- Third-party Calibration Services

- OEM Calibration Services

- By End User

- Clinical Laboratories

- Hospitals

- Others (Home-care, Ambulatory, OEM Labs)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed biomedical engineers inside multi-specialty hospitals, third-party service executives across North America, Europe, and Asia-Pacific, and procurement managers at OEM service labs. Their insights guided us in validating average service pricing, frequency of recalibration, and typical outsourcing ratios, allowing us to refine assumptions surfaced during desk work.

Desk Research

We began by mining unrestricted data from tier-1 regulators such as the U.S. FDA's recall and MAUDE databases, the European Commission's EUDAMED notices, and periodic guidance from ISO 13485 custodians to map mandatory calibration intervals. Trade bodies, including AAMI, IEEE's medical device working groups, and the International Organization of Legal Metrology, provided benchmarks on equipment accuracy drift. Our team then extracted hospital and laboratory equipment installed-base figures from national statistics portals (e.g. CDC's NHSN, Eurostat medical technology files) and cross-checked trends via peer-reviewed journals in Biomedical Instrumentation & Technology.

To size revenue, we accessed audited filings and investor decks of leading calibration providers through D&B Hoovers, complemented by headline contract values captured in Dow Jones Factiva. Shipment traces from Volza and patent renewal counts in Questel helped us calibrate emerging-market demand. This list is illustrative; numerous additional open and paid sources contributed contextual data and gap clarifications.

Market-Sizing & Forecasting

A top-down model reconstructs the global serviceable market from installed counts of imaging, vital-sign, and infusion devices, applying region-specific calibration frequency and average service price assumptions. Supplier roll-ups on sampled MRI, ventilator, and infusion-pump fleets act as selective bottom-up checkpoints. Key variables include ISO-mandated calibration cycles, growth in high-value imaging installations, hospital bed additions, service-price inflation, and the share of outsourced contracts. Multivariate regression, feeding these drivers, produces the 2025-2030 outlook, while scenario analysis stress-tests high-regulation and low-capex futures.

Data Validation & Update Cycle

Outputs pass three stages: internal variance scans, peer review by a senior analyst, and anomaly reconciliation with fresh public filings. Reports refresh annually, and interim updates trigger when regulatory shifts or sizable mergers materially alter baseline assumptions. A final pass occurs immediately before client delivery.

Why Mordor's Medical Equipment Calibration Baseline Inspires Confidence

Published market values often diverge because firms adopt different service scopes, calibration intervals, and currency bases.

According to Mordor analysts, choosing a device-level installed-base anchor and an annually refreshed price book keeps our baseline tightly linked to measurable activity. For context, other 2024 estimates span USD 1.63 billion to USD 1.94 billion.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.77 B (2025) | Mordor Intelligence | - |

| USD 1.63 B (2024) | Global Consultancy A | Excludes calibration of home-care devices and relies on a conservative 15-month interval assumption |

| USD 1.94 B (2024) | Trade Journal B | Blends maintenance revenues with calibration fees, inflating addressable value |

| USD 1.70 B (2024) | Industry Association C | Uses list-price averages without discount normalization and omits emerging-market uptake |

In short, our disciplined scope selection, dual-approach modeling, and rolling data checks give decision-makers a transparent, repeatable baseline that balances caution with real-world market signals.

Key Questions Answered in the Report

What is the projected size of the Medical Equipment Calibration Market in 2031?

The Medical Equipment Calibration Market size is forecast to reach USD 3.35 billion by 2031 under an 11.22% CAGR during 2026-2031.

Which equipment category currently commands the largest share?

Imaging systems such as CT, MRI, and x-ray units held 32.78% of global revenue in 2025 within the Medical Equipment Calibration Market.

Why are third-party calibration providers growing faster than OEM service arms?

Hospitals and clinics adopt multi-vendor cost-optimization strategies, pushing third-party firms to a 13.96% CAGR through 2031 in the Medical Equipment Calibration Market.

How do new FDA regulations affect calibration demand?

The FDA QMSR aligns U.S. rules with ISO 13485 and mandates deeper traceability, expanding documentation and service requirements.

Which region will see the fastest calibration service growth?

Asia-Pacific is projected to record a 12.14% CAGR through 2031 in the Medical Equipment Calibration Market thanks to rapid hospital construction and local device manufacturing expansion.

What is the main bottleneck slowing service capacity worldwide?

A shortage of ISO/IEC 17025-accredited technicians vacancy rates near 20% in some regions limits how quickly providers can scale.

Page last updated on: