U.S. Behavioral Health Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 76.25 Billion |

| Market Size (2026) | USD 79.79 Billion |

| Market Size (2031) | USD 100.15 Billion |

| Growth Rate (2026 - 2031) | 4.65% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

U.S. Behavioral Health Market Analysis by Mordor Intelligence

The U.S. Behavioral Health Market size is projected to be USD 76.25 billion in 2025, USD 79.79 billion in 2026, and reach USD 100.15 billion by 2031, growing at a CAGR of 4.65% from 2026 to 2031.

Between 2018 and 2024, behavioral health utilization in the United States increased by 62.6%, reflecting a growing demand for care across routine, crisis, and follow-up settings. Nearly 25% of adults in the country live with a mental illness, while 18.33%, or 46.7 million individuals, meet the criteria for a substance use disorder.[1]Mental Health America, “State of Mental Health in America 2025,” Mental Health America, mhanational.org However, a significant treatment gap remains, as 54.7% of adults with mental illness received no treatment in 2024, and only 19.3% of individuals aged 12 or older who required substance use treatment accessed it. This unmet demand drives investments in outpatient services, integrated care, medication management, and digital access. Competitive dynamics are shifting toward scalable networks, improved reimbursement alignment, and broader clinical reach, creating opportunities for operators capable of delivering measurable outcomes for complex patients.

Key Report Takeaways

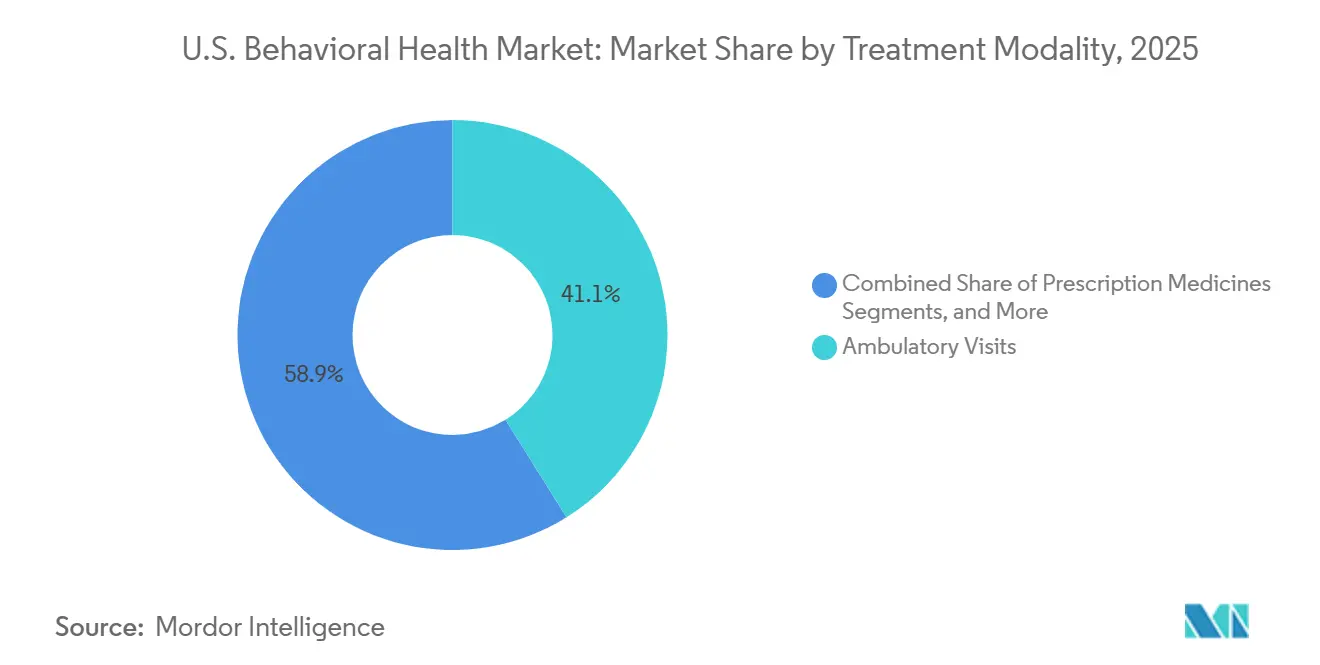

- By treatment modality, ambulatory visits held 41.10% share in 2025, while prescription medicines are projected to expand at a 5.25% CAGR through 2031.

- By condition group, mental health conditions accounted for 72.2% share in 2025, while co-occurring mental health and substance use disorder conditions are forecasted to grow at a 5.95% CAGR through 2031.

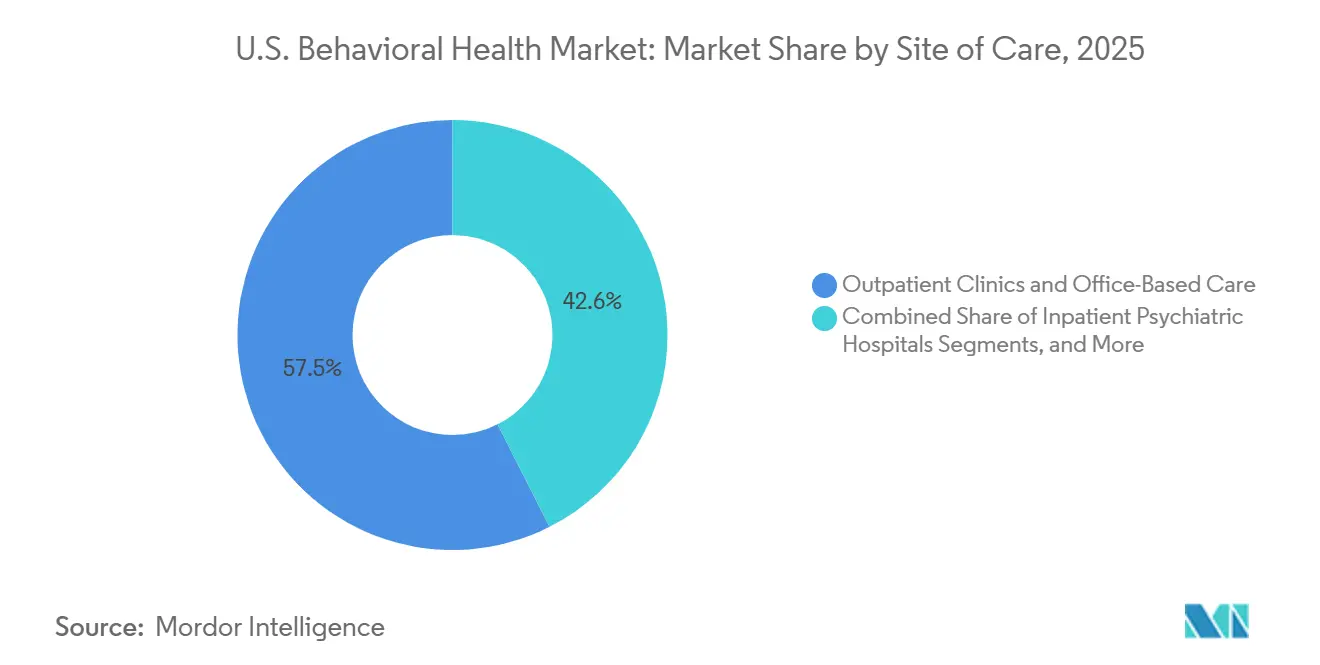

- By site of care, outpatient clinics and office-based care captured 57.45% share in 2025, while PHPs and IOPs are advancing at a 6.86% CAGR through 2031.

- By age cohort, adults represented 69.66% share in 2025, while adolescents are projected to record the fastest growth at a 6.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

U.S. Behavioral Health Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Tightening parity enforcement and network adequacy requirements | +0.5% | National, with most aggressive enforcement in GA, NY, WA, CA, CO, MD | Short term (≤ 2 years) |

| Medicare and medicaid coverage expansion for IOP, CCBHC, and crisis services | +0.8% | National, rural and low-income populations in all regions benefit most | Medium term (2-4 years) |

| Persistent unmet demand in co-occurring mental health and SUD conditions | +0.9% | National, with highest co-occurring burden in Appalachia, rural South, and Mountain West | Long term (≥ 4 years) |

| Sustained tele-buprenorphine and controlled substance telehealth prescribing | +0.6% | National, transformative for rural areas in the South, Midwest, and Mountain West with limited OTP access | Medium term (2-4 years) |

| Shift from cash-pay point solutions toward in-network, value-based care models | +0.5% | National, employer and commercial payer markets in Northeast, Midwest, and Pacific Coast states | Medium term (2-4 years) |

| Measurement-based care and AI-enabled outcomes tracking | +0.4% | National, with early scaling in urban academic health systems and digital-native platforms | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening Parity Enforcement Reshapes Reimbursement and Network Adequacy

State and federal parity enforcement is transforming compliance into a revenue-critical issue for the United States behavioral health market. In 2024 and 2025, Georgia imposed nearly USD 25 million in fines on 22 insurers for non-quantitative treatment limitations, while Washington fined Kaiser Foundation Health Plan USD 300,000, and Regence BlueShield and Premera Blue Cross USD 550,000 each for similar violations.[2]Center for Health Care Strategies, “Medicare Intensive Outpatient Program Coverage Update,” Center for Health Care Strategies, chcs.org Payers are expanding provider networks and improving outpatient reimbursements to reduce regulatory scrutiny. Although the 2024 MHPAEA Final Rule adopted a federal non-enforcement stance in May 2025, states like Washington, Colorado, Maryland, and California incorporated its provisions into state laws, maintaining compliance expectations in major commercial markets.[3]Centers for Medicare & Medicaid Services, “Telehealth FAQ, February 2026,” CMS, cms.gov This state-level adoption establishes a national baseline for access and documentation standards, ensuring providers who meet these criteria benefit from higher reimbursement quality.

Medicare and Medicaid Coverage Expansion Unlocking Access at Mid-Acuity Levels

Coverage expansions are addressing gaps in the United States behavioral health market, particularly for care levels between outpatient visits and inpatient services. Medicare began covering intensive outpatient program services on January 1, 2024, under the Consolidated Appropriations Act, 2023, enabling over 60 million beneficiaries to access reimbursable mid-acuity care. Geographic restrictions for behavioral health telehealth were permanently removed, allowing beneficiaries to receive care at home beyond the 2027 general telehealth deadline. Medicaid has also expanded Certified Community Behavioral Health Clinics from 67 facilities in 8 states in 2017 to over 500 across 46 states and the District of Columbia.[4]KFF, “Certified Community Behavioral Health Clinics and Medicaid Recognition, May 2026,” KFF, kff.org By FY2025, 19 states recognized CCBHCs as Medicaid providers. The CMS ACCESS behavioral health model, launching in July 2026 with 85 behavioral health organizations and major payer alignment, strengthens outcome-linked payment systems and supports scalable mid-acuity care pathways.[5]Substance Abuse and Mental Health Services Administration, “Co-occurring Mental Illness and Substance Use Data, 2025,” SAMHSA, samhsa.gov

Persistent Unmet Demand in Co-occurring Mental Health and SUD Conditions

Unmet demand for dual-diagnosis care remains a key growth driver in the United States behavioral health market. In 2024, 41.2% of the 21.2 million adults with both mental illness and substance use disorder received no treatment, and only 14.5% accessed integrated care. In January 2026, the White House reported 48.4 million Americans, or 16.8% of the population, had a substance use disorder, with 95.6% of untreated individuals perceiving no need for care. The stimulant-fentanyl fourth wave has intensified psychiatric complexities, with psychostimulant-related deaths rising from 3.9 to 10.4 per 100,000 people between 2018 and 2023, and stimulant use increasing 8.63% from 2021 to 2022. Providers with integrated clinical models are well-positioned to manage stepped care and attract higher-acuity, higher-reimbursing patient groups.

Sustained Tele-buprenorphine and Controlled-Substance Telehealth Prescribing

Tele-buprenorphine is enhancing medication access and retention in the United States behavioral health market, particularly in underserved areas. A VA cohort study linked telehealth use in buprenorphine treatment to a 52% lower risk of treatment discontinuation for opioid use disorder and a 54% lower risk for mental health conditions. A study in Oregon and Washington found telehealth-only buprenorphine treatment reduced discontinuation rates by 61% compared to office-based care. The DEA's Fourth Temporary Extension, issued in December 2025, allows telemedicine prescriptions for Schedule II to V controlled substances until December 31, 2026, without requiring prior in-person visits, benefiting approximately 5 million Americans with opioid use disorder. Policy variations across states, rather than clinical evidence, remain the primary barrier to equitable access. Organizations capable of scaling compliant virtual medication pathways in underserved regions are well-positioned to address these gaps.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Workforce shortages and low public-payer reimbursement rates | -1.0% | National, most severe in rural South, Mountain West, and lower-income urban markets | Long term (≥ 4 years) |

| Ghost networks, prior authorization friction, and utilization management barriers | -0.7% | National, with disproportionate impact in MA, Medicaid managed care markets, and rural areas | Medium term (2-4 years) |

| Medicaid eligibility churn and supplemental funding cliffs | -0.5% | National, highest acute impact in Medicaid-expansion states and safety-net dependent markets | Short term (≤ 2 years) |

| Safety-net facility closures in residential and community-based settings | -0.4% | Rural America, Pacific Coast, New England, and Appalachian states | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Workforce Shortages and Low Public-Payer Reimbursement Rates

Workforce shortages remain a significant barrier in the United States behavioral health market. By December 2025, 137 million Americans, or 40% of the population, lived in federally designated mental health professional shortage areas, with the number of such designations increasing from 6,418 in 2024 to 6,807 in 2026. By 2038, projected shortfalls include 99,840 mental health counselors, 99,840 psychologists, 77,050 addiction counselors, and 36,780 adult psychiatrists. The supply of psychiatrists is expected to decline from 37,470 in 2026 to 36,550 in 2038, even as annual demand rises by 40.7%. Rural areas face significant access challenges, with rural counties nearly three times more likely than urban ones to lack psychologists, and 22% of rural counties reporting no clinical social workers.

Ghost Networks, Prior Authorization Friction, and Utilization Management Barriers

Administrative challenges continue to hinder demand in the United States behavioral health market. In 2025, a review revealed that 55% of behavioral health providers listed under Medicare Advantage were inactive in 2023, while 28% of Medicaid managed care providers were also inactive. In rural counties, the Medicare Advantage inactive provider rate reached 63%, with 72% of these providers erroneously listed. Of these, 46% had retired or left practice, and 21% had never contracted with the plan. Prior authorization requirements further complicate access, as reauthorization is often needed every 8 to 20 sessions, consuming 5% to 10% of session revenue.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Modality: Telehealth Redefining the Ambulatory Channel

In 2025, ambulatory visits accounted for 41.10% of the United States behavioral health market, leading as care shifted toward outpatient and virtual settings. Behavioral health made up 65.6% of all United States telehealth visits in 2024, a significant rise from 18.4% in 2018. Total behavioral health telehealth visits reached 66.4 million, surpassing the 62.8 million primary care telehealth visits during the same period. This shift highlights telehealth's evolution into a standard delivery channel for routine therapy, medication management, and follow-ups.

Prescription medicines are the fastest-growing treatment modality, with the United States behavioral health market for this segment projected to grow at a 5.25% CAGR from 2026 to 2031. Stimulant prescriptions rose by 53.3% between 2018 and 2024, while antipsychotic volumes increased by 45.4%. Nurse practitioners and physician assistants managed 34.3% of prescription volume in 2024, surpassing psychiatrists and primary care physicians.

By Condition Group: Co-occurring Conditions Outgrow the Largest Segment

Mental health conditions held a 72.2% share in 2025, making them the largest condition group in the United States behavioral health market. Anxiety disorders led telehealth use among Medicare beneficiaries in 2024, with 9.45 million visits, followed by 8.77 million visits for depressive disorders. Substance use disorders remain smaller but are growing due to contingency management programs supported by Medicaid Section 1115 waivers in several states. Co-occurring conditions are the fastest-growing segment, with a projected 5.95% CAGR from 2026 to 2031. A 2026 study demonstrated that integrated buprenorphine and psychotherapy significantly improved remission rates, reinforcing the value of combined care for dual-diagnosis populations.

By Site of Care: PHP and IOP Emerging as the Market's Structural Inflection Point

Outpatient clinics and office-based care represented 57.45% of the United States behavioral health market in 2025, reflecting a shift from inpatient infrastructure to flexible, cost-effective settings. Residential treatment centers and inpatient psychiatric hospitals remain essential for high-acuity cases but face challenges like high labor costs and limited growth potential. PHPs and IOPs are the fastest-growing site category, with a forecasted 6.86% CAGR through 2031. Medicare's IOP coverage expansion in January 2024 created a reimbursable care level for 60 million beneficiaries. Virtual IOPs have shown to reduce readmission rates to 4% or less, compared to national psychiatric readmission rates exceeding 20% within six months.

By Age Cohort: Adolescent Surge Creates a Distinct Clinical Submarket

Adults accounted for 69.66% of the United States behavioral health market in 2025, remaining the largest age cohort across conditions, modalities, and care sites. Medicaid and CHIP play a critical role, covering nearly 50% of adults with opioid use disorder. Policy changes directly impact visit volumes, medication access, and provider participation for this group. Adolescents are the fastest-growing cohort, with a projected 6.67% CAGR from 2026 to 2031. In 2025, 51% of 97,000 youth screened for depression reported frequent suicidal ideation, the highest rate since 2014. Diagnosed anxiety disorders among adolescents aged 12 to 17 rose by 61% from 2016 to 2023. Telehealth has proven effective in narrowing access gaps, with outcomes for high-risk adolescents comparable to their lower-risk peers after 12 sessions.

Geography Analysis

Long-established academic medical infrastructure and a higher psychiatrist density than the national average position the Northeast as the most densely served region in the United States behavioral health market. Massachusetts has 41.34 psychiatrists per 100,000 residents, followed by Rhode Island at 37.94, Connecticut at 35.59, and New York at 35.02, compared to the national average of 18.26 per 100,000. Telehealth usage is also high, with 17.8% of urban patients making telehealth claims in December 2025, compared to 12.2% in rural areas. New York's behavioral health access standard, implemented in July 2025, requires care within 10 days, increasing pressure on payers and networks to expedite services. Despite these advantages, in-network access challenges persist, as highlighted by a 2025 lawsuit against Carelon Behavioral Health, which revealed ghost rates of 73% to 94% across several counties.

The South faces significant access gaps in the United States behavioral health market relative to its population needs. Mississippi has 9.85 psychiatrists per 100,000 residents, Alabama 10.59, and Tennessee 10.82, while rural suicide rates in 2023 were 20.2 per 100,000 compared to 13.8 in urban areas. Texas and Florida, despite large provider pools, still face practitioner shortages of 606 and 545, respectively, as per HRSA estimates. The fragility of safety-net systems is evident from Arisa Health's 2026 exit from its 41-county community mental health center contract in Arkansas following a USD 4.4 million funding cut. Telehealth adoption for mental health is growing rapidly, with psychotherapy leading telehealth procedure categories, offering a scalable solution to address workforce shortages.

Competitive Landscape

The United States behavioral health market is moderately fragmented at the national level, with rapid consolidation in outpatient and digital care. Private equity-backed transactions in behavioral health increased by 47% year-over-year through Q3 2025, with 75 announced or completed deals. Stronger outpatient platforms maintained transaction multiples in the 11x to 14x EBITDA range. This activity reflects buyers' focus on scaling through networks, compliance, and payer alignment, while rewarding platforms that integrate access, utilization management, and measurable outcomes—capabilities often lacking in standalone practices. Strategic combinations are steadily channeling more patient volume into larger organized networks, despite visible fragmentation.

Universal Health Services announced a USD 835 million acquisition of Talkspace on March 9, 2026. Upon completion, the combined entity will operate 346 inpatient psychiatric facilities, outpatient clinics, and virtual therapy services across all 50 states and the District of Columbia, reaching over 200 million Americans through insurance and employer benefits. This integration of inpatient assets, mid-acuity programs, and virtual care into a single delivery structure sets a benchmark few operators can match. Similarly, Spring Health's merger with Alma in May 2026 created a platform serving nearly 170 million lives, linking employer-sponsored care navigation with a large independent clinician network. These developments highlight the market's shift toward comprehensive platforms addressing the full care journey rather than isolated niches.

U.S. Behavioral Health Industry Leaders

Acadia Healthcare Company, Inc.

Behavioral Health Group

Teladoc Health, Inc.

Universal Health Services, Inc.

Newport Healthcare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Spring Health and Alma merged to create the first "lifelong mental health platform," impacting 170 million lives by combining precision mental healthcare with clinician infrastructure and payer contracting capabilities.

- May 2026: Ksana Health secured an ARPA-H contract worth up to USD 17.9 million to develop a Large Health Behavior Model using behavioral data from smartphones and wearables linked to electronic health records, in partnership with leading health organizations.

- April 2026: Tava Health raised USD 40 million in Series C funding to launch three products—Overture for employer-sponsored therapy, Symphony for AI-driven clinical documentation, and Tempo as a care navigation hub—covering 93% of the U.S. commercially insured population.

- March 2026: Universal Health Services acquired Talkspace for USD 835 million, positioning itself as the only operator offering inpatient, outpatient, PHP, IOP, and virtual behavioral health services nationwide.

- March 2026: Grow Therapy raised USD 150 million in Series D funding at a USD 3 billion valuation, following USD 1 billion in revenue and 7 million therapy visits in 2025, with 26,000 providers and over 125 health plans.

U.S. Behavioral Health Market Report Scope

As per the scope of the report, the behavioral health market encompasses the ecosystem of healthcare services, treatments, and digital platforms that address mental health conditions and the daily lifestyle habits that impact a person's physical and emotional well-being.

The U.S. Behavioral Health Market is segmented by treatment modality, condition group, site of care, and age cohort. By treatment modality, the market includes ambulatory visits, prescription medications, and other treatment services. By condition group, the market is categorized into mental health conditions (mood disorders, anxiety disorders, psychotic disorders, trauma- and stressor-related disorders, eating disorders, neurodevelopmental and behavioral disorders), substance use disorders (alcohol use disorder, opioid use disorder, stimulant use disorder, cannabis use disorder), and co-occurring mental health and substance use disorders. By site of care, the market is segmented into outpatient clinics and office-based care, partial hospitalization and intensive outpatient programs, inpatient psychiatric hospitals, residential treatment centers, and others. By age cohort, the market is categorized into children, adolescents, adults, and the geriatric population. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Ambulatory Visits |

| Prescription Medicines |

| Other Treatment Services |

| Mental Health Conditions | Mood Disorders |

| Anxiety Disorders | |

| Psychotic Disorders | |

| Trauma- and Stressor-Related Disorders | |

| Eating Disorders | |

| Neurodevelopmental and Behavioral Disorders | |

| Substance Use Disorders | Alcohol Use Disorder |

| Opioid Use Disorder | |

| Stimulant Use Disorder | |

| Cannabis Use Disorder | |

| Co-occurring Mental Health and SUD Conditions |

| Outpatient Clinics and Office-Based Care |

| Partial Hospitalization and Intensive Outpatient Programs |

| Inpatient Psychiatric Hospitals |

| Residential Treatment Centers |

| Others |

| Children |

| Adolescents |

| Adults |

| Geriatric Population |

| By Treatment Modality | Ambulatory Visits | |

| Prescription Medicines | ||

| Other Treatment Services | ||

| By Condition Group | Mental Health Conditions | Mood Disorders |

| Anxiety Disorders | ||

| Psychotic Disorders | ||

| Trauma- and Stressor-Related Disorders | ||

| Eating Disorders | ||

| Neurodevelopmental and Behavioral Disorders | ||

| Substance Use Disorders | Alcohol Use Disorder | |

| Opioid Use Disorder | ||

| Stimulant Use Disorder | ||

| Cannabis Use Disorder | ||

| Co-occurring Mental Health and SUD Conditions | ||

| By Site of Care | Outpatient Clinics and Office-Based Care | |

| Partial Hospitalization and Intensive Outpatient Programs | ||

| Inpatient Psychiatric Hospitals | ||

| Residential Treatment Centers | ||

| Others | ||

| By Age Cohort | Children | |

| Adolescents | ||

| Adults | ||

| Geriatric Population | ||

Key Questions Answered in the Report

What is the projected value of the United States behavioral health market by 2031?

The United States behavioral health market is forecast to reach USD 100.15 billion by 2031 from USD 79.79 billion in 2026, with a 4.65% CAGR over the forecast period.

Which treatment modality leads behavioral care spending in the United States?

Ambulatory visits were the largest treatment modality in 2025 with a 41.10% share, reflecting the strong shift toward outpatient and telehealth-based delivery.

Which condition group is growing fastest in behavioral health services?

Co-occurring mental health and substance use disorder conditions are the fastest-growing condition group, with a projected 5.95% CAGR through 2031.

Why are PHPs and IOPs gaining traction so quickly?

PHPs and IOPs are projected to grow at a 6.86% CAGR because Medicare added IOP coverage in 2024 and payers are moving clinically appropriate patients away from inpatient beds.

Which age group is showing the fastest demand growth?

Adolescents are the fastest-growing age cohort with a 6.67% CAGR, supported by rising diagnosis rates and high levels of depression and suicidal ideation screening results.

What is the biggest constraint on provider expansion across the country?

Workforce shortages remain the largest structural barrier, with 137 million Americans living in mental health professional shortage areas as of December 2025.

Page last updated on: