Capnography Devices Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

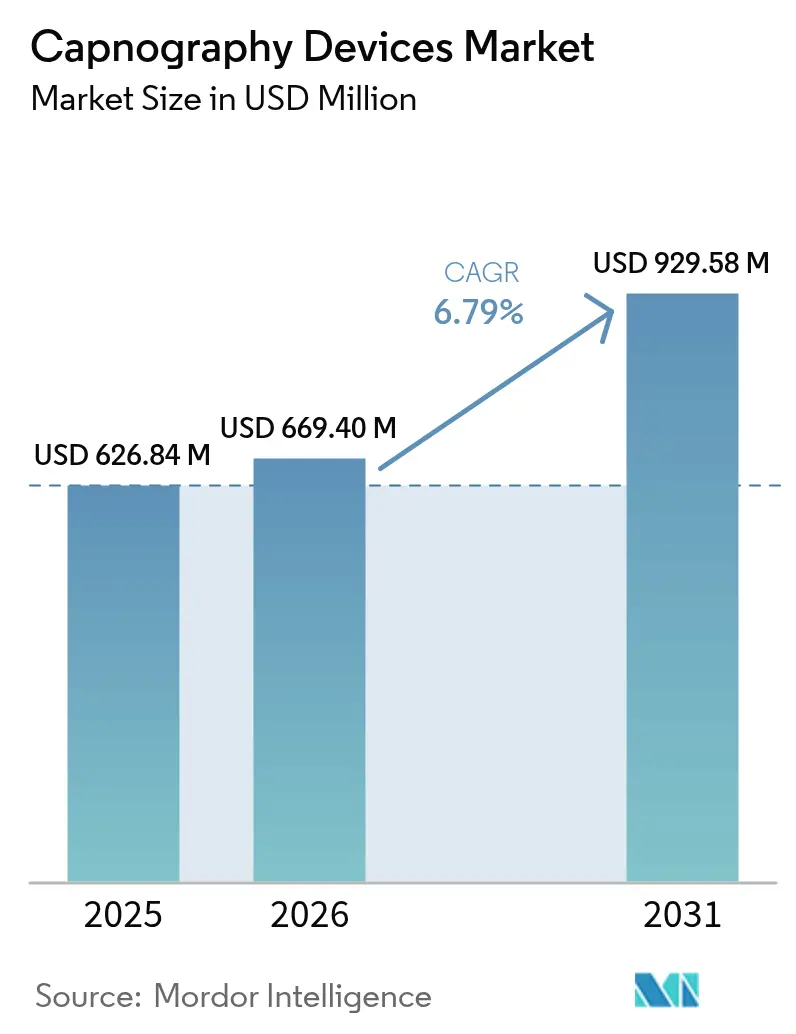

| Market Size (2026) | USD 669.4 Million |

| Market Size (2031) | USD 929.58 Million |

| Growth Rate (2026 - 2031) | 6.79% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Capnography Devices Market Analysis by Mordor Intelligence

The Capnography devices market size is expected to grow from USD 626.84 million in 2025 to USD 669.4 million in 2026 and is forecast to reach USD 929.58 million by 2031 at 6.79% CAGR over 2026-2031. Rising recognition of capnography as a front-line safeguard against respiratory compromise and its expanding role in early sepsis detection keep demand firm across acute, ambulatory and home-care settings. Growth is reinforced by steady procedural volume gains, especially in outpatient centers where continuous CO₂ monitoring is now considered essential for patient safety. Technology innovation is accelerating, led by AI-enhanced waveform analytics, micro-stream sensors that operate at ultra-low flows and wireless form factors that integrate seamlessly with remote patient-monitoring hubs. The Capnography devices market is also benefitting from widening professional-society endorsements that make CO₂ monitoring mandatory for moderate sedation, gastrointestinal endoscopy and opioid-based pain management, prompting hospitals to retrofit existing monitors with capnography modules. While supply-chain pressures and technologist shortages weigh on installation timelines, the underlying demand drivers remain intact, pointing to a resilient medium-term outlook.

Key Report Takeaways

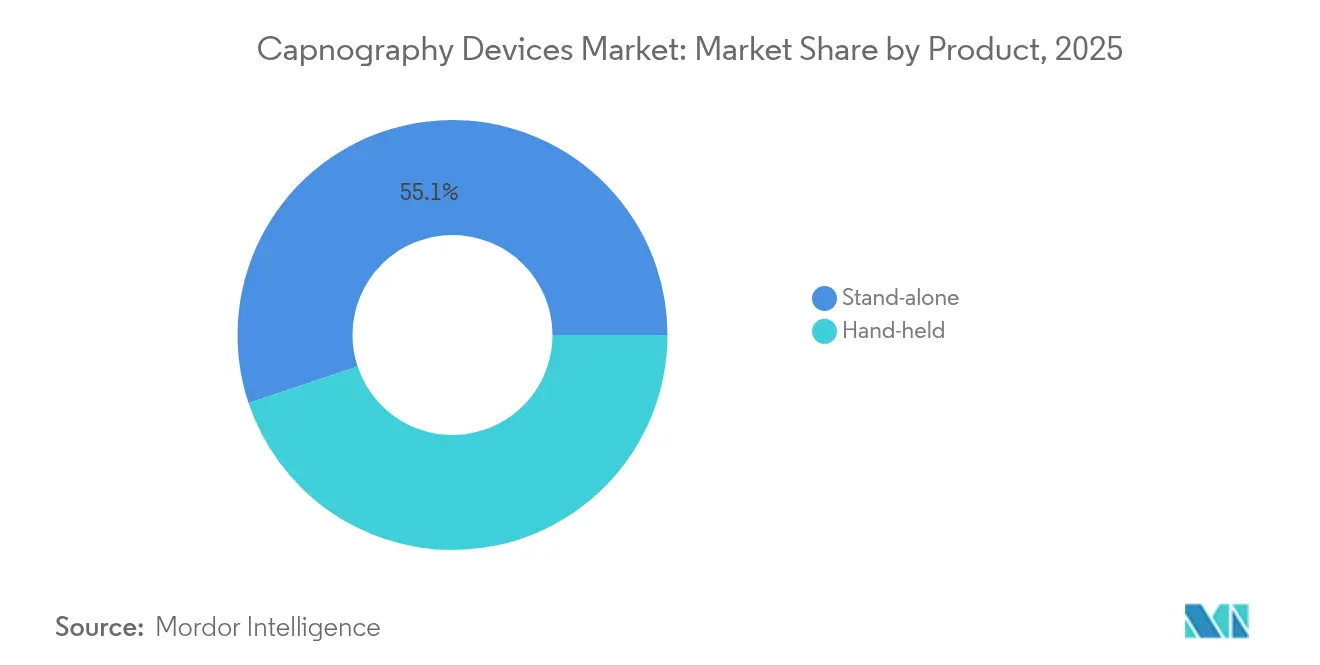

- By product type, stand-alone systems led with 55.12% revenue share in 2025, whereas hand-held devices are projected to record the fastest 7.66% CAGR to 2031.

- By technology, the side-stream segment held 61.78% of Capnography devices market share in 2025; micro-stream platforms are forecast to expand at an 7.92% CAGR through 2031.

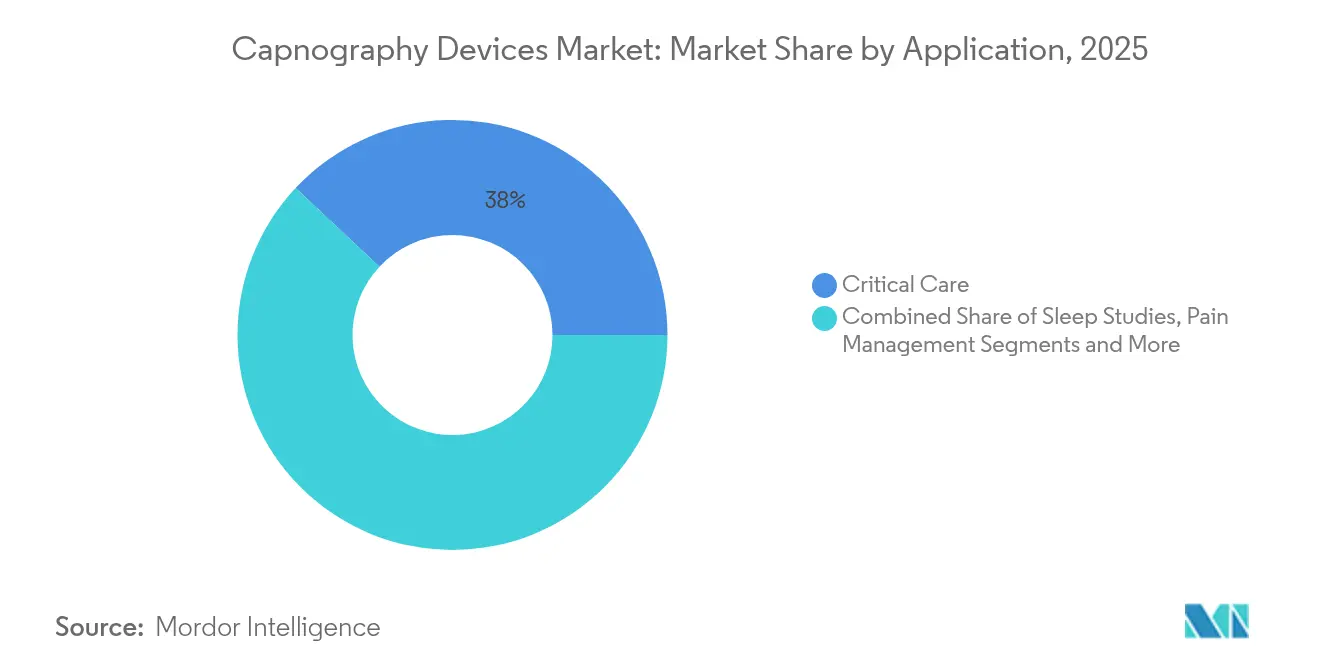

- By application, critical-care monitoring accounted for 38.02% of Capnography devices market size in 2025, while procedural sedation is advancing at an 8.19% CAGR to 2031.

- By end-user, hospitals dominated with 66.88% share in 2025; ambulatory surgical centers show the highest 8.66% CAGR outlook.

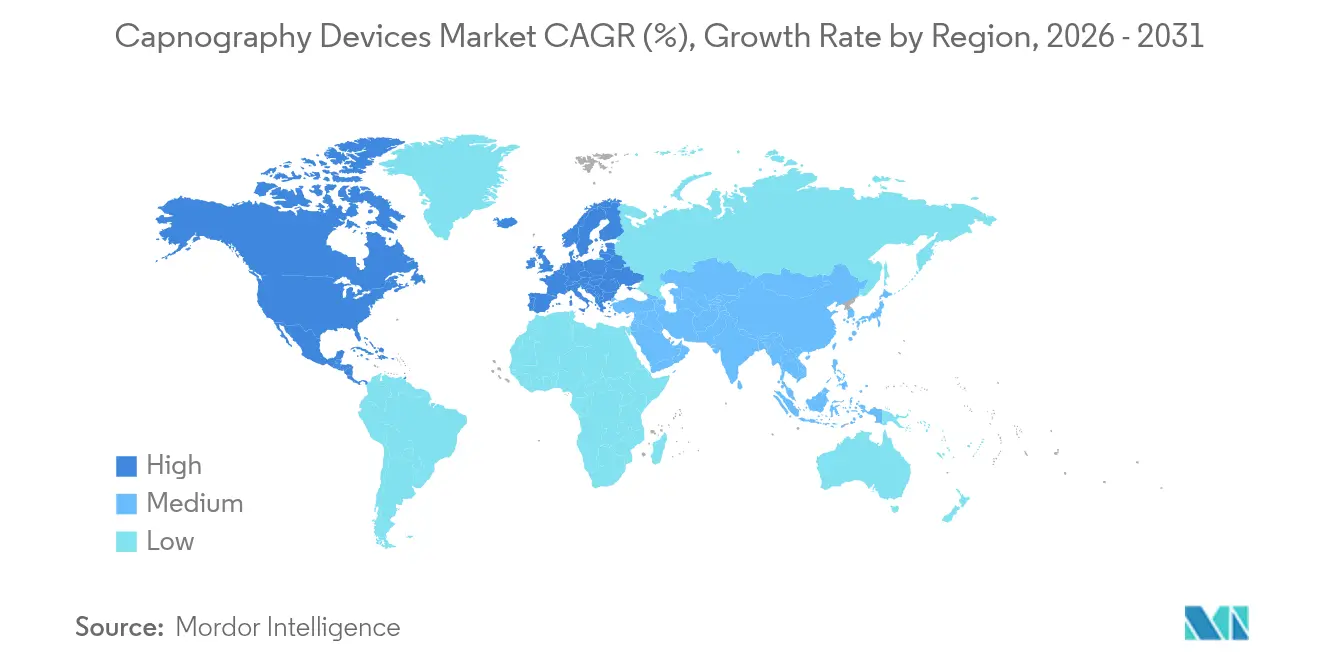

- By geography, North America captured 42.32% share in 2025; Asia-Pacific is the fastest-growing region at 9.08% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Capnography Devices Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Number Of Surgeries Worldwide | +1.2% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Growing Prevalence Of Respiratory Diseases | +1.5% | Global, particularly APAC and emerging markets | Long term (≥ 4 years) |

| Technological Advancements In Capnography Devices | +1.8% | North America & EU leading, APAC adoption following | Short term (≤ 2 years) |

| Strong Professional-Society Recommendations | +0.9% | Global, with regulatory emphasis in developed markets | Medium term (2-4 years) |

| AI-Enabled Waveform Analytics For Early Sepsis Detection | +1.1% | North America & EU core, expansion to APAC | Short term (≤ 2 years) |

| Integration Of Capnography Into Remote-Patient-Monitoring Wearables | +0.8% | Global, with early adoption in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Number of Surgeries Worldwide

Ambulatory surgical centers treated 3.3 million Medicare beneficiaries in 2024, underscoring a systemic shift toward outpatient care where reliable respiratory monitoring is indispensable [1]Medicare Payment Advisory Commission, “Report to the Congress: Medicare Payment Policy,” medpac.gov. Enhanced recovery protocols and increasingly complex minimally invasive techniques demand real-time CO₂ measurement to catch hypoventilation before oxygen saturation drops. As more specialties adopt moderate sedation outside the operating room, Capnography devices market adoption widens among gastroenterologists, cardiologists and pain-management teams. Purchasing decisions now prioritize monitors that are portable, battery-powered and Wi-Fi–enabled, allowing seamless use from pre-op to discharge bays. Vendors that bundle disposables under value contracts are gaining traction by lowering per-procedure costs in price-sensitive ambulatory settings.

Growing Prevalence of Respiratory Diseases

Chronic respiratory illnesses such as COPD and post-viral complications continue to rise, pushing healthcare providers to adopt continuous CO₂ monitoring for early deterioration detection. Capnography has demonstrated higher sensitivity than pulse oximetry alone in identifying hypoventilation, which is driving protocols that combine both modalities in respiratory wards. Sleep labs increasingly deploy portable capnographs for home-based studies, supporting faster diagnosis and treatment initiation for obstructive sleep apnea. Public-health agencies warn of elevated readmission rates tied to undetected nocturnal hypoventilation, prompting insurers to reimburse capnography use in chronic-care bundles. These dynamics nurture sustained Capnography devices market expansion across in-patient and at-home environments.

Technological Advancements in Capnography

Manufacturers have miniaturized infrared sensors and embedded machine-learning firmware that extracts predictive indicators from raw waveforms. The latest micro-stream modules require 50% fewer calibrations and reliably operate in sub-200 mL min-¹ flow conditions, which is critical for neonatal and transport cases. AI-driven analytics flag sepsis risk up to six hours before conventional symptoms, achieving 97% prediction accuracy in multi-center trials. Cloud connectivity also enables remote biomedical service diagnostics, reducing instrument downtime. Collectively, these innovations help hospitals standardize on a single monitoring architecture, fueling repeat-purchase and software-upgrade revenue streams that underpin long-term Capnography devices market growth.

Strong Professional-Society Recommendations

Guidelines from the American Society of Anesthesiologists, the American College of Emergency Physicians, and the European Society of Gastrointestinal Endoscopy call for mandatory CO₂ monitoring during moderate sedation procedures. Compliance audits increasingly reference capnography trace documentation as proof of vigilance, encouraging facilities to retrofit legacy monitors. Specialty boards incorporate waveform-interpretation modules into maintenance-of-certification curricula, ensuring new cadres of clinicians can read capnograms fluently. Insurers in several U.S. states now link quality bonuses to documented CO₂ monitoring, embedding capnography deeper into clinical workflow. This regulatory-plus-education push reinforces an adoption flywheel that keeps the Capnography devices market on a positive trajectory.

Restraints Impact Analysis of Capnography Devices Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage Of Skilled Respiratory & Anesthesia Technologists | -0.8% | Global, particularly acute in North America & Europe | Medium term (2-4 years) |

| High Capital & Disposable Costs Of Capnography Systems | -1.1% | Global, with greater impact in emerging markets | Long term (≥ 4 years) |

| Slow ISO Revision On Microstream Disposables Delays Tenders | -0.6% | Global, with concentration in Europe & regulated markets | Short term (≤ 2 years) |

| Limited Neonatal Data On Ultra-Low-Flow Microstream Accuracy | -0.4% | Global, particularly impacting specialized pediatric centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled Respiratory & Anesthesia Technologists

Vacancy rates for respiratory therapists and anesthesia technologists surpassed 12% in 2024, a record high that slows new-device rollouts[2]American Society of Radiologic Technologists, “Workforce Survey 2024,” asrt.org. Facilities without sufficient expertise struggle to interpret complex waveform anomalies, under-utilizing advanced functions and weakening the clinical value proposition. Vendors respond with auto-interpretation software and interactive tutorials to shorten learning curves, but onboarding still extends procurement cycles. Academic programs expand enrollment yet face faculty shortages, signalling that labor tightness will persist into the medium term. Consequently, some hospitals defer capnography upgrades until staffing stabilizes, tempering near-term Capnography devices market momentum.

High Capital & Disposable Costs of Capnography Systems

Standalone monitors range from USD 4,500 to USD 8,000 per unit, and sampling lines can add USD 6-10 per procedure, straining budgets in low-margin facilities. Reimbursement policies seldom cover disposables directly, forcing administrators to justify expenditures via avoided adverse-event costs. In emerging economies, currency volatility compounds procurement risk, delaying tenders until exchange rates settle. Manufacturers pursue cost-down initiatives such as consolidated molding facilities and universal connectors to drive scale benefits. Subscription models bundling service, disposables and analytics are gaining favor, yet high upfront outlays remain a headwind that trims Capnography devices market penetration in cost-sensitive geographies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Capnography Devices Market Segment Analysis

By Product:

Portability Drives InnovationThe Capnography devices market size for stand-alone systems accounted for USD 345.51 million in 2025, equivalent to 55.12% of total revenue. Hospitals value their full-screen displays, waveform storage and advanced alarm options that support critical-care workflows. However, hand-held devices are carving out a rapid 7.66% CAGR thanks to emergency medical services, transport teams and dental practices that require light, battery-powered units. In many regions, EMS protocols now treat capnography as a standard vital sign for intubated patients, propelling bulk purchases by ambulance fleets.

Demand for mobility also spurs hybrid cart-mounted solutions that dock hand-held modules when high-resolution analysis is needed. Manufacturers integrate Bluetooth and cellular modems so paramedics can stream waveforms to emergency departments for pre-arrival triage. As connectivity expands, software subscriptions become a rising share of product revenue, aligning vendor incentives with device uptime. This ecosystem approach positions portable platforms to capture incremental Capnography devices market share even while stand-alone consoles remain indispensable for intensive-care environments.

By Technology:

Micro-stream Gains MomentumSide-stream analyzers retained the largest Capnography devices market share at 61.78% in 2025, favored for versatility and compatibility with existing monitors. Yet micro-stream units are growing at an 7.92% CAGR and are expected to narrow the gap by 2031. Their ultra-low sampling flow minimizes dead-space impact and improves accuracy in neonates, obese patients and those with low tidal volumes. Clinical studies reveal superior correlation between end-tidal CO₂ and arterial PaCO₂ across variable breathing patterns, reinforcing clinician confidence.

Operational efficiency is another selling point: closed water traps slash filter changes and reduce alarm fatigue from clogging. Lower disposables usage limits waste generation, an increasingly important procurement criterion under hospital sustainability mandates. As micro-stream sensors transition from proprietary to semi-standard connectors, price premiums are expected to compress, accelerating conversions. Main-stream technology will remain important in operating rooms that prefer airway-attached cuvettes to avoid sampling delays, but its share is likely to plateau over the forecast horizon.

By Application:

Procedural Sedation ExpansionCritical-care monitoring led 2025 revenues at USD 238.32 million, representing 38.02% of Capnography devices market size. End-tidal CO₂ is entrenched in ventilation weaning protocols and sepsis bundles, ensuring a stable installed base in ICUs. The fastest growth, however, appears in procedural sedation, which is set to climb at an 8.19% CAGR as outpatient endoscopy, electrophysiology and interventional radiology volumes swell. Sedation guidelines now stipulate continuous CO₂ tracking to detect hypoventilation before SpO₂ drops, shifting demand to compact monitors that fit crowded procedure rooms.

Sleep-medicine departments also adopt portable capnographs for at-home polysomnography, capitalizing on reimbursement updates that favor decentralized testing. Pain-management clinics use capnography during opioid titration to avert respiratory depression, creating a secondary surge in demand. Veterinary and dental offices, historically underserved, represent niche but rising users as simplified menus cater to non-anesthesiologist workflows. Together, these developments broaden the clinical footprint and diversify revenue streams within the Capnography devices market.

By End User:

Ambulatory Centers Lead GrowthHospitals commanded 66.88% of Capnography devices market share in 2025, underpinned by ICU, OR and emergency-department demand . They remain the anchor for multi-parameter monitor upgrades that bundle capnography as a plug-in module. Ambulatory surgical centers, however, outpace all others with a 8.66% CAGR to 2031. Cost pressure and patient preference for same-day discharge drive procedural migration, making compact, Wi-Fi-enabled capnographs attractive. These facilities often standardize on consumables to streamline supply chains, encouraging single-vendor agreements.

Home-health agencies and tele-ICU networks also explore wearable CO₂ sensors that feed remote dashboards, though reimbursement pathways are still evolving. EMS organizations continue plugin refresh cycles as evidence mounts that pre-hospital end-tidal CO₂ improves intubation success and post-resuscitation care. Collectively, non-hospital segments are expected to raise their combined share of Capnography devices market size, buffering vendors against budget fluctuations in the acute-care sector.

Geography Analysis

North America Capnography Devices Market

North America remained the largest regional contributor with 42.32% of 2025 revenue, buoyed by early clinician adoption, broad reimbursement and a strong supplier footprint. Federal alignment with ISO 13485 and swift 510(k) pathways shorten time-to-market for product enhancements, keeping domestic portfolios current. Strategic interoperability alliances, such as the 2024 Masimo-Philips integration that embedded NomoLine technology into multi-parameter monitors, give providers a simpler upgrade roadmap.

Europe Capnography Devices Market

Europe delivers steady, replacement-driven growth anchored in stringent safety protocols. The European Commission’s 2025 supply-chain transparency rules compel manufacturers to confirm continuity of capnography disposables, fostering resilient procurement frameworks. National health systems favor integrated monitors that consolidate capnography, oximetry and hemodynamics to minimize bedside clutter. Meanwhile, regional funding for digital health pilots accelerates adoption of cloud-connected capnographs in rural clinics.

APAC, MEA and South America Capnography Devices Market

Asia-Pacific represents the fastest-growing region with a 9.08% CAGR to 2031, propelled by rising surgical volumes, urban hospital construction and increasing chronic respiratory disease incidence. Government initiatives that subsidize ICU bed expansion in China and India indirectly galvanize Capnography devices market demand. Although country-specific regulatory timelines vary, the push for local manufacturing partnerships is reducing import tariffs and speeding deployments. Australia, Japan and South Korea continue as premium-technology markets where AI-enhanced waveform analysis commands early attention. Middle East & Africa and South America trail in adoption but show upticks where public-private partnerships bring modern critical-care infrastructure to tertiary centers.

Regulatory Landscape

Capnography devices are regulated as medical devices with premarket and quality-system requirements that shape time-to-market and documentation. In the United States, the FDA classifies gaseous-phase CO2 analyzers under Product Code CCK as Class II devices subject to special controls (21 CFR 868.1400), and manufacturers must plan for meaningful 510(k) timelines as review duration has trended longer for recent Class II CCK submissions. A recent product example is Covidien, LLC receiving FDA 510(k) clearance (K253030) in May 2026 for the Capnostream 35 Portable Respiratory Monitor, which highlights continued throughput for portable respiratory monitoring platforms.

On the manufacturing and postmarket side, the FDA Quality Management System Regulation (QMSR) became effective on February 2, 2026, aligning US quality system expectations more closely with ISO 13485:2016 and tightening readiness needs for design controls, risk management, and supplier oversight. In Europe, the EU MDR (Regulation (EU) 2017/745) continues to govern conformity assessment, while the European Commission advanced targeted amendment proposals in December 2025 to reduce certain compliance burdens, keeping notified-body capacity and clinical documentation requirements in focus for capnography OEMs and disposable suppliers. Internationally, ISO 80601-2-55 remains the core safety and performance standard for respiratory gas monitors, and active 2026 standard-development activity, including a Serbia standards project for prSRPS EN ISO 80601-2-55:2026, signals an evolving compliance baseline for connected and low-flow monitoring designs.

Value Chain Analysis

The capnography devices value chain starts with upstream electronics and polymer inputs, then moves into precision sensor components (notably NDIR infrared detectors, optics, and gas-sampling valves) for OEM design, assembly, and clinical calibration. Channel execution follows via hospital tenders, GPO frameworks, EMS procurement, and distributor-led placements into ambulatory and home-care settings. A critical profit pool sits in recurring consumables, including sampling lines and water traps for sidestream and microstream workflows, which ties device selection to dependable disposable availability and standard connector strategies.

Operational risk concentrates around specialized infrared sensor components and semiconductor capacity, where shortages can elongate lead times for monitors and embedded modules. Sterilizable plastics and molded disposables also need consistent tooling and quality controls to maintain tender eligibility. Downstream, demand increasingly centers on bundled patient-monitoring ecosystems where capnography modules and disposables attach to installed bases of multiparameter monitors, raising switching costs. BD strengthening its advanced monitoring footprint through the 2024 completion of its Edwards Lifesciences Critical Care product group acquisition shows how large medtech platforms use portfolio breadth and contracting leverage to tighten distribution access and pull-through of monitoring consumables across acute-care accounts.

Competitive Landscape

The capnography space features a moderate concentration level where five leading vendors exceed 65% combined share, yet switchability remains viable due to standard connectors and competitive disposables pricing. Medtronic stakes its leadership on the Microstream portfolio, recognized for low-flow precision and broad OEM integrations. Masimo follows closely, leveraging its NomoLine waterless sampling sets that cut maintenance time and enhance infection control. Philips and Dräger strengthen positions by embedding capnography modules into existing patient monitors, thereby lowering incremental capital outlay for hospitals.

Strategic collaborations define the current playbook. The Masimo-Philips agreement of June 2024 enabled plug-and-play waveform streaming to IntelliVue monitors, reducing training needs for mixed fleets. Becton Dickinson’s 2025 acquisition of a hemodynamic-monitoring unit aims to cross-sell capnography disposables into its extensive critical-care customer base. New entrants target wearable sensors and AI-based analytics, hoping to bypass entrenched capital cycles. However, they face hurdles in clinical validation and reimbursement coding, both of which favor incumbent firms with established service infrastructures.

Competitive edge increasingly hinges on software. Vendors that release algorithm updates to detect apnea, airway obstruction and early sepsis accrue value beyond hardware margins, nurturing subscription revenue. Open-architecture data gateways are becoming table stakes as health-system CIOs insist on seamless EHR integration. Manufacturers that demonstrate cybersecurity robustness and comply with the FDA’s 2025 pre-market software-bill-of-materials guidance are expected to win stakeholder trust and grow Capnography devices market footprint.

Capnography Devices Industry Leaders

Becton, Dickinson and Company

Koninklijke Philips N.V.

Masimo Corporation

Medtronic Plc

Nihon Kohden Corporation

- *Disclaimer: Major Players sorted in no particular order

Capnography Devices Market Companies Covered in this Report

- Medtronic

- Koninklijke Philips

- Masimo

- Dragerwerk

- Nihon Kohden

- Beckton Dickinson

- Smiths Medical (Smiths Group)

- Nonin Medical

- SunMed

- Infinium Medical

- Welch Allyn (Hillrom / Baxter)

- DiMedica

- GE Healthcare

- Zoll Medical

- Hamilton Medical

- Mindray

- Teleflex

- Capnomed

- Qinhuangdao Kapunuomaite Medical

- CapnoMedical (CapnoAcademy)

Market Opportunities and Future Outlook

White space is expanding as capnography moves beyond operating rooms into transport, wearables, and protocol-driven respiratory surveillance. Prehospital and interfacility transport use-cases are broadening through formal guidance, including 2026 clinical protocols that call out nasal cannula capnography for continuous monitoring during patient transport and in respiratory or metabolic presentations such as sepsis, supporting incremental purchases of portable, battery-powered monitors and compatible sampling sets. Evidence dissemination is also widening the neonatal and transport footprint, including July 2026 Journal of Perinatology findings from the CAPNO study on continuous non-invasive capnometry for neonatal transport to detect accidental extubation, reinforcing a defined need for ultra-low-flow accuracy and robust alarm algorithms.

Technology opportunity centers on higher signal quality at low tidal volumes, workflow simplification, and software-led risk detection. FDA 510(k) activity in May 2026 for Covidien, LLC's Capnostream 35 Portable Respiratory Monitor highlights continued product refresh cycles in portable respiratory monitoring, while AI-enabled clinical decision support is moving into continuous monitoring form factors. There is also room to improve faster verification tools in emergency and trauma procedures, including colorimetric capnography applications studied for rapid confirmation tasks where speed can matter operationally, which may open adjacent demand for single-use, low-training consumables alongside traditional waveform capnography in acute-care pathways.

Recent Industry Developments in Capnography Devices Market

- June 2026: Masimo received FDA 510(k) clearance for an AI-enabled opioid-induced respiratory depression (OIRD) detection capability integrated into the Radius VSM wearable continuous patient monitor. The clearance advances capnography-adjacent respiratory risk detection in wearable monitoring workflows and supports broader adoption of software-led surveillance alongside conventional CO2 monitoring in acute and step-down settings.

- September 2025: Philips and Masimo announced a renewed multi-year strategic collaboration to advance access to patient monitoring measurement technologies. The partnership reinforces interoperability and measurement-technology availability across installed monitor fleets, which influences procurement decisions for integrated capnography modules and compatible consumable ecosystems.

- September 2024: BD completed its acquisition of the Edwards Lifesciences Critical Care product group and rebranded it as BD Advanced Patient Monitoring. The move expands BD's smart connected care and advanced monitoring portfolio, strengthening cross-selling leverage for respiratory and hemodynamic monitoring solutions and associated disposables within hospital contracting channels.

Capnography Devices Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers revenue generated from capnography devices that measure and display CO2 waveforms and end-tidal CO2 to support patient monitoring across inpatient and outpatient care, including transport settings. The scope includes stand-alone and hand-held capnography devices used for clinical monitoring.

Scope exclusions: We exclude service contracts, maintenance, and training revenue, and we do not count anesthesia delivery systems unless capnography device revenue is separately identifiable.

Segments Covered in This Report

- By Product

- Hand-held

- Stand-alone

- By Technology

- Side-stream

- Main-stream

- Micro-stream

- By Application

- Critical Care

- Sleep Studies

- Pain Management

- Procedural Sedation

- Other Applications

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Other End-Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping where capnography demand comes from and how it is regulated and reimbursed, since this often explains adoption timing by care setting. We used public sources such as FDA device databases (510(k) and recall notices), CDC and National Center for Health Statistics releases, and CMS hospital and outpatient datasets to understand procedure mix, safety guidance, and setting shifts.

To keep assumptions realistic, we also referenced sources such as WHO health statistics, OECD health expenditure indicators, and peer-reviewed anesthesia and critical care journals that discuss capnography use in procedural sedation, airway management, and respiratory monitoring. Company annual reports and investor presentations were reviewed to understand product positioning and regional exposure, and a paid subscription focused on company financials and news was used to cross-check recent developments. The sources listed above are illustrative, and other public references were also used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work was used to pressure test adoption assumptions and pricing ranges, especially where public data is limited on replacement cycles and the split between hand-held and stand-alone units. We spoke with a mix of hospital clinicians, biomedical engineering and procurement teams, distributors, and device industry experts across APAC, EMEA, and the Americas, so the model reflects buying behavior in critical care and procedural sedation.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 14% | APAC: 41% |

| Mid tier: 48% | Functional/Unit leaders: 40% | EMEA: 32% |

| Smaller Players: 15% | Managers: 46% | Americas: 27% |

Market-Sizing & Forecasting

For sizing, we use a top-down and bottom-up mix. We first reconstruct procedure volumes and monitored patient pools by care setting and geography, then translate that demand into device needs using usage and replacement patterns. The totals are checked using selective bottom-up approximations such as sampled ASP by device category, channel checks, and supplier revenue splits by region, which helps adjust penetration assumptions.

Inputs in the model include procedural sedation volumes, ICU and emergency airway management activity, growth in ambulatory surgical centers, device replacement cycle expectations, and observed price bands for mainstream, sidestream, and microstream technologies. Since utilization differs by setting, we also adjust for transport and pre-hospital usage where it is materially present, and gaps are handled through conservative ranges that are later revisited through follow-up discussions.

Forecasts are built using scenario analysis supported by exponential smoothing for steadier indicators, since guideline updates and capital budget cycles can create step changes. The scenario paths are aligned to expert views on patient safety compliance, technology mix shifts, and hospital spending, and then checked so the growth profile stays practical.

Data Validation & Update Cycle

Model outputs are validated through multiple checks, including comparing implied device volumes against procedure and bed signals, and reviewing whether pricing assumptions match what buyers report from recent tenders. When large variances show up by region or care setting, we revisit the penetration logic and re-contact selected respondents to confirm whether the difference is real or an input issue.

Before sign-off, the work is reviewed in steps so calculations, assumptions, and narrative stay aligned, and unusual growth rates are challenged against independent signals like regulatory actions and hospital utilization trends. Reports are refreshed annually, with interim updates for material events such as a major recall or a notable change in clinical guidance. Right before delivery, we do a fresh final pass so clients receive the latest updated view.

Mordor Intelligence's Capnography Devices Market Size Compared Against Other Published Estimates

Published market numbers for capnography devices can vary even when the topic looks the same, because each publisher picks its own year, scope, and pricing rules. Differences also come from how device categories are grouped, and whether the estimate is built from clinical demand signals or from reported revenue groupings.

The biggest gap drivers in this market usually come from what gets counted as revenue, the base year used, and how technology mix is priced over time. Some estimates blend in accessories or disposables, apply faster ASP uplift, or use a base year that does not reflect recent purchasing patterns and replacement cycles, which can move the market value even before forecast assumptions are applied.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.67 B (2026) | |

| Global Consultancy A | USD 0.67 B (2023) | Uses a 2023 base year and a higher near-term growth path, and the scope may be interpreted more broadly when segmenting by components, which can lead to partial inclusion of disposables or accessory value in some builds. |

| Industry Publisher B | USD 0.67 B (2024) | Anchors the series to 2024 and can diverge when pricing is escalated faster than observed purchasing behavior, or when currency timing and inflation adjustments are applied differently across regions. |

The spread is mainly explained by base-year choice and whether accessory or disposable revenue is included alongside device revenue, rather than a different view on clinical adoption. When the total is anchored to procedure-linked demand and device-only pricing, with replacement cycles rechecked through primary calls, the 2026 value stays consistent with the device scope treatment applied by Mordor Intelligence.

Key Questions Answered in the Report

How big is the Capnography Devices Market?

The Capnography Devices Market size is expected to reach USD 669.4 million in 2026 and grow at a CAGR of 6.79% to reach USD 929.58 million by 2031.

What are the primary barriers to broader capnography adoption?

High capital and disposable costs, along with shortages of skilled respiratory and anesthesia technologists, remain the chief hurdles to faster market penetration.

Who are the key players in Capnography Devices Market?

Becton, Dickinson and Company, Koninklijke Philips N.V., Masimo Corporation, Medtronic Plc and Nihon Kohden Corporation are the major companies operating in the Capnography Devices Market.

Which is the fastest growing region in Capnography Devices Market?

Asia-Pacific shows the highest regional CAGR at 9.08%, driven by rising surgical volumes, investments in ICU capacity, and rapid adoption of AI-enabled medical technologies.

Which region has the biggest share in Capnography Devices Market?

In 2025, the North America accounts for the largest market share in Capnography Devices Market.

Page last updated on: