Diagnostic Dermatology Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

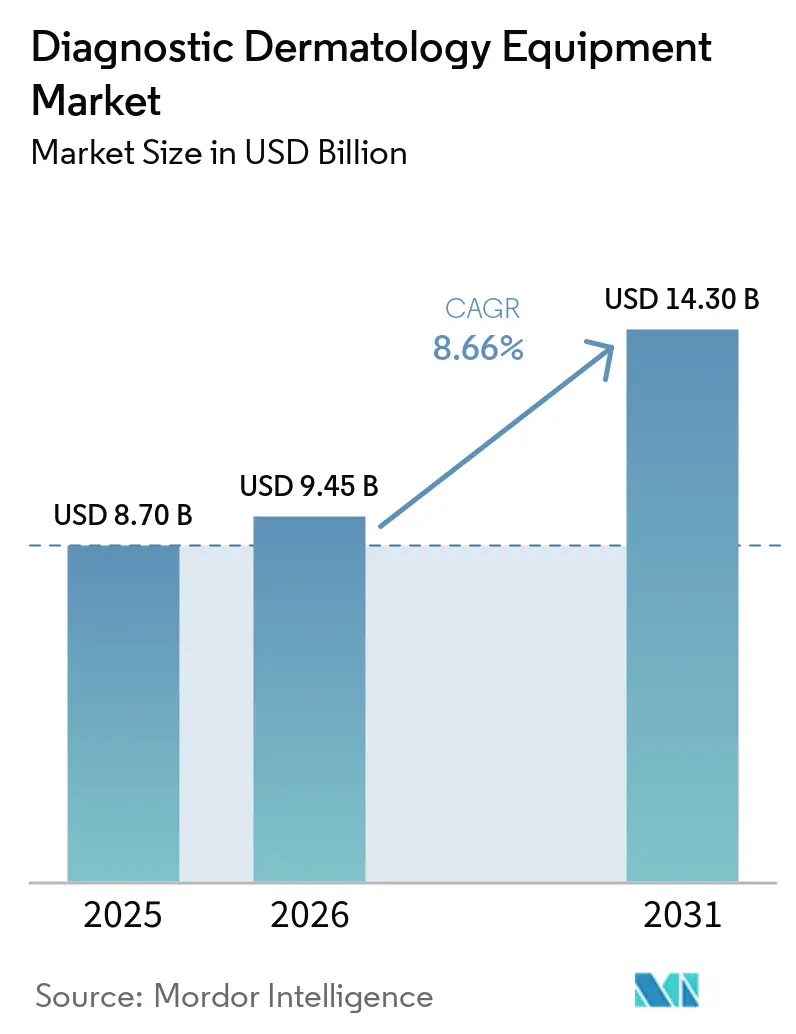

| Market Size (2026) | USD 9.45 Billion |

| Market Size (2031) | USD 14.30 Billion |

| Growth Rate (2026 - 2031) | 8.66% CAGR |

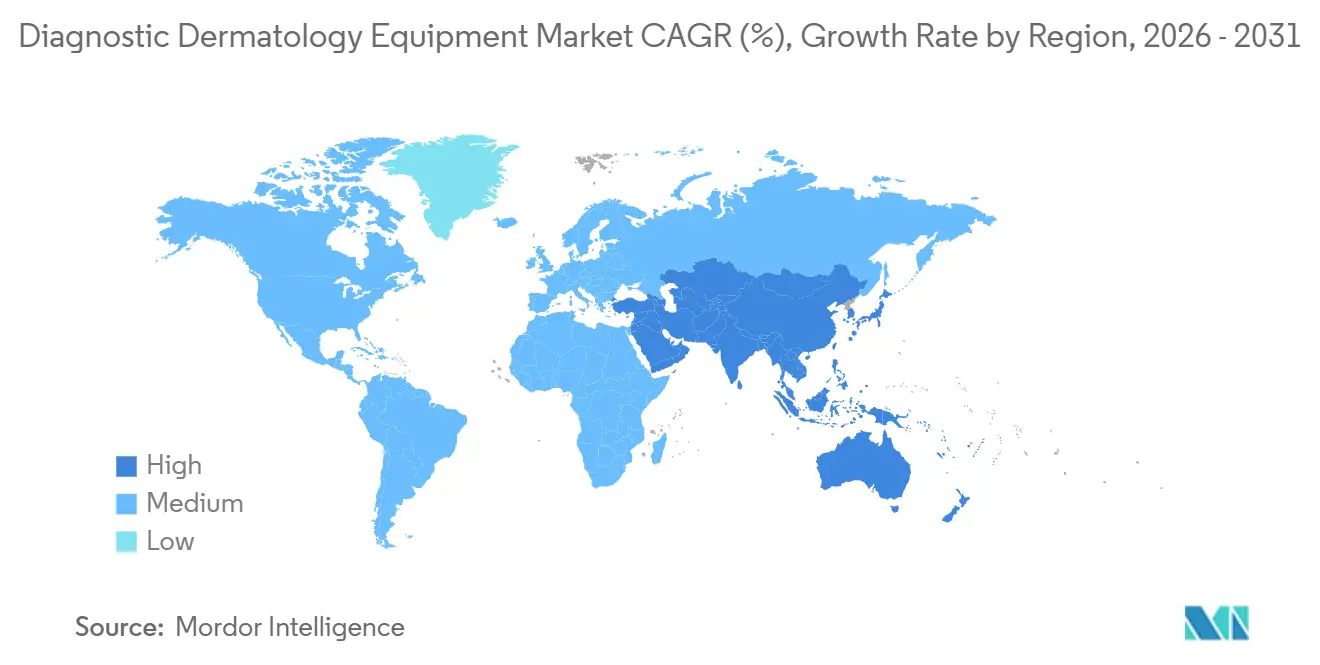

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Diagnostic Dermatology Equipment Market Analysis by Mordor Intelligence

The Diagnostic Dermatology Equipment Market size is expected to increase from USD 8.70 billion in 2025 to USD 9.45 billion in 2026 and reach USD 14.30 billion by 2031, growing at a CAGR of 8.66% over 2026-2031.

Adoption accelerates as skin cancer incidence rises and screening workflows expand, shifting triage into primary care. The diagnostics dermatology equipment market is further supported by steady gains in non-invasive imaging, where high-resolution OCT and LC-OCT reduce diagnostic uncertainty before biopsy and support treatment selection. AI-enabled diagnostic devices and teledermatology workflows broaden access and reduce bottlenecks across hub-and-spoke care models. Competitive dynamics intensify as established imaging vendors face AI-native entrants following United States FDA clearances that validate algorithm-enabled approaches for real-world clinical settings.

Key Report Takeaways

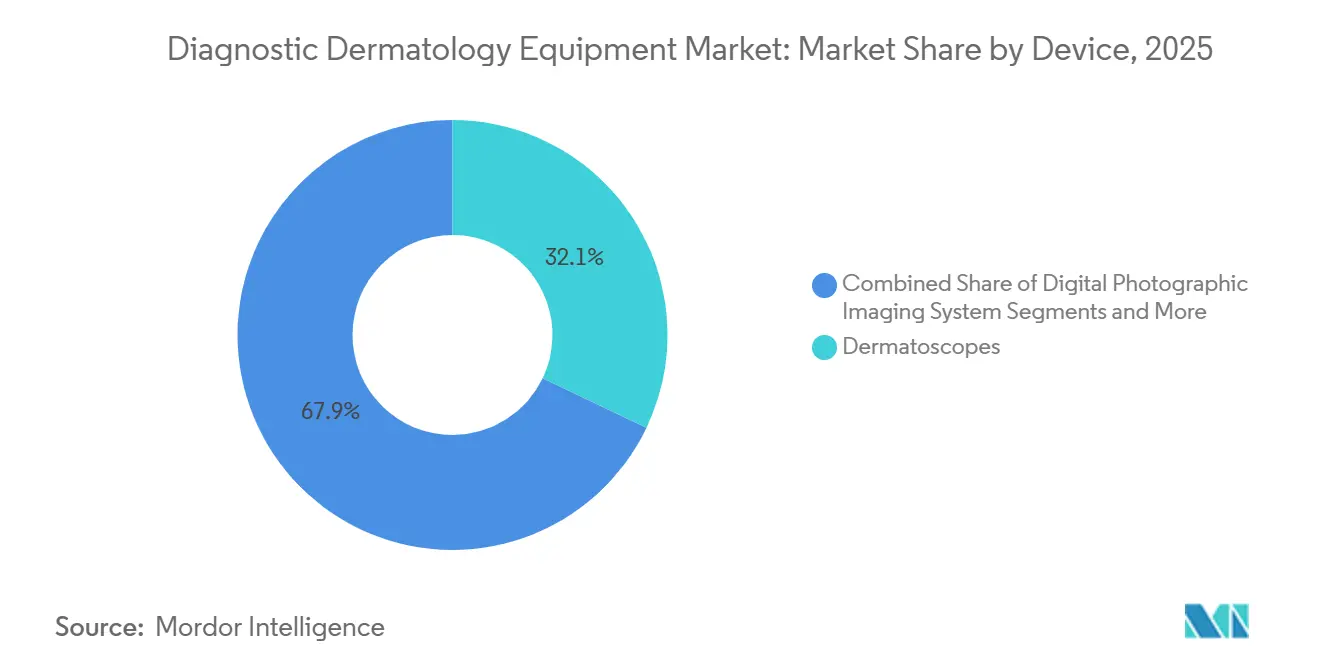

- By device type, dermatoscopes led with 32.10% of the diagnostics dermatology equipment market share in 2025, while OCT devices are projected to expand at an 8.90% CAGR through 2031.

- By portability, handheld or pocket dermatoscopes accounted for a 36.10% share in 2025, and the segment is projected to grow at an 8.70% CAGR during 2026–2031.

- By application, skin cancer diagnosis accounted for a 38.21% share of the dermatology diagnostics equipment market in 2025, while pigmented lesion mapping and longitudinal monitoring are set to grow at an 8.81% CAGR to 2031.

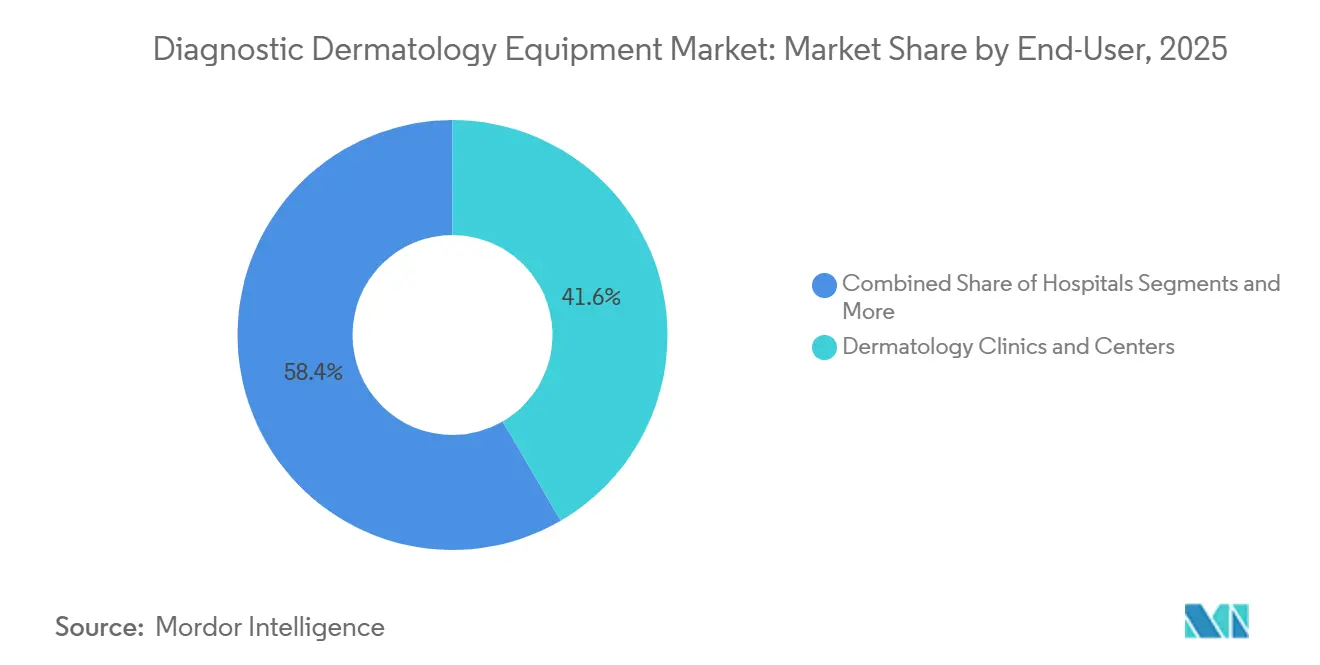

- By end-user, dermatology clinics and centers held a 41.60% share in 2025 and are expected to record an 8.65% CAGR over the forecast period.

- By geography, North America held 39.60% of the diagnostic dermatology equipment market share in 2025, while the Asia Pacific is projected to post the fastest growth at an 8.90% CAGR during 2026–2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Diagnostic Dermatology Equipment Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising skin cancer incidence and screening program expansion | +2.1% | Global, with acute concentration in Australia, the U.S., and Northern Europe | Medium term (2–4 years) |

| Shift to non-invasive imaging | +1.8% | North America and EU, with spillover to APAC urban centers | Medium term (2–4 years) |

| AI-enabled diagnostic tools and teledermatology adoption | +2.4% | APAC core with early gains across emerging teledermatology networks | Short term (≤ 2 years) |

| RCM reimbursement momentum (category-1 CPT codes) | +1.2% | U.S., with limited spillover pending EU MDR harmonization | Long term (≥ 4 years) |

| Emergent LC-OCT hybrid modality expands use-cases | +1.2% | Europe-linked innovation with U.S. entry post-FDA clearance | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Skin Cancer Incidence and Screening Program Expansion

Skin cancer prevalence keeps early detection at the center of care delivery, which prompts sustained investment in diagnostic imaging. In the United States, in 2025, an estimated 104,960 new cases of invasive melanoma and localized melanoma carry a 99% five-year survival rate, which motivates system-level screening initiatives and image-guided triage pathways that can be scaled into primary care settings.[1]The Skin Cancer Foundation, “Skin Cancer Facts & Statistics,” skincancer.org Australia continues to face one of the world’s highest melanoma incidence rates, and national stakeholders maintain a strong emphasis on targeted screening and enhanced access to diagnostic tools for timely intervention. This clinical reality supports steady demand for connected dermatoscopes and interoperable imaging platforms that enable store-and-forward consultations and streamline referrals to dermatology. Health agencies and professional associations also promote prevention and screening activities, which indirectly sustain device utilization across the diagnostic dermatology equipment market. As health systems standardize protocols, the Diagnostics dermatology equipment market tracks consistent upgrades from standalone optical tools to integrated image-management and AI-supported review.

Shift to Non-Invasive Imaging

Non-invasive imaging is expanding clinical use because it helps stratify lesions before biopsy and supports treatment decisions with high-resolution structural information. LC-OCT and OCT platforms demonstrate strong clinical performance and operating efficiency, with LC-OCT providing near-cellular resolution and deeper penetration to visualize epidermal and dermal architecture in one session. The FDA clearance of an LC-OCT system in March 2025 formalized U.S. entry for this hybrid modality, which strengthens clinician confidence in optical workflows that can reduce unnecessary excisions and guide pre-surgical margin assessment. Correlation studies continue to show high agreement with histopathology for key basal cell carcinoma features, which helps embed OCT and LC-OCT in diagnostic pathways before invasive sampling. As non-invasive imaging aligns with faster clinical decisions, the Diagnostics dermatology equipment market benefits from replacement cycles that prioritize higher-resolution devices and interoperable software. AI-Enabled Diagnostic Tools and Teledermatology Adoption

RCM Reimbursement Momentum (Category-1 CPT Codes)

Coverage fundamentals help normalize utilization, but reimbursement remains uneven across payers. Category I CPT codes for reflectance confocal microscopy have been in effect since 2017, and the Medicare Physician Fee Schedule specifies national payment amounts for image acquisition and interpretation that anchor provider billing. Commercial coverage policies vary, with some plans classifying RCM as investigational or limiting coverage pending more evidence of improved outcomes, which constrains uniform scale-up across community practices. Policy variability creates a split between academic centers with research budgets and community clinics with tighter margins, which moderates the diagnostics dermatology equipment market’s near-term pacing in RCM.

Emergent LC-OCT Hybrid Modality Expands Use-Cases

LC-OCT fuses the advantages of RCM and OCT, offering near-cellular resolution with greater depth to visualize dermal invasion patterns in one continuous acquisition. Published reviews document LC-OCT’s capability to resolve architecture relevant to BCC subtyping, with strong concordance against histopathology for characteristic features that inform treatment selection.[2] Lucas Boussingault et al., “Line-Field Confocal Optical Coherence Tomography of Basal Cell Carcinoma: Systematic Correlation with Histopathology,” Diagnostics (Basel), pmc.ncbi.nlm.nih.gov Company-reported pre-surgical data further reinforce the modality’s role in identifying residual tumor features at margins, which supports real-time decision making in operative workflows. As clinical protocols adopt LC-OCT with integrated dermoscopy, usability gains and efficient targeting of suspicious regions improve consistency across settings. This broadens the diagnostic dermatology equipment market toward hybrid systems that cover oncology and inflammatory dermatoses within one platform.

Restraint Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High acquisition and ownership costs for advanced systems | -1.4% | APAC Tier 2 and Tier 3 cities, Latin America, private clinics | Short term (≤ 2 years) |

| Shortage of trained operators; workflow time constraints | -0.8% | Global, with sharper gaps in rural and underserved areas | Medium term (2–4 years) |

| Regulatory/data-governance hurdles for AI/ML (SAMD) | -0.6% | EU and U.S. | Long term (≥ 4 years) |

| Inconsistent reimbursement for imaging/teledermatology | -1.0% | U.S. commercial payers and APAC markets without broad coverage | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Acquisition and Ownership Costs for Advanced Systems

Capital intensity remains a constraint, especially for private practices and smaller clinics that face tight operating margins. Advanced imaging suites and total-body 3D systems require facility readiness, trained staff, and IT infrastructure for secure storage, which compounds initial outlays beyond device price. Integration with clinical photography and AI software also involves ongoing licensing and upgrades, which commits providers to recurring expenses over multi-year periods. These realities encourage phased adoption that starts with connected dermatoscopes and image-management software, then proceeds to non-invasive imaging modules as case volumes grow. Where hospital systems lead capital programs, deployments cluster in academic centers with research and training mandates, while community facilities progress through shared-service models and teledermatology alliances. This staged approach moderates near-term purchasing, yet it preserves demand for interoperable platforms in the diagnostics dermatology equipment market.

Shortage of Trained Operators; Workflow Time Constraints

Non-invasive imaging requires consistent technique and experience for image acquisition and interpretation, which introduces a training curve for clinicians and technicians. Clinics that rely on short appointment slots face scheduling pressure when adding multi-step imaging workflows to existing visit structures. Some providers reserve imaging blocks or leverage teledermatology reading networks to mitigate bottlenecks, but coverage variability can restrict these options. Professional education and point-of-care decision support in software help, yet broad proficiency still takes time to build across diverse practice settings. These factors slow diffusion into settings without established imaging teams, which tempers the diagnostics dermatology equipment market’s potential to scale uniformly. Over time, AI-augmented workflows and remote reading arrangements can ease the burden, provided clinical governance and documentation requirements are met.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device: OCT Systems Outpace Dermatoscopes as Precision-Imaging Demand Escalates

Dermatoscopes commanded 32.10% share of the diagnostics dermatology equipment market size in 2025, affirming their position as the entry point for triage across primary care and dermatology. Routine use of connected dermatoscopes helps standardize image capture and supports store-and-forward workflows, which expands access for patients and accelerates referrals to specialists when needed. OCT platforms are projected to post the highest growth at an 8.90% CAGR during 2026–2031, driven by use cases that include lesion stratification and treatment planning for superficial versus non-superficial basal cell carcinoma. Clinical correlation continues to validate hybrid LC-OCT for BCC features that align with histopathology, which strengthens clinician trust in non-invasive imaging as a pre-biopsy step. As software becomes the organizing layer for image management and remote review, the diagnostics dermatology equipment market tilts toward integrated ecosystems that combine optical capture, AI decision support, and archival.

By Portability: Handheld Dermatoscopes Drive Teledermatology While Benchtop Systems Anchor Specialist Workflows

Handheld or pocket dermatoscopes held a 36.10% share in 2025 and are projected to grow at an 8.60% CAGR through 2031, reflecting their role at the front line of skin lesion evaluation and remote triage. Smartphone-compatible accessories and connected workflows improve image quality consistency and enable primary-care users to refer higher-risk cases efficiently. Stationary dermatoscopes and fixed optical systems remain critical in high-volume clinics, where stable optics and integrated capture rigs reduce motion artifacts and support standardized examinations. Trolley-mounted imaging suites that automate body mapping accelerate longitudinal monitoring and data capture, especially when paired with AI-enabled change detection. These device formats expand the diagnostics dermatology equipment market by covering both quick capture in primary care and more comprehensive imaging in specialty centers. Benchtop or console systems for RCM and OCT anchor specialist workflows that need near-histologic detail or deeper structural views to guide management. Hospitals and academic centers typically deploy these systems to help teams maintain technique, interpretation skills, and standardized reporting. The diagnostics dermatology equipment market increasingly favors interoperable software for image archiving, annotations, and remote reads, which reduces friction across multi-site networks. Portfolio breadth across handheld, stationary, and console formats strengthens vendor positioning as providers align purchases with diverse clinical use cases across the care continuum.

By Application: Skin Cancer Diagnosis Dominates; Pigmented Lesion Monitoring Gains Momentum Through AI-Powered Total-Body Photography

Skin cancer diagnosis accounted for a 38.21% share of the diagnostics dermatology equipment market size in 2025, supported by the high daily incidence in the United States and the strong survival benefit of early-stage detection. Device innovation in this application continues to focus on improving sensitivity and supporting referral decisions at the primary-care level. An FDA De Novo clearance in 2024 for an AI-enabled device illustrates regulatory traction for tools that help non-specialists evaluate suspicious lesions before referral. Subsequent clinical studies reported high sensitivity for melanoma, BCC, and SCC combined and documented a reduction in missed cancers when physicians used the device, which aligns with the need to close training and access gaps in community settings. As triage improves and biopsy is reserved for higher-risk lesions, the diagnostics dermatology equipment market benefits from consistent image capture and structured review that advance earlier intervention.

By End-User: Dermatology Clinics Lead Adoption; Hospitals Invest in Advanced Imaging for Complex Case Management

Dermatology clinics and centers held 41.60% share in 2025 and continue to expand by integrating connected dermatoscopy into routine screening. Image capture at the point of care feeds remote review or on-site specialist interpretation, which fits standard appointment lengths and supports timely decision making. As clinics add OCT or LC-OCT for selected cases, they strengthen triage before biopsy and align diagnostic resources with lesion risk profiles. Clinics also rely on image-management platforms for archiving and follow-up, which deepens software engagement over time. These factors sustain a stable base of device use in specialty settings and drive replacement cycles within the diagnostics dermatology equipment market.

Hospitals and academic medical centers invest in console-grade RCM, OCT, and LC-OCT for complex cases and surgical planning. FDA-cleared LC-OCT enhances pre-surgical margin assessment potential and supports post-excision checks, which can reduce re-excision rates when adopted within structured protocols. Enterprise purchasing prioritizes multimodal capability and interoperability with enterprise image archives and teledermatology workflows. As hospitals standardize non-invasive imaging and longitudinal monitoring, they often serve as regional hubs that read images captured at affiliate clinics, which multiplies the utility of each system. This hub-and-spoke approach strengthens the diagnostics dermatology equipment market by balancing capital concentration with distributed use across broader patient populations.

Geography Analysis

North America accounted for 39.60% share of the diagnostics dermatology equipment market size in 2025, supported by defined reimbursement frameworks for confocal imaging and institutional investment in non-invasive diagnostics. Medicare has maintained CPT pathways for RCM with specified national payment amounts, which anchor billing and pave the way for broader clinical use in select centers. Rising emphasis on skin cancer prevention and early detection also reinforces consistent device utilization across screening and oncology programs. The FDA’s AI and machine learning framework for medical devices introduces a predictable route for algorithm updates, which shortens innovation cycles for AI-enabled imaging solutions in the diagnostics and dermatology equipment market.

Europe maintains significant adoption across Germany, France, and the United Kingdom, where robust clinical infrastructure and public coverage support advanced imaging. EU-centered innovation in LC-OCT has accelerated with recent United States FDA clearance, which encourages transatlantic clinical validation and best-practice exchange. Provider networks emphasize quality and compliance, which favors imaging platforms with clear clinical evidence and defined postmarket plans. As hospital systems scale longitudinal monitoring and integrate AI-assisted change analysis, use cases broaden beyond oncology toward inflammatory dermatoses characterization. This environment supports continued platform adoption that integrates dermoscopy, OCT, and LC-OCT into unified workflows in the diagnostics dermatology equipment market.

Asia Pacific is the fastest-growing region with an 8.90% projected CAGR during 2026–2031, led by the continued expansion of dermatology services and the diffusion of teledermatology in underserved areas. Australia illustrates the region’s high-risk profile, with age-standardized incidence among the highest worldwide and a sustained national focus on targeted screening and rural access to imaging. As health systems promote remote care and standardized screening, handheld dermatoscopes gain traction in community settings supported by image-management software and remote reading. Company-led initiatives to extend 3D body-mapping access in communities outside major metro areas further underline the role of mobile imaging in APAC’s growth trajectory. These developments expand the diagnostic dermatology equipment market by connecting primary care to specialist centers through interoperable imaging and AI triage workflows.

Competitive Landscape

The diagnostics dermatology equipment market is characterized by a diverse mix of optical imaging vendors, AI-focused entrants, and integrated software platforms that combine capture, analytics, and remote reading. Some of the major players of DermLite, FotoFinder Systems GmbH, HEINE Optotechnik GmbH & Co. KG, and More. Canfield Scientific continues to advance AI-enabled total-body and facial imaging systems for clinical and aesthetic applications, which helps providers standardize documentation and longitudinal tracking. FotoFinder Systems entered a new phase in July 2025 following GHO Capital’s majority investment, with plans to accelerate expansion and evolve toward subscription-based software aligned to AI-assisted dermoscopy. These moves reflect a broader shift toward platform revenue and continuous feature delivery across the diagnostics dermatology equipment market.

AI-native devices are reshaping triage in primary care. An AI-enabled elastic scattering spectroscopy device received FDA De Novo clearance in January 2024 to support evaluation of lesions suspicious for melanoma, BCC, or SCC, signaling regulatory acceptance for algorithm-assisted diagnostics outside dermatology offices. Company-reported studies in 2025 showed high sensitivity and improved detection among physicians using the device, which expands the installed base beyond specialist centers and supports the diagnostics dermatology equipment market’s growth into distributed care settings.

Evidence depth and platform integration are emerging differentiators. As hospitals standardize enterprise imaging and clinics align with teledermatology, vendors that deliver interoperable capture, analytics, and cloud archiving have an advantage. This reinforces platform-led purchasing across the diagnostics dermatology equipment market and rewards companies with robust clinical evidence and clear regulatory roadmaps.

Diagnostic Dermatology Equipment Industry Leaders

Canfield Scientific, Inc.

FotoFinder Systems GmbH

DermaSensor Inc.

DermLite

HEINE Optotechnik GmbH & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Lumea forged a partnership with Primaa, a top provider of integrated AI solutions specializing in dermatopathology and breast pathology. This collaboration notably broadens Lumea's diagnostic ecosystem, catering to dermatology groups globally.

- July 2025: GHO Capital Partners agreed to acquire a majority stake in FotoFinder Systems, with plans to accelerate global growth and subscription software initiatives linked to AI-assisted dermoscopy.

- June 2025: DermaSensor and academic collaborators announced publication of two pivotal studies that assessed the standalone performance of the company’s elastic scattering spectroscopy device and its impact on primary-care physicians’ detection and management of skin cancer.

- March 2025: Damae Medical received FDA 510(k) clearance for its deepLive LC-OCT system, enabling high-resolution skin imaging for non-invasive evaluation and accelerating the company’s U.S. expansion following its prior CE marking.

Global Diagnostic Dermatology Equipment Market Report Scope

As per the scope of the report, diagnostic dermatology equipment refers to specialized medical tools and imaging systems used by healthcare professionals to examine, identify, and monitor skin, hair, and nail conditions. These devices, ranging from handheld dermatoscopes to advanced AI-powered imaging, enable non-invasive, precise, and early detection of lesions, diseases, and cancers.

The diagnostic dermatology equipment is segmented into, by device, portability, application, end user, and geography. By device, the market is segmented into dermatoscopes, digital photographic imaging systems, reflectance confocal microscopy (RCM), optical coherence tomography (OCT), high-frequency ultrasound (HFUS), electrical impedance spectroscopy (EIS), total body 3D imaging systems, microscopes and trichoscopes, skin biopsy diagnostics instruments, and others. By portability, the market is segmented into handheld/pocket dermatoscopes, stationary/fixed dermatoscopes, trolley-mounted/tabletop imaging systems, benchtop/console RCM and OCT systems, and others. By application, the market is segmented into skin cancer diagnosis, pigmented lesion mapping & longitudinal monitoring, inflammatory skin diseases, hair & scalp disorders, aesthetic & dermatologic surgery planning/documentation, and other applications. By end-user, the market is segmented into hospitals, dermatology clinics & centers, primary care & ambulatory care centers, academic & research institutes, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and trends for 17 countries across major regions worldwide. The report offers market size and forecasts in value (USD) for the above segments.

| Dermatoscopes |

| Digital Photographic Imaging Systems |

| Reflectance Confocal Microscopy (RCM) |

| Optical Coherence Tomography (OCT) |

| High-Frequency Ultrasound (HFUS) |

| Electrical Impedance Spectroscopy (EIS) |

| Total Body 3D Imaging Systems |

| Microscopes And Trichoscopes |

| Skin Biopsy Diagnostics Instruments |

| Others |

| Handheld/Pocket Dermatoscopes |

| Stationary/Fixed Dermatoscope |

| Trolley-Mounted/Tabletop Imaging Systems |

| Benchtop/Console RCM And OCT Systems |

| Others |

| Skin Cancer Diagnosis | Melanoma |

| Non-melanoma Skin Cancers | |

| Pigmented Lesion Mapping & Longitudinal Monitoring | |

| Inflammatory Skin Diseases | |

| Hair & Scalp Disorders | |

| Aesthetic & Dermatologic Surgery Planning/Documentation | |

| Other Applications |

| Hospitals |

| Dermatology Clinics & Centers |

| Primary Care & Ambulatory Care Centers |

| Academic & Research Institutes |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Device | Dermatoscopes | |

| Digital Photographic Imaging Systems | ||

| Reflectance Confocal Microscopy (RCM) | ||

| Optical Coherence Tomography (OCT) | ||

| High-Frequency Ultrasound (HFUS) | ||

| Electrical Impedance Spectroscopy (EIS) | ||

| Total Body 3D Imaging Systems | ||

| Microscopes And Trichoscopes | ||

| Skin Biopsy Diagnostics Instruments | ||

| Others | ||

| By Portability | Handheld/Pocket Dermatoscopes | |

| Stationary/Fixed Dermatoscope | ||

| Trolley-Mounted/Tabletop Imaging Systems | ||

| Benchtop/Console RCM And OCT Systems | ||

| Others | ||

| By Application | Skin Cancer Diagnosis | Melanoma |

| Non-melanoma Skin Cancers | ||

| Pigmented Lesion Mapping & Longitudinal Monitoring | ||

| Inflammatory Skin Diseases | ||

| Hair & Scalp Disorders | ||

| Aesthetic & Dermatologic Surgery Planning/Documentation | ||

| Other Applications | ||

| By End-User | Hospitals | |

| Dermatology Clinics & Centers | ||

| Primary Care & Ambulatory Care Centers | ||

| Academic & Research Institutes | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the growth outlook for diagnostics dermatology equipment through 2031?

The Diagnostics dermatology equipment market size is USD 9.45 billion in 2026 and is projected to reach USD 14.30 billion by 2031 at an 8.66% CAGR, driven by non-invasive imaging, AI-enabled devices, and teledermatology integration.

Which geography is expected to grow fastest by 2031?

Asia Pacific is projected to post the fastest growth with an 8.90% CAGR during 2026-2031, supported by expanding dermatology services and adoption of remote imaging workflows.

Which device categories are leading and which are growing fastest?

Dermatoscopes led with a 32.10% share in 2025, while OCT devices are projected to grow fastest with an 8.90% CAGR due to pre-biopsy stratification and treatment-planning use cases.

What are the key barriers to wider adoption in community settings?

High ownership costs, variable commercial coverage, and training requirements for non-invasive imaging slow uniform adoption, although Medicare CPT pathways for confocal imaging and AI-enabled workflows are improving economics and usability.

How is AI changing diagnostic workflows in dermatology?

FDA guidance for AI/ML in medical devices supports faster iterative improvements, and De Novo and 510(k) clearances for AI-enabled imaging tools are enabling primary-care triage and hybrid non-invasive imaging in surgical planning.

Which applications will see the strongest momentum to 2031?

Skin cancer diagnosis remains the largest use, while pigmented lesion mapping and longitudinal monitoring is projected to grow fastest as 3D body mapping and AI change analysis scale across high-risk cohorts.

Page last updated on: